Global Viral Clearance Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

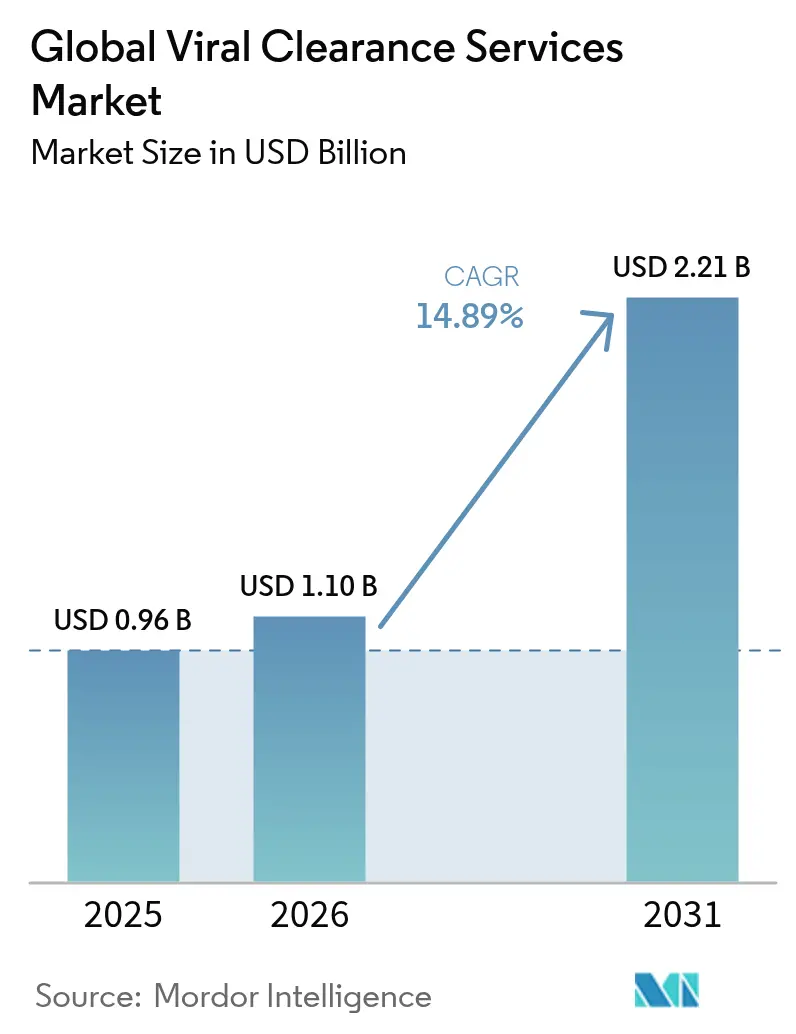

| Market Size (2026) | USD 1.1 Billion |

| Market Size (2031) | USD 2.21 Billion |

| Growth Rate (2026 - 2031) | 14.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

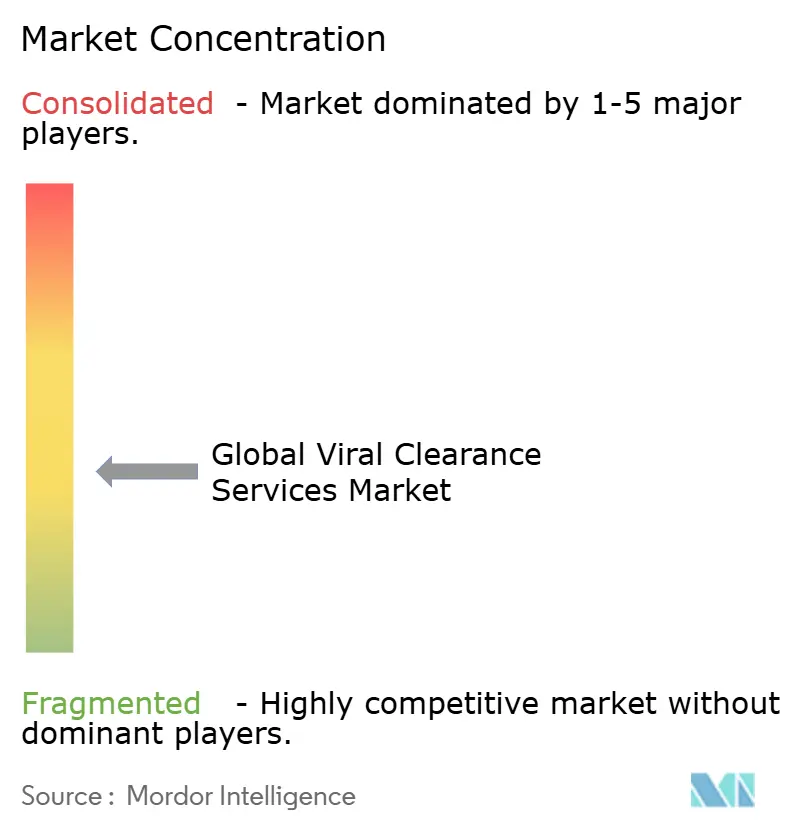

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Viral Clearance Services Market Analysis by Mordor Intelligence

The viral clearance services market size is expected to grow from USD 0.96 billion in 2025 to USD 1.10 billion in 2026 and is forecast to reach USD 2.21 billion by 2031 at 14.89% CAGR over 2026-2031. The doubling trajectory reflects surging demand for viral safety validation across biologics, vaccines, and advanced modalities such as cell and gene therapies. Platform-based validation encouraged by the United States Food and Drug Administration’s (FDA) Q5A(R2) update has shortened study timelines, turning viral clearance from a compliance checkbox into a strategic enabler of faster product launches fda.gov. Rapid expansion of adeno-associated virus (AAV) and lentiviral vector pipelines has further magnified the need for bespoke protocols, while outsourcing to specialist contract development and manufacturing organizations (CDMOs) accelerates capacity growth.

Key growth catalysts include the global renaissance in large-molecule manufacturing, harmonized regulatory frameworks across major markets, and the steady industrialization of continuous bioprocessing. Competitive dynamics are reshaping as traditional equipment vendors extend into services and specialist contract research organizations (CROs) buy manufacturing assets to provide end-to-end offerings. Despite a robust outlook, cost-intensive multi-virus studies, shortages of skilled biosafety personnel, and fragmented guidance for novel modalities pose headwinds.

Key Report Takeaways

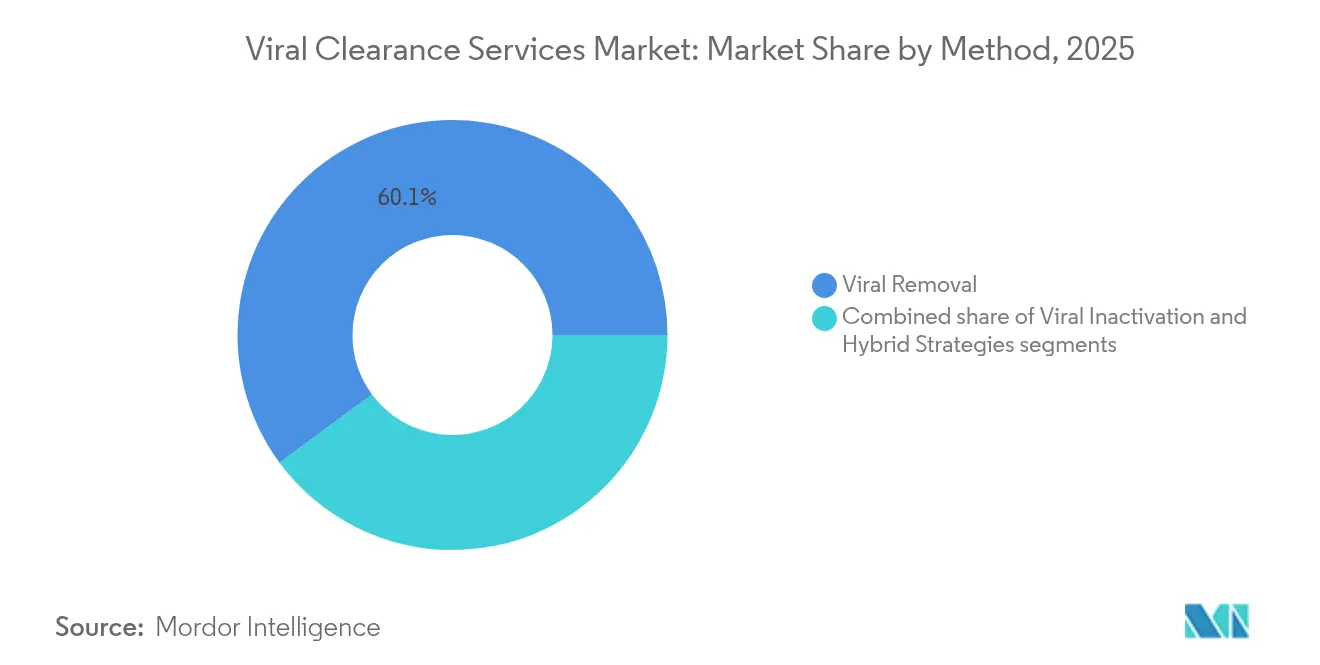

- By methodology, viral removal techniques held a 60.12% share of the viral clearance services market in 2025, while hybrid strategies are projected to grow at a 16.79% CAGR to 2031.

- By application, recombinant proteins led with 43.10% revenue share in 2025; gene and cell therapies are forecast to expand at an 17.95% CAGR through 2031.

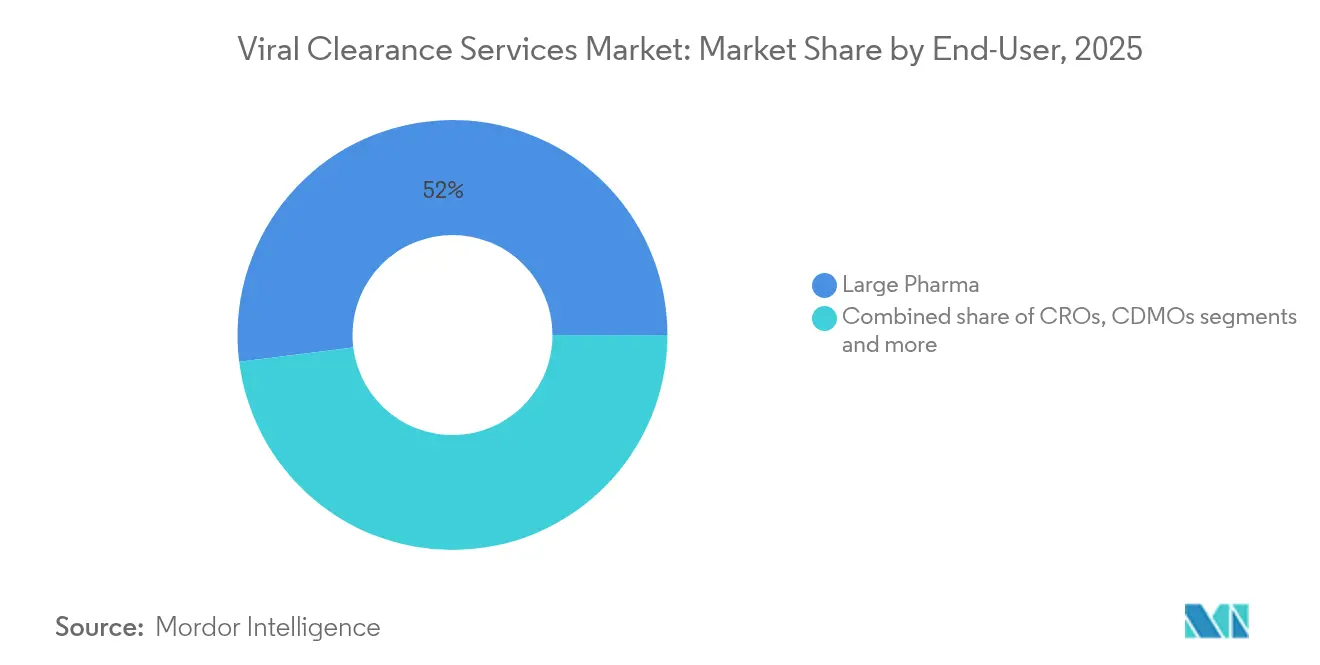

- By end-user, large pharmaceutical companies accounted for 51.98% of the viral clearance services market share in 2025, but CDMOs record the fastest projected CAGR at 16.63% through 2031.

- By geography, North America commanded 38.85% of the viral clearance services market size in 2025, whereas Asia Pacific is advancing at a 16.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Viral Clearance Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for viral safety validation in large-molecule manufacturing | +3.2% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Expanding biologics & biosimilar pipeline worldwide | +2.8% | Global, with emerging market acceleration in APAC | Long term (≥ 4 years) |

| Cell & gene therapy boom requiring bespoke protocols | +2.7% | Global, with regulatory leadership in US & EU | Long term (≥ 4 years) |

| Outsourcing surge to specialist CRO/CDMOs | +2.1% | North America & EU core, spill-over to APAC | Short term (≤ 2 years) |

| Continuous bioprocessing drives in-line clearance technologies | +1.9% | North America & EU, early adoption in select APAC markets | Medium term (2-4 years) |

| AI-enabled predictive validation platforms shorten study timelines | +1.5% | North America & EU, gradual APAC adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Viral Safety Validation in Large-Molecule Manufacturing

Large-molecule production has shifted viral clearance upstream into process design. FDA guidance[1]Food and Drug Administration, “Q5A(R2) Viral Safety Evaluation of Biotechnology Products,” fda.gov now rewards platform approaches, letting manufacturers reuse clearance data across monoclonal antibody programs while preserving safety. Continuous bioprocessing lines incorporate in-line virus filters that provide real-time assurance, improving yields and lowering re-validation costs. Companies with such integrated capabilities launch products sooner and limit regulatory queries, turning viral clearance capacity into a clear competitive advantage. Equipment innovators have responded with high-flux filters that safeguard product quality without compromising throughput.

Expanding Biologics & Biosimilar Pipeline Worldwide

More than 700 gene therapies and hundreds of biosimilars are under development, and each new entrant needs rigorous clearance. International Council for Harmonisation (ICH) efforts have standardized requirements so that a single validation package can underpin submissions on multiple continents. Service providers therefore capture a larger slice of development budgets. Eurofins Scientific, for example, has reported a rebound in large contracted studies and allocated additional capacity[2]Eurofins Scientific, “9M 2024 Trading Update,” cdnmedia.eurofins.com to viral safety work.

Cell & Gene Therapy Boom Requiring Bespoke Protocols

AAV, lentiviral, and oncolytic platforms demand protocols tuned to vector size, envelope structure, and tissue tropism. The FDA’s approval of therapies like BEQVEZ for hemophilia B underscores the maturing regulatory path, yet every new vector serotype can trigger novel safety questions. Lonza and Charles River now market vector-specific clearance panels that cut weeks off development time while maintaining global compliance. These bespoke services position providers to capture premium pricing as the gene therapy wave gains momentum.

Outsourcing Surge to Specialist CRO/CDMOs

Biopharma companies increasingly view in-house viral clearance suites as non-core, opting instead for CDMOs that run hundreds of studies annually. This model delivers economies of scale, gives smaller biotech firms instant access to seasoned virologists, and buffers large firms against sudden project surges. Merck’s USD 600 million acquisition of Mirus Bio and Charles River’s USD 292.5 million purchase of Vigene Biosciences exemplify the vertical integration shaping the viral clearance services market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost & complexity of multi-virus validation studies | -2.4% | Global, with acute impact in emerging markets | Short term (≤ 2 years) |

| Shortage of skilled virology and biosafety workforce | -1.8% | North America & EU primarily, emerging in APAC | Medium term (2-4 years) |

| Fragmented global guidance for novel modalities (e.g., AAV) | -1.2% | Global, with regulatory leadership gaps in emerging markets | Long term (≥ 4 years) |

| Supply-chain gaps in qualified model viruses & reference standards | -0.9% | Global, with concentration risks in specialized suppliers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost & Complexity of Multi-Virus Validation Studies

Comprehensive studies often involve three to five model viruses, each tested across multiple process steps. The total research outlays range from USD 500,000 to USD 2 million, straining smaller biotech budgets and deterring innovators in resource-limited regions. Reagent supply chains are fragile, with long lead times for qualified seed stocks. Service providers are countering costs by adopting non-infectious surrogates and data-rich platform validations that regulators now accept.

Shortage of Skilled Virology and Biosafety Workforce

Demand for experienced virologists has outstripped supply by 42% since 2018, according to sector analyses. Retirements in the public-health laboratory system exacerbate the gap, while academic pipelines struggle to keep pace. Firms are automating routine assays and partnering with universities on fast-track certification programs, yet talent scarcity continues to limit global capacity additions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Method: Hybrid Strategies Drive Innovation

Viral removal methods captured 60.12% of the viral clearance services market size in 2025, reaffirming their status as the backbone of bioprocess safety. Chromatography, depth filtration, and virus-retentive membranes deliver predictable log-reduction values across monoclonal antibodies and recombinant proteins. Continuous downstream trains now weave these steps into single-use, closed systems that maintain sterility while minimizing hold times.

Hybrid strategies, though accounting for a smaller base, are growing at 16.79% CAGR through 2031 and are reshaping service portfolios. Providers integrate solvent/detergent inactivation, low-pH hold, and UV-C irradiation with physical removal in deliberate sequences that address both enveloped and non-enveloped threats. Asahi Kasei’s Planova FG1 filter demonstrates how high-flux membranes accelerate throughput without sacrificing virus log-reduction factors. The viral clearance services market size for hybrid protocols is projected to expand from USD 140 million in 2025 to USD 355 million in 2031, underscoring industry appetite for multimodal resilience.

Second-generation hybrids layer high-pressure processing or nanofiltration onto legacy steps to combat robust parvoviruses. AI-guided design tools suggest optimal step combinations, reducing experimental runs by up to 30%. These innovations enhance predictability and support regulators’ push toward risk-based, science-driven validation frameworks. As continuous manufacturing gains traction, providers able to integrate hybrid modules inline will gain share at the expense of batch-oriented competitors.

By Application: Gene Therapies Reshape Validation Paradigms

Recombinant proteins held 43.10% of the viral clearance services market share in 2025, benefiting from standardized platform studies that cover multiple antibody variants. Segment efficiencies stem from shared capture, polishing, and viral reduction trains that lower marginal costs per molecule.

Gene and cell therapies, however, are expanding at an 17.95% CAGR and will reach an estimated 29.35% of the overall viral clearance services market size by 2031. AAV manufacturing shifts from adherent to suspension systems, achieving 85-95% vector recovery while imposing stringent removal of replication-competent particles. Each new serotype may necessitate fresh clearance data, limiting economies of scale but driving premium service demand. Providers offer vector-specific virus spiking panels and replicate-competent AAV assays to satisfy regulators in the United States and European Union.

Monoclonal antibodies continue steady demand as next-generation formats such as bispecifics enter clinical phases, yet clearance expectations remain familiar, easing provider workloads. Tissue- and blood-derived products require orthogonal inactivation methods to counter endogenous viruses. Vaccine manufacturers seek balance between antigen integrity and pathogen inactivation, leaning on solvent/detergent or UV-C steps combined with filtration.

By End-User: CDMOs Capture Outsourcing Wave

Large pharmaceutical companies accounted for 51.98% of viral clearance services market share in 2025, leveraging in-house biosafety labs alongside selective outsourcing for surge capacity. Internal capabilities ensure proprietary process know-how remains confidential while preserving scheduling flexibility for late-stage programs.

CDMOs, though smaller today, are outpacing all other segments at 16.63% CAGR. Massive deals such as Lonza’s USD 1.2 billion purchase of Roche’s Vacaville site have added reactor volume and biosafety suites primed for outsourced work. The viral clearance services market size attributable to CDMOs is forecast to grow from USD 270 million in 2025 to USD 680 million in 2031. Small and mid-size biotech firms gravitate toward CDMOs to avoid capital-intensive BSL-2/3 labs and to tap veteran virologists who can navigate multiple regulatory jurisdictions. CROs with specialized assay portfolios attract early-stage innovators, while academic centers focus on method development and workforce training rather than high-throughput commercial work.

Geography Analysis

North America controlled 38.85% of the viral clearance services market in 2025 and remains the global nexus for regulatory leadership, venture funding, and large-scale plant expansions. Fujifilm’s USD 1.2 billion North Carolina project will triple bioreactor output by 2031, creating new demand for integrated clearance validation. Robust supply networks for qualified model viruses, plus proximity to FDA reviewers, enhance the region’s strategic importance. The viral clearance services market size in North America is expected to climb from USD 380 million in 2025 to USD 800 million in 2031.

Europe maintains a substantial presence underpinned by the European Medicines Agency’s comprehensive viral safety guidance and the European Commission’s 2024 biotechnology strategy. Roche’s €90 million gene therapy hub in Germany and Novartis’s €40 million vector facility in Slovenia expand regional capacity. Yet Europe’s multi-country regulatory landscape and rising labor costs temper growth to single-digit CAGRs, keeping its share stable rather than expansionary.

Asia Pacific is the fastest mover, advancing at a 16.22% CAGR. China’s decision to lift foreign ownership limits for cell and gene therapy within free-trade zones and Japan’s expedited Sakigake pathway shorten approval windows and attract multinational sponsors. Regional CDMOs like WuXi Biologics and Takara Bio are investing in vector suites and high-capacity virus filtration trains. The viral clearance services market size in Asia Pacific is projected to leap from USD 210 million in 2025 to USD 518 million by 2031, closing the gap with established Western hubs. Talent shortages persist, yet government grants and university partnerships aim to broaden the virology talent pool.

Competitive Landscape

The viral clearance services market is moderately fragmented but trending toward consolidation as boundary lines blur between equipment suppliers, testing laboratories, and full-service CDMOs. Merck’s purchase of Mirus Bio for USD 600 million secures vector expertise, while Charles River’s USD 292.5 million buyout of Vigene Biosciences adds CGMP vector production to an already extensive safety testing portfolio. Such deals create one-stop shops that appeal to gene therapy sponsors needing both GMP vectors and clearance validation under one roof.

Technology leadership serves as a differentiator. Asahi Kasei’s next-generation FG1 filter, AI-guided protocol design platforms, and continuous processing modules offer measurable time and cost savings, raising customers' switching barriers. Providers that marry proprietary filters with in-house virology labs can lock in multi-year master service agreements.

White-space opportunities are richest in bespoke modalities—oncolytic viruses, mRNA, and personalized cell therapies—where standardized approaches fall short. Specialist players using machine learning to forecast clearance robustness or digital twins to simulate virus removal before wet-lab work are emerging challengers. Strategic alliances between niche AI firms and established CDMOs accelerate the commercialization of such tools.

Pricing competition remains rational owing to high technical complexity and regulator scrutiny, yet tier-2 providers in Asia are offering bundled packages to capture cost-sensitive projects. Intellectual-property protection, data integrity, and global regulatory track records continue to influence sponsor selection.

Global Viral Clearance Services Industry Leaders

Charles River Laboratories

Lonza Group

Merck KGaA

Texcell SA

WuXi AppTec

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Hovione and iBET formed ViSync Technologies to develop drug-delivery solutions for gene and cell therapies, focusing on formulation and manufacturing of advanced biologics.

- February 2025: BioCina and NovaCina concluded a merger that created an integrated CDMO spanning cell-line development to sterile fill-finish.

- January 2025: Fujifilm Diosynth Biotechnologies announced USD 8 billion in global biomanufacturing investments, including plans to double its Denmark site and triple North Carolina reactors.

- October 2024: Asahi Kasei Medical launched the Planova FG1 virus removal filter featuring higher flux and enhanced retention for biotherapeutics.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we view the viral clearance services market as third-party laboratory activities that design, execute, and document virus removal or inactivation studies on biopharmaceutical intermediates and finished biologics before regulatory submission. The work typically spans chromatography or nanofiltration step validation, solvent-detergent or low-pH inactivation, and confirmatory assays that satisfy ICH Q5A(R2) guidance.

Scope note: in-house quality-control testing performed within a sponsor's own plant and sales of stand-alone virus filtration consumables are outside our lens.

Segmentation Overview

- By Method

- Viral Removal

- Chromatography

- Protein A Capture

- Ion-Exchange

- Affinity & Mixed-Mode

- Filtration

- Nanofiltration

- Depth Filtration

- Membrane Adsorbers

- Precipitation (PEG/Ethanol)

- Chromatography

- Viral Inactivation

- Solvent/Detergent Treatment

- Low-pH Incubation

- UV-C Irradiation

- Heat / Pasteurization

- High-Pressure Processing

- Hybrid Strategies

- Viral Removal

- By Application

- Recombinant Proteins

- Monoclonal Antibodies

- Tissue & Blood-derived Products

- Vaccines

- Gene & Cell Therapies

- Viral Vectors

- Other Applications

- By End-User

- Large Pharma

- Small & Mid-size Biotech

- Contract Development & Manufacturing Organizations (CDMOs)

- Contract Research & Testing Organizations (CROs)

- Academic & Government Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with QC directors at CDMOs, viral safety officers in large pharma, and regional regulators across North America, Europe, and East Asia clarified prevailing study designs, turnaround times, and price dispersion.

Follow-up surveys with procurement heads validated the typical discount applied to list assay prices when multi-project bundles are awarded.

Desk Research

We gathered baseline inputs from tier-1 regulators and associations, such as the FDA Biologics License Application database, EMA public assessment reports, WHO biologics pipeline tracker, and the International Society for Cell & Gene Therapy newsletters, which together reveal yearly volumes of new products that must undergo viral safety work.

Trade statistics from UN Comtrade and import duties on chromatography media helped calibrate average consumables spend, while company 10-Ks and investor decks highlighted outsourcing ratios at leading CDMOs.

Subscription resources, including D&B Hoovers for financials and Dow Jones Factiva for recent contract wins, enriched revenue splits across service providers.

The sources cited are illustrative; many others informed data checks and narrative refinement.

Market-Sizing & Forecasting

We built a top-down demand pool starting with approved and late-phase biologics counts, applied therapy-specific penetration rates for outsourced viral studies, and then reconciled totals with selective bottom-up checks (sampled CDMO revenues multiplied by blended average study price).

Key variables include worldwide Phase III biologics pipeline, share of cell-and-gene therapies requiring hybrid strategies, updates to ICH Q5A, CDMO capacity additions, and currency-adjusted average study prices.

Multivariate regression combined with scenario analysis captures how pipeline growth and regulatory changes drive revenue through 2030.

Data Validation & Update Cycle

Outputs pass anomaly tests against historic outsourcing ratios, peer revenue disclosures, and macro indicators.

Senior analysts review every model; reports refresh yearly, with interim patches when major regulatory or capacity shifts occur.

Clear Reasons Our Viral Clearance Services Baseline Commands Confidence

Published estimates often diverge because firms pick differing service scopes, apply dissimilar average selling prices, or update data at unequal intervals.

Key gap drivers in this space include whether hybrid removal-inactivation protocols are counted, how list prices are discounted, and if local-currency fees are converted using spot or average annual rates. Mordor's disciplined scope alignment, dual-path validation, and annual refresh cadence narrow those variances.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.96 B | Mordor Intelligence | - |

| USD 0.83 B | Global Consultancy A | Omits hybrid protocols; counts only fee-for-service contracts |

| USD 1.13 B | Trade Journal B | Uses list prices without ASP blending and spot FX conversion |

In sum, our balanced definition, mixed top-down and bottom-up verification, and transparent variable set give decision-makers a dependable starting point, while still flagging where alternative scopes push figures higher or lower.

Key Questions Answered in the Report

What regulatory change is reshaping viral clearance strategies?

The FDA’s Q5A(R2) update endorses risk-based, platform validation, allowing data reuse across multiple biologics and shortening overall development timelines.

Which viral clearance methodology is currently favored in commercial bioprocessing?

Chromatography and depth-filtration steps remain the industry’s preferred foundation because they deliver predictable log-reduction values and integrate easily with closed, single-use downstream trains.

How is outsourcing influencing competitive dynamics among service providers?

Biopharma sponsors increasingly rely on CDMOs for biosafety studies, prompting high-value acquisitions that bundle vector production with clearance testing under one contract.

What technological innovation is boosting efficiency in virus removal?

Next-generation high-flux filters such as Planova FG1 increase throughput without sacrificing retention, supporting continuous processing workflows in large-molecule manufacturing.

Which talent challenge is constraining capacity expansion?

A global shortage of experienced virologists and biosafety professionals is delaying facility ramps and prompting firms to invest in automation and university partnerships for workforce development.

How are cell and gene therapies altering viral clearance requirements?

Vector-specific risks in AAV and lentiviral platforms demand bespoke clearance panels and replicate-competent virus assays that go beyond traditional monoclonal antibody protocols.

Page last updated on: