Market Overview

| Study Period | 2020 - 2031 |

|---|---|

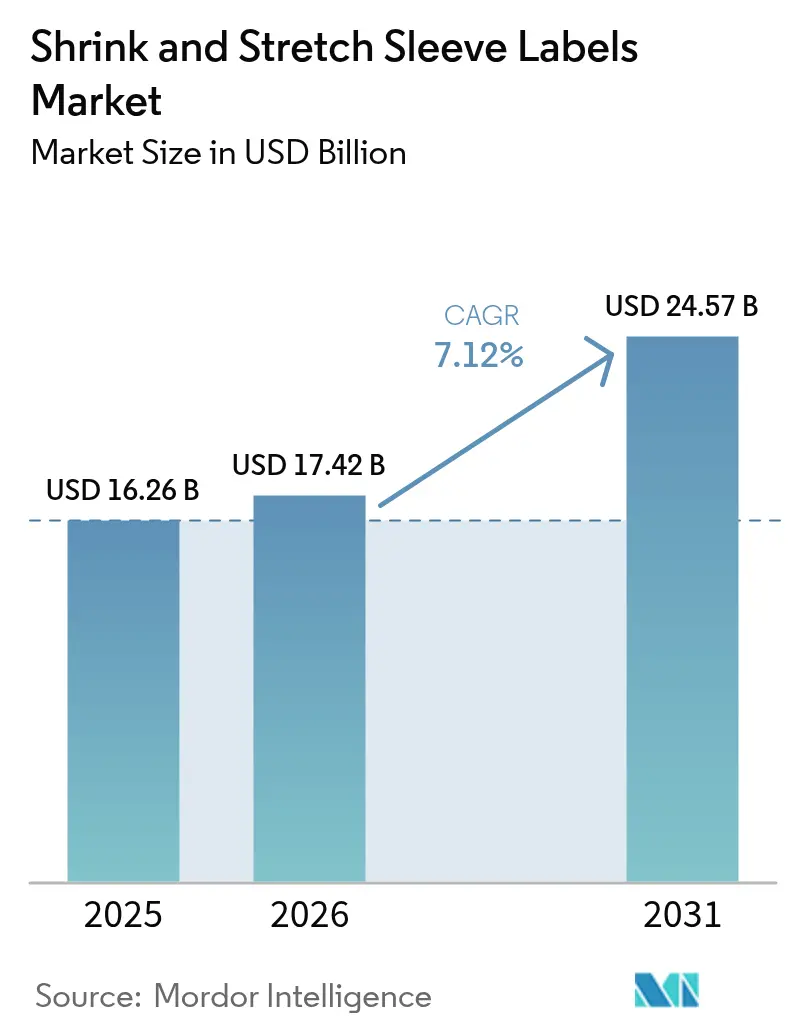

| Market Size (2026) | USD 17.42 Billion |

| Market Size (2031) | USD 24.57 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

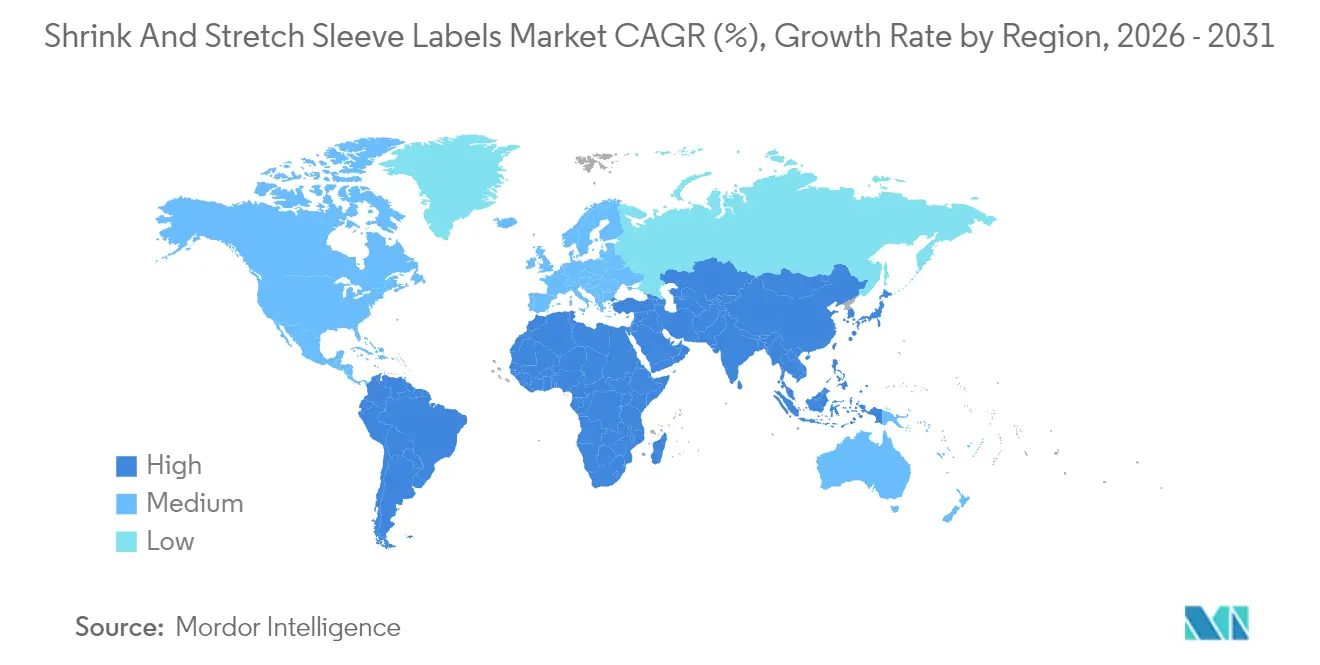

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Shrink And Stretch Sleeve Labels Market Analysis by Mordor Intelligence

The shrink and stretch sleeve labels market size was valued at USD 16.26 billion in 2025 and estimated to grow from USD 17.42 billion in 2026 to reach USD 24.57 billion by 2031, at a CAGR of 7.12% during the forecast period (2026-2031). Expansion rests on brand owners seeking 360-degree graphics that lift shelf impact, fulfill tamper-evident mandates, and align with strict recycling targets. Rapid gains in digital inkjet capacity let converters print short runs of 1,000 sleeves or fewer, slashing entry costs for craft brewers and niche beverage producers. Pharmaceutical regulations that require visible integrity indicators reinforce demand, while functional drinks favor light-blocking sleeves that maintain ingredient potency. Europe leads by value thanks to early adoption of premium packaging, yet Asia-Pacific registers the quickest growth as rising disposable incomes boost packaged beverage consumption.

Key Report Takeaways

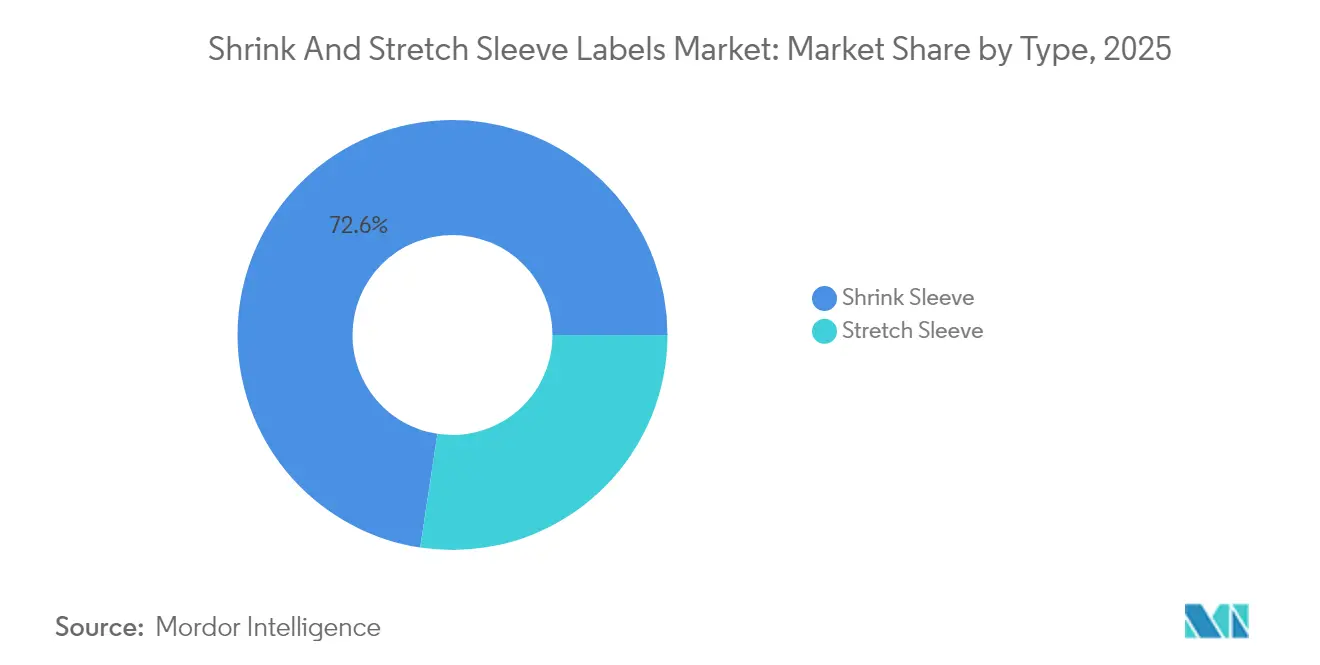

- By type, shrink sleeves held 72.60% of the shrink and stretch sleeve labels market share in 2025; the stretch sleeve segment is projected to expand at an 8.05% CAGR through 2031.

- By material, PET captured 36.45% of the shrink and stretch sleeve labels market size in 2025 and is advancing at a 7.62% CAGR on the back of bottle-to-bottle recyclability.

- By end user, the pharmaceutical segment is forecast to grow at an 8.28% CAGR between 2026-2031, outpacing food applications.

- By geography, Europe commanded 29.55% revenue in 2025, whereas Asia-Pacific is expected to post an 7.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Shrink And Stretch Sleeve Labels Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for 360° high-definition graphics to boost shelf appeal | +1.2% | Global, with premium focus in North America and Europe | Medium term (2-4 years) |

| Rising demand for tamper-evident and anti-counterfeit packaging | +0.9% | Global, regulatory-driven in North America and EU | Short term (≤ 2 years) |

| Growth in packaged beverages and functional drinks | +1.5% | Asia-Pacific core, spill-over to global markets | Long term (≥ 4 years) |

| Shift toward recyclable PETG and floatable sleeve films | +0.8% | EU-led, expanding to North America | Medium term (2-4 years) |

| Digital inkjet short-run printing lowering MOQ for niche SKUs | +1.0% | Global, craft beverage focus | Short term (≤ 2 years) |

| Smart interactive features (thermochromic, QR) enabling marketing | +0.6% | North America and EU premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Packaged Beverages and Functional Drinks

Functional drinks use sleeve technology to protect light-sensitive nutrients and display expanded nutritional panels. One in three shoppers now ranks immune support as a top purchase criterion, strengthening demand for drinks formulated with vitamin C, elderberry, and probiotics.[1]TricorBraun, “Packaging Perspectives on Functional Beverages,” tricorbraun.com Full-body graphics give brands 150% more printable area than pressure-sensitive labels, allowing claims, QR codes, and authenticity seals. Premier Protein trimmed plastic by 35% by migrating to PET bottles wrapped in light-blocking shrink sleeves that feature perforations for easy removal during recycling. Craft brewers that previously needed orders of 100,000 decorated cans now source as few as 7,000 cans fitted with shrink sleeves, widening access for seasonal releases.

Digital Inkjet Short-Run Printing Lowering MOQ for Niche SKUs

Water-based inkjet presses achieve production speeds 2.3 times higher than earlier systems while eliminating solvent residue concerns in food packaging. Converters now profitably accept 1,000-unit jobs versus the 100,000-unit threshold required for flexography, enabling hyper-targeted SKUs for regional promotions and e-commerce bundles. Design iterations finalize in days, not weeks, giving marketers real-time feedback loops. Digital volume is projected to reach 9.7% of total label output by 2029, expanding at a 4.4% CAGR in square-meter terms. Shrink and stretch sleeve labels market participants that integrate inline finishing with inkjet heads gain agility that legacy gravure lines cannot match.

Demand for 360° High-Definition Graphics to Boost Shelf Appeal

Brands increasingly treat the entire container as bill-board space, leveraging sleeves to print photorealistic images and metallic gradients that differentiate crowded categories.[2]Beverage Industry, “Full-Body Graphics Lift Brand Visibility,” beverageindustry.com The format adapts to curves, tapers, and asymmetric shapes without wrinkling, permitting bottle designs that double as brand signatures. Wine producers embed NFC tags and QR codes under clear over-varnish, merging storytelling with authenticity verification. Premium cosmetics adopt unique container silhouettes paired with shrink sleeves to command price premiums in prestige channels. Rapid SKU proliferation inside supermarkets sustains volume momentum for converters with high-resolution rotogravure and offset hybrid lines.

Shift Toward Recyclable PETG and Floatable Sleeve Films

Klöckner Pentaplast’s SmartCycle film uses washable inks that detach in caustic baths, allowing bottles to reenter food-grade rPET loops at scale. Association of Plastic Recyclers protocols require label flotation or easy removal; crystallizable PET sleeves now achieve 95% ink release, preserving optical clarity in recycled pellets. EU rules mandate 25% recycled content in beverage PET from 2025, steering brands toward floatable or low-density films that separate cleanly during sink-float steps. Sleeve suppliers market embedded perforations that consumers tear off before disposal, further reducing contamination.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recycling hurdles of multimaterial sleeves contaminating PET streams | -0.7% | EU-led, expanding globally | Medium term (2-4 years) |

| Competition from stand-up pouches and direct-to-container printing | -1.1% | Global, technology-driven disruption | Short term (≤ 2 years) |

| Resin-price volatility from geopolitical supply shocks | -0.5% | Global, commodity-dependent | Short term (≤ 2 years) |

| EU/NA curbs on PVC sleeves inflating compliance costs | -0.4% | North America and EU regulatory zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Stand-Up Pouches and Direct-to-Container Printing

Lightweight pouches use 60% less plastic than rigid bottles and cost only USD 0.20 per unit compared with USD 0.50 for comparable PET containers.[3]Volpak, “Cost Advantages of Stand-Up Pouches,” volpak.comDigital can printers such as Velox now run 500 cans per minute, eliminating sleeve film altogether and appealing to sustainability-focused craft brands. Direct decoration removes the heat tunnel, trim scrap, and adhesive usage inherent to shrink lines. Cost differentials widen in high-volume carbonated beverages where sleeve application adds 2–2.5 times unit cost relative to offset printing. The shrink and stretch sleeve labels market nonetheless preserves relevance by serving irregular containers that pouches or cans cannot mimic.

Resin-Price Volatility from Geopolitical Supply Shocks

PET feedstock prices remain elevated as Middle-East tensions tighten crude availability, forcing European polyester producers into curtailments. Polyethylene, polypropylene, and PVC pricing show flat-to-down trajectories due to tepid demand, yet PET tracks upward because of purified terephthalic acid (PTA) cost inflation. Converters implement defensive buying to hedge exposure, but smaller firms with limited storage face margin compression. Price uncertainty discourages capital outlays for new sleeve lines, which can exceed USD 5 million per ten-color gravure press. Supply instability also propels interest in recycled content and bio-based resins that diversify away from virgin feedstocks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Stretch Sleeves Gain Despite Shrink Dominance

Shrink sleeves controlled 72.60% of the shrink and stretch sleeve labels market in 2025, reflecting their proven fit for complex bottle geometries and tamper-evident safety seals. High-speed automatic applicators run beyond 800 bottles per minute with error rates under 0.5%, a performance metric difficult for alternate formats. Stretch sleeves need no heat tunnel, trimming energy use by up to 40%, and support recycling because consumers can easily remove them before disposal. The segment’s 8.05% CAGR through 2031 surpasses overall market pace as European beverage brands adopt low-carbon packaging to achieve Scope 3 commitments.

Although shrink technology retains primacy, future production likely evolves toward a dual-solution ecosystem. Shrink formats will secure pharmaceutical vials, functional drinks, and contoured household cleaners that demand form-fitting coverage. Stretch sleeves will expand in water, dairy, and economy cola where price sensitivity intersects with sustainability positioning. Production lines increasingly pair servo-driven mandrel applicators with vision systems that inspect sleeve placement in real time, minimizing rework. Suppliers confirm that both sleeve types now accept the same water-based inkjet inks, simplifying graphic changeovers and reinforcing flexible manufacturing strategies in the shrink and stretch sleeve labels market.

By Material: PET Leadership Reinforced by Recycling Mandates

PET commanded a 36.45% share of the shrink and stretch sleeve labels market size in 2025 and maintains 7.62% growth on regulatory tailwinds that prioritize circular packaging. Wash-off inks from Siegwerk enable bottle-to-bottle recycling with 95% label removal efficiency, safeguarding rPET purity levels suitable for direct food contact. PVC faces decisive headwinds as the EU capped lead content at 0.1% beginning November 2024, prompting widespread reformulation. Polyethylene sleeves target chemical drums and agrochemical jugs that require stress-crack resistance, whereas OPS remains an economical choice for low-temperature dairy but loses traction in carbonated drinks due to scuffing concerns.

Manufacturers invest in floatable PETG that carries less density than standard PET, allowing it to rise in sink-float separators. LINTEC’s recycled film labelstock contains over 80% rPET and yields 24% lower CO₂ emissions versus virgin film. Material decisions now appear in carbon-impact scorecards during brand procurement, elevating sleeve recyclability to strategic level. Over the forecast horizon, PET is projected to widen leadership as more brands publish circularity roadmaps, cementing its influence across every tier of the shrink and stretch sleeve labels market.

By End User: Pharmaceutical Growth Outpaces Food Dominance

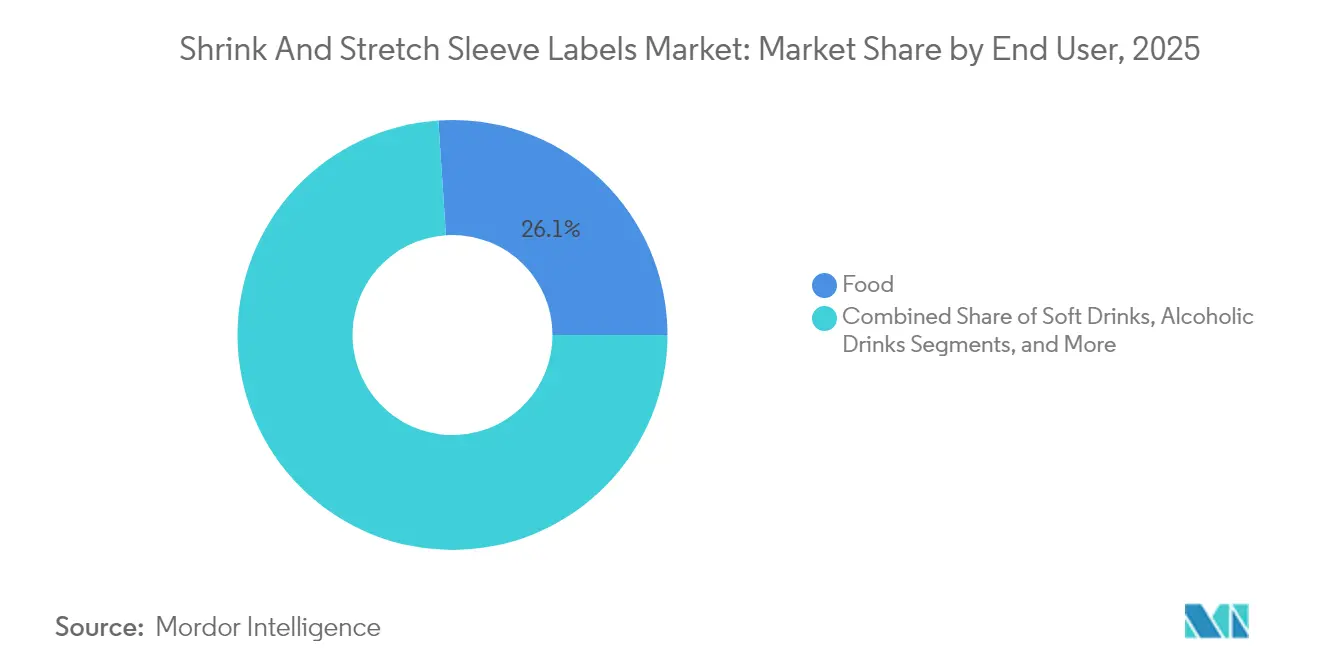

Food applications held 26.05% revenue in 2025, supported by ready-to-drink coffees, flavoured waters, and shelf-stable sauces that rely on 360-degree branding to highlight natural ingredients. The pharmaceutical segment, however, is accelerating at an 8.28% CAGR to 2031, spurred by FDA rules that require tamper-evident features on over-the-counter medicines. Serialization codes imprinted under shrink films permit end-to-end traceability, limiting counterfeit risks in global distribution.

Cosmetic and household products use sleeves to wrap oddly contoured dispensers and trigger bottles, elevating shelf presence in premium aisles. Soft drink and beer labels continue to account for the largest absolute volume yet witness slower growth as consumption patterns plateau in developed markets. Healthcare volume climbs as injectable biologics, nutraceutical gummies, and topical antiseptics enter consumer channels that demand visible safety cues. The interplay of security, sustainability, and branding positions pharmaceuticals as the fastest-expanding use case inside the shrink and stretch sleeve labels market.

Geography Analysis

Europe retained 29.55% revenue in 2025 due to robust environmental policies and a culture of premium packaging. Germany, France, and the United Kingdom direct a sizable share of capital expenditure toward sleeve film lines fitted with energy-efficient infrared tunnels. EU Packaging and Packaging Waste Regulation stipulates recyclability by 2030, driving demand for PET-based sleeves that detach cleanly in wash plants. The region’s average selling price per thousand sleeves exceeds the global mean by 12% because of sophisticated graphic requirements and low minimum runs requested by boutique spirits.

Asia-Pacific records the fastest trajectory at an 7.86% CAGR thanks to surging disposable income, urbanization, and the rise of functional beverages. China’s express packaging standard GB 43352-2023 restricts heavy metals in inks, compelling local converters to adopt compliant chemistries. Thailand pilots label-free PET bottles that store product data in QR codes printed on caps, pressuring traditional sleeve volumes yet opening new avenues for smart interactive films. Japan’s early adoption of water-based inkjet for flexible film aligns with its plastics resource circulation act, fostering home-grown innovations that resonate across regional markets.

North America benefits from a vibrant craft beer ecosystem and a well-established healthcare framework. Tamper-evident needs in pharmaceuticals and over-the-counter nutritional supplements ensure a baseline of steady demand. South America leverages abundant PET resin supply yet remains exposed to currency swings that limit capital spending on high-end presses. The Middle East and Africa trail in installed capacity but exhibit pockets of high value in premium imported spirits and personal care, which rely on sleeves for brand elevation. Taken together, geographic diversity underpins the long-term resilience of the shrink and stretch sleeve labels market.

Regulatory Landscape

The EU Packaging and Packaging Waste Regulation (EU) 2025/40 entered into force on 11 February 2025 and applies from 12 August 2026, prioritizing packaging designed for material recycling and compatibility with collection, sorting, and recycling systems across the union. This reinforces the shift away from sleeve constructions that hinder PET recycling and elevates demand for wash-off inks, floatable films, and easy consumer-removal features.

In the United States, sleeves used on food packaging must comply with FDA requirements for materials intended for food contact, including the Food Contact Notification (FCN) process where applicable, which can affect ink and film chemistry selection and change-control practices for converters supplying food and beverage. In the United Kingdom, the Plastic Packaging Tax framework applies to finished packaging components and can extend to labels if manufactured separately, with tax liability linked to meeting the 30% recycled-content threshold, increasing the need for documented recycled-content and component-level accounting across sleeve supply chains.

Competitive Landscape

The shrink and stretch sleeve labels market shows moderate concentration with the top five converters controlling about 45% of global revenue. CCL Industries posted 9% sales growth in Q4 2024 as acquisitions and specialty labels boosted volumes. Multi-Color Corporation expanded its footprint by acquiring Eximpro and Starport Technologies, adding shrink capacity and RFID expertise to its portfolio. Avery Dennison’s Intelligent Labels unit recorded double-digit unit growth as RFID incursions penetrated beverage and personal-care lines.

Strategic moves favor investments in recyclable materials, washable inks, and digital embellishment. Berry Global channeled R&D toward light-weight shrink films compatible with near-infrared sorting, while Klöckner Pentaplast launched SmartCycle to lock in customers subject to EU recycled content quotas. Technology challengers such as Velox promote direct-to-shape inkjet that eliminates film, drawing interest from carbon-reduction programs. Patent filings covering perforated tear-strips and low-energy shrink ovens underscore persistent innovation, even as material inflation nudges converters to evaluate backward integration into resin compounding.

The ongoing wave of consolidation grants large players pricing power, end-to-end service capabilities, and geographic risk diversification. Smaller regional converters differentiate through artisan-level graphics and flexible turnaround. Success ultimately hinges on the capacity to balance sustainability compliance, evolving brand aesthetics, and stringent regulatory environments that collectively shape the future direction of the shrink and stretch sleeve labels market.

Shrink And Stretch Sleeve Labels Industry Leaders

CCL Industries

Fuji Seal International

Berry Global Group

Multi-Color Corporation

KP Klockner Pentaplast

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

PPWR-driven design-for-recycling requirements and brand circularity scorecards create whitespace for sleeve solutions that separate cleanly in PET recycling and reduce material use without sacrificing application performance. Innovia Films" RayoFloat high-shrink polyolefin sleeve film (February 2025) offers improved recyclability by enabling sink-float separation with PET streams and supports thinner gauges while preserving performance.

Another opportunity sits at the intersection of compliance and marketing agility: short-run, high-graphics sleeves that add tamper evidence and traceability features for regulated and premium categories. The report context points to minimum order quantities dropping to around 1,000 sleeves with digital inkjet, helping niche beverage and personal-care brands iterate SKUs quickly, while PVC curbs tighten and recycling constraints become procurement gating factors. Converters that standardize recyclable film structures, washable-ink systems, and easy-removal/perforated designs can capture projects where brand owners re-platform labels to meet recyclability and recycled-content targets.

Recent Industry Developments

- June 2026: CCL Industries completed the acquisition of Sleever International Company SA, integrating the shrink sleeve platform into its labeling operations and aligning related film activities under Innovia Films. The deal strengthens CCLs global scale in shrink sleeves and expands its ability to offer sustainability-focused sleeve solutions across multinational brand accounts.

- February 2025: Innovia Films launched its RayoFloat high-shrink polyolefin sleeve film, designed to improve PET recycling compatibility and enable thinner gauges, aligning with circularity targets and brand packaging strategies.

- May 2024: Fuji Seal initiated a horizontal recycling system for shrink sleeve labels with PIETRO Co., Ltd., advancing label-to-label resource circulation and supporting brand packaging sustainability commitments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of shrink and stretch sleeve labels sold for packaging, where a printed film sleeve is applied over a container for branding, information, and on-pack impact. Our sizing follows demand from label converting through to end-use packaging consumption across major regions.

Scope exclusions: We exclude self-adhesive pressure-sensitive labels, in-mold labels, and direct container printing where no sleeve label is supplied.

Segmentation Overview

- By Type

- Shrink Sleeve

- Stretch Sleeve

- By Material

- PVC

- PET / PET-G

- PE

- OPP and OPS

- Other Materials (PO, PLA, etc.)

- By End User

- Food

- Soft Drinks

- Alcoholic Drinks

- Cosmetics and Household

- Pharmaceutical

- Other End Users

- By Geography

- North America

- United States

- Canada

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research built the starting structure for the model and helped us avoid making assumptions without a reference point. We reviewed public packaging and plastics statistics from national customs and trade databases, including the UN Comtrade dataset, and we also checked government manufacturing and producer price series where label and film proxies are available.

To keep inputs realistic, we relied on source types such as sustainability and recycling guidance from agencies like the US EPA and the European Commission, trade association publications for packaging and plastics, and peer-reviewed articles that discuss sleeve materials and recyclability constraints. Company annual reports, investor decks, and press releases were used to track capacity moves, geographic footprints, and exposure to beverage and food packaging. A paid subscription for company financials and news helped cross-check timelines and market signals. This list is illustrative, and we referenced additional public sources for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions were used to translate secondary signals into sleeve label demand, especially where sleeves are embedded inside broader packaging lines. We spoke with participants across the value chain, including label converters, film suppliers, packaging buyers, and distribution-side experts, covering APAC, EMEA, and the Americas, so the assumptions align with local packaging formats and material preferences.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 15% | APAC: 43% |

| Mid tier: 60% | Functional/Unit leaders: 37% | EMEA: 37% |

| Smaller Players: 15% | Managers: 48% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where packaging demand indicators and trade-linked supply signals are used to reconstruct the regional sleeve label revenue pool, and then the totals are filtered based on adoption of sleeve formats across key end uses. To keep the outputs grounded, we corroborate with selective bottom-up approximations, including sampled converter revenues, channel checks on sleeve label mix, and volume by container formats multiplied by typical label cost ranges.

Inputs used in the model include beverage and food packaging output trends, regional consumption of PET bottles and other sleeve-friendly containers, film material mix shifts (PVC versus PET-G and PE), average label thickness and yield assumptions, and pricing direction linked to polymer and printing input costs. Where data is patchy, we use neighboring-country proxies and adjust them with interview feedback on local penetration and price points, then review the results for reasonableness.

For forecasting, scenario analysis is used around a base case, since sleeve growth is sensitive to sustainability rules, recyclability design changes, and brand conversion cycles. Assumptions for penetration, material substitution, and price progression are set using a mix of historical patterns and what interviewees expect to hold over the next five years.

Data Validation & Update Cycle

Validation is done through triangulation across three angles: demand indicators, supply-side capacity and trade flows, and pricing realism checks, so no single weak data point over-pulls the result. Outliers are flagged when growth rates or regional shares move outside normal packaging trends, and we recheck the underlying drivers before sign-off.

Reports are refreshed annually, and interim updates are triggered when material events occur, such as major capacity additions, policy changes affecting label recyclability, or sharp resin price moves. Before delivery, we run a fresh review pass and re-contact sources where a key assumption has shifted, so clients receive the most current view available.

Mordor Intelligence's Shrink and Stretch Sleeve Labels Market Sizing Compared With Other Published Estimates

Published market sizes for sleeve labels can vary a lot, even when the topic name looks the same. The differences usually come from what each study counts as a sleeve label, which years are used as the base, how prices are carried forward, and how aggressively end-use adoption is projected.

The table highlights a spread that is mainly explained by scope and year alignment, along with whether stretch sleeves are fully included or treated as a smaller adjacent format. Some publishers also include broader shrink label formats or apply uniform global price assumptions, which can lift totals in regions where packaging mix and film choices differ.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 17.42 B (2026) | |

| Global Consultancy A | USD 15.78 B (2024) | Uses an earlier base year and a different forecast window, and its end-use weighting can understate the more recent conversion to full-body sleeves in beverages and household products. |

| Industry Publisher B | USD 15.70 B (2026) | Focuses on shrink sleeves and related packaging formats, which can leave stretch sleeves and some material-specific pricing effects less consistently captured across regions. |

The table shows that part of the gap is simply the year being compared, and part comes from what is counted inside the market. In Mordor Intelligence's model, the total is tied to shrink and stretch sleeve labels as a packaging label product, and pricing and adoption are checked against end-use packaging volumes before the final number is locked.

Key Questions Answered in the Report

What is the current value of the shrink and stretch sleeve labels market?

The market is valued at USD 17.42 billion in 2026 and is projected to reach USD 24.57 billion by 2031, registering a 7.12% CAGR.

Which sleeve type is growing fastest?

Stretch sleeves are expanding at an 8.05% CAGR because they eliminate heat tunnels and simplify recycling.

How does digital inkjet printing influence market dynamics?

Inkjet presses lower minimum orders to 1,000 sleeves and cut lead times to four weeks, allowing niche beverage and personal-care brands to launch short-run SKUs quickly.

Which region is expected to post the highest growth rate?

Asia-Pacific is forecast to grow at an 7.86% CAGR through 2031, driven by expanding consumer goods output and rising disposable incomes.

Page last updated on: