Urgent Care Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

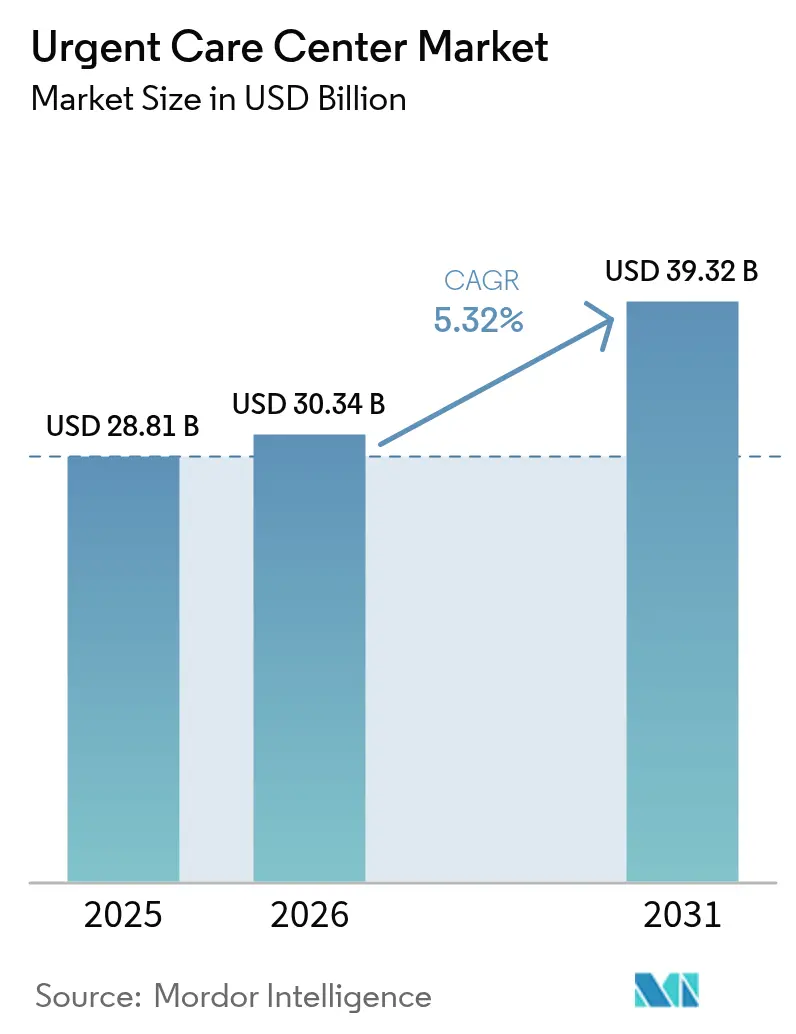

| Market Size (2026) | USD 30.34 Billion |

| Market Size (2031) | USD 39.32 Billion |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

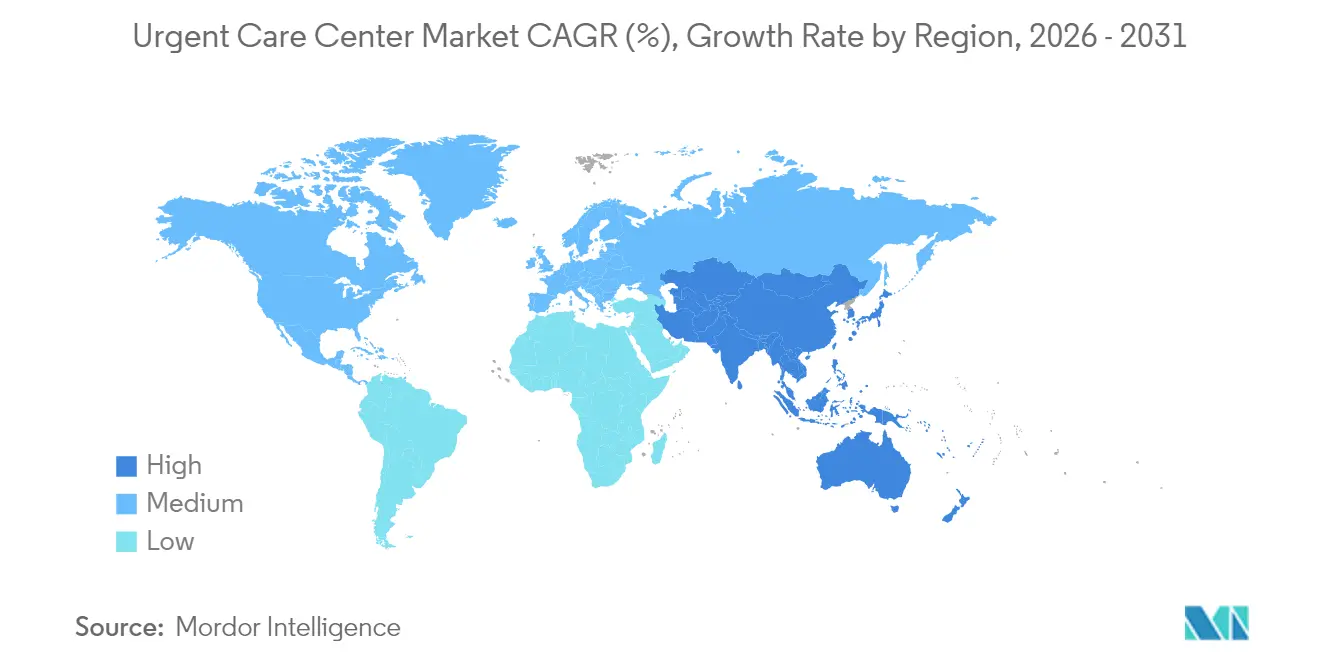

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Urgent Care Center Market Analysis by Mordor Intelligence

The urgent care center market size was valued at USD 28.81 billion in 2025 and estimated to grow from USD 30.34 billion in 2026 to reach USD 39.32 billion by 2031, at a CAGR of 5.32% during the forecast period (2026-2031). Sector momentum reflects emergency-department overcrowding, partnerships between retail chains and health-systems, and rapid digital scheduling uptake, all of which steer patients toward lower-cost same-day care. Corporate chains keep scale advantages through standardized clinical protocols, while hospital-owned facilities accelerate site openings to relieve inpatient bottlenecks and to tighten referral loops. Service-mix evolution is unmistakable: trauma care still attracts the largest visit volumes, yet vaccination and preventive offerings now grow fastest as operators reposition sites as frontline primary-care hubs. Geographic reach broadens as operators pivot to rural communities where 57 million residents lack adequate access to hospital-based services. Heightened consolidation, expanding advanced-practice provider (APP) staffing needs, and reimbursement pressure from value-based insurance plans will shape competitive dynamics through 2030.

Key Report Takeaways

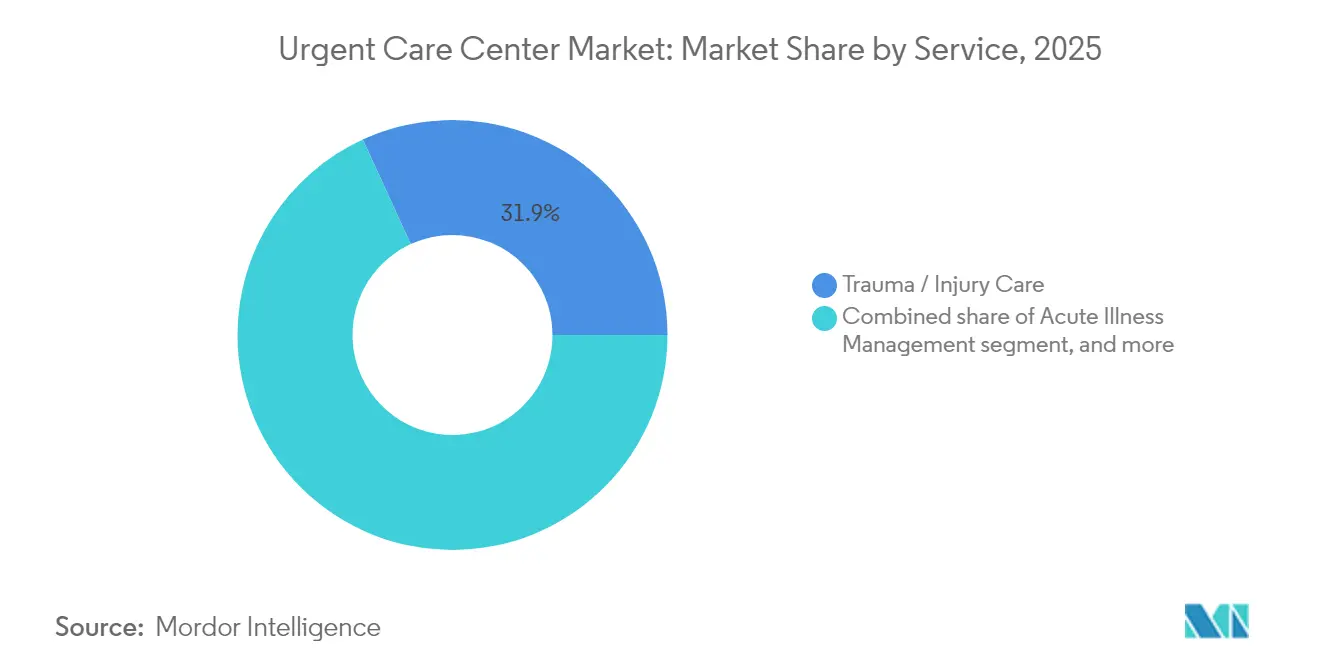

- By service, trauma and injury care led with 31.85% urgent care center market share in 2025, whereas vaccination and preventive services are forecast to expand at a 6.86% CAGR through 2031.

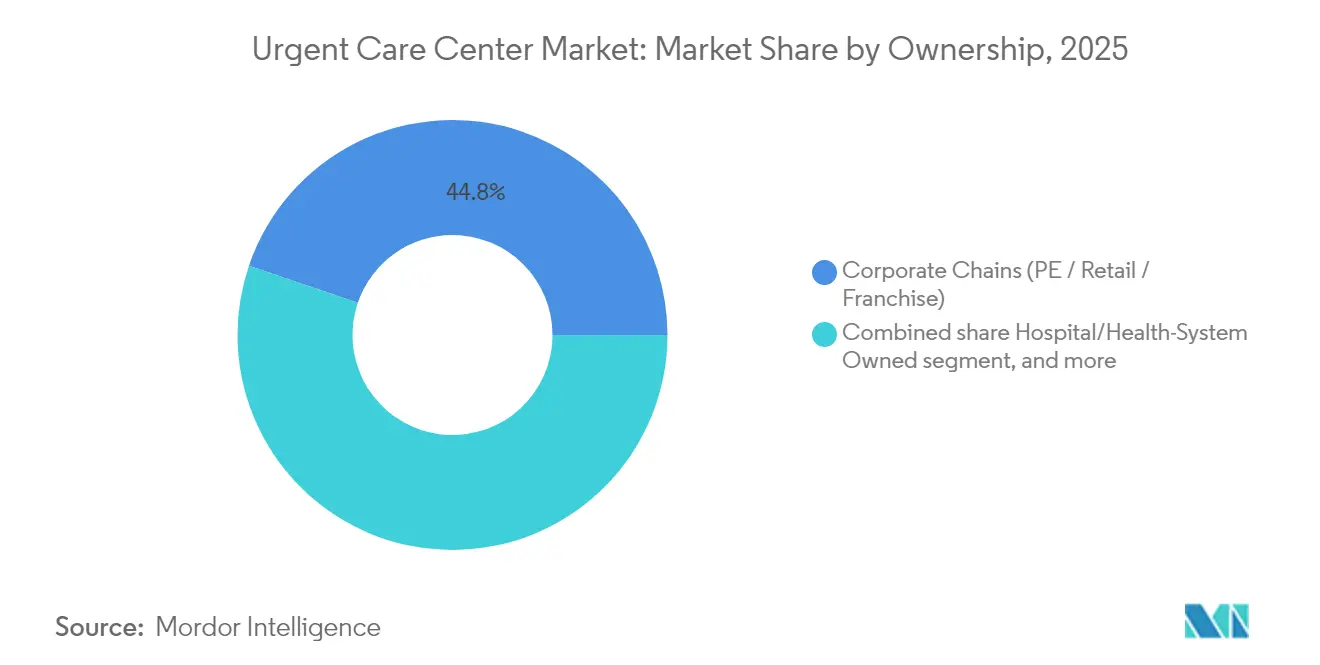

- By ownership, corporate chains captured 44.78% of the urgent care center market in 2025, and hospital-owned facilities are advancing at a 7.21% CAGR to 2031.

- By age group, adults aged 18–64 years made up 35.12% of 2025 patient volumes, while pediatric visits are projected to rise at a 6.74% CAGR to 2031.

- By geography, North America retained 47.90% revenue share in 2025, whereas Asia-Pacific is anticipated to log the quickest 6.29% CAGR during the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Urgent Care Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Emergency-department overcrowding shifting non-critical cases to urgent care | +1.8% | Global; most acute in North America | Short term (≤2 years) |

| Partnerships between retail chains & health systems accelerating site roll-outs | +1.2% | North America & Europe; emerging in APAC | Medium term (2–4 years) |

| Digital scheduling & tele-urgent add-ons enhancing patient capture rates | +0.9% | Global; led by developed markets | Medium term (2–4 years) |

| Active-lifestyle injuries among Millennials & Gen-Z populations | +0.7% | Global; concentrated in urban centers | Long term (≥4 years) |

| Expansion of value-based & high-deductible insurance plans favoring low-cost settings | +0.6% | North America; gaining traction in Europe | Medium term (2–4 years) |

| Aging populations seeking same-day care for chronic exacerbations | +0.3% | Global; most pronounced in developed markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Emergency-Department Overcrowding Shifting Non-Critical Cases to Urgent Care

Median emergency-department wait times have risen 16% since 2014, funneling lower-acuity patients toward urgent care centers that can deliver equivalent treatment at lower cost[1]Chris Pappas, “Pappas, Kuster Urge Action to Reduce Emergency Department Wait Times in New Hampshire,” congressmanchrispappas.house.gov. RAND research estimates that one-third of non-urgent ED encounters could be redirected, saving up to USD 4.4 billion annually. Hospitals consequently embed urgent care sites inside integrated delivery networks, transforming former competitors into throughput partners for ED de-congestion. Payer push toward site-of-care optimization reinforces the shift, as value-based contracts penalize unnecessary ED utilization. Collectively these demand-side and payer-side forces lock in steady volume growth for the urgent care center market.

Digital Scheduling & Tele-Urgent Add-Ons Enhancing Patient Capture Rates

Artificial-intelligence engines orchestrate patient intake, slot utilization, and documentation. CityMD’s multi-year pact with Notable automates front-end tasks for nearly 200 clinics handling 4 million visits each year, coinciding with a 60% visit surge since 2019. Surveys show 55% of consumers now prefer digital channels and 74% rate appointment speed as decisive. Telehealth reached 39.3% adult utilization in 2022; 80.5% experienced no technical glitches and three-quarters deemed visit quality equal to in-person care[2]Jiyeong Lee, “Telehealth Utilization and Associations in the United States During the Third Year of the COVID-19 Pandemic,” jmir.org. “Tele-untethered” models remove virtual waiting rooms, with 76% of users favoring freedom to multitask and saving 55 minutes per session. Digital capacity therefore heightens patient throughput, lifts net promoter scores, and entrenches competitive differentiation inside the urgent care center market.

Active-Lifestyle Injuries Among Millennials & Gen Z Populations

Millennials are now in prime earning and recreation years, spurring demand for safe, convenient musculoskeletal care when sports or fitness injuries strike. Gen Z’s preference for mobile scheduling and transparent pricing dovetails with urgent care’s walk-in ethos. Gig-economy participation further nudges these cohorts toward urgent care sites because many hold high-deductible plans that penalize ED use. Operators respond by embedding point-of-care X-ray, on-site casting, and sports-medicine fellowships, reinforcing brand relevance in dense urban and affluent suburban catchments. The demographic pipe-line assures long-run growth and supports new specialty clinics inside the urgent care center market.

Expansion Of Value-Based & High-Deductible Insurance Plans Favoring Low-Cost Settings

U.S. enrollment in high-deductible plans surpassed 64 million lives in 2024, incentivizing patients to price-shop before choosing care venues. Urgent care encounters typically cost 10 times less than ED visits, meeting payer mandates to steer consumers to efficient sites. Medicare Advantage and commercial payers integrate site-of-service modifiers and shared-savings deals that reward urgent care pivoting, thereby lifting visit volumes and reimbursement certainty for scale players. Europe’s shift toward diagnosis-related-group budgeting similarly prompts public payers to pilot urgent care models, extending global tailwinds for the urgent care center market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Physician & advanced-practitioner shortages in rural and suburban catchments | −1.4% | Global; acute in rural North America | Short term (≤2 years) |

| State-level certificate-of-need / licensing hurdles (US, EU select markets) | −0.8% | North America; select European markets | Medium term (2–4 years) |

| Growing competition from telehealth-only and retail pharmacy clinics | −0.5% | Global; strongest in developed markets | Medium term (2–4 years) |

| Reimbursement ambiguity in emerging markets limiting ROI | −0.4% | Latin America, parts of APAC & Africa | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Physician & Advanced-Practitioner Shortages in Rural and Suburban Catchments

Thirteen percent of Americans live in primary-care shortage areas, and the shortfall may swell to 49,000 physicians by 2030. Employing APPs mitigates gaps—63% of medical groups intend to add new APP roles in 2025—yet formal onboarding exists in only 70% of ambulatory sites. Rural EDs lack emergency physicians in 27% of counties, pushing urgent care centers to stretch clinician coverage with leaner staffing ratios. Productivity rises when APP penetration deepens, but competition for talent inflates labor costs and may slow clinic roll-outs, tempering the urgent care center market CAGR.

State-Level Certificate-Of-Need / Licensing Hurdles (US, EU Select Markets)

Thirty-five U.S. states and Washington D.C. still require certificate-of-need (CON) approval for major ambulatory investments, delaying builds by 12–24 months and imposing legal fees that deter smaller entrants[3]National Conference of State Legislatures, “Certificate of Need State Laws,” ncsl.org. Reforms are uneven: North Carolina and South Carolina repealed key provisions, whereas Tennessee will retain selective oversight until 2027. Meanwhile, anti-kickback and quality-reporting mandates persist, obliging multistate operators to navigate patchwork compliance regimes that elongate ramp-up timelines inside the urgent care center market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Trauma Care Dominance amid Preventive Growth

Trauma and injury care accounted for 31.85% of 2025 revenue, underscoring an enduring core at the urgent care center market’s clinical mix. On-site X-ray, fracture stabilization, and laceration repair divert patients from EDs and offer favorable payer economics. Acute illness management ranks second, handling respiratory and gastrointestinal conditions with rapid throughput. Diagnostic advances now include ultrasound and advanced imaging, raising average ticket size.

Vaccination and preventive offerings expand fastest at a 6.86% CAGR, reshaping centers from episodic venues to comprehensive health destinations. Mass immunization campaigns and travel medicine bundles fill scheduling valleys, while AI-driven triage engines support standardized care. A Cedars-Sinai study found virtual urgent care algorithms outscored physicians for treatment appropriateness on common complaints, validating decision-support adoption. Preventive momentum creates spillover demand for chronic-condition screening and lifestyle coaching, elevating cross-sell potential within the urgent care center market size at both national and local levels.

By Ownership: Corporate Chains Lead while Health Systems Accelerate

Corporate operators held 44.78% of the urgent care center market in 2025, leveraging centralized procurement and uniform EHR systems to maintain cost efficiencies. Their standardized branding and digital front doors ensure strong consumer recall and rapid check-in, crucial for price-sensitive patients.

Hospital-owned sites, however, chart the briskest 7.21% CAGR to 2031 as health-systems acquire locations to stem ED overflow and tighten specialist pipelines. Deals such as Ardent Health’s purchase of 18 NextCare clinics and UPMC’s partnership with GoHealth highlight acquisition appetite. Private-equity sponsors steer further consolidation, with integration initiatives boosting collection rates 12% and trimming accounts-receivable days 39% post-close. Such financial engineering accelerates roll-outs but heightens exit-cycle risk if multiples compress.

By Age Group: Adult Volumes Anchor, Pediatric Visits Surge

Adults aged 18–64 composed 35.12% of 2025 footfall, benefiting from employer insurance, sports injuries, and remote-work flexibility that favors quick walk-in care. This demographic’s digital savviness supports adoption of scheduling apps and virtual queueing, sustaining baseline traffic for the urgent care center market.

Pediatric volumes grow fastest at a 6.74% CAGR as parents flee ED waits. Youth utilization jumped from 21.6% to 28.4% of children between 2021–2022, with adolescents 12–17 leading at 30.3%. Centers invest in child-friendly décor, behavioral-health consultation rooms, and sports physicals to monetize seasonal peaks. Geriatric engagement lags, tied to complex comorbidities, yet telehealth bridges gaps and promises future uplift once mobility barriers lessen.

Geography Analysis

North America captured 47.90% of 2025 revenue, underpinned by insurance mechanisms that reimburse out-of-hospital encounters and by well-established clinic chains. Consolidators continue to target suburban infill opportunities while pivoting toward rural counties where 57 million residents remain underserved. CON reform across the Carolinas, plus Tennessee’s phased deregulation, eases expansion and invites cross-state operator entries, fortifying the urgent care center market size within the region.

Asia-Pacific provides the sharpest 6.29% CAGR outlook. China’s aging demographic, India’s 275-million-plus eSanjeevani consultations, and Japan’s robust telemedicine adoption validate urgent care viability. Public-private partnerships blend physical clinics with digital triage kiosks located in transit hubs, yielding high-volume low-acuity throughput models that mirror U.S. suburban prototypes.

Europe, Middle East & Africa, and South America log moderate growth. European universal-care systems restrict private pay volumes, yet cross-border telehealth and expatriate communities sustain niche demand. Gulf nations deploy urgent care inside medical-tourism corridors, while Brazil and Colombia flirt with hybrid ED-urgent models inside private hospitals. Currency volatility and regulatory opacity temper speed of scale-out but open localized franchise pathways for risk-tolerant investors.

Competitive Landscape

Industry fragmentation persists yet consolidation quickens. CVS Health commands the largest branded footprint through 1,100+ MinuteClinics and 49 health-system alliances. UnitedHealth’s Optum divested selected MedExpress sites under antitrust scrutiny, demonstrating regulatory brake capacity. CityMD wields AI to trim administrative costs and sustain 4 million annual visits, illustrating technology-enabled operating leverage.

Rural white-space represents the next battleground. Chains deploy mobile vans to test viability before committing brick-and-mortar, a tactic that slashes capital risk. Occupational health, sports-medicine, and hybrid ED-urgent models serve as adjacency wedges. Private-equity–backed groups finance multi-state roll-ups, optimizing revenue-cycle systems and staffing mixes for EBITDA lift ahead of exit. Yet high interest-rate environments may elongate holding periods, rewarding operators with durable cash-flow profiles.

Emergent moats revolve around digital front ends, unified EHRs, and consumer-facing apps that integrate with insurer directories. APP shortages could throttle growth; operators now sponsor tuition and residency pipelines to lock talent. Market incumbents unable to meet rising patient experience benchmarks risk volume leakage to digitally fluent rivals, propelling a Darwinian wave across the urgent care center market.

Urgent Care Center Industry Leaders

NextCare Holdings, Inc.

Select Medical Holdings (Concentra, Inc.)

UnitedHealth Group (MedExpress )

HCA Healthcare (CareNow / CareSpot)

CVS Health (MinuteClinic)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: CityMD partnered with Notable to embed AI automation across nearly 200 clinics, improving scheduling and registration as patient volumes climbed 60% since 2019.

- March 2025: Walgreens disclosed plans to divest CityMD, signaling realignment of retail-clinic strategies amid financial headwinds.

- February 2025: MinuteClinic and Emory Healthcare Network extended in-network collaboration across Georgia to combat physician shortages via same-day and virtual options.

- January 2025: Concentra posted USD 1.9 billion revenue and moved to acquire Nova Medical Centers for USD 265 million, broadening occupational-health reach across 67 sites.

- January 2025: Ardent Health purchased 18 NextCare clinics in New Mexico and Oklahoma to deepen ambulatory density around flagship hospitals.

Global Urgent Care Center Market Report Scope

As per the scope of the report, urgent care centers are medical care facilities that offer healthcare services on a walk-in non-appointment basis for acute illnesses or injuries that are not life-threatening. The Urgent Care Center Market is segmented by Service (Trauma/Injury Services, Vaccination Services, Acute Illness Treatment Services, Diagnostic Services, and Other Services), Ownership (Corporate Owned, Hospital Owned, and Physician Owned), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the abovementioned segments.

| Trauma / Injury Care |

| Acute Illness Management |

| Vaccination & Preventive Services |

| Diagnostic & Screening Services |

| Other Services |

| Corporate Chains (PE / Retail / Franchise) |

| Hospital / Health-System Owned |

| Physician Group Owned |

| Other Ownerships |

| Pediatrics (0-17 yrs) |

| Adults (18-64 yrs) |

| Geriatrics (65+ yrs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service | Trauma / Injury Care | |

| Acute Illness Management | ||

| Vaccination & Preventive Services | ||

| Diagnostic & Screening Services | ||

| Other Services | ||

| By Ownership | Corporate Chains (PE / Retail / Franchise) | |

| Hospital / Health-System Owned | ||

| Physician Group Owned | ||

| Other Ownerships | ||

| By Age Group | Pediatrics (0-17 yrs) | |

| Adults (18-64 yrs) | ||

| Geriatrics (65+ yrs) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the urgent care center market?

The urgent care center market size is USD 30.34 billion in 2026 and is forecast to reach USD 39.32 billion by 2031.

How fast is the urgent care center market expected to grow?

The market is projected to expand at a 5.32% CAGR between 2026 and 2031.

Which service segment leads the urgent care center market?

Trauma and injury care held 31.85% of 2025 revenue, making it the largest service segment.

Which ownership model is growing the fastest?

Hospital-owned urgent care facilities are advancing at a 7.21% CAGR through 2031.

Why are retail chains key to urgent care expansion?

Retail-health partnerships combine accessible storefronts with health-system clinical expertise, accelerating site roll-outs and patient acquisition.

Which region offers the highest growth potential?

Asia-Pacific shows the fastest 6.29% CAGR outlook, thanks to aging populations and significant digital-health investments.

Page last updated on: