Voice-over Wi-Fi (VoWiFi) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

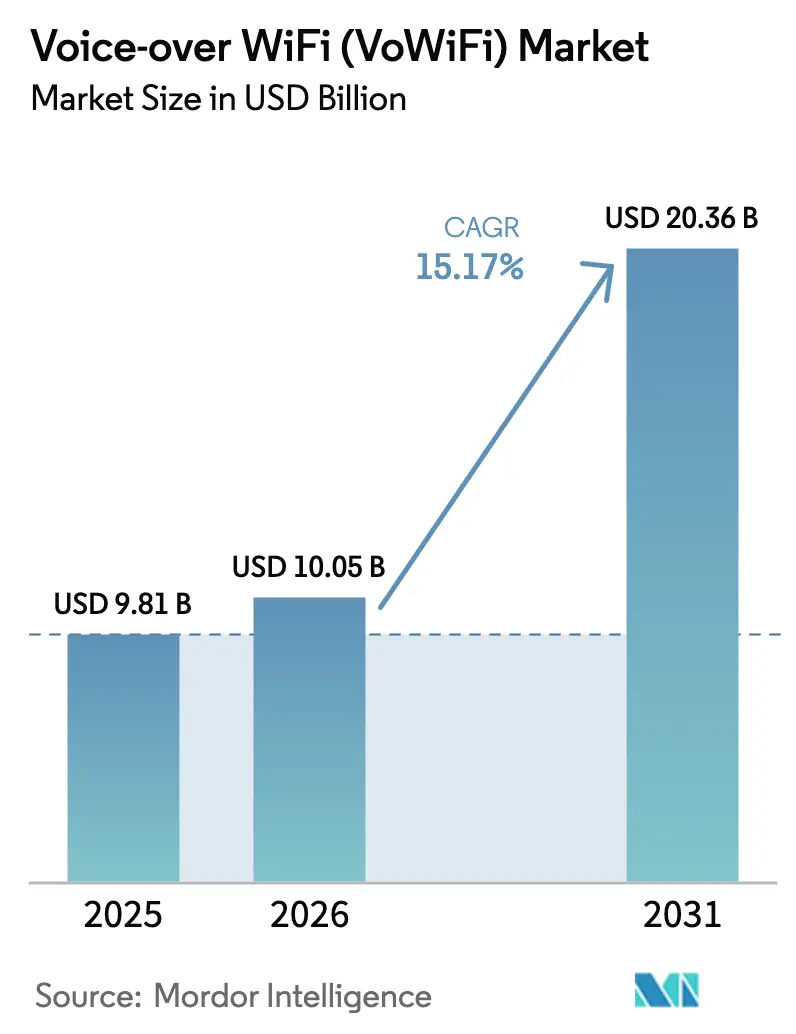

| Market Size (2026) | USD 10.05 Billion |

| Market Size (2031) | USD 20.36 Billion |

| Growth Rate (2026 - 2031) | 15.17% CAGR |

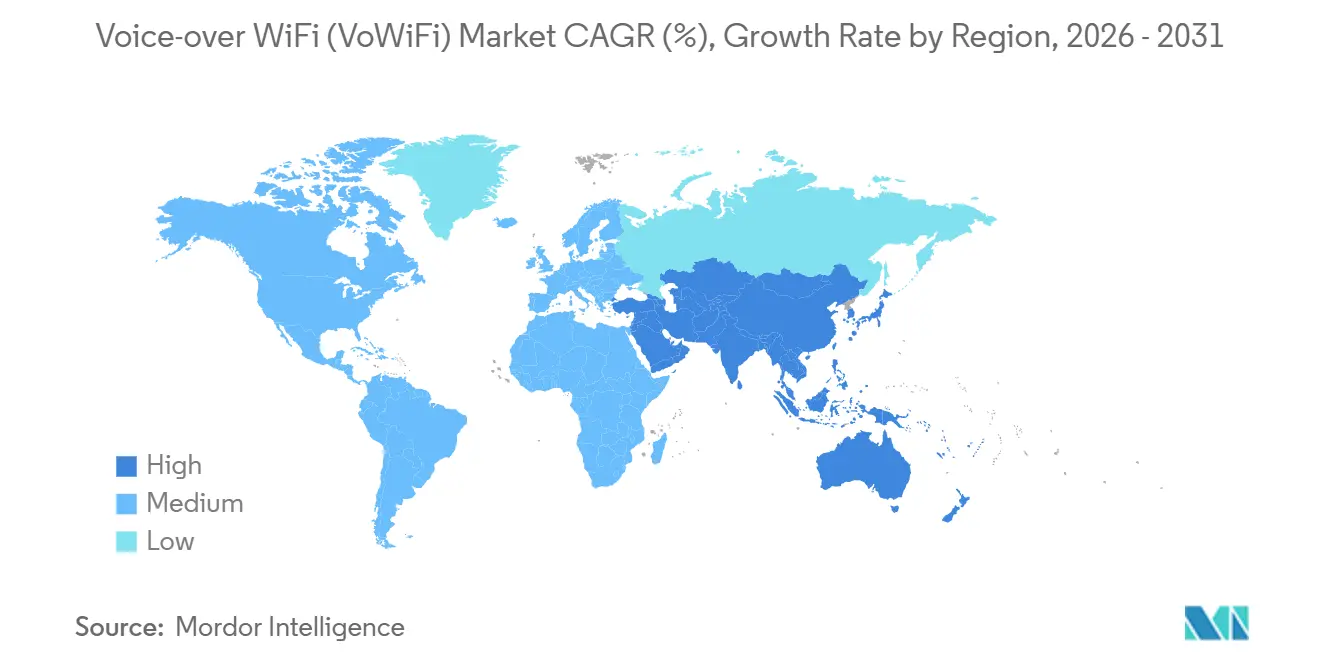

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

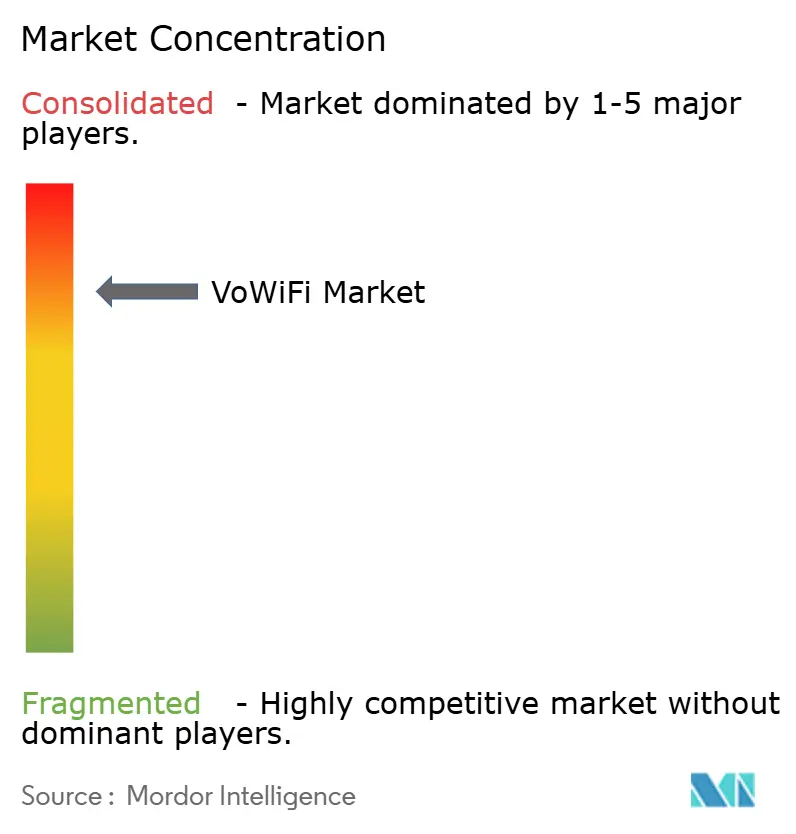

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Voice-over Wi-Fi (VoWiFi) Market Analysis by Mordor Intelligence

The Voice-over Wi-Fi (VoWiFi) Market size reached USD 10.05 billion in 2026 and is forecast to climb to USD 20.36 billion by 2031, advancing at a 15.17% CAGR during 2026-2031. Expanding indoor coverage gaps in mid-band and millimeter-wave 5G layers, emergency-service location mandates, and cost-focused Wi-Fi offload strategies are the primary forces lifting the VoWiFi market. Infrastructure vendors continue to migrate session management to cloud platforms, enabling faster rollouts for tier-2 operators. Device makers now embed ePDG client stacks in entry-level smartphones, broadening addressable demand. At the same time, unresolved Wi-Fi spectrum congestion and limited monetization levers restrain margin expansion for service providers.

Key Report Takeaways

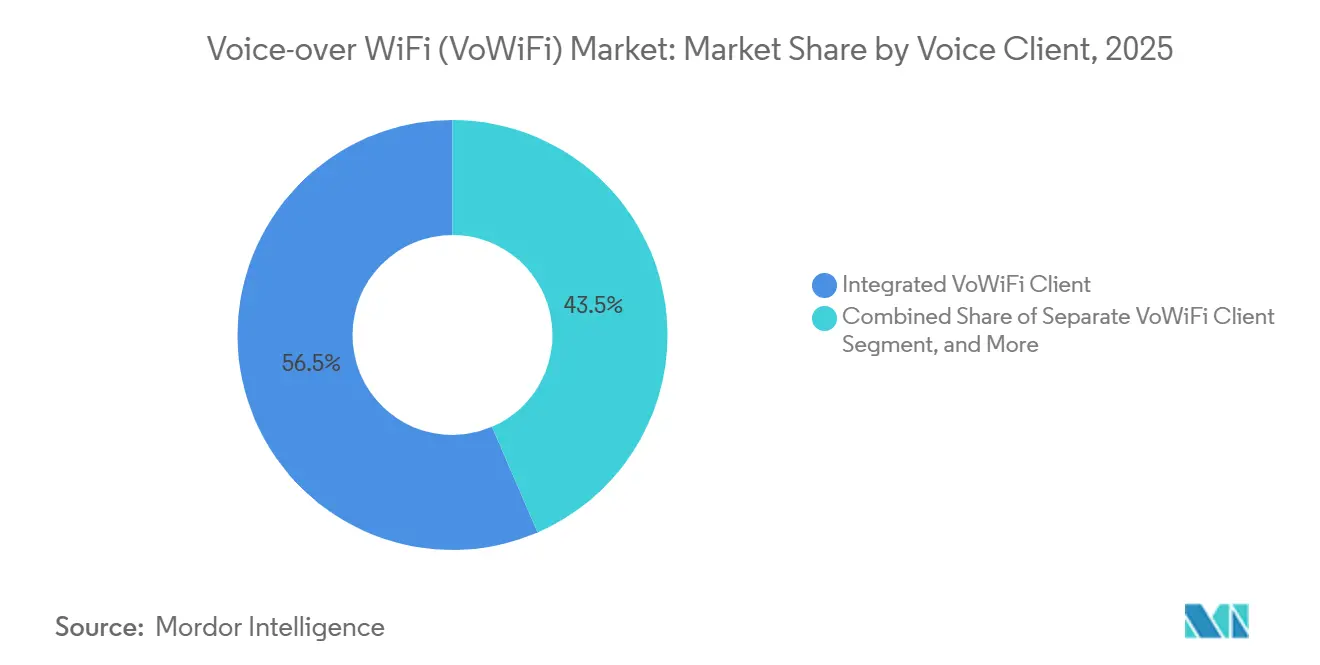

- By voice client, integrated clients commanded 56.48% of the Voice-over Wi-Fi (VoWiFi) Market share in 2025, while browser-based VoWiFi client is anticipated to grow at a 17.32% CAGR between 2026-2031.

- By device type, smartphones led with 80.36% share in 2025 and other connected devices are anticipated to grow at a 15.49% CAGR during 2026-2031.

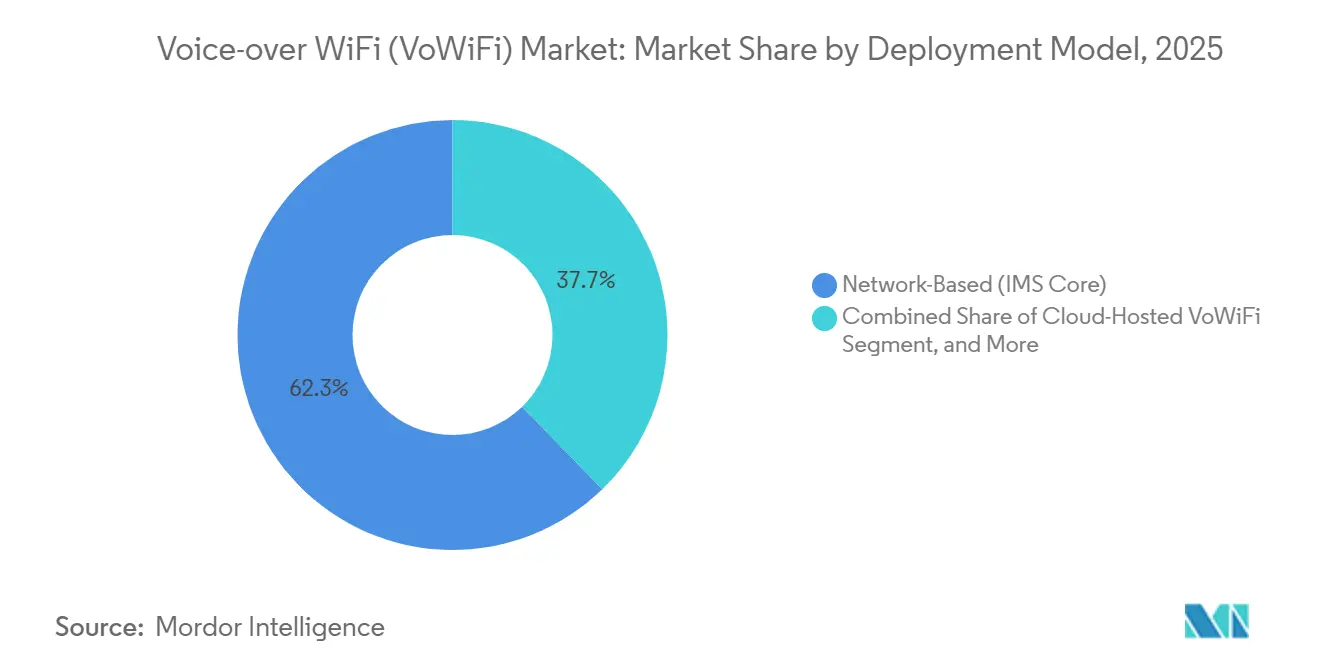

- By deployment model, network-based segment led with 62.27% revenue share in 2025 and cloud-hosted architectures are set to progress at a 16.14% CAGR during 2026-2031.

- By end-user, residential consumers led with 47.84% revenue share in 2025, and public-safety and government agencies will record the fastest growth at a 15.77% CAGR between 2026-2031.

- By geography, the Asia-Pacific region generated 45.16% of 2025 revenue, while the Middle East will register the highest regional CAGR at 15.33% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Voice-over Wi-Fi (VoWiFi) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of carrier-grade Wi-Fi roaming agreements | +3.2% | Global, with early traction in Europe and Asia-Pacific | Medium term (2-4 years) |

| Rising indoor-coverage gaps in 5G NR deployments | +4.1% | North America, Europe, and urban Asia-Pacific | Short term (≤ 2 years) |

| Growing penetration of VoWiFi-capable handsets | +2.8% | Global, led by Asia-Pacific and Middle East | Medium term (2-4 years) |

| Enterprise BYOD security mandates favoring Wi-Fi calling firewalls | +1.9% | North America and Europe | Long term (≥ 4 years) |

| Government emergency-service mandates for Wi-Fi E911 indoors | +2.3% | North America, with spillover to Australia and select EU markets | Short term (≤ 2 years) |

| Energy-efficiency regulations pushing device OEMs to offload voice to Wi-Fi | +1.4% | Europe and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Carrier-Grade Wi-Fi Roaming Agreements

Mobile network operators embed VoWiFi roaming in wholesale agreements to cut international termination fees and avoid PSTN interconnect charges. The GSMA 2025 IR.92 amendment standardized ePDG discovery, allowing seamless voice sessions across visited networks.[1]GSMA, “IR.92 VoLTE and VoWiFi Interoperability Specifications Amendment,” GSMA, gsma.com Vodafone’s pan-European trial cut voice delivery costs by 40% and spurred similar deals among tier-1 carriers. Operators in spectrum-constrained Southeast Asia now view carrier-grade roaming as a coverage extension tool rather than a premium service. Passpoint R3 further simplified credential provisioning, reducing friction for end-users. These shifts collectively lift traffic off licensed spectrum and improve operator economics.

Rising Indoor Coverage Gaps in 5G NR Deployments

Mid-band and millimeter-wave signals lose up to 20 dB within concrete structures, forcing operators to keep LTE overlays for voice continuity. VoWiFi fills those gaps without new small cells, letting carriers retire legacy layers in urban cores. Verizon’s 2025 Manhattan C-band rollout redirected 60% of indoor calls to VoWiFi within 90 days, reducing planned small-cell density by 30%. The quick ROI encourages similar approaches across North America and Europe.

Growing Penetration of VoWiFi-Capable Handsets

Chipset vendors embed ePDG clients in low-cost devices, making VoWiFi a baseline feature even in entry-level smartphones. Apple automated VoWiFi activation in iOS 18, and Samsung ships default-enabled VoWiFi across 80 carrier partners. The GSM Association estimates 78% of 2025 smartphone shipments included VoWiFi support, narrowing historic capability gaps in emerging markets. Wider handset availability directly lifts user adoption and traffic volumes.

Government Emergency-Service Mandates for Wi-Fi E911 Indoors

The FCC ruled that 80% of wireless indoor E911 calls must deliver ≤50-meter accuracy by 2026, a target unattainable with cellular triangulation alone. VoWiFi uses registered access-point databases to provide sub-10-meter precision, prompting U.S. operators to accelerate ePDG deployment. Australia and several EU members adopted similar guidelines, reinforcing the regulatory push. Public-safety networks such as FirstNet now require VoWiFi support on certified devices, cementing the technology in emergency response workflows.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent VoWiFi-to-VoLTE handoff quality issues | -2.1% | Global, particularly in markets with legacy IMS cores | Short term (≤ 2 years) |

| Limited monetization models for MNOs | -1.8% | Global, with acute pressure in mature markets | Medium term (2-4 years) |

| Carrier-Wi-Fi spectrum congestion in unlicensed 6 GHz bands | -1.3% | North America and Europe | Medium term (2-4 years) |

| Slow adoption of Wi-Fi CERTIFIED 6 Release 2 APs in rural markets | -0.9% | Rural regions globally, especially in South America and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent VoWiFi-to-VoLTE Handoff Quality Issues

Real-time IPsec tunnel renegotiation introduces 200-400 milliseconds of jitter, resulting in audible gaps that users perceive as dropped calls. Ericsson’s 2025 field data showed 18% mid-call drop rates during Wi-Fi-to-cellular transitions, far exceeding VoLTE benchmarks. Smaller operators with legacy cores struggle to fund the predictive authentication upgrades required to close the gap. Until quality stabilizes, some consumers disable VoWiFi, slowing overall traffic growth.

Limited Monetization Models for MNOs

Open-Internet rules bar differential pricing for VoWiFi, preventing carriers from charging premiums despite cost savings. Attempts to bundle VoWiFi into higher-tier plans faced swift regulatory pushback in the United States, and over-the-top voice apps deliver comparable quality at zero incremental cost. Operators therefore treat VoWiFi primarily as a cost-reduction lever, delaying revenue payback on ePDG and IMS investments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Voice Client: Integrated Clients Anchor Adoption, Browsers Gain Ground

Integrated clients contributed 56.48% of 2025 revenue, powered by OS-level authentication that removes user friction. Browser-based options, though smaller, are growing at a 17.32% CAGR. The Voice-over Wi-Fi (VoWiFi) Market size attached to browser clients benefits from WebRTC maturity that makes installation-free voice attractive for bring-your-own-device environments. Enterprises value policy control and zero-trust separation that browsers deliver. Integrated clients still excel at predictive handoffs, reducing latency during coverage changes, yet browser innovations continue to narrow the performance gap.

A second driver is Passpoint R3, which automates credential provisioning for browser sessions. Cisco’s Webex Calling realized 30% lower development costs by avoiding native client builds, and this spending efficiency appeals to mid-market enterprises. Over the forecast, integrated clients will retain the largest share, but browser solutions will account for an expanding slice of the Voice-over Wi-Fi (VoWiFi) Market.

By Device Type: Smartphones Dominate as IoT Devices Accelerate

Smartphones held 80.36% revenue share in 2025, underlining their central role in voice communication. Other connected devices, although smaller, are expected to rise at a 15.49% CAGR. Industrial gateways, telematics units, and medical wearables all gain from chipset-level ePDG integration, which removes the need for separate cellular modules. The Voice-over Wi-Fi (VoWiFi) Market share for smartphones will gradually erode as these emerging endpoints adopt Wi-Fi calling due to cost and energy considerations.

Qualcomm’s sub-USD 5 VoWiFi-ready IoT chipset opened the door for voice-enabled sensors across manufacturing floors. Automotive makers embed VoWiFi in telematics control units to satisfy eCall regulations when cellular service is weak. Hospitals prefer VoWiFi for patient monitors because in-building cellular restrictions do not apply to Wi-Fi. Laptops and tablets play a secondary role, but larger batteries help them maintain continuous ePDG tunnels during long meetings.

By Deployment Model: IMS Core Still Reigns, Cloud Grows Quickly

Network-based IMS cores represented 62.27% of 2025 revenue. Operators safeguard lawful intercept compliance and leverage sunk investment in hardware. Cloud-hosted VoWiFi, however, is expected to grow at a rate of 16.14% annually as hyperscalers make pay-as-you-grow pricing more attractive for smaller carriers. The VoWiFi market size realized through cloud models is expanding because launch timelines shrink from more than a year to a few months.

Oracle’s Communications Cloud reduced deployment cycles to 90 days, enabling greenfield mobile virtual network operators to roll out VoWiFi without owning data centers. Hybrid edge-cloud approaches emerge, where ePDG authentication remains on-premises for latency, while analytics and billing shift to the public cloud. Release 18 APIs lower vendor lock-in, allowing operators to mix components from multiple suppliers.

By End-User: Residential Remains Core, Public Safety Surges Ahead

Residential consumers supplied 47.84% of 2025 revenue as operators bundled VoWiFi with home broadband to offload traffic. Public-safety agencies will advance at 15.77% CAGR during 2026-2031, benefiting from FirstNet and similar national mandates. This upswing enlarges the Voice-over Wi-Fi (VoWiFi) Market because government procurement budgets fund rapid device refresh cycles.

Small and medium enterprises select VoWiFi to extend PBX features to mobiles, cutting voice bills by 40%. Large enterprises integrate Wi-Fi calling into unified communications suites for global employees. The U.S. Department of Homeland Security’s directive to enable VoWiFi on federal-issue handsets added 2.1 million devices in 2025, illustrating how policy moves can swing demand quickly.

Geography Analysis

Asia-Pacific generated 45.16% of VoWiFi revenue in 2025. China Mobile’s Wi-Fi 6E fabric and Reliance Jio’s fixed-wireless bundles underline the region’s spectrum scarcity workaround. KT covered subway tunnels with Wi-Fi calling, easing customer churn. Japan’s carriers completed interoperability testing, and India mandated VoWiFi support on new smartphones, enlarging handset readiness across rural zones.

Middle East will post the fastest 15.33% CAGR. Saudi Arabia’s regulator ordered nationwide VoWiFi by mid-2025.[2]Communications, Space and Technology Commission, “VoWiFi Deployment Mandate under Vision 2030,” CST, cst.gov.sa South Africa streamlined licensing to 90 days, letting smaller carriers deploy quickly. Nigeria saw adoption rise to 15% of mobile users in 2025 as enterprise Wi-Fi offset poor cellular penetration in Lagos. UAE operators now offer cross-emirate roaming, minimizing call drops during inter-city travel.

North America leans on VoWiFi to meet E911 mandates and shrink indoor densification budgets. T-Mobile integrated VoWiFi with its 5G standalone core, cutting urban call-drop rates by 35%. Verizon’s C-band plan saved USD 200 million in small-cell costs by steering indoor calls to Wi-Fi. Canada cleared 6 GHz VoWiFi with no individual licenses, accelerating regional uptake. Europe shows mixed progress because cross-border roaming rests on voluntary agreements, yet Germany already records 22% of voice minutes over Wi-Fi. South America remains city-centric, with Brazil mandating VoWiFi in new licenses while Argentina and Chile face infrastructure constraints.

Competitive Landscape

The voice-over Wi-Fi (VoWiFi) market is highly concentrated. Cisco, Nokia, and Ericsson dominate ePDG and IMS deployments by leveraging existing operator contracts. Oracle disrupted incumbents with a cloud-native IMS that lowers capital spend by 60%. Device makers Apple, Samsung, and Xiaomi differentiate through predictive handoff algorithms that pre-authenticate ePDG tunnels, uplifting customer experience.

White-space opportunities emerge in enterprise VoWiFi management integrated with zero-trust security. Ribbon Communications patented AI-driven quality optimization that adjusts codecs to real-time Wi-Fi congestion.[3]United States Patent and Trademark Office, “Ribbon Communications AI-Driven VoWiFi Quality-of-Service Optimization Patent Filing,” USPTO, uspto.gov Smaller vendors Aptilo Networks and Boingo Wireless target public hotspots and venues that require flexible session management. Anticipated Wi-Fi 7 certification in 2026 will introduce deterministic latency, likely narrowing quality gaps with VoLTE and intensifying competition.

Strategic partnerships continue to shape the landscape. Nokia’s USD 85 million cloud IMS win across 12 Middle Eastern markets showcases demand for full-stack cloud migrations. Samsung announced predictive algorithms that cut handoff drops 40%, strengthening its flagship differentiation. Reliance Jio expanded VoWiFi to 1,000 municipalities, putting pressure on slower rivals. T-Mobile demonstrated the first fully integrated 5G-VoWiFi mobility in the United States, and Cisco launched cloud UC with native browser-based VoWiFi, halving enterprise costs relative to on-premises PBX.

Voice-over Wi-Fi (VoWiFi) Industry Leaders

Oracle Corporation

Cisco Systems Inc.

Nokia Corporation

Telefonaktiebolaget LM Ericsson

Huawei Technologies Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Nokia signed a USD 85 million agreement with a Middle Eastern tier-1 operator for cloud-native IMS supporting VoWiFi across 12 markets.

- November 2025: Samsung confirmed Galaxy S25 devices will include predictive VoWiFi handoff that lowers drop rates 40%.

- October 2025: Reliance Jio expanded VoWiFi to 500 additional Indian cities, raising total coverage past 1,000 municipalities.

- September 2025: T-Mobile completed VoWiFi integration with its 5G standalone core across 50 U.S. metros.

- August 2025: Cisco launched Unified Communications Manager Cloud with native browser-based VoWiFi.

Global Voice-over Wi-Fi (VoWiFi) Market Report Scope

The Voice-over Wi-Fi (VoWiFi) Market Report is Segmented by Voice Client (Integrated VoWiFi Client, Separate VoWiFi Client, and Browser-based VoWiFi Client), Device Type (Smartphones, Tablets and Laptops, and Other Connected Devices), Deployment Model (Network-Based IMS Core, Cloud-Hosted VoWiFi, and Hybrid Edge-Cloud), End-User (Residential Consumers, Small and Medium Enterprises, Large Enterprises, and Public-Safety and Government Agencies), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Integrated VoWiFI Client |

| Separate VoWiFI Client |

| Browser-based VoWiFi Client |

| Smartphones |

| Tablets and Laptops |

| Other Connected Device Types |

| Network-Based (IMS Core) |

| Cloud-Hosted VoWiFi |

| Hybrid (Edge-Cloud) |

| Residential Consumers |

| Small and Medium Enterprises |

| Large Enterprises |

| Public-Safety and Government Agencies |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Voice Client | Integrated VoWiFI Client | |

| Separate VoWiFI Client | ||

| Browser-based VoWiFi Client | ||

| By Device Type | Smartphones | |

| Tablets and Laptops | ||

| Other Connected Device Types | ||

| By Deployment Model | Network-Based (IMS Core) | |

| Cloud-Hosted VoWiFi | ||

| Hybrid (Edge-Cloud) | ||

| By End-User | Residential Consumers | |

| Small and Medium Enterprises | ||

| Large Enterprises | ||

| Public-Safety and Government Agencies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will Voice-over WiFi (VoWiFi) deployments become by 2031?

Total Voice-over WiFI (VoWiFi) service revenues are projected to reach USD 20.36 billion in 2031, almost doubling the 2026 level while expanding at a 15.17% CAGR during 2026-2031.

Which geographic region is currently generating the most Voice-over WiFI (VoWiFi) revenue?

Asia-Pacific led with 45.16% of global 2025 revenue, fueled by nationwide Wi-Fi 6E rollouts in China and aggressive bundling strategies in India.

Why are public-safety agencies accelerating adoption of Wi-Fi calling?

Indoor E911 location mandates require sub-50-meter accuracy that Wi-Fi positioning can meet, prompting FirstNet and similar networks to embed VoWiFi in all certified devices.

What is the biggest technical hurdle to seamless Wi-Fi calling today?

Quality drops during VoWiFi-to-VoLTE handoffs persist because IPsec tunnel re-establishment adds 200-400 ms of jitter, leading to higher mid-call drop rates than pure VoLTE sessions.

How are operators funding large-scale deployments without heavy capital outlay?

Many tier-2 carriers choose cloud-hosted IMS and ePDG services with pay-as-you-grow pricing, cutting launch timelines from 18 months to roughly 90 days and lowering upfront costs by about 60%.

Which device category is poised for the fastest growth beyond smartphones?

Connected endpoints such as industrial IoT gateways, automotive telematics units, and medical wearables are set to expand at a 15.49% CAGR through 2031 as chipsets ship with embedded ePDG clients.et size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the VoWiFi Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: