Photo Printing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 27.76 Billion |

| Market Size (2031) | USD 34.34 Billion |

| Growth Rate (2026 - 2031) | 4.33% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Photo Printing Market Analysis by Mordor Intelligence

The Photo Printing Market size was valued at USD 26.61 billion in 2025 and estimated to grow from USD 27.76 billion in 2026 to reach USD 34.34 billion by 2031, at a CAGR of 4.33% during the forecast period (2026-2031).

Growth rests on three pillars: the relentless rise of smartphone image capture, ongoing consumer appetite for tangible keepsakes, and steady improvements in print quality that persuade buyers to trade up to premium formats. Operators are capitalizing on mobile-first ordering journeys, AI-assisted image curation, and subscription services that turn digital clutter into regular revenue. Consolidation is reshaping the competitive map as scale and workflow automation become decisive cost levers; yet specialist brands still carve out space through superior materials and boutique service. Regionally, North America retains revenue leadership, while Asia-Pacific supplies the fastest incremental demand to rising disposable incomes and deep smartphone penetration.

Key Report Takeaways

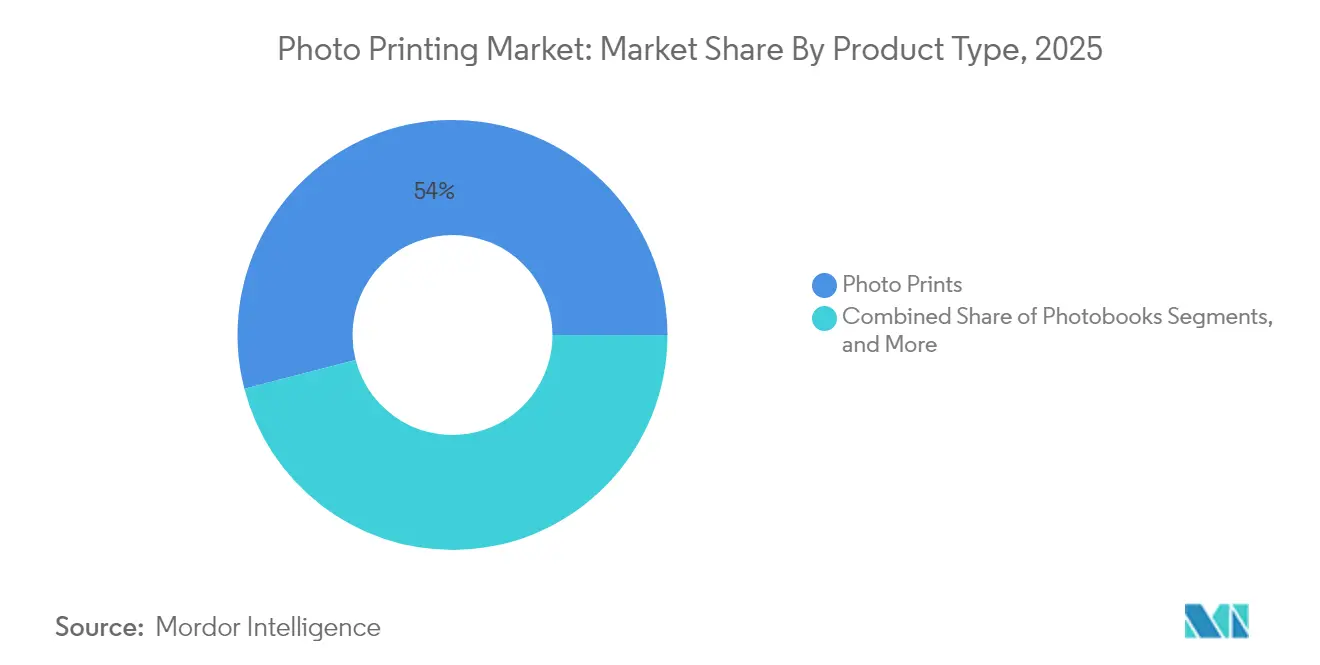

- By product type, wall décor led premium expansion with 10.74% CAGR, whereas photo prints controlled 54.02% of the photo printing market share in 2025.

- By print technology, inkjet secured 46.20% of the photo printing market size in 2025; dye-sublimation is projected to grow the fastest at 9.05% CAGR to 2031.

- By distribution channel, online platforms captured 61.05% of revenue in 2025 and are advancing at 8.04% CAGR.

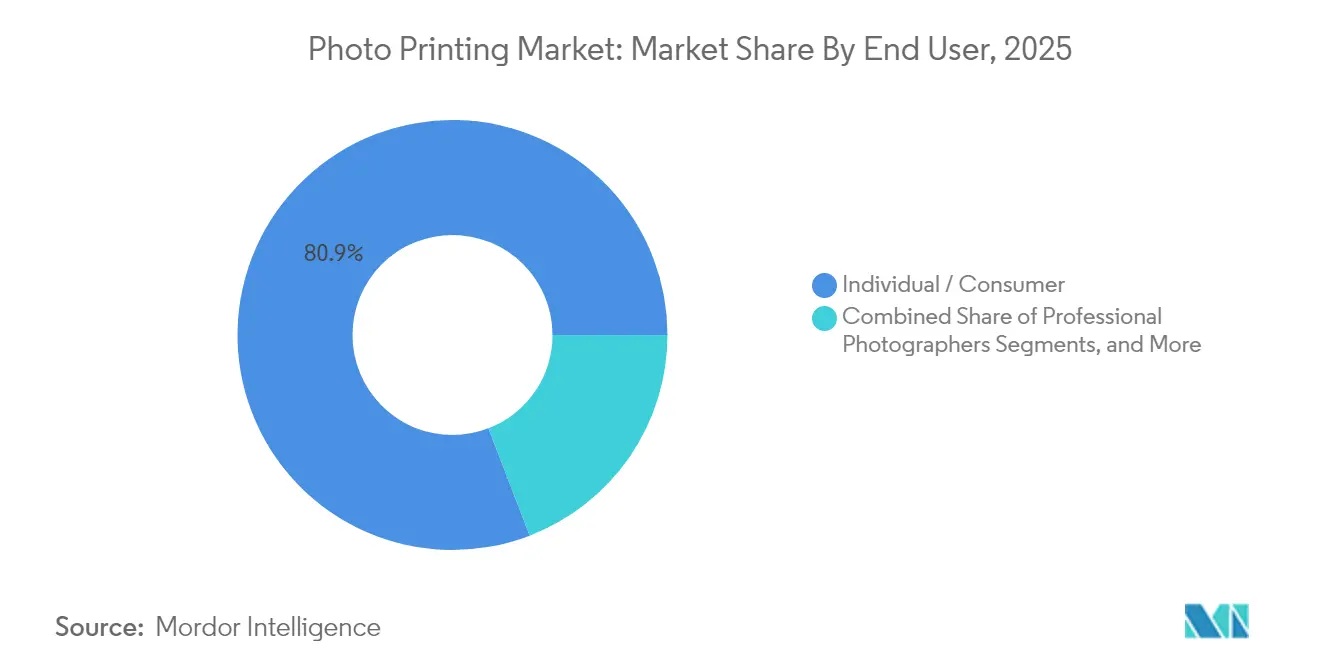

- By end user, individual/consumer orders contributed 80.85% of the photo printing market size in 2025 and are set to expand at 7.28% CAGR.

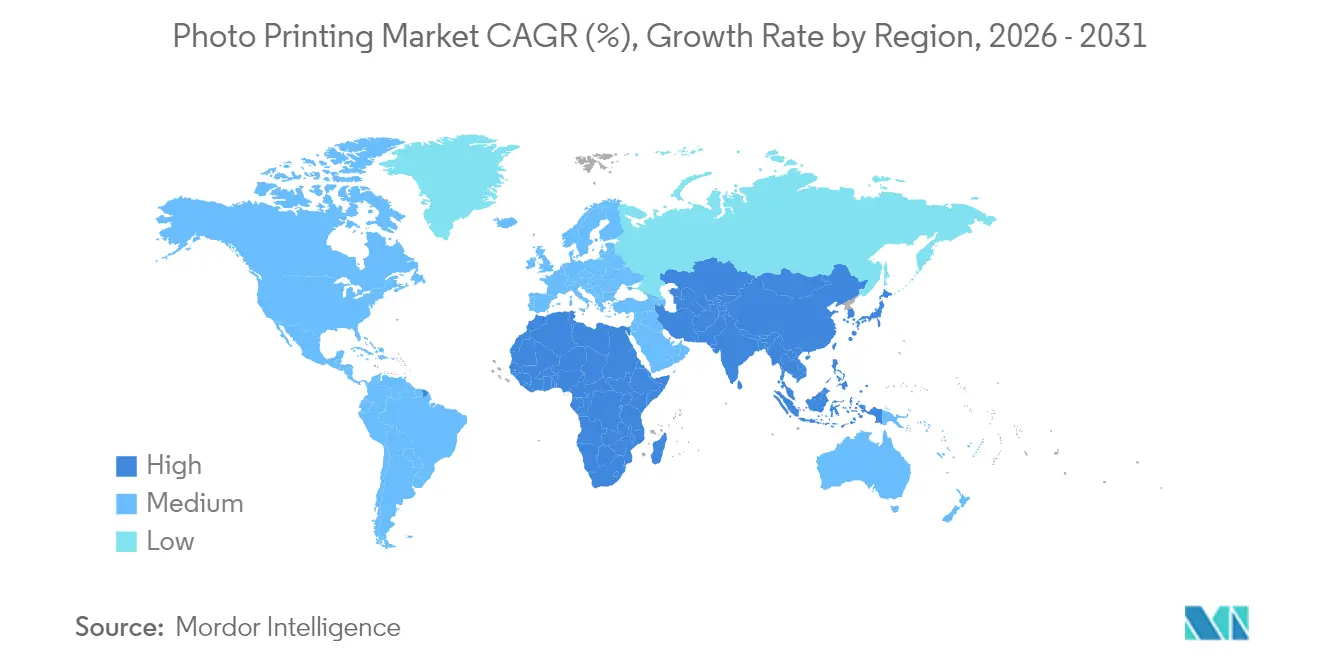

- By geography, North America held 31.95% revenue share in 2025, while Asia-Pacific is set to post the highest 6.94% CAGR to 2031.

- Leading players like Shutterfly, CEWE, Fujifilm, Snapfish, and Canon hold substantial market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Photo Printing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smartphone-led photo explosion | +1.8% | Global, with stronger impact in APAC and emerging markets | Medium term (2-4 years) |

| Demand for photobooks and photo gifts | +1.2% | North America and EU core, expanding to APAC | Long term (≥ 4 years) |

| E-commerce and app-based ordering | +1.0% | Global, led by developed markets | Short term (≤ 2 years) |

| AI-generated image curation boosts print volumes | +0.8% | North America and EU early adoption, APAC following | Medium term (2-4 years) |

| Subscription "memory-box" print services | +0.6% | North America and EU primarily | Long term (≥ 4 years) |

| Blockchain-verified limited-edition prints | +0.4% | Global luxury markets, concentrated in major cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth of Photo Printing Market in North America

The North American photo printing market has experienced consistent growth in recent years. The surge in mobile photography and the widespread sharing of images on social media are driving consumers to transform their digital snapshots into physical prints. This trend, along with the rising popularity of home and small office photo printers, as well as the increased use of photo kiosks and online printing services, is fueling the market's growth.

The United States dominates the region's photo printing landscape, accounting for over 80% of the revenue. Meanwhile, Canada, with its tech-savvy populace, is the second-largest market, witnessing a rising appetite for personalized photo merchandise. The industry is witnessing a surge in e-commerce and m-commerce platforms tailored for photo printing services. Moreover, there is a notable uptick in adopting large-format, high-quality photo printing for home decor and professional applications. Additionally, the sector is witnessing a trend toward integrating AI and machine learning to elevate photo editing and personalization capabilities.

Smartphone-led photo explosion

Smartphones now dominate everyday imaging, creating a reservoir of high-resolution content that consumers increasingly want in physical form. Post-pandemic surveys in Japan show nearly 40% of teenagers and more than 30% of adults in their twenties and thirties feeling a stronger urge to photograph outings and social occasions, reinforcing demand for prints[1]Source: Camera & Imaging Products Association, “CIPA 2025 Imaging Consumer Survey,” cipa.jp. . Professional studios also monetize mobile shots through hybrid packages that raise average order value. Enhanced mobile apps shorten the path from capture to checkout, and cross-device cloud sync ensures users can finish orders on larger screens when preferred. Parents remain a key cohort, routinely translating milestone moments into photobooks, calendars, and wall décor.

Demand for photobooks and photo gifts

Personalized books, canvases, and keepsakes have shifted from niche to mainstream as consumers attach premium value to curated storytelling. The ease of drag-and-drop design tools and AI layout assistance reduces creation time, while high-capacity seasonal workflows allow vendors to serve holiday peaks without sacrificing turnaround. Corporate gifting is an emerging layer, especially in employee-recognition programs that seek customized memorabilia. Seasonal demand patterns remain pronounced, with holiday periods driving significant volume spikes that require scalable production and fulfillment capabilities.

E-commerce and app-based ordering

Digital storefronts claim the lion’s share of sales because they merge broad catalogues, real-time previews, and doorstep delivery in one interface. Seamless mobile integration and subscription checkout options lower friction and boost repeat frequency. Operators combine recommendation engines, automated color correction, and batch upload features to turn casual browsers into active buyers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital sharing replaces physical prints | -1.4% | Global, stronger in developed markets | Medium term (2-4 years) |

| High price sensitivity and commoditization | -1.1% | Global, particularly in emerging markets | Short term (≤ 2 years) |

| Tightening sustainability rules on photo chemicals | -0.8% | EU and North America primarily, expanding globally | Long term (≥ 4 years) |

| Specialty paper supply-chain bottlenecks | -0.6% | Global, acute in North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital sharing replaces physical prints

Social platforms offer instant gratification, unlimited reach, and zero incremental cost, tempting younger cohorts to bypass printing. Cloud archives supply perpetual backups, further eroding the perceived need for physical products. Yet overlap persists; many users still order prints for gifting, décor, or archival integrity. Vendors fight attrition by emphasizing tactile value, color fidelity, and permanence beyond scrolling feeds.

High price sensitivity and commoditization

Standardized 4×6 prints are widely available and largely indistinguishable, letting shoppers chase the lowest price. Margin pressure worsens when pulp and pigment costs climb, forcing producers to choose between rate increases or thinner spreads. Success tilts toward brands that package service quality, premium substrates, and fast fulfilment to justify higher tickets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Wall décor steers premium growth

In 2025, Photo Prints retained the largest slice at 54.02%, but Wall Décor on metal and acrylic is expanding 10.74% annually, signaling a shift toward high-impact display pieces. The photo printing market size for wall décor is forecast to widen rapidly as consumers treat personal images as interior design elements. Metal prints deliver superior vibrancy and scratch resistance, while acrylic adds depth and gloss that paper cannot replicate. Suppliers leverage these differentiators to lift average selling prices and offset commoditized print segments. Photobooks keep steady momentum because narrative collections satisfy the desire for organized storytelling. Cards spike seasonally, and calendars plateau as mobile planners supplant desk formats. Overall, category mix continues to favor premium, emotion-laden products that buffer revenue against price wars in standard prints.

The strategy pays dividends in mature markets where discretionary spending is high and buyers chase unique aesthetics. Meanwhile, mainstream formats still underpin volume, granting producers scale efficiencies. Diversifying into décor and giftable thus balances risk, stabilizes margins, and meets the evolving tastes of digitally native buyers seeking distinctive physical expressions.

By Print Technology: Dye-sublimation picks up speed

Inkjet accounted for 46.20% revenue in 2025 and remains the workhorse across labs and at-home units, yet dye-sublimation’s 9.05% CAGR reflects its edge in durability, color consistency, and instant-dry output. The photo printing market share held by dye-sublimation is expected to rise as kiosk operators and event photographers prioritise smudge-proof finishes.

Silver-halide wet labs keep a foothold in fine-art circles, prized for archival longevity. Digital toner presses cater to bulk commercial runs where per-page cost trumps substrate flexibility. Inkjet vendors are countering with higher-density nozzles and eco-solvent inks; Epson’s new printhead factory quadruples capacity to sustain global demand. Technology selection now revolves around matching resolution, media compatibility, and throughput to specific use cases rather than pursuing a single dominant process.

By Distribution Channel: Online platforms command growth

Online Platforms generated 61.05% of 2025 revenue and will climb 8.04% annually through 2031 as shoppers favor mobile uploads, AI auto-enhancement, and doorstep delivery. The photo printing market size for e-commerce far outstrips in-store alternatives because catalogue breadth and on-demand personalization are hard to duplicate in brick-and-mortar settings. App ecosystems recruit new cohorts by linking directly to camera rolls and social feeds, while subscription add-ons build stickier economics.

Retail photo labs, though shrinking, still meet urgent need-it-now jobs and appeal to users wanting in-person advice. Instant kiosks occupy airports and malls, offering rapid gratification but facing strong substitution from smartphone-to-home fulfilment. Mail-order houses cater to legacy customers yet increasingly push clients toward digital storefronts for convenience. Integrated omnichannel strategies—order online, pick up in store—are gaining traction in dense urban centers.

By End User: Consumers remain the volume engine

Individual buyers represented 80.85% of revenue in 2025 and will grow at 7.28% CAGR as life-event photography, social media inspiration, and smartphone quality improvements promote printing. The photo printing market size attached to consumer orders continues to dwarf corporate and pro segments, but professionals exert outsized influence on quality benchmarks. Pricing pressures stemming from rising overheads are nudging studios to upsell archival papers, frames, and digital add-ons.

Enterprises deploy branded gifts, employee awards, and marketing collateral, yet demand tracks broader economic cycles. Professional photographers remain a niche yet profitable customer base, specifying color-managed workflows and premium substrates that guide vendor R&D. Catering to both everyday consumers and specialized pros enables balanced portfolio management across economic climates.

By Print Material: Metal leads substrate innovation

Paper still dominates at 70.75%, but metal is sprinting ahead with 11.09% CAGR. Spectacular color saturation, fade resistance, and downstream framing savings validate a price premium that elevates margin. The photo printing market size for metal substrates is climbing as designers and homeowners seek gallery-grade presentation without glass. Canvas holds steady to its artistic texture, while acrylic commands luxury positioning through depth effects. Wood and fabric stay niche for rustic or textile-centric aesthetics. Vendors widen assortments to capture every décor taste, but metal’s durability and modern feel make it the flagship for upselling.

Geography Analysis

North America generated 31.95% of 2025 revenue on the back of entrenched consumer print habits, high household incomes, and mature e-commerce logistics. Growth is slower than global averages because of market saturation and digital-first millennials, yet premium décor categories and AI-driven convenience are keeping the region in positive territory. Regulatory focus on sustainable chemistry is pushing suppliers toward water-based inks and recyclable packaging, fueling product innovation.

Europe mirrors North America in maturity but places sharper emphasis on eco-credentials. Legislative pressure around hazardous chemicals and single-use plastics encourages vendors to upscale to environmentally preferable substrates and coatings. Demand remains steady for photobooks and seasonal cards, with Germany, France, and the United Kingdom anchoring volume. Subscription models resonate with time-pressed families seeking automated memory archiving.

Asia-Pacific is the headline growth story, posting 6.94% CAGR through 2031 as rising middle-class incomes, prolific smartphone usage, and a burgeoning gifting culture converge. Consumers in China gravitate toward personalized décor as part of home-improvement spending waves, while India’s premiumization trend lifts average order value for customized gifts. Japan’s youth photography resurgence supports incremental domestic demand. Local players often pair mobile payment methods with vernacular interfaces, lowering barriers for first-time print buyers. The geographic mix therefore balances mature-market premium upselling with emerging-market volume gains.

Competitive Landscape

The photo printing market features moderate fragmentation. Shutterfly, CEWE, Fujifilm, Snapfish, and Canon remain front-of-mind, but nimble app-native entrants continually test price ceilings and user-experience benchmarks. Consolidation is accelerating: Xerox agreed to acquire Lexmark for USD 1.5 billion, aiming to unlock USD 200 million in synergies within two years[3]Source: Xerox Holdings Corp., “Xerox to Acquire Lexmark International,” xerox.com.. In parallel, Getty Images closed a USD 3.7 billion merger with Shutterstock to build an AI-ready visual-content powerhouse.

Strategic playbooks cluster into three camps. First, technology leaders invest in AI-driven enhancement, automated workflows, and specialty substrates to stand apart on quality. Second, service-centric operators focus on friction-free ordering, rapid fulfilment, and white-glove packaging. Third, cost leaders pursue large-scale manufacturing and aggressive pricing to win budget shoppers. White-space opportunities center on subscription boxes, AI curation, and eco-friendly materials that meet tightening regulatory and consumer sustainability demands. Fujifilm’s cooperation with Konica Minolta on multifunction printers highlights industry willingness to pool R&D for scale economies. Expect further deals as incumbents fortify against app-led disruptors carving share among younger demographics.

Photo Printing Industry Leaders

Shutterfly

CEWE

Fujifilm (Wonder Photo)

Snapfish

Canon (Photo Printers & Services)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Getty Images finalized the USD 3.7 billion takeover of Shutterstock, projecting USD 150-200 million annual cost savings within three years.

- December 2024: Xerox revealed plans to buy Lexmark for USD 1.5 billion, eyeing synergy capture above USD 200 million in 24 months.

- June 2024: Epson broke ground on a USD 34 million printhead plant in Sakata City, Japan, slated to quadruple output by September 2025.

- June 2024: DNP Group launched the DP-DS820DX duplex photo printer, 40% smaller and 30% faster than its predecessor, with cumulative sales of JPY 4 billion targeted by

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the photo printing market as revenue generated from ordering physical photo products, prints, photobooks, wall décor, cards, and small gift items produced from digital or analog images through retail kiosks, online platforms, and professional labs worldwide.

According to Mordor Intelligence, this includes service fees and bundled materials but excludes sales of dedicated photo printers, ink, and paper sold at retail.

Segmentation Overview

- By Product Type

- Photo Prints

- Photobooks

- Photo Cards

- Calendars

- Wall Decor (Canvas, Metal, etc.)

- Personalized Photo Gifts

- By Print Technology

- Inkjet

- Dye-sublimation

- Silver-Halide (Wet Lab)

- Digital Press / Toner

- By Distribution Channel

- Online Platforms

- Retail Photo Labs

- Instant Kiosks

- Mail-order Services

- By End User

- Individual / Consumer

- Professional Photographers

- Corporate / Enterprise

- By Print Material

- Paper

- Canvas

- Metal

- Acrylic

- Wood and Fabric

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed executives at online photo labs, kiosk operators, and wholesale photofinishers across North America, Europe, and key Asia-Pacific hubs. Additional calls with paper mills and dye-sublimation OEMs helped us validate capacity utilization and average selling prices, while consumer pulse surveys in multiple languages gauged print-per-user ratios and gifting peaks.

Desk Research

We began with trade-class shipment records and tariff lines for photographic paper (HS 491191) on UN Comtrade, smartphone install data from the ITU, and annual camera shipment statistics issued by CIPA.

Analyst teams also screened postal and parcel traffic updates from USPS and UPU, consumer spend tables from the U.S. Bureau of Economic Analysis, and association white papers such as the Photo Marketing Association's end-user surveys.

Financial clues on leading service providers were gathered through D&B Hoovers and verified against 10-K filings, ensuring revenue streams attributable strictly to paid photo output.

These sources, among several others consulted, provided the foundational volumes, price windows, and demographic baselines that feed our model.

Market-Sizing & Forecasting

A top-down build starts with the global smartphone and digital camera installed base, matches it with measured print-per-device penetration, and converts captured volumes to value using region-specific blended ASPs. Selective bottom-up roll-ups from listed service revenues and sampled order tickets then test and refine totals.

Variables such as e-commerce share of retail, holiday seasonality indices, professional wedding counts, paper price spreads, average photobook page counts, and regional GDP-per-capita shifts serve as key model levers.

Forecasts employ multivariate regression layered on ARIMA to capture both structural growth and cyclical gift-season bumps endorsed by our expert panel.

Data gaps in bottom-up inputs are bridged through calibrated imputation guided by nearest-neighbor benchmarks.

Data Validation & Update Cycle

Outputs pass variance checks against historical ratios, peer signals, and shipment audit trails before a senior analyst review.

Models refresh annually, with interim updates triggered by material M&A, postal tariff swings, or sudden input-price shocks, ensuring clients always receive a current view.

Why Mordor's Photo Printing Baseline Commands Credible Reliability

Published estimates differ because firms vary in scope, price assumptions, and refresh timing.

Our team acknowledges these gaps upfront and shows how disciplined scope choices and continuous model hygiene resolve them for decision-makers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 26.61 Bn (2025) | Mordor Intelligence | - |

| USD 26.25 Bn (2025) | Global Consultancy A | Bundles commercial printing hardware and service contracts |

| USD 22.15 Bn (2024) | Industry Portal B | Relies on static ASPs, omits app-only micro-orders |

| USD 21.27 Bn (2024) | Regional Survey C | Excludes photo gifts, limited geographic sample |

In sum, the disciplined mix of fit-for-purpose sources, clear segment boundaries, and iterative cross-checks allows Mordor's baseline to remain transparent, repeatable, and dependable for strategic planning.

Key Questions Answered in the Report

What is the current size of the Photo Printing Market?

The global Photo Printing Market generated USD 27.76 billion in 2026 and is projected to grow to USD 34.34 billion by 2031 at a 4.33% CAGR.

Which region is growing the fastest?

Asia-Pacific is the fastest-expanding geography, forecast to register 6.94% CAGR through 2031 on the back of rising disposable incomes and deep smartphone penetration.

Which product segment shows the highest growth rate?

Wall décor printed on metal and acrylic substrates is advancing at 10.74% CAGR, well above the market average, due to its premium aesthetic and durability.

How dominant are online sales channels?

Online Platforms already account for 61.05% of revenue and are rising 8.04% annually, reflecting clear consumer preference for mobile-first ordering and doorstep delivery.

What technologies are reshaping the market?

Dye-sublimation is gaining momentum for its instant-dry, durable output, while AI-driven image curation and subscription “memory-box” services are redefining user experience and revenue predictability.

Are sustainability regulations affecting suppliers?

Yes. Stricter rules on photo chemicals in North America and Europe are pushing vendors toward water-based inks and recyclable materials, spurring product innovation and new operational standards.

Page last updated on: