Vision Inspection And Inline QA As A Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.69 Billion |

| Market Size (2031) | USD 2.41 Billion |

| Growth Rate (2026 - 2031) | 7.40% CAGR |

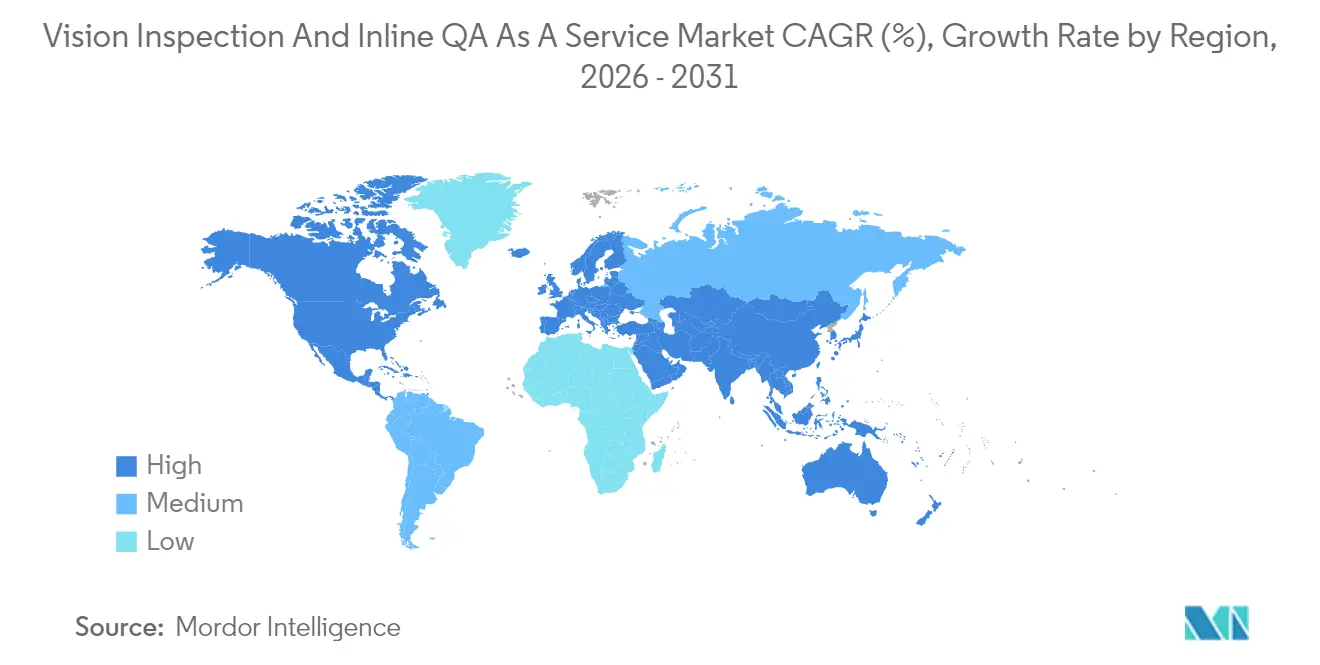

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vision Inspection And Inline QA As A Service Market Analysis by Mordor Intelligence

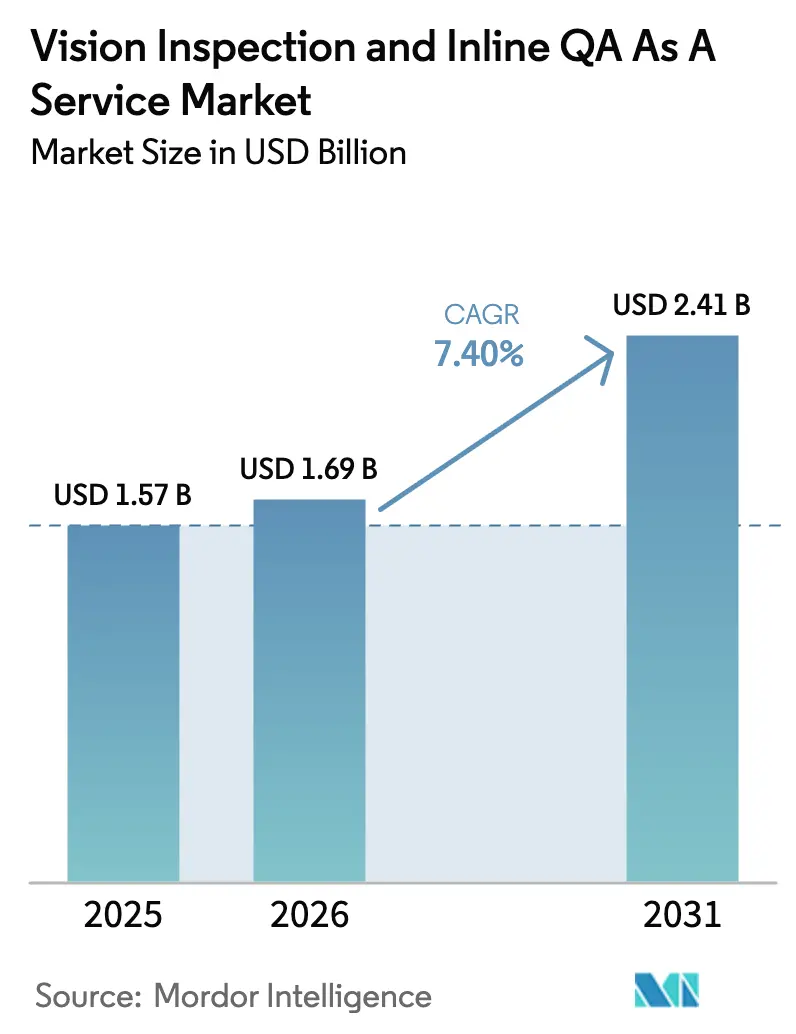

The Vision Inspection and Inline QA as a Service market size is expected to grow from USD 1.57 billion in 2025 to USD 1.69 billion in 2026 and is forecast to reach USD 2.41 billion by 2031 at 7.4% CAGR over 2026-2031. The anticipated growth stems from rising demand for subscription-based quality assurance, which converts formerly capital-intensive vision systems into outcome-driven services; persistent cost pressure from product recalls; and steady advances in deep-learning accuracy, which now routinely exceed 95% across many industrial defect classes. Manufacturers are increasingly migrating quality workloads to scalable cloud and edge platforms, while federated learning blends defect data from multiple sites to enhance model precision without disclosing proprietary information. As Industry 4.0 programs mature, vision inspection becomes the cornerstone of closed-loop production, automatically feeding results into MES and ERP systems to adjust line parameters in real time. Hybrid deployments balance these digital ambitions with strict data-sovereignty regulations, especially in Europe and China, where locally hosted inference satisfies privacy rules yet keeps the cloud available for continuous model training. Finally, outcome-based contracts, in which providers charge only for verified quality improvements, realign incentives between manufacturers and technology vendors and accelerate market adoption.

Key Report Takeaways

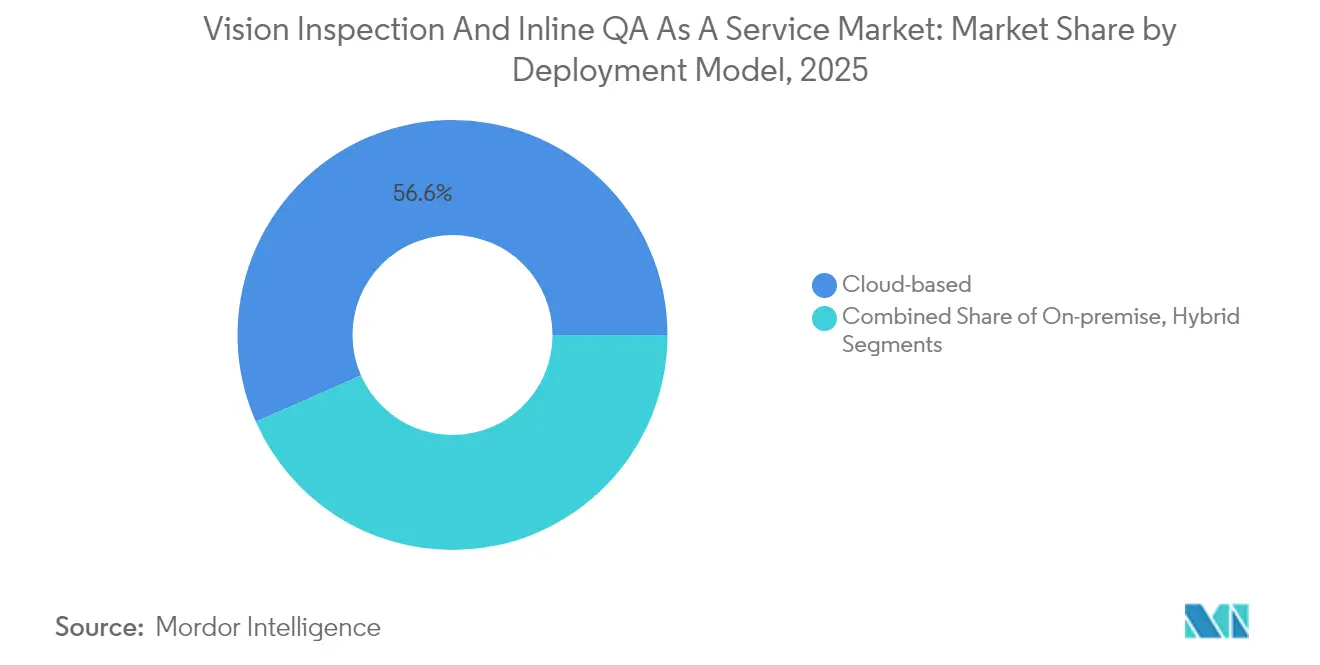

- By deployment model, cloud-based captured 56.62% of the Vision Inspection and Inline QA as a Service Market share in 2025.

- By offering type, Vision Inspection and Inline QA as a Service Market size for Platform-as-a-Service is projected to grow at a 9.33% CAGR between 2026–2031.

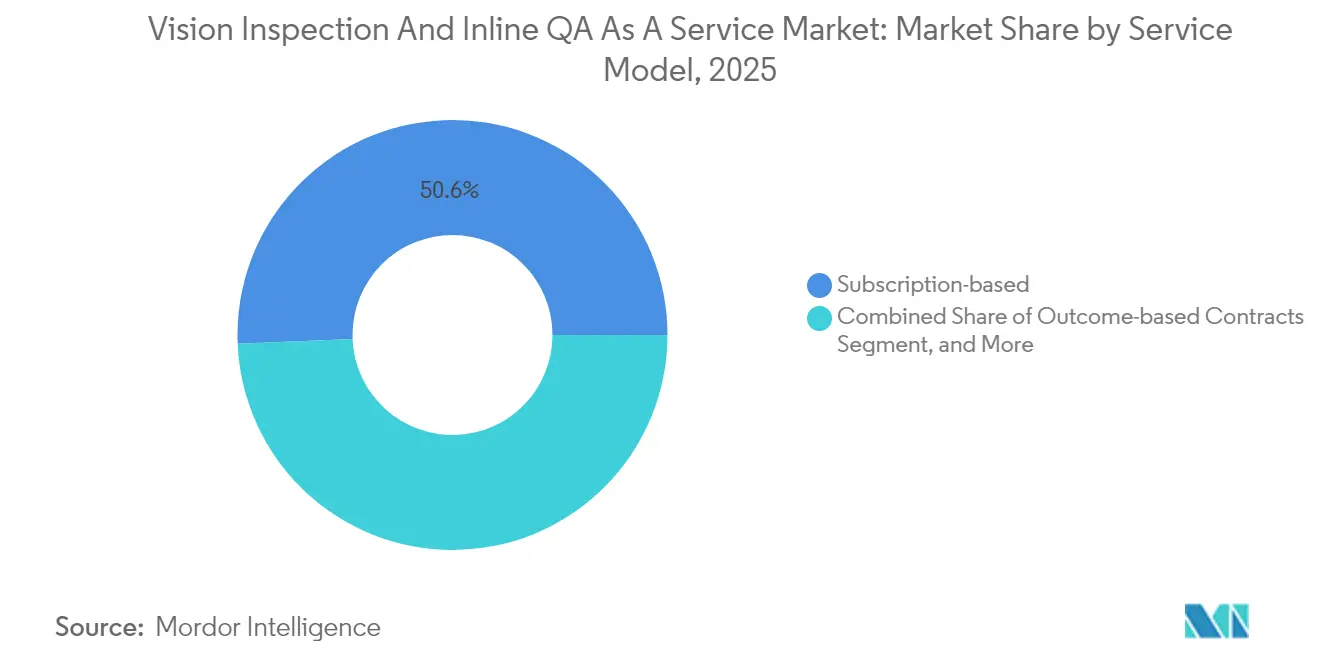

- By service model, subscription-based contracts captured 50.64% of the Vision Inspection and Inline QA as a Service Market share in 2025.

- By end-user industry, Vision Inspection and Inline QA as a Service Market size for logistics and e-commerce is projected to grow at 9.31% CAGR between 2026–2031.

- By geography, Asia-Pacific captured 33.78% of the Vision Inspection and Inline QA as a Service Market revenue share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vision Inspection And Inline QA As A Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Industry 4.0 Smart-Factory Programs | +2.1% | Global, with APAC leading implementation | Medium term (2-4 years) |

| Growing Need for Inline QA To Curb Costly Recalls | +1.8% | Global, particularly regulated industries | Short term (≤ 2 years) |

| Shift From Cap-Ex Vision Hardware to Subscription Pricing | +1.5% | North America and Europe are early adoption, APAC follows | Medium term (2-4 years) |

| Deep-Learning Accuracy Breakthroughs in Defect Detection | +1.3% | Global, with technology centers leading | Long term (≥ 4 years) |

| Federated Defect Library Network Effects | +0.9% | Global, concentrated in manufacturing hubs | Long term (≥ 4 years) |

| ESG-Driven Zero-Waste, Pay-Per-Defect Models | +0.7% | Europe and North America are leading, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Industry 4.0 Smart-Factory Programs

Smart-factory rollouts place automated quality control at the heart of digital production, because inline vision inspection supplies real-time feedback that immediately tunes process variables for continuous improvement. Asian manufacturers benefit from government incentives that underwrite pilot projects, allowing for rapid scaling once performance targets are met. Closed-loop quality data flow straight into MES dashboards, prompting line-side adjustments that can slash scrap rates within weeks of deployment. Vision systems also generate granular audit trails that satisfy ISO 9001 and evolving cyber-physical quality standards. Training investments, often running into several million USD annually for large plants, focus on re-skilling traditional quality engineers to operate AI-enabled tools, an approach that preserves institutional know-how while elevating analytical capabilities. In the long run, plant-wide data integration establishes a foundation for predictive maintenance and adaptive scheduling that further boosts OEE.

Growing Need for Inline QA to Curb Costly Recalls

Average direct recall expenses now exceed USD 12 million per incident, while associated brand damage and litigation can multiply losses manyfold. Inline vision inspection intercepts defects during production, rather than at post-process audit, reducing recall probability by up to 78% in automotive and aerospace use cases. Pharmaceutical lines utilize 100% camera-based checks to verify fill level, cap integrity, and label legibility, all of which are logged with electronic signatures to comply with FDA 21 CFR Part 11. Food plants integrate color cameras with hyperspectral sensors to spot contamination and packaging faults without slowing throughput. The financial impact is compelling: each prevented recall translates directly into retained margin and safeguards consumer trust, reinforcing executive commitment to continuous monitoring.

Shift From Cap-Ex Vision Hardware to Subscription Pricing

Legacy machine-vision deployments required upfront payments between USD 50,000 and USD 200,000 per line, hindering adoption among mid-sized manufacturers. Service-based models convert that burden into monthly fees as low as USD 500, bundling cameras, software, and updates in a single invoice that scales with usage. This operating-expense structure aligns with lean finance strategies and frees capital for other modernization projects. Providers shoulder hardware refresh cycles, allowing plants to gain access to the latest sensors without requiring new approvals. In outcome-based variants, fees hinge on verified quality KPI improvements, aligning vendor incentives with production goals and stimulating continuous algorithm refinement. As a result, facilities can trial vision AI in isolated stations and later roll out factory-wide with predictable payback schedules.

Deep-Learning Accuracy Breakthroughs in Defect Detection

Vision Transformer architectures achieve detection accuracy that surpasses that of older convolutional networks by eight percentage points, enabling the reliable identification of hairline cracks and subtle surface blemishes.[1]IEEE Computer Society, “Vision Transformer Architectures for Defect Detection,” ieee.org Synthetic image generation produces vast labeled datasets from limited sample parts, tackling the rarity problem that once hindered model robustness. Edge inference chips now process frames in under 10 milliseconds, an essential threshold for lines moving more than 1,000 units per minute. Federated learning securely shares model weights among facilities, raising accuracy without compromising proprietary product geometries. Together, these innovations democratize high-precision inspection, letting smaller plants gain competencies previously reserved for global conglomerates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IP And Data-Sovereignty Concerns with Cloud Inspection | -1.2% | Europe and China most affected by regulations | Short term (≤ 2 years) |

| Complex Integration with Legacy Automation Assets | -0.9% | Global, particularly in established manufacturing regions | Medium term (2-4 years) |

| Volatile GPU-Cloud Pricing Impacts Service Margins | -0.7% | Global, affecting service providers' profitability | Short term (≤ 2 years) |

| Shortage Of Vision-AI Implementation Talent | -0.8% | Global, most acute in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

IP and Data-Sovereignty Concerns with Cloud Inspection

Manufacturers handling proprietary designs are hesitant to stream production imagery to distant data centers, fearing IP leakage and potential regulatory penalties under the GDPR or China’s Cybersecurity Law. Hybrid topologies address these barriers by hosting inference engines on factory servers while relaying anonymized performance statistics to the cloud for analytics. Nevertheless, this dual-stack architecture adds 25-40% to deployment budgets and demands sophisticated DevSecOps oversight. Sensitive sectors, such as aerospace, often employ encryption and air-gapping measures that restrict external connectivity, slowing rollout schedules and tempering short-term revenue realization for service providers.

Shortage of Vision-AI Implementation Talent

The intersection of optics, AI, and industrial engineering remains a niche skill set. A majority of plants report prolonged hiring cycles for roles such as machine-vision integration engineer or AI process specialist. Vendors invest heavily in onboarding programs that blend academic computer-vision theory with shop-floor realities, such as vibration and fluctuating illumination. This learning curve can stretch project timelines by several months, especially in brownfield sites where legacy PLCs require bespoke interfaces. Although universities are expanding curricula, the depth of practical expertise develops only through multi-year exposure to live production lines, implying a persistent skills gap through the forecast horizon.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Solutions Bridge Security Gaps

Hybrid architectures rose quickly because they allowed firms to keep sensitive defect images within plant networks while leveraging cloud elasticity for model training. The Vision Inspection and Inline QA as a Service market size associated with hybrid deployments is projected to compound at 8.62% annually until 2031, outpacing the total market by more than one percentage point. Early adopters in regulated pharmaceuticals cited immediate regulatory compliance wins following the switch to split-processing topologies.

Hybrid rollouts also leverage edge accelerators embedded directly in smart cameras, eliminating round-trip latency and enabling inspection rates of over 500 frames per second for high-speed bottling or SMT lines. Vendors are increasingly pre-packaging IT-OT security modules, allowing hybrid systems to link smoothly with zero-trust architectures. Cloud-first plants still dominate overall revenue, but hybrid offerings serve as door-openers for risk-averse segments, broadening the Vision Inspection and Inline QA as a Service market footprint across geographies bound by strict privacy codes.

By Offering Type: Platform Integration Drives Growth

SaaS subscriptions delivered 45.88% of sector revenues in 2025 thanks to simplified browser-based configuration and automatic feature rollouts. The Vision Inspection and Inline QA as a Service market share, currently dominated by Platform-as-a-Service, is projected to grow rapidly, driven by a 9.33% CAGR, as factories increasingly favor holistic control towers over isolated applications. Early movers appreciate PaaS dashboards that unify inspection results with OEE metrics, spare-parts inventories, and predictive maintenance alerts.

PaaS ecosystems also nurture third-party connectors that extend vision analytics into SAP or Oracle ERP suites, reducing integration workloads for plant IT teams. Hardware-as-a-Service, although smaller, is gaining traction in remote regions lacking robust supply chains, where leasing enclosures and lighting rigs reduces import logistics. Across all models, multi-tenant designs reduce per-user compute costs, freeing vendor R&D budgets for continual algorithmic refinements that sustain competitive differentiation.

By Service Model: Outcomes Replace Inspections

Traditional per-inspection billing began to lose relevance as plants demanded ROI alignment. By 2025, subscription contracts held the majority share at 50.64%, but outcome-based deals are gaining favor and are expected to expand faster than any other pricing method at a 9.9% clip. Providers backstop their performance guarantees with redundant camera arrays and continuous model retraining, ensuring 95% or higher detection rates even amid significant changes or seasonal lighting shifts.

Outcome agreements convert quality problems into quantifiable savings, such as scrap reductions or declines in warranty claims, and CFOs increasingly weigh these savings against fee structures during purchasing cycles. Although contract drafting grows more complex, requiring shared data on baseline defect rates, successful pilots foster deep, multi-year relationships in which vendors co-innovate with clients on broader automation roadmaps.

By End-User Industry: Electronics Lead, Logistics Accelerate

Electronics plants accounted for 27.95% of 2025 revenues, driven by semiconductor back-end packaging and high-density PCB assembly that impose micron-level tolerances. The Vision Inspection and Inline QA as a Service market size for electronics lines is expected to continue rising as chiplet architectures and advanced packaging increase the number of inspection points per device.

Logistics and e-commerce hubs are the breakout vertical, forecast to book a 9.31% CAGR. Camera tunnels now verify barcode readability, detect crushed parcels, and confirm dimensional accuracy before loading bays, ensuring next-day delivery SLAs. The automotive, pharmaceutical, and food industries maintain healthy growth trajectories, supported by stringent compliance codes, but do not match the speed of parcel-handling deployments that integrate inspection with robotic sorting arms.

Geography Analysis

Asia-Pacific, responsible for 33.78% of 2025 sales, benefits from dense contract-manufacturing clusters that share support infrastructure and talent pools. Chinese policy incentives fund AI upgrades in thousands of SMEs, while Japanese Tier 1 automotive suppliers lead in process-specific vision algorithms that scrutinize paint gloss uniformity at line speeds exceeding 600 bodies per day. Taiwanese PCB specialists utilize federated defect libraries to harmonize standards across multi-site networks and expedite ramp-up when onboarding new consumer electronics customers.

North America follows closely, buoyed by automotive recall avoidance imperatives and aerospace traceability mandates. U.S. plants tend to gravitate toward outcome-based contracts that shift risk to suppliers, while Canadian resource processors adopt vision systems for timber grading and ore quality checks, thereby broadening the reach of the Vision Inspection and Inline QA as a Service market beyond discrete manufacturing. [2]U.S. Food and Drug Administration, “21 CFR Part 11 Electronic Records Guidance,” fda.gov Mexico’s rapidly expanding appliance and electronics corridors create additional green-field opportunities for cloud-ready inspection stacks. Europe sustains mid-single-digit growth under the weight of GDPR, which channels many deployments into hybrid configurations. German OEMs integrate inline QA with upstream digital twins, feeding real-time measurements into simulation models that refine design tolerances. In contrast, the Middle East is poised for the fastest advance, with Vision 2030 programs allocating automation budgets that push regional CAGR to 9.07%. Green-field plants in Saudi Arabia and the United Arab Emirates leapfrog legacy limitations by embracing cloud-native QA services from day one, while localized data centers meet sovereignty rules and accelerate adoption across GCC members.

Competitive Landscape

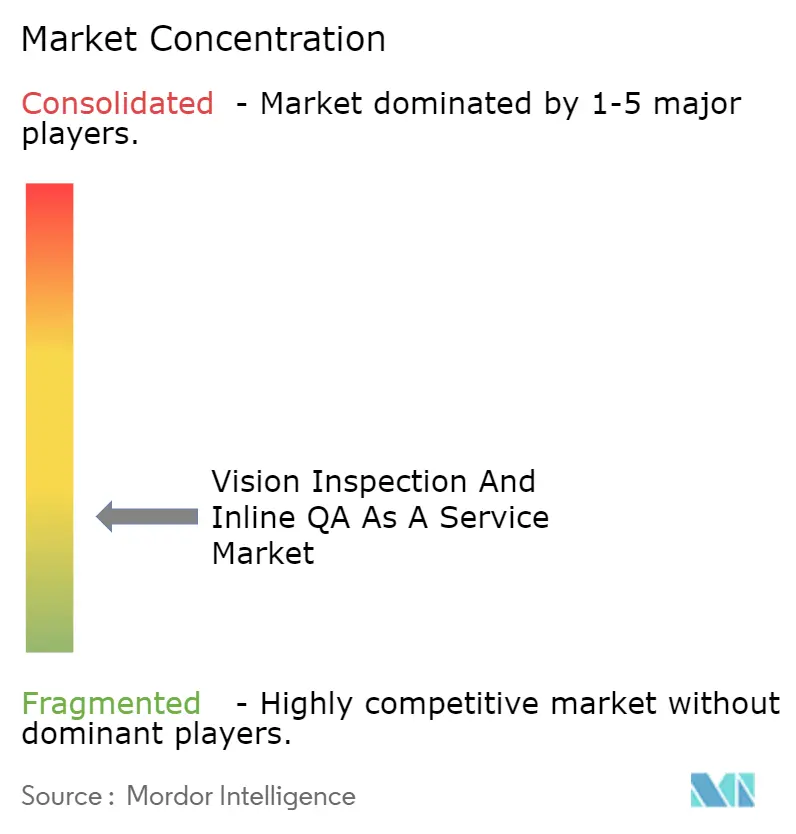

The market remains moderately fragmented because no single vendor has successfully addressed every vertical and deployment scenario. Classic machine-vision original-equipment firms defend incumbency with deep optics expertise and extensive installer networks. However, cloud hyperscalers and AI-first startups enter the market via scalable subscription models that bypass high upfront hardware costs, enticing smaller factories to pilot their services. Hardware differentiation is fading as commodity sensors flood the supply chain; instead, model accuracy, ease of integration, and pricing alignment are distinguishing the winners.

Strategic collaborations proliferate. Automation stalwarts license startup neural-network engines to revitalize their product portfolios, while camera manufacturers integrate edge GPUs to support increasingly richer models without requiring host PCs.[3]Amazon Web Services, “Computer Vision for Manufacturing,” aws.amazon.com System integrators bundle no-code ML platforms with cobots, enabling mid-tier plants to automate both handling and inspection simultaneously. Buyers favor vendors that provide turnkey connectors into major MES suites, as seamless data flow now outranks raw pixel resolution in purchasing criteria.

Startups build defensible moats around federated learning networks that aggregate millions of annotated samples across customers yet preserve confidentiality. Such collective intelligence can boost detection accuracy several percentage points above siloed rivals, and cost to replicate is steep. Meanwhile, hyperscalers pad service stickiness by embedding inspection results inside broader cloud analytics and IoT dashboards, encouraging customers to standardize on their platforms for all operational data.

Vision Inspection And Inline QA As A Service Industry Leaders

Instrumental Inc.

Landing AI Inc.

Qualitas Technologies Pvt Ltd

Cyth Systems Inc.

Visionerf SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: NVIDIA Corporation invested USD 50 million in federated-learning infrastructure aimed at collaborative defect-detection model training across dispersed plants.

- February 2025: Siemens AG and Microsoft jointly unveiled an integrated Platform-as-a-Service offering that binds vision inspection with ERP and MES layers for mid-market manufacturers.

- February 2025: Intel Corporation added sub-5 millisecond edge-processing features to its Industrial Vision platform, enabling real-time decisions on lines moving at speeds exceeding 1,000 parts per minute.

- January 2025: Amazon Web Services introduced an outcome-based pricing tier that guarantees 95% detection accuracy and levies penalties if performance dips below contract thresholds.

Global Vision Inspection And Inline QA As A Service Market Report Scope

| Cloud-based |

| On-premise |

| Hybrid |

| Hardware-as-a-Service (HaaS) |

| Software-as-a-Service (SaaS) |

| Platform-as-a-Service (PaaS) |

| Subscription-based |

| Pay-per-Inspection |

| Outcome-based Contracts |

| Food and Beverage |

| Automotive |

| Electronics |

| Pharmaceuticals |

| Logistics and E-commerce |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Deployment Model | Cloud-based | ||

| On-premise | |||

| Hybrid | |||

| By Offering Type | Hardware-as-a-Service (HaaS) | ||

| Software-as-a-Service (SaaS) | |||

| Platform-as-a-Service (PaaS) | |||

| By Service Model | Subscription-based | ||

| Pay-per-Inspection | |||

| Outcome-based Contracts | |||

| By End-user Industry | Food and Beverage | ||

| Automotive | |||

| Electronics | |||

| Pharmaceuticals | |||

| Logistics and E-commerce | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the Vision Inspection and Inline QA as a Service market in 2026?

The sector is valued at USD 1.69 billion in 2026 and is set to reach USD 2.41 billion by 2031, growing at a 7.4% CAGR.

Which deployment approach is expanding the fastest?

Hybrid solutions are forecast to register an 8.62% CAGR as firms balance cloud scalability with local data control.

What pricing models are gaining popularity among manufacturers?

Outcome-based contracts, where providers charge only for verified quality improvements, are advancing at a 9.9% CAGR.

Which vertical offers the strongest near-term growth?

Logistics and e-commerce facilities are expected to grow the fastest, with a 9.31% CAGR driven by the increasing need for parcel inspections.

Why are deep-learning advances important for inline QA?

Vision Transformer models now achieve 97% defect classification accuracy, enabling the reliable detection of subtle anomalies without requiring human review.

What is the main barrier to faster adoption globally?

A skill shortage in implementing AI-driven vision systems inflates project timelines and raises integration costs, particularly in developed markets.

Page last updated on: