Edutainment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.87 Billion |

| Market Size (2031) | USD 9.12 Billion |

| Growth Rate (2026 - 2031) | 9.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

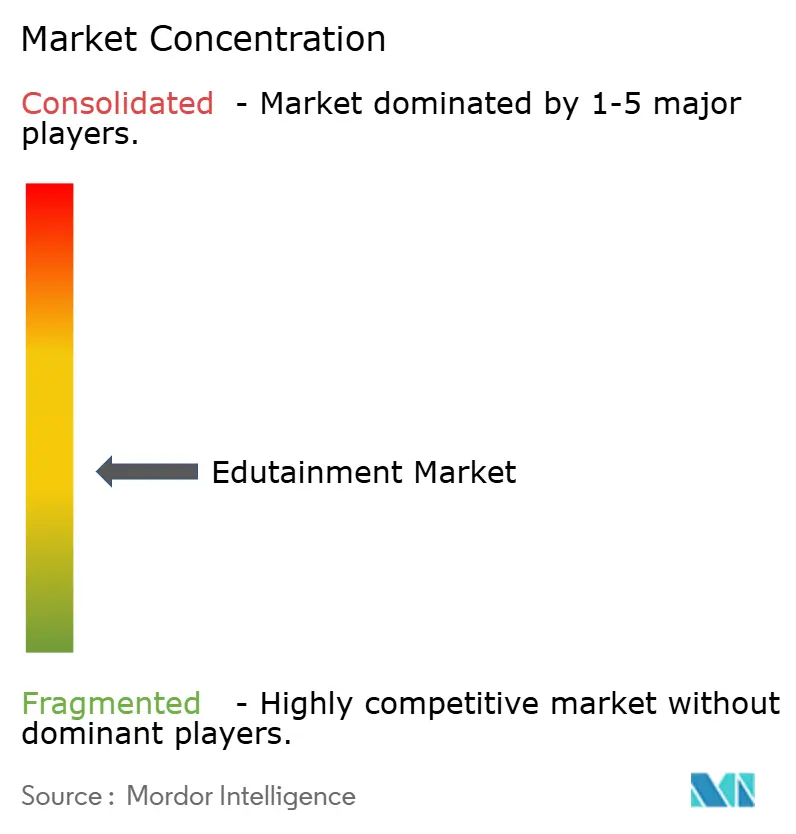

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Edutainment Market Analysis by Mordor Intelligence

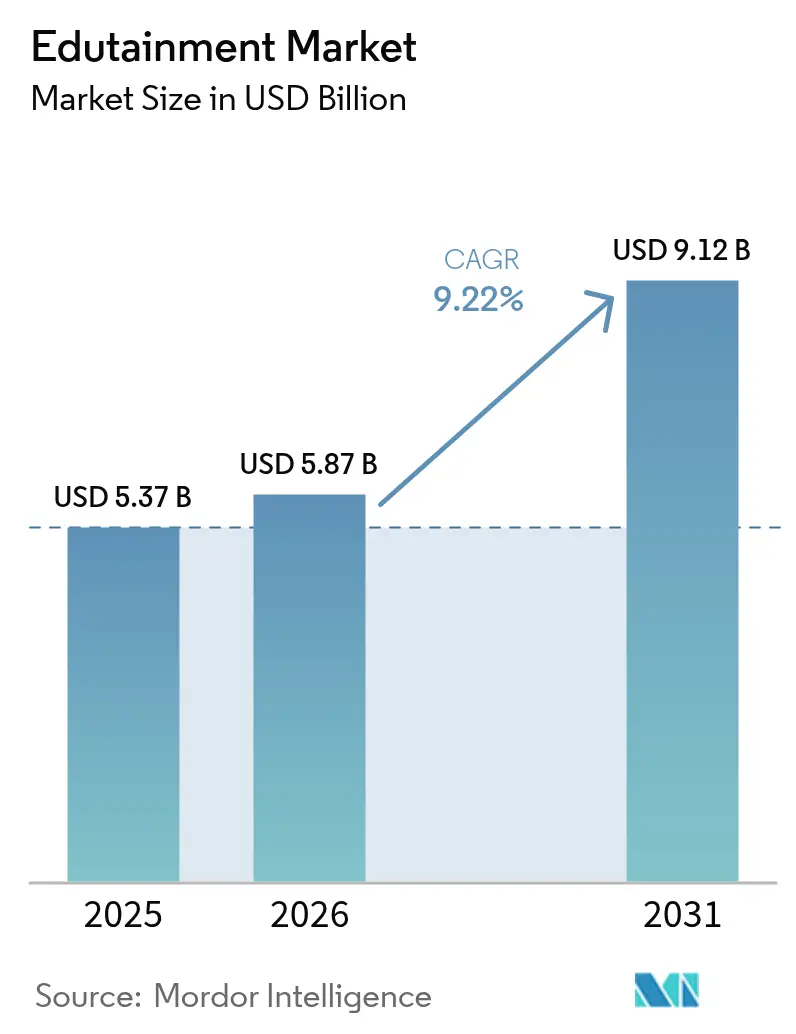

The edutainment market size was valued at USD 5.37 billion in 2025 and estimated to grow from USD 5.87 billion in 2026 to reach USD 9.12 billion by 2031, at a CAGR of 9.22% during the forecast period (2026-2031). This measured growth reflects a maturing landscape in which established platforms consolidate user bases while emerging technologies such as 5G and augmented reality transform content delivery. Interactive products continue to attract the largest daily active user pools, yet hybrid formats that meld game mechanics with structured instruction are scaling rapidly. Mobile apps dominate distribution thanks to global 5G roll-outs that enable real-time, multiplayer learning sessions, while corporate purchasers expand spending on immersive soft-skill up-skilling modules. The edutainment market is also shaped by intensifying regulatory scrutiny over children’s data privacy, favoring companies that can balance engagement with compliance. Meanwhile, falling content-production costs from generative-AI authoring tools widen entry paths for niche providers and regional specialists.

Key Report Takeaways

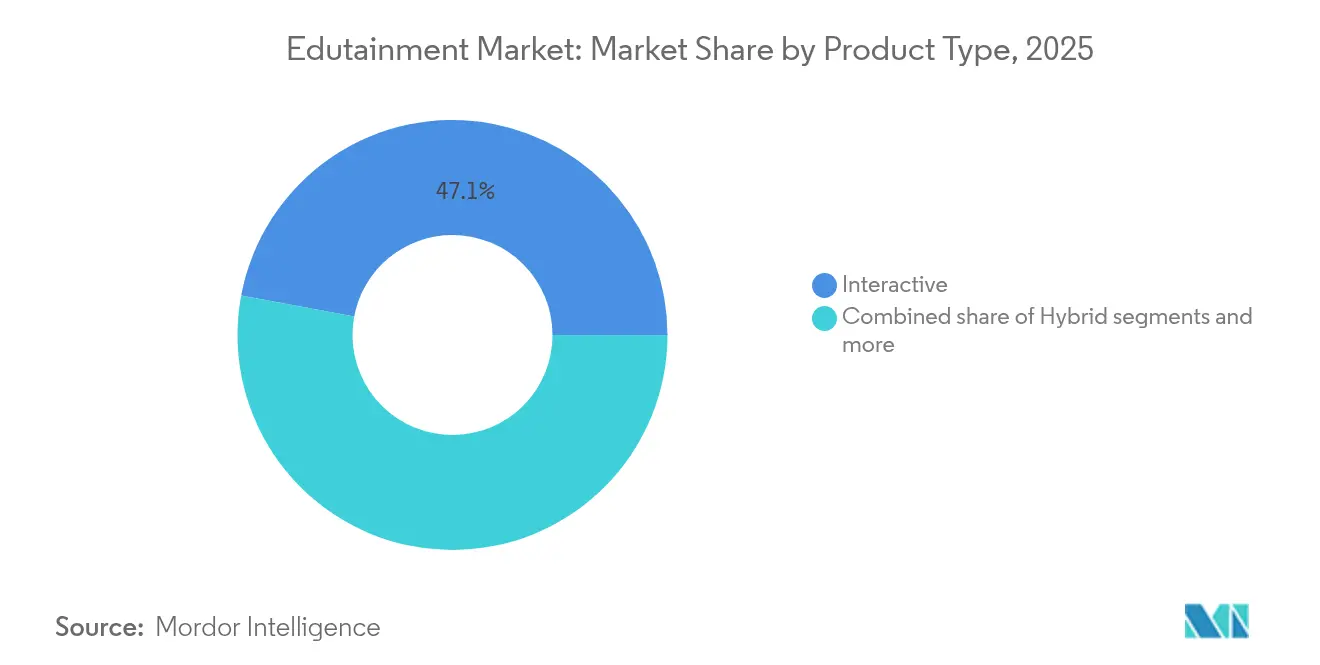

- By product type, interactive offerings accounted for 47.05% of the edutainment market share in 2025; hybrid products are forecast to post the fastest 18.11% CAGR through 2031.

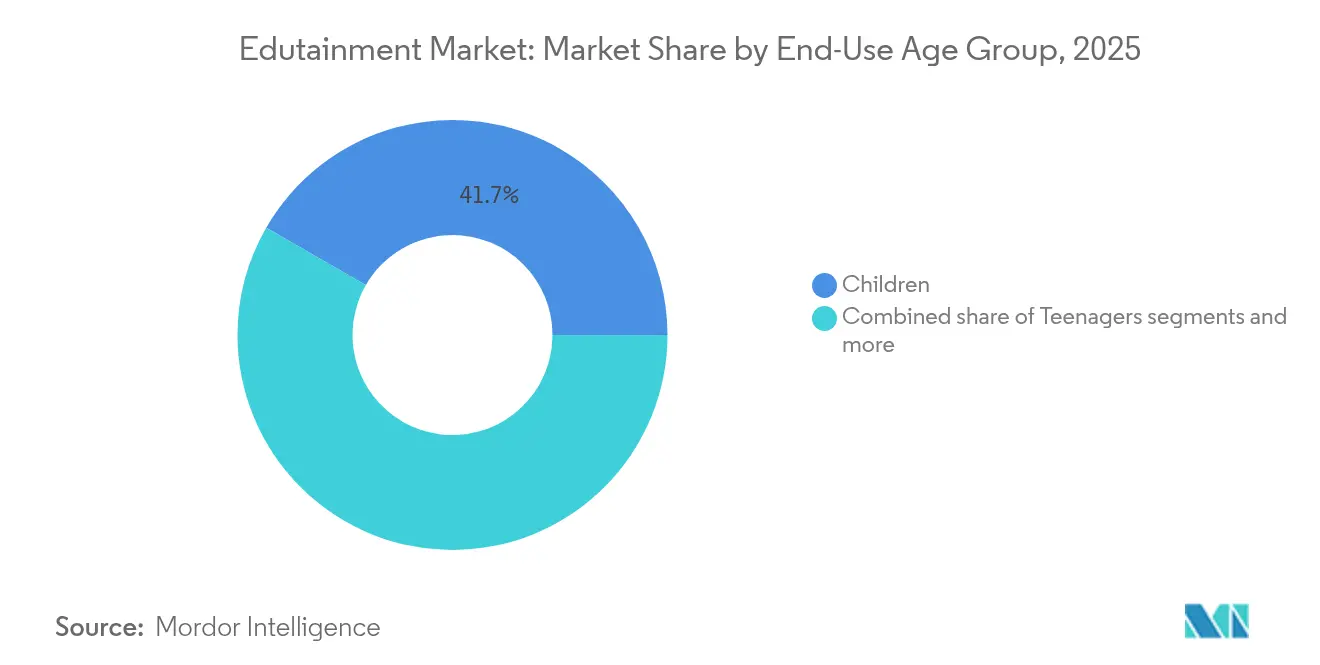

- By end-use age group, children held a 41.68% share of the edutainment market size in 2025, while young adults are projected to expand at a 13.81% CAGR to 2031.

- By platform, mobile apps led with 57.62% of the edutainment market share in 2025; AR/VR is the fastest-growing platform at a 25.39% CAGR through 2031.

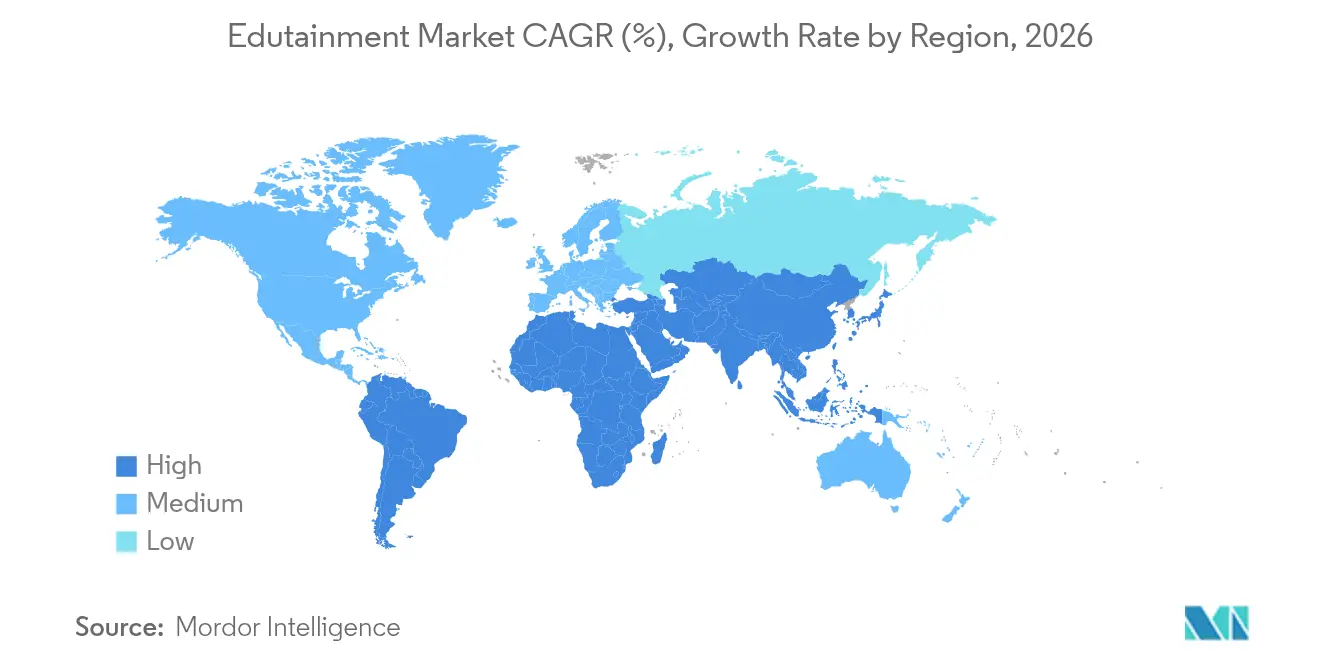

- By geography, North America commanded 33.10% of the edutainment market share in 2025; Asia-Pacific is advancing at a 10.21% CAGR, the highest regional growth rate.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Edutainment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G-enabled mobile micro-learning boom | +0.9% | Global, with APAC leading | Medium term (2-4 years) |

| Rapid adoption of gamified language-learning apps | +0.7% | Global, strongest in North America & Europe | Short term (≤ 2 years) |

| Government STEM mandates in K-12 curricula | +0.6% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Corporate up-skilling budgets for immersive soft-skills | +0.4% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Edutainment IP extensions by global entertainment studios | +0.3% | Global, concentrated in content hubs | Short term (≤ 2 years) |

| Generative-AI tools slashing content-production costs | +0.6% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G-Enabled Mobile Micro-Learning Boom

Ultra-low latency networks transform educational content delivery by enabling real-time collaborative experiences that previously required desktop computing power. 5G infrastructure deployment reached 85% population coverage across major metropolitan areas in 2024, reducing content buffering delays that historically disrupted immersive learning sessions [1]IEEE, “5G-Enabled Mobile Learning: Infrastructure and Applications,” ieee.org. . The technology's impact extends beyond faster downloads to support augmented reality applications that overlay contextual information onto physical environments, creating location-based learning opportunities in museums, retail spaces, and outdoor settings. Corporate training programs increasingly leverage 5G-enabled mobile devices for just-in-time skill development, allowing employees to access procedural guidance during actual work tasks rather than separate training sessions. This shift toward ambient learning integration represents a fundamental departure from scheduled educational activities toward continuous capability enhancement embedded within daily workflows.

Rapid Adoption of Gamified Language-Learning Apps

Behavioral psychology research demonstrates that variable reward schedules in gamified applications generate higher user retention rates than traditional educational software, with daily active usage increasing 40-60% when competitive elements and social features are integrated. Duolingo's streak mechanics and league competitions drove 51% growth in daily active users during 2024, demonstrating how game design principles sustain long-term engagement beyond initial novelty periods [2]Securities and Exchange Commission, “Duolingo, Inc. Form 10-K 2023,” sec.gov. . The success of language learning applications creates template opportunities for other subject areas, as mathematics and science educators adopt similar progression systems, achievement badges, and peer comparison features. Revenue models benefit from this engagement pattern, as sustained daily usage increases conversion rates from free to premium subscriptions while generating advertising inventory for supplementary monetization streams.

Government STEM Mandates in K-12 Curricula

National education policies increasingly mandate coding and robotics instruction as core curriculum requirements, creating institutional demand that transcends individual teacher preferences or school district budget constraints. India's National Education Policy 2020 allocated USD 1.2 billion toward digital infrastructure and STEM program development, while China's "Double Reduction" policy redirected after-school tutoring expenditures toward government-approved educational technology platforms[3]Ministry of Education, India, “National Education Policy 2020,” education.gov.in. . These policy frameworks establish minimum technology adoption thresholds that guarantee baseline market demand regardless of economic fluctuations or competitive dynamics. The regulatory approach differs significantly from voluntary adoption patterns, as schools must demonstrate compliance through standardized assessments that measure students' computational thinking and digital literacy skills.

Corporate Up-Skilling Budgets for Immersive Soft-Skills

Enterprise learning expenditures shifted toward virtual reality training modules as remote work arrangements highlighted deficiencies in traditional presentation-based professional development programs. Walmart's deployment of VR training across 4,700 stores for customer service and leadership scenarios demonstrated measurable improvements in employee confidence and performance metrics compared to classroom-based alternatives. The technology's ability to simulate high-stakes interpersonal interactions—such as difficult customer conversations or performance management discussions—provides practice opportunities that role-playing exercises cannot replicate authentically. Corporate training budgets increasingly favor immersive solutions that generate quantifiable skill improvements over traditional workshops that rely primarily on knowledge transfer without behavioral reinforcement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented curriculum standards slowing procurement | –0.4% | Global, most acute in federal systems | Long term (≥ 4 years) |

| Screen-time health concerns prompting regulatory scrutiny | –0.3% | North America & EU, expanding globally | Medium term (2-4 years) |

| High upfront AR/VR hardware costs in emerging markets | –0.6% | MEA & South America, selective APAC | Medium term (2-4 years) |

| Teacher training gaps for interactive pedagogy | –0.4% | Global, severe in resource-constrained regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Curriculum Standards Slowing Procurement

Educational content must align with diverse state, provincial, and national curriculum frameworks, creating development costs that scale exponentially with geographic market expansion. The United States maintains 50 different state education standards alongside Common Core adoption variations, while European Union countries implement 27 distinct national curricula that resist harmonization efforts[4]UNESCO, “Global Education Monitoring Report 2024,” unesco.org. . Content localization requirements extend beyond language translation to encompass cultural references, historical perspectives, and pedagogical approaches that reflect regional educational philosophies. This fragmentation prevents economies of scale in content production and forces companies to choose between broad market coverage with generic materials or deep market penetration with customized offerings that limit scalability potential.

High Upfront AR/VR Hardware Costs in Emerging Markets

Virtual reality headset prices remain prohibitive for institutional adoption in price-sensitive markets, despite gradual cost reductions from USD 800-1,200 to USD 300-500 for entry-level devices during 2024. Educational institutions in emerging economies typically allocate USD 50-100 per student annually for technology purchases, making VR deployment feasible only through government subsidies or international development funding programs. The hardware requirement creates a binary adoption pattern where schools either commit to comprehensive VR integration or avoid the technology entirely, limiting market penetration to well-funded districts and private institutions. Apple's Vision Pro pricing at USD 3,500 further stratifies the market, positioning advanced mixed-reality capabilities exclusively within premium educational segments that can justify the investment through differentiated learning outcomes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Interactive Strength Meets Hybrid Momentum

Interactive products maintain a 47.05% market share in 2025, reflecting sustained demand for gamified learning experiences that combine entertainment mechanics with educational objectives. Hybrid solutions demonstrate the fastest growth at 18.11% CAGR through 2031, as content creators blend interactive elements with traditional instructional videos and assessment tools to maximize engagement across diverse learning preferences. The hybrid approach addresses institutional concerns about screen time limitations while preserving the motivational benefits of game-based learning through carefully balanced content portfolios. Non-interactive products retain relevance in formal educational settings where curriculum compliance requires structured presentation of information, though their static nature limits user engagement compared to dynamic alternatives.

Explorative products represent emerging opportunities as virtual field trips and simulation-based learning gain acceptance among educators seeking authentic experiential learning without logistical constraints. The COVID-19 pandemic accelerated the adoption of virtual laboratory experiences and historical site tours, creating precedents for immersive educational content that transcends physical limitations. Generative AI tools increasingly support hybrid product development by automating content adaptation across different interaction modes, reducing production costs while maintaining pedagogical effectiveness across varied learning contexts.

By End-Use Age Group: Adult Learning Acceleration

Children command 41.68% market share in 2025, benefiting from parental willingness to invest in educational technology and institutional adoption through schools and childcare facilities. Young adults exhibit the fastest growth at 13.81% CAGR, driven by corporate training initiatives and professional development programs that leverage gamified learning for skill acquisition. This demographic shift reflects changing workforce development needs as automation displaces routine tasks while creating demand for creative problem-solving and interpersonal skills that traditional training methods struggle to develop effectively.

Teenagers represent a challenging segment due to competing entertainment options and academic pressure that limits discretionary learning time, though language learning applications successfully capture this audience through social features and peer competition mechanics. Adults increasingly engage with edutainment content for personal enrichment and career advancement, particularly in technology-related subjects where rapid industry evolution requires continuous skill updates. The convergence of professional development and entertainment creates opportunities for content that serves both career advancement and leisure interests simultaneously.

By Platform: Mobile Apps Lead Despite AR/VR Surge

Mobile apps dominate with 57.62% market share in 2025, capitalizing on smartphone ubiquity and the convenience of learning during commute times, breaks, and other transitional moments throughout daily routines. AR/VR platforms demonstrate exceptional growth at 25.39% CAGR, though from a smaller base that limits near-term market impact despite technological advancement. Web-based platforms maintain steady adoption among institutional users who require multi-device access and administrative oversight capabilities that mobile applications often lack due to interface constraints.

PC/Console platforms serve specialized applications requiring high-performance computing, particularly in STEM subjects involving complex simulations or 3D modeling exercises. TV/Streaming integration represents an emerging distribution channel as smart television adoption increases and content creators develop lean-back educational experiences suitable for family viewing contexts. The platform diversity reflects varying use cases rather than competitive displacement, as successful edutainment companies increasingly adopt multi-platform strategies that optimize content delivery for specific learning scenarios and user preferences.

Geography Analysis

North America maintains 33.10% market share in 2025, supported by established educational technology infrastructure and corporate training budgets that prioritize employee development investments. Asia-Pacific demonstrates the fastest regional growth at 10.21% CAGR, driven by government digitization initiatives, expanding middle-class populations, and mobile-first technology adoption patterns that bypass traditional computing infrastructure. European markets emphasize data privacy compliance and pedagogical research validation, creating higher barriers to entry but also premium pricing opportunities for solutions that meet stringent regulatory requirements.

Middle East and Africa represent emerging opportunities as internet connectivity improves and government education investments increase, though economic volatility and infrastructure limitations constrain near-term growth potential. South America benefits from Spanish and Portuguese language content localization efforts by global platforms, while regional content creators develop culturally relevant educational materials that address local curriculum requirements and learning preferences. The geographic distribution reflects varying stages of digital transformation rather than inherent market size limitations, suggesting convergence potential as infrastructure development progresses across emerging economies.

Competitive Landscape

The edutainment market is highly fragmented, with the top five players accounting for a relatively small share of the overall landscape. This opens up significant opportunities for regional platforms and specialized content creators to capture niche segments that global firms often find cost-prohibitive to address. The fragmentation is driven by a range of factors, including varied curriculum standards, the need for language localization, and culturally specific content preferences. These elements limit the scalability of standardized solutions and prevent universal adoption across geographies. Duolingo, holding a leading position among focused platforms, has shown how a freemium model and viral growth strategies can build substantial market presence. Meanwhile, tech giants like Microsoft and Google tend to integrate educational tools within their broader ecosystems, using them as value-adds rather than standalone revenue drivers.

Differentiation in this space is increasingly defined by a company’s ability to personalize content and deliver multi-modal learning experiences. Firms are investing in artificial intelligence to monitor user behavior and adapt learning paths based on individual performance and preferences. These adaptive systems improve user engagement, increasing retention and encouraging users to upgrade to premium tiers. In 2024 alone, patent filings for adaptive learning algorithms rose by 34%, signaling an intense race to secure competitive edges in personalization. Platforms that master this dynamic not only deliver better learning outcomes but also benefit from network effects and valuable data feedback loops. As a result, personalization is becoming a central pillar for long-term success in edutainment.

Despite growing competition, there are still substantial white-space opportunities in the sector. Areas like specialized professional training, culturally tailored content for emerging markets, and location-based educational experiences remain underdeveloped. These segments often require deep domain knowledge or cultural fluency, which global players may lack. Regional startups and niche content developers are well-positioned to address these gaps with greater authenticity and relevance. As market dynamics evolve, success will hinge on the ability to pair localized content with scalable, tech-enabled delivery models. This shift marks a turning point from broad, one-size-fits-all platforms to agile, user-centric edutainment solutions.

Edutainment Industry Leaders

Duolingo

BYJU’S

Kahoot!

Roblox Corp. (Education

LEGO Education

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Duolingo launched an AI-powered conversation practice feature using GPT-4 integration, enabling personalized dialogue scenarios that adapt to user proficiency levels and learning objectives. The feature represents a significant technological advancement in language learning applications, potentially disrupting traditional tutoring services through scalable conversational practice opportunities.

- August 2024: Microsoft announced USD 50 million investment in Minecraft Education expansion, adding chemistry and physics simulation capabilities that enable students to conduct virtual experiments within the game environment.

- July 2024: Roblox Corporation established partnerships with 15 major school districts to provide free access to Roblox Studio for computer science curricula, reaching over 500,000 students across the United States. The initiative positions Roblox as a legitimate educational platform while building long-term user relationships that may convert to entertainment usage.

- June 2024: BYJU'S completed restructuring agreement with creditors, securing USD 200 million in working capital to continue operations and international expansion plans. The financial stabilization enables the company to maintain its position in the Indian market while pursuing growth opportunities in Southeast Asia and the Middle East.

Global Edutainment Market Report Scope

A complete background analysis of the Global Edutainment Market, which includes an assessment of the national accounts, economy, and emerging market trends by segments, significant changes in the market dynamics, and market overview is covered in the report.

| Interactive |

| Non-Interactive |

| Hybrid |

| Explorative |

| Children |

| Teenagers |

| Young Adults |

| Adults |

| Mobile Apps |

| PC / Console |

| Web-based |

| AR / VR |

| TV / Streaming |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | Belgium | |

| Netherlands | ||

| Luxembourg | ||

| NORDICS | Denmark | |

| Finland | ||

| Iceland | ||

| Norway | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia | Singapore | |

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

| By Product Type | Interactive | ||

| Non-Interactive | |||

| Hybrid | |||

| Explorative | |||

| By End-Use Age Group | Children | ||

| Teenagers | |||

| Young Adults | |||

| Adults | |||

| By Platform | Mobile Apps | ||

| PC / Console | |||

| Web-based | |||

| AR / VR | |||

| TV / Streaming | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Peru | |||

| Chile | |||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| BENELUX | Belgium | ||

| Netherlands | |||

| Luxembourg | |||

| NORDICS | Denmark | ||

| Finland | |||

| Iceland | |||

| Norway | |||

| Sweden | |||

| Rest of Europe | |||

| Asia-Pacific | India | ||

| China | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| South East Asia | Singapore | ||

| Malaysia | |||

| Thailand | |||

| Indonesia | |||

| Vietnam | |||

| Philippines | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | United Arab Emirates | ||

| Saudi Arabia | |||

| South Africa | |||

| Nigeria | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

How big is the edutainment market in 2026?

The edutainment market size is USD 5.87 billion in 2026, with projections pointing to USD 9.12 billion by 2031.

Which product format leads sales?

Interactive titles command 47.05% of 2025 revenue, reflecting strong user engagement driven by game mechanics.

Which region is growing the fastest?

Asia-Pacific leads with a 10.21% CAGR, propelled by government STEM mandates and mobile-first adoption.

What technology trend is reshaping content delivery?

5G networks enable real-time, mobile micro-learning experiences, boosting engagement and opening location-based AR use cases.

Why is hybrid content gaining ground?

Hybrid formats blend gamification with structured lessons, meeting institutional compliance needs while sustaining learner motivation.

Page last updated on: