Vinyl Acetate Homopolymer Emulsion Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

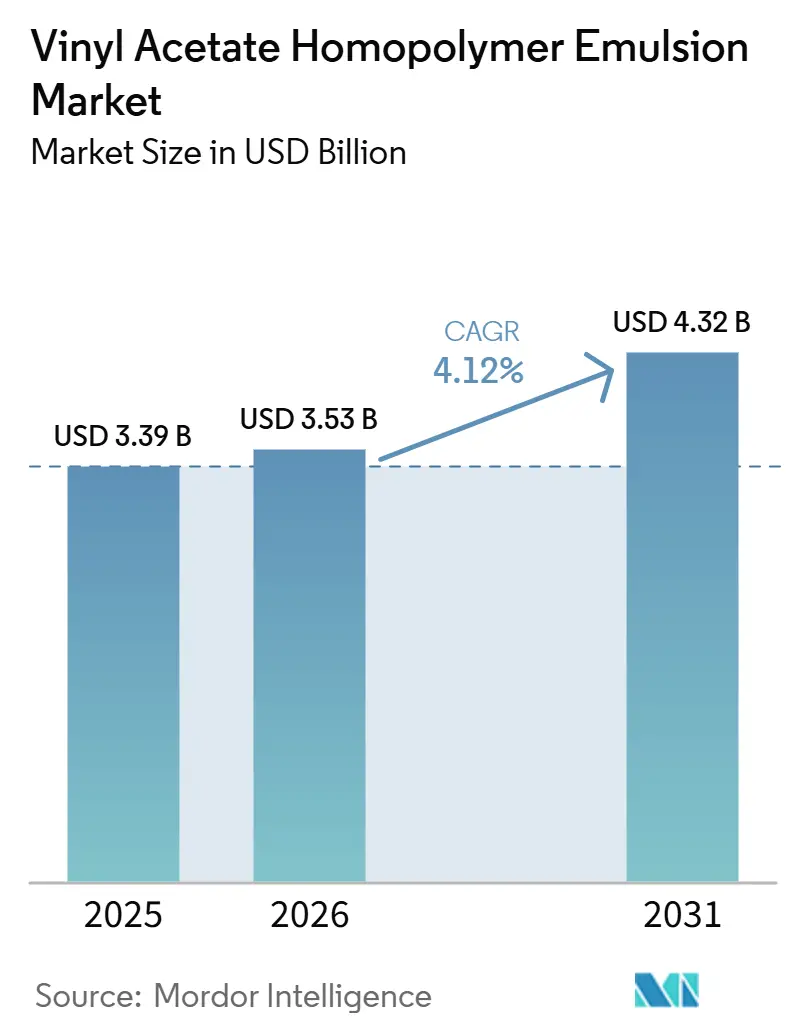

| Market Size (2026) | USD 3.53 Billion |

| Market Size (2031) | USD 4.32 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

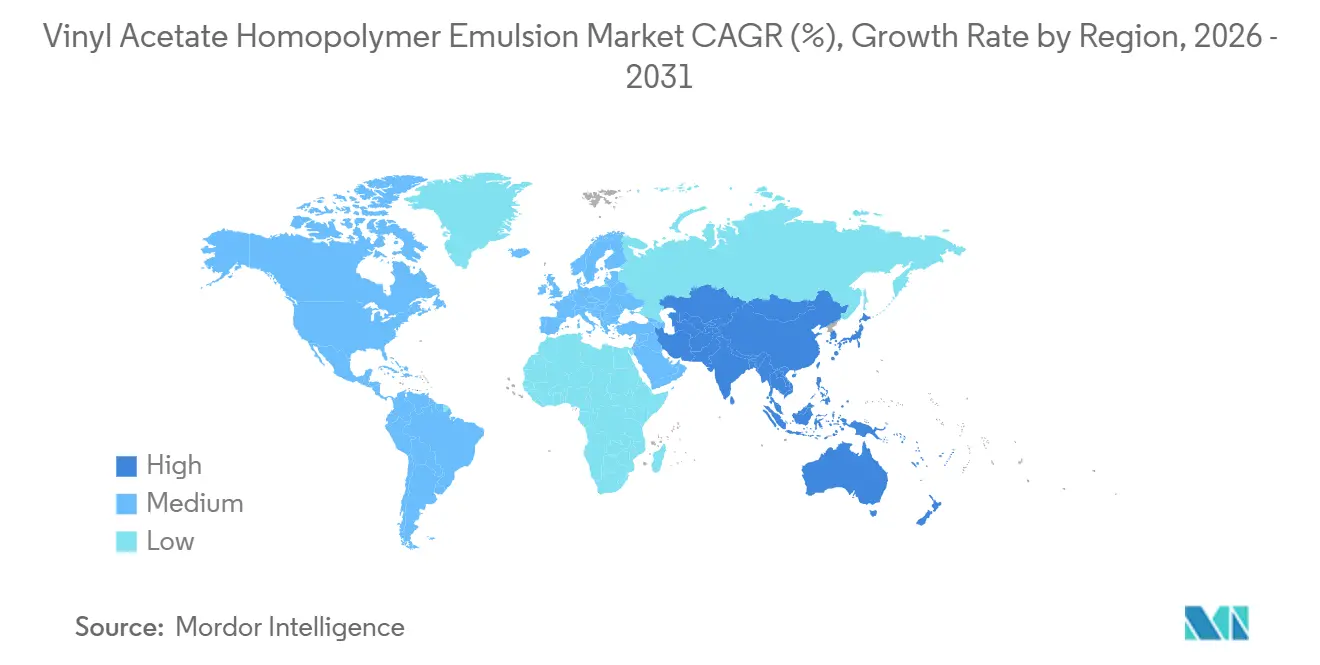

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

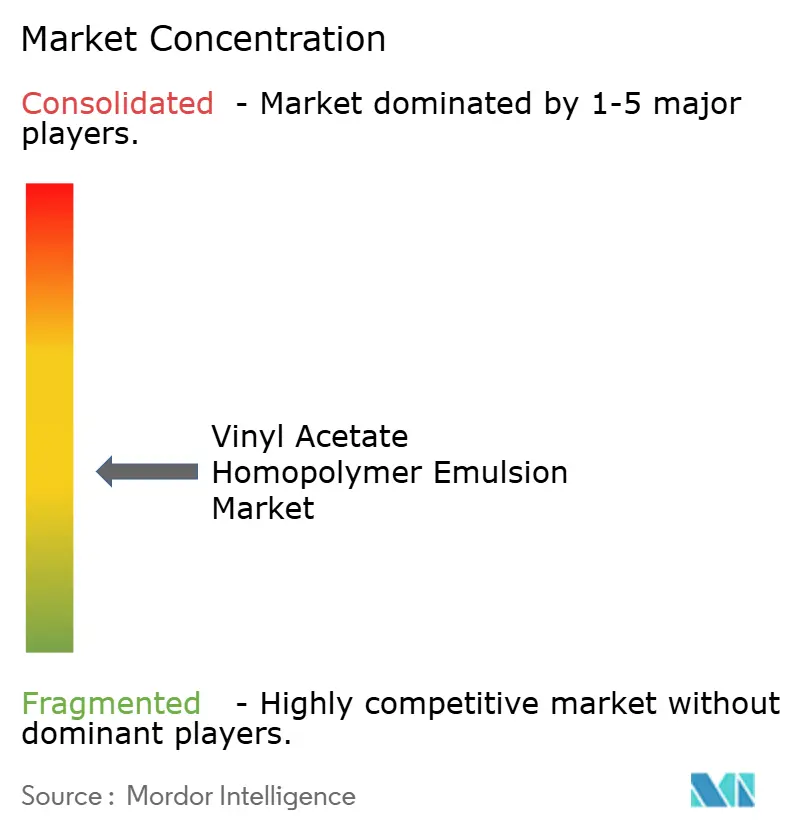

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vinyl Acetate Homopolymer Emulsion Market Analysis by Mordor Intelligence

The Vinyl Acetate Homopolymer Emulsion Market size is projected to expand from USD 3.39 billion in 2025 and USD 3.53 billion in 2026 to USD 4.32 billion by 2031, registering a CAGR of 4.12% between 2026 to 2031. Regulatory mandates, particularly China's updated standards for low-volatile organic compound formulations, are pushing architectural and industrial coatings towards waterborne platforms. This shift is bolstering the demand for vinyl acetate homopolymer binders. Companies like Wacker and Celanese are expanding capacities in the region, ensuring a more secure supply and reduced lead times. Meanwhile, innovations in cold-seal and barrier coatings are creating new opportunities in recyclable flexible packaging. In South and Southeast Asia, there's a surge in hygiene-grade non-woven production, and a rising demand for low-volatile organic compound adhesives in electric vehicle assembly, both contributing to incremental growth. However, producers face challenges: feedstock volatility and stiff competition from acrylic and vinyl acetate ethylene copolymer emulsions are squeezing margins. In response, many are pivoting towards specialty grades and emphasizing circularity credentials.

Key Report Takeaways

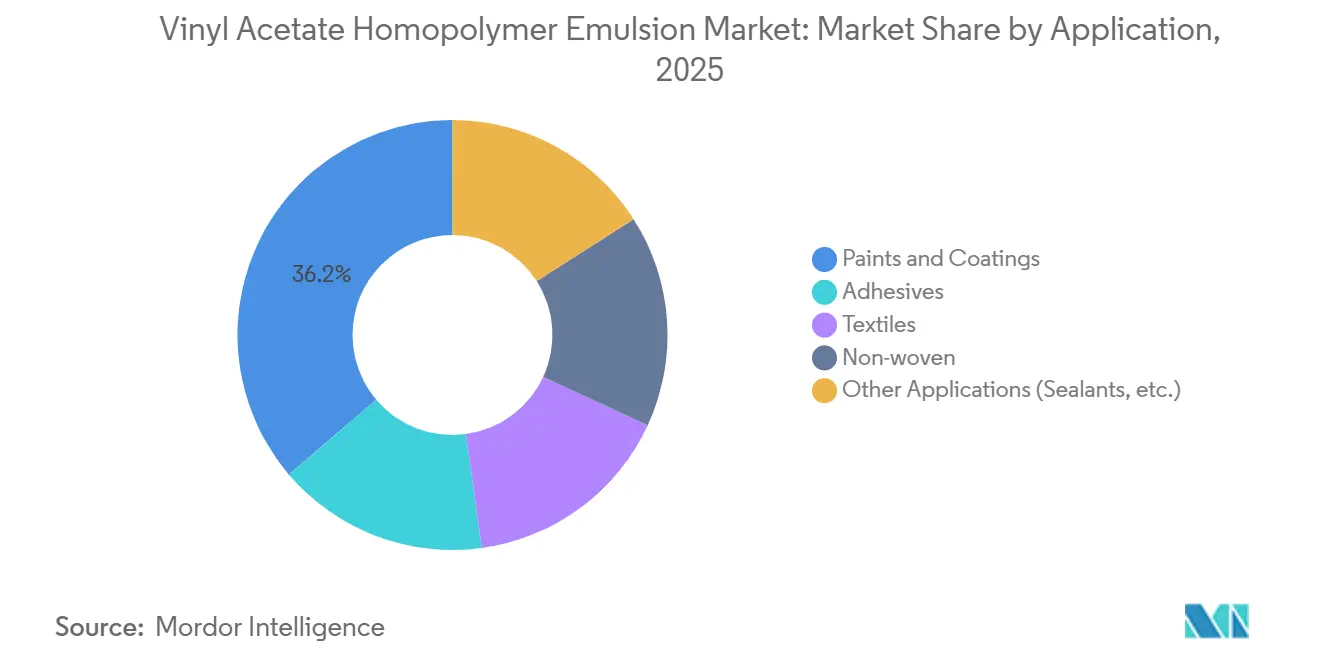

- Paints and Coatings led with 36.22% of 2025 application revenue in the vinyl acetate homopolymer emulsion market, while Non-Woven applications are projected to expand at a 4.22% CAGR through 2026 to 2031, the fastest among application segments.

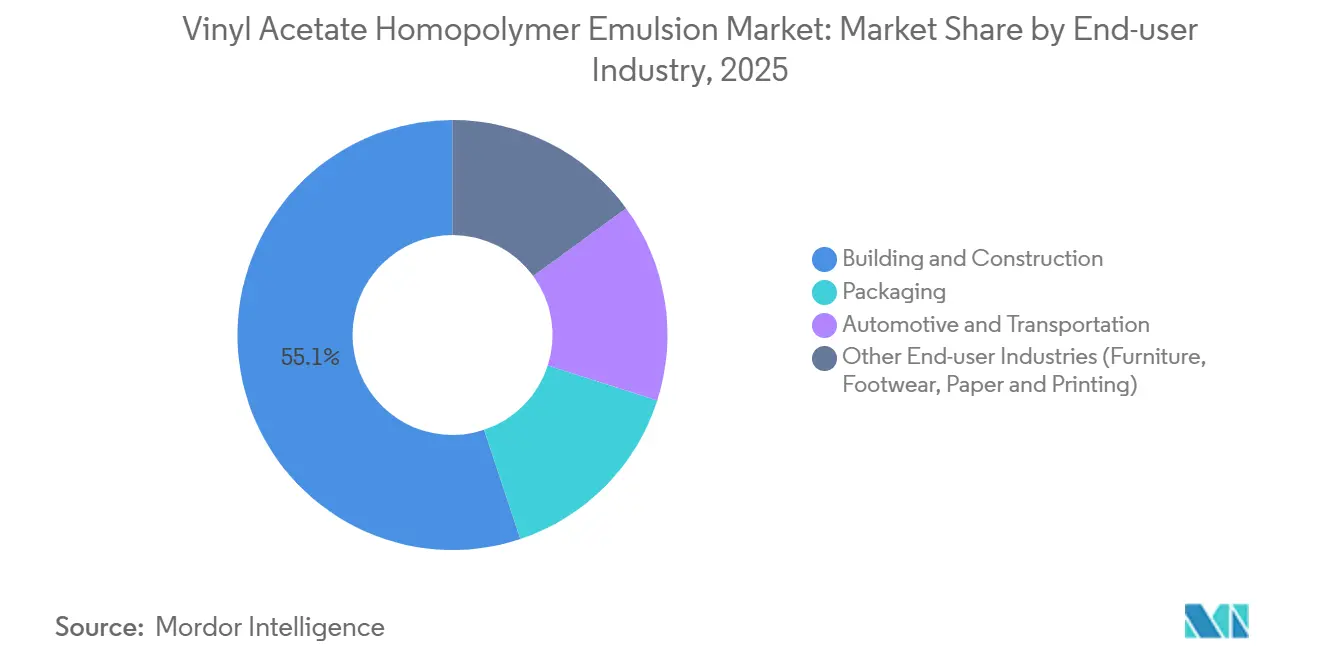

- Building and Construction held 55.12% of the 2025 end-user demand, the largest share in the vinyl acetate homopolymer emulsion market, while Automotive and Transportation is forecast to record the highest end-user growth at a 4.77% CAGR between 2026 and 2031.

- Asia-Pacific accounted for 46.67% of global revenue in 2025 and is advancing at a regional CAGR of 4.65% between 2026 and 2031, retaining its position as both the largest and fastest-growing geography in the vinyl acetate homopolymer emulsion market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vinyl Acetate Homopolymer Emulsion Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory shift toward low-VOC paints and coatings | +1.2% | Global, strongest in China, the EU, and North America | Medium term (2-4 years) |

| Growing paper and tissue production in Asia and Europe | +0.6% | Asia-Pacific core, Europe secondary | Long term (≥ 4 years) |

| Boom in non-woven hygiene output across South and Southeast Asia | +0.8% | South Asia and ASEAN countries | Medium term (2-4 years) |

| Adoption as functional barrier coatings for recyclable mono-material packaging | +0.9% | Global, led by EU and North America | Medium term (2-4 years) |

| Demand for digital-printing-grade binder emulsions | +0.4% | Global, early adoption in Asia-Pacific and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Shift Toward Low-VOC Paints And Coatings

On June 1, 2026, China enforced its GB 30981.1-2025 and GB 30981.2-2025 regulations, tightening limits on formaldehyde, heavy metals, aromatics, and volatile organic compounds. Concurrently, GB 37824-2019 mandates a significant level of abatement efficiency for non-methane hydrocarbon emissions exceeding a specific threshold in standard regions. These regulations steer formulators towards waterborne systems. Here, vinyl acetate homopolymer emulsions ensure compliance, sidestepping the need for expensive thermal oxidizers. Europe mirrors this trend with expanding bans on per- and polyfluoroalkyl substances and reduced volatile organic compound limits, while the United States sets a deadline in early 2027 for aerosol-coating regulations issued by the Environmental Protection Agency. Across the globe, downstream users prioritize binders devoid of aromatics and with minimal residual monomers. This trend gives a competitive advantage to suppliers who provide pre-qualified, regulation-compliant grades. The tightening regulations are also hastening the shift away from high-solids solvent systems in industrial metal and plastic coatings. This shift broadens the market for vinyl acetate homopolymer emulsions. Notably, a large proportion of Asia-Pacific coating formulators now prioritize "waterborne compliance" in their purchasing decisions, highlighting the influence of policy on procurement choices.

Growing Paper And Tissue Production In Asia And Europe

Urbanization and the increasing adoption of sanitary products are driving significant growth in tissue machine capacity in China, India, and ASEAN[1]Dow Inc., “2025 Form 10-K,” dow.com. Vinyl acetate homopolymer emulsions, known for their uniform film formation and strong adhesion, are favored by high-speed coaters and remain a cost-effective choice compared to styrene-acrylic alternatives. In Europe, as mills pivot from graphic-paper lines to recyclable packaging grades, there is a surge in demand for low-odor binders with customized rheology. A recent product launch highlights the merging priorities of hygiene, packaging, and recyclability. This innovation allows heat-sensitive snacks and confections to transition from traditional plastics to a more sustainable barrier-coated paper. Typically, these barrier-coated formats rely on vinyl acetate homopolymer emulsions. These emulsions not only harmonize with mineral or nanocellulose additives but also resist aqueous food simulants, offering greater formulation flexibility compared to solvent systems. This creates a beneficial cycle: as pulp expansion boosts coating demand, innovations in coating further propel paper's competition with flexible plastics.

Boom In Non-Woven Hygiene Output Across South And Southeast Asia

Converters of disposable hygiene products in India, Indonesia, and Vietnam recently commissioned several spun-bond and melt-blown lines, with additional lines planned for delivery in the near future. Vinyl acetate homopolymer emulsions, known for their soft-hand and low-yellowing properties, are bonding agents that meet skin contact migrant-free standards. This compliance sets them apart from traditional solvent-borne styrenic resins. The vinyl acetate homopolymer emulsion market is expected to grow steadily, driven by unit growth, solvent substitution, and local content mandates favoring domestic sourcing from regional plants. Synthomer reported significant volume growth in specialty vinyl polymers, crediting the resilience to hygiene-related non-wovens, which are often secured with long-term supply contracts, providing a buffer against market cyclicality. Rising labor costs are fueling a shift towards high-speed spray-bonding technologies. Here, the precise particle-size distributions of vinyl acetate homopolymer emulsions play a crucial role, ensuring uniform web integrity with reduced additive levels, thereby enhancing cost-efficiency.

Adoption As Functional Barrier Coatings For Recyclable Mono-Material Packaging

Proposals for the European Union's Packaging and Packaging Waste Regulation, combined with increasing extended-producer-responsibility fees, are pushing brand owners towards single-layer structures that are easier to recycle. When co-formulated with nanocellulose, mineral platelets, or specialty waxes at low coat weights, vinyl acetate homopolymer emulsions can serve as effective barriers against oxygen and mineral oil. This offers a seamless conversion path on existing gravure or flexographic printing lines. Smart Planet Technologies’ HyperBarrier showcases that mineral-rich coatings can provide significantly better oxygen resistance compared to polyethylene, all while being repulpable. Producers of vinyl acetate homopolymer emulsions are collaborating with paper mills and converting original equipment manufacturers to unify test methods and secure recyclability certifications from organizations like PTS and Aticelca, bolstering customer trust. With data revealing that a majority of consumers prefer recyclable options, the adoption of functional barriers signals a robust growth trajectory, bolstered by policy support, extending beyond the European Union into North America and the increasingly receptive Asia-Pacific region.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| VAM feedstock price volatility | -0.7% | Global, acute in regions reliant on imported ethylene | Short term (≤ 2 years) |

| Competition from acrylic and VAE copolymer emulsions | -0.5% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Difficulty meeting food-contact migration limits without costly cross-linkers | -0.3% | EU and North America, emerging in the Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

VAM Feedstock Price Volatility

Produced from ethylene and acetic acid, the cost of vinyl acetate monomer is closely linked to upstream benchmarks of crude oil and natural gas, which experienced significant quarterly fluctuations[2]Henkel, “Sealed for Circularity: Henkel Launches First Cold Seal Solution for Barrier-Coated Paper,” henkel.com. Outages at major vinyl acetate monomer units in Taiwan and the United States caused a significant increase in spot prices, highlighting the industry's susceptibility to unexpected downtimes. Regional price disparities, intensified by freight bottlenecks and tariff changes, compel Asian emulsion producers to navigate a tightrope between domestic and imported ethylene. This price volatility not only diminishes margins on fixed-price contracts but also complicates the cost-plus price pass-through, a challenge especially pronounced for smaller formulators. While major players like Celanese and Wacker, with their backward-linked vinyl acetate monomer capacities and ethylene pipelines, enjoy some insulation from these swings, they still acknowledge feedstock fluctuations as a significant earnings risk in their annual reports. In response, procurement teams are broadening their supply sources and securing longer-term ethylene swap contracts, albeit with the understanding that these hedges introduce additional overhead and counterparty risks.

Competition From Acrylic And VAE Copolymer Emulsions

Acrylic and vinyl acetate ethylene copolymer emulsions, known for their superior exterior durability and ultraviolet resistance, are exerting price pressure on vinyl acetate homopolymer grades. This shift is particularly evident in the architectural and pressure-sensitive adhesive markets. Wacker’s Polymers division faced a decline in sales and a significant drop in earnings before interest, taxes, depreciation, and amortization. The company attributed these setbacks to a weakened construction demand and heightened competition in lower-margin segments. Meanwhile, Arkema’s Adhesive Solutions experienced an increase in volumes, despite a dip in prices. This trend underscores the fierce cost competition within emulsion categories. In response to these market dynamics, companies are rationalizing their product lines. For instance, Synthomer is reducing its focus on base commodities. Instead, it is channeling investments into specialty vinyl polymers, notably those with the International Sustainability and Carbon Certification PLUS mass-balance certification. This strategic pivot not only enhances their market positioning but also helps reclaim pricing power in eco-labeled niches. While acrylics are gaining traction, especially in Europe and North America, where weatherability is paramount, they serve as a formidable substitute for commodity architectural paints. Here, the price premiums associated with acrylics are often justified by the extended repaint cycles they offer.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Regulation-Driven Coatings Hold Primacy As Non-Wovens Accelerate

Paints and Coatings contributed significantly to the overall revenue, equivalent to 36.22% of 2025 revenue, anchoring the vinyl acetate homopolymer emulsion market share lead in applications. Architectural formulations dominate within this slice, buoyed by China’s shift to waterborne systems and Europe’s tightening VOC ceilings. During the same horizon, performance-grade emulsions with co-monomer grafting are expected to chip away at solvent-borne industrial coatings, broadening the application base.

Non-Woven applications are anticipated to begin from a relatively smaller market base. are forecast to rise at a 4.22% CAGR between 2026 and 2031. Hygiene converters are increasingly favoring vinyl acetate homopolymer binders due to their low-odor profile and softness. Notably, a significant number of leading diaper producers in Southeast Asia have approved grades supplied locally. Meanwhile, the adhesive segment is experiencing steady growth. This is largely driven by a shift towards recyclable mono-material packaging, which has heightened the demand for resealable and cold-seal systems. These systems, in turn, depend on high-tack homopolymer dispersions. Although textile and other applications contribute a smaller share to the overall value, they serve as crucial testing grounds for digital-printing binders and specialty sealants. Innovations that prove successful in these areas often transition to higher-volume segments, ensuring a continuous flow in the product pipeline.

By End-User Industry: Construction Dominates While EV-Led Automotive Gains Pace

Building and Construction captured 55.12% of the 2025 demand. In the vinyl acetate homopolymer emulsion market, the construction sector remains the primary end-user. Key applications include tile adhesives, exterior insulation and finish system base coats, and architectural paints. To address this demand, Wacker has significantly expanded its Nanjing facility, more than doubling its polymer powder production capacity to support the growing dry-mix mortar market. Projections suggest consistent growth in construction usage. Although cyclical slowdowns may impact the pace of growth, strong urban infrastructure programs in India and Indonesia, with substantial annual investments in housing and transport, continue to drive this expansion.

The Automotive and Transportation sectors represented a small portion of overall consumption, but are slated for a 4.77% CAGR through 2026 to 2031. Among end-users, the automotive sector is leading the charge. Electric vehicle battery packs demand low-volatile organic compound sealants that boast dielectric stability. Vinyl acetate homopolymer emulsions, when modified with urethane or epoxy functionality, emerge as the go-to solution, offering both adhesion and flame retardancy. The packaging industry maintains a stable market share, bolstered by the European Union and North American retailers' push for barrier-coated paper rollouts. Meanwhile, sectors like furniture laminates, bookbinding, and footwear make up the remainder, growing in tandem with gross domestic product and providing a stabilizing effect against overall market volatility.

Geography Analysis

Asia-Pacific remains the demand epicenter, accounting for 46.67% of 2025 revenue and expanding at a 4.65% CAGR through 2026 to 2031. China's dominance in coatings volumes, coupled with India's surge in hygiene production, drives the market's momentum. Celanese's Nanjing complex, with significant production capacity for vinyl acetate monomer and vinyl acetate ethylene emulsion, stands as a testament to the localized supply strategies essential for catering to the region's vast consumption. Regulatory momentum, particularly China's GB 30981 series, solidifies the shift towards waterborne products. Meanwhile, hygiene plants in the Association of Southeast Asian Nations region offer an incremental boost. India's ambitious goal to double housing availability anchors the demand for construction-related coatings. Furthermore, a proposed reduction in the goods and services tax on water-based paints could significantly accelerate their adoption.

North America and Europe collectively represent a substantial portion of global spending. In the United States, the Environmental Protection Agency's deadline for aerosol coatings, combined with state-level regulations on volatile organic compounds, promotes the adoption of vinyl acetate homopolymer in consumer goods. Concurrently, Wacker's expansion in Kentucky fortifies the domestic supply chain. Europe's push towards a circular economy fuels demand for mono-material barrier applications. Arkema's strategic acquisition of Dow's flexible-packaging adhesives business positions it to benefit from this policy momentum. Despite the maturity of construction markets, mandates for retrofit energy efficiency and a focus on automotive lightweighting continue to drive modest growth.

While South America accounts for a smaller share of global revenue, it reaps benefits from Brazilian infrastructure projects and investments in original equipment manufacturer automotive. However, currency volatility poses challenges, especially in raw-material import costs. This unpredictability nudges converters towards local sourcing. Responding to this trend, Synthomer has localized its products, transitioning previously imported European grades to its United States and Latin American plants, thereby reducing exposure to freight and duties. The Middle East and Africa, though smaller in absolute size, witness pockets of significant growth. This expansion is particularly notable where Saudi and South African housing initiatives align with a rising disposable income and increased hygiene consumption, albeit starting from a modest base and facing constraints due to limited polymerization capacity.

Competitive Landscape

The Vinyl Acetate Homopolymer Emulsion Market is moderately fragmented. Sustainability features like mass-balance bio-content, recyclability, and fluorocarbon-free formulations are pivotal differentiators. For instance, Henkel’s cold-seal paper coating underscores the market's demand for such attributes, leading upstream suppliers to craft binders that are pre-validated for paper recycling. The intensity of intellectual property is on the rise; a patent by Dow and Rohm & Haas on silicone-modified binders highlights a blending of acrylic and vinyl acetate chemistry, paving the way for innovative performance enhancements. Smaller players in regional hubs like China, India, and Southeast Asia are capitalizing on local feedstock access and reduced overheads, allowing them to price aggressively. This trend poses margin compression challenges for larger multinationals operating in commoditized segments.

Vinyl Acetate Homopolymer Emulsion Industry Leaders

Wacker Chemie AG

Celanese Corporation

Dow

Arkema

Chang Chun Group.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Wacker Chemie announced in its annual report that it has expanded VAE dispersions capacity at Calvert City, United States, reinforcing supply resilience and supporting demand in construction, coatings, and adhesives amid challenging global market conditions.

- March 2024: Sekisui Specialty Chemicals relaunched its Selvol Ultiloc polyvinyl alcohol copolymer series, boosting VAM-based product offerings with improved adhesion, water resistance, and flexibility for coatings, adhesives, and construction applications.

Global Vinyl Acetate Homopolymer Emulsion Market Report Scope

Vinyl acetate homopolymer emulsion is produced by polymerizing vinyl acetate monomers in water, forming a milky white dispersion of polyvinyl acetate (PVAc). It offers excellent adhesion to porous substrates like paper, wood, and textiles, making it vital in adhesives, paints, and coatings. Its water-based nature ensures low VOC emissions, recyclability, and compatibility with sustainable construction and packaging applications, supporting global demand for eco-friendly materials.

The Global Vinyl Acetate Homopolymer Emulsion Market is segmented by application, end-user industry, and geography. By Application, the market is segmented into paints and coatings, adhesives, textiles, non-woven, and other applications such as sealants. By End-user Industry, the market is segmented into building and construction, packaging, automotive and transportation, and other end-user industries, including furniture, footwear, paper, and printing. The report also covers the market size and forecasts for the Global Vinyl Acetate Homopolymer Emulsion Market in 19 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Paints and Coatings |

| Adhesives |

| Textiles |

| Non-woven |

| Other Applications (Sealants, etc.) |

| Building and Construction |

| Packaging |

| Automotive and Transportation |

| Other End-user Industries (Furniture, Footwear, Paper and Printing) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | Paints and Coatings | |

| Adhesives | ||

| Textiles | ||

| Non-woven | ||

| Other Applications (Sealants, etc.) | ||

| By End-user Industry | Building and Construction | |

| Packaging | ||

| Automotive and Transportation | ||

| Other End-user Industries (Furniture, Footwear, Paper and Printing) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will the vinyl acetate homopolymer emulsion market be by 2031?

The vinyl acetate homopolymer emulsion market size is projected to reach USD 4.32 billion by 2031, growing at a 4.12% CAGR from 2026.

Which application segment is expanding the fastest?

Non-Woven hygiene materials are forecast to grow at a 4.22% CAGR through 2031 as diaper and feminine-care producers in South and Southeast Asia scale capacity.

Why is Asia-Pacific the dominant region for vinyl acetate homopolymer emulsions?

Asia-Pacific commands 46.67% of global revenue thanks to China’s construction activity, India’s rising manufacturing, and ASEAN hygiene demand, all reinforced by local capacity expansions from major suppliers.

Which end-user industry offers the highest growth potential beyond construction?

Automotive and Transportation, especially electric-vehicle assembly, is poised for a 4.77% CAGR through 2026 to 2031 as low-VOC adhesives and sealants gain ground.

How are suppliers managing feedstock price volatility?

Leading producers mitigate VAM swings through backward integration, multi-year ethylene contracts, and geographic diversification of production assets.

Page last updated on: