Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 9.08 Billion |

| Market Size (2031) | USD 12.23 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

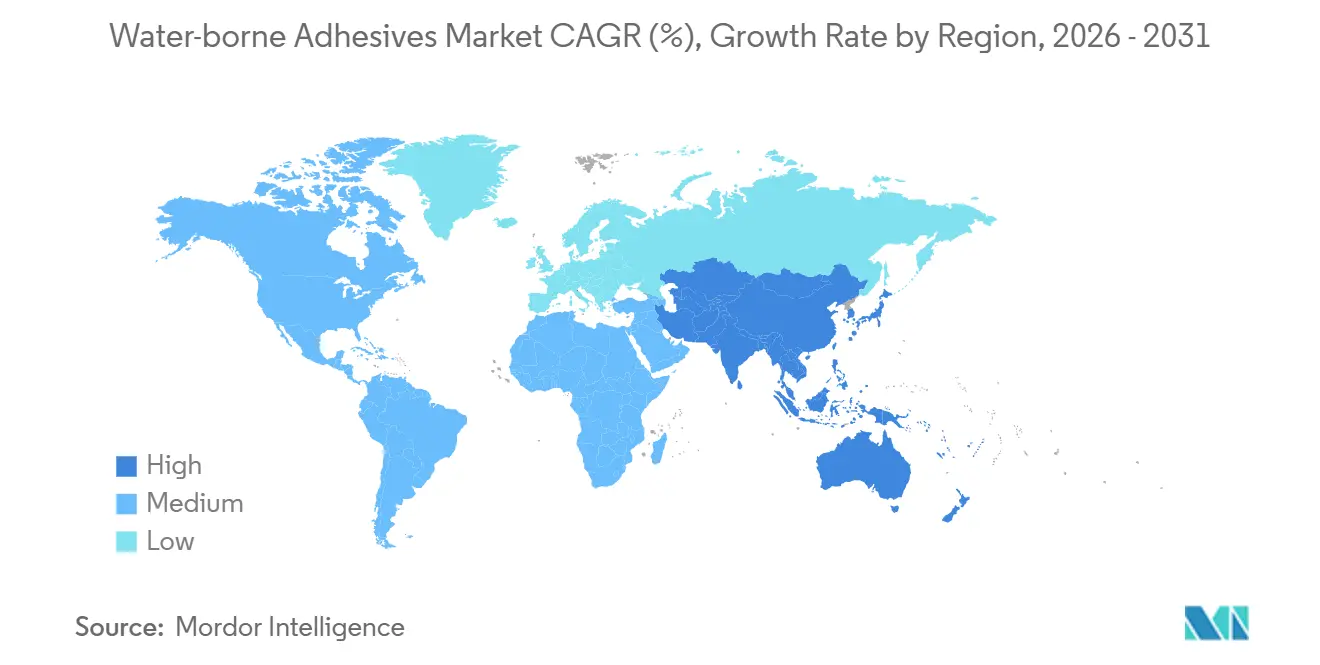

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Water-borne Adhesives Market Analysis by Mordor Intelligence

The Water-borne Adhesives Market size is estimated at USD 9.08 billion in 2026 and is expected to reach USD 12.23 billion by 2031, at a CAGR of 6.12% during the forecast period (2026-2031). Heightened scrutiny of volatile organic compound (VOC) emissions, especially in China, the European Union, and the United States, is accelerating the replacement of solvent-borne chemistries with water-based alternatives. Fast-moving fulfillment centers that seal more than 300 corrugated cases per minute favor polyvinyl acetate (PVA) emulsions that cure within three seconds, while modular building contractors in Indonesia and Thailand increasingly specify low-VOC adhesives to meet green-building rating thresholds. Polyurethane (PU) dispersions are also gaining traction in lightweight vehicles where automakers now replace steel rivets with 300 bonding points per car, cutting curb weight by 2.2 pounds and improving fuel economy by 3%. Flexible packaging converters are adopting next-generation acrylic emulsions that pass United States Food and Drug Administration (FDA) 21 CFR 175.105 migration limits, enabling solvent-free laminates for retort pouches.

Key Report Takeaways

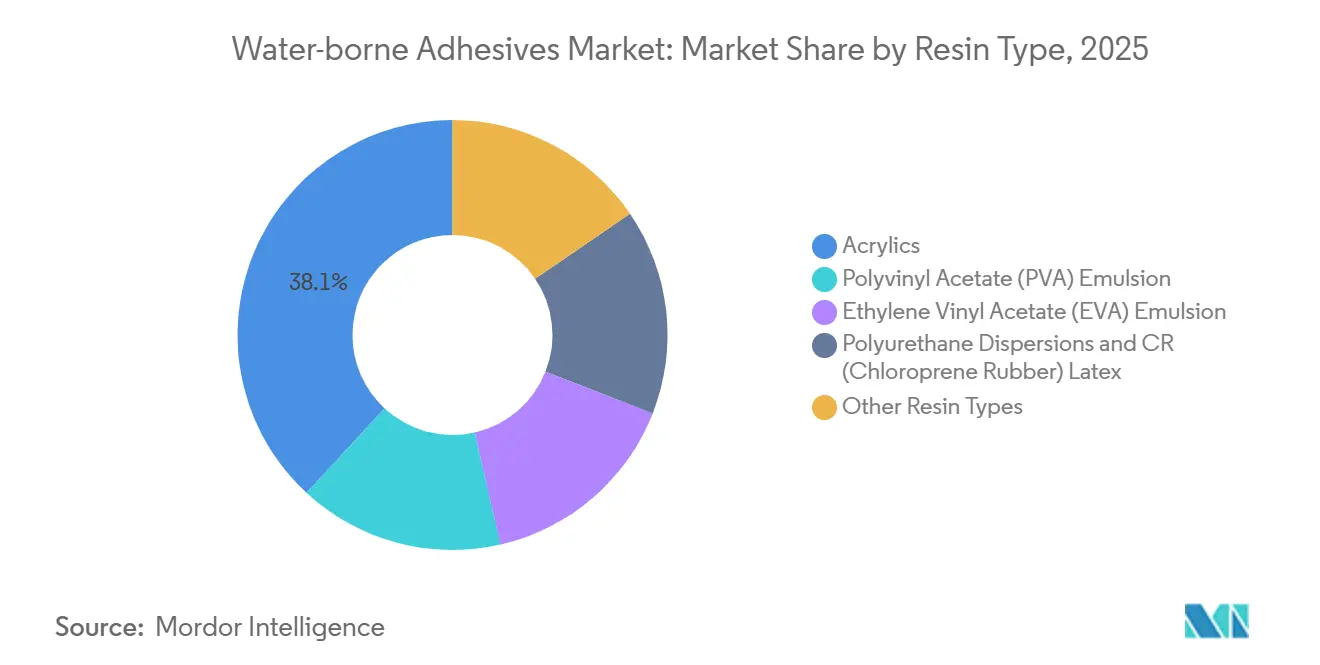

- By resin type, acrylics led with 38.12% of the water-borne adhesives market share in 2025, while polyurethane dispersions are projected to register the highest CAGR at 6.71% through 2031.

- By application, flexible packaging commanded 40.44% of the water-borne adhesives market size in 2025; laminating and filmic structures are forecast to expand at a 7.52% CAGR to 2031.

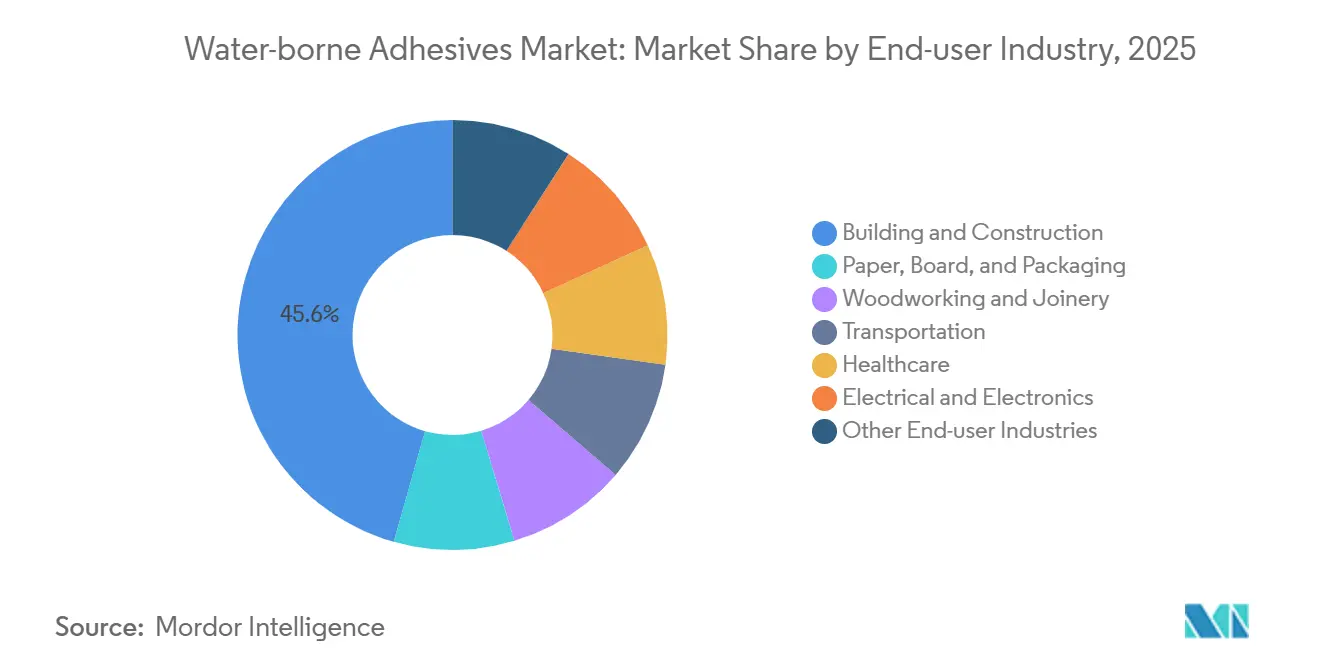

- By end-user industry, building and construction accounted for 45.59% revenue in 2025, whereas healthcare is advancing at a 6.37% CAGR through 2031.

- By substrate, paper and paperboard captured 51.28% volume in 2025, yet plastics and films are forecast to grow at a 6.51% CAGR through 2031 as mono-material pouches gain favor.

- By geography, Asia-Pacific held 40.45% market share in 2025 and is set to grow at a 6.92% CAGR to 2031 on the back of stringent regional VOC caps.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Water-borne Adhesives Market*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce-led boom in corrugated packaging | +1.4% | North America, China, India | Short term (≤ 2 years) |

| VOC-reduction mandates | +1.8% | North America, EU, China | Medium term (2-4 years) |

| ASEAN modular construction | +1.1% | Indonesia, Thailand, Vietnam, spill-over to India | Medium term (2-4 years) |

| Lightweight automotive bonding | +0.9% | Germany, United States, Japan, South Korea | Long term (≥ 4 years) |

| Bio-based food-contact breakthroughs | +0.7% | North America, EU, early adoption in Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce-Led Boom in Corrugated Packaging

Global online sales reached USD 6 trillion in 2025, prompting logistics operators to redesign secondary packaging for faster throughput and lower damage rates. Corrugated converters now use water-based starch and PVA adhesives that develop set speed within three seconds, enabling production lines to exceed 300 meters per minute without the fire hazards seen in hot-melt systems[1]United Nations Conference on Trade and Development, “Global E-Commerce Outlook 2026,” unctad.org. Rising demand for right-sized boxes has increased the packaging-to-product weight ratio, which elevates adhesive consumption per shipment. Major e-retailers such as Amazon eliminated plastic air pillows in 2024, accelerating the switch to paper-based cushioning bonded with water-borne chemistries. Similar commitments by Walmart and Alibaba have reinforced this trajectory, making corrugated packaging the single-largest growth node in the water-borne adhesives market.

VOC-Reduction Mandates Driving Solvent-to-Water Switch

China’s GB 33372-2020 caps VOCs in water-borne products at 50 g/kg, while the European Union’s Directive 2004/42/EC restricts decorative coatings to 30 g/L and contact adhesives to 50 g/L. In the United States, the Environmental Protection Agency’s National Emission Standards for Hazardous Air Pollutants require a 95% VOC capture rate or low-emitting formulations. California’s Air Resources Board (CARB) Phase 2 regulation sets an even tighter 25 g/L ceiling for architectural coatings. Collectively, these rules have forced converters to reformulate, thereby boosting demand across the water-borne adhesives market.

ASEAN Modular Construction Spurring Fast-Setting PVA Demand

Indonesia earmarked USD 412 billion for infrastructure from 2024-2029, with one-third allocated to prefabricated housing that prefers fast-curing water-based adhesives. Thailand’s Eastern Economic Corridor funnels THB 3 trillion (USD 85 billion) into industrial townships where off-site fabrication trims labor by 40%. Vietnam’s QCVN 01:2021 VOC standard of 75 g/L also nudges builders toward aqueous systems. PVA emulsions formulated with latent cross-linkers achieve handling strength in 15 minutes, enabling stacked panel transport without delamination, a decisive edge over solvent-borne counterparts.

Lightweight Automotive Bonding Boosting PU Dispersions

Global light-vehicle output hit 88 million units in 2025, with electric vehicles making up 18%. Automakers seek to extend driving range by shedding mass, replacing 55 pounds of metal fasteners with 2.2 pounds of PU dispersion adhesive per vehicle. These water-borne dispersions bond aluminum, composites, and high-strength steel without galvanic corrosion. ISO 11343-certified products now deliver 25 MPa lap-shear strength on oiled steel, while thermally conductive grades filled with boron nitride dissipate heat in 800-V battery packs.

Restraints Impact Analysis of Water-borne Adhesives Market*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heat-resistance gap in high-temperature uses | -0.6% | Global, notably automotive under-hood and electronics | Medium term (2-4 years) |

| Limited reach in high-end structural bonding | -0.4% | North America, EU, Japan | Long term (≥ 4 years) |

| Higher capex for water-borne lines | -0.3% | India, Southeast Asia, South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Heat-Resistance Gap Limits Entry into High-Temperature Uses

Most aqueous formulations degrade above 120 °C, preventing deployment in engine compartments where ambient temperatures exceed 150 °C and in electronics reflow soldering peaks of 260 °C. Epoxy and polyimide systems retain integrity at 200 °C for thousands of hours, a performance envelope water-based products cannot match without sacrificing film formation. The rise of silicon-carbide inverters demanding 175 °C adhesives further sidelines water-borne chemistries, while aerospace specs such as ASTM D5868 require 80% strength retention at 180 °C, effectively excluding them[2]ASTM International, “Standard D5868,” astm.org .

Limited Penetration in High-End Structural Bonding

Wind-turbine blades need 30 MPa tensile strength and 15 kJ/m² fracture toughness per DNV GL guidelines, metrics attainable only by epoxy variations under current technology. ISO 11343 crash-test retention targets of 70% bond strength after 1,000 hours at 85 °C/85% RH are challenging for aqueous dispersions that cure via water evaporation. Marine standards from Lloyd’s Register require 10,000-hour salt-spray endurance that water-based systems can meet only with pricey inhibitors. Consequently, silicone and moisture-curing polyurethane keep their footing in curtain-wall glazing and façade panels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Water-borne Adhesives Market Segment Analysis

By Resin Type:

PU Dispersions Gain on AcrylicsAcrylics held 38.12% of revenue in 2025, buoyed by pressure-sensitive labels and paper converting, where 10-15 N/25 mm peel adhesion suffices. The water-borne adhesives market size for PU dispersions is projected to increase at a 6.71% CAGR to 2031 as automakers and footwear brands demand abrasion resistance and flexibility unrivaled by acrylics. Covestro’s Dispercoll U series posts 800% elongation and 25 MPa tensile strength without free isocyanate, positioning it for single-component systems that simplify plant logistics. PVA emulsions still dominate woodworking, forming transparent glue lines and penetrating porous substrates, while EVA emulsions remain preferred for carpet backing and hygiene disposables despite a 20% cost premium.

Innovation is narrowing the performance gap: self-crosslinking acrylics now reach 3 MPa lap-shear strength on aluminum, previously an epoxy stronghold. Bio-based resins remain below 5% but are rising as Henkel and Wacker launch lignin and starch derivatives. Chloroprene latex continues to lose share after the EU REACH restricted nitrosamine precursors. Collectively, the shift toward high-function PU dispersion broadens the value pool inside the water-borne adhesives market.

By Application:

Laminating Outpaces Flexible PackagingFlexible packaging represented 40.44% market share in 2025 as brands migrated from rigid formats to stand-up pouches that cut material use by 30%-50%. The water-borne adhesives market size for laminating and filmic structures is forecast to grow at 7.52% through 2031, fueled by multilayer barrier films combining polyethylene and metallized polyester. FDA-compliant solvent-free systems now leave <5 mg/m² residuals, opening retort pouch opportunities.

Tapes and labels benefit from e-commerce tamper-evidence needs, while flooring adhesives certified under LEED emit <50 µg/m³ total VOCs. Bookbinding faces digital substitution yet retains premium hardcovers that rely on neutral-pH PVAs. Non-woven hygiene lines seek formaldehyde-free formulations, enabling water-borne dispersions to capture elastic attachment and wetness-indicator niches.

By End-User Industry:

Healthcare AcceleratesBuilding and construction generated 45.59% revenue in 2025, underpinned by LEED and Living Building Challenge criteria setting <50 g/L VOC limits. Healthcare is poised for a 6.37% CAGR to 2031 as ISO 10993-compliant acrylics dominate wound dressings that maintain adhesion for seven days without skin maceration. The water-borne adhesives market share for packaging remains high due to carton sealing and label application.

Woodworking applications must meet CARB Phase 2 formaldehyde caps, spurring uptake of PVAs. Transportation interior trims increasingly adopt PU dispersions for acoustic damping below 100 °C. Electronics remain a smaller niche given heat limits, although silver-filled conductive emulsions are edging into flexible printed circuits processed at ≤150 °C.

By Substrate:

Plastics Narrow the Gap with PaperPaper and paperboard substrates provided 51.28% bonding volume in 2025, dominated by corrugated, folding carton, and tissue lamination lines that value low-cost starch and PVA blends. Plastics and films are growing 6.51% thanks to recyclable mono-material pouches; new aqueous laminating systems deliver 3 N/15 mm peel on corona-treated polyethylene without solvent primers.

Wood composites employ phenol-resorcinol and melamine-urea-formaldehyde adhesives, achieving 1.5 MPa dry-bond and 0.8 MPa wet-bond strength. Metal applications remain relegated to pre-painted coil, where epoxy-acrylic hybrids provide chromate-free corrosion resistance, while glass bonding for windshield replacements still relies on moisture-curing PU. Textile and non-woven sectors demand wash-durable dispersions that survive 60 °C cycles and 120 °C drying, a capability met by heat-activated cross-linkers in PU dispersions.

Geography Analysis

APAC Water-borne Adhesives Market

Asia-Pacific controlled 40.45% of revenue in 2025 and is expected to compound at a 6.92% CAGR through 2031 on the back of China’s GB 18582-2020 and GB 30981-2020, which cap VOCs in adhesives at 50 g/kg. Indonesia’s USD 412 billion infrastructure plan favors modular housing that relies on fast-setting PVAs, while Thailand’s THB 3 trillion Eastern Economic Corridor drives low-VOC demand. India’s Goods and Services Tax reforms lowered interstate costs by 15%, enabling bulk production hubs in Gujarat and Tamil Nadu. Japan’s 2025 workplace exposure limits of 10 ppm toluene push formulators toward aqueous platforms.

North America Water-borne Adhesives Market

North America’s construction and automotive markets have plateaued, yet e-commerce and healthcare sustain 3%-4% growth. The United States NESHAP rule rewards converters that switch to water-borne products by obviating thermal oxidizers. Canada’s 2024 formaldehyde cap of 0.05 ppm accelerates PVA uptake in cabinetry. Mexico’s tier-1 suppliers now specify aqueous structural adhesives to satisfy OEM sustainability scorecards.

Europe Water-borne Adhesives Market

Europe continues to lead on regulation: Germany’s TA Luft limits VOC stack emissions to 20 mg/m³, while France’s RE2020 enforces lifecycle carbon audits that favor bio-based adhesives. Post-Brexit UK REACH retained EU restrictions on carcinogens, maintaining momentum toward solvent-free formulations. Nordic circular programs advocate design-for-disassembly, positioning water-borne adhesives for recyclable furniture.

South America and MEA Water-borne Adhesives Market

South America is regaining momentum after a short recession. Brazil’s CONAMA 452 harmonizes with 50 g/L VOC caps, spurring adoption in architectural coatings, whereas Argentina’s panel mills comply with MERCOSUR’s 0.1 ppm formaldehyde limit, boosting urea-formaldehyde emulsions. The Middle East and Africa remain nascent; Saudi megaprojects and South African renewables create localized demand for low-VOC bonding in solar laminates and turbine blades.

Competitive Landscape

The water-borne adhesives market is moderately consolidated. Henkel opened a EUR 50 million technology center in Düsseldorf in 2025 to scale latent-reactive PU dispersions that cure at 80 °C for automotive trim and electronics potting. H.B. Fuller’s USD 1.85 billion acquisition of ND Industries added high-margin engineered adhesives for industrial assemblies. Arkema’s 2024 purchase of Prochimir expanded its South American footprint with eight sites and EUR 120 million annual sales. Sika commissioned a USD 45 million plant in Egypt in 2025 to capture rising North African construction demand. White-space innovation revolves around heat-resistant aqueous systems, bio-based food-contact grades, and conductive dispersions for flexible electronics. Patent filings climbed double digits in 2024-2025, highlighting self-crosslinking acrylics and graphene-filled formulations. Third-party certifications such as GreenGuard Gold now serve as de facto entry tickets to premium construction and consumer packaged goods accounts, with 12 manufacturers publishing Environmental Product Declarations in 2025.

Water-borne Adhesives Industry Leaders

Henkel AG & Co. KGaA

H.B. Fuller Company

Arkema

3M

Dow

- *Disclaimer: Major Players sorted in no particular order

Water-borne Adhesives Market Companies Covered in this Report

- 3M

- Arkema

- Ashland

- Avery Dennison Corporation

- Benson Polymers Pvt Ltd.

- DIC CORPORATION

- Dow

- Dymax

- Evonik Industries AG

- H.B. Fuller Company

- HBK

- Henkel AG & Co. KGaA

- Jowat SE

- MAPEI S.p.A.

- Parker Hannifin Corp

- Pidilite Industries Ltd.

- PPG Industries, Inc.

- Sika AG

- Soudal Group

- Wacker Chemie AG

Recent Industry Developments in Water-borne Adhesives Market

- October 2025: Sika AG opened a USD 45 million water-borne adhesive plant in Suez, Egypt, with 75,000 tons/year capacity to serve North African construction megaprojects.

- June 2025: Henkel AG invested EUR 50 million in its Düsseldorf technology hub to develop latent-reactive PU dispersions targeting 80 °C cure.

- October 2024: 3M, in collaboration with Worthington Enterprises, has introduced Fastbond Pressure Sensitive Adhesive 1049. This new water-based, sprayable adhesive is designed for enhanced application efficiency.

Water-borne Adhesives Market Report Scope and Research Methodology

Market Definition and Coverage

We size the water-borne adhesives market as revenue from formulations that use water as the carrier for polymer dispersions, acrylic, PVA, EVA, styrene-butadiene, and polyurethane, sold to packaging, construction, woodworking, transport, healthcare, and electronics users. Mordor Intelligence tracks demand across five regions within this boundary.

Scope Exclusion: solvent-borne, hot-melt, UV-cured, reactive two-part chemistries, and finished pressure-sensitive tape rolls.

Segments Covered in This Report

- By Resin Type

- Acrylics

- Polyvinyl Acetate (PVA) Emulsion

- Ethylene Vinyl Acetate (EVA) Emulsion

- Polyurethane Dispersions and CR (Chloroprene Rubber) Latex

- Other Resin Types

- By Application

- Flexible Packaging

- Tapes and Labels

- Paper Converting and Graphic Arts

- Laminating and Filmic Structures

- Flooring and Carpeting

- Bookbinding and Publishing

- Non-woven and Hygiene Products

- Others

- By End-user Industry

- Building and Construction

- Paper, Board, and Packaging

- Woodworking and Joinery

- Transportation

- Healthcare

- Electrical and Electronics

- Other End-user Industries

- By Substrate

- Paper and Paperboard

- Plastics and Films

- Wood and Composites

- Metals

- Glass and Ceramics

- Others

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed plant engineers, label converters, flooring installers, and distributors in Asia-Pacific, Europe, the Americas, and the Middle East. Their input on substitution rates, solids, and net prices tightened assumptions before triangulation.

Desk Research

We drew trade data from UN Comtrade, Eurostat, USITC, and China Customs, then overlaid insights from FEICA, TAPPI, and APA. Company 10-Ks, investor decks, and Dow Jones Factiva flagged capacity moves; D&B Hoovers checked revenues. Many additional open sources filled volume and price gaps.

Market-Sizing & Forecasting

We anchor demand through a top-down build: end-use surface area × loading factor × realized price, then adjust for net trade. Supplier roll-ups covering a significant portion of world volume serve as a bottom-up check. Key variables like parcel growth, floor space, vehicle output, VOC timelines, and acrylic-to-PVA spreads feed a multivariate model that indicates a growth rate to the end of the forecast period.

Data Validation & Update Cycle

Dual-analyst reviews flag variances above five percent and trigger fresh calls. We refresh figures each year, with interim tweaks after major capacity shifts or rule changes.

How Mordor Intelligence's Water-borne Adhesives Market Size Compares to Other Published Estimates

Published numbers often diverge because scopes drift and pricing bases vary.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.57 B (2025) | Mordor Intelligence | - |

| USD 38.63 B (2024) | Global Consultancy A | Adds hot-melt & tapes; values at list price |

| USD 34.89 B (2024) | Trade Journal B | Bundles starch binders; no regional discounts |

Because our scope stays tight, our mixed model is tested through real-world interviews, and our refresh cadence is annual, decision-makers receive a baseline that remains transparent, current, and repeatable.

Key Questions Answered in the Report

What is the current value of the water-borne adhesives market?

The market size is estimated at USD 9.08 billion in 2026 and is projected to reach USD 12.23 billion by 2031.

Which region leads global demand?

Asia-Pacific accounts for 40.45% of global revenue and shows the fastest 6.92% CAGR through 2031.

Which resin type is growing fastest?

Polyurethane dispersions are expanding at a 6.71% CAGR due to rising automotive and footwear adoption.

Why are VOC regulations important for adhesive selection?

Caps of 30-50 g/L in major economies effectively eliminate many solvent-borne products, pushing users toward low-emission water-borne chemistries.

How do water-borne adhesives improve vehicle performance?

Replacing 55 pounds of mechanical fasteners with just 2.2 pounds of PU dispersion cuts curb weight and boosts fuel economy by about 3%.

What are the key challenges for water-borne formulations?

Heat-resistance limitations above 120 °C and higher capex for specialized production lines restrict penetration in high-temperature and price-sensitive applications.

Page last updated on: