Video Surveillance As A Service (VSaaS) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

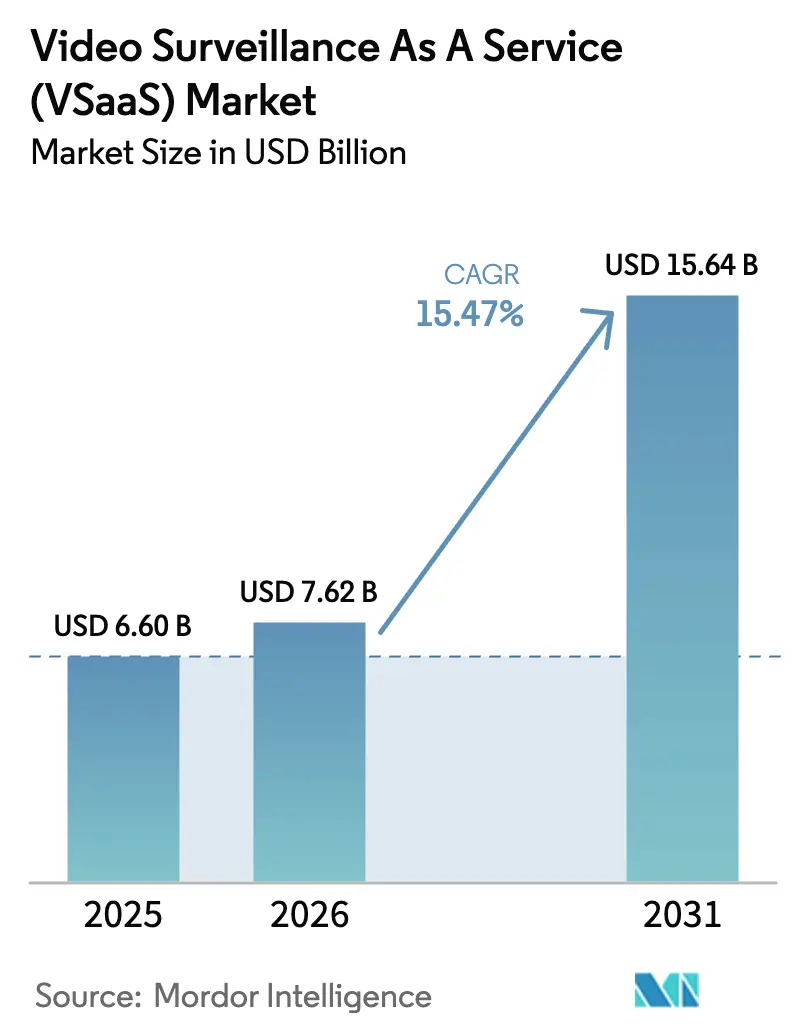

| Market Size (2026) | USD 7.62 Billion |

| Market Size (2031) | USD 15.64 Billion |

| Growth Rate (2026 - 2031) | 15.47% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

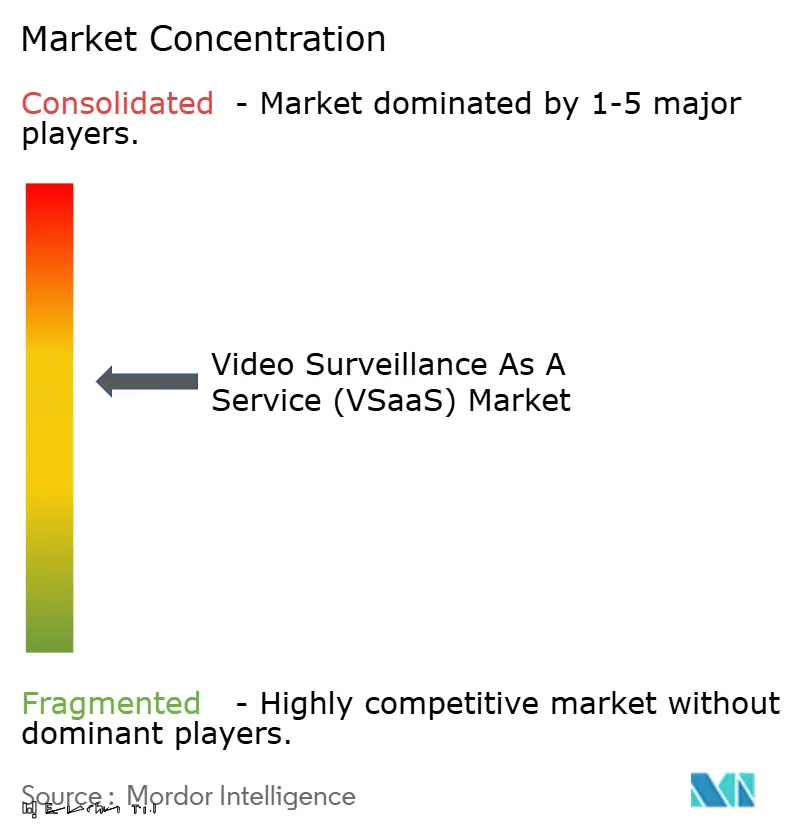

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Video Surveillance As A Service (VSaaS) Market Analysis by Mordor Intelligence

The video surveillance as a service market size in 2026 is estimated at USD 7.62 billion, growing from 2025 value of USD 6.60 billion with 2031 projections showing USD 15.64 billion, growing at 15.47% CAGR over 2026-2031. Momentum stems from enterprises shifting away from capital-intensive, on-premise video management toward subscription-based cloud delivery. Edge-AI cameras are cutting bandwidth by up to 70% and allowing higher-resolution feeds to move to the cloud at sustainable cost, while 5G corridors in China, the UAE, and the Nordics unlock ultra-low-latency analytics. Insurance incentives, ESG directives that replace diesel guard tours, and post-COVID municipal budgets favoring operational expenditure all reinforce uptake. Collectively these factors push the video surveillance as a service market toward scale economies, richer analytics, and wider acceptance as a strategic operational tool.

Key Report Takeaways

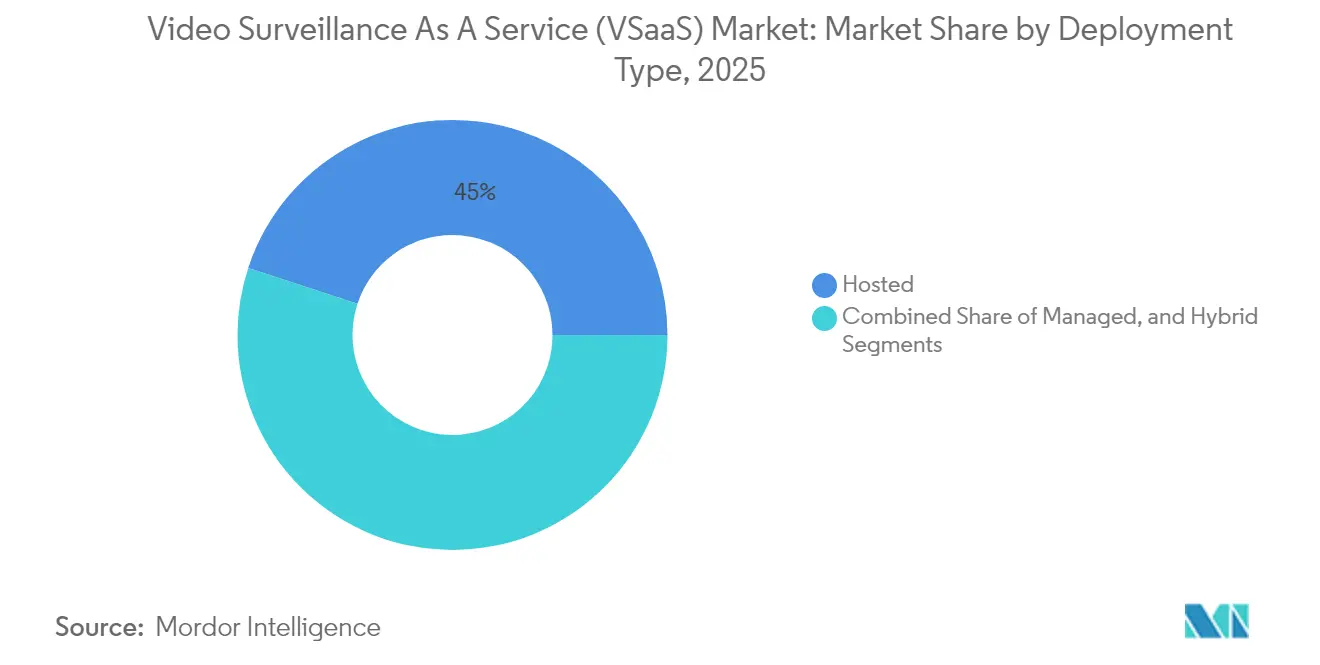

- By deployment model, hosted solutions held 44.95% revenue share in 2025; hybrid deployments are set for the fastest 16.97% CAGR through 2031.

- By AI feature, standard non-AI systems retained 62.92% of the video surveillance as a service market share in 2025, while AI-enabled offerings are projected to expand at 17.46% CAGR.

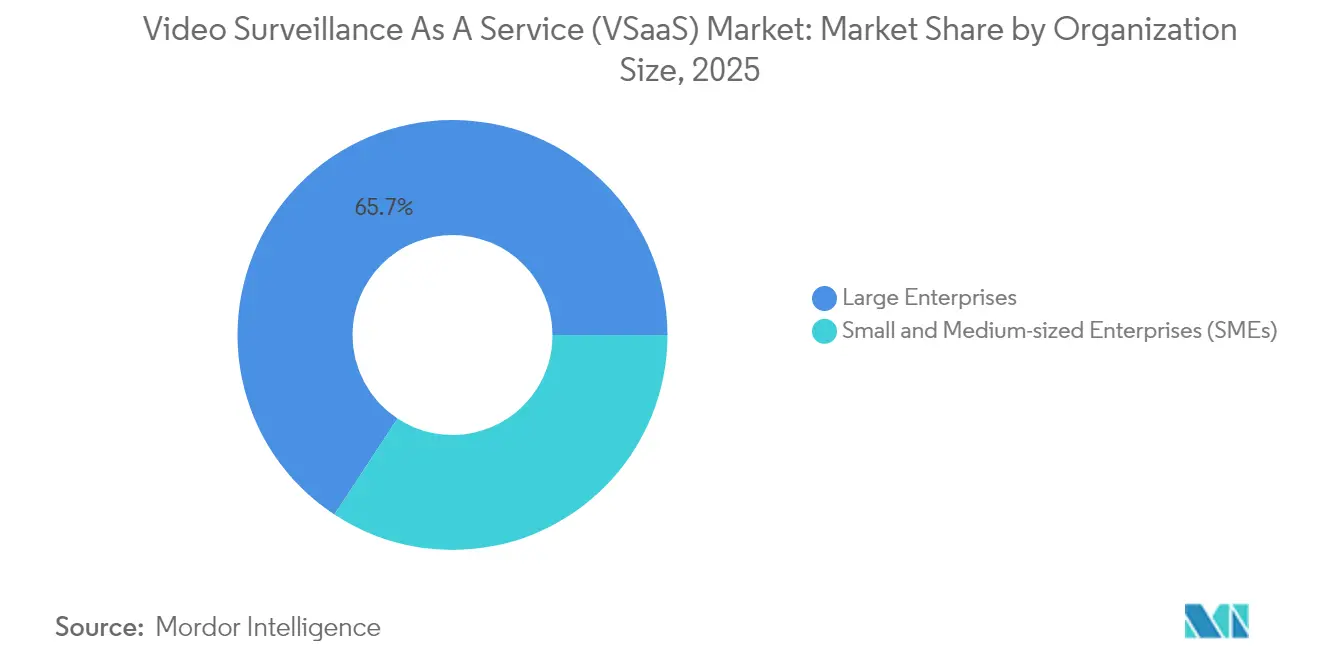

- By organization size, large enterprises captured 65.74% of 2025 revenue; small and medium-sized enterprises will post the highest 16.29% CAGR to 2031.

- By vertical, commercial applications led with 36.62% share in 2025; infrastructure-focused smart-city and traffic projects will accelerate at a 15.82% CAGR.

- By geographically, North America dominated with 34.91% share in 2025, whereas Asia will deliver the highest 15.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Video Surveillance As A Service (VSaaS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Proliferation of Edge-AI Cameras Enabling Cost-Efficient Cloud Off-load | +2.8% | Global, with early adoption in North America & APAC | Medium term (2-4 years) |

| Accelerated 5G Roll-outs in Smart-City Corridors (China, UAE, Nordics) | +2.1% | APAC core, spill-over to MEA and Europe | Short term (≤ 2 years) |

| Insurance Premium Discounts for VSaaS-Protected Commercial Assets (U.S., U.K.) | +1.5% | North America & Europe | Medium term (2-4 years) |

| ESG-Driven "Green Surveillance" Mandates Replacing Diesel Guard Tours (EU) | +1.2% | Europe, expanding to North America | Long term (≥ 4 years) |

| Shift from Cap-Ex to Op-Ex Procurement in Post-COVID Municipal Budgets | +1.9% | Global, with emphasis on developed markets | Short term (≤ 2 years) |

| Integration of VSaaS with Gen-AI Video Summaries for Retail Loss Prevention | +1.8% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Proliferation of Edge-AI Cameras Enabling Cost-Efficient Cloud Off-load

Edge-AI cameras conduct primary analytics locally, transmitting only metadata or critical clips to the cloud, driving bandwidth savings and faster incident response. Intel documented that intelligent multimodal security architectures lower outbound traffic by 70% and allow compliance with sovereignty rules by retaining raw footage onsite while still leveraging cloud analytics. [1]Intelligent Systems Group, “Demystifying Intelligent Multimodal Security Systems,” Intel, intel.comGlobal industrial and infrastructure operators are therefore scaling 4K fleets without incurring proportionate network cost, pushing the video surveillance as a service market into higher-definition use cases.

Accelerated 5G Roll-outs in Smart-City Corridors (China, UAE, Nordics)

China’s 800 smart-city pilots rely on 5G to interlink thousands of nodes, enabling dynamic video routing and integrated response systems.[2]China Smart Cities Task Force, “Smart Cities Development Report,” U.S.–China Economic and Security Review Commission, uscc.govSimilar city-scale deployments in Dubai and Helsinki demonstrate that millisecond latency transforms public-safety workflows from reactive evidence gathering to live, situational command. This connectivity premium positions local operators to deliver differentiated services, sustaining premium pricing within the video surveillance as a service market.

Insurance Premium Discounts for VSaaS-Protected Commercial Assets (U.S., U.K.)

U.S. and U.K. insurers offer 5–15% premium reductions when policyholders deploy certified cloud surveillance. The actuarial impact—lower theft claims, faster liability resolution—feeds explicit ROI models for retailers and logistics operators, converting security from cost center to risk-mitigation asset. As actuarial evidence grows, insurance-linked adoption continues to fuel the video surveillance as a service market.

ESG-Driven “Green Surveillance” Mandates Replacing Diesel Guard Tours (EU)

The EU Green Deal encourages electrification and emissions cuts across security operations. Logistics parks and corporate campuses replace diesel patrols with solar-powered cameras and cloud monitoring, cutting fuel consumption and aligning with scope-3 reporting. Compliance-driven upgrades pull VSaaS contracts into facilities budgets historically reserved for fleet operations, broadening addressable spend.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Sovereign-Cloud Requirements Hindering Cross-Border Footage Storage (EU) | -2.3% | Europe, expanding to other regions | Short term (≤ 2 years) |

| Escalating Egress Bandwidth Fees in Tier-2 and -3 Cities | -1.8% | Global, particularly emerging markets | Medium term (2-4 years) |

| Vendor-Lock-in Concerns Around Proprietary Video Codecs | -1.2% | Global | Long term (≥ 4 years) |

| Public Backlash on Continuous Facial-Recognition in Democracies (Canada, Germany) | -1.9% | North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Sovereign-Cloud Requirements Hindering Cross-Border Footage Storage (EU)

European regulators increasingly demand in-region storage for video evidence. Vendors must spin up dedicated zones or partner with local IaaS providers, lifting unit cost and complicating pan-EU fleet management. The resulting price pressure could slow conversion to pure cloud subscription models, tempering growth in the video surveillance as a service market across compliance-heavy sectors.

Public Backlash on Continuous Facial Recognition in Democracies (Canada, Germany)

Municipal moratoria and privacy advocates continue to scrutinize live face matching. This tension forces providers to build opt-in workflows, field-select algorithmic transparency tools, and, in some cities, turn off biometric features entirely. The compromise lengthens sales cycles and shifts R&D budgets toward privacy-preserving analytics, moderating near-term AI uptake within the video surveillance as a service market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Hybrid Models Bridge Legacy Infrastructure

Hosted services accounted for 44.95% revenue in 2025 as firms embraced fully managed storage, authentication, and firmware management. Hybrid configurations, however, will pace the segment at a 16.97% CAGR because enterprises can attach existing NVRs and cameras to the cloud, mitigating rip-and-replace costs. This dual-stack pathway makes hybrid the pragmatic gateway into the video surveillance as a service market for asset-heavy verticals such as manufacturing and airports. Vendors providing unified dashboards that abstract on-premise and cloud devices are winning multi-year contracts and demonstrating stickier ARR profiles.

Migration agility also helps municipalities comply with sovereign-cloud mandates: sensitive feeds remain local while metadata-driven AI runs off-site. Consequently, hybrid architectures serve as hedges against evolving data localization rules, reinforcing their strategic importance in the broader video surveillance as a service market.

By AI Feature: Standard Solutions Maintain Dominance Despite AI Acceleration

Standard, non-AI offerings held 62.92% of 2025 revenue, underscoring that many organizations still prioritize resilient storage and basic remote access. Yet AI-ready subscriptions are climbing 17.46% annually, reflecting cost declines in GPU compute and demand for behavior analytics. As more cloud platforms embed pretrained models into base tiers, AI will become table stakes rather than premium add-on, gradually tipping revenue mix toward intelligence-driven services across the video surveillance as a service market size for AI-enabled segments.

AI adoption is strongest in logistics and multi-store retail where exception detection directly ties to shrinkage KPIs. These measurable ROI gains shorten payback, accelerating conversion from standard tiers. Even conservative sectors such as utilities now pilot anomaly detection for perimeter monitoring, signaling an inevitable rise in AI penetration across the video surveillance as a service industry.

By Organization Size: SMEs Drive Future Growth Through Democratized Access

Large enterprises formed 65.74% of 2025 spend owing to multi-campus rollouts and custom integrations. However, subscription pricing and plug-and-play hardware bundles lower entry barriers for SMEs, who will expand at a 16.29% CAGR. Verkada, for example, moved downstream by packaging cameras, environmental sensors, and five-year software licenses in a single invoice, winning schools and clinics that lack full-time IT staff.

SME influx diversifies demand patterns—favoring mobile apps, automatic firmware updates, and bundled cyber insurance endorsements. This tailwind broadens the video surveillance as a service market size for cost-sensitive tiers and encourages vendors to introduce lightweight SKUs with shorter contract terms.

By Vertical: Infrastructure Applications Accelerate Smart-City Adoption

Commercial deployments remain the revenue anchor at 36.62% share, particularly in finance, retail, and hospitality where compliance and customer experience converge. Infrastructure projects—smart-city traffic cameras, public-transport hubs—will record a 15.82% CAGR as governments integrate video feeds with IoT sensor layers to orchestrate lighting, parking, and emergency response in real time.

India’s 2025 CCTV standards push requires compliant cybersecurity and quality certification, driving municipalities toward cloud platforms that guarantee firmware provenance and audit trails. Such mandates reinforce the video surveillance as a service market share for certified vendors and create export blueprints for other emerging economies.

Geography Analysis

North America led with 34.91% revenue in 2025, buoyed by early cloud normalization, strong channel ecosystems, and national retailers standardizing on SaaS video platforms. Federal stimulus for critical-infrastructure resilience further accelerates upgrades, and insurance-risk models incentivize private fleets to switch. Yet public debate over live facial recognition imposes state-level variability that vendors must navigate through modular feature licensing.

Asia-Pacific will grow fastest at 15.93% CAGR as smart-city megaprojects in China, India, and Southeast Asia demand massive, centrally managed camera fleets. 5G densification allows city planners to layer AI analytics across intersections and transit hubs, creating proof points that inspire neighboring municipalities. Local data-sovereignty rules encourage partnerships between global VSaaS brands and regional cloud operators, shaping a federated delivery model within the video surveillance as a service market.

Europe combines sophisticated demand with stringent privacy. The EU’s sovereign-cloud push forces replication of storage clusters inside member borders, elevating operating cost but also fostering domestic IaaS alliances. Nordic regions remain exemplars of 5G-enabled surveillance, while Germany and France advance cautiously under biometric-use moratoria. The Middle East, led by the UAE, invests heavily in integrated command centers, though broader MEA adoption is gated by connectivity and skills gaps.

Competitive Landscape

The field features a blend of traditional camera manufacturers retrofitting cloud stacks and born-in-the-cloud challengers scaling ARR. Verkada’s USD 4.5 billion valuation underscores capital markets’ preference for subscription revenue and verticalized hardware-software integration. AlwaysAI’s computer-vision SDK pact with Eagle Eye injects AI differentiation into a mature VMS platform, illustrating coopetition where pure-play analytics firms embed within incumbent ecosystems.

Hardware incumbents such as Hikvision and Dahua race to retain install-base relevance by exposing REST APIs and launching tiered cloud archives, yet must reconcile legacy codec lock-in concerns. Channel partners increasingly bundle finance plans, cybersecurity SLAs, and insurance endorsements, turning VSaaS into an outcome-based procurement anchored on risk reduction rather than camera count. As M&A consolidates niche analytics engines into platform suites, the video surveillance as a service market edges toward moderate concentration, though long-tail regional specialists remain active in project-based smart-city bids.

White-space lies in industrial IoT convergence: platforms that fuse SCADA data with real-time video for predictive maintenance can unlock cross-functional budgets. Vendors able to certify for critical-infrastructure cybersecurity standards (IEC 62443, ISO 27001) will gain durable competitive moats as governments tighten procurement baselines.

Video Surveillance As A Service (VSaaS) Industry Leaders

ADT Inc.

Johnson Controls International Plc

Axis Communications AB

Avigilon

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: India enacted mandatory BIS certification for all CCTV devices, pushing manufacturers toward cyber-secure by design production and opening opportunities for compliant VSaaS integrators.

- February 2025: Verkada closed a funding round led by General Catalyst, lifting valuation to USD 4.5 billion and earmarking capital for international channel expansion and AI chip R&D.

- December 2024: Convergint partnered with Verkada to bundle cloud video and access control into municipality-friendly service contracts, aligning with op-ex procurement trends.

- October 2024: alwaysAI integrated its computer-vision pipeline with Eagle Eye Networks’ VMS, bringing object detection and automated summaries to existing cloud camera fleets.

Global Video Surveillance As A Service (VSaaS) Market Report Scope

Video Surveillance as a Service (VSaaS) is a cloud-based solution enabling users to remotely access, store, and manage surveillance footage over the internet, moving away from traditional on-premise hardware. This service integrates video cameras, cloud storage, and management software, all accessible via web portals or mobile apps.

The study tracks the revenue accrued through the sale of video surveillance as a service (VSaaS) by various players across the globe. It also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The video surveillance as a service (VSaaS) market is segmented by deployment (hosted, managed, and hybrid), vertical (commercial, industrial, residential, infrastructure, public facilities & government, and defense and military), and geography (North America, Europe, Asia Pacific, Middle East and Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Hosted |

| Managed |

| Hybrid |

| Standard (Non-AI) VSaaS |

| AI-enabled VSaaS (Analytics, Facial ID, LPR) |

| Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises |

| Commercial | Retail |

| Banking and Financial Services | |

| Hospitality and Entertainment | |

| Healthcare Facilities | |

| Data Centres and Co-location | |

| Industrial | Manufacturing |

| Energy and Utilities | |

| Residential | |

| Infrastructure | Smart-City and Traffic Management |

| Transportation Hubs (Airports, Seaports) | |

| Public Facilities and Government | |

| Defense and Military |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Deployment Type | Hosted | ||

| Managed | |||

| Hybrid | |||

| By AI Feature | Standard (Non-AI) VSaaS | ||

| AI-enabled VSaaS (Analytics, Facial ID, LPR) | |||

| By Organization Size | Small and Medium-sized Enterprises (SMEs) | ||

| Large Enterprises | |||

| By Vertical | Commercial | Retail | |

| Banking and Financial Services | |||

| Hospitality and Entertainment | |||

| Healthcare Facilities | |||

| Data Centres and Co-location | |||

| Industrial | Manufacturing | ||

| Energy and Utilities | |||

| Residential | |||

| Infrastructure | Smart-City and Traffic Management | ||

| Transportation Hubs (Airports, Seaports) | |||

| Public Facilities and Government | |||

| Defense and Military | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the video surveillance as a service market?

The market is worth USD 7.62 billion in 2026 and is forecast to reach USD 15.64 billion by 2031 at a 15.47% CAGR.

Which deployment model is growing fastest?

Hybrid deployments will grow at 16.97% CAGR through 2031 as enterprises link existing cameras to cloud analytics without full replacement.

How quickly are AI-enabled VSaaS solutions expanding?

AI-ready subscriptions are projected to increase at 17.46% CAGR, outpacing standard packages as analytics move into mainstream security budgets.

Why are SMEs adopting VSaaS now?

Lower entry pricing, bundled hardware, and minimal IT overhead enable SMEs to access enterprise-grade surveillance with predictable operating expense.

Which region will offer the highest growth opportunity?

Asia-Pacific will post a 15.93% CAGR through 2031, powered by large-scale smart-city investments and 5G infrastructure rollouts.

What is the biggest regulatory hurdle for VSaaS providers?

Data-sovereignty mandates in the EU and other jurisdictions require in-country storage, raising infrastructure costs and complicating cross-border fleet management.

Page last updated on: