Water Free/ Waterless Urinal Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

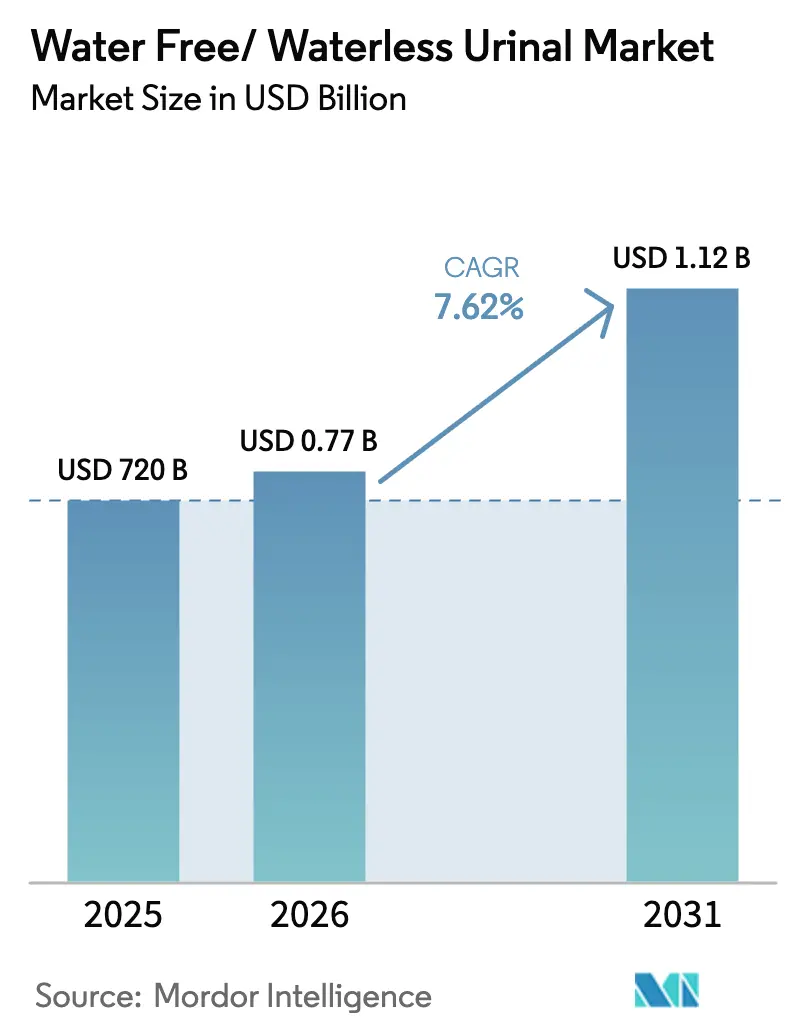

| Market Size (2026) | USD 0.77 Billion |

| Market Size (2031) | USD 1.12 Billion |

| Growth Rate (2026 - 2031) | 7.62% CAGR |

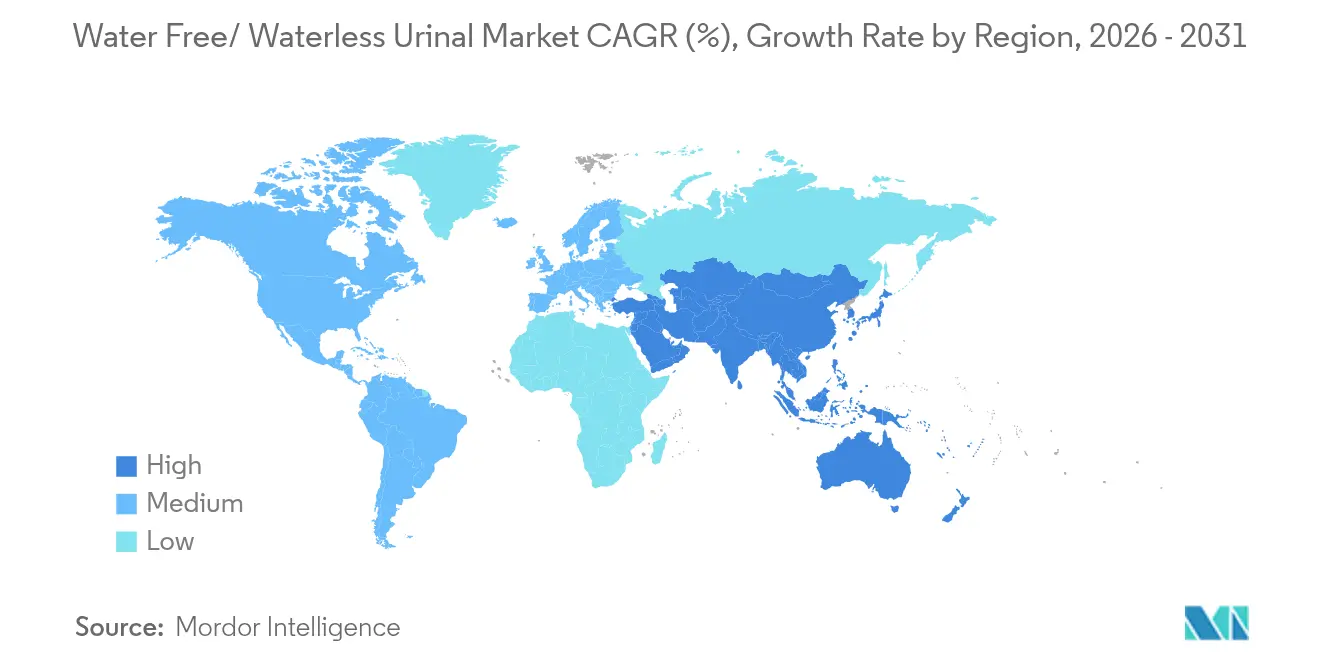

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

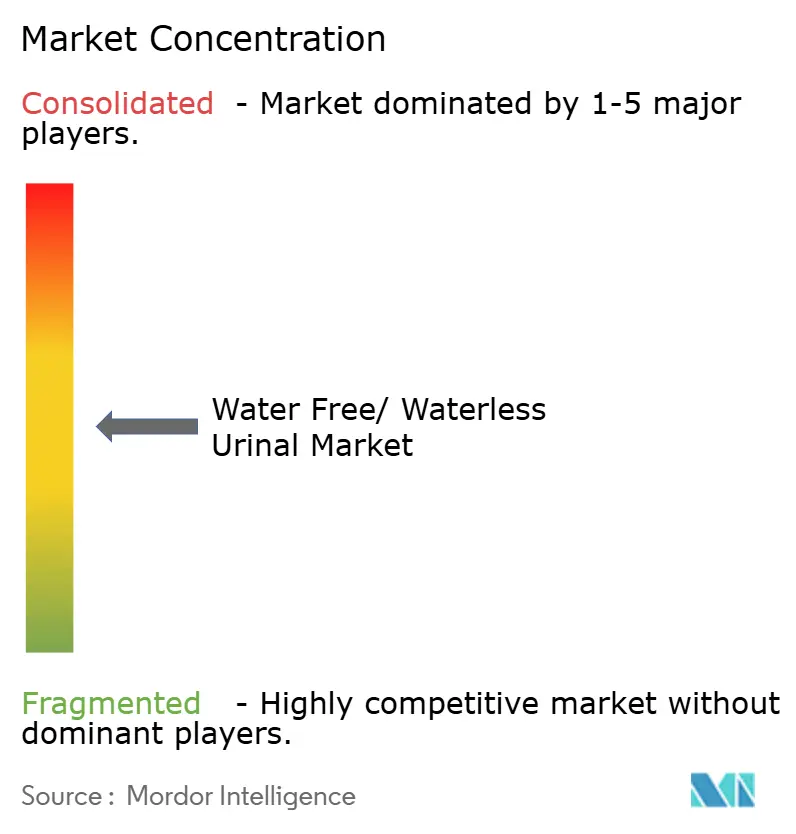

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Water Free/ Waterless Urinal Market Analysis by Mordor Intelligence

Water Free/ Waterless Urinal market size in 2026 is estimated at USD 774.86 million, growing from 2025 value of USD 720 million with 2031 projections showing USD 1.12 billion, growing at 7.62% CAGR over 2026-2031. Current adoption is propelled by accelerating water scarcity pressures, green building mandates, and corporate sustainability programs that position zero-water fixtures as a practical conservation solution. Regulatory alignment continues to tighten, with municipalities such as San Francisco capping urinal flows at 0.125 gpf, a level that effectively promotes water-free designs[1]San Francisco Public Utilities Commission, “Water Efficient Urinal Ordinance,” SFPUC, sfwater.org. Liquid-sealant cartridge systems dominate the water-free/ waterless urinal market with a 38.5% share in 2024, while membrane traps record the fastest 9.65% CAGR as facility managers prioritize lower maintenance. Commercial buildings still account for 69.7% of installations, although residential do-it-yourself kits are fueling an 8.55% CAGR and broadening the customer base. North America retains the largest regional footprint at 35.1% share, yet the Asia Pacific growth corridor is advancing at 8.91% CAGR as China and India embed conservation targets in new construction codes.

Key Report Takeaways

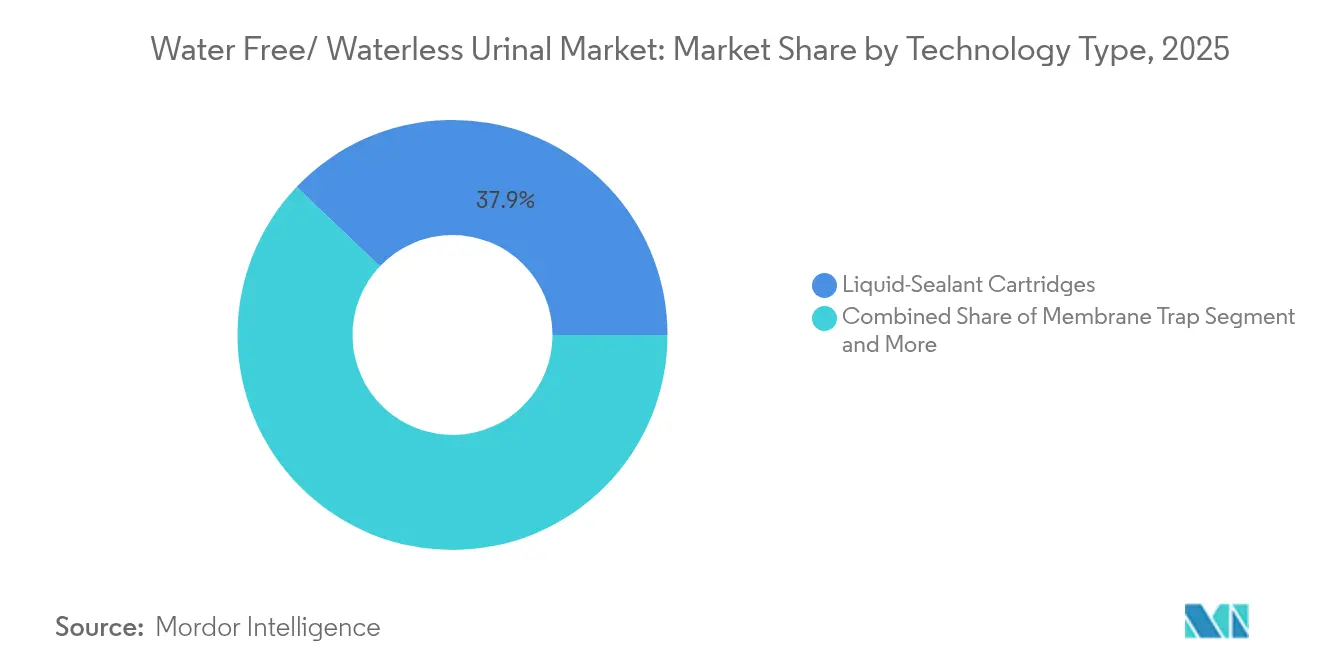

- By technology type, liquid-sealant cartridges led with 37.92% of the water-free/ waterless urinal market in 2025, and membrane traps are rising at a 9.08% CAGR through 2031.

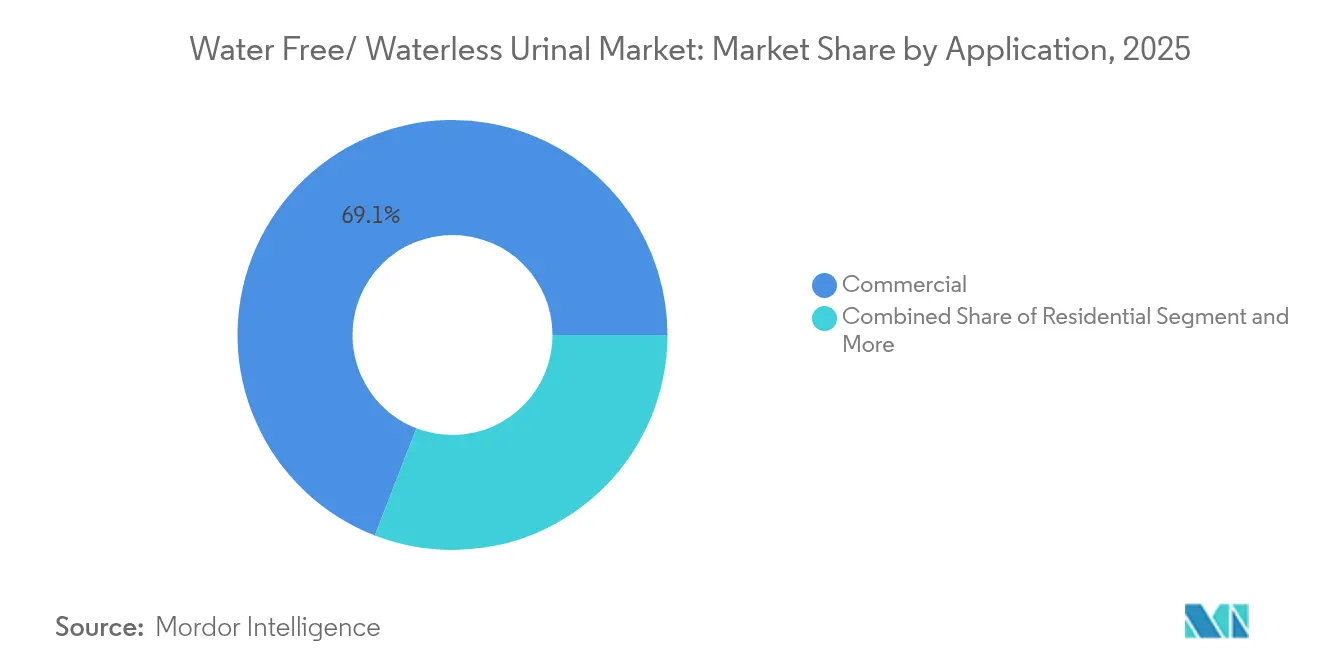

- By application, the commercial segment held 69.12% revenue share of the water-free/ waterless urinal market in 2025, while the residential category is expanding at an 8.12% CAGR to 2031.

- By material, vitreous china accounted for 52.05% of the water-free/ waterless urinal market size in 2025, but poly-composite units are projected to grow at a 8.61% CAGR.

- By distribution channel, offline sales maintained a 71.05% share in 2025, whereas online platforms are forecast to rise at an 10.42% CAGR.

- By geography, North America dominated with 34.72% of the water-free/ waterless urinal market in 2025; the Asia Pacific region is projected to advance at an 8.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Water Free/ Waterless Urinal Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter corporate ESG targets and transparency requirements | 1.5% | Global, led by North America & Europe | Long term (≥ 4 years) |

| Escalating water scarcity regulations and green building mandates | 1.2% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Lower total cost of ownership versus traditional flush urinals | 1.0% | Global, particularly APAC emerging markets | Short term (≤ 2 years) |

| Increased deployment in high-footfall public infrastructure | 0.8% | North America & APAC core, spill-over to MEA | Medium term (2-4 years) |

| LEED and WELL certification incentives driving adoption in institutional construction | 0.7% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Growing DIY adoption in residential retrofits using cartridge-replacement kits | 0.7% | North America & Europe residential markets | Short term (≤ 2 years) |

| Expansion of dry sanitation mandates in remote/off-grid housing and work camps | 0.6% | Global, concentrated in water-stressed regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Corporate ESG Targets and Transparency Requirements

Global real-estate investors disclose water metrics under the GRESB framework, which lists waterless urinals as approved “dry fixtures”[2]GRESB BV, “2025 Real Estate Assessment Reference Guide,” GRESB, gresb.com. Fortune 500 retailers, led by Walmart, deploy high-efficiency urinals in every new store to meet water stewardship targets. Sloan Valve Company secured the 2024 EPA WaterSense Excellence Award, signaling that institutional buyers prefer vendors with documented sustainability credentials. Science-based targets are pushing companies toward measurable water reduction goals that cannot be met by incremental flow-rate cuts alone. Procurement policies now embed specific language for water-free fixtures, providing continuous demand for the water-free/ waterless urinal market.

Escalating Water Scarcity Regulations and Green Building Mandates

Integrated urban water regulations are now requiring zero-water fixtures in new developments. The European Union’s 2024 Urban Wastewater Treatment Directive pushes member states to prioritize water reuse, indirectly supporting the adoption of dry urinals[3]Publications Office of the European Union, “Directive (EU) 2024/… on Urban Wastewater Treatment,” Official Journal of the European Union, eur-lex.europa.eu. Cities that faced droughts, including Brisbane, mandate waterless urinals in public buildings. New York City obliges developers to submit conservation plans before approving waterless installations[4]New York City Department of Buildings, “Water Conservation Plan Guidelines for Waterless Urinals,” NYC DOB, nyc.gov. IAPMO’s 2023 Water Efficiency and Sanitation Standard sets detailed performance metrics that align directly with water-free technologies. LEED projects can earn up to four points for installing waterless urinals, making the fixtures an obvious choice for certification-focused construction.

Lower Total Cost of Ownership Versus Traditional Flush Urinals

Each zero-water fixture eliminates up to 40,000 gallons of annual consumption and drives rapid payback where water tariffs are high. Dubai Municipality’s deployment of nearly 500 units saves 52 million L and USD 163,000 in yearly water charges. Maintenance savings arise from the absence of flush valves that are frequently damaged in public restrooms. TOTO’s EcoPower approach captures energy from minimal rinse cycles, reducing electricity costs and supporting off-grid installations. Typical commercial payback periods range from 18 to 24 months, reinforcing the economic rationale behind the water-free/ waterless urinal market.

Increased Deployment in High-Footfall Public Infrastructure

Airport, subway, and highway facilities specify waterless urinals to lower utility bills and meet sustainability reporting requirements. Philadelphia International Airport budgeted USD 145 million for restroom upgrades that include dry units and contactless features. Japanese highway operators report annual savings of USD 247,000 at Moriya Service Area and USD 25,000 at Minori after switching to low-water systems. High-visibility projects deliver proof of performance, encouraging other public agencies to adopt similar solutions. Transit authorities fold water-efficiency requirements into capital plans, ensuring a multi-year installation pipeline for vendors in the water free waterless urinal industry.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher upfront capital cost versus ≥0.5 gpf water-efficient fixtures | -0.7% | Price-sensitive markets, particularly emerging economies | Short term (≤ 2 years) |

| Retrofitting constraints due to incompatible legacy plumbing gradients | -0.5% | North America & Europe with aging infrastructure | Medium term (2-4 years) |

| Municipal code disparities causing permitting delays across jurisdictions | -0.4% | Global, particularly fragmented regulatory environments | Medium term (2-4 years) |

| Performance risk from low-cost or counterfeit cartridges in price-sensitive markets | -0.3% | APAC & MEA emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher Upfront Capital Cost Versus Water-Efficient Fixtures

Waterless units cost two to three times more than standard 1.0 gpf urinals, discouraging budget–controlled buyers despite lifecycle savings. A residential Baja model retails for USD 248, outpacing many conventional alternatives. Public procurement rules often reward the lowest upfront bid, undermining technologies that succeed on total cost. Subsidized water tariffs in some regions further delay cost parity. Utility rebates and vendor financing programs are emerging to close the gap and accelerate adoption in the water-free/ waterless urinal market.

Retrofitting Constraints Due to Incompatible Legacy Plumbing Gradients

Many buildings lack the recommended two-degree drain slope and venting for undiluted urine transport. Upgrading the stack can require extensive demolition and specialized piping materials to resist corrosion. Municipal codes sometimes still demand a cold-water supply line, even when the fixture is designed to operate dry, adding complexity. Technical training gaps among installers heighten perceived risk. Manufacturers now ship retrofit kits and offer remote design support, yet structural limitations continue to slow upgrades across older portfolios in the water free waterless urinal industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology Type: Cartridge Systems Drive Innovation

Liquid-sealant cartridges controlled 37.92% of the water-free/ waterless urinal market in 2025, supported by well-known odor barriers and standard replacement routines that simplify facility scheduling. Falcon Waterfree’s cartridge design helped Dubai Municipality save 52 million L of water each year. Membrane traps are accelerating at 9.08% CAGR because they cut service frequency, withstand cleaning chemicals, and eliminate the need for sealant liquids that can evaporate in hot climates.

The segment now attracts research funding aimed at extending membrane life to two years or longer. Biological block inserts occupy a smaller niche but appeal to eco-conscious facilities looking for natural bio-enzymatic odor control. Mechanical float-ball systems persist in extreme cold sites where sealants can thicken. Hybrid concepts, such as Sloan’s bi-weekly rinse system, blend micro-flush cycles with waterless design to ease transition in conservative markets. Continuous performance gains ensure technology choice remains a key differentiator in the water-free/ waterless urinal market.

By Material: Durability Drives Poly-Composite Growth

Vitreous china maintained a 52.05% share of the water-free/ waterless urinal market size in 2025 due to its familiar look, chemical resistance, and existing production lines. Poly-composite bowls are projected to expand at 8.61% CAGR as stadiums, schools, and correctional facilities demand impact-resistant, lightweight units that lower installation labor. Manufacturers exploit these composites to mold complex airflow channels that improve splash control and odor capture.

Stainless steel installations persist in food processing, healthcare, and high-security environments where infection-control cleaning is routine. Emerging fiberglass reinforced plastic designs promise even longer life in coastal climates. Decision makers now weigh lifetime repairs and vandalism costs rather than sticker price alone. As building owners benchmark maintenance metrics for ESG reports, rugged materials are gaining ground across the water-free/ waterless urinal market.

By Application: Residential Adoption Accelerates

Commercial venues still contributed 69.12% of 2025 revenues as corporate offices, industrial sites, and malls integrate measurable water reduction steps into annual sustainability reports. Many property managers now specify waterless urinals across new builds to secure LEED credits without sacrificing restroom capacity. The residential segment is recording an 8.12% CAGR as consumers gain confidence with do-it-yourself cartridge replacement kits and as drought-prone regions incentivize retrofits through rebate vouchers.

Innovators like Ekam Eco Solutions demonstrate scalability in emerging economies: a single unit in an Indian apartment block saves 151,000 L per year and reduces septic system loads. Schools and universities in both developed and developing nations are also switching to waterless units to satisfy green campus goals. Healthcare facilities test sealed systems that limit airborne pathogens. The widening application mix underpins resilient demand across the water-free/ waterless urinal market.

By Distribution Channel: E-Commerce Transforms Access

Offline wholesalers still held a 71.05% share in 2025 because designers and contractors rely on established supply chains for technical submittals and bulk pricing. Showrooms enable side-by-side comparisons, an advantage when facility teams evaluate odor control claims. Online sales are growing at 10.42% CAGR as homeowners and small businesses appreciate direct-to-door logistics and installation videos. Platforms such as Ferguson blend self-service ordering with on-site pickup, illustrating an omnichannel shift.

Manufacturers leverage digital storefront analytics to refine cartridge bundle offerings by geography and climate. Professional installers increasingly source detailed specification sheets online, even when final purchases route through traditional distributors. Warranty registration portals cultivate a recurring maintenance business. The channel landscape is therefore evolving rapidly, reinforcing customer choice throughout the water-free/ waterless urinal market.

Geography Analysis

North America generated the largest regional revenue in 2025, capturing 34.72% of the water-free/ waterless urinal market due to mandatory ultra-low-flow codes and widespread adoption of LEED and WELL certification. Municipal programs reimburse up to USD 400 per fixture in drought-affected states, trimming payback to under two years. Corporate campuses use public dashboards to track every gallon saved, increasing peer pressure and cementing the specification of dry urinals in renovation guidelines.

Europe follows with a tightly regulated framework that is now strengthening under the Urban Wastewater Directive. Germany illustrates untapped volume: Researchers at Wuppertal Institut note that only 100,000 waterless urinals are installed among 6 million total units, signaling a large replacement opportunity. Scandinavia leads per-capita penetration through aggressive energy-plus building codes. The Middle East and North Africa region continues to accelerate because water tariffs exceeded electricity tariffs for the first time in 2024, making conservation investments economically attractive. Dubai’s government installations serve as proof points that influence hotel and shopping-mall retrofits.

Asia Pacific is forecast to grow at 8.45% CAGR, the fastest pace within the water free/ waterless urinal market. China’s latest building rules cap indoor water use and promote dual plumbing for reclaimed supply, driving new developments toward dry fixtures. India’s Jal Jeevan Mission funds urban water projects that reward innovative demand-side technologies, and local producers have begun exporting cost-optimized models to Southeast Asia. Advanced economies such as Japan push hybrid technology to align with national smart-city pilots, while Australia’s prolonged drought keeps conservation top of mind across new schools and public buildings.

Mordor Intelligence provides coverage of the water free/ waterless urinal market across other key regional markets, including Asia, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The market remains moderately fragmented, with global plumbing brands and specialized waterless firms vying for contracts. Sloan Valve Company, Kohler Co., and American Standard Brands cross-sell waterless lines through entrenched distributor networks and multi-product bundles. URIMAT Schweiz AG and Falcon Waterfree Technologies concentrate on core dry-fixture R&D, resulting in deep patent portfolios and long-term service agreements. This mix holds merger potential, evidenced by KWC Group’s purchase of Newcastle Joinery Ltd. in December 2024, which broadened capacity for custodial installations.

Product positioning pivots around total cost of ownership arguments. Sloan offers cartridge subscription plans that lock in aftermarket revenues while reassuring facility managers of predictable maintenance budgets[5]U.S. Environmental Protection Agency, “EPA WaterSense 2024 Excellence Award – Sloan Valve Company,” EPA, epa.gov. Kohler certified 120 additional WaterSense products in 2023, demonstrating continued scaling of conservation lines. TOTO differentiates with energy-harvesting EcoPower to reduce both water and electricity loads. Smaller regional firms leverage lower labor costs to penetrate price-sensitive segments, particularly in Asia Pacific, where infrastructure projects require local content.

Firms also compete on digital service layers. Remote monitoring apps flag cartridge replacement cycles based on actual use counts, cutting labor visits. Augmented-reality maintenance guides support inexperienced plumbers in emerging markets. Training partnerships with plumbing schools create early brand loyalty. As companies capture more lifecycle data, they refine designs for easier recycling and end-of-life recovery, aligning with circular-economy commitments that influence investor evaluations within the water free/ waterless urinal market.

Water Free/ Waterless Urinal Industry Leaders

Falcon Waterfree Technologies

Sloan Valve Company

Duravit AG

Kohler Co

American Standard Brands

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Plumbing Manufacturers International highlighted Falcon Waterfree Technologies’ hybrid urinal achieving 98% water reduction in its 2024 Annual Report.

- January 2025: TOTO USA launched redesigned urinals with EcoPower flushometer technology that captures flow energy and achieves an 87% reduction in water use while eliminating external power needs.

- December 2024: KWC Group acquired Newcastle Joinery Ltd. to expand its sanitary solutions portfolio in high-security applications.

- July 2024: Sloan Valve Company earned the 2022 EPA WaterSense Excellence Award for leadership in water-saving restroom solutions including waterless urinals.

Global Water Free/ Waterless Urinal Market Report Scope

The water-free or waterless urinal market consists of sanitary fixtures designed to operate without water, utilizing trap inserts or cartridges to manage urine flow and odor. These urinals are environmentally sustainable, reduce operational costs, and comply with green building standards, making them increasingly popular in commercial and public facilities globally.

The water-free/ waterless urinals market is segmented by technology, application, distribution channel, and region. By technology, the market is segmented into liquid sealant cartridges, membrane traps, biological blocks, and mechanical balls. By applications, the market is segmented into residential and commercial. By distribution channels, the market is segmented into offline and online. By region, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The report offers market sizes and forecasts in terms of value (USD) for all the above segments.

| Liquid-Sealant Cartridges |

| Membrane Traps / Valve Barriers |

| Biological Blocks |

| Mechanical Float-Balls |

| Vitreous China |

| Stainless Steel |

| Poly-composite / FRP |

| Commercial |

| Residential |

| Others (public spaces, institutional, etc.) |

| Offline (Plumbing Wholesalers, DIY Stores) |

| Online (e-commerce, D2C) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Technology Type | Liquid-Sealant Cartridges | |

| Membrane Traps / Valve Barriers | ||

| Biological Blocks | ||

| Mechanical Float-Balls | ||

| By Material | Vitreous China | |

| Stainless Steel | ||

| Poly-composite / FRP | ||

| By Application | Commercial | |

| Residential | ||

| Others (public spaces, institutional, etc.) | ||

| By Distribution Channel | Offline (Plumbing Wholesalers, DIY Stores) | |

| Online (e-commerce, D2C) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the water free/ waterless urinal market by 2031?

The market is forecast to reach USD 1.12 billion by 2031 based on an 7.62% CAGR.

Which technology segment is growing fastest?

Membrane traps are advancing at a 9.08% CAGR, the highest among available technologies.

Why are waterless urinals attractive for commercial buildings?

They save up to 40,000 gallons per unit each year, cut maintenance on flush valves and contribute toward LEED water credits.

What is the main barrier to wider adoption?

Higher upfront fixture costs remain the primary obstacle, especially in price-sensitive markets, despite strong total cost of ownership benefits.

Page last updated on: