Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

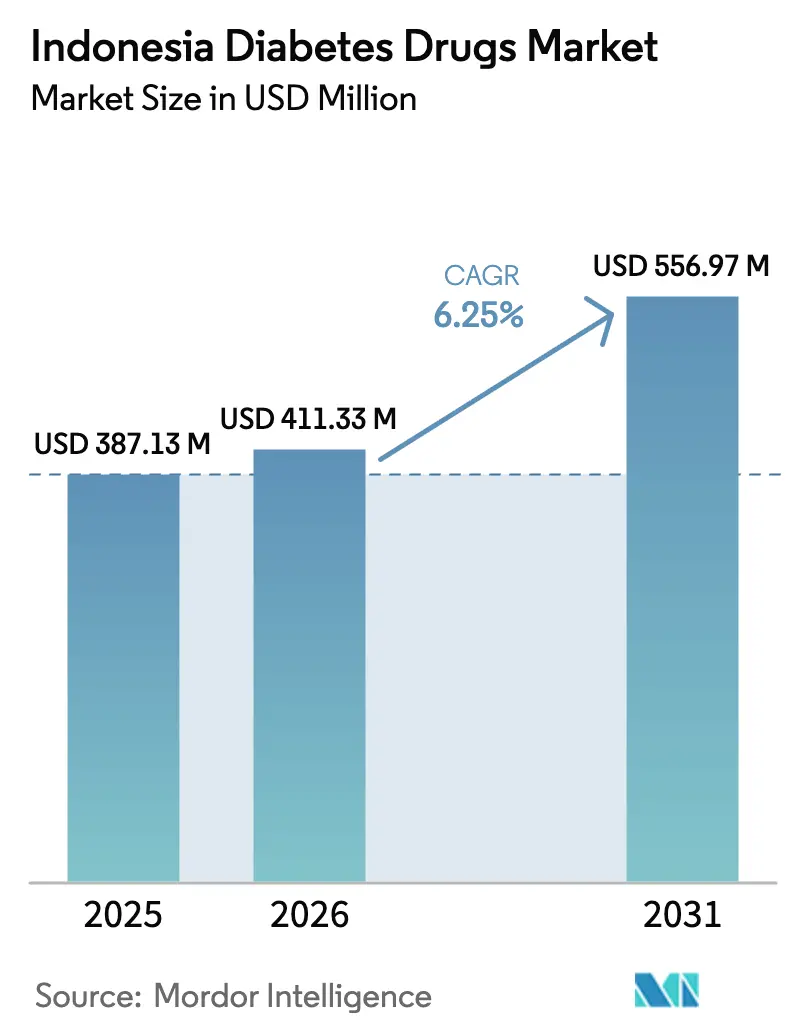

| Base Year Market Size (2025) | USD 387.13 Million |

| Market Size (2026) | USD 411.33 Million |

| Market Size (2031) | USD 556.97 Million |

| Growth Rate (2026 - 2031) | 6.25% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Diabetes Drugs Market Analysis by Mordor Intelligence

The Indonesia Diabetes Drugs Market size was valued at USD 387.13 million in 2025 and is estimated to grow from USD 411.33 million in 2026 to reach USD 556.97 million by 2031, at a CAGR of 6.25% during the forecast period (2026-2031).

Persistent growth rests on a widening patient pool, national health insurance coverage, and policy incentives that reward local packaging over complete import substitution. Demand is reinforced by rising obesity, dietary changes in urban areas, and the pivot toward cardio-renal protection with novel agents. At the same time, reimbursement ceilings and cold-chain gaps temper upside, steering manufacturers to hybrid operating models that combine offshore API supply with on-shore finishing. As a result, the Indonesi diabetes drugs market is evolving toward a dual-tier structure: high-volume generics within the national formulary and premium injectables in private channels.

Key Report Takeaways

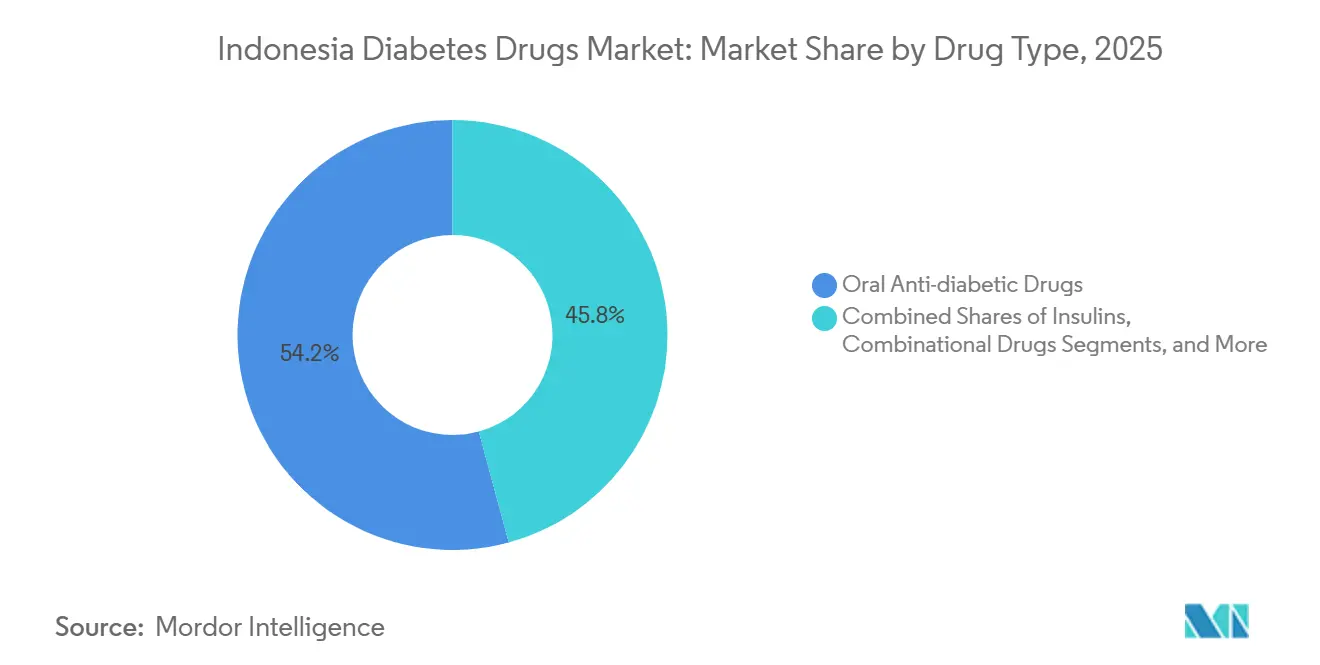

- By drug type, oral anti-diabetic therapies led with 54.22% of the Indonesia diabetes drugs market share in 2025, while non-insulin injectables are advancing at an 8.45% CAGR through 2031.

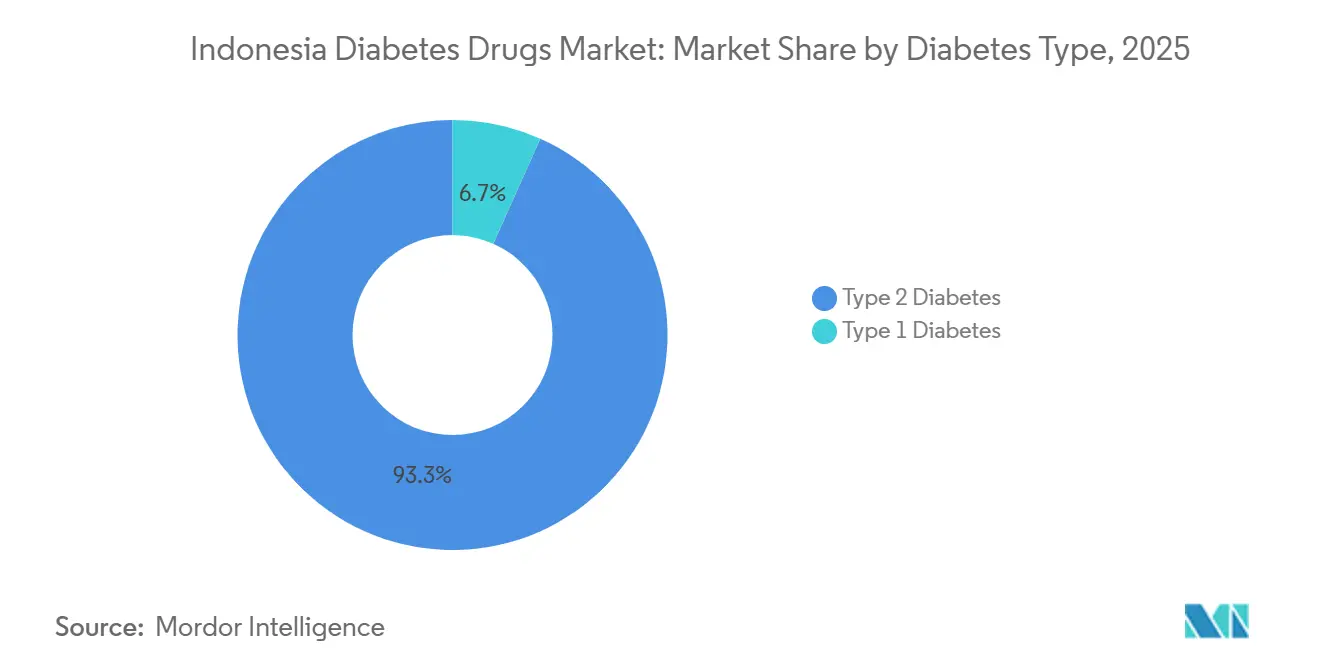

- By diabetes type, Type 2 therapies accounted for 93.30% of the Indonesia diabetes drugs market in 2025 and are forecast to grow at a 7.20% CAGR to 2031.

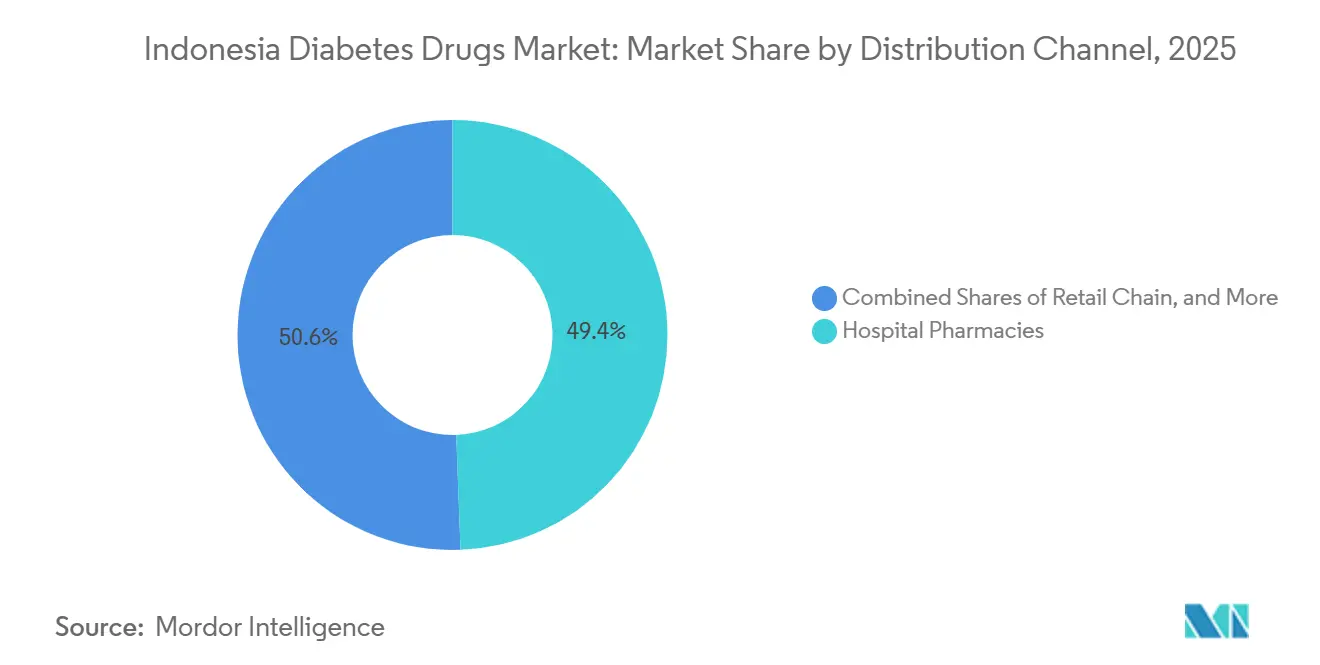

- By distribution channel, hospital pharmacies accounted for 49.40% of revenue in 2025; online pharmacies are set to expand at a 9.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Diabetes Drugs Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Escalating diabetes prevalence & lifestyle shifts | +1.8% | National, with urban concentration in Jakarta, Surabaya, Bandung | Medium term (2–4 years) |

| National health insurance (JKN) expansion improves reimbursement access | +1.2% | National, strongest in Java and Sumatra | Long term (≥4 years) |

| Rapid uptake of novel classes (SGLT-2, GLP-1) for cardio-renal benefits | +1.5% | Urban centers (Java), gradual spill-over to Kalimantan and Sulawesi | Medium term (2–4 years) |

| Domestic insulin manufacturing partnerships | +0.9% | National, with production hubs in West Java | Long term (≥4 years) |

| Tele-pharmacy & digital adherence tools reach remote islands | +0.7% | Eastern Indonesia (Papua, Maluku, Nusa Tenggara), secondary impact in Java | Short term (≤2 years) |

| TKDN & halal-certification incentives spur local production investment | +0.6% | National, policy-driven gains in West Java, East Java | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Escalating Diabetes Prevalence & Lifestyle Shifts

Indonesia’s patient base is growing faster than clinical capacity. A 2024 microsimulation forecast indicates that prevalence will rise from 9.19% in 2020 to 16.09% by 2045, with deaths doubling in the absence of policy change. Obesity climbed to 23.4% in 2023, up from 21.8% in 2018, and a mid-2025 screening campaign revealed central obesity in more than half of adult women. Urban centers such as Jakarta, Surabaya, and Bandung now exhibit entrenched fast-food consumption and sedentary commutes. The International Diabetes Federation projects 28.6 million Indonesians will live with diabetes by 2045, implying steady prescription demand.[2]International Diabetes Federation, “IDF Diabetes Atlas 2025,” idf.org Those demographics underpin the 6.25% CAGR forecast for the Indonesia diabetes drugs market and explain the 8.45% annual growth outlook for GLP-1 receptor agonists.

National Health Insurance Expansion Improves Reimbursement Access

Jaminan Kesehatan Nasional (JKN) enrolled more than 240 million citizens by 2025 and finances essential oral agents and human insulin. Its INA-CBG bundles guarantee volume yet apply price ceilings that squeeze margins. A 2025 WHO audit found that hospital procurement prices exceeded reimbursement caps, forcing facilities to either absorb losses or ration stock.[1]World Health Organization, “Essential Medicines Price and Availability Survey Indonesia 2025,” who.int Still, the program has reduced out-of-pocket spending and stabilized refill adherence, anchoring baseline volume growth in the Indonesian diabetes drugs market. Manufacturers prize formulary inclusion, while premium products such as GLP-1s remain outside JKN and chase private-pay demand.

Rapid Uptake of Novel Classes for Cardio-Renal Benefits

Endocrinologists prioritize cardiovascular and renal endpoints, accelerating SGLT-2 and GLP-1 adoption in metropolitan Java. Glyxambi secured local approval with EMPA-REG mortality data in late 2020. Novo Nordisk introduced Ozempic in March 2024, targeting privately insured patients. Wegovy’s entrance later that year further segmented the injectable space. Real-world Indonesian cohorts confirm comparable cardio-renal benefits across dapagliflozin and empagliflozin, meaning payer access often dictates prescribing. Off-formulary positioning concentrates sales in private hospitals, yet the Indonesia diabetes drugs market still records 8.45% CAGR for non-insulin injectables from a low base.

Domestic Insulin Manufacturing Partnerships

Novo Nordisk’s July 2024 alliance with Bio Farma established local packaging for insulin aimed at 1 million users over 10 years. Kalbe Farma, the nation’s largest drug maker, already licenses Novo formulations. TKDN scoring favors such hybrid models where multinational firms retain API control but perform final assembly locally, lowering tariffs and bolstering tender eligibility. At the same time, the strategy reduces lead-time risk, dependence on imported APIs persists, tempering complete self-sufficiency in the Indonesia diabetes drugs market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Heavy reliance on imported APIs & finished insulin | -0.8% | National, acute in eastern provinces (Papua, Maluku, Nusa Tenggara) | Short term (≤2 years) |

| BPJS price caps compress manufacturer margins | -1.1% | National, most severe for products on Fornas formulary | Long term (≥4 years) |

| Cold-chain gaps outside java hinder insulin distribution | -0.6% | Eastern Indonesia (Papua, South Sulawesi, Maluku) | Medium term (2–4 years) |

| Shortage of endocrinologists limits advanced therapy adoption | -0.9% | National, concentrated impact in Kalimantan, Sulawesi, and outer islands | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Heavy Reliance on Imported APIs & Finished Insulin

Indonesia procures most of its insulin and active ingredients from abroad, exposing the supply chain to currency fluctuations and export curbs. The 2025 WHO survey noted recurring stockouts and procurement costs exceeding reimbursement ceilings in Papua and South Sulawesi, leading to rationing in public hospitals. The Novo Nordisk–Bio Farma deal localizes packaging but not API synthesis, so risk remains embedded in the Indonesian diabetes drugs market.

BPJS Price Caps Compress Manufacturer Margins

E-catalogue ceilings under BPJS reimburse drugs well below global analog benchmarks. Hospitals face negative spreads when purchase prices top INA-CBG rates, curbing uptake of higher-value biologics. Glyxambi, despite outcome-trial backing, remains off-formulary and confined to private facilities. Such pressures bifurcate the Indonesia diabetes drugs market into large-volume generics and niche premium offerings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Injectables Gain Share as Cardio-Renal Evidence Accumulates

Oral therapies dominated the Indonesia diabetes drugs market with 54.22% market share in 2025, anchored by metformin and sulfonylureas, which are reimbursed under JKN. Yet non-insulin injectables are growing fastest, with an 8.45% CAGR. The Indonesia diabetes drug market for GLP-1s is expected to increase sharply as Ozempic and Wegovy penetrate employer plans. Local insulin finishing under the Bio Farma partnership should lower logistics costs, though API dependence persists. Hospital and tele-pharmacy channels increasingly deliver high-cost injectables, while BPJS ceilings confine innovation within oral classes.

The Indonesia diabetes drugs market continues to balance affordability and outcome-driven care. Oral generics stay relevant in rural clinics, but endocrinologists in Jakarta and Surabaya favor GLP-1s for dual glucose and weight control. Cold-chain improvements and TKDN incentives will determine how quickly injectables expand beyond Java. Still, oral combination products such as Glyxambi struggle without formulary inclusion, highlighting the reimbursement bottleneck facing mid-priced innovations.

By Diabetes Type: Type 2 Dominance Reflects Epidemiology, Yet Type 1 Remains Underserved

Type 2 therapies accounted for 93.30% of the Indonesian diabetes drug market share in 2025. Rising obesity and sedentary lifestyles in urban centers drive a 7.20% CAGR for this segment, pushing the Indonesia diabetes drugs market size for Type 2 treatments steadily higher. Cardiometabolic comorbidity favors SGLT-2 and GLP-1 classes, though uptake still hinges on private insurance.

Type 1 patients confront acute access challenges. Insulin stockouts in Papua and Maluku, coupled with a shortage of specialists, limit the adoption of intensive regimens. The Indonesia diabetes drugs market’s growth within Type 1 therefore lags, constrained by cold-chain fragility and the absence of novel non-insulin therapies. Expanded tele-pharmacy programs may eventually narrow that gap.

By Distribution Channel: Online Pharmacies Exploit Logistics Gaps

Hospital pharmacies accounted for 49.40% of sales in 2025, as specialists prescribe complex therapies. Procurement cost pressures, however, incentivize substitution toward cheaper generics. Online pharmacies, growing at a 9.75% CAGR, capitalize on direct-to-patient deliveries that bypass brick-and-mortar bottlenecks, especially for GLP-1 injections that require refrigeration. The Indonesia diabetes drugs market attributable to e-pharmacies is projected to expand rapidly as Halodoc and Alodokter integrate payment, teleconsulting, and logistics.

Community pharmacies rely on chat-based telepharmacy, but regulatory clarity is pending. Once standard rules emerge, the Indonesia diabetes drugs market may see a surge in hybrid models where patients refill online and pick up locally, further diluting hospital dominance.

Geography Analysis

Revenue remains concentrated in Java due to population density and specialist clusters. Jakarta, Surabaya, and Bandung collectively account for the bulk of the Indonesian diabetes drug market. Sumatra follows, with Medan and Palembang seeing rising private-insurance penetration. Nevertheless, access to analogue insulin and GLP-1 outside provincial capitals is patchy, due to price caps and cold-chain limitations.

Kalimantan and Sulawesi exhibit faster patient-growth rates as mining towns urbanize, yet lagging infrastructure curbs the uptake of advanced therapies. An October 2024 audit showed analogue insulin stocked in only 43.2% of private pharmacies, reflecting uneven distribution capacity. The eastern provinces hold the smallest slice of the Indonesian diabetes drugs market but face the widest care gaps.

Digital health platforms now spearhead outreach to Papua, Maluku, and Nusa Tenggara. Halofit’s GLP-1 home-delivery model demonstrates how e-commerce logistics circumvent island supply fractures. For manufacturers, local partnerships with state distributor Kimia Farma, plus digital channels, are essential to penetrate non-Java markets. TKDN scoring and halal mandates further encourage onshore finishing to expand the geographic reach of the Indonesia diabetes drugs market.

Competitive Landscape

The Indonesia diabetes drugs market features a moderately competitive mix of multinational innovators focused on premium injectables, while domestic firms dominate volume generics. Novo Nordisk, Sanofi, Eli Lilly, and Boehringer Ingelheim compete in the analogue-insulin and GLP-1 segments. Indonesian players Kalbe Farma, Kimia Farma, Dexa Medica, and Sanbe Farma dominate the cost-sensitive oral and human insulin space, aided by TKDN preferences.

Local content and halal policies have spurred cross-licensing deals rather than greenfield plants. Novo Nordisk’s tie-up with Bio Farma typifies the approach, securing tender eligibility while retaining API control. Kimia Farma leverages its 1,300-outlet pharmacy network to bundle retail and manufacturing advantages. Online platforms add a new battleground: Halodoc’s partnership with Novo Nordisk aligns GLP-1 delivery with digital coaching, capturing affluent urban users.

Looking ahead, competitive intensity will center on securing formulary listings and digital distribution alliances. Domestic firms may climb the value chain by absorbing packaging technology, while multinationals guard innovation pipelines. The Indonesia diabetes drugs market thus balances price-driven public demand with premium private niches.

Indonesia Diabetes Drugs Industry Leaders

Sanofi

PT Kalbe Farma Tbk

Merck & Co.

Eli Lilly and Company

Novo Nordisk A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Daewoong obtained BPOM approval for Enavogliflozin, expanding SGLT-2 choices.

- October 2025: Halodoc debuted Halofit, a digital weight-management clinic delivering GLP-1 therapies with Novo Nordisk Indonesia; consultations quadrupled from March to September 2025.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study counts every prescription diabetes medicine sold in Indonesia, including insulins, oral anti-diabetics, non-insulin injectables, and fixed-dose combinations, valued at landed price into hospital, retail-chain, and online pharmacies. The classification mirrors Ministry of Health drug codes and excludes any device revenue.

Glucose monitors, nutraceuticals, herbal remedies, and veterinary diabetes drugs remain outside the scope.

Segmentation Overview

- By Drug Type

- Oral Anti-Diabetic Drugs

- Insulins

- Non-Insulin Injectables

- Combination Drugs

- By Diabetes Type

- Type 1 Diabetes

- Type 2 Diabetes

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Detailed Research Methodology and Data Validation

Primary Research

We interviewed endocrinologists, hospital buyers, leading retail pharmacists, and reimbursement officers across Java, Sumatra, and Sulawesi. Their input on dose frequency, discount ladders, and patient mix refined assumptions and checked desk findings.

Desk Research

Mordor analysts gather prevalence and therapy data from Riskesdas surveys, BPJS Kesehatan claims, WHO Global Health Observatory, and Badan Pusat Statistik trade files, then map import volumes through UN Comtrade and adjust rupiah trends with Bank Indonesia bulletins.

Company 10-Ks, budget bills, and journals such as BMC Endocrine Disorders reveal pricing levers and molecule uptake. D&B Hoovers and Dow Jones Factiva enrich revenue splits. The list is illustrative, and many additional open sources fed validation.

Market-Sizing & Forecasting

Our model starts with a top-down prevalence-to-treated-patient build, multiplies by drug share and average daily dose to derive units, and prices these with channel-specific ASPs. Supplier shipment roll-ups and retail audits provide bottom-up sense checks. Drivers such as adult prevalence, insulin initiation rules, GLP-1 listing status, rupiah path, and generic penetration feed a multivariate regression with ARIMA smoothing to project through 2030.

Data Validation & Update Cycle

Outputs face three analyst reviews, and any variance beyond two standard deviations versus import or sales series triggers re-checks with experts. We refresh annually and push interim updates whenever reimbursement or currency swings materially shift the baseline.

Why Mordor's Indonesia Diabetes Drugs Baseline Deserves Trust

Because publishers vary scope, currency methods, and refresh cadence, their numbers diverge.

Our annually renewed, claims-anchored baseline keeps scope tight to prescription drugs and uses rolling FX, yielding steadier figures.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 387.13 m (2025) | Mordor Intelligence | - |

| USD 1.10 b (2024) | Regional Consultancy A | Adds devices and OTC items |

| USD 301.58 m (2024) | Global Consultancy B | Omits non-insulin injectables |

| USD 482.65 m (2023) | Industry Journal C | Uses dated base and fixed FX |

The spread shows inflated totals when devices are bundled and compressed figures when key drug classes are left out or data are dated, whereas Mordor's disciplined blend of audited data and field insight delivers the balanced, repeatable baseline decision-makers need.

Key Questions Answered in the Report

How fast is spending on diabetes drugs rising in Indonesia?

The Indonesia diabetes drugs market is on track to grow at a 6.25% CAGR from 2026 to 2031, lifting value from USD 435.11 million in 2026 to USD 556.97 million by 2031.

Which therapy class is expanding most quickly?

Non-insulin injectables, led by GLP-1 receptor agonists, are advancing at an 8.45% CAGR thanks to combined glucose-lowering and weight-loss benefits.

What share of sales happens through online pharmacies?

Online platforms held a modest slice in 2025 but are forecast to grow at 9.75% CAGR, making them the fastest-rising distribution channel for diabetes drugs.

Why do multinationals package insulin locally?

TKDN local-content rules and halal certification create tender advantages for products finished in Indonesia, prompting firms like Novo Nordisk to partner with Bio Farma for on-shore packaging.

What is the biggest supply-chain challenge outside Java?

Maintaining a 2-8 °C cold chain for insulin across remote islands remains the chief hurdle, leading to periodic stockouts in provinces such as Papua and Maluku.

Page last updated on: