Vehicle Roadside Assistance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 32.8 Billion |

| Market Size (2031) | USD 41.33 Billion |

| Growth Rate (2026 - 2031) | 4.73% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

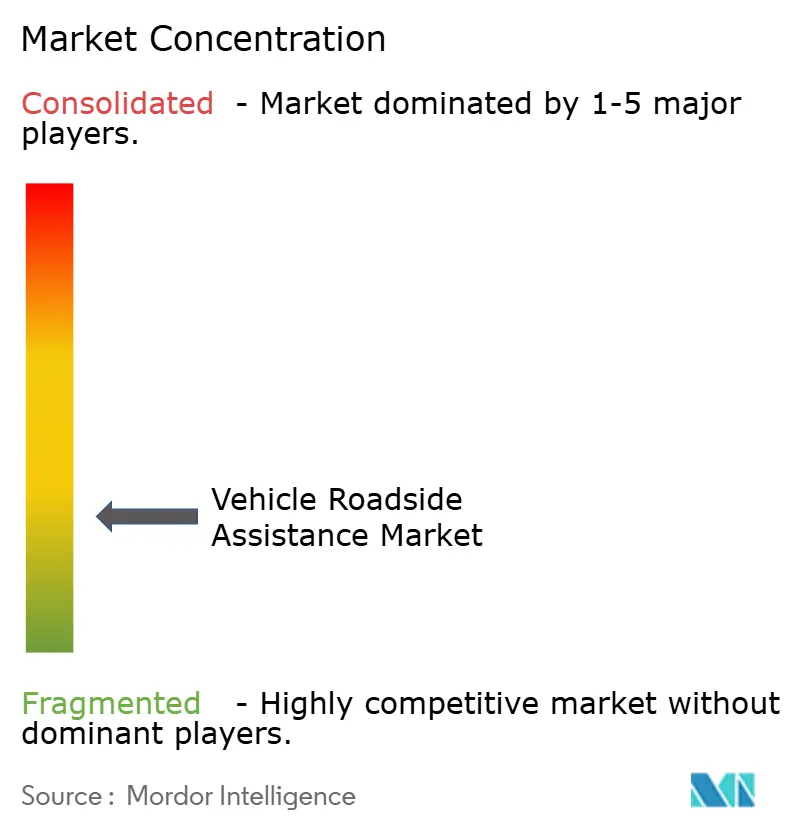

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vehicle Roadside Assistance Market Analysis by Mordor Intelligence

The vehicle roadside assistance market size is expected to grow from USD 31.32 billion in 2025 to USD 32.8 billion in 2026 and is forecast to reach USD 41.33 billion by 2031 at 4.73% CAGR over 2026-2031. Expansion stems from rising global car ownership, rapid digitalisation of dispatch operations, and higher expectations for seamless support across vehicle platforms. Strategic consolidation among insurers, automotive clubs, and technology firms is building wide-reaching service networks that blend insurance policies with app-driven roadside solutions. At the same time, the growth of connected cars gives operators telematics data that improves predictive maintenance, cuts response times, and raises average revenue per incident. Elevated input costs and labour shortages persist, yet economies of scale from recent acquisitions offset much of this pressure, allowing leading players to maintain competitive pricing while investing in EV-specific tooling.

Key Report Takeaways

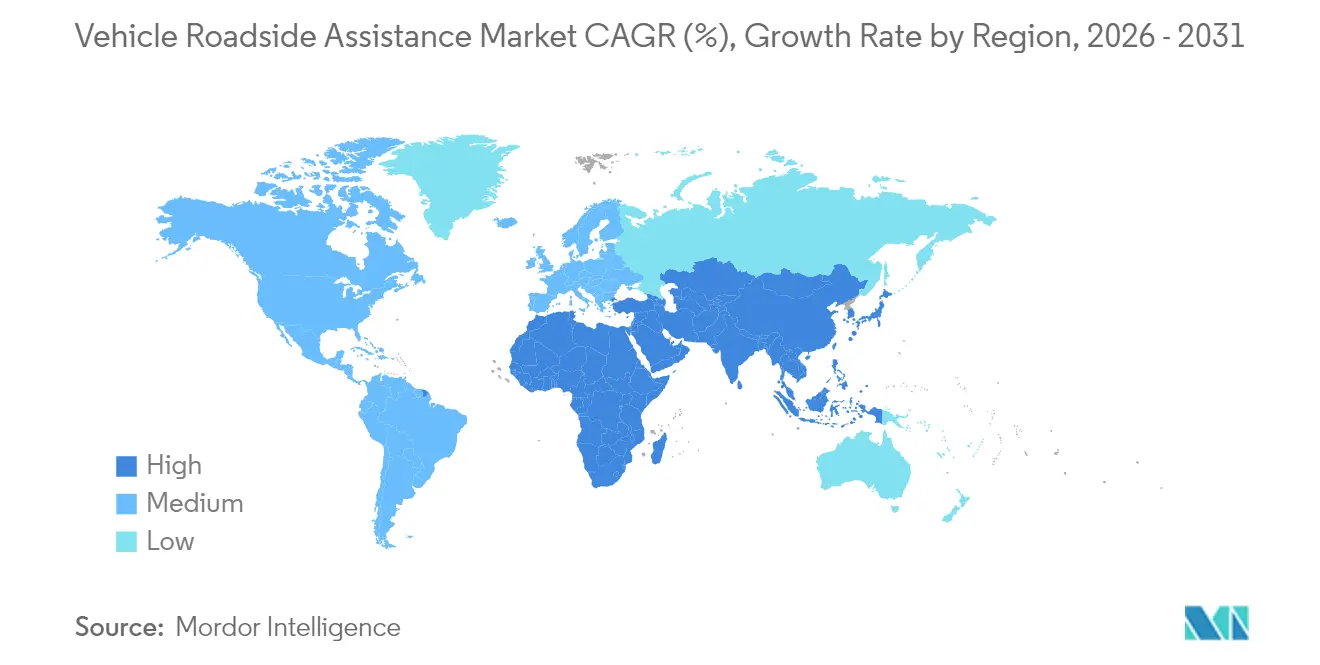

- By geography, North America commanded 39.12% of the vehicle roadside assistance market share in 2025, whereas Asia-Pacific is projected to register a 5.86% CAGR to 2031.

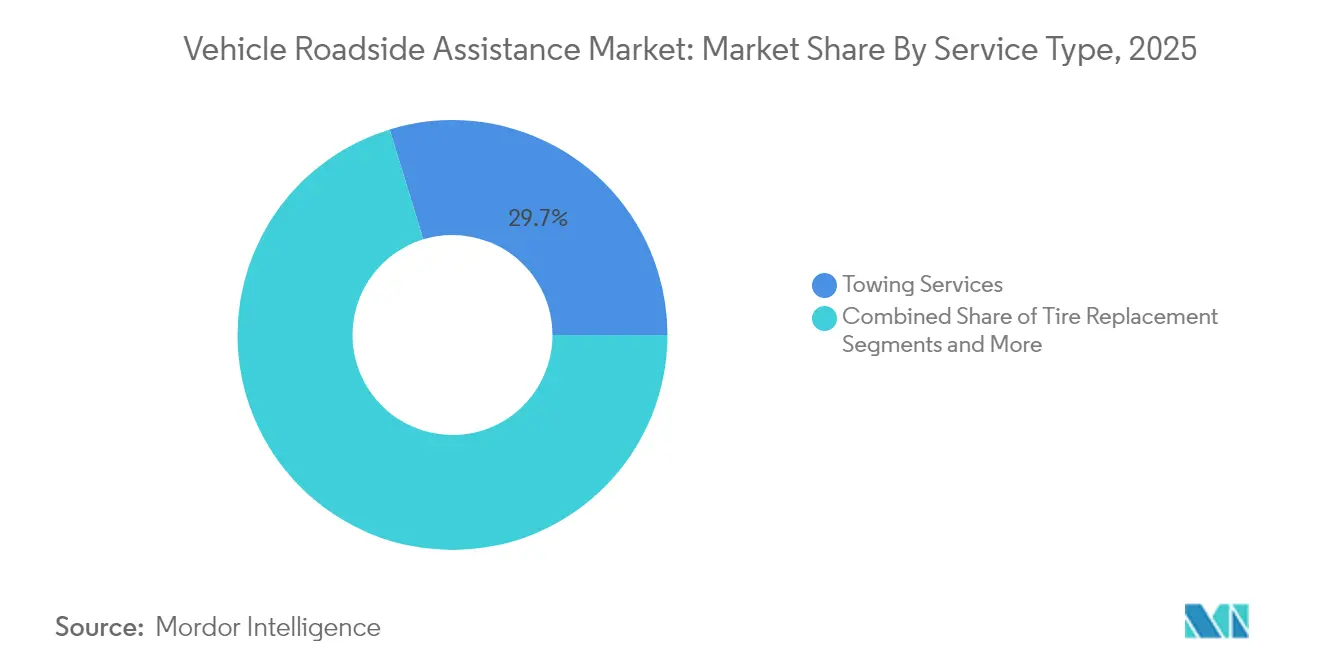

- By service type, towing led with 29.72% of vehicle roadside assistance market share in 2025; tire replacement is forecast to record a 7.62% CAGR through 2031.

- By provider type, motor insurance companies controlled 32.21% of the vehicle roadside assistance market size in 2025, while automotive clubs are tracking a 8.7% CAGR to 2031.

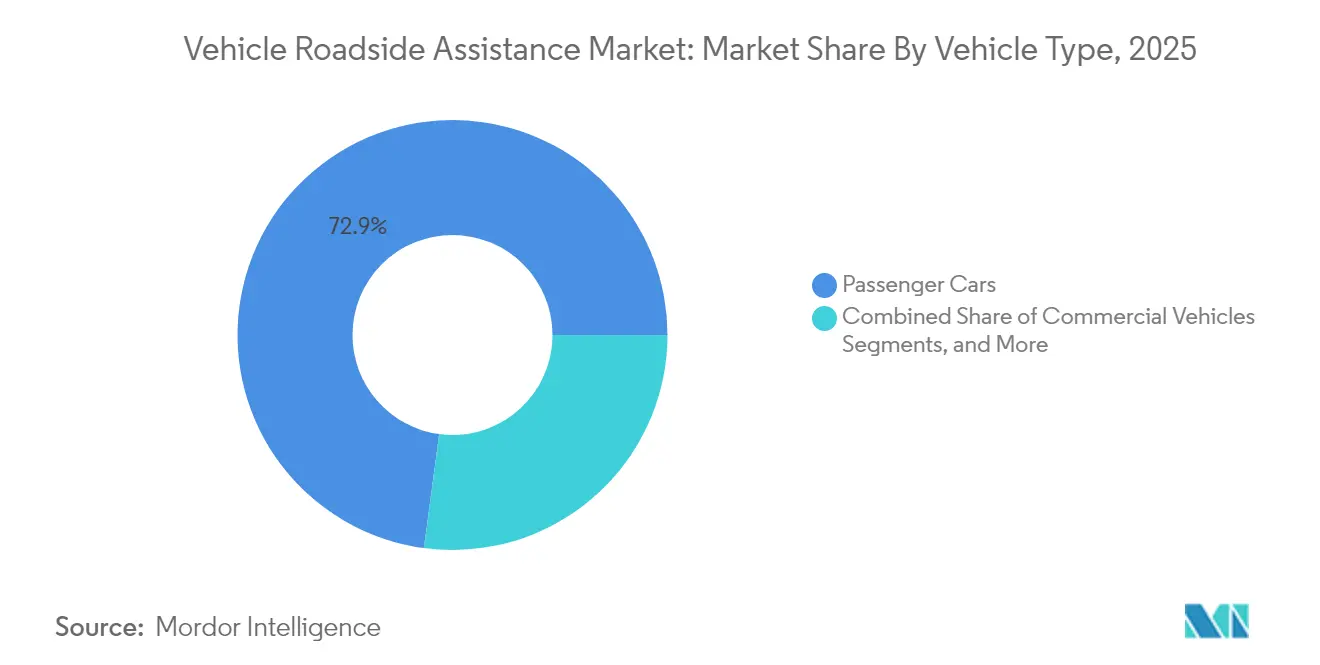

- By vehicle type, passenger cars accounted for 72.88% of the vehicle roadside assistance market size in 2025, and commercial vehicles are forecast to grow at a 7.28% CAGR through 2031.

- The vehicle roadside assistance market is moderately concentrated. AAA, Agero Inc., Allianz Partners, RAC Motoring Services, and AA plc form the top tier, leveraging broad networks, insurer relationships, and technology investments.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vehicle Roadside Assistance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global vehicle ownership | +1.0% | Global, with strongest impact in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Increasing vehicle-breakdown incidents | +0.7% | Global, particularly North America and Europe with aging fleets | Short term (≤ 2 years) |

| Integration of technology & telematics | +1.2% | North America & Europe leading, Asia-Pacific following | Long term (≥ 4 years) |

| Growth in electric vehicles (EVs) | +0.6% | Global, with China and Europe leading adoption | Long term (≥ 4 years) |

| Insurance & OEM partnerships | +0.3% | North America & Europe primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Vehicle Ownership

Vehicle registrations are rising sharply across emerging markets, bringing millions of first-time drivers who often rely on professional assistance for maintenance and roadside recovery. The International Energy Agency projects 17 million global EV sales in 2024, with China representing more than 45% of total car sales, Europe 25%, and the United States crossing 11% [1]Source: International Energy Agency, “Global EV Outlook 2025,” iea.org.. The combination of traditional internal-combustion vehicles and a growing electric fleet expands the roadside vehicle assistance market by boosting service diversity and complexity.

Increasing Vehicle-Breakdown Incidents

The average age of cars in the United States keeps rising, and integrated electronics create new failure points. Bosch addressed this need by buying Roadside Protect in February 2025, adding 12,000 towing partners to serve complex vehicles and ageing fleets [2]Source: Robert Bosch GmbH, “Bosch Acquires Roadside Protect,” bosch.com.. Incident frequency supports predictable revenue streams and justifies investment in specialized recovery equipment, which further enlarges the vehicle roadside assistance market.

Integration of Technology & Telematics

Connected-car diagnostics and predictive analytics allow providers to dispatch help faster and prevent some failures altogether. AAA rolled out AI-enabled member-support tools that sharpen communication and free agents for complex cases[3]Source: AAA, “AAA Implements AI Tools to Enhance Member Experience,” newsroom.aaa.com . Urgently, leveraging telematics data, achieved a 26% gross margin in Q1 2025 while retaining every enterprise contract signed since Q2 2024. These gains pull more customers into digital programs, sustaining growth for the vehicle roadside assistance market.

Growth in Electric Vehicles (EVs)

EV adoption changes the incident mix—from engine-related faults toward flat tires, battery-system alerts, and high-voltage safety needs. Recurrent Auto notes fewer than 4% of EV callouts involve complete battery depletion. AAA’s mobile-charging pilot and the Urgently-SparkCharge alliance show how specialized services command premium fees while strengthening brand loyalty.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High operational costs | -0.8% | Global, particularly impacting smaller providers | Short term (≤ 2 years) |

| Fragmented & unorganized sector in developing countries | -0.5% | Asia-Pacific, Latin America, Middle East & Africa | Medium term (2-4 years) |

| Dependency on vehicle-insurance policies | -0.3% | Global, with higher impact in mature insurance markets | Medium term (2-4 years) |

| Lack of consumer awareness | -0.2% | Emerging markets primarily, rural areas globally | Short term (≤ 2 years) |

| Data-privacy & cybersecurity risks | -0.2% | Global, particularly regions with strict data regulations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Operational Costs

Rising wages and investments in flatbed trucks, mobile chargers, and technician training squeeze smaller firms. Allstate exited a loss-making roadside contract in late 2024 after an 18.2% revenue drop, underscoring how price-sensitive partnerships can turn unviable under inflationary pressure. These realities hasten consolidation, fortifying economies of scale for the vehicle roadside assistance market’s largest operators.

Fragmented & Unorganized Sector in Developing Countries

In many emerging economies, informal recovery services prevail, resulting in uneven quality and delayed response times. International brands eye this gap as a gateway to expansion but must outlay capital for call-centre infrastructure, digital platforms, and training. When structure improves, however, it widens the vehicle roadside assistance market by unlocking latent demand for reliable services.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Towing Leads While Tire Services Accelerate

Towing owned 29.72% of the vehicle roadside assistance market share in 2025 and remains indispensable when vehicles cannot restart on-site. Tire replacement, projecting a 7.62% CAGR, gains traction as vehicle miles driven climb and consumers increasingly eschew DIY fixes. Fuel delivery slips where EV penetration rises, but battery jump-starts, lockouts, and winching remain stable volumes. Advanced on-site repairs, including sensor resets and software updates, continue to grow thanks to AI-backed diagnostic apps that limit unnecessary tows and enlarge the vehicle roadside assistance market.

Second-generation mobile-charging rigs now roll out in high-density EV corridors, earning premium fees and bolstering service differentiation. Providers that master both conventional and EV-specific tasks place themselves to capture recurring revenue and raise the vehicle roadside assistance market size within this segment.

By Provider Type: Insurance Dominance Challenged by Club Resurgence

Motor insurers held 32.21% of the vehicle roadside assistance market size in 2025, bundling coverage and roadside response to lift customer retention. Automotive clubs, rejuvenated by mobile apps, loyalty rewards, and travel perks, are expected to expand at 8.7% CAGR, narrowing the gap. App-based disruptors leverage transparent pricing and geo-tracking to win younger demographics, nudging incumbents to modernise.

OEM programs remain vital for EV owners because high-voltage systems require trained handlers. Meanwhile, Agero supports two-thirds of North American auto insurers, orchestrating more than 12 million annual events through integrated telematics. Hybrid delivery models that combine insurer, club, and digital capabilities are emerging, keeping the vehicle roadside assistance market fluid and competitive.

By Vehicle Type: Passenger Cars Lead While Commercial Vehicles Accelerate

Passenger cars produced 72.88% of 2025 service incidents worldwide, a testament to private-vehicle dominance and expansion in emerging regions. Commercial vehicles, forecast for a 7.28% CAGR, are fast catching up due to e-commerce, last-mile delivery, and fleet electrification. Downtime for delivery vans and trucks translates to revenue loss, motivating fleet managers to sign multi-year assistance contracts.

Light vans demand quick tire and battery fixes, while heavy trucks need specialised towing cranes and road-side diagnostics. Two-wheelers remain important in Asia’s dense cities, often serviced by mobile mechanics on small pickups. Provider investment in high-capacity tow rigs and EV-certified technicians broadens service scope, further enlarging the vehicle roadside assistance market.

By End User: Individual Consumers Dominate While Corporate Fleets Drive Growth

Individual motorists composed 48.35% of 2025 demand, valuing convenience and digital-first experiences. Corporate and fleet operators will expand by 6.65% CAGR, securing predictable volumes and higher per-ticket revenue. Municipal fleets, emergency services, and government bodies represent steady long-term clients owing to mission-critical uptime requirements. Providers now weave roadside data into fleet management dashboards, boosting preventive maintenance and tightening fuel economy. These tailored offerings lift switching costs and cement loyalty, strengthening overall vehicle roadside assistance market growth.

Geography Analysis

North America led with 39.12% of global share in 2025, fuelled by large car fleets, well-maintained highways, and legacy clubs such as AAA that serve 61 million members. Bosch’s acquisition of Roadside Protect and Allianz’s AUD 642 million agreement with the Royal Automobile Association illustrate how consolidation deepens national coverage and amplifies cross-selling.

Europe sits second, shaped by strict environmental rules, a dense motorway network, and surging EV registrations. The European Road Services Alliance unites RAC, Europ Assistance, Falck, and VHD to provide pan-continental help, standardising quality and accelerating mobile-charging deployment. Insurance partners such as Allianz and OEMs like Volvo refine integrated packages that offer warranty, insurance, and roadside service in one app.

Asia-Pacific records the fastest regional CAGR at 5.86%, propelled by a swelling middle class and aggressive EV subsidies in China. Diversified income levels leave room for basic rescue options in rural districts and premium digital services in metropolitan areas. Market fragmentation invites global entrants to forge joint ventures and upgrade technician training, steps that will keep lifting the vehicle roadside assistance market in the region.

Competitive Landscape

The vehicle roadside assistance market is moderately concentrated. AAA, Agero Inc., Allianz Partners, RAC Motoring Services, and AA plc form the top tier, leveraging broad networks, insurer relationships, and technology investments. AAA alone generates USD 3.9 billion in annual revenue and continues transitioning members to mobile-first channels.

Digital innovators accelerate competitive churn. Urgently connects 13,700 service partners across North America and maintains perfect enterprise-contract retention since mid-2024, showcasing tech-driven stickiness. Scale provides bargaining power for new flatbed trucks, EV chargers, and bulk insurance deals, further widening the gap with local operators.

Region-specific specialists still thrive where intimate road knowledge or regulatory barriers favour incumbents. Yet high capital needs for EV tooling, together with data-privacy mandates, raise entry hurdles each year. As larger companies continue to absorb local outfits, the vehicle roadside assistance market moves toward higher efficiency and broader geographic reach.

Vehicle Roadside Assistance Industry Leaders

AAA (American Automobile Association

Agero Inc.

Allianz Partners

RAC Motoring Services

AA plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: IAG completed its strategic alliance with the Royal Automobile Club of Western Australia, acquiring RAC Insurance for USD 400 million and signing a 20-year distribution agreement valued at USD 950 million.

- March 2025: Allianz and Volvo Car UK extended their roadside assistance collaboration for Volvo customers across the United Kingdom.

- February 2025: Bosch acquired Roadside Protect, adding 12,000 towing partners and strengthening its digital roadside platform in North America.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global vehicle roadside assistance market as all on-road emergency services, towing, battery jump or replacement, flat-tire help, fuel delivery, lockout access, minor mechanical fixes, winching, and, increasingly, mobile EV charging, delivered by insurers, OEM programs, automotive clubs, digital platforms, warranty administrators, or independent fleets to passenger and commercial vehicles anywhere beyond a workshop setting.

Scope Exclusion: Workshop-only repair or maintenance packages that never dispatch help to the breakdown location are kept outside our sizing.

Segmentation Overview

- By Service Type

- Towing Services

- Tire Replacement

- Battery Jump/Replacement

- Lockout Service

- Fuel Delivery

- Winch/Extrication

- Minor On-site Repair

- By Provider Type

- Motor Insurance Companies

- Automotive OEMs

- Automotive Clubs

- Independent Warranty Providers

- App-based Digital Platforms

- Fleet & Leasing Companies

- By Vehicle Type

- Passenger Cars

- Commercial Vehicles

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Two-Wheelers (Motorcycles)

- By End User

- Individual Consumers

- Corporate & Fleet Operators

- Government & Municipal Agencies

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Middle East And Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with assistance-dispatch managers, insurer product heads, club executives, and fleet supervisors across North America, Europe, Asia-Pacific, and selected Middle-East markets helped us verify typical call-out rates, average service prices, and emerging EV-specific requirements. Follow-up surveys with technicians and app-based aggregators refined assumptions on response-time commitments and regional cost differentials.

Desk Research

We began with up-to-date accident, vehicle-in-use, and new-registration datasets from bodies such as OICA, Eurostat, the National Highway Traffic Safety Administration, and Transport Canada, which let our team benchmark incident frequencies across 60+ countries. Complementary signals, EV parc counts, average vehicle age, fuel-price trends, and motor-insurance penetration were mined from energy agencies, finance ministries, and leading auto clubs. Subscription databases that Mordor analysts access, including D&B Hoovers for company revenues and Dow Jones Factiva for deal flow, provided additional context on provider networks and service pricing. The sources mentioned illustrate the breadth of publications consulted; many more public and paid references were reviewed during data collection and validation.

Market-Sizing & Forecasting

Mordor Intelligence first applies a top-down model that scales each country's registered vehicle base by empirically derived breakdown incidence and assistance subscription ratios, adjusted for vehicle age mix and climatic severity. Results are cross-checked through selective bottom-up roll-ups of provider revenues and sampled average service price × call volume calculations, so totals align with on-ground billing realities. Key inputs include EV share, median vehicle age, urban distance traveled, insurance policy bundling rates, technician labor costs, and app-based dispatch adoption. Forecasts to 2030 rely on multivariate regression that relates call-out demand to projected vehicle stock, EV adoption curves, macroeconomic growth, and historical seasonality; coefficients are stress tested with scenario analysis shared by primary experts to capture shifts in mobility and regulation.

Data Validation & Update Cycle

Before release, our analysts reconcile model outputs against independent financial filings, traffic incident statistics, and shipment data. Any variance beyond preset thresholds triggers a re-run and fresh expert check. The report is refreshed every twelve months, with interim updates whenever material events, major regulatory changes or landmark acquisitions, alter baseline assumptions.

Why Mordor's Vehicle Roadside Assistance Baseline Stands Reliable

Published market values frequently diverge because firms choose different service baskets, pricing bases, and refresh cadences. We acknowledge these gaps upfront. Most variation stems from whether motor club memberships are counted, how free warranty assistance is priced, and the speed at which EV-specific services are layered into totals. Mordor's scope captures only monetized, on-road interventions and employs yearly vehicle parc updates, whereas some peers extrapolate from older accident data or report booked revenue in local currencies without consistent FX treatment.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 31.32 B (2025) | Mordor Intelligence | - |

| USD 27.73 B (2025) | Global Consultancy A | Excludes complimentary OEM programs and applies constant 2023 exchange rates |

| USD 26.58 B (2024) | Industry Journal B | Uses partial regional scope and assumes flat assistance subscription penetration |

Differences aside, the comparison shows that Mordor's disciplined inclusion of all paid, on-road interventions and its annual refresh cycle give decision makers a dependable, transparent baseline anchored to clearly traceable variables.

Key Questions Answered in the Report

How big is the vehicle roadside assistance market in 2026?

The vehicle roadside assistance market size reached USD 32.8 billion in 2026 and is projected to rise to USD 41.33 billion by 2031.

Which region leads the vehicle roadside assistance market today?

North America accounts for the largest regional position, capturing 39.12% of vehicle roadside assistance market share in 2025 due to high car ownership and a mature service network.

What service generates the highest revenue?

Towing services contributed 29.72% of worldwide revenue in 2025 and remain indispensable across all vehicle segments.

How is electrification changing roadside assistance?

EV growth is spurring demand for specialised offerings such as mobile charging and flatbed towing, with EV-related services forecast to expand at an 10.83% CAGR through 2031.

Who are the key players in the vehicle roadside assistance market?

Major providers include AAA, Agero Inc., Allianz Partners, RAC Motoring Services, and AA plc, each leveraging scale, technology, and strategic partnerships to maintain competitive advantage.

Why is consolidation accelerating in this market?

High capital requirements for EV-ready equipment and digital platforms push smaller firms toward partnerships or acquisitions, allowing larger players to build scalable, multi-channel service ecosystems.

Page last updated on: