Medical Spa Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 26.20 Billion |

| Market Size (2031) | USD 47.17 Billion |

| Growth Rate (2026 - 2031) | 12.48% CAGR |

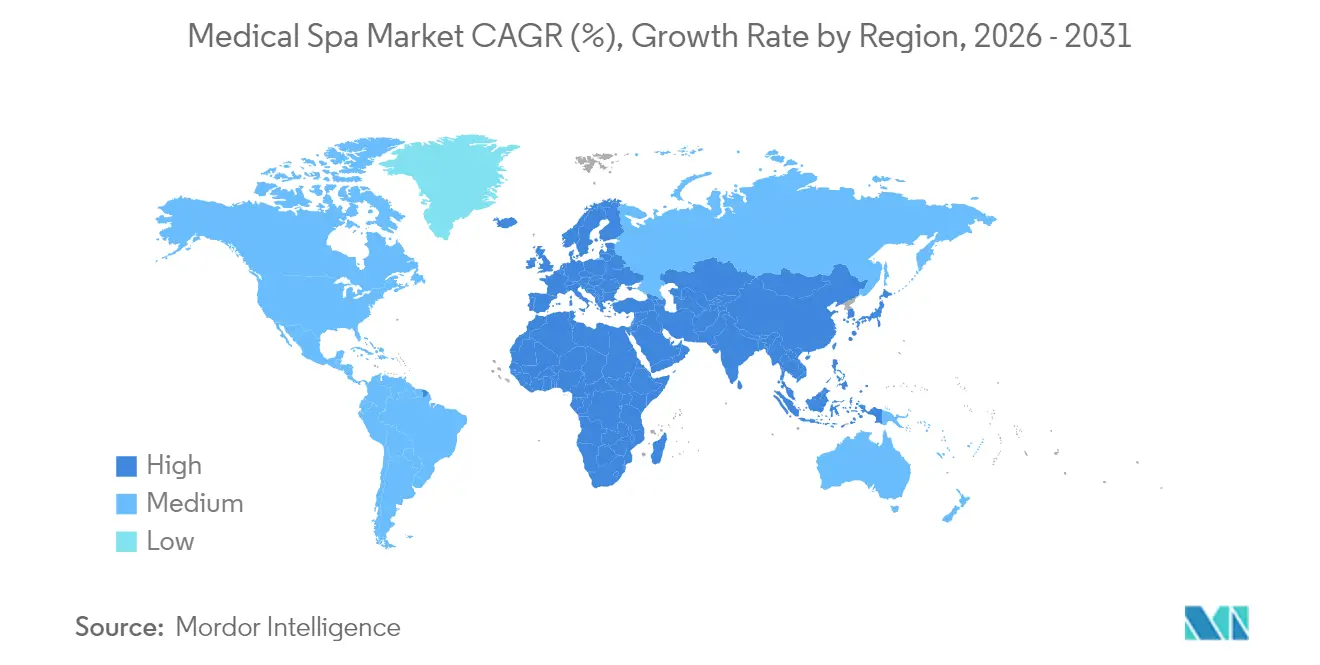

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

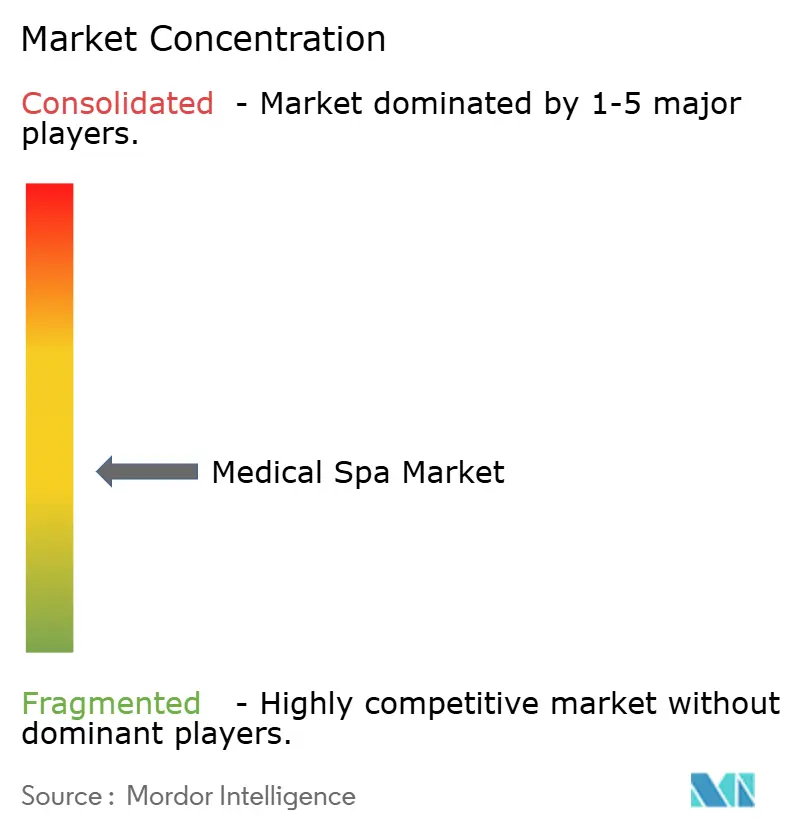

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Spa Market Analysis by Mordor Intelligence

The Medical Spa Market size is projected to be USD 23.29 billion in 2025, USD 26.20 billion in 2026, and reach USD 47.17 billion by 2031, growing at a CAGR of 12.48% from 2026 to 2031.

The acceleration reflects sustained demand for minimally invasive procedures, wider demographic appeal and continued technological upgrades such as energy-based platforms and AI-guided skin diagnostics. Investors view the medical spa market as a cash-pay, recurring-revenue segment insulated from reimbursement pressures, while consumers increasingly perceive aesthetic services as routine wellness maintenance. Asia-Pacific is becoming the principal growth engine because disposable incomes are climbing and medical tourism ecosystems are maturing, whereas North America concentrates on service sophistication and technology differentiation. Competitive intensity is rising as private equity platforms consolidate single-site operators to create multi-state brands that leverage centralized marketing, bulk equipment purchasing and compliance management.

Key Report Takeaways

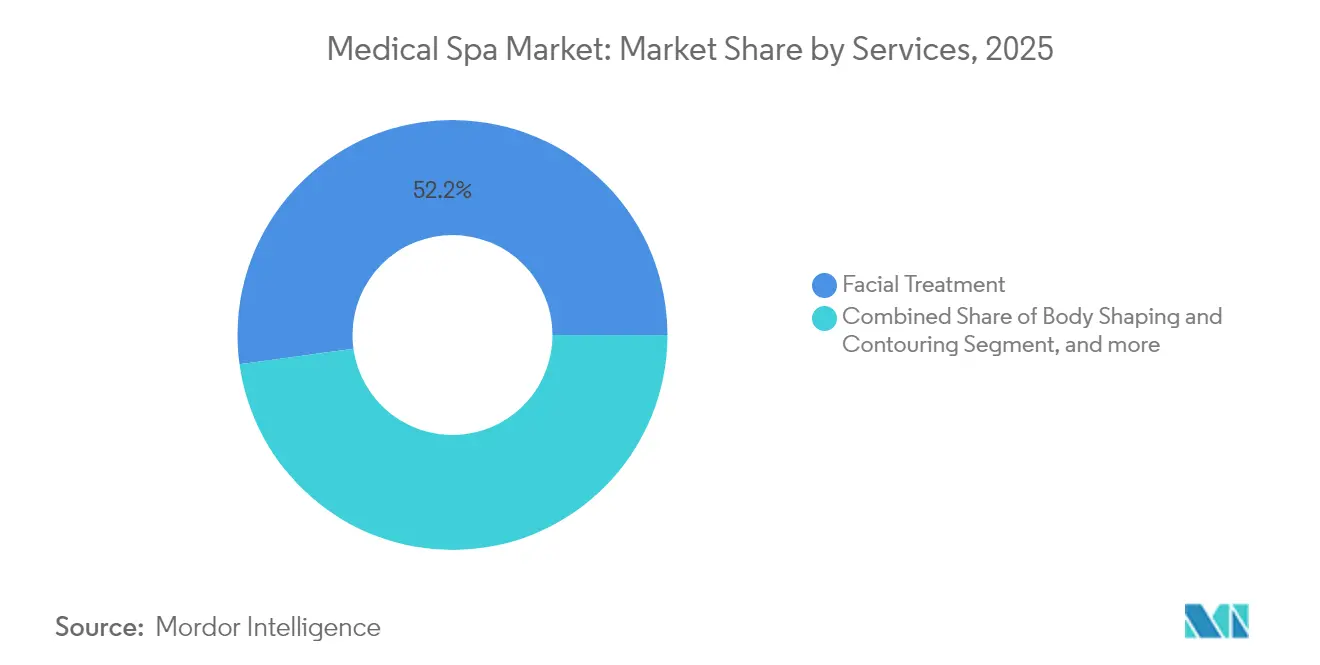

- By services, facial treatments held 52.18% of medical spa market share in 2025, while laser hair removal is advancing at a 15.22% CAGR to 2031.

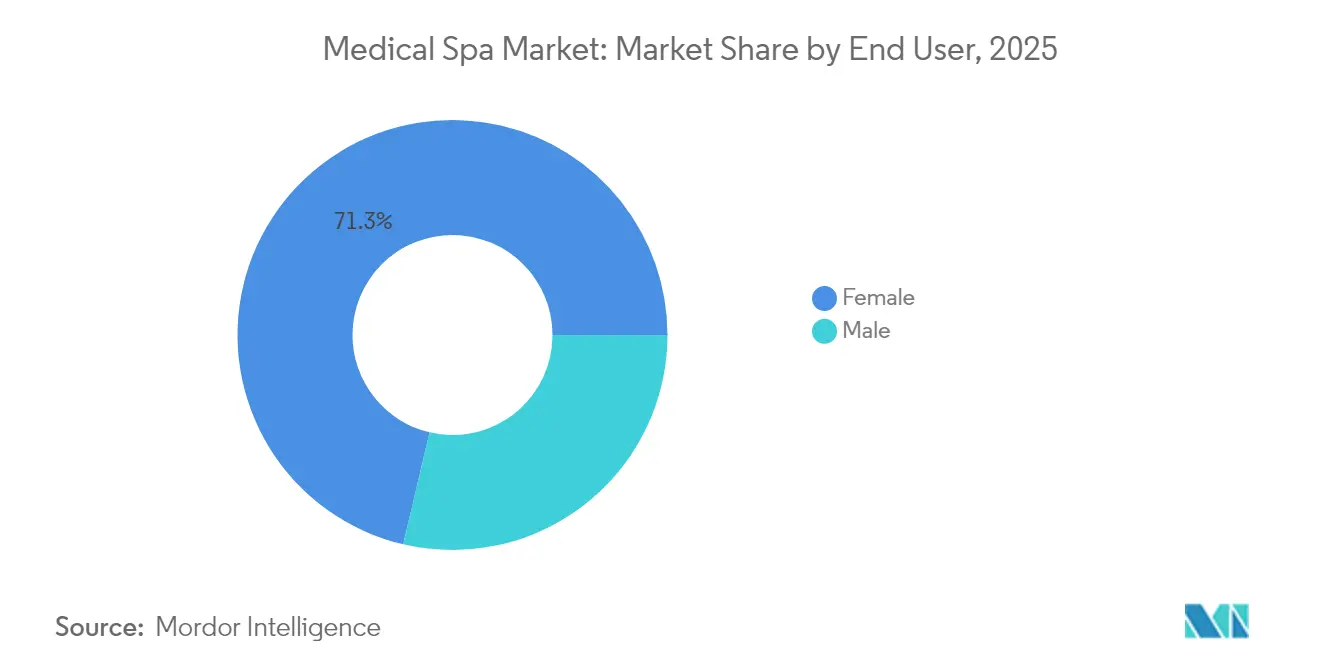

- By end user, female segment accounted for 71.32% of the medical spa market size in 2025, whereas the male segment is growing at a 15.94% CAGR through 2031.

- By geography, North America led with 36.95% revenue share in 2025; Asia-Pacific is projected to expand at a 14.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Medical Spa Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for minimally invasive cosmetic procedures | +3.2% | Global, highest in North America & Asia-Pacific | Medium term (2-4 years) |

| Influence of social media & beauty culture | +2.8% | Global, strong in North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Rising disposable income in emerging economies | +2.1% | Asia-Pacific core, spill-over to Latin America & MEA | Long term (≥ 4 years) |

| Aging population seeking anti-aging solutions | +1.9% | North America & Europe primary, Asia-Pacific secondary | Long term (≥ 4 years) |

| AI-powered personalization & skin diagnostics | +1.5% | North America & Europe early adoption, Asia-Pacific scaling | Medium term (2-4 years) |

| Subscription-based wellness models | +1.1% | North America & Europe, emerging in Asia-Pacific cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Minimally Invasive Cosmetic Procedures

Non-surgical treatments recorded 30% demand growth in 2024.[1] International Association for Physicians in Aesthetic Medicine, “Non-Surgical Procedure Trends 2024,” iapam.com Consumers value shorter recovery and natural-looking outcomes that energy-based devices and injectables can provide. The American Society for Laser Medicine and Surgery recently cleared 1,726 nm lasers for acne management, expanding the minimally invasive toolkit.[2]American Society for Laser Medicine and Surgery, “1726 nm Device Clearance,” aslms.org Integrated treatment plans that combine neuromodulators, fillers and fractional lasers replicate surgical-quality results without scalpel intervention. Clinics report rising average ticket sizes because patients now bundle multiple therapies during the same visit. This preference is reshaping staffing models by prioritizing advanced-practice providers and device specialists, reinforcing expansion across the medical spa market.

Influence of Social Media & Beauty Culture

Digital platforms introduced 48.9% of patients to their current providers, with Instagram dominating discovery at 64.1% usage. Viral aesthetics such as the “Instagram face” drive interest in cheek enhancement, lip shaping and jawline contouring. Short-form video on TikTok has normalized injectables among consumers under 30. Yet unrealistic expectations foster dissatisfaction: a recent study linked higher revision requests to social media-referred clients. Providers are responding with enhanced consultations and pre-procedure education to align outcomes with digital imagery.

Rising Disposable Income in Emerging Economies

China’s aesthetic medicine sector upheld by a growing middle class and urban lifestyle shifts. The Asia-Pacific wellness economy already represents 11% of regional GDP and is expanding 10% annually. Financing products such as installment plans and membership credits are broadening access beyond high-income tiers. Governments in Thailand, Malaysia and Indonesia are upgrading medical tourism corridors, which funnel regional demand into accredited facilities. As premium technologies become affordable through equipment leasing, tier-2 cities are emerging as new catchment areas for medical spa operators.

Aging Population Seeking Anti-Aging Solutions

Global life expectancy gains fuel interest in regenerative aesthetics as seniors pursue therapies that blend cosmetic results with wellbeing benefits. Stem-cell-derived exosomes, peptide cocktails and fractional radiofrequency-assisted microneedling are popular among baby boomers because they promise collagen restoration rather than camouflage. Mental health studies link appearance satisfaction with improved self-esteem, supporting uptake among older adults. Providers bundle skin resurfacing with wellness services such as IV nutrition to deliver holistic age-management programs. The trend is especially pronounced in Europe, where preventive health budgets qualify certain aesthetic services as quality-of-life interventions, further supporting the medical spa market.

Restraints Impact Analysis of Medical Spa Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of equipment & advanced procedures | -2.1% | Global, heavier on smaller operators | Medium term (2-4 years) |

| Limited insurance coverage for aesthetic services | -1.8% | North America & Europe primary, emerging Asia-Pacific | Long term (≥ 4 years) |

| Shortage of certified practitioners & regulatory complexity | -1.5% | Global, acute in fast-growing markets | Short term (≤ 2 years) |

| Cybersecurity & data privacy risks | -0.9% | Global, highest in regulated markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Equipment & Advanced Procedures

State-of-the-art energy platforms can cost more than USD 500,000 per site and require updates within five years. Leasing mitigates upfront cash but lifts long-term expense as bundled service contracts add 10%-15% to annual outlay.[3]Asian Development Bank, “Wellness Economy in Asia-Pacific,” adb.org The financial burden splits the market: multi-site chains deploy the newest lasers, while small clinics extend depreciation cycles and risk obsolescence. Vendors have started subscription plans where disposable applicators and maintenance are packaged into per-treatment fees, but margins compress when utilization falters. This capital intensity constrains entry in rural zones and slows technology diffusion, creating structural challenges for the medical spa market.

Limited Insurance Coverage for Aesthetic Services

Most nations classify elective aesthetics outside public or private health benefit schedules. Patients therefore fund 100% of treatment costs, which restrains frequency among middle-income groups. Medical credit cards and BNPL platforms raise adoption but carry interest rates that reach 26%, leading cautious consumers to delay repeat sessions. Lack of transparent pricing complicates budgeting because quotes for a single laser resurfacing series can vary twofold within the same metro. Without broader reimbursement, providers must continuously demonstrate value through outcome tracking and bundled maintenance memberships.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Medical Spa Market Segment Analysis

By Services:

Market Leaders and Emerging WinnersFacial treatments generated 52.18% of 2025 revenue, cementing their role as the anchor product line that draws regular appointments and cross-selling opportunities. The medical spa market size for facial rejuvenation is forecast to grow further as clinics integrate AI complexion mapping that tailors peel depth, microneedling needle length and light-based protocols to patient phenotype. Injectable trends such as “Baby Botox” encourage earlier adoption among consumers aged 25-34, enhancing lifetime value per client. Laser hair removal, the fastest-expanding segment at 15.22% CAGR, benefits from diode platforms capable of treating Fitzpatrick V-VI skin types. Its popularity among male clients and time-poor professionals supports strong weekday utilization.

Non-invasive body contouring technologies, including cryolipolysis and high-intensity focused ultrasound, are gaining traction as complementary upsells to facial programs. Tattoo removal demand is rising as picosecond lasers shorten clearance timelines from 10 sessions to six, improving satisfaction and clinic throughput. Scars and striae treatments, once niche, now leverage fractional resurfacing combined with platelet-rich plasma to deliver visible textural improvement. Overall, the services portfolio is diversifying from single-modality therapies toward curated combinations that lift average revenue per visit and lock in longer-term care plans, reinforcing expansion across the medical spa market.

By End User:

Shifting Demographic MixFemale consumers represented 71.32% of market revenue in 2025, reflecting established demand and broad awareness. Repeat visits average 6.8 per year among this cohort, underlining high annuity potential for membership models. The male segment, expanding at a 15.94% CAGR, is changing marketing narratives by emphasizing performance and grooming rather than beauty. Clinics that reserve discrete waiting areas and streamline check-in apps report higher conversion rates with men. Unisex facility design is also emerging as couples schedule joint appointments, encouraging family-level retention strategies.

Generational diversification is equally important. Gen Z clients often view light doses of neuromodulators as wrinkle prevention, producing earlier entry to the funnel and longer lifetime revenue. Baby boomers, meanwhile, are prepared to pay premium pricing for regenerative solutions that merge health and appearance benefits. Clinics aligning service menus with these divergent expectations widen their catchment without fragmenting brand identity. Educational content delivered through social channels aids segmentation by addressing age-specific concerns in relatable language.

Geography Analysis

North America Medical Spa Market

North America secured 36.95% revenue share in 2025, supported by high disposable income, robust regulatory frameworks and the presence of device innovators that pilot new platforms domestically. The United States propels regional demand through aggressive clinic rollouts inside medical office buildings, while Canada gains incremental growth from inbound wellness tourists seeking bundled vacation-procedure packages. Mexico attracts US patients with cost advantages yet maintains board-certified standards that reassure international clientele. Cross-border dynamics encourage bilingual staff hires and omni-currency payment gateways.

APAC Medical Spa Market

Asia-Pacific is forecast to deliver a 14.52% CAGR to 2031, underscoring its role as the growth backbone of the medical spa market. China remains pivotal as urban consumers dedicate larger disposable income shares to personal care and as hospital-affiliated aesthetic centers extend credit-card-linked memberships. Japan advances technological leadership in ultrashort-pulse lasers, while South Korea exports K-beauty protocols and training curricula that influence regional practice standards. India’s tier-1 and tier-2 cities gain traction through medical tourism corridors anchored by private hospital groups that allocate floor space to hybrid wellness-aesthetic wings.

Europe, GCC and LATAM Medical Spa Market

Europe continues stable mid-single-digit expansion based on cross-border treatment access within the Schengen Area and mature wellness culture. Germany, France and Italy emphasize clinical excellence, whereas Spain combines aesthetic packages with coastal retreat experiences. Eastern Europe offers cost-efficient procedures that attract UK and Irish clients seeking lower out-of-pocket payments post-Brexit travel adjustments. The Middle East witnesses premium demand centered in GCC hubs that co-locate luxury hospitality with specialist clinics. Latin America shows similar hybrid tourism drivers, with Brazil’s established cosmetic surgery reputation feeding non-surgical procedure spill-over.

Competitive Landscape

The medical spa industry is highly fragmented; 81% of operators run a single location. Private equity-backed roll-ups are addressing this fragmentation by acquiring profitable clinics and converting them into 10-plus-unit regional chains. More than USD 3.1 billion has flowed into the sector across 400 transactions during the past five years. Management Service Organization (MSO) frameworks let financial sponsors manage non-clinical functions while physicians retain medical oversight, enabling scale without violating corporate practice of medicine statutes.

Technology is a central competitive lever. Chains differentiate through AI-based dermal imaging, 3D-printed treatment guides and cloud-linked patient portals that track progress photos and recommend follow-up cycles. Vendors such as Cynosure Lutronic are consolidating device portfolios to offer multi-modal workstations that reduce clinic footprint and training hours. Subscription wellness models that package injections, chemical peels and IV therapy for a fixed monthly price are building predictable revenue streams and lowering churn.

Barriers to entry remain moderate: clinical licensing requirements are stringent yet navigable, while equipment financing options proliferate. However, cyber-security obligations are intensifying as biometric imaging increases data sensitivity. Competitive intensity is expected to heighten in suburban catchments where population density supports multiple brands, encouraging operators to fortify referral pathways with dermatologists, plastic surgeons and fitness influencers.

Medical Spa Industry Leaders

Qazi Cosmetic Clinic

Willow Med Spa

The Biomed Spa

Nassif Medical Spa

Beauty Fix MedSpa

- *Disclaimer: Major Players sorted in no particular order

Medical Spa Market Companies Covered in this Report

- Allure Medspa

- Canyon Ranch

- Clinique La Prairie

- Four Seasons Hotels & Resorts

- Qazi Cosmetic Clinic

- Willow Med Spa

- The BioMed Spa

- Beauty Fix MedSpa

- Nassif Medical Spa

- Cocoon Medical Spa

- Hilton Spas

- SkinSpirit

- Ideal Image

- Sono Bello

- Evolution MedSpa Boston

- Ritz-Carlton Spas

- Miraval Group

- Rosewood - Sense Spa

- Lanserhof

- Joali Being

Recent Industry Developments in Medical Spa Market

- March 2025: Cytrellis Biosystems received regulatory approval from Health Canada and Saudi Food and Drug Authority for its ellacor system with Micro-Coring technology, expanding global reach into markets projected to reach USD 7.2 billion (Canada) and USD 1.8 billion (Saudi Arabia) by 2030. This approval enables the company to address unmet needs in non-surgical facial wrinkle treatment across emerging markets

- July 2024: Face Haus introduced AI Skin Analysis technology to enhance customer consultations and provide personalized skincare recommendations, representing the integration of artificial intelligence into routine medical spa operations. This technology deployment demonstrates the industry's shift toward data-driven treatment personalization and enhanced patient engagement.

- April 2024: Cynosure announced its merger with Lutronic to form Cynosure Lutronic, Inc., combining expertise in aesthetic energy devices with laser technology leadership to create a comprehensive portfolio of aesthetic solutions. The merger aims to revolutionize patient care across cosmetic dermatology, plastic surgery, and medical aesthetics through enhanced R&D capabilities.

Global Medical Spa Market Report Scope

Medical spas, sometimes referred to as medi-spas or medspas, seek to combine some medical procedures normally performed in a doctor's office with the experience of a day spa. This report aims to provide a detailed analysis of Medical Spa Market. It focuses on the market dynamics, emerging trends in the segments and regional markets, and insights into various product and application types. Additionally, it analyzes the key players and competitive landscape in Medical Spa Market. The Medical Spa Market is Segmented by Services (Facial Treatment, Body Shaping and Contouring, Laser Hair Removal, Tattoo Removal, Scars & Striae, Other Services), By End User (Male and Female), By Geography (North America, Europe, Asia-Pacific, Latin America, Middle-East and Africa). The report offers the value (In USD billion) for the above segments.

Segmentation Overview

| Facial Treatment |

| Body Shaping & Contouring |

| Laser Hair Removal |

| Tattoo Removal |

| Scars & Striae Treatment |

| Injectables |

| Female |

| Male |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Services | Facial Treatment | |

| Body Shaping & Contouring | ||

| Laser Hair Removal | ||

| Tattoo Removal | ||

| Scars & Striae Treatment | ||

| Injectables | ||

| By End User | Female | |

| Male | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast size of the medical spa market by 2031?

The medical spa market size is projected to reach USD 47.17 billion by 2031, reflecting a 12.48% CAGR during 2026-2031.

Which service line currently generates the highest revenue?

Facial treatments dominate, accounting for 52.18% of medical spa market share in 2025.

Which geographic region will grow the fastest through 2031?

Asia-Pacific is expected to post a 14.52% CAGR, driven by rising disposable income and expanding medical tourism platforms.

How quickly is male demand for medical spa services rising?

The male end-user segment is advancing at a 15.94% CAGR as social media normalizes cosmetic grooming among men.

Why are private equity firms investing in medical spas?

Investors are attracted to the cash-pay model, recurring treatment cycles and the opportunity to consolidate a fragmented provider base for scale efficiencies.

What are the main barriers preventing smaller clinics from upgrading technology?

High acquisition costs for new energy devices and limited access to affordable financing restrain smaller operators from rapid equipment refresh cycles.

Page last updated on: