Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

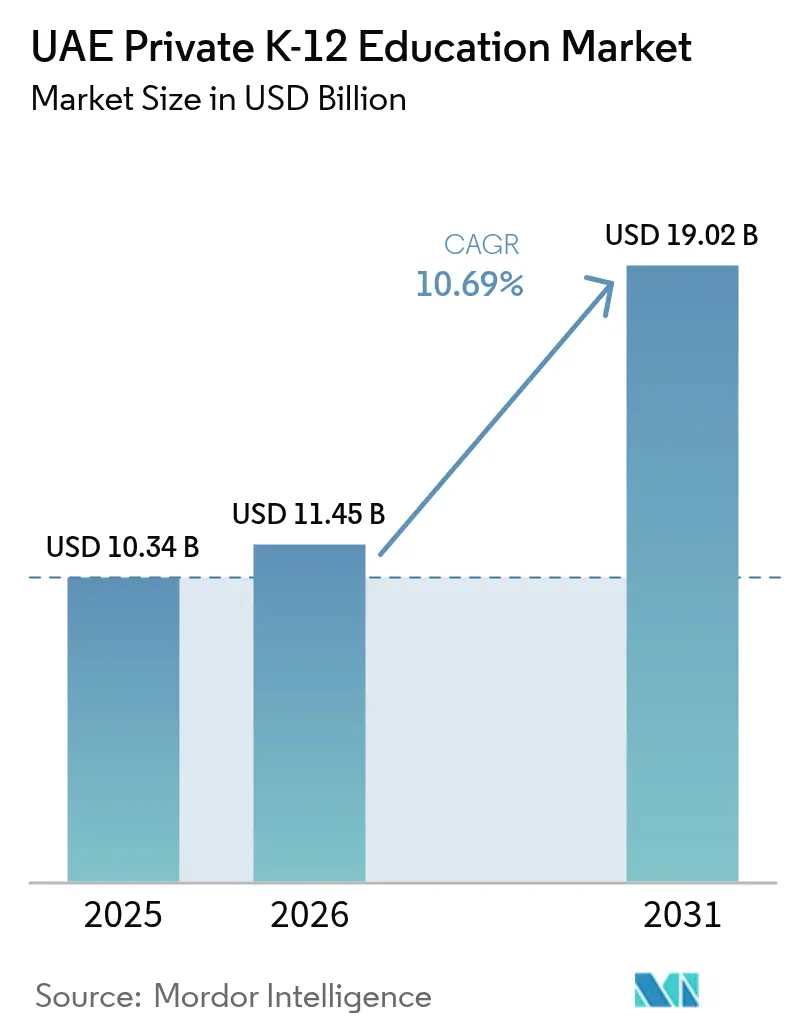

| Base Year Market Size (2025) | USD 10.34 Billion |

| Market Size (2026) | USD 11.45 Billion |

| Market Size (2031) | USD 19.02 Billion |

| Growth Rate (2026 - 2031) | 10.69% CAGR |

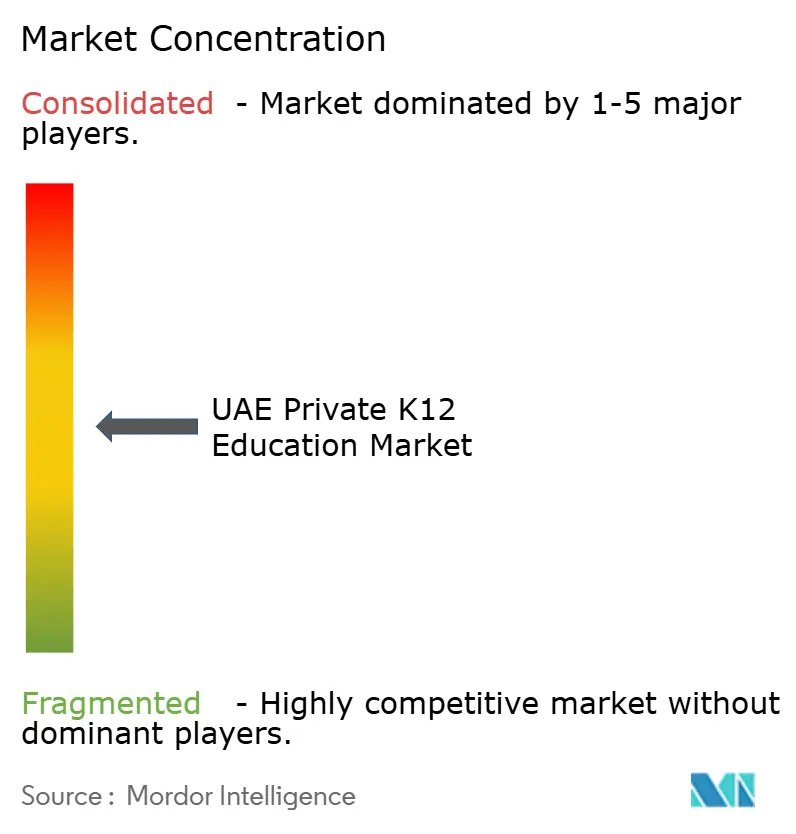

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Private K-12 Education Market Analysis by Mordor Intelligence

The UAE Private K-12 Education Market size was valued at USD 10.34 billion in 2025 and estimated to grow from USD 11.45 billion in 2026 to reach USD 19.02 billion by 2031, at a CAGR of 10.69% during the forecast period (2026-2031).

Robust expansion is powered by sustained expatriate inflows, Vision 2030-aligned privatization policies and higher disposable incomes that enable families to favor premium schooling options. Demand is most pronounced in Dubai, where a rigorous quality-assurance regime under the Knowledge and Human Development Authority (KHDA) continues to attract international operators while maintaining curriculum diversity.

Across the UAE private K-12 education market, early-years capacity additions, rapid EdTech adoption and foreign ownership allowances in education free zones have further elevated investor confidence, evidenced by multiple nine-figure capital injections from global asset managers. Even so, tuition-fee inflation and regulatory fee caps pose affordability challenges for middle-income households, nudging operators to explore mid-tier and blended-learning propositions that balance cost with quality.

Key Report Takeaways

- By geography, Dubai commanded 57.63% revenue share in 2025, while Ajman is projected to expand at a 9.97% CAGR through 2031.

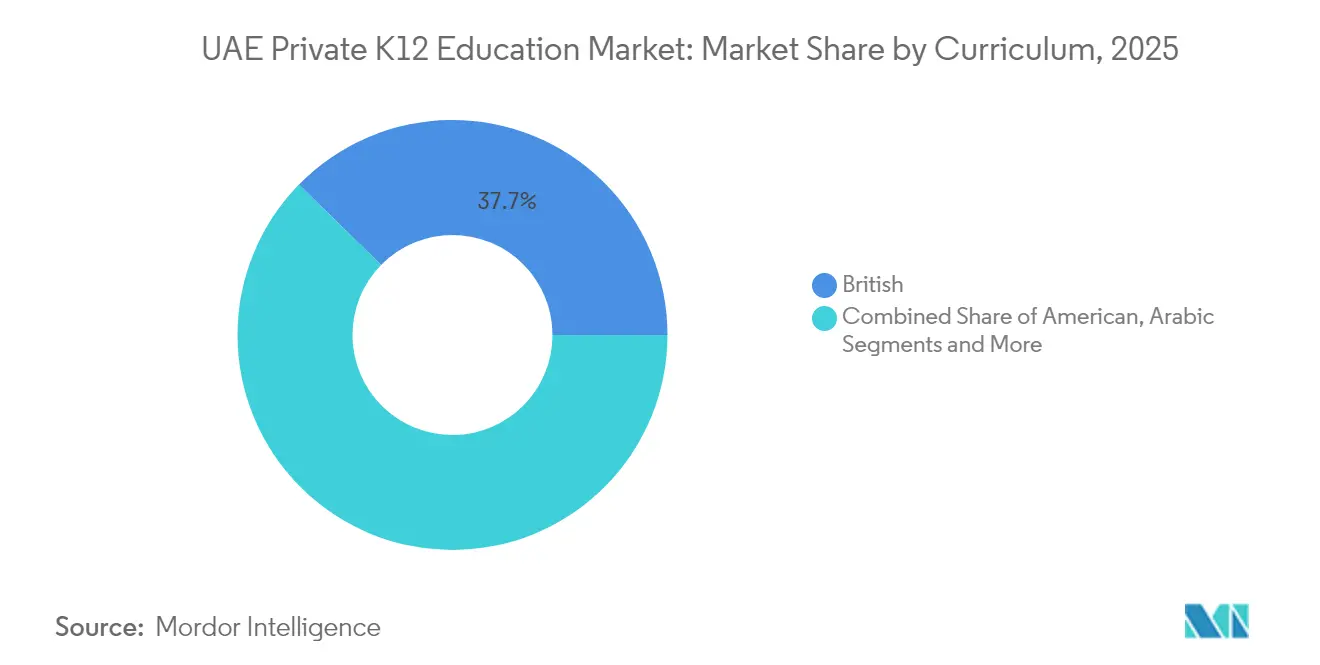

- By curriculum, the British curriculum captured 37.66% of the UAE private K-12 education market share in 2025, and the CBSE curriculum is forecast to post a 7.61% CAGR between 2026-2031.

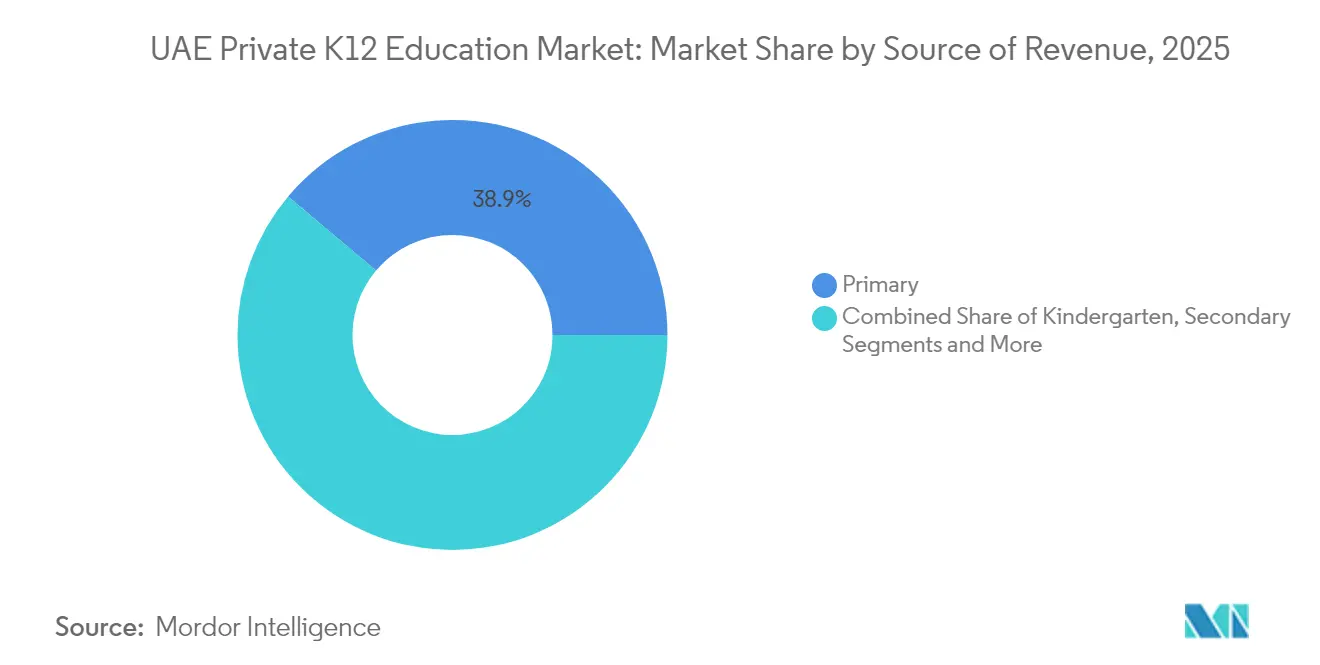

- By source of revenue, the primary segment accounted for 38.85% of the UAE private K-12 education market size in 2025, whereas kindergarten is advancing at a 10.88% CAGR to 2031.

- By nationality, expat students dominated the landscape, accounting for 90.55% of the UAE K-12 market share in 2025; however, the K-12 market size for local students is projected to expand at a 9.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Private K-12 Education Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expat-family population growth & premiumisation | +2.8% | Dubai, Abu Dhabi, Sharjah | Medium term (2-4 years) |

| Government privatisation agenda & Vision 2030 alignment | +2.1% | UAE-wide, Dubai lead | Long term (≥ 4 years) |

| Rising disposable income & preference for international curricula | +1.9% | Dubai, Abu Dhabi premium segments | Medium term (2-4 years) |

| Rapid EdTech adoption enhancing value proposition | +1.4% | Dubai, Abu Dhabi, spillover to Northern Emirates | Short term (≤ 2 years) |

| Expansion of mid-market school offerings by established operators | +1.6% | Sharjah, Northern Emirates, and outer Dubai districts | Medium term (2–4 years) |

| Policy support for private investment in education | +1.3% | UAE-wide, particularly in free zones and education hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expat-Family Population Growth & Premiumisation

Dubai’s private-school enrollment climbed 6% in the 2024-25 academic year to 387,441 students across 227 institutions, underscoring the magnet effect of a diversified expatriate workforce. Premium segments advanced even faster, with Taaleem Holdings reporting an 18.80% year-over-year enrollment surge that now generates 87.42% of its operating revenues. Land allocations totaling more than 1.5 million sq ft for new campuses delivered an extra 10,000 student seats in 2024, signaling proactive capacity planning by the Knowledge Fund Establishment. [1]Knowledge Fund Establishment, “Knowledge Fund Establishment looks to the future with strong growth,” kf.gov.ae Higher-income expatriates relocating to the UAE private K-12 education market prioritize international curricula that offer globally recognized qualifications. Corporate relocations also fuel the premiumisation trend, as multinational employers often subsidize tuition packages to attract talent. This demographic dynamic underpins sustained demand for British and U.S. curriculum schools even as emerging Asian programs gain traction.

Government Privatisation Agenda & Vision 2030 Alignment

Public-policy momentum remains strong with Dubai’s Education 33 strategy targeting 100 new private schools and 49,000 affordable seats by 2033. Federal support is visible in the AED 989.2 million budget allocation to the Ministry of Education in 2024, which creates complementary infrastructure enabling private growth. Free-zone regulations that permit 100% foreign ownership encourage renowned brands such as Harrow School and Reigate Grammar School to enter the UAE private K-12 education market via franchise or management contracts. Vision 2030 frames education as a pillar of a knowledge-based economy, aligning governmental goals with operator expansion strategies. Streamlined licensing and land-lease incentives reduce entry barriers and shorten construction timelines. Over the long term, this policy environment is expected to lift market penetration of organized school chains and enhance quality benchmarks nationwide.

Rising Disposable Income & Preference for International Curricula

Dubai approved a 2.35% tuition-fee increase for 2025-26 based on the Education Cost Index, giving premium operators limited but steady pricing headroom. Employer tuition allowances also buoy household purchasing power; Emirates NBD’s AED 200 million “Get Future Ready” scheme exemplifies corporate support for education benefits that sustain enrollment even during economic volatility.[2]Emirates NBD, “Learning and Development | Upskill and Get Future Ready,” emiratesnbd.com The British curriculum retains its leadership with 37% of Dubai enrollments, while U.S. programs hold 14%, mirroring expatriate preferences for globally portable credentials. The UAE private K-12 education market continues to attract Indian families seeking CBSE schools, and the board’s 107 UAE campuses mark its largest offshore footprint. Rising incomes thus reinforce a consumer tilt toward established curricula that align with university admission requirements in home countries.

Rapid EdTech Adoption Enhancing Value Proposition

Alef Education posted AED 759 million revenues in 2024 and secured contract extensions with Abu Dhabi’s education authority through 2033, illustrating the commercial scale attainable via digital-learning solutions. GESS Dubai exhibitions showcase heightened interest in AI, AR and data analytics tools as schools in the UAE private K-12 education market seek instructional differentiation.[3]The Young Vision, “GESS Dubai 2024 to Spotlight EdTech,” theyoungvision.com GEMS Education’s forthcoming School of Research and Innovation will feature advanced robotics and AI laboratories, demonstrating how premium campuses convert technology leadership into pricing power. KHDA’s regulated frameworks for distance-learning evaluation ensure minimum standards for hybrid and online models, promoting confidence among parents considering blended options. EdTech integration also streamlines administrative workflows, potentially easing fee-cap pressures by lowering operating costs over time.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tuition-fee inflation outpacing wage growth | -1.6% | Dubai, Abu Dhabi middle-income segments | Short term (≤ 2 years) |

| KHDA/ADEK fee-cap regulations | -1.2% | Dubai, Abu Dhabi | Medium term (2-4 years) |

| High teacher turnover and recruitment costs | -1.0% | National; most acute in Tier 2 schools | Medium term (2–4 years) |

| Parent shift toward hybrid and home-school models | -0.8% | Urban expat-heavy areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tuition-Fee Inflation Outpacing Wage Growth

Although KHDA capped 2025-26 fee increases at 2.35%, cumulative hikes still strain budgets for families with multiple children. Affordable initiatives such as GEMS Founders Dubai South, with annual fees beginning at AED 27,300, respond directly to this cost-income gap. Employers continue to widen tuition allowance programs, yet coverage varies and often leaves middle-management families under-insured. As a result, demand is gravitating toward mid-market schools that balance quality and affordability within the UAE private K-12 education market. Economic swings in expatriate source countries add another layer of uncertainty to household planning. Persistent affordability tension may curb premium-segment growth unless operators diversify price points or enhance scholarship schemes.

KHDA/ADEK Fee-Cap Regulations

KHDA’s Education Cost Index ties annual fee adjustments to operational-cost movements, limiting revenue upside for operators despite rising input costs. ADEK rules in Abu Dhabi allow exceptional 15% hikes only when schools prove financial losses and sustain 80% enrollment, setting a high bar for approval. [4]KHDA, “Education Cost Index set at 2.6 percent for 2024-25,” khda.gov.ae Mandatory disclosure of all charges via fee fact sheets further sharpens parental price sensitivity. Smaller chains in the UAE private K-12 education market face disproportionate compliance burdens, particularly around documentation and audit readiness. Maintaining educational quality amid tight fee controls necessitates operational efficiencies that may defer capital-intensive improvements. Over time, persistent caps could accelerate consolidation as scale advantages become critical for margin stability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source of Revenue: Early Years Drive Growth Momentum

Kindergarten and primary schooling dominate revenue streams within the UAE private K-12 education market. In 2025, the primary segment delivered 38.85% revenue share, reflecting its large enrollment base and compulsory nature for most expatriate families. Kindergarten, while smaller, is forecast to generate a 10.88% CAGR between 2026-2031, the fastest among all stages, driven by heightened parental awareness of early childhood learning outcomes. Taaleem Holdings’ acquisition of Kids First Group, securing a 95% stake in nurseries, corroborates institutional conviction in early-years upside. New capacity releases by the Knowledge Fund Establishment added thousands of pre-K seats in 2024, ensuring supply keeps pace with younger expatriate inflows. Employers in fast-growing sectors now factor early childhood education into family relocation packages, reinforcing kindergarten enrollment resilience.

Early-years expansion also benefits from Dubai’s Education 33 emphasis on holistic child development, which prescribes mandated student-teacher ratios that appeal to quality-conscious parents. Operators capture cross-selling opportunities by offering seamless progression from nursery to primary classes on the same campus, boosting lifetime value per student within the UAE private K-12 education market. ESG-driven corporate subsidies focused on female workforce participation further incentivize investment in on-site or partner nurseries. Secondary education retains a 35.05% share as families commit to international diplomas, yet its growth is steadier than the explosive kindergarten trajectory. Intermediary (middle-school) programs occupy 8.28% of revenue and act as a bridge that locks in retention ahead of high-stakes exams. Overall, the mix shift toward younger cohorts positions operators to secure longer enrollment duration and recurring cash flows.

By Curriculum: British Dominance Faces CBSE Challenge

The British model continues to anchor the UAE private K-12 education market with a 37.66% share in 2025, supported by its alignment with UK university admission pathways and a sizable Commonwealth expatriate base. American programs follow with 30.72% share, favored by Emirati nationals seeking U.S. college matriculation. CBSE’s 7.61% forecast CAGR makes it the fastest-growing curriculum amid deepening India-UAE economic ties and an Indian diaspora exceeding 3.5 million. The board’s 107 UAE schools represent its largest overseas footprint, showcasing scalability potential. Operators increasingly launch dual-curriculum campuses to diversify risk and capture multiple demographic segments. French, German and International Baccalaureate programs collectively hold 4.43%, serving niche communities yet adding to the multicultural appeal of the market.

KHDA and ADEK ensure quality parity across curricula, mandating periodic inspections that publish transparent ratings influential in parental decision-making. Recent approvals favor British expansions, with five of the six new Dubai schools for 2024-25 following UK frameworks. Nonetheless, CBSE’s momentum is evident in Sharjah and Northern Emirates where fee sensitivity intersects with high academic rigor. Curriculum choice also influences per-capita fee structures, with British and IB programs commanding premium pricing in the UAE private K-12 education market, whereas CBSE remains competitively priced. Over the medium term, the rivalry between UK and Indian boards is likely to intensify, pushing operators to innovate around ancillary offerings such as global internship pathways and STEM specializations.

By Nationality: Emirati Enrolment Accelerates Despite Expatriate Dominance

Expatriate children accounted for 90.55% of private-school enrolment in 2025, underscoring Dubai and Abu Dhabi’s position as the world’s largest hub for K-12 students following British, Indian, and American curricula. Demand is propelled by long-term Golden Residence visas and a diversified economy that attracts global professionals in technology, finance, and logistics. Private operators opened 10 additional campuses for the 2024-25 academic year, raising Dubai’s enrolment base to 387,441 students across 227 private schools. Federal Decree-Law No. 18 of 2020 obliges every private school to embed Emirati social studies and Arabic-language modules, ensuring cultural preservation even within global syllabi. These policies together deliver a dual promise of international accreditation for expatriate families and national identity reinforcement for locals.

Local enrolment is gaining momentum; Emirati students are projected to expand at a 9.63% CAGR between 2026 and 2031. KHDA’s Education 33 strategy provides merit-based scholarships in premium schools. The Dubai Distinguished Students Programme further lowers tuition barriers for top-performing nationals while mandating Arabic instruction in early years to strengthen language proficiency. Rising household wealth from non-oil sectors enables Emirati families to choose international campuses that were once the preserve of expatriates. Long-term residency paths convert many expatriate households into permanent education consumers, bolstering overall market stability. As a result, bilingual programs blending IB or A-Level credentials with UAE culture are scaling quickly to capture both segments.

Geography Analysis

Dubai accounted for 57.63% of 2025 revenues in the UAE private K-12 education market, buoyed by its role as a global business hub and its well-established KHDA governance model. Abu Dhabi contributed second dominating share, leveraging government and hydrocarbon sector employment to sustain premium-segment growth. Sharjah captured 9.41%, positioning itself as a value-for-money alternative with cultural-heritage cachet. Rapid urbanization in Ajman translated to the country’s highest projected CAGR of 9.97% for 2026-2031, aided by lower real-estate costs that translate into affordable fees. Ras Al Khaimah, Fujairah and Umm Al Quwain collectively offer 7.90% growth potential as tourism and manufacturing projects attract new residents.

Regional policy support reinforces geographic diversification. Dubai’s Education 33 blueprint calls for 100 new schools by 2033, while ADEK’s 39 updated policies enhance transparency and quality across Abu Dhabi campuses. Sharjah’s Masaar development will host a 42,000 sq m Reigate Grammar campus opening in 2027, highlighting northern emirate ambitions to lure international brands. Free-zone structures in Ras Al Khaimah offer long land leases and 100% foreign equity, appealing to operators seeking greenfield opportunities without KHDA oversight. Improved transport corridors shorten commute times, making cross-emirate schooling viable for families. Collectively, these factors could gradually rebalance enrollment share away from Dubai toward emerging hubs, although Dubai is expected to retain clear primacy through the forecast horizon.

Competitive Landscape

The UAE private K–12 education market shows moderate concentration, with the top school groups holding a significant share of total enrollment and revenue. GEMS Education leads the sector and has recently secured major funding to support its expansion plans. SABIS continues to prioritize standardization across its network of schools, while Aldar Education leverages its real estate capabilities to build integrated, mixed-use education campuses. Taaleem Holdings is strengthening its premium market position through new school developments and strategic acquisitions such as Kids First nursery. Innoventures Education is targeting underserved areas in Sharjah and the Northern Emirates to attract more price-sensitive expatriate families.

Strategic differentiation increasingly hinges on technology and teacher-quality metrics. Alef Education’s 10-year contract extension with Abu Dhabi’s authority exemplifies the viability of digital-first learning solutions in public-private contexts. Operators also innovate through hybrid models that combine online platforms with brick-and-mortar facilities to expand catchment without proportionate capex. Fee-cap headwinds accelerate cost-efficiency programs, including shared-services centers and bulk procurement of learning resources. At the same time, premium schools justify higher fees by investing in AI labs, robotics studios and university counseling services that translate into alumni success stories.

Global capital continues to flow into the UAE private K-12 education market. Dubai Holding joined a USD 14.5 billion bid for Nord Anglia in March 2025, signaling appetite to build transcontinental portfolios. Cognita’s acquisition of Al Ain English Speaking School underlines the attractiveness of regional bolt-ons that deliver instant market access. Free-zone policies permitting full foreign ownership and dividend repatriation draw international operators that value regulatory clarity. Looking ahead, M&A is expected to intensify, particularly around mid-market chains that can be scaled via standardized systems and central procurement.

UAE Private K-12 Education Industry Leaders

GEMS Education

SABIS Education Services

Aldar Education

Taaleem Holdings

Innoventures Education

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Taaleem Holdings signed a Sale and Purchase Agreement to acquire a 95% stake in Kids First Group, expanding its early-childhood portfolio.

- March 2025: Dubai Holding participated in a USD 14.5 billion consortium to acquire Nord Anglia, marking a significant global expansion move.

- March 2025: GEMS Education announced a USD 300 million growth investment plan to develop new schools and upgrade existing facilities.

- January 2025: GEMS Education confirmed a USD 100 million premium campus in Dubai featuring advanced EdTech infrastructure.

UAE Private K-12 Education Market Report Scope

This report provides a comprehensive background analysis of the UAE private K12 education market, covering the current market trends, restraints, investment analysis, detailed information on the various segments, and a competitive landscape of the education industry.

The market is segmented by geography, source of revenue, and curriculum. By geography, the market is further segmented into the North Region, West Region, South Region, and East Region. By source of revenue, the market is further segmented into kindergarten, primary, intermediary, and secondary. By curriculum, the market is further segmented into American, British, Arabic/UAE, Indian, and Other Curricula. The market size and forecasts are provided in terms of value (USD) for all the above segments.

By Source of Revenue

| Kindergarten |

| Primary |

| Intermediary |

| Secondary |

By Curriculum

| American |

| British |

| Arabic |

| CBSE |

| Other Curriculum |

By Nationality

| Expat Students |

| Local Students |

By City

| Abu Dhabi |

| Dubai |

| Sharjah |

| Rest of UAE |

| By Source of Revenue | Kindergarten |

| Primary | |

| Intermediary | |

| Secondary | |

| By Curriculum | American |

| British | |

| Arabic | |

| CBSE | |

| Other Curriculum | |

| By Nationality | Expat Students |

| Local Students | |

| By City | Abu Dhabi |

| Dubai | |

| Sharjah | |

| Rest of UAE |

Key Questions Answered in the Report

How large is the UAE private K-12 education market in 2026?

The market is valued at USD 11.45 billion in 2026 and is forecast to reach USD 19.02 billion by 2031.

What is the projected CAGR for UAE private K-12 education between 2026 and 2031?

The compound annual growth rate is expected to be 10.69% over the forecast period.

Which emirate leads in private school revenue?

Dubai leads with 57.63% market share, supported by a robust KHDA regulatory framework and diverse curricula.

Which curriculum is growing fastest in UAE private schools?

The CBSE curriculum shows the strongest momentum with a 7.61% CAGR forecast through 2031.

What factors are driving investment in UAE private schools?

Key drivers include expatriate population growth, Vision 2030 privatization initiatives and rapid EdTech adoption.

How concentrated is the competitive landscape?

The top five operators control about 50% of revenue, giving the market a moderate concentration score of 6.

Page last updated on: