Voice Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

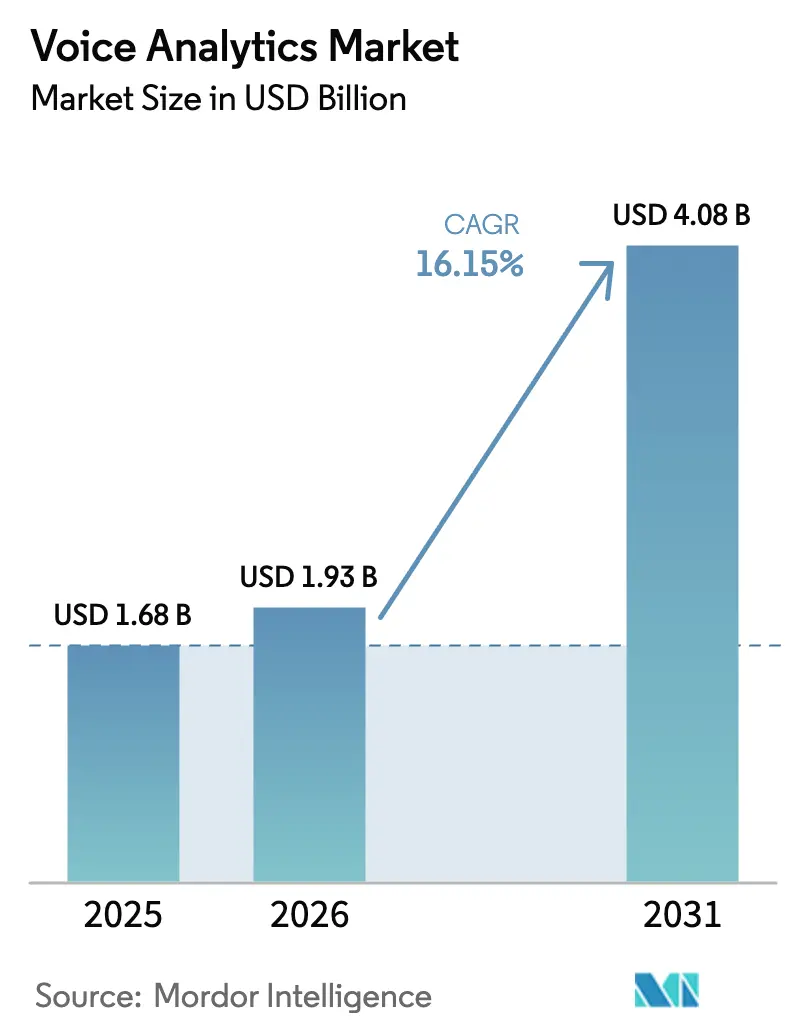

| Market Size (2026) | USD 1.93 Billion |

| Market Size (2031) | USD 4.08 Billion |

| Growth Rate (2026 - 2031) | 16.15% CAGR |

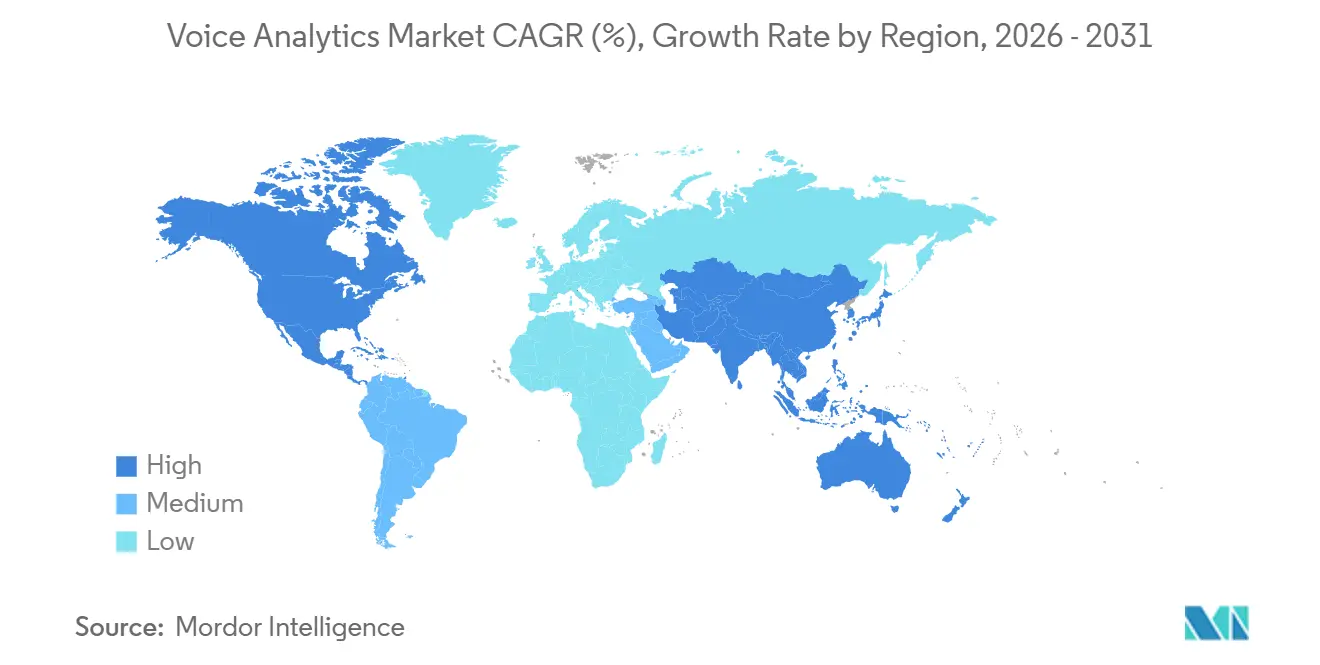

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

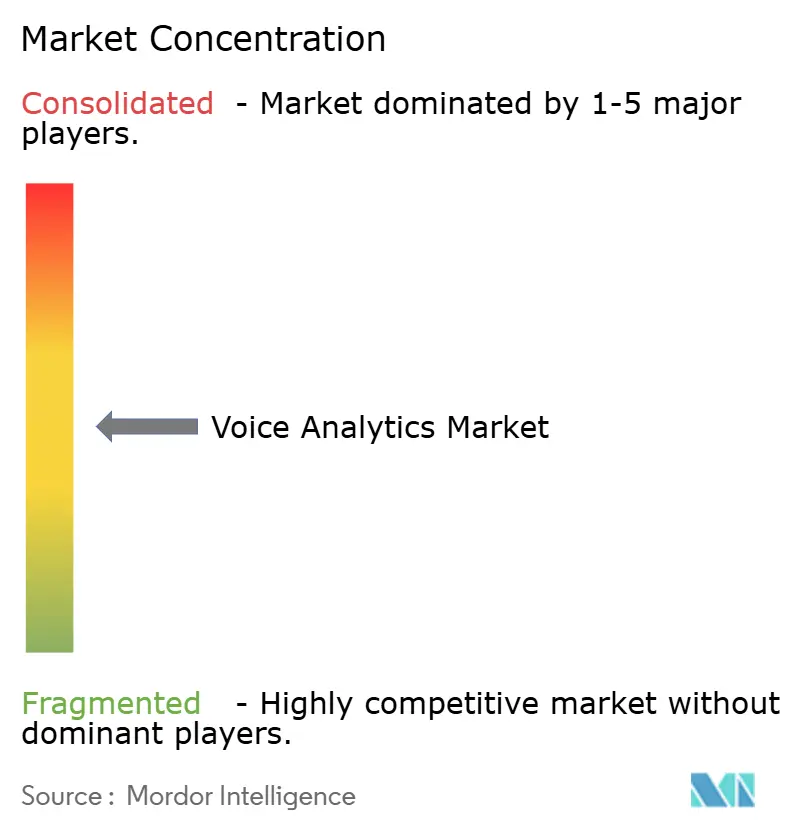

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Voice Analytics Market Analysis by Mordor Intelligence

The voice analytics market size was valued at USD 1.68 billion in 2025 and estimated to grow from USD 1.93 billion in 2026 to reach USD 4.08 billion by 2031, at a CAGR of 16.15% during the forecast period (2026-2031). Rapid migration from legacy on-premise systems to cloud-native contact-center platforms is pulling transcription, sentiment scoring, and compliance monitoring into a single API. Financial-services and healthcare regulations now require searchable archives of every recorded interaction, forcing enterprises to embed analytics at the point of capture. Self-supervised learning is shrinking labeling budgets by up to 70%, letting regional vendors match incumbents on accuracy without vast proprietary datasets. Carbon-efficient model architectures are also emerging as energy costs trigger board-level sustainability mandates across the voice analytics market.

Key Report Takeaways

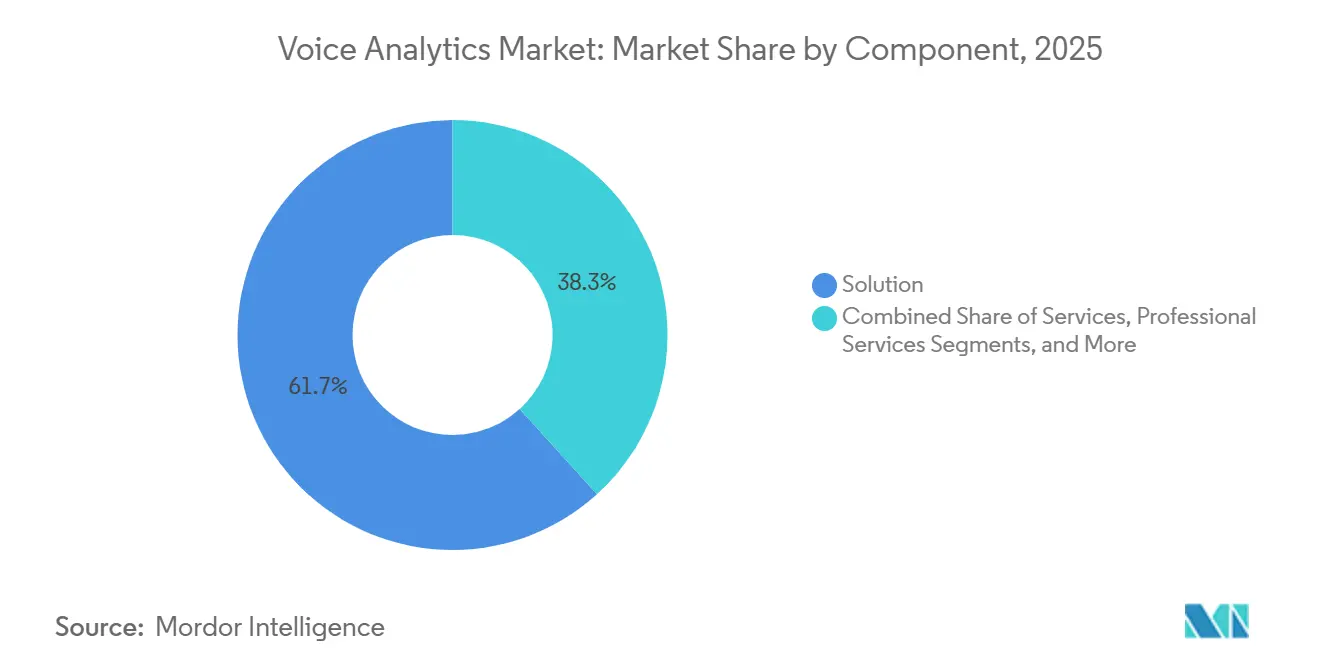

- By component, solutions held 61.73% of voice analytics market share in 2025, while services are projected to expand at a 16.42% CAGR through 2031.

- By deployment mode, cloud captured 70.53% revenue in 2025 and is forecast to advance at a 16.76% CAGR to 2031.

- By organization size, large enterprises led with 57.84% of 2025 revenue; small and medium-sized enterprises are climbing at a 17.13% CAGR.

- By application, call monitoring commanded 30.26% revenue in 2025, yet health monitoring is accelerating at 16.22% CAGR on the back of new reimbursement codes.

- By end-user vertical, banking, financial services, and insurance controlled 26.61% of 2025 revenue, whereas healthcare is pacing the field at a 17.02% CAGR.

- By geography, North America accounted for 40.72% revenue in 2025, while Asia Pacific is on track for a 17.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Voice Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-native Contact-Center Adoption | +2.8% | Global; strongest in North America and Europe | Medium term (2-4 years) |

| Regulatory Mandates for Voice Recording | +2.5% | North America, Europe, Singapore, Hong Kong | Short term (≤ 2 years) |

| Real-time CX Analytics to Reduce Churn | +2.2% | Global; retail and telecom verticals | Medium term (2-4 years) |

| Self-supervised Learning Reducing Labels | +1.8% | Global; rapid uptake in Asia Pacific and Latin America | Long term (≥ 4 years) |

| Speech Emotion AI for Mental-Health Screening | +1.5% | United States, Japan, selected European markets | Long term (≥ 4 years) |

| On-device Federated Learning for Privacy | +1.3% | Europe, China, privacy-conscious enterprises worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud-Native Contact-Center Adoption

Contact-center-as-a-service revenue exceeded USD 7 billion in 2024, and vendors have folded low-latency transcription into their core stacks. Enterprises now spin up compliant voice workflows within weeks instead of months, cutting total cost of ownership by up to 40% over five years. Hyperscalers compete on sub-200-millisecond transcription, and edge-optimized inference endpoints keep the voice analytics market moving toward real-time intervention. The economic case is compelling, ISG Research estimated that cloud-native deployments cut total cost of ownership by 30 to 40 percent over 5 years by eliminating hardware refresh cycles and enabling elastic scaling during peak call volumes.

Regulatory Mandates for Voice Recording Compliance

Fines topping USD 1.1 billion in 2024 underscored that electronic-communication retention is non-negotiable for broker-dealers.[1]U.S. Securities and Exchange Commission, “Enforcement Action on Electronic Communications Preservation,” sec.gov In healthcare, the U.S. Centers for Medicare and Medicaid Services introduced reimbursement codes in 2025 for remote patient monitoring that includes voice-based symptom tracking, provided the platform meets Health Insurance Portability and Accountability Act encryption standards. Similar obligations in Europe and Asia ensure a stable base of mandated demand. As data-sovereignty rules tighten, hybrid architectures that keep raw audio on domestic servers while syncing model updates from the cloud are becoming standard within the voice analytics market.

Real-Time CX Analytics to Reduce Churn and Upsell

Telecom operators that escalated negative-sentiment calls within 30 seconds cut churn by up to 20% in 2024. Retailers are applying similar logic to sales calls; Talkdesk introduced an AI-powered retail assistant in November 2024 that listens for buying signals such as product comparisons or budget mentions, then surfaces personalised offers from the CRM in real time. Standardized KPIs released by the International Telecommunication Union in 2025 have improved multivendor interoperability, adding momentum to deployment pipelines.

Self-Supervised Learning Minimizing Labeling Needs

Pre-training on unlabelled audio delivers competitive accuracy with a fraction of annotated data, slashing budgets by 60-70%.[2]arXiv, “Self-Supervised Learning for Speech Recognition,” arxiv.org Researchers at Meta published wav2vec 2.0 results in 2024 showing that pre-training on 53,000 hours of unlabelled Libri-Light data, then fine-tuning on just 10 minutes of labelled speech, achieved word-error rates competitive with models trained on 100 hours of fully annotated data. Regional vendors can therefore build dialect-robust models for low-resource languages, widening participation in the voice analytics market and eroding incumbent data moats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Privacy and Surveillance Concerns | -1.9% | Global; acute in Europe and privacy-conscious enterprises | Short term (≤ 2 years) |

| High Integration and License Costs for SMEs | -1.6% | Latin America, Africa, Southeast Asia | Medium term (2-4 years) |

| Dialect and Acoustic Variability | -1.4% | Asia Pacific, Africa, Latin America | Long term (≥ 4 years) |

| Carbon Footprint of Large Speech Models | -1.2% | Global; regulatory pressure in European Union and California | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Surveillance Concerns

Voice recordings qualify as biometric data under the General Data Protection Regulation, requiring explicit opt-in consent and short retention windows.[3]General Data Protection Regulation, “Article 9 Biometric Data,” gdpr-info.eu The U.S. Telephone Consumer Protection Act prohibits recording calls without prior consent in 11 two-party-consent states, complicating multi-state deployments and exposing enterprises to class-action litigation if consent workflows fail. Privacy-advocacy reports have highlighted cases in which emotion detection influenced employee evaluations without transparent review, prompting companies to roll out dashboards that explain why a given alert was triggered.

High Integration and License Costs for SMEs

Typical enterprise list pricing can exceed USD 300 per agent per month once real-time sentiment and compliance modules are enabled. Custom connectors to legacy customer-relationship-management systems often cost SMEs USD 25,000 to USD 63,000, delaying payback cycles. Usage-based and freemium tiers are emerging, yet limited IT resources and bandwidth constraints in emerging markets remain hurdles for broad SME participation in the voice analytics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain as Customization Complexity Rises

Solutions generated 61.73% of 2025 revenue, but professional and managed services are forecast to grow at a 16.42% CAGR through 2031 as enterprises outsource dialect tuning, model monitoring, and compliance workflows. The voice analytics market size for managed services is projected to widen as vendors bundle quarterly retraining, assuring minimum word-error-rate thresholds.

Commoditization pressure is mounting on stand-alone speech engines because hyperscalers now offer transcription for USD 0.015 per minute.Voice biometrics modules are gaining traction in banking; the module authenticates callers by analysing 100-plus vocal characteristics-pitch, cadence, formant frequencies-eliminating the need for security questions and cutting average handle time by 30 to 45 seconds per call. Consequently, vendors pivot toward outcome-based contracts that guarantee accuracy, driving a higher share of value toward services. Verint’s professional-services backlog surpassed USD 200 million in 2024, a signal that services revenue is becoming critical inside the voice analytics market.

By Deployment Mode: Cloud Dominance Expands with Edge Inference

Cloud held 70.53% of revenue in 2025 and is projected to rise at a 16.76% CAGR to 2031. Automatic scaling, GPU-optimized inference, and weekly model updates make cloud the default for most buyers, while edge appliances handle low-latency preprocessing. Hybrid offerings such as AWS Outposts preserve on-premise data residency but sync model weights from the cloud, satisfying regulatory demands without ceding elasticity.

On-premise remains relevant for defense and highly regulated finance, yet its voice analytics market share declines yearly as capital-expenditure budgets tighten. China's data-localisation laws favour on-premise or domestic-cloud deployments; the Cyberspace Administration of China mandates that voice data collected within the country remain on servers physically located in China, benefiting local vendors such as iFlytek over multinational platforms. Studies of European telecom carriers found cloud contact centers delivered 22 fewer hours of downtime per 1,000 agents, reinforcing the reliability argument.

By Organization Size: SME Adoption Accelerates on SaaS Pricing

Large organizations controlled 57.84% of 2025 revenue, leveraging complex integrations and stringent service-level agreements. SMEs, however, are forecast to grow at a 17.13% CAGR, the highest among all segments. Entry-level tiers price below USD 100 per agent per month, and self-service onboarding compresses deployment timelines from months to days, broadening the voice analytics market.

Freemium models convert proof-of-concept users to paid plans once call volume scales, while vertical templates reduce integration effort. Nevertheless, connectivity gaps and limited local IT talent continue to dampen uptake in parts of Africa and Southeast Asia.

By Application: Health Monitoring Surges on Reimbursement Codes

Call monitoring remained the largest revenue generator at 30.26% in 2025. Health monitoring is forecast to expand at a 16.22% CAGR through 2031, buoyed by U.S. and Japanese reimbursement codes that compensate providers for voice-based remote patient monitoring. The voice analytics market size for clinical documentation is therefore set to widen quickly as electronic health-record integrations mature.

Sales and marketing teams use speech analytics to surface objection-handling patterns; a 2024 study in the International Research Journal of Modernization in Engineering Technology and Science found that AI-driven sales coaching lifted conversion rates by 8 to 12 percent by flagging missed buying signals and suggesting alternative pitches. Compliance audits automate keyword checks mandated by financial regulators, cementing the application stack as enterprises move from sampling to 100% call coverage.

By End-User Vertical: Healthcare Outpaces BFSI Growth

Banking, financial services, and insurance generated 26.61% of 2025 revenue due to mandatory record-keeping. Healthcare, however, is growing at 17.02% CAGR as ambient clinical-documentation tools reduce physician burnout and raise coding accuracy. The voice analytics market size within hospitals and outpatient networks is thus on a steep ascent.

Retail and e-commerce applications focus on omnichannel sentiment analysis, tracking customer emotion across phone, chat, and social media to predict churn and personalise offers. Government deployments focus on emergency-call triage and intelligence analysis, though budget cycles can elongate procurement. BFSI remains the largest vertical due to its combination of regulatory obligation, high transaction values that justify per-call analytics costs, and mature contact-centre infrastructure, yet healthcare's faster growth signals a long-term shift toward clinical and wellness applications.

Geography Analysis

North America held 40.72% of 2025 revenue. Two-party-consent laws in 11 U.S. states drive granular consent workflows, and Financial Industry Regulatory Authority rules require six-year call retention, locking in demand. Hyperscaler innovation pipelines are headquartered in the United States, and new telehealth reimbursement codes turn clinics into early adopters. Mexico’s bilingual near-shoring boom is also lifting Spanish-English analytics demand.

Asia Pacific records the fastest growth at a 17.93% CAGR to 2031. India’s Bhashini project is seeding open-source speech models for 22 languages, while Japan’s policy paper on aging prioritizes speech interfaces for elder care. Provincial subsidies in China favor domestic speech engines due to strict data-localization rules, and Southeast Asia’s mobile-first economies pilot low-bandwidth deployments for micro-finance and agricultural advisory.

Europe benefits from a clear compliance framework under the General Data Protection Regulation and the pending AI Act. Emotion-detection systems fall under high-risk classification, prompting on-premise or private-cloud rollouts with explainability layers. Middle East sovereign-wealth funds co-invest in Arabic dialect models, and emerging African contact centers favor on-premise appliances because of connectivity limits, yet market-entry barriers are falling as bandwidth improves.

Regulatory Landscape

Regulation for voice analytics is tightening around biometric processing, AI transparency, and telecom consumer-protection rules, raising the compliance bar for call recording, transcription, sentiment, and voice biometrics. In the European Union, Regulation (EU) 2024/1689 (AI Act) sets harmonized obligations for AI systems and increases requirements for certain biometric and emotion recognition use cases in voice processing, pushing vendors toward clearer disclosures, documentation, and risk controls.

In 2026, telecom and privacy regulators added operational requirements that affect voice capture and monitoring workflows. The Telecom Regulatory Authority of India (TRAI) issued a February 2026 direction requiring access providers to use AI/ML to detect and flag suspected unsolicited commercial communications within two hours via a distributed ledger technology (DLT) platform, reinforcing demand for real-time analytics and verifiable logs. New Zealand issued the Biometric Processing Privacy Code 2025, with a transition period ending 3 August 2026, and the US FCC proposed rules in September 2024 to define AI-generated calls and strengthen AI-enabled detection and blocking under the TCPA, which collectively increases the need for consent, auditability, and governance across deployments.

Value Chain Analysis

The value chain starts with audio capture and telephony and contact-center platforms (CCaaS, UCaaS, recording, and session services), then moves to speech-to-text and language models (often sourced from hyperscalers or specialized speech vendors). From there, the analytics layer performs sentiment and emotion scoring, topic discovery, compliance monitoring, and fraud and biometric checks. Value increasingly concentrates in orchestration and integration, including connectors into CRM, workforce engagement, case management, and industry systems, supported by professional services for domain tuning, policy configuration, and continuous model monitoring.

Downstream, distribution and deployment are shaped by channel partners, BPOs, and public-sector procurement vehicles, with partnerships used to bundle complementary capabilities and accelerate adoption. Teleperformance partnering with Sanas (February 2025) aimed to bring real-time speech understanding into CX operations, while Daon partnering with CallMiner (April 2025) targeted biometric identity verification and liveness detection within conversation intelligence. Clearspeed partnering with Carahsoft (May 2025) also targeted government buyers through vehicles such as NASA SEWP V and NASPO ValuePoint. In regulated finance, SteelEye partnering with Intelligent Voice (June 2024) shows how compliance surveillance and voice transcription and analytics are packaged together to meet retention and supervisory expectations.

Competitive Landscape

The voice analytics market is moderately concentrated; the top five vendors held roughly 55-60% revenue in 2025. NICE and Verint maintain strongholds in regulated verticals with turnkey compliance integrations. Hyperscalers undercut independent software vendors on price by embedding transcription in broader customer-experience suites, pressuring margins.

Disruptors such as Uniphore, which raised USD 400 million by late 2025, offer self-supervised toolkits that reduce domain-adaptation cycles to five days, appealing to fast-moving enterprises. SentinelOne’s purchase of Pindrop in 2024 shows convergence between voice biometrics and cybersecurity, opening a lane for fraud-detection suites that authenticate in two seconds.

Differentiation centers on multilingual accuracy, sub-200-millisecond latency, and explainable AI dashboards that satisfy Article 22 of the General Data Protection Regulation. Vendors achieving ISO 27001, SOC 2 Type II, and Health Insurance Portability and Accountability Act compliance command premium pricing, though audit timelines are shortening, lowering the moat for newcomers.

Voice Analytics Industry Leaders

NICE Ltd

Verint Systems

Genesys Cloud Services, Inc.

Callminer Inc.

Uniphore Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity is the shift from post-call analytics to low-latency, agentic self-service and real-time intervention, which expands spend from quality monitoring into automated resolution, workflow execution, and governance. Product activity in 2026 reflects this transition, with Microsoft making real-time voice agents generally available in Copilot Studio for Dynamics 365 Contact Center (April 2026), Five9 launching a new release of Voice AI Agents with an AI Agent Studio for governance (June 2026), and NICE repositioning CXone around agentic AI while introducing its Workforce Empowerment Suite to manage human employees alongside AI agents (June 2026). These launches create whitespace for vendors that can deliver sub-second transcription plus action orchestration across CRM, ITSM, and back-office systems, while maintaining auditable policies for regulated buyers.

Compliance-driven modernization also supports demand for vendors that can operationalize biometric and AI transparency requirements without slowing deployment timelines. The EU AI Act (Regulation (EU) 2024/1689) and its requirements for high-risk use cases and transparency increase buyer attention on explainability layers, human-in-the-loop review, and defensible audit trails for emotion and sentiment and biometric functions, while New Zealand’s Biometric Processing Privacy Code 2025 transition ending 3 August 2026 pushes privacy-by-design controls for biometric voice use. In parallel, security and fraud prevention tied to the voice channel is becoming a purchase criterion, as shown by Krisp’s June 2026 introduction of Voice Security and Speech Analytics capabilities for contact centers, indicating budget allocation toward governance, policy enforcement, and risk scoring integrated directly into voice workflows.

Recent Industry Developments

- July 2026: NICE extended its AI-powered customer experience solution to the AWS European Sovereign Cloud, positioning its platform for regulated customers with stricter data residency and sovereignty requirements. The update strengthens deployment options for voice analytics and agentic CX workloads across Europe where buyers increasingly demand controlled hosting environments.

- June 2026: Verint launched four agentic AI-powered products, including Workforce Intelligence, Desktop Intelligence, Quality Intelligence, and Verint Agent Factory, expanding beyond classic speech analytics into outcome orchestration. This broadens competitive differentiation around real-time guidance, automation, and governance capabilities built on conversation data.

- March 2024: Verint expanded its contact center business analytics suite with Verint Genie Bot, adding automation and analytics features that use conversation context to improve agent and supervisor workflows. The release reinforced bundling analytics with operational tooling, making it easier for enterprises to embed insights into day-to-day contact center execution.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers software and related services that help organizations capture voice interactions (live or recorded), convert speech into usable text, and then analyze it for insights such as sentiment, compliance, and agent performance.

Scope exclusions: We exclude microphone and telecom hardware, generic voice-user-interface stacks, and standalone speech-to-text engines that are sold without an analytics layer.

Segmentation Overview

- By Component

- Solution

- Speech Analytics Engine

- Voice Biometrics Module

- Dashboards and Reporting

- Services

- Professional Services

- Managed Services

- By Deployment Mode

- On-Cloud

- Premise

- By Organization Size

- Small and Medium-sized Enterprises

- Large Enterprises

- By Application

- Health Monitoring

- Sentiment Analysis

- Sales and Marketing

- Risk and Fraud Detection

- Call Monitoring

- Compliance Audit

- By End-User Vertical

- Retail and E-commerce

- Telecom and IT

- BFSI

- Healthcare

- Government and Defense

- Other End-User Verticals

- Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to build the demand context and to check how quickly adoption is moving across regions and end users. For voice analytics, we start by tracking contact center activity, workforce trends, and digital adoption using public references such as the US Bureau of Labor Statistics, the US Census Bureau, OECD digital economy indicators, and ITU telecom statistics.

We also review sources such as SEC filings and investor presentations of public companies, regulator publications that shape call recording and retention, association websites, and reputed press coverage of contact center modernization. Where helpful, we used paid subscriptions for company financials and news, patent databases to track speech and NLP themes, and an import-export shipment-level database for select enabling infrastructure signals. These desk sources are illustrative only, and we checked additional references for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to translate the desk view into realistic sizing assumptions, with a focus on pricing, adoption rates, and what buyers count as a voice analytics deployment versus a bundled speech feature. We spoke with solution providers, channel and implementation partners, and enterprise users across APAC, EMEA, and the Americas, so we could compare regional buying patterns, compliance needs, and rollout timelines, then reconcile them into one consistent model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 21% | APAC: 42% |

| Mid tier: 48% | Functional/Unit leaders: 30% | EMEA: 31% |

| Smaller Players: 22% | Managers: 49% | Americas: 27% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where enterprise and contact center voice-interaction volumes are reconstructed by region, then filtered through recorded-call penetration and analytics adoption rates, before being converted to revenue using typical pricing constructs. We then corroborate results with selective bottom-up approximations, such as sampled supplier revenue splits, channel checks on typical contract sizes, and a volume times ASP view (per seat or per minute) for common deployments.

Variables that materially influence the model include cloud contact center penetration, share of interactions recorded and searchable, retention and compliance intensity (which affects storage and analytics usage), average seats or minutes covered per deployment, and packaging changes that shift spend from stand-alone analytics into broader customer experience bundles. When bottom-up inputs are incomplete, we handle gaps through conservative ranges and by separating recurring software subscriptions from implementation and ongoing support, so double counting is avoided.

For forecasting, we use scenario analysis anchored on expert expectations for cloud migration, compliance-driven recording, and adoption by large enterprises versus mid-sized users. We also smooth the annual path so adoption curves do not jump unrealistically from one year to the next.

Data Validation & Update Cycle

Outputs are checked against independent signals so that outliers are caught early, for example when revenue per seat drifts outside interview-backed ranges or when regional totals exceed plausible cloud readiness. A second analyst reviews model logic and key assumptions, and re-contact triggers are used when a core input moves outside its expected band, such as a pricing reset, packaging changes, or a shift in the deployment mix.

Reports are refreshed annually, with interim updates when material events can shift demand. This includes changes to call recording rules, new compliance expectations, or platform shifts that change implementation effort and the recurring revenue mix. Before delivery, we complete a final pass so clients receive an updated view based on the latest public and primary signals.

Mordor Intelligence's Voice Analytics Market Size Measured Against Other Published Estimates

Published market sizes for voice analytics can differ even when the growth direction looks similar, mainly because the counted revenue streams are not the same and the base year is not aligned. Pricing treatment also matters, because voice analytics is often purchased as part of broader contact center and customer experience bundles.

Some external totals look larger because they appear to include broader speech technology revenues, such as stand-alone transcription engines and adjacent platform layers that are not always sold as analytics. In contrast, the tally for Mordor Intelligence counts voice analytics solutions and related services only when they are tied to analyzing voice interactions for use cases like sentiment, compliance, and agent performance, and it excludes pure speech-to-text sold without analytics.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.68 B (2025) | |

| Global Research Publisher A | USD 1.48 B (2024) | Uses an earlier base year and a narrower revenue capture that emphasizes call monitoring and selected risk uses, which can understate uplift from newer cloud-packaged analytics subscriptions. |

| Industry Research Publisher B | USD 4.16 B (2025) | Uses a wider product scope that appears to fold in adjacent speech technology and platform revenues, which can inflate totals when transcription and enabling layers are counted alongside analytics. |

The table indicates that the biggest spread comes from scope and base-year timing rather than a dispute on adoption direction. By tying the revenue build to measurable signals like recorded interaction intensity, cloud contact center penetration, and interview-validated price bands, the sizing remains transparent and repeatable across regions.

Key Questions Answered in the Report

What CAGR is projected for the voice analytics market from 2026-2031?

The market is forecast to expand at a 16.15% CAGR over 2026-2031.

Which component segment is growing fastest?

Services, covering consulting and managed operations, is projected to rise at a 16.42% CAGR.

Why is healthcare adopting voice analytics so rapidly?

New reimbursement codes for remote patient monitoring and ambient clinical documentation are propelling 17.02% CAGR growth in healthcare.

How dominant is cloud deployment within the sector?

Cloud accounted for 70.53% revenue in 2025 and is advancing at a 16.76% CAGR as enterprises favor elasticity and weekly model updates.

Which region will grow the quickest through 2031?

Asia Pacific is expected to record the fastest growth at a 17.93% CAGR, supported by language-localization projects and demographic shifts.

Page last updated on: