Vitamin D Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

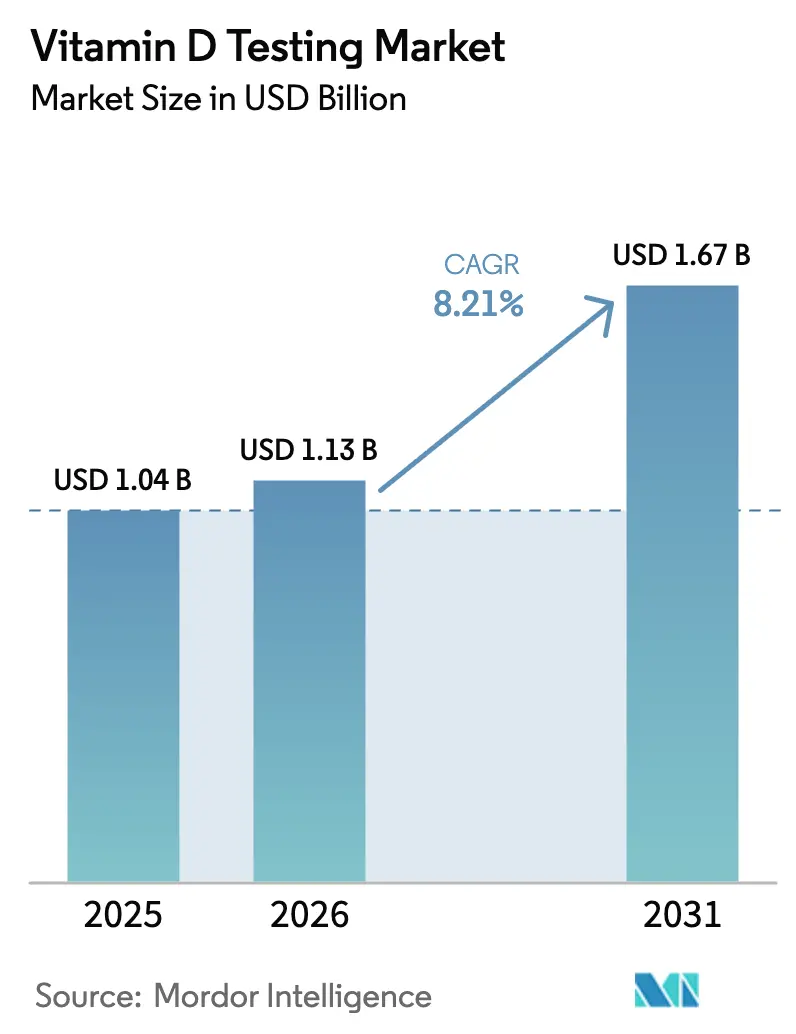

| Market Size (2026) | USD 1.13 Billion |

| Market Size (2031) | USD 1.67 Billion |

| Growth Rate (2026 - 2031) | 8.21% CAGR |

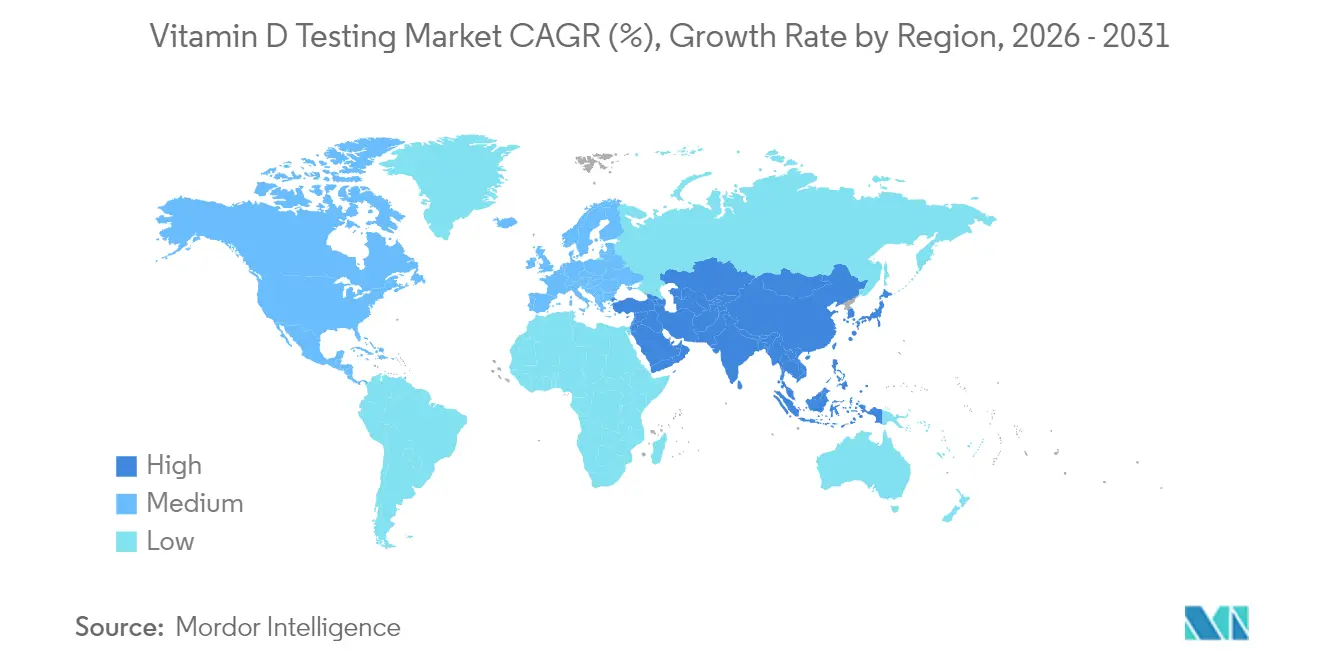

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vitamin D Testing Market Analysis by Mordor Intelligence

The Vitamin D testing market size is expected to grow from USD 1.04 billion in 2025 to USD 1.13 billion in 2026 and is forecast to reach USD 1.67 billion by 2031 at 8.21% CAGR over 2026-2031. Rapid adoption of automated chemiluminescence immunoassay (CLIA) platforms is lowering per-test costs and enabling high-throughput workflows that support expanding screening programs. Regulatory alignment—most notably the U.S. Food and Drug Administration’s framework for laboratory-developed tests—reduces methodology uncertainty and encourages investment in advanced analytical platforms. Preventive-care incentives, expanded reimbursement codes, and fortification-surveillance mandates jointly elevate test volumes across healthcare systems. Meanwhile, dried blood spot micro-sampling is broadening patient access by enabling reliable remote collection under ambient conditions.

Key Report Takeaways

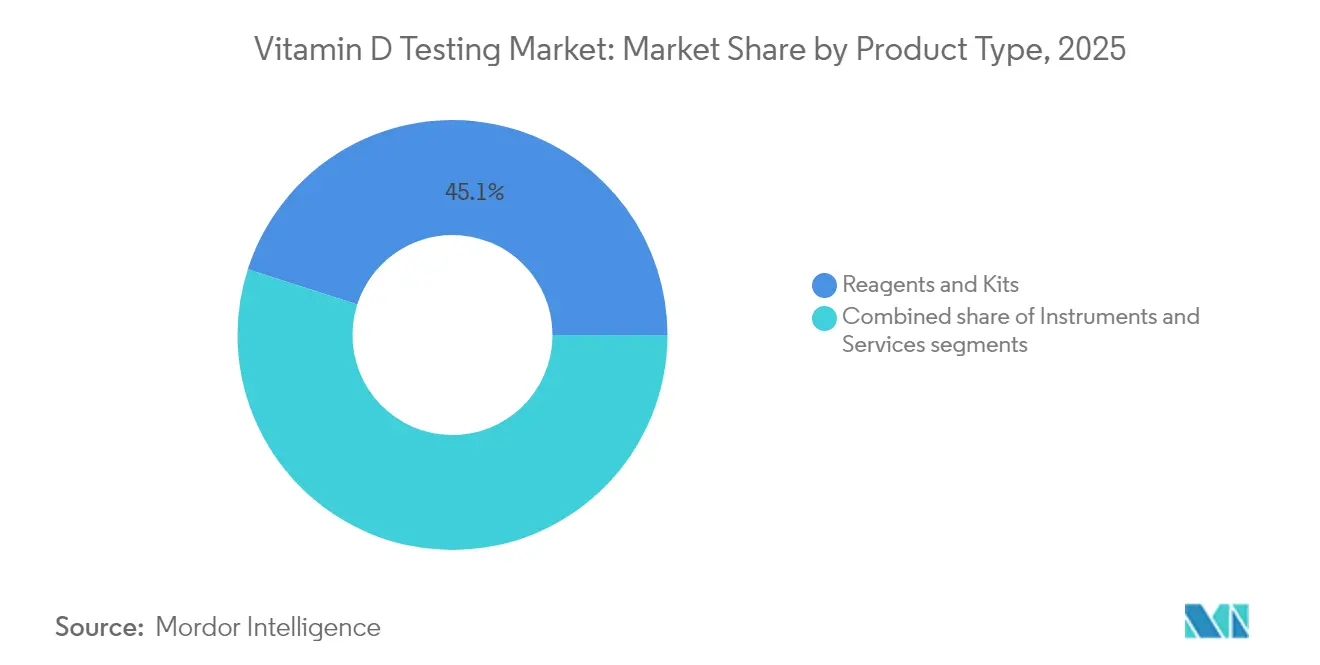

- By product type, reagents and kits accounted for 45.05% of the Vitamin D testing market share in 2025 while the services segment is on track for an 8.87% CAGR to 2031.

- By technology, CLIA held 38.25% share of the Vitamin D testing market in 2025; LC-MS/MS is projected to expand at a 9.30% CAGR through 2031.

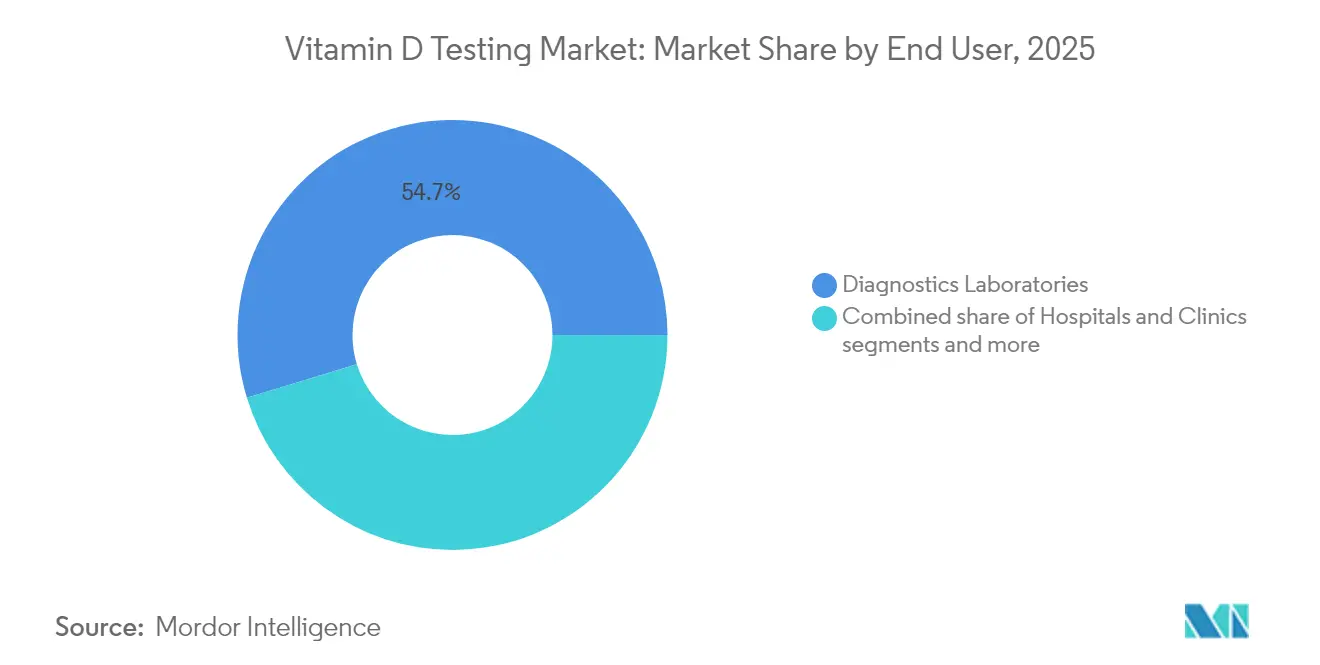

- By end user, diagnostic laboratories commanded 54.72% share of the Vitamin D testing market size in 2025 whereas home-care and remote testing is growing at a 9.78% CAGR.

- By sample type, serum/plasma represented 61.10% share of the Vitamin D testing market in 2025 and dried blood spot collection is advancing at a 10.25% CAGR through 2031.

- By geography, North America led with 41.80% of the Vitamin D testing market size in 2025, while Asia-Pacific records the fastest 10.74% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vitamin D Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of vitamin-D deficiency diagnoses | +2.1% | Global, highest in MENA and Northern Europe | Medium term (2-4 years) |

| Shift to preventive healthcare & routine screening | +1.8% | North America and EU, expanding into urban APAC | Long term (≥ 4 years) |

| CLIA automation lowering per-test cost | +1.5% | Global, led by high-volume laboratory markets | Short term (≤ 2 years) |

| Emerging reimbursement codes in Europe & U.S. | +1.2% | North America and EU, selective APAC markets | Medium term (2-4 years) |

| AI-enabled at-home micro-sample kits | +0.9% | North America, Western Europe, urban APAC | Long term (≥ 4 years) |

| National fortification policies prompting surveillance testing | +0.7% | Canada, Finland, UK policy regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Vitamin-D Deficiency Diagnoses

Roughly 1 billion people live with inadequate vitamin D levels, with prevalence soaring to 82.1% among Black Americans and 69.2% in Latino communities. Clinical guidelines published by the Endocrine Society in 2024 created precise testing criteria for high-risk populations, which paradoxically expanded targeted demand even while discouraging universal screening. Providers increasingly embed vitamin D assessment in chronic-disease management programs for diabetes, cardiovascular disease, and osteoporosis, sustaining growth of the Vitamin D testing market. The confluence of aging populations, limited sun exposure in urban lifestyles, and malabsorption disorders further reinforces systematic screening in many regions. Government surveillance linked to food-fortification programs adds another steady testing stream, translating population-health priorities into laboratory demand.

Shift to Preventive Healthcare & Routine Screening

Value-based reimbursement models encourage early detection, making vitamin D measurement a routine metric in preventive health check-ups covered by Medicare Advantage plans and a growing list of private insurers. Direct-to-consumer laboratory spending is poised to surpass USD 9 billion by 2033, giving consumers unprecedented power to order tests without physician mediation. Employers embed vitamin D tracking in corporate wellness dashboards, encouraging regular employee monitoring that generates predictable sample volumes. Senior-care programs integrate deficiency checks into fall-prevention initiatives, enhancing adherence to supplementation regimens. Collectively these behavioral and policy shifts underpin sustained expansion of the Vitamin D testing market.

CLIA Automation Lowering Per-Test Cost

Fully robotic CLIA systems can process more than 3,600 assays per hour, driving economies of scale while trimming labor expenditures. Platforms such as Roche’s cobas 8000 handle up to 1,000 samples each hour and require minimal water, cutting utilities and biohazard waste. Lower costs empower payers to authorize broader testing, supporting higher throughput facilities and consolidating smaller providers under reference-lab networks. Analytical reliability also rises because AI modules continuously flag outlier data, lowering repeat-test rates. These efficiency gains reinforce the competitive stance of established laboratories and spur additional uptake across emerging markets, accelerating revenue for the Vitamin D testing market.

Emerging Reimbursement Codes in Europe & U.S.

Introduction of CPT code 82306 established uniform billing for 25-hydroxyvitamin D assays in the United States, eliminating many administrative ambiguities that previously discouraged routine claims submission. Medicare now reimburses testing for chronic kidney disease, malabsorption, and osteoporosis, while European payers embed vitamin D monitoring into integrated care bundles. Harmonized reimbursement structures narrow patient out-of-pocket obligations and solidify predictable revenue for labs, bolstering the Vitamin D testing market across multiple geographies. As private insurers adopt similar coverage, laboratory cashflows stabilize, lowering investment risk for automation and advanced analytics procurement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pricing pressure from bundled wellness panels | -1.4% | North America & EU, high-competition markets | Short term (≤ 2 years) |

| Variability between assay methods | -0.9% | Global, particularly affecting multi-site laboratories | Medium term (2-4 years) |

| Dried-blood-spot sample stability concerns | -0.6% | Global, highest impact in remote/tropical regions | Medium term (2-4 years) |

| Regulatory scrutiny over direct-to-consumer claims | -0.8% | Global, strictest in EU and select US states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pricing Pressure from Bundled Wellness Panels

Volume-based contracting has encouraged insurers to reimburse comprehensive metabolic screens that include vitamin D for a single all-in price, compressing margins on individual assays. Consolidated national labs can leverage scale, but regional independents often absorb lower reimbursement, forcing them to renegotiate supplier contracts. Consumer-direct platforms mirror this pressure by marketing multi-analyte panels at discount prices to gain share, intensifying price competition in the Vitamin D testing market. Larger players counteract by automating workflows and cross-selling allergy or hormone panels to maintain profitability.

Regulatory Scrutiny over Direct-to-Consumer Claims

The FDA’s phased regulation of laboratory-developed tests reclassifies many vitamin D assays as medical devices, compelling direct-to-consumer companies to invest in quality-system compliance and clinical validation. European marketing rules further restrict health claims, limiting promotional freedom. Diverse state laws in the United States introduce additional complexity and potential fines for non-compliance. These governance hurdles slow product launches and raise operational costs, tempering short-term expansion of the Vitamin D testing market in consumer channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Services Growth Outpaces Traditional Reagents

The services arm of the Vitamin D testing market expanded at an 8.87% CAGR toward 2031, propelled by hospital outsourcing and reference-lab consolidation. Reagents and kits still delivered 45.05% Vitamin D testing market share in 2025, yet their revenue margins tightened because automated systems consume fewer consumables per assay. Instruments represent the smallest revenue slice, but every analyzer placement establishes a long-tail reagent annuity that underpins supplier profitability. Laboratories unable to fund automation increasingly subcontract specialized vitamin D panels to service providers, reinforcing service-segment momentum. Acquisitions like Quest Diagnostics’ USD 1 billion LifeLabs deal highlight the race for network scale that amplifies purchasing leverage and geographic reach.

Reagent manufacturers respond by innovating high-sensitivity chemistries compatible with both CLIA and emerging LC-MS/MS platforms, safeguarding demand even as per-test consumption falls. Digital integration services that link analyzers to laboratory information systems deliver incremental revenue while differentiating suppliers. Meanwhile, point-of-care service models flourish in primary-care clinics where rapid readouts inform supplementation decisions during a single visit, extending the Vitamin D testing market beyond central laboratories.

By Technology: LC-MS/MS Disrupts CLIA Dominance

CLIA produced 38.25% of 2025 revenue thanks to low running costs and fully automated operation. Yet LC-MS/MS achieved a 9.30% CAGR as new systems blend mass-spectrometry precision with walk-away automation that mitigates labor intensity. The Vitamin D testing market size associated with LC-MS/MS platforms is set to grow steadily because clinicians demand higher specificity in complex cases such as chronic kidney disease. FDA scrutiny of laboratory-developed tests pushes labs toward standardized LC-MS/MS kits, accelerating uptake. ELISA retains a foothold in cost-sensitive settings, while radio-immunoassay declines due to radiological waste protocols.

Early adopters report that LC-MS/MS reduces repeat testing triggered by cross-reactivity in CLIA assays, thereby improving clinical confidence. Suppliers now bundle cloud-based calibration updates that simplify maintenance, widening accessibility for mid-size laboratories. As reimbursement remains method agnostic, laboratories can align platform selection with case-mix complexity, fueling multi-platform coexistence that broadens the Vitamin D testing market.

By End User: Home-Care Disruption Accelerates

Diagnostic laboratories maintained 54.72% share of the Vitamin D testing market in 2025, but home-care and remote testing posted a 9.78% CAGR through 2031 as consumers embraced convenience and data ownership. Telemedicine consults frequently bundle vitamin D assessments into chronic-care regimens, driving kit shipments directly to patient homes. Hospitals confronted by staffing shortages lean on reference labs for non-urgent micronutrient testing, diverting volume away from in-house benches. The Vitamin D testing market size for remote channels will keep climbing because payers acknowledge the cost-effectiveness of decentralized monitoring.

Equipment makers now collaborate with courier networks to guarantee overnight delivery of dried blood spot mailers, minimizing turnaround anxiety. Clinicians gain electronic access to trend graphs that flag relapse risks, enhancing care coordination. Such service evolution expands the Vitamin D testing market while redefining competitive boundaries between diagnostic firms, digital-health startups, and retail pharmacies.

Geography Analysis

North America generated 41.80% of 2025 revenue thanks to broad insurance coverage and advanced automation infrastructure. Asia-Pacific, however, is the growth engine with a 10.74% CAGR anchored by urbanization, rising middle-class health awareness, and private-sector diagnostic investment. Organized lab networks in India penetrate tier-3 towns, while Chinese demand swells alongside nutraceutical consumption trends. Europe continues steady expansion through fortification-driven surveillance programs and aging demographics, but reimbursement austerity limits upside. Middle East and Africa markets show early promise as governments modernize healthcare and grapple with surprisingly high deficiency in sun-rich climates.

Competitive Landscape

North America retains leadership through large reference-lab chains, comprehensive CPT coding, and recent acquisitions that widen branch footprints. The Vitamin D testing market size in this region benefits from Medicare coverage for high-risk cohorts, though price pressures from bundled wellness panels curb further upside.

Asia-Pacific’s double-digit expansion is supported by competitive manufacturing costs enabling affordable testing, while private insurance uptake fuels volume in metropolitan areas. Europe focuses on outcome-based care and food-fortification monitoring, embedding vitamin D assessment in public-health dashboards. In all regions, home-based testing is emerging as the universal growth lever that democratizes access and compresses turnaround times.

Competitive differentiation has shifted from assay menus toward data analytics, patient portals, and interoperability with electronic health records. Market leaders package population-health dashboards that present aggregated deficiency trends, helping insurers craft targeted supplementation campaigns. Partnerships between device startups and hospital systems spur ecosystem growth without compromising incumbent dominance, sustaining balanced rivalry within the Vitamin D testing market.

Vitamin D Testing Industry Leaders

F. Hoffmann-La Roche Ltd.

DiaSorin S.p.A.

Abbott

Siemens Healthcare GmbH

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Health Canada cleared NanoSpeed’s rapid vitamin D test, expanding licensed methodologies for retail clinics.

- March 2025: Polaris DX introduced Igloo Pro, a point-of-care device delivering vitamin D results in minutes to dental practices and primary-care offices.

Global Vitamin D Testing Market Report Scope

As per the scope of the report, the Vitamin D Test assists in detecting the vitamin D level in the human body.

The Vitamin D Testing Market is segmented by Test Type (25-Hydroxy Vitamin D Test, and 1,25 Dihydroxy Vitamin D Test), End-User (Hospitals & Clinics, Diagnostics Labs, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, worldwide. The report offers the value (USD million) for the above segments.

| Reagent & Kits |

| Instruments |

| Services |

| LC–MS/MS |

| Chemiluminescence Immunoassay (CLIA) |

| ELISA |

| Radio-Immunoassay (RIA) |

| Others |

| Diagnostic Laboratories |

| Hospitals & Clinics |

| Home-care & Remote Testing |

| Others |

| Serum / Plasma |

| Whole Blood |

| Dried Blood Spot |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type (Value) | Reagent & Kits | |

| Instruments | ||

| Services | ||

| By Technology (Value) | LC–MS/MS | |

| Chemiluminescence Immunoassay (CLIA) | ||

| ELISA | ||

| Radio-Immunoassay (RIA) | ||

| Others | ||

| By End User (Value) | Diagnostic Laboratories | |

| Hospitals & Clinics | ||

| Home-care & Remote Testing | ||

| Others | ||

| By Sample Type (Value) | Serum / Plasma | |

| Whole Blood | ||

| Dried Blood Spot | ||

| Others | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Vitamin D Testing Market size?

The Vitamin D Testing Market is projected to register a CAGR of 8.21% during the forecast period (2026-2031)

Who are the key players in Vitamin D Testing Market?

F. Hoffmann-La Roche Ltd., DiaSorin S.p.A., Abbott, Siemens Healthcare GmbH and Thermo Fisher Scientific Inc. are the major companies operating in the Vitamin D Testing Market.

Which is the fastest growing region in Vitamin D Testing Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Vitamin D Testing Market?

In 2025, the North America accounts for the largest market share in Vitamin D Testing Market.

What years does this Vitamin D Testing Market cover?

The report covers the Vitamin D Testing Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Vitamin D Testing Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: