Market Overview

| Study Period | 2020 - 2030 |

|---|---|

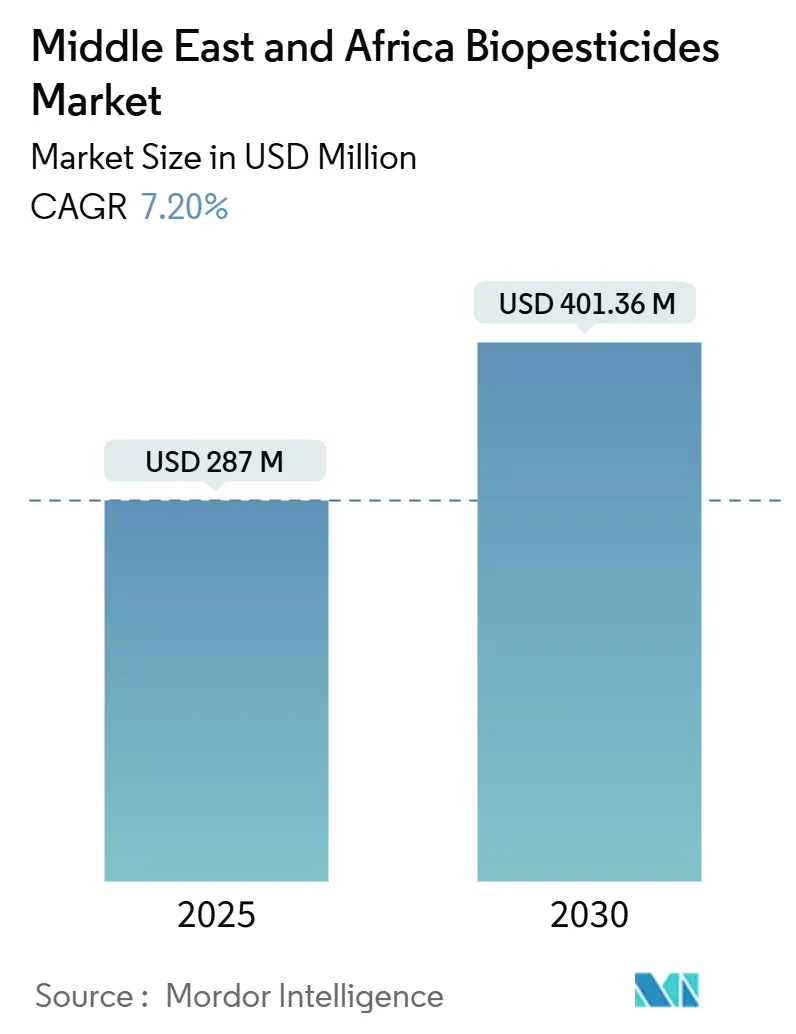

| Market Size (2025) | USD 287 Million |

| Market Size (2030) | USD 401.36 Million |

| Growth Rate (2025 - 2030) | 7.20% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Africa |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East & Africa Biopesticides Market Analysis by Mordor Intelligence

The Middle East & Africa biopesticides market size stands at USD 287 million in 2025 and is forecast to reach USD 401.36 million by 2030, translating into a 7.2% CAGR through the period. This growth is driven by stricter pesticide regulations, increasing organic farming area, and continuous sovereign-fund investments in desert-adapted biological research. The Middle East maintains market leadership through expedited microbial approval processes and advanced irrigation systems, while Africa shows the highest growth rate as exporters pursue residue-free certifications. Industry developments focus on heat-stable encapsulation technology, drone-compatible liquid formulations, and strategic acquisitions to expand microbial collections for future product development. Market potential exists in improving farmer education, reducing per-hectare costs, and developing climate-resistant formulations for smallholder farmers, particularly in regions where conventional pesticides have lost effectiveness due to pest resistance.

Key Report Takeaways

- By product type, bioinsecticides led with 28.6% of the Middle East & Africa biopesticides market share in 2024, while bioherbicides hold the highest forecast CAGR at 9.2% to 2030.

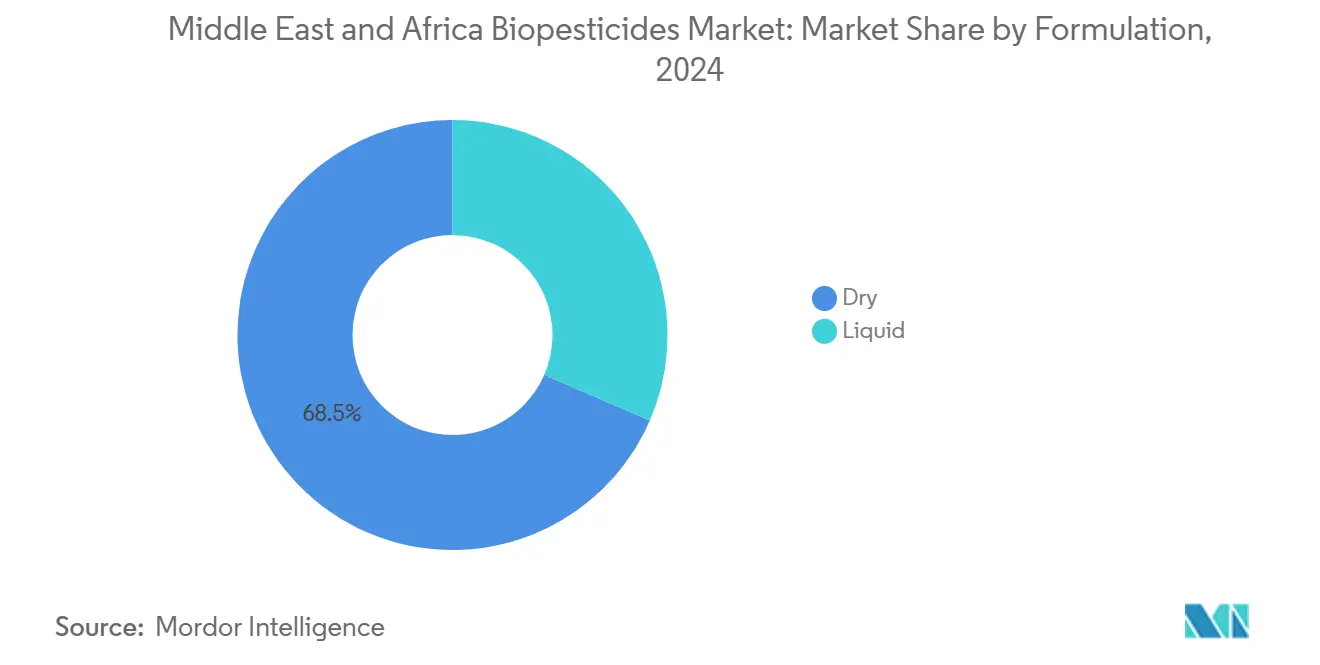

- By formulation, dry products accounted for 68.5% of the Middle East & Africa biopesticides market size in 2024, while liquid products are advancing at an 8.6% CAGR through 2030.

- By mode of application, foliar spray accounted for 32.3% of the Middle East & Africa biopesticides market in 2024, and seed treatment is projected to expand at a 9.5% CAGR through 2030.

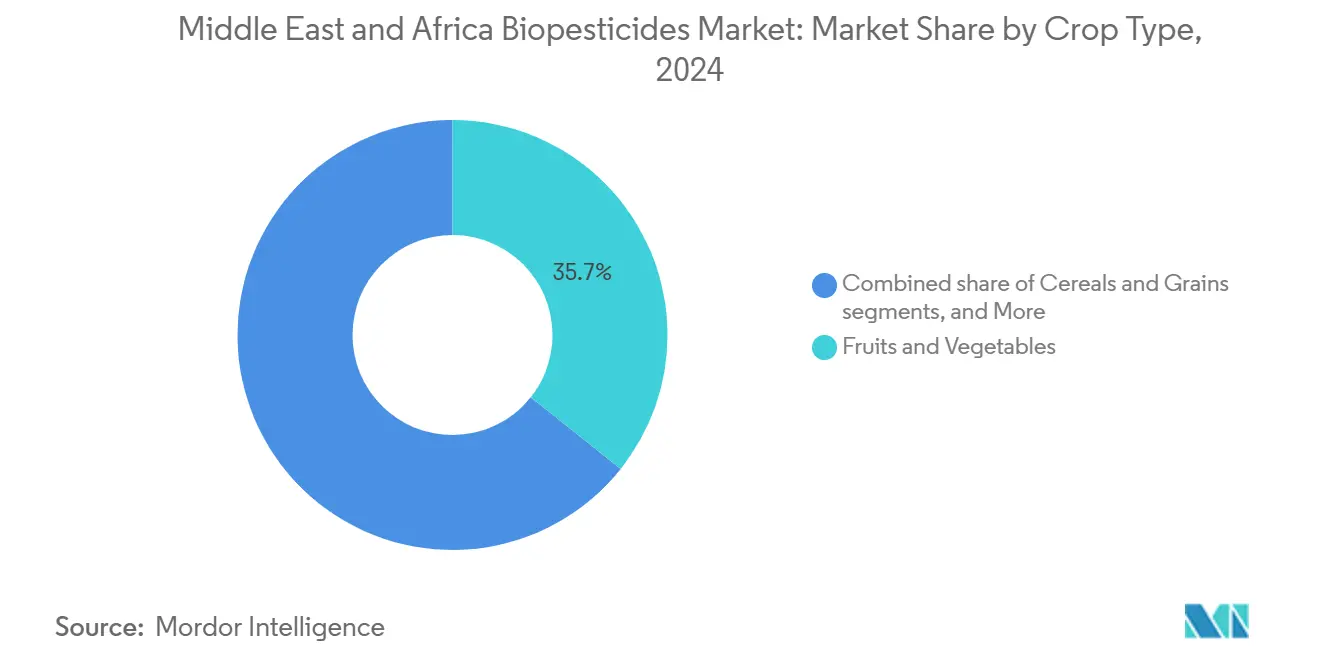

- By crop type, fruits and vegetables captured 35.7% of the Middle East & Africa biopesticides market in 2024, and oilseeds and pulses are projected to hold the highest forecast CAGR of 8.8% from 2024 to 2030.

- By geography, Africa captured 58.8% of the market size in 2024, and the Middle East is anticipated to expand at a market-leading 6.7% CAGR to 2030.

Middle East & Africa Biopesticides Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory bans on key synthetic actives | +1.8% | Middle East core, expanding to North Africa | Medium term (2-4 years) |

| Fast-track approvals for microbial products | +1.2% | UAE, Saudi Arabia, with spillover to Egypt | Short term (≤ 2 years) |

| Expansion of certified organic farmland | +1.5% | Africa-wide, particularly East Africa export corridors | Long term (≥ 4 years) |

| Rising pest resistance to chemical pesticides | +2.1% | Global, with acute pressure in cotton and date palm regions | Short term (≤ 2 years) |

| Adoption of drone-enabled precision bio-spraying | +0.8% | GCC countries, expanding to commercial farms across Middle East & Africa | Medium term (2-4 years) |

| Gulf Cooperation Council (GCC) sovereign-fund investments in desert-adapted biocontrol R&D | +0.6% | UAE, Saudi Arabia, with technology transfer potential | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory bans on key synthetic actives

Authorities across the region have curtailed dozens of high-hazard chemistries since 2024, triggering a compliance-led pivot toward microbial options. The UAE outlawed several organophosphates and presented a unified digital registry that filters unapproved products. Tunisia subsidizes up to 50% of organic certification costs, making on-farm biology more viable[1]Source: United Nations Development Programme, “Organic Farming and Sustainable Agriculture Practices,” sdgprivatefinance.undp.org. This regulatory tightening extends beyond household pesticides to agricultural applications, where concerns about groundwater contamination and food safety residues are driving policy changes. Exporters have responded quickly because residue compliance now decides border clearance. This stringency shortens product lifecycles for older actives and accelerates rerouting of R&D budgets to biological control firms.

Fast-track approvals for microbial products

The UAE’s biotechnology blueprint prioritizes 120-day review windows for bio-inputs, versus the standard multi-year docket for synthetics. Saudi Arabia’s Vision 2030 funds validation trials at King Abdulaziz City for Science and Technology further trim regulatory friction. Multinationals seize the advantage via regional hubs that cluster research, pilot production, and regulatory affairs staff. Faster clearances slash carrying costs, unlock earlier revenue, and lure venture dollars toward niche microbial startups. This regulatory efficiency advantage is attracting international biocontrol companies to establish regional headquarters and manufacturing facilities in the GCC, creating a competitive advantage that extends throughout the broader Middle East & Africa market.

Expansion of certified organic farmland

The price premiums for certified produce increase farmer income and offset the higher costs of advanced biopesticides. These premiums typically range from 20-30% above conventional crop prices, providing significant financial incentives for farmers. Market demand, rather than regulations, drives growth in the Middle East and Africa biopesticides market, with increasing consumer preference for organic products and sustainable farming practices. The organic certification process, while rigorous, enables farmers to access premium markets and establish long-term buyer relationships. The growing awareness of environmental sustainability and food safety among consumers further reinforces this market stability.

Rising pest resistance to chemical pesticides

Cotton bollworm populations shrug off multiple pyrethroids across West and Central Africa, and Omani date producers battle dubas bug strains immune to neonicotinoids. Researchers log resistance to new chemistries within three seasons, compelling growers to rotate with multi-mode biologicals that slow adaptation. Farmer demand peaks in crops where export premiums or pest devastation alter the income calculus quickly. This resistance pressure creates a compelling value proposition for biopesticides, which typically employ multiple modes of action and are less prone to resistance development due to their complex biological mechanisms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short shelf life in hot climates | -1.4% | Region-wide, particularly acute in desert areas | Short term (≤ 2 years) |

| Higher per-hectare cost vs. generics | -1.1% | Price-sensitive smallholder segments across Africa | Medium term (2-4 years) |

| Farmer awareness and training gaps | -0.9% | Rural areas across Middle East & Africa, particularly in traditional farming regions | Long term (≥ 4 years) |

| Illicit gray-market imports of counterfeit biopesticides | -0.7% | Border regions and informal distribution channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Short shelf life in hot climates

Ambient warehouse temperatures top 45 °C in peak season, slashing microbial viability well before sale. Cold-chain coverage remains limited outside major cities. Though encapsulation advances bolster survival, unit costs rise, restricting access for budget-constrained buyers. Seasonal ordering patterns worsen wastage, especially for small dealers that lack turnover speed. Companies are investing heavily in heat-stable formulation technologies, including encapsulation systems and UV-resistant carriers, but these advanced formulations typically carry premium pricing that limits accessibility. The shelf life constraint creates particular challenges for seasonal demand patterns, where products must remain viable through extended storage periods between planting seasons.

Higher per-hectare cost vs. generics

Generic insecticides, priced 30-50% lower per hectare, remain prevalent on farms with limited cash flow. The required frequent reapplication of biological products widens this cost difference. Limited access to credit prevents farmers from transitioning to biologicals unless processors or exporters share the expenses. The higher number of applications needed for certain biopesticides increases seasonal costs. The price difference between synthetic and biological pesticides is decreasing as synthetic pesticide prices rise due to raw material inflation and regulatory compliance costs, while improved manufacturing scale enhances biopesticide production efficiency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bioinsecticides remain dominant amid resistance pressure

The segment held 28.6% of the Middle East & Africa biopesticides market share in 2024 as growers confronted aggressive bollworm, leafminer, and dubas bug outbreaks. Bacillus thuringiensis and Beauveria bassiana products retain farmer trust because replicated trials prove rapid knockdown. The Middle East & Africa biopesticides market size within bioinsecticides is projected to grow by 2030, propelled by premium fruit and cotton acreage that cannot risk residue violations.

Bioherbicides grow fastest at a 9.2% CAGR since herbicide-resistant pigweed and ryegrass spread through cereal basins. R&D targets allelopathic fungi that suppress seed viability under arid conditions. Bionematicides scale slower yet remain vital in protected horticulture, while biofungicides secure citrus post-harvest quality where synthetic fungicide limits tighten. Widespread pest mutation keeps substitution barriers low. Multinationals co-formulate insect proteins with botanical oils for an extended spectrum. Startups license gene editing to silence insect detox pathways, aligning product pipelines with upcoming resistance management guidelines.

By Formulation: Dry products command scale while liquids accelerate

Dry formulations command the largest market share at 68.5% in 2024, primarily due to their superior stability and shelf life performance under the Middle East & Africa region's challenging climatic conditions. Granular and powder formulations can withstand high temperatures and humidity fluctuations that would rapidly degrade liquid products, making them particularly suitable for distribution networks that lack cold chain infrastructure. The dry formulation advantage is most pronounced in remote agricultural areas where storage conditions are suboptimal and product turnover is slow. Water-dispersible granules and wettable powders have gained particular traction among commercial growers who value consistent performance and extended storage capability.

Liquid formulations are experiencing the fastest growth at 8.6% CAGR through 2030, driven by advances in stabilization technologies and the superior application characteristics that liquids offer for precision agriculture systems. Companies are developing heat-stable liquid formulations using advanced encapsulation technologies and UV-resistant carriers that address the region's climatic challenges. In November 2023, FMC Ventures' investment in AgroSpheres' biodegradable encapsulation technologies exemplifies the industry's focus on developing liquid formulations that can perform reliably in extreme conditions[2]Source: FMC Corporation, “FMC Ventures | Investing in New Agricultural Technologies,” fmc.com.

By Mode of Application: Foliar spray leads, seed treatment surges

Foliar spray applications maintain the dominant position with 32.3% market share in 2024, reflecting the method's versatility and compatibility with existing farmer practices and equipment across the Middle East & Africa region. The foliar application method provides direct pest contact and rapid biological agent establishment, making it particularly effective for bioinsecticides and biofungicides targeting above-ground pest and disease pressure. The segment benefits from established spray equipment availability and farmer familiarity, reducing adoption barriers compared to specialized application methods.

Seed treatment represents the fastest-growing application mode at 9.5% CAGR through 2030, driven by the method's efficiency and early-season protection benefits. The growth reflects increasing adoption of biological seed treatments for soil-borne pest and disease control, particularly in cereal and oilseed crops where early establishment protection is critical. Seed treatment applications offer several advantages, including precise dosing, reduced environmental exposure, and protection during the vulnerable seedling stage.

By Crop Type: Fruits and vegetables dominate while oilseeds gain

Fruits and vegetables command the largest market share at 35.7% in 2024, reflecting the high-value nature of these crops and their sensitivity to pesticide residues in export markets. The segment's dominance is driven by stringent maximum residue limits in international markets and consumer preferences for residue-free produce, creating strong economic incentives for biological pest control adoption. Protected agriculture systems, which are expanding rapidly in the GCC countries, rely heavily on biological control agents to maintain pest management effectiveness while meeting food safety standards. In January 2025, the UAE's AeroFarms AgX facility and similar vertical farming initiatives demonstrate the integration of biological pest control in controlled-environment agriculture

Oilseeds and pulses represent the fastest-growing crop segment at 8.8% CAGR through 2030, driven by expanding production areas and increasing adoption of integrated pest management practices. The growth is particularly strong in countries like Ethiopia and Kenya, where export-oriented pulse production requires compliance with international organic and residue standards. Cereals and grains maintain a substantial market position due to their large cultivation areas, though adoption rates are lower due to price sensitivity and traditional farming practices.

Geography Analysis

Africa captured 58.8% of the market size in 2024, while the Middle East is anticipated to expand at a market-leading 6.7% CAGR to 2030. The Middle East region dominates the Middle East & Africa biopesticides market, driven by advanced agricultural infrastructure, supportive regulatory frameworks, and substantial government investments in agricultural biotechnology. The UAE leads regional adoption through initiatives such as the Food Tech Valley partnerships and the Abu Dhabi-International Cooperative Banking Association (ICBA) collaboration on desert agriculture research, creating demand for climate-adapted biological solutions. Regulatory frameworks in the GCC countries favor fast-track approvals for microbial products, thereby reducing time-to-market barriers and encouraging investment in innovation. The Middle East's market leadership reflects both the region's financial resources and strategic commitment to agricultural modernization.

African demand, though smaller today, expands at a double-digit pace. Kenya, Uganda, and Tanzania collectively surpass 1 million certified-organic hectares, guaranteeing recurring consumption of Bacillus and Trichoderma products for export vegetables. The Middle East & Africa biopesticides market remains fragmented across francophone and anglophone distribution channels, demanding localized labeling and training materials. The regional growth trajectory is supported by increasing international development funding for sustainable agriculture and growing recognition of biological pest control as essential for long-term agricultural productivity.

Egypt connects the two subregions through its significant export sector and increasing pest resistance challenges in cotton and tomato crops. The country's shift toward organic and biodynamic farming practices, supported by organizations like SEKEM and the Egyptian Biodynamic Association, creates structured demand for biological pest control solutions[3]Source: farmonaut, “Sustainable Egyptian Agriculture: 5 Ways to Boost Climate Resilience,” farmonaut.com. The government eyes carbon-credit revenue tied to reduced chemical usage, which further incentivizes microbial replacements. Government initiatives supporting sustainable agriculture, combined with international partnerships and carbon market opportunities, create multiple incentives for biological pest control adoption that extend beyond immediate pest management needs.

Competitive Landscape

The Middle East & Africa biopesticides market exhibits high concentration with increasing consolidation through strategic acquisitions and partnerships among multinational agrochemical companies and specialized biocontrol firms. Market concentration is evolving as established players like Bayer AG, BASF SE, and Syngenta Group expand their biological portfolios through internal development and external partnerships, while pure-play biological companies like Koppert Biological Systems and Certis Biologicals establish regional distribution networks.

Acquisition strategy shapes growth. Certis Biologicals absorbed select AgBiome assets and, in August 2024, licensed RNA-interference patents from Renaissance BioScience. Ginkgo Bioworks purchased a 115,000-isolate microbial library to shorten discovery timelines. The competitive dynamics reflect the industry's transition from niche biological solutions to mainstream integrated pest management offerings, with companies investing heavily in climate-adapted formulations and precision application technologies suited to desert agriculture conditions.

Firms that pair microbial strains with digital farm-management platforms secure data loops that prove return on investment to skeptical growers. Niche local players carve space by isolating endemic microbes already adapted to desert soils, then contracting toll manufacturing to serve neighborhood distributors. The competitive landscape is increasingly shaped by regulatory compliance capabilities and the ability to navigate diverse approval processes across Middle East & Africa countries, creating advantages for companies with established regulatory expertise and local market knowledge.

Middle East & Africa Biopesticides Industry Leaders

BASF SE

FMC Corporation

Sumitomo Chemical Co. Ltd

Koppert Biological Systems (Koppert B.V.)

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Silal and Bayer signed an MoU at the World Agri-Tech Innovation Summit. The agreement extends their partnership and focuses on developing sustainable desert agriculture, which is anticipated to drive the adoption of biopesticides in the Middle East and Africa region. The collaboration includes implementing digital farming solutions and conducting vegetable seed trials suited to Middle East and Africa conditions, potentially increasing the demand for biological crop protection solutions in the region.

- August 2024: IPL Biologicals announced a partnership with Spain-based Azufrera y Fertilizantes Pallarés, S.A.U. (AFEPASA) for global joint registration of microbial biopesticides with a specific focus on the Middle East and Africa market entry, supported by planned USD 48 million Gujarat facility investment to serve regional export markets.

- May 2024: Andermatt Group and Novonesis introduced soy inoculant products in African markets, strengthening the Middle East and Africa biopesticides market through enhanced nitrogen fixation and improved soil health in legume cultivation systems.

Middle East & Africa Biopesticides Market Report Scope

This report defines biopesticides as commercially manufactured products derived from natural materials, such as animals, plants, bacteria, and certain minerals. The market studied includes biopesticides applied by farmers and large commercial growers in crops and non-crop agricultural practices.

The report covers the Middle East and African biopesticides market trends and is segmented by product type (bioherbicide, biofungicide, bioinsecticide, and other products), formulation (liquid and dry), mode of application (soil, seed, foliar, and other modes of application), crop type (crop-based and non-crop-based) and geography (Middle East and Africa). The report offers the market size and forecasts in value (USD) for all the above segments.

By Product Type

| Bioinsecticide |

| Biofungicide |

| Bioherbicide |

| Bionematicide |

By Formulation

| Liquid |

| Dry |

By Mode of Application

| Soil Treatment |

| Seed Treatment |

| Foliar Spray |

| Other Modes of Application |

By Crop Type

| Cereals and Grains |

| Fruits and Vegetables |

| Oilseeds and Pulses |

| Turf and Ornamentals |

By Geography

| Africa | South Africa |

| Kenya | |

| Uganda | |

| Tanzania | |

| Nigeria | |

| Rest of Africa | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| Rest of Middle East |

| By Product Type | Bioinsecticide | |

| Biofungicide | ||

| Bioherbicide | ||

| Bionematicide | ||

| By Formulation | Liquid | |

| Dry | ||

| By Mode of Application | Soil Treatment | |

| Seed Treatment | ||

| Foliar Spray | ||

| Other Modes of Application | ||

| By Crop Type | Cereals and Grains | |

| Fruits and Vegetables | ||

| Oilseeds and Pulses | ||

| Turf and Ornamentals | ||

| By Geography | Africa | South Africa |

| Kenya | ||

| Uganda | ||

| Tanzania | ||

| Nigeria | ||

| Rest of Africa | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| Rest of Middle East | ||

Key Questions Answered in the Report

What is the current value of the MEA biopesticides market, and how fast is regional demand projected to grow?

The market is valued at USD 287 million in 2025. Revenue is forecast to rise at a 7.2% CAGR to reach USD 401.36 million by 2030.

Which product category holds the largest share?

Bioinsecticides led with 28.6% of 2024 sales.

Why are liquid formulations gaining traction?

Encapsulation and drone compatibility push liquids toward an 8.6% CAGR through 2030.

Which crops generate the highest spending on biological control?

Fruits and vegetables accounted for 35.7% of purchases in 2024 due to strict residue limits.

Who are the leading suppliers in the region?

Bayer AG, BASF SE, Syngenta Group, Koppert Biological Systems (Koppert B.V.), FMC Corporation and Sumitomo Chemical Co. Ltd collectively are the leading suppliers in the region..

Page last updated on: