Volatile Organic Compound Gas Sensor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

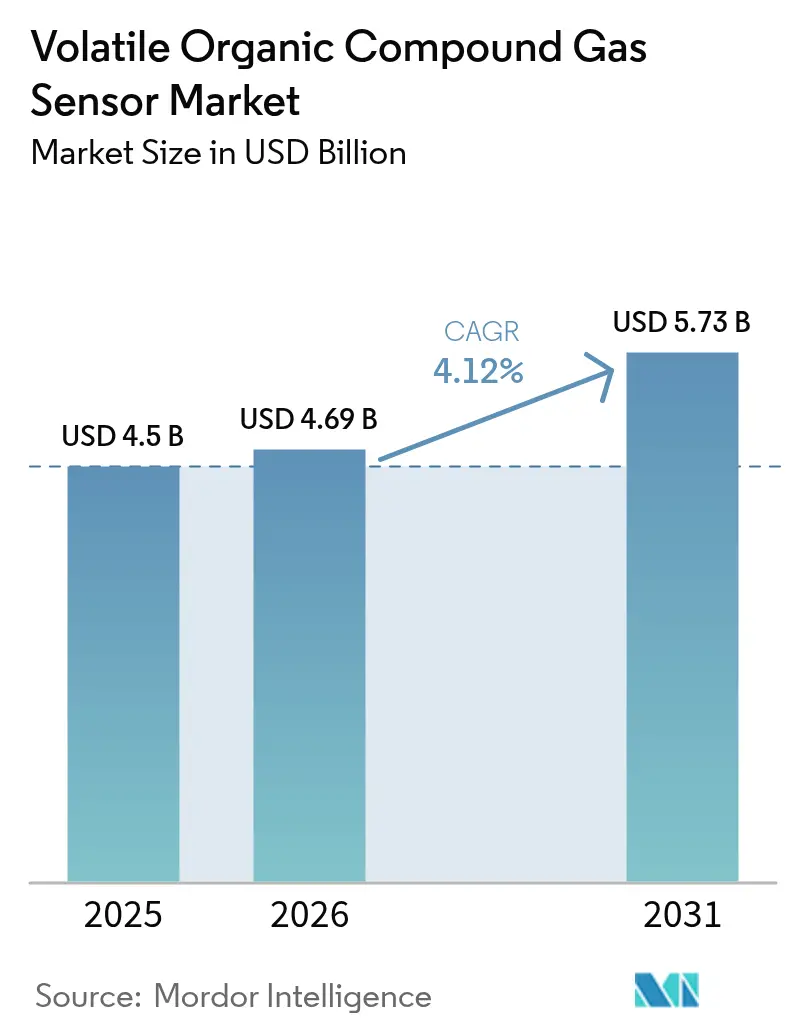

| Market Size (2026) | USD 4.69 Billion |

| Market Size (2031) | USD 5.73 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

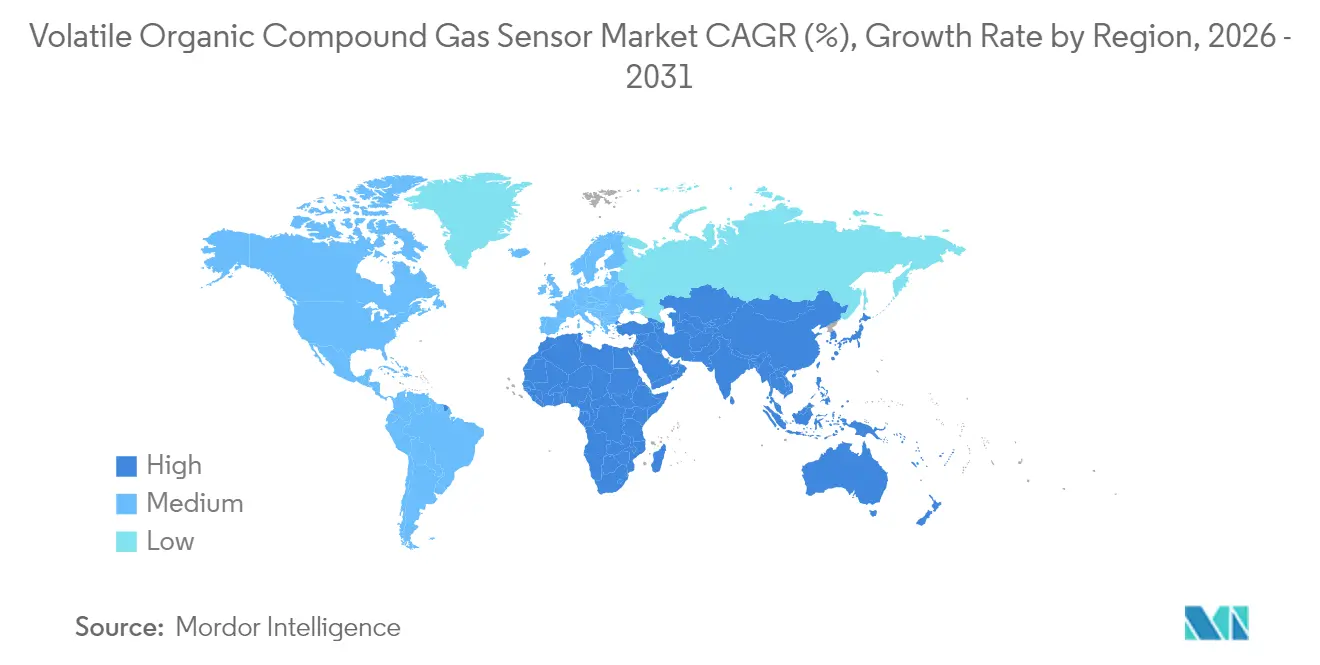

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

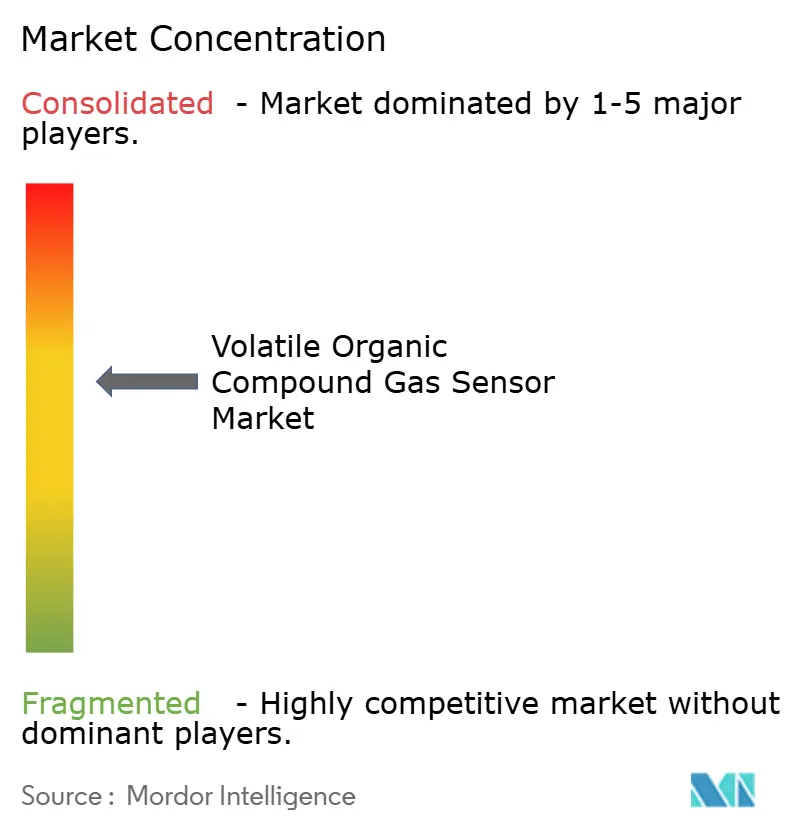

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Volatile Organic Compound Gas Sensor Market Analysis by Mordor Intelligence

The VOC sensors market size is expected to grow from USD 4.5 billion in 2025 to USD 4.69 billion in 2026 and is forecast to reach USD 5.73 billion by 2031 at 4.12% CAGR over 2026-2031. Demand strengthens as indoor-air-quality codes narrow permissible volatile-organic-compound exposure limits, prompting commercial buildings to install continuous monitors. Smart-home hub vendors bundle VOC detection to distinguish premium offerings, while automotive and battery manufacturers rely on rapid-response sensors to detect solvent leakage on electric-vehicle production lines. Low-power micro-electromechanical-system photoionization detectors allow badge-style wearables for industrial staff, and green-building certifications award points for real-time air-quality reporting. These converging trends anchor growth across the VOC sensors market worldwide.

Key Report Takeaways

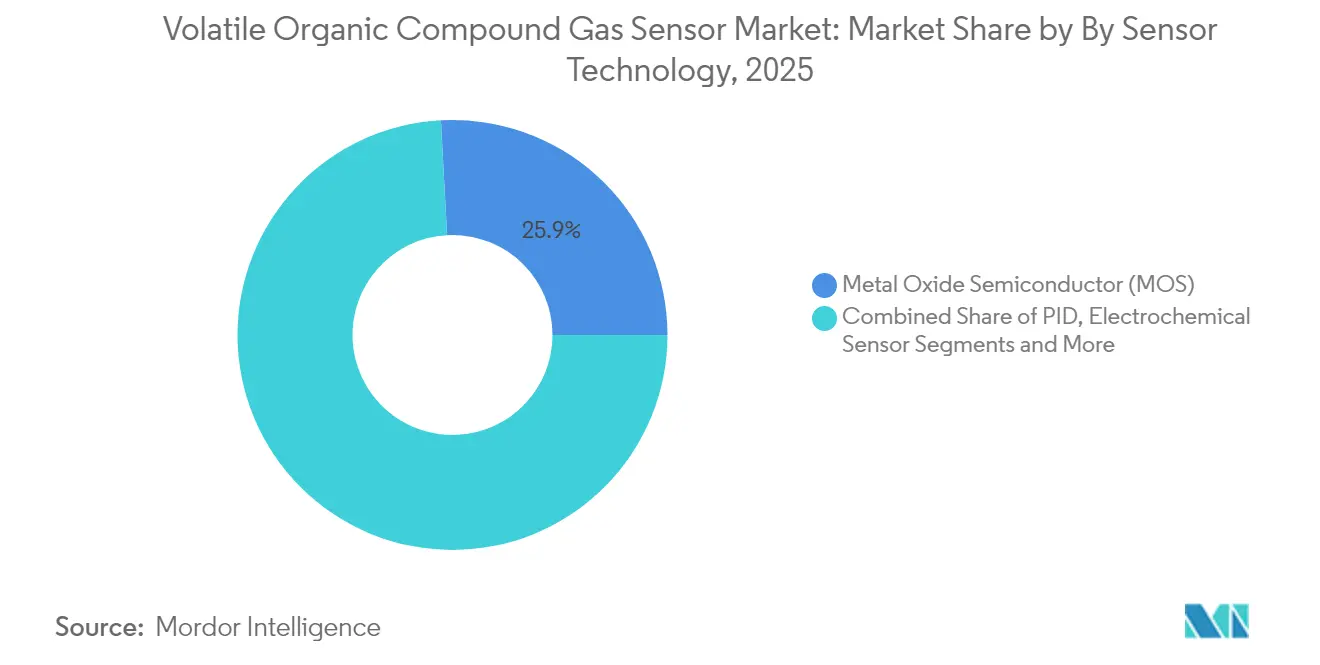

- By sensor technology, metal-oxide-semiconductor devices held a 25.86% revenue share of the VOC sensors market in 2025, whereas photoionization detectors are forecast to grow at a 7.85% CAGR from 2026-2031.

- By device form factor, fixed wall-mounted monitors accounted for 41.12% of VOC sensors market share in 2025; wearable badges are poised to advance at a 9.12% CAGR through 2031.

- By connectivity, wired interfaces such as BACnet and Modbus represented 55.75% of the VOC sensors market size in 2025, while low-power wide-area wireless links are expanding at a 8.70% CAGR to 2031.

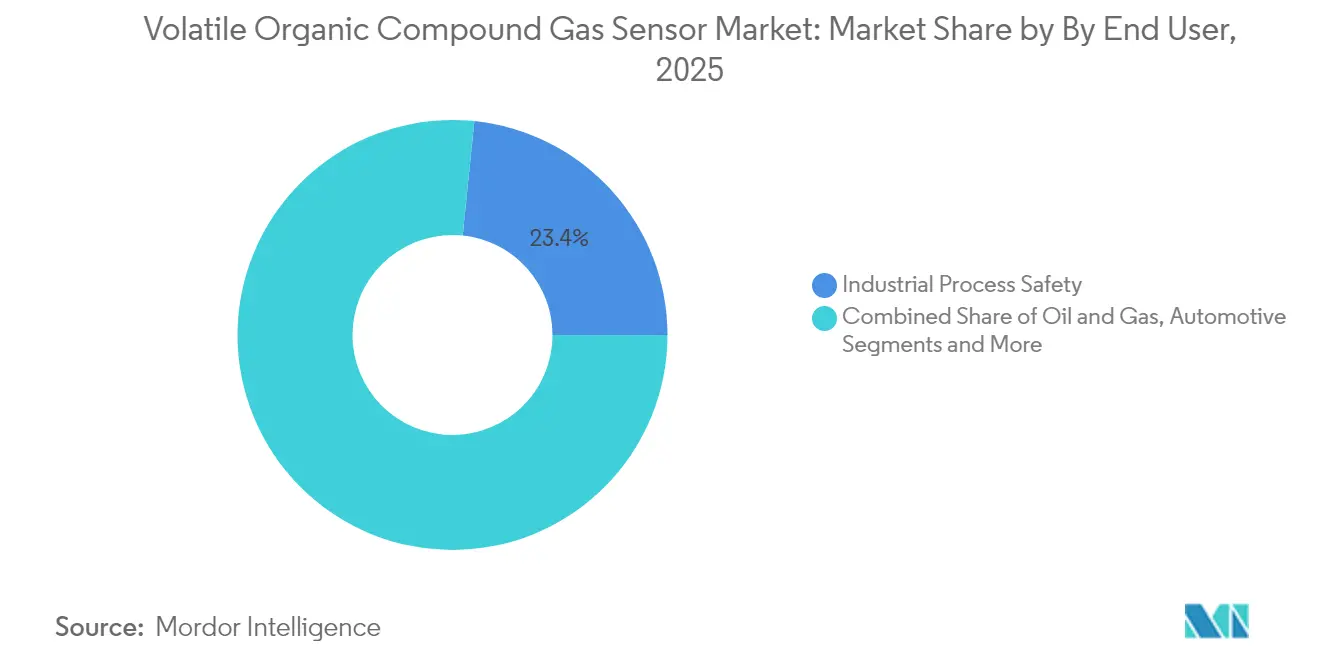

- By end-use industry, industrial process safety comprised 23.38% of the VOC sensors market in 2025; consumer electronics and smart homes are the fastest-growing vertical at an 8.25% CAGR through 2031.

- By geography, Asia-Pacific contributed 31.55% of 2025 revenue; the Middle East and Africa is the fastest-growing region at a projected 8.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Volatile Organic Compound Gas Sensor Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Tightening Indoor Air-Quality Standards across North America & Europe | +1.8 | North America & Europe, with spillover to Asia Pacific | Medium term (~ 3-4 yrs) |

| Integration of VOC Sensors into Smart-Home IoT Platforms | +1.2 | Global, with early adoption in North America & Europe | Medium term (~ 3-4 yrs) |

| Demand from EV Battery Manufacturing Lines in Asia for Solvent-Leak Detection | +0.9 | Asia Pacific, primarily China, South Korea & Japan | Short term (≤ 2 yrs) |

| Adoption of Low-Power MEMS-PID Sensors Enabling Wearable VOC Badges | +1.5 | Global, with strongest uptake in industrial economies | Medium term (~ 3-4 yrs) |

| Green-Building Certification Schemes Mandating Continuous VOC Monitoring | +1.1 | North America & Europe, with emerging impact in Asia Pacific | Long term (≥ 5 yrs) |

| Source: Mordor Intelligence | |||

Stricter Indoor-Air-Quality Standards across North America & Europe

Building owners must demonstrate continuous compliance with tightened exposure limits for formaldehyde, benzene and other VOCs. Bulk procurement of fixed wall-mounted detectors and BACnet gateways supports rapid retrofits in hospitals, schools and transit hubs. Demand concentrates on projects governed by ASHRAE-62.1 and EN-16798 guidelines, anchoring short-term momentum for the VOC sensors market.

Integration of VOC Sensors into Smart-Home IoT Platforms

Voice-assistant hubs and connected thermostats position VOC sensing as a wellness feature. MOS chips drawing less than 20 mW integrate over I²C or BLE, while Matter 1.2 interoperability enables vendor-agnostic pairing. High shipment volumes widen the addressable base and lower unit prices, sustaining medium-term growth for the VOC sensors market.[1]Connectivity Standards Alliance, “Matter 1.2 Specification,” csa-iot.org

Demand from EV Battery Manufacturing Lines in Asia

Gigafactories that coat electrodes with N-methyl-2-pyrrolidone require line-side VOC readings below 5 ppm. Photoionization detector arrays respond within two seconds and integrate with programmable-logic-controller safety loops, underpinning volume expansion across the VOC sensors market in Asia.

Adoption of Low-Power MEMS-PID Sensors Enabling Wearable Badges

MEMS miniaturisation of ultraviolet lamps has slashed power budgets by 70%, enabling coin-cell badges that log personal exposure for eight-hour shifts. Chemical plants now issue the badges to contractors in confined-space entry zones, widening the long-term addressable base for the VOC sensors market.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Calibration Drift of PID Sensors in High-Humidity Climates | ~-0.8 | Southeast Asia, Middle East, tropical regions globally | Short term (≤ 2 yrs) |

| Lack of Harmonised Interoperability Protocols among Sensor Brands | ~-1.2 | Global, with highest impact in commercial building sector | Medium term (~ 3-4 yrs) |

| Price Sensitivity in Mass-Market Smart-Home Segment | ~-0.7 | Global consumer markets, particularly price-sensitive regions | Medium term (~ 3-4 yrs) |

| Supply-Chain Volatility for Semiconductor Sensor Materials | ~-0.5 | Global, with concentrated impact on Asian manufacturing | Short term (≤ 2 yrs) |

| Source: Mordor Intelligence | |||

Calibration Drift of PID Sensors in High-Humidity Climates

PID output can drop 15% in environments above 85% relative humidity as water molecules quench photoionisation. Users incur added costs for compensation algorithms and frequent recalibration, tempering near-term uptake in food-processing plants and pulp mills across Southeast Asia and parts of South America.[2]Singapore National Environment Agency, “Guidelines on Indoor Air Quality,” nea.gov.sg

Lack of Harmonised Interoperability Protocols among Sensor Brands

Although Zigbee, Thread and LoRaWAN exist, payload encoding for VOC indices is not uniform. Integrators must write custom middleware, slowing multi-vendor deployments and moderating the medium-term rollout of large-scale networks within the VOC sensors market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Technology: MOS Leads While PID Accelerates

MOS devices generated 25.86% of revenue in 2025, holding the largest VOC sensors market share because they balance price and performance. Photoionization detectors will post a 7.85% CAGR through 2031, outpacing the overall VOC sensors market. Premium industrial users require sub-3-second response times and wide chemical coverage, driving the VOC sensors market size for PID modules upward. Future MOS roadmaps incorporate multi-pixel arrays for species selectivity, while PID vendors explore graphene windows to reach sub-ppm sensitivity.

Across the MOS segment, falling wafer costs and temperature-modulation algorithms safeguard incumbent share even as niche applications shift to PID or quartz-crystal microbalance designs. Entrants must navigate intellectual-property clusters covering heater-drive patterns, which raise barriers in the VOC sensors market.

By Device Form Factor: Dominance of Fixed Monitors, Momentum for Wearables

Wall-mounted panels captured 41.12% of 2025 revenue and remain core to building-automation retrofits that rely on PoE cabling. Wearable badges post the highest 9.12% CAGR, reflecting regulatory emphasis on personal exposure data in digital logbooks. The VOC sensors market size tied to badges climbs steadily as MEMS-PID designs prove eight-hour battery life.

Portable handheld detectors retain relevance for first responders but cede volume to continuous fixed monitors that support compliance documentation. Multi-parameter IAQ cubes face competition from smart-thermostat OEMs that integrate individual sensors directly onto motherboard daughtercards, yet they still contribute meaningfully to the VOC sensors market.

By Connectivity: Wired Dominates, Low-Power Wide-Area Growing

Deterministic wired links such as BACnet-MS/TP, Modbus-RTU and Ethernet/IP held 55.75% of 2025 revenue. Facility managers reuse existing twisted-pair backbones, ensuring the VOC sensors market share for wired connections remains solid. Low-power wide-area radios—LoRaWAN, NB-IoT and LTE-M—are projected to advance at a 8.70% CAGR. Gateways backhaul encrypted payloads from battery-powered nodes, expanding the VOC sensors market size committed to LPWA architectures.

Wi-Fi and Zigbee are prevalent in smart homes but face congestion in 2.4 GHz bands. Bluetooth Low Energy remains a commissioning tool rather than a telemetry backbone within the VOC sensors market.

By End-use Industry: Process Safety Commands, Smart-Home Surges

Process safety dominated spending with 23.38% of 2025 revenue. Explosion-proof enclosures and SIL-2 certifications elevate unit prices and sustain the VOC sensors market. Consumer electronics and smart-home devices record the fastest 8.25% CAGR, reflecting frequent refresh cycles in connected air purifiers, thermostats and voice assistants.

Healthcare and pharmaceutical plants specify sub-ppm detection thresholds, particularly in aseptic filling suites. Food and beverage producers adopt MOS sensors to monitor ethylene levels, yet price sensitivity limits penetration compared with tightly regulated industries, moderating the VOC sensors market in those facilities.

By Distribution Channel: Direct Sales Prevail, E-commerce Expands

Direct sales dominate explosion-proof and SIL-certified equipment because customers demand turnkey calibration, site-acceptance testing and long-term service contracts. Distributors and value-added resellers support building-automation integrators, whereas e-commerce gains traction for consumer replacement cartridges, reinforcing aftermarket revenue throughout the VOC sensors market.

Geography Analysis

Asia-Pacific contributed 31.55% of 2025 turnover, supported by gigafactory and cathode-active-material capacity expansions in China, Japan and South Korea. PID sensors pair with edge-analytics boxes to meet rapid compliance audits that require real-time dashboards delivered to provincial environmental bureaus. Investments in battery and semiconductor supply chains position Asia-Pacific as the foremost region within the VOC sensors market.

North America benefits from a building-retrofit cycle funded by federal tax credits that subsidize high-efficiency HVAC systems integrating VOC monitoring. Enterprise campuses use LoRaWAN IAQ nodes to track workplace wellness, and Canada’s green-building council awards LEED points for continuous reporting, reinforcing the VOC sensors market.

Europe’s Ecodesign directive pushes manufacturers to disclose VOC performance in use. Fixed monitors maintain acetone vapors below 10 ppm in German automotive paint shops. The Middle East and Africa post the quickest 8.85% CAGR as smart-city pilots in Saudi Arabia and the United Arab Emirates embed IAQ dashboards into municipal command centers, and South African mines trial wearable badges for underground crews, enlarging the regional VOC sensors market.

South America experiences steadier growth. Brazil aligns national exposure limits with ACGIH tables, driving procurement by petrochemical complexes near São Paulo. Mexico’s maquiladora corridor adds low-cost MOS sensors to comply with USMCA environmental clauses, supporting the VOC sensors market across the region.

Regulatory Landscape

Regulation affecting VOC gas sensing demand is shaped by air-quality compliance, emissions monitoring, and chemical-management frameworks across major regions. In the United States, EPA guidance for monitoring programs continues to define target compound lists and quality assurance expectations used by public networks (for example, PAMS VOC guidance and PS-8 for VOC continuous emission monitoring systems were updated in November 2025). This influences how industrial and environmental VOC instrumentation is specified, validated, and calibrated.

In Europe, the consolidated text of REACH (Regulation (EC) No 1907/2006) re-issued in October 2025 reinforces substance-level controls that affect materials selection and declarations across sensor components and finished devices. EPA actions under VOC content rules also signal enforcement posture, including a May 2026 decision denying innovative product exemption applications under the national VOC emission standards framework. That sustains pressure on manufacturers and downstream users to document VOC performance and compliance pathways rather than rely on exemptions.

Value Chain Analysis

The value chain for VOC gas sensors spans specialty inputs (semiconductor wafers, MEMS components, metal oxides, UV sources for PID, packaging and filters), sensor element fabrication and calibration, and assembly into modules and finished devices. Upstream technology choices split between MOS die suppliers focused on high-volume consumer and embedded modules, and PID and other premium technologies oriented to industrial safety and low-ppm detection needs. Midstream participants add signal processing, humidity and temperature compensation, and connectivity stacks (I2C and BLE in embedded modules, BACnet, Modbus, Ethernet, and CAN in building and industrial deployments), then qualify products to customer specifications such as explosion-proof/SIL requirements in process safety.

Downstream, system integrators and OEMs embed VOC sensing into building automation, smart-home platforms, and industrial control environments. In many cases, sensors feed PLC or SCADA architectures that trigger ventilation or abatement control actions. Distribution bifurcates between direct sales with long-term service and calibration support for regulated industrial sites and commercial buildings, and higher-throughput channels for consumer devices and replacement components. Investment and innovation also appear among niche developers expanding multi-gas capabilities, such as VOCSens securing funding in June 2025 to accelerate multi-gas sensing development, reflecting continued specialization alongside scale-driven MOS supply.

Competitive Landscape

The VOC sensors market is moderately consolidated. Sensirion, Bosch Sensortec and Renesas supply more than one-third of MOS die volumes to consumer-electronics manufacturers. Ion Science and Riken Keiki dominate stationary PID equipment for industrial safety, leveraging proprietary ultraviolet lamp designs. ABB integrates optical-fiber VOC modules into its distributed control system portfolio, positioning itself for large oil-and-gas projects.

Strategic moves illuminate competitive positioning. In 2024 Sensirion released the SGP42, which employs on-device neural-network inference to distinguish paint fumes from cooking odors. Bosch Sensortec licensed a carbon-nanotube coating that improves sub-ppm selectivity in high-humidity settings. Siemens added MQTT payload templates to its QAM-2030 IAQ sensor, facilitating cloud integration with MindSphere.

Partnerships shape go-to-market channels. Alphasense bundles LoRa end-nodes with Chinese gateway maker Milesight, while Aeroqual and Kaiterra cross-license calibration curves to accelerate development of multiparameter panels. NevadaNano leverages a US Defense Logistics Agency contract to validate its Molecular Property Spectrometer for hazardous-location approvals, widening its reach within the VOC sensors market.

Cost pressure persists in consumer channels. Amphenol Advanced Sensors outsourced MOS die fabrication to a 200 mm CMOS foundry in Taiwan, cutting cost of goods by 18% during 2025. Figaro Engineering counters with five-year warranty terms and field-replaceable filter caps, sustaining competitiveness in the VOC sensors market.

Volatile Organic Compound Gas Sensor Industry Leaders

Sensirion AG

Bosch Sensortec GmbH

Figaro Engineering Inc.

Amphenol Advanced Sensors (incl. Telaire)

Alphasense Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary whitespace sits in standardized, quantitative VOC measurement and reporting for industrial and building deployments where buyers want results that are comparable across sites and suppliers. The emergence of EN 17628:2022, used as a framework for localization, identification, and quantification of diffuse VOC emissions and cited within BAT-oriented approaches, lifts demand for sensors and systems that move beyond relative VOC indices. Vendors that support repeatable quantification, traceability, and documentation have clearer pathways into procurement.

Protocol and test-method gaps also create room for vendors that package sensors with validated lab and field testing approaches, including region-specific efforts such as the South Coast AQMD VOC sensors laboratory testing protocol that supports more consistent evaluation and procurement. Technology and solution opportunities concentrate on low-power architectures and process-integrated supervision. Academic and technical roadmaps highlight integrated photonic approaches (VIS-NIR photonic gas sensors) being evaluated for real-time indoor air quality and industrial monitoring, while flexible TFT-based sensors using IGZO active layers have demonstrated ultra-low power consumption (reported at 1.2 micro-Watts), which aligns with wearable badges and battery-operated nodes. On the industrial side, standards and local supervision approaches such as Zhejiang Provincial Standard T/EERT 030-2022, which emphasizes condition monitoring across production, treatment, and emission stages, support deployments where VOC sensing is tied to control loops and maintenance actions rather than standalone alarms.

Recent Industry Developments

- July 2026: Sensirion announced global availability of its SEK-SGP4x Evaluation Kit for prototyping SGP40 and SGP41 VOC and NOx sensors in indoor air quality designs. The kit lowers integration friction for OEMs by packaging hardware and tooling around established sensor parts. Faster design-in cycles support higher-volume adoption in smart-home and building-automation product lines.

- May 2025: Sensirion launched the SEN6x sensor platform, an all-in-one environmental monitoring solution that measures multiple parameters including VOCs for smart building applications. Consolidating sensing elements into a platform format simplifies BOM and firmware integration for HVAC and IAQ equipment makers. The move also strengthens platform-style selling where calibration and algorithms become part of the delivered module value.

- June 2024: Bosch Sensortec introduced the BME690, a 4-in-1 MEMS indoor air quality sensor that includes VOC detection alongside volatile sulfur compounds, humidity, temperature, and pressure, with materially lower power consumption than its predecessor. The higher integration level supports smaller, battery-friendly IAQ products and increases the addressable embedded-module footprint. It also raises competitive pressure on discrete-sensor approaches in consumer electronics and compact IAQ monitors.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers devices and sensing elements that detect and measure volatile organic compounds in air and similar environments, and the related hardware value generated from VOC sensing demand across industrial, commercial, and consumer use.

Scope exclusions: We exclude laboratory analytical instruments (such as chromatographs and mass spectrometers), general-purpose gas detectors that are not specified for VOC measurement, and pure software or services sold without VOC sensing hardware.

Segmentation Overview

- By Sensor Technology

- Photoionization Detector (PID)

- Metal Oxide Semiconductor (MOS)

- Electrochemical Sensor

- Optical Fiber Sensor

- Quartz Crystal Microbalance (QCM)

- Others

- By Device Form Factor

- Fixed/Wall-Mounted Monitors

- Handheld/Portable Detectors

- Wearable Badges

- Integrated Multi-Parameter IAQ Monitors

- Embedded Sensor Modules

- By Connectivity

- Wired (BACnet, Modbus, Ethernet, CAN)

- Wireless

- Wi-Fi

- Bluetooth/BLE

- Zigbee/Thread

- LoRaWAN/NB-IoT/LTE-M

- By End-use Industry

- Industrial Process Safety

- Oil and Gas and Petrochemical

- Automotive and Transportation

- Consumer Electronics and Smart Homes

- Commercial Buildings and Offices

- Healthcare and Pharmaceuticals

- Food and Beverage Production

- Academic and RandD Laboratories

- Others

- By Detection Range

- Less than 1 ppm

- 1 - 10 ppm

- 10 - 100 ppm

- Greater than 100 ppm

- By Distribution Channel

- Direct Sales

- Distributor / VAR Channel

- E-commerce

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

To build a clean starting point, we first collected public information that helps explain where VOC sensing is being used and how demand is shifting. Common inputs came from sources such as the US Environmental Protection Agency (EPA), the European Environment Agency (EEA), the World Health Organization (WHO), and the International Energy Agency (IEA), which are useful for emissions context, indoor air quality, and industrial activity signals.

We also reviewed items like public company filings, product datasheets, regulatory and building guidance (including references tied to green building and ventilation), patent databases, and reputable press coverage to understand technology direction and average selling price movement. Where needed, we used paid subscriptions for company financials and intelligence, plus patent databases, to sanity check supplier exposure and innovation intensity. These desk research sources are not exhaustive, and many other public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Next, we validated assumptions through expert interviews and structured surveys with sensor makers, module integrators, channel partners, and end users who buy VOC monitoring for workplace air quality programs and indoor air quality initiatives. Since this is a global market, we balanced feedback across APAC, EMEA, and the Americas so that regional adoption differences and typical pricing patterns could be reflected in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 13% | APAC: 45% |

| Mid tier: 59% | Functional/Unit leaders: 31% | EMEA: 34% |

| Smaller Players: 16% | Managers: 56% | Americas: 21% |

Market-Sizing & Forecasting

Our sizing starts with a top-down build that reconstructs the addressable demand pool using air-quality monitoring deployments and industrial safety rollouts, which are then translated into VOC sensor volumes and value using typical device content and pricing. To keep the totals grounded, we cross-check with selective bottom-up approximations such as sampled supplier revenue splits, channel checks, and a volume times ASP view for key use cases.

Key inputs in the model include indoor air quality adoption in buildings, industrial automation and safety spending signals, emissions and workplace exposure compliance pressure, typical replacement cycles for installed sensors, and expected ASP drift as low-power and miniaturized designs expand into higher volumes. When bottom-up references are incomplete for smaller suppliers or private players, gaps are handled through conservative share and price bands that we review with interview feedback. For forecasting, we use scenario analysis tied to expert views on regulation timing, building retrofit activity, and industrial uptime priorities, and then we run a sensitivity pass to see how changes in adoption and ASP assumptions move the total.

Data Validation & Update Cycle

Each major step is checked through triangulation, where outputs are compared against independent signals like regional industry activity, indoor air quality program momentum, and supplier commentary on shipments and pricing. If a number looks off, we re-check units, currency timing, and the implied volume, and then a second analyst reviews the logic before sign-off.

The report is refreshed annually, and interim updates are triggered when material events occur such as major regulatory changes, supply disruptions, or notable shifts in sensor pricing. Before publication or delivery, a final pass is done to ensure assumptions, conversions, and recent developments are reflected consistently across the model.

Mordor Intelligence's Volatile Organic Compound Gas Sensor Market Size Versus Other Published Estimates

Published estimates for VOC gas sensors can look far apart because the market boundary is not always treated the same way, and the base year can shift between studies. Differences also come from whether the number represents VOC-specific sensing hardware only, or if adjacent gas sensing products and monitoring systems are mixed into the same total.

By tracking deployment indicators and refreshing currency timing and scope rules, Mordor Intelligence keeps the VOC sensor value tied to VOC-specific sensing demand, which can differ from approaches that lean heavily on broad gas-sensing totals or mix in wider detection equipment categories.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.69 B (2026) | |

| Trade Publisher A | USD 0.15 B (2024) | Often scoped as VOC sensor components and select applications only, with a 2024 base year and limited capture of industrial deployments and multi-sensor device content, which can keep the total smaller. |

| Industry Research Outlet B | USD 0.17 B (2025) | Uses a different study window and may focus on stand-alone VOC sensor unit sales, while treating broader gas detector systems and integrated monitoring value inconsistently across regions. |

The spread in the table mainly reflects scope and unit-of-measure choices, not just forecasting style. When the definition is kept consistent and inputs like deployments, replacement cycles, and ASP movement are checked step by step, the final number becomes easier to trace and repeat for planning decisions.

Key Questions Answered in the Report

What is the current size of the VOC sensors market?

The VOC sensors market is valued at USD 4.69 billion in 2026.

How fast will the VOC sensors market grow through 2031?

It is forecast to expand at a 4.12% CAGR, reaching USD 5.73 billion by 2031.

Which sensor technology is gaining the most momentum?

Photoionization detectors are projected to grow at a 7.85% CAGR between 2026 and 2031.

Why are VOC sensors important for EV battery production?

They detect solvent leaks such as N-methyl-2-pyrrolidone in real time, protecting workers and satisfying regulatory audits on electrode-coating lines.

Which region will see the fastest market expansion?

The Middle East and Africa is expected to post the highest 8.85% CAGR due to smart-city and industrial-safety projects.

Are wearable VOC badges a niche or a growth area?

Wearable badges record the highest 9.12% CAGR through 2031, driven by low-power MEMS-PID technology and stricter personal-exposure regulations.

Page last updated on: