Emulsion Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

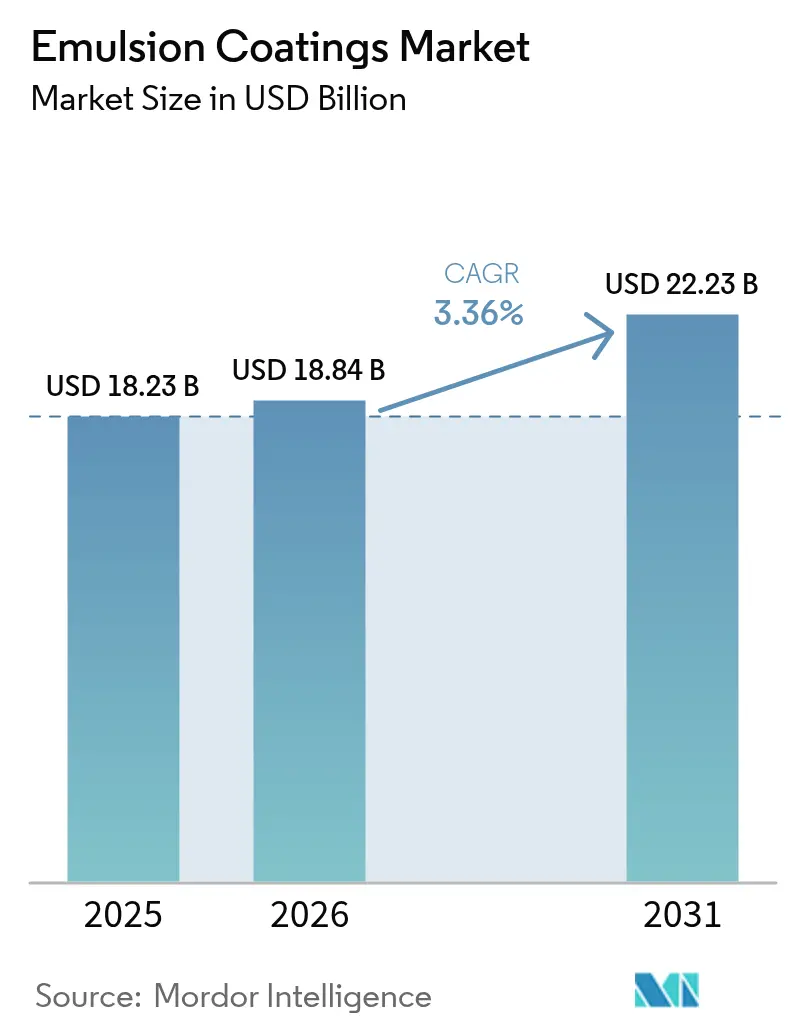

| Market Size (2026) | USD 18.84 Billion |

| Market Size (2031) | USD 22.23 Billion |

| Growth Rate (2026 - 2031) | 3.36% CAGR |

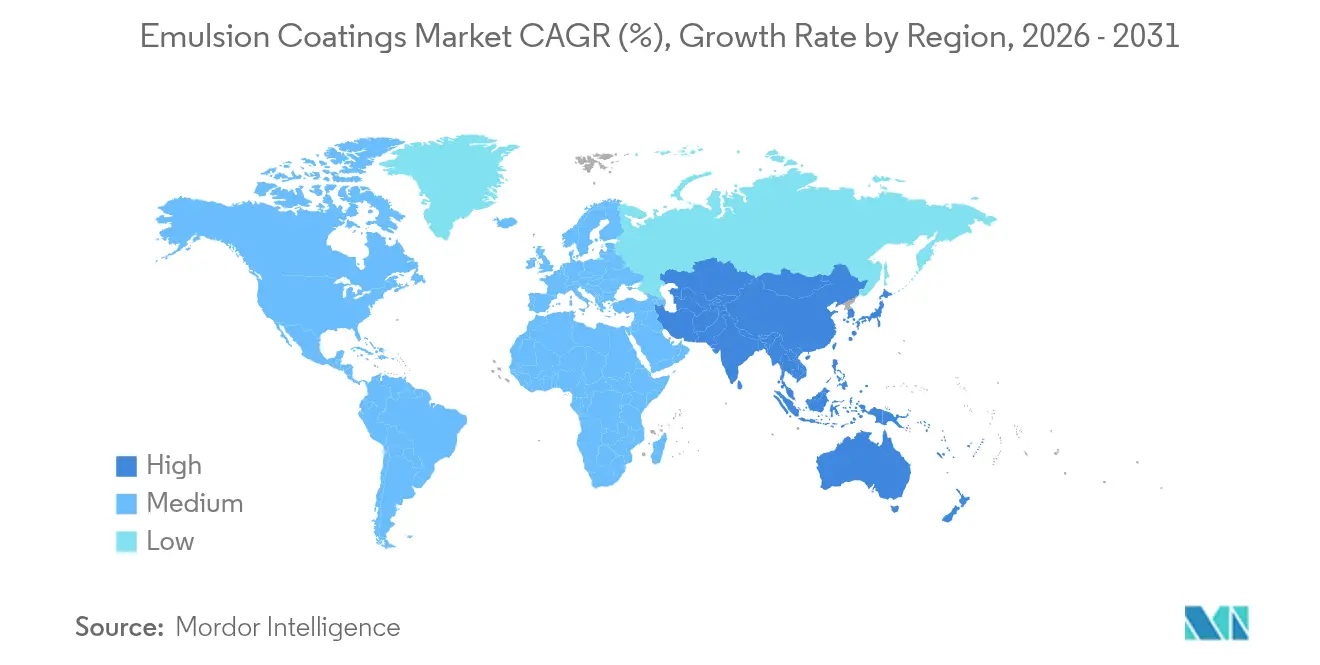

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Emulsion Coatings Market Analysis by Mordor Intelligence

The emulsion coatings market size in 2026 is estimated at USD 18.84 billion, growing from 2025 value of USD 18.23 billion with 2031 projections showing USD 22.23 billion, growing at 3.36% CAGR over 2026-2031. This steady expansion reflects sustained construction activity, durable demand from industrial users, and rapid adoption of low-VOC water-borne chemistries that increasingly rival solvent-based performance. Regulatory frameworks in North America, Europe, and parts of Asia continue to tighten permissible solvent content, accelerating the shift toward advanced acrylic, polyurethane, and hybrid emulsions. Meanwhile, manufacturing hubs in the Asia-Pacific leverage scale advantages and local feedstock availability to supply cost-competitive formulations that meet global performance benchmarks. Digital color-matching, faster-curing systems, and smarter supply-chain tools further enhance the customer experience and help producers protect their margins in an environment of volatile raw-material costs.

Key Report Takeaways

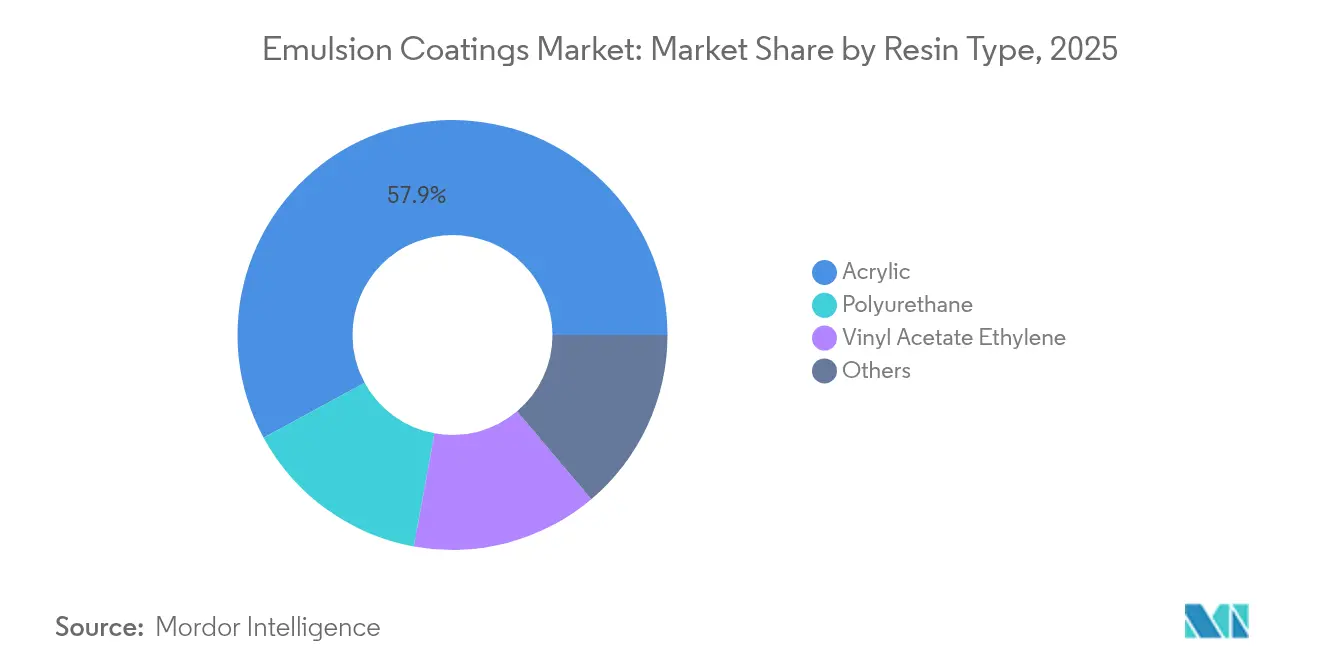

- By resin type, acrylic resins held 57.92% of the emulsion coatings market share in 2025, while polyurethane emulsions are forecast to expand at a 4.17% CAGR through 2031.

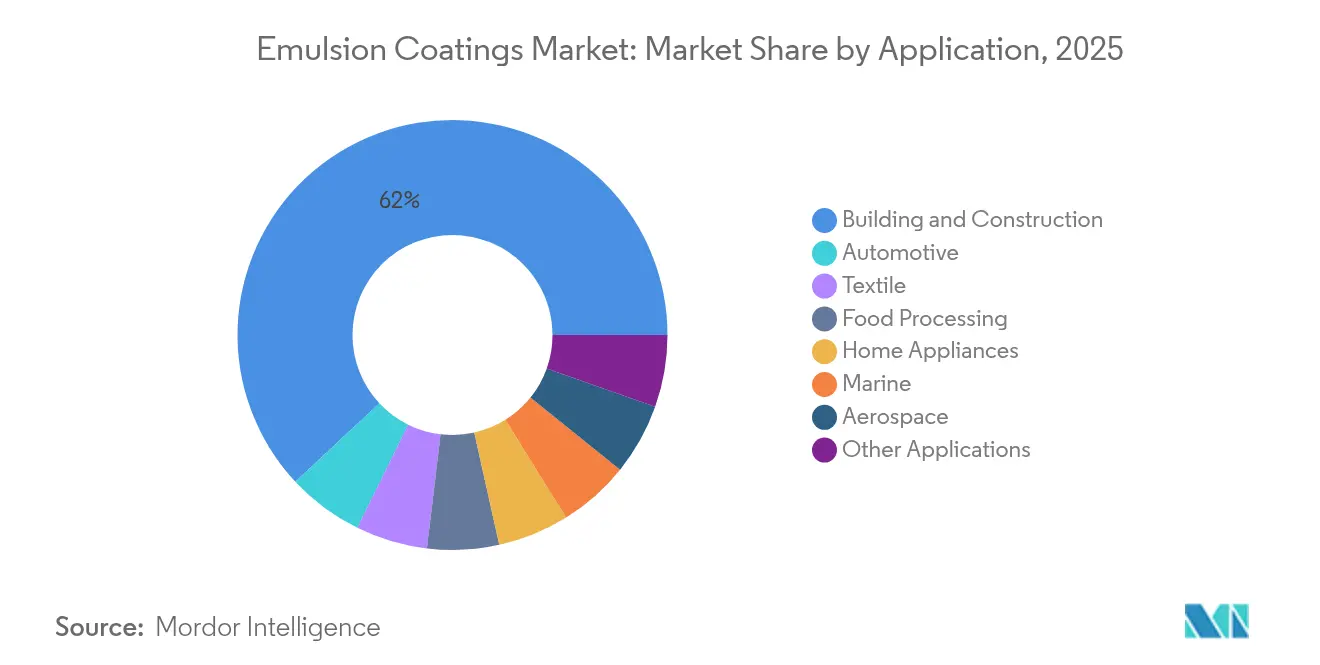

- By application, building and construction accounted for 61.95% of the emulsion coatings market size in 2025, whereas automotive coatings are set to advance at a 4.06% CAGR to 2031.

- By geography, the Asia-Pacific region commanded 45.05% of the revenue in 2025 and is projected to grow at a 3.82% CAGR, outpacing all other regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Emulsion Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory tailwinds on VOC and carbon-reduction | +0.8% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rapid formulation advances closing performance gap | +0.6% | Global, led by Asian production hubs | Long term (≥ 4 years) |

| Urban refurbishment boom in Asian megacities | +0.5% | China, India, ASEAN | Short term (≤ 2 years) |

| OEM shift to high-speed water-borne lines in appliances | +0.4% | Automotive and appliance clusters worldwide | Medium term (2-4 years) |

| Climate-proof infrastructure needs | +0.3% | Coastal and extreme-climate regions on all continents | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Tailwinds on VOC and Carbon-Reduction

Multiple jurisdictions now cap VOC levels for architectural coatings at or below 30 g/L, prompting formulators to accelerate the development of waterborne coatings. The European Commission’s Industrial Emissions revisions and California’s latest amendments to Rule 1113 exemplify the policy momentum that directly benefits the emulsion coatings market. U.S. states aligning with these benchmarks broaden the compliance footprint and reinforce demand for low-solvent chemistries across the residential, commercial, and industrial spectrum.

Rapid Formulation Advances Closing Performance Gap

Breakthrough acrylic copolymers launched by BASF in 2024 delivered chemical resistance levels once reserved for two-component polyurethanes[1]BASF SE, “Next-Generation Acrylic Copolymers for High-Performance Waterborne Coatings,” basf.com. Hybrid crosslinking technology enhances hardness, weatherability, and early block resistance, enabling single-pack, waterborne systems to replace solvent-rich alternatives in the fields of equipment, transportation, and protective maintenance. Nanofiller dispersions strengthen barrier properties, while bio-derived crosslinkers improve adhesion without compromising sustainability.

Urban Refurbishment Boom in Asian Megacities

Government-backed urban renewal programs across China, India, and fast-growing ASEAN economies drive large-volume demand for interior and exterior architectural paints. China’s Ministry of Housing and Urban-Rural Development allocates multi-year budgets to refurbish aging residential blocks, specifying low-VOC finishes that extend coating lifecycles[2]Ministry of Housing and Urban-Rural Development, “Urban Renewal Action Plan 2023-2025,” mohu.gov.cn. India’s Smart Cities Mission ties infrastructure grants to sustainability criteria, cementing a sizable pipeline for high-performance water-borne products.

OEM Shift to High-Speed Water-Borne Lines in Appliances

Appliance producers are converting electrostatic booths and curing ovens to accommodate next-generation emulsions that rapidly flash off moisture, reduce bake temperatures, and eliminate costly solvent-recovery loops. Whirlpool committed USD 150 million to retrofit North American plants in 2024, citing 25% shorter cycle times and 75% lower VOC emissions. Automotive OEMs, such as Tesla, deploy similar technology in high-output paint shops, reinforcing cross-sector momentum.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acrylic acid and VAM price volatility | -0.7% | Global, especially price-sensitive architectural segments | Short term (≤ 2 years) |

| Skilled-labor gaps for correct film application | -0.4% | Developed markets, emerging across the Asia-Pacific | Medium term (2-4 years) |

| Water scarcity and wastewater-treatment cost inflation | -0.2% | Water-stressed regions in the Middle East, North Africa, and parts of Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acrylic Acid and VAM Price Volatility

Supply disruptions linked to weather events and major maintenance turnarounds periodically spike feedstock costs, squeezing margins for commodity-grade architectural paints. Smaller regional producers without long-term contracts face the greatest exposure, prompting some to curtail output or pursue mergers to stabilize sourcing. Raw-material swings also trigger frequent surcharge announcements from multinational suppliers, forcing downstream customers to recalibrate budgets and inventory cycles.

Skilled-Labor Gaps for Correct Film Application

Water-borne coatings demand tighter surface preparation, humidity control, and film-build management than legacy solvent systems. The National Association of Home Builders recorded upward of 430,000 unfilled construction positions in 2024, many involving finishing trades. Producers collaborate with trade schools, distributors, and applicator networks on certification programs that standardize best practices and reduce warranty claims.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylic Dominance Faces Polyurethane Challenge

Acrylic solutions retained 57.92% of the emulsion coatings market share in 2025, owing to balanced cost-to-performance profiles across interior walls, façades, and DIY projects. The introduction of self-crosslinking acrylic-polyurethane hybrids by Dow in 2024 further blurred the boundary between commodity and premium grades. Polyurethane emulsions are projected to post the fastest expansion at a 4.17% CAGR through 2031, as industrial and automotive end-users demand superior abrasion resistance, chemical resilience, and gloss retention. Vinyl acetate ethylene copolymers maintain steady niches in paper, textile, and adhesive formulations, while specialty styrene-acrylic blends satisfy marine and aerospace regulations that require flame retardancy and low smoke density. Competitive positioning is increasingly dependent on polymer architecture customization, renewable content options, and compatibility with automated spray or roll-coat lines.

Downstream customers continually benchmark resin systems on hardness development, water whitening, and dirt pick-up resistance, criteria that now approach solvent-borne levels. Producers, therefore, channel research and development spending toward particle-size optimization, surfactant-free stabilization, and multifunctional additive packages that deliver stain blocking alongside early water resistance. Such advances help acrylic chemistries maintain volume leadership even as polyurethane grades capture higher-value pockets.

By Application: Construction Stability Meets Automotive Dynamism

Building and construction accounted for 61.95% of the emulsion coatings market size in 2025, driven by cyclical repaint demand and policy-driven green building programs. Exterior topcoats with elastomeric crack-bridging properties mitigate thermal cycling stress on concrete façades, while interior low-odor finishes support faster turnover in commercial real estate. Protective concrete sealers and floor coatings extend the lifespan of assets in transport terminals and industrial warehouses, supporting large-scale operations.

Automotive OEMs and tier suppliers are expected to register the fastest growth at a 4.06% CAGR to 2031, driven by the adoption of lightweight substrates, electrification assembly layouts, and a shift toward compact modular paint shops. Water-borne basecoat-clearcoat stacks deliver reduced bake temperatures and improved first-time-through rates, enabling throughput gains without expanding floor space. Appliances, food processing equipment, and HVAC housings also adopt refined emulsions certified for indirect food contact or antimicrobial performance. Niche segments such as aerospace cabin interiors and marine antifouling remain specialized, yet they validate high-value formulation strategies that often transfer back into mainstream markets.

Geography Analysis

The Asia-Pacific region accounted for 45.05% of global revenue in 2025, underpinned by China’s infrastructure outlays and India’s Smart Cities investments, which collectively sustain tens of millions of gallons of architectural paint demand each year. Ongoing relocation of specialty chemicals production to Southeast Asia enhances regional self-sufficiency and shortens lead times for export-oriented OEMs. The emulsion coatings market benefits from favorable government policies that incentivize water conservation, VOC reduction, and circular-economy practices.

North America ranks second, driven by stringent EPA air-toxics rules and the Inflation Reduction Act’s building-efficiency tax credits that reward low-emission products. Renovation cycles in residential housing and mandated bridge refurbishments keep baseline demand resilient even when new construction slows. Europe follows closely, with the EU Green Deal reinforcing eco-label criteria and carbon-pricing schemes that encourage specifiers to adopt water-borne solutions. Growth in these mature regions remains modest, yet elevated average selling prices buoy revenue.

Latin America, the Middle East, and Africa together represent a sizable catch-up opportunity. Brazil’s Casa Verde e Amarela housing subsidy program, Mexico’s near-shoring-driven industrial parks, and Saudi Arabia’s giga-projects, such as NEOM, all require high-performance coatings that tolerate extreme climates. Political risk, currency volatility, and fragmented distribution complicate entry strategies; however, multinationals that localize production and establish installer training networks stand to reap outsized gains.

Regulatory Landscape

VOC and chemical-management rules continue to steer formulation choices toward water-borne emulsions. Several jurisdictions use low-VOC benchmarks, including architectural limits at or below 30 g/L in parts of North America, which procurement and compliance teams treat as reference points. In the United States, US EPA oversight under TSCA adds compliance workload around PFAS reporting and recordkeeping, including TSCA Section 8(a)(7). The agency also maintains Significant New Use Rule requirements for certain long-chain PFAS used as surface coatings, which affects both manufacturers and importers of coated articles.

In Europe, EU REACH obligations, including SVHC communication thresholds, and the evolving CLP framework drive updates to labeling, classification, and mixture-notification requirements that can cascade through global supply chains serving the EU market. ECHA has also highlighted the transition of Poison Centre Notifications and Unique Formula Identifier (UFI) requirements into a stricter compliance phase. EU CLP transitional provisions linked to Regulation (EU) 2024/2865 form part of the compliance timeline for products newly placed on the market, reinforcing the need for auditable formulation data and tighter packaging-label governance for hazardous mixtures.

Value Chain Analysis

The value chain begins with upstream petrochemical and specialty-chemical feedstocks that support key monomers, such as acrylic acid and vinyl acetate, plus functional additives including surfactants, defoamers, coalescents, and preservatives. Midstream producers convert these inputs into waterborne polymer dispersions and latex binders through emulsion polymerization and related dispersion processes. They then blend the binders with pigments, notably titanium dioxide, fillers, and performance additives to produce finished emulsion coatings. Volatility in acrylic acid and VAM inputs remains a central cost and availability variable for architectural grades, shaping sourcing strategies that rely on multi-sourcing, contractual terms, and regional production hubs.

Downstream, coatings manufacturers sell through contractor and retail channels for architectural paints and through direct-to-OEM and applicator networks for industrial, automotive, appliance, and protective segments. Supplier qualification depends on consistency, application-window robustness, and compliance documentation. Process control and digitalization are increasingly visible differentiators in the midstream stage: recent academic work in 2026 highlights predictive modeling and advanced reactor-control approaches for seeded semi-batch emulsion polymerization, which aligns with industry efforts to reduce batch variability and shorten formulation-to-scale-up cycles.

Competitive Landscape

The emulsion coatings market is moderately concentrated, with global players such as The Sherwin-Williams Company occupying the top tier. The top five players in the market hold a significant share of the global market. Scale grants purchasing leverage in acrylic acid, titanium dioxide, and specialty surfactants, enabling leaders to buffer input shocks more effectively than smaller rivals. Robust capital budgets fund continuous plant debottlenecking, energy-efficient reactors, and digital color-matching tools that heighten customer stickiness. Innovation pipelines focus on multifunctional polymers, low-sheen exterior grades that resist early chalking, and food-contact-safe interior coatings that meet the new regulations for e-commerce fulfillment centers. Sustainability goals drive the launch of bio-based binders, while lifecycle-assessment dashboards help specifiers quantify their carbon footprints. Strategic acquisitions remain a preferred route to market expansion; AkzoNobel’s purchase of Grupo Orbis’s decorative business in 2024 immediately bolstered its Latin American footprint and widened its retail channel access.

Regional producers counterbalance with hyper-localized shades, flexible batch sizes, and rapid logistics. However, compliance costs tied to emerging PFAS-restriction legislation and tougher wastewater standards strain thin balance sheets, nudging some to seek joint ventures with raw-material suppliers or explore specialty niches such as functional primers or conductive inks. Digital marketplaces for professional painters add another competitive dimension, granting early movers data-driven upselling capabilities.

Emulsion Coatings Industry Leaders

The Sherwin-Williams Company

PPG Industries, Inc.

AkzoNobel N.V.

Nippon Paint Holdings Co., Ltd.

RPM International Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities cluster around three practical areas of whitespace: (1) compliant low-odor, low-VOC architectural coatings that align with tighter VOC caps and green-building criteria, (2) higher-performance water-borne systems that replace solvent-borne stacks in industrial and OEM lines, and (3) better supply security in binders and monomers to reduce exposure to acrylic acid and VAM swings. In 2026, activity across the chain points to these levers, including BASF expanding dispersions capacity at its Mangalore (India) and Durban (South Africa) sites. WYN Polymers also started up a new reactor that increased water-based polymer output by about 30%, indicating continued investment in waterborne binder supply to support emulsion-coatings demand across regions.

Investment is also showing up in product and formulation pathways. Nouryon launched Alcosperse OTA-100 in 2026 to help formulators produce higher-performing, low-odor architectural paints with reduced VOC levels, reflecting demand for additive packages that maintain performance while meeting compliance and indoor-air requirements. On the R&D side, the growing use of machine learning and predictive process modeling in coatings and polymerization workflows supports faster iteration on compliant formulations and more consistent plant execution, particularly for OEMs and large contractors that require tighter batch-to-batch control and documentation.

Recent Industry Developments

- April 2026: The Sherwin-Williams Company launched Emerald Symmetry Interior Acrylic, positioned as a zero-VOC interior paint with 22% plant-based carbon content and certifications aligned to green building and indoor-air requirements. The launch reinforces premium architectural demand for low-odor, low-emission water-borne emulsions and adds emphasis on bio-based content and third-party certification as differentiators.

- March 2025: Asian Paints Limited approved additional capex for its Dahej, Gujarat VAE and VAM manufacturing facility, increasing the total project cost to INR 3,250 crore. Expanding upstream monomer and binder availability supports emulsion-coatings supply security and reduces exposure to external sourcing risk for high-volume architectural and industrial formulations.

- April 2024: The Lubrizol Corporation announced a USD 20 million investment to upgrade acrylic emulsion manufacturing capacity at its Gastonia, North Carolina site. The added capability strengthens regional supply for waterborne binder demand and supports faster customer service for coatings producers operating under tightening VOC and performance requirements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the emulsion coatings market covers water-based coating formulations where polymer binders are dispersed in water and sold as coatings for protective and decorative uses across major end-use industries, measured in value terms.

Scope exclusions: This sizing excludes solvent-borne coatings and powder coatings, and it also excludes upstream polymer emulsion raw material sales when they are not sold as coatings.

Segmentation Overview

- By Resin Type

- Acrylic

- Vinyl Acetate Ethylene

- Polyurethane

- Others

- By Application

- Building and Construction

- Automotive

- Aerospace

- Home Appliances

- Marine

- Food Processing

- Textile

- Other Applications

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Australia and New Zealand

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with pinning down the demand pool, the pricing boundary, and the end-use exposures that typically drive consumption of water-based coatings. Public sources were used to anchor model inputs, such as national construction statistics and building permits, automotive production series, trade and customs coatings codes where available, and environmental agency publications on VOC regulations.

To keep assumptions realistic, we also reviewed manufacturer annual reports and investor decks, association websites for paints and coatings, and technical journals covering formulation trends like acrylic and VAE systems. In a few places, paid subscriptions for company financials and news intelligence were referenced to normalize segment mixes and to sanity check price movement timing across regions. The desk sources listed here are illustrative only, and many additional public sources were consulted for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming what is actually counted as emulsion coatings in commercial sales, and how demand shifts across building and construction, automotive, appliances, marine, and textile uses. We spoke with a mix of raw material informed experts, coatings formulators, distributors, and large end users across APAC, EMEA, and the Americas, so gaps from desk inputs could be closed and pricing and mix assumptions could be tested.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 12% | APAC: 49% |

| Mid tier: 42% | Functional/Unit leaders: 35% | EMEA: 32% |

| Smaller Players: 19% | Managers: 53% | Americas: 19% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand reconstruction where construction activity, industrial production signals, and vehicle output were translated into likely coating consumption, and then converted into value using region-specific price ranges and mix splits. The totals were then corroborated using selective bottom-up approximations, mainly from supplier revenue exposure checks, sampled ASP multiplied by volume proxies, and distributor channel feedback, which helped adjust for undercounted applications.

Key inputs used in the model included the share of water-based coatings adoption by end-use, acrylic versus VAE and polyurethane emulsion mix, typical dry film usage rates in architectural and industrial jobs, regional construction spending trends, and the timing of VOC compliance upgrades that pull demand toward emulsions. For forecasting, scenario analysis was applied around construction cycles, auto production outlook, and pricing progression, and the final trajectory was aligned to what primary experts viewed as realistic adoption and mix change speeds. Where bottom-up signals were incomplete, gaps were handled through proportional allocation based on end-use share, regional capacity footprint, and validated price bands rather than forcing a full supplier roll-up.

Data Validation & Update Cycle

Outputs were checked against independent signals like resin demand direction, construction and auto indicators, and the expected split of architectural versus industrial coatings in each region. When variances showed up, assumptions were revisited in steps, starting with scope checks, then pricing timing, and then mix and adoption rates, followed by a second analyst review before sign-off.

The report is refreshed annually, and interim updates are made when material events affect demand or pricing, such as major regulatory changes, sharp feedstock swings, or sudden regional construction slowdowns. Before delivery, a fresh pass is completed so the client receives an updated view with the latest available public indicators and validated assumptions.

Mordor Intelligence's Emulsion Coatings Market Estimate Compared With Other Published Estimates

Published estimates for emulsion coatings can vary a lot even when the market name sounds identical, because the counted products and the pricing boundary are often not aligned. Differences also come from whether the model leans more on end-use demand signals or on broad revenue assumptions that are not fully reconciled with application realities.

By tracking resin mix shifts, end-use demand indicators, and currency timing across regions, Mordor Intelligence keeps the estimate tied to coatings sold as emulsions for defined applications, instead of blending in adjacent solvent-borne categories or upstream polymer emulsion sales.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 18.84 B (2026) | |

| Trade Journal A | USD 14.11 B (2024) | Uses an earlier base year and a wider technology lens that appears to mix water-based with other formulation types, which shifts the counted value and makes the timing less comparable. |

| Industry Publisher B | USD 9.00 B (2023) | Leans on a narrower application framing (mainly architectural and limited industrial) and applies growth rates forward without clearly harmonizing regional price bands and mix changes. |

The spread across sources is largely explained by year alignment, scope boundaries, and how pricing and mix are treated over time. When scope is kept consistent to emulsion coatings sold into defined end uses, and when the price and mix assumptions are checked against real demand signals, the market value becomes easier to replicate and explain.

Key Questions Answered in the Report

What is the current value of the emulsion coatings market?

The emulsion coatings market size reached USD 18.84 billion in 2026 and is projected to increase to USD 22.23 billion by 2031.

Which resin segment is growing the fastest?

Polyurethane emulsions are expanding at a 4.17% CAGR because they meet demanding durability standards in automotive and industrial uses.

Why is Asia-Pacific the largest regional market?

Large-scale infrastructure spending, strong manufacturing bases, and supportive environmental policies contribute to the Asia-Pacific region's 45.05% global revenue share.

How do VOC regulations influence product development?

Tighter VOC caps worldwide are pushing formulators to accelerate waterborne innovation, boosting low-solvent products that comply without performance trade-offs.

What challenges do producers face with raw materials?

Volatile pricing for acrylic acid and vinyl acetate monomer strains margins, especially for smaller firms lacking long-term supply contracts.

Which end-use sector shows the highest growth rate?

Automotive coatings post the strongest momentum, registering a 4.06% CAGR as OEMs convert paint lines to high-speed water-borne processes.

Page last updated on: