Acrylic Emulsions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.59 Billion |

| Market Size (2031) | USD 16.41 Billion |

| Growth Rate (2026 - 2031) | 5.44% CAGR |

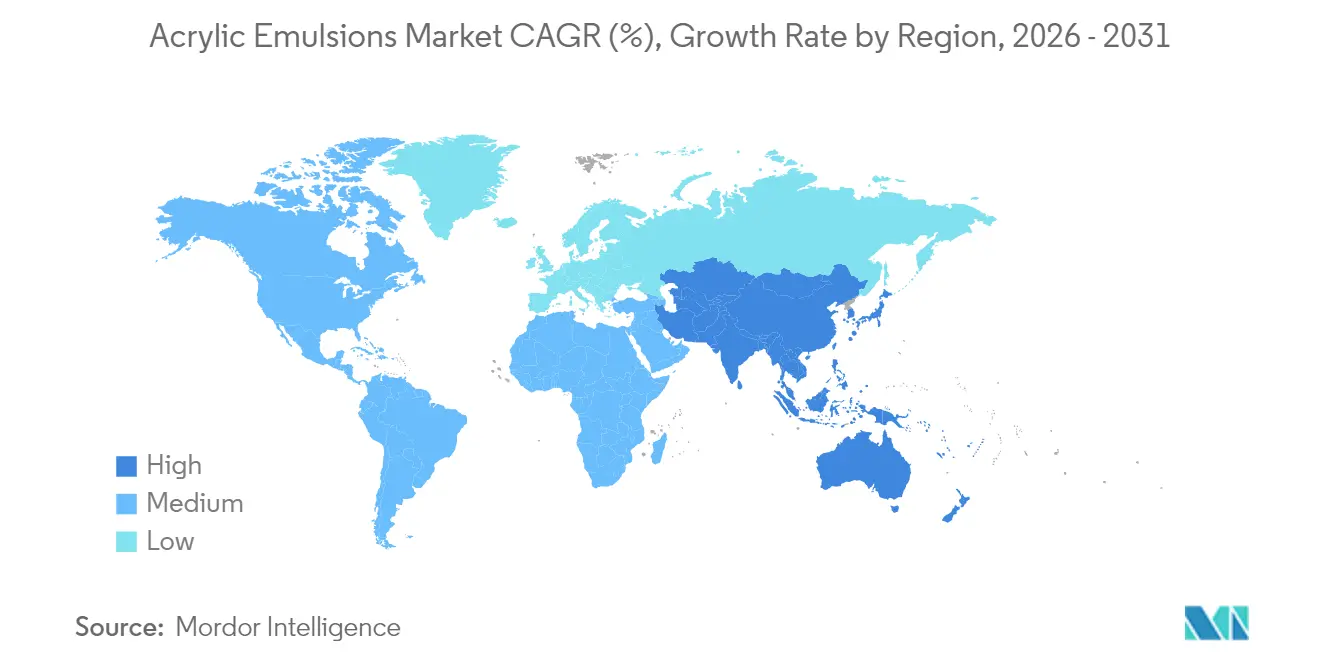

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

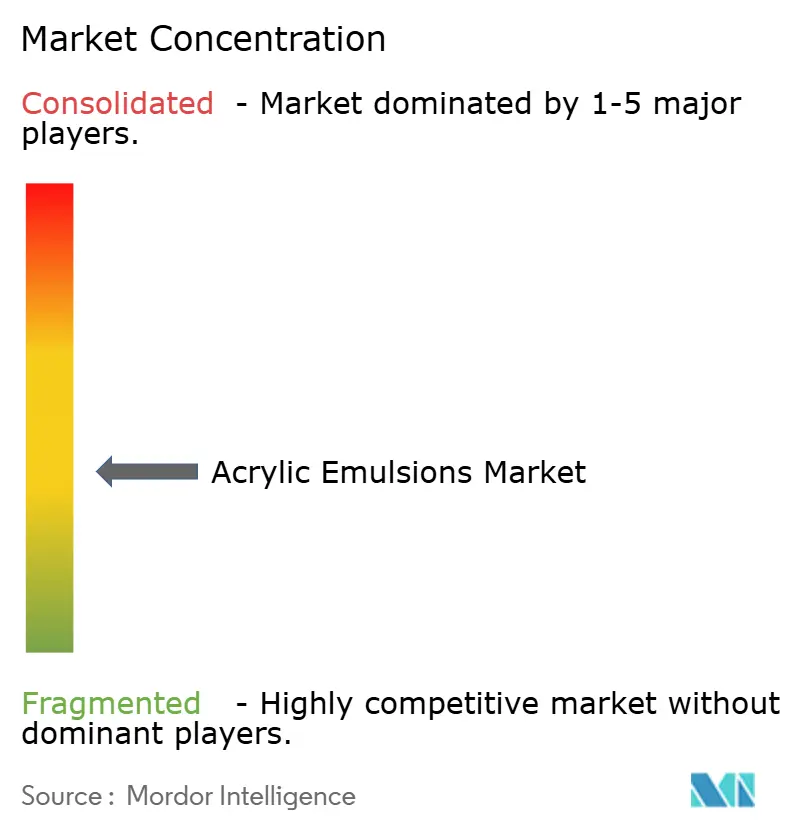

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acrylic Emulsions Market Analysis by Mordor Intelligence

The Acrylic Emulsions Market size is expected to grow from USD 11.94 billion in 2025 to USD 12.59 billion in 2026 and is forecast to reach USD 16.41 billion by 2031 at 5.44% CAGR over 2026-2031. Regulatory pressure that favors water-borne formulations, steady infrastructure spending in Asia-Pacific, and rapid adoption of digital printing technologies underpin this expansion. Paint makers, adhesive formulators, and paper converters continue to switch from solvent to water-borne systems to secure compliance with low-VOC rules in the United States, Canada, and the European Union. At the same time, manufacturers are investing in self-crosslinking and PFAS-free chemistries to capture premium niches, while capacity additions in the United States and the Netherlands safeguard supply security. Though feedstock price volatility presses margins, technology upgrades and sustainability commitments provide headroom for value-based pricing, enabling producers to preserve profitability even when monomer costs fluctuate.

Key Report Takeaways

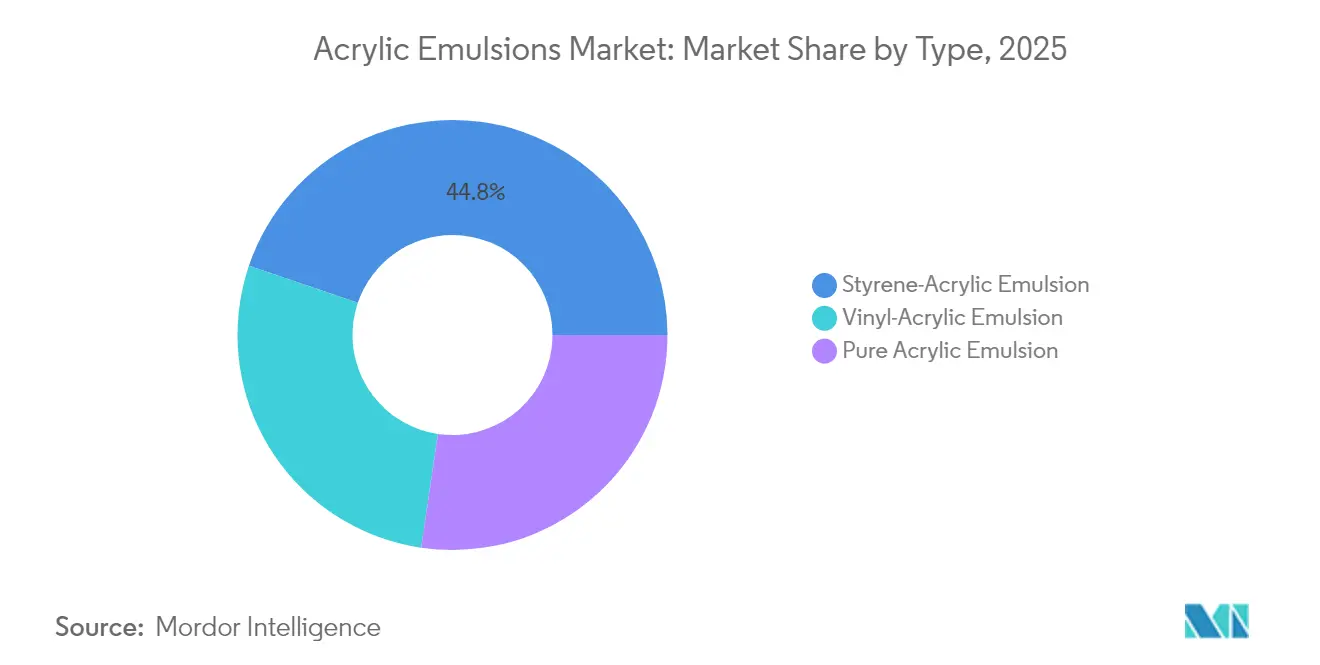

- By type, styrene-acrylic captured 44.78% acrylic emulsions market share in 2025, whereas vinyl-acrylic is forecast to expand at a 6.14% CAGR through 2031.

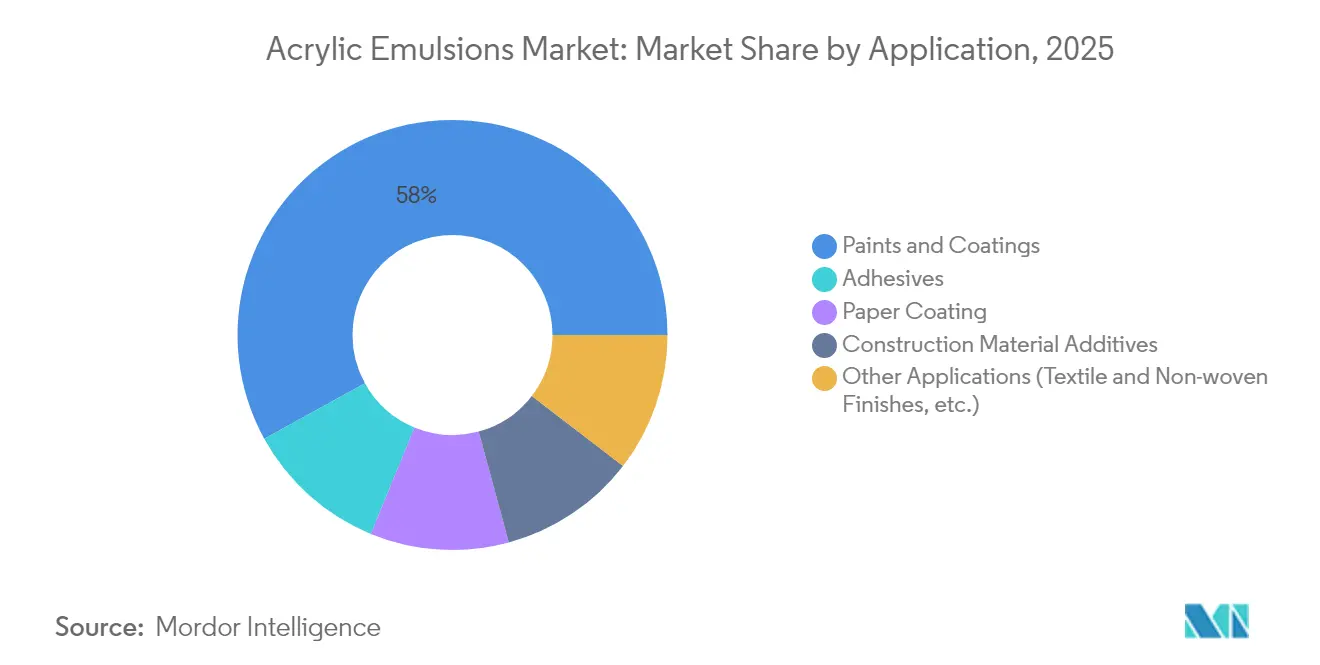

- By application, paints and coatings accounted for 58.02% of the acrylic emulsions market size in 2025; adhesives are set to grow the fastest at 6.03% CAGR to 2031.

- By geography, Asia-Pacific led with 46.05% revenue share in 2025 and is advancing at a 5.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Acrylic Emulsions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low-VOC push for water-borne paints/coatings | +1.2% | North America and Europe | Medium term (2-4 years) |

| Booming construction spending in developing nations | +1.8% | Asia-Pacific core; Latin America, MEA spill-over | Long term (≥ 4 years) |

| Digital ink-jet printing inks adoption | +0.7% | North America and Europe | Short term (≤ 2 years) |

| Shift to food-grade flexible-pack adhesives | +0.9% | Asia-Pacific and North America | Medium term (2-4 years) |

| Cool-roof and reflective coatings demand | +0.6% | Hot-climate regions worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low-VOC Push for Water-Borne Paints and Coatings

California continues to cap VOC content for flat architectural paint at 50 g/L, compelling formulators to phase out solvent-rich chemistries. The United States Environmental Protection Agency extended aerosol coating compliance dates to January 2027, granting producers time to perfect water-based blends that match solvent-borne performance. Canada enforced VOC limits across 130 consumer product categories in January 2024, reinforcing a global regulatory shift that channels demand toward acrylic emulsions. Producers are therefore scaling self-crosslinking systems that raise film hardness without external crosslinkers, widening the addressable market. These policy moves give the acrylic emulsions market multi-year visibility and help offset monomer-cost swings.

Booming Construction Spending in Developing Countries

China’s 2025 budget maintains a 5% GDP growth target, supported by USD 1.11 trillion in infrastructure outlays, while India increased 2025–26 capital expenditure by 11.1% to INR 11.11 lakh crore. New highways, metros, and industrial parks lift consumption of architectural coatings, concrete additives, and flexible packaging adhesives that employ acrylic dispersions. Across Southeast Asia, manufacturing relocations drive factory construction, magnifying volumes. Because acrylic emulsions provide durability, adhesion, and low odor, they remain the binder of choice for builders that must meet tightening environmental standards. Rising middle-class income levels also spur residential repaint cycles, keeping baseline demand resilient.

Digital Ink-Jet Printing Inks Adoption

Label converters and folding-carton printers are migrating from analog to digital presses to run shorter jobs and enable customized packaging. Acrylic emulsions supply the resin backbone in water-based ink-jet formulations that demand rapid film formation, high color density, and strong substrate bonding. BASF’s new water-based dispersion line in Heerenveen, the Netherlands, targets this requirement and expands supply for European converters[1]Chemical Engineering Editors, “BASF Expands Water-Based Polymer Capacity in the Netherlands,” chemicalengineering.com. Printers benefit from odor-free operation and lower fire-code compliance costs, accelerating substitution away from solvent inks. The trend diversifies sales beyond traditional paint channels and cushions producers against cyclical construction swings.

Shift to Food-Grade Flexible-Pack Adhesives

Regulators are scrutinizing adhesives that contact food, leading packagers to phase out PFAS-containing chemistries in favor of safer acrylic systems. Studies show water-borne all-acrylic latexes can produce high-peel lamination bonds without fluorinated surfactants. Global snack and ready-meal brands now demand adhesive suppliers certify compliance with FDA and EU food-contact rules, enabling acrylic emulsions to secure premium pricing. As flexible packaging displaces rigid containers, the volume upside compounds, reinforcing long-term growth for the acrylic emulsions market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Preference for polyurethane dispersions | -0.8% | Global, strongest in industrial coatings | Medium term (2-4 years) |

| Acrylic monomer price volatility | -1.1% | Global, acute in cost-sensitive uses | Short term (≤ 2 years) |

| UV yellowing of styrene-rich emulsions | -0.4% | Global, mainly exterior façade coatings | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Preference for Polyurethane Dispersions

Water-borne polyurethane dispersions often outclass acrylics in chemical and abrasion resistance, allowing them to gain ground in automotive trim, wood flooring, and heavy-duty metal coatings. Recent research on 2K UV-curable polyurethane chemistries highlights breakthroughs in low-emission performance. While acrylics answer with hybrid designs and self-crosslinking networks, the gap in very high-stress environments remains, capping share growth in select premium niches. Yet acrylics retain cost and process advantages in the mid-performance tier, ensuring balanced competition rather than outright displacement.

Acrylic Monomer Price Volatility

Global methacrylic acid and butyl acrylate prices swung widely in 2024–25 as oversupply in Asia met soft downstream demand. Spot declines of 12% in early 2025 provided temporary relief but also created inventory risks when prices rebounded. Producers cope by adopting formula-based contracts and hedging feedstock through vertical integration. BASF’s move to bio-based ethyl acrylate starting Q4 2024 moderates carbon footprints and introduces supply diversity, yet buyers still monitor crude-linked propylene costs that influence acrylic acid economics. Persistent volatility encourages formulators to optimize recipes for cost flexing, potentially delaying new-grade adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Styrene-Acrylic Dominance Faces Vinyl Challenge

Styrene-acrylic grades held 44.78% of global revenue in 2025. Their balanced hardness, water resistance, and price position them as the workhorse for interior architectural paint and paper saturation lines. Through 2031, styrene-acrylic volumes will climb steadily, but the segment’s share will edge downward as users diversify into vinyl-rich systems. Vinyl-acrylic emulsions are set to grow 6.14% annually, riding demand for flexible construction adhesives, sealants, and low-temperature coated boards. Pure acrylics command the premium tier, favored in high-gloss exterior walls and cool-roof elastomeric where colour retention and UV durability are paramount.

Advanced self-crosslinking technologies reinforce this hierarchy. Studies show DAAM-ADH networks in styrene-acrylic road sealants boost bond strength by more than 50% over conventional grades. Producers market modular platforms that let customers fine-tune Tg and hardness with minimal lab reformulation, saving time to market. Meanwhile, vinyl-acrylic suppliers stress plasticizer-free flexibility that withstands thermal cycling in laminate flooring and weather-barrier membranes. Pure acrylics leverage bio-based monomer options to target sustainability-conscious architects, widening the value gap versus lower-priced chemistries.

By Application: Paints Maturity Contrasts Adhesives Growth

Paints and coatings consumed 58.02% of worldwide volume in 2025, reflecting decades of entrenched usage in architectural walls, roof membranes, and industrial primers. Regulatory tailwinds assure a steady replacement cycle as solvent systems exit. Nonetheless, the mature nature of repaint demand restrains segment CAGR, compelling suppliers to differentiate on washability, scrub resistance, and tint retention. Adhesives constitute the most vibrant outlet, expanding 6.03% per year as flexible packaging overtakes rigid formats and as modular construction needs high-performance laminating and flooring glues.

Paper coating users adopt water-borne barrier layers to eliminate PFAS. Research on silicone-modified acrylic lattices shows promise for grease-proof wraps, illustrating the segment’s technology cross-fertilization. Construction additives, though smaller in absolute terms, gain relevance as concrete modifiers that cut shrinkage and raise freeze-thaw endurance. Textile and non-woven finishes capitalize on soft-hand emulsions that impart anti-pilling and flame-retardant attributes without harsh solvents. Collectively, these applications diversify revenue streams and buffer the acrylic emulsions market against cyclical downturns in any single end use.

Geography Analysis

Asia-Pacific contributed 46.05% of global revenue in 2025 and will post a 5.98% CAGR to 2031. China’s Verbund site expansions supply local binders for booming public-works paint consumption, while India’s elevated capex pipeline translates directly into fresh commercial and residential floor space. ASEAN members such as Vietnam and Indonesia host export-oriented furniture and packaging clusters that rely on water-borne coatings to meet OECD buyer standards. The region also houses world-scale feedstock plants, enabling integrated players to balance cost pressure and drive economies of scale.

North America remains a regulatory trendsetter. The EPA’s revised aerosol rules and CARB’s low-VOC caps force continuous R&D investment, yet they simultaneously defend incumbents with proven compliance credentials. Infrastructure renewal under the U.S. Infrastructure Investment and Jobs Act pumps spending into bridges, transit hubs, and public buildings, all of which favor durable, low-odor coatings. Canada’s country-wide VOC regulations, effective 2024, harmonize requirements and simplify cross-border product portfolios. Mexico’s maquiladora network attracts appliance and automotive manufacturers that specify water-borne finishes to secure export approvals.

Europe emphasizes sustainability leadership. BASF’s shift to bio-based ethyl acrylate and the Dutch dispersion expansion illustrate the region’s drive to decarbonize the chemicals value chain. Germany supports cool-roof retrofits through building-efficiency subsidies, widening the market for reflective acrylic membranes. France and the United Kingdom promote circular-economy criteria in public procurement, favoring resins with life-cycle-assessment backing. Although South America and the Middle-East and Africa together represent less than 10% of global consumption, rising urbanization and increased access to mortgage financing encourage residential repainting and infrastructure projects, providing long-run upside.

Competitive Landscape

The acrylic emulsions market is moderately fragmented. BASF, Dow, Arkema, and Synthomer anchor global supply with integrated monomer production, broad technology platforms, and multi-continent manufacturing footprints. These leaders funnel double-digit R&D budgets into self-crosslinking lattices, PFAS-free dispersions, and bio-mass-balance resins that carry certified carbon-footprint reductions. Second-tier specialists such as Lubrizol and Synthomer carve revenue from niche segments like graphic-arts binders, pressure-sensitive adhesives, and non-woven hygiene finishes.

Strategic moves center on capacity expansions in growth regions. Lubrizol is investing USD 20 million to boost North Carolina output, shortening lead times to U.S. converters and coating blenders. BASF commissioned a new water-borne dispersion train in the Netherlands in 2024 to serve European packaging and ink-jet customers. Mergers complement organic growth: Synthomer finalized the USD 226 million acquisition of Hexion’s performance adhesives business, adding North American acrylic expertise and targeting USD 12 million in annual cost synergies.

Sustainability acts as the primary differentiation lever. BASF now offers more than 60 acrylic grades under its biomass-balance or renewable-raw-material schemes, claiming up to 30% lower cradle-to-gate carbon footprints. Dow markets EVOQUE pre-composite polymer technology that lifts titanium dioxide hiding efficiency, letting paint makers cut TiO₂ levels and save cost and embodied carbon. Intellectual-property filings in low-temperature crosslinkers and nanoclay-reinforced barrier coatings underscore the innovation tempo, erecting patent fences that raise entry barriers for new contenders.

Acrylic Emulsions Industry Leaders

BASF SE

Dow

Arkema Group

Synthomer plc

Celanese Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Celanese Corporation's partnership with Cloverdale Paint enables the use of captured CO₂ in the production of vinyl acetate-based emulsions. This initiative reduces emissions by over 1 million pounds annually through the manufacturing of architectural paints, contributing to the acrylic emulsions market.

- April 2024: Lubrizol invested USD 20 million to upgrade its acrylic emulsion production line at its Gastonia, North Carolina plant. The upgrade enhanced reactor flexibility and downstream filtration capabilities to support the production of new acrylic emulsions.

Global Acrylic Emulsions Market Report Scope

Acrylic resin emulsions are usually prepared by polymerizing various acrylic monomers in water, usually in the presence of an emulsifier or a dispersing agent. Acrylic emulsions are used to produce paints and coatings to improve the impact of the viscosity of substrates, surface effectiveness, and resistance. The acrylic emulsions market is segmented by type, application, and geography. By type, the market is segmented into pure acrylic emulsions, styrene acrylic emulsions, and vinyl acrylic emulsions. The report also covers the size and forecasts for the acrylic emulsions market in 17 countries across major regions. The market sizing and forecast for each segment are based on value (USD million).

| Pure Acrylic Emulsion |

| Styrene-Acrylic Emulsion |

| Vinyl-Acrylic Emulsion |

| Paints and Coatings |

| Construction Material Additives |

| Paper Coating |

| Adhesives |

| Other Applications (Textile and Non-woven Finishes, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Pure Acrylic Emulsion | |

| Styrene-Acrylic Emulsion | ||

| Vinyl-Acrylic Emulsion | ||

| By Application | Paints and Coatings | |

| Construction Material Additives | ||

| Paper Coating | ||

| Adhesives | ||

| Other Applications (Textile and Non-woven Finishes, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

Why are water-borne acrylics gaining share in architectural paint?

Low-VOC regulations in the United States, Canada, and Europe limit solvent content, pushing paint makers toward water-based acrylic binders that comply without sacrificing film durability.

What is the fastest-growing application for the acrylic emulsions market through 2031?

Adhesives lead growth at a projected 6.03% CAGR, fueled by flexible packaging demand and stricter food-contact requirements that favor acrylic chemistry.

Which region contributes the most to global consumption?

Asia-Pacific holds 46.05% of 2025 revenue and is expected to post a 5.98% CAGR as China and India expand infrastructure and manufacturing capacity.

How will digital printing affect acrylic emulsion demand?

Ink-jet printers rely on water-based acrylic inks for rapid curing and high color density, creating a diversified growth avenue beyond traditional paint and coating markets.

What role does sustainability play in competitive strategy?

Leading suppliers differentiate through bio-based monomers, PFAS-free grades, and carbon-reduction certifications, enabling premium pricing and long-term customer contracts.

Page last updated on: