Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 30.99 Billion |

| Market Size (2031) | USD 42.21 Billion |

| Growth Rate (2026 - 2031) | 6.38% CAGR |

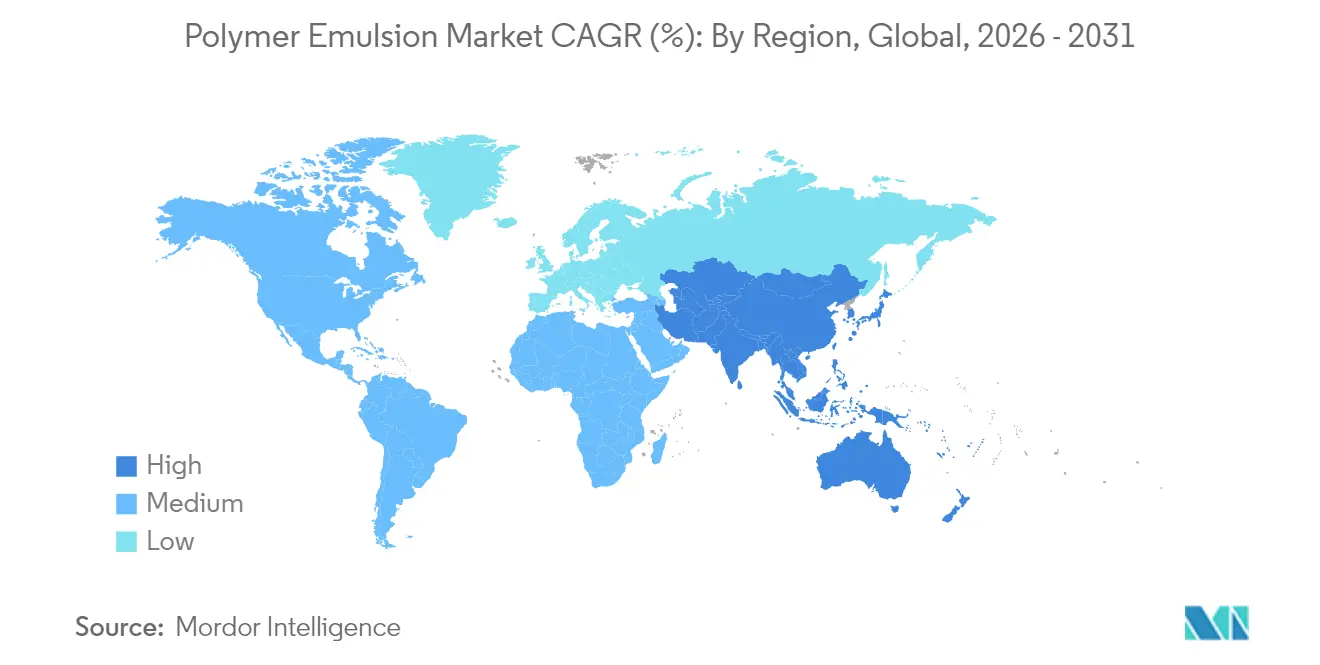

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polymer Emulsions Market Analysis by Mordor Intelligence

The Polymer Emulsions Market size is expected to grow from USD 29.13 billion in 2025 to USD 30.99 billion in 2026 and is forecast to reach USD 42.21 billion by 2031 at 6.38% CAGR over 2026-2031. Growth is led by tightening global air-quality rules that speed the replacement of solvent technologies with water-based systems, especially in architectural paints and industrial finishes. Accelerated adoption is also supported by recent breakthroughs in surfactant-free photoinitiated emulsion polymerization that reduce processing energy and improve colloidal stability pubs.rsc.org. Regulatory bans on solvent adhesives in Europe, together with parallel low-VOC mandates in North America and Asia, are pushing packaging, automotive, and construction value chains toward sustainable chemistries. Suppliers are responding with bio-based monomers, renewable-energy-powered plants, and digitally guided formulation platforms that compress time-to-market for new grades.

Key Report Takeaways

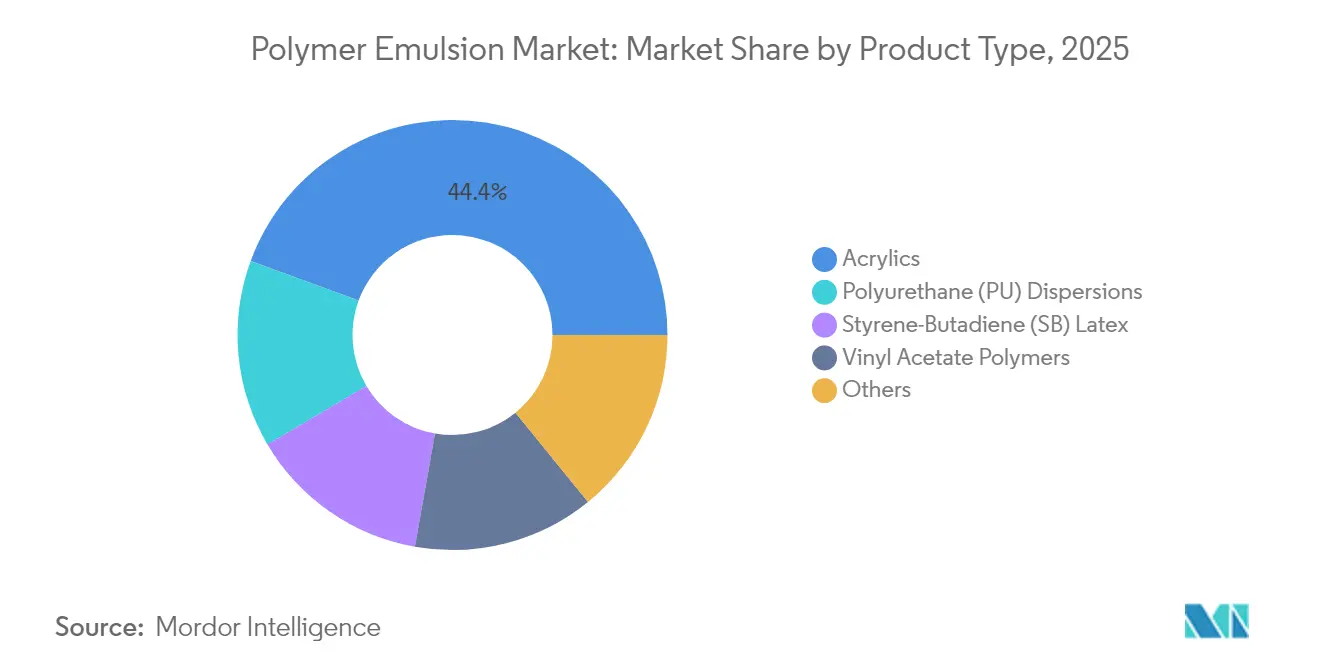

- By product type, acrylics led with 44.40% revenue share in 2025, while polyurethane dispersions are forecast to expand at a 6.78% CAGR through 2031.

- By application, paints and coatings accounted for 45.70% share of the polymer emulsions market size in 2025; adhesives and carpet backing are advancing at a 6.95% CAGR.

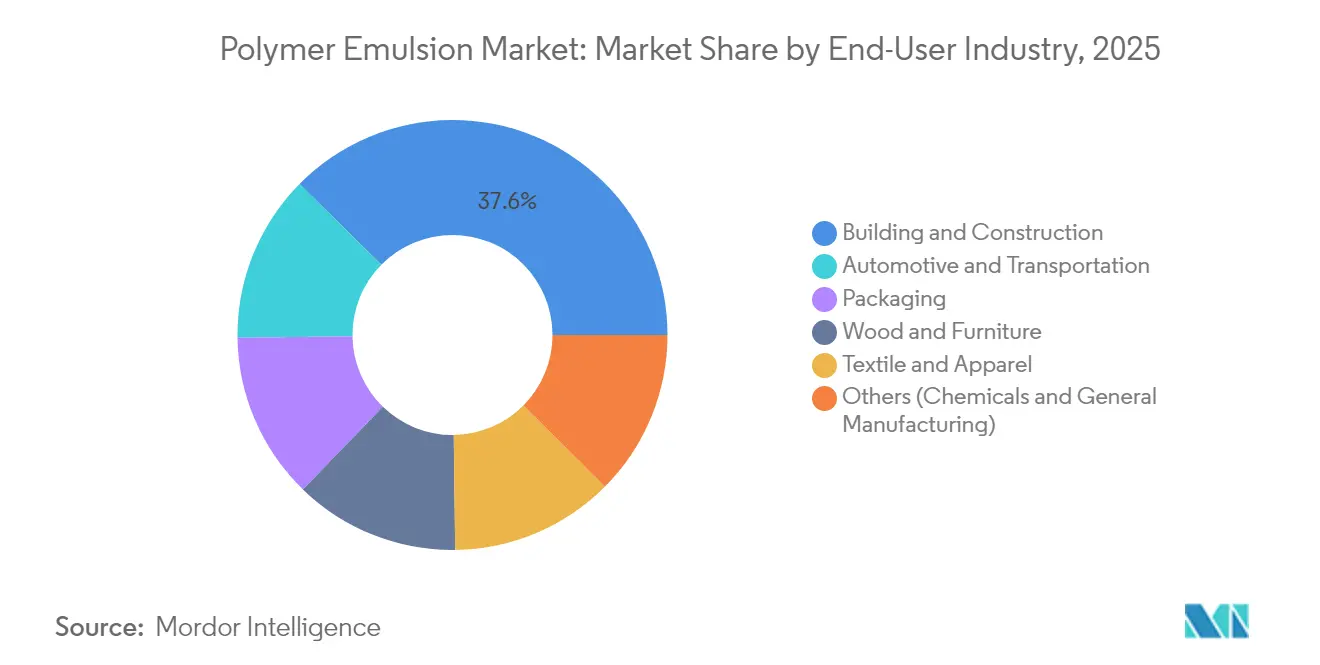

- By end-user industry, building and construction held 37.60% of polymer emulsions market share in 2025, whereas automotive and transportation is growing fastest at 7.29% CAGR.

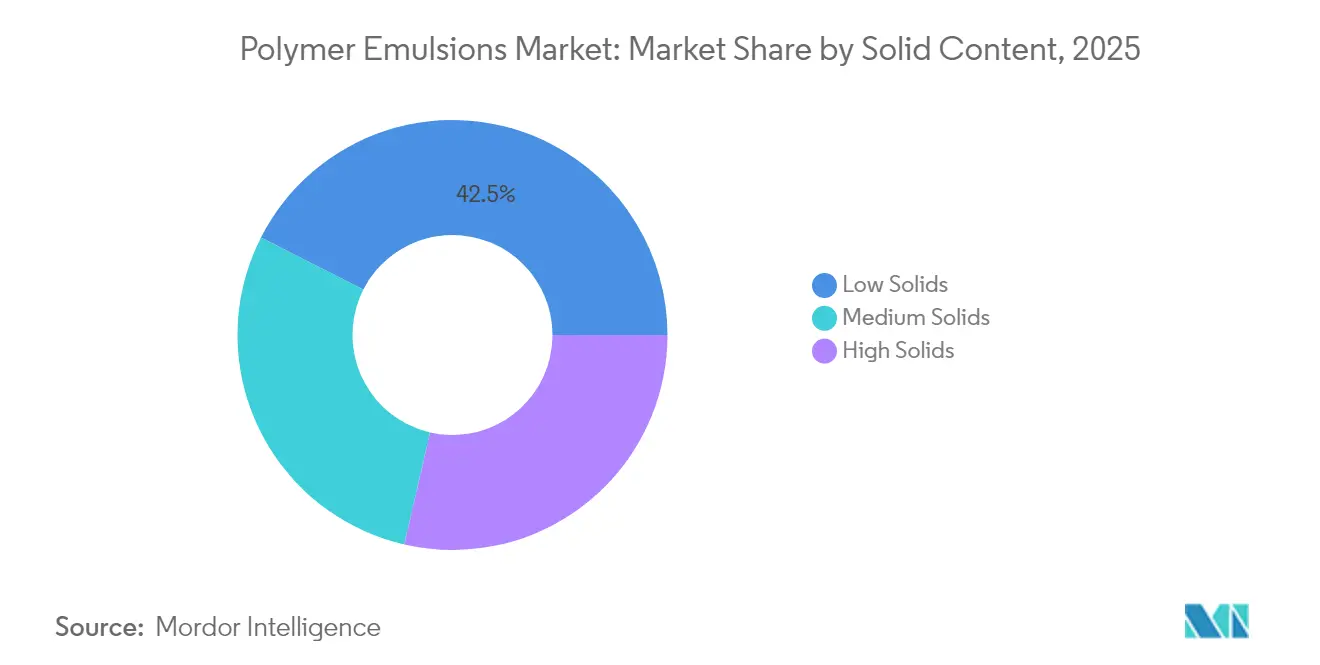

- By solid content, low-solids grades captured 42.50% share in 2025; medium-solids formulations are slated to post a 7.26% CAGR.

- By geography, Asia-Pacific commanded 40.85% of revenue in 2025 and is pacing regional growth at 7.11% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polymer Emulsions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Market | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Low-VOC Water-borne Coatings Fueled by Asia's Construction Boom | +1.80% | Asia-Pacific, with spillover to North America and Europe | Medium term (2-4 years) |

| OEM Automotive Demand for Eco-Friendly Scratch-Resistant Finishes in North America and Europe | +1.50% | North America and Europe, with emerging influence in Asia-Pacific | Medium term (2-4 years) |

| EU Bans on Solvent-Borne Adhesives Boosting Packaging Emulsion Uptake | +1.30% | Europe, with global supply chain implications | Short term (≤ 2 years) |

| Capacity Expansions of Acrylic Emulsion Plants in GCC Nations | +1.00% | Middle East, with export impact to Europe and Asia | Medium term (2-4 years) |

| Increased Textile and Paper Industry Usage | +0.90% | Global, with concentration in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Low-VOC Water-Borne Coatings Fueled by Asia’s Construction Boom

Asian megacities continue to add housing and infrastructure at record pace, raising demand for water-based exterior and interior paints that comply with strict emission targets. China’s latest air-quality plan and India’s updated National Building Code promote coatings below 50 g VOC l⁻¹, spurring rapid substitution of solvent alkyds. Manufacturers answer with acrylic latexes such as Lamberti’s ESACOTE AC 509 that pair corrosion resistance with low odor[1]Lamberti, “The Next Generation of Sustainable, High-Performance DTM Coatings,” surfacetreatment.lamberti.com. Health-and-safety benefits, easier cleanup, and fewer worker exposure limits reinforce preference for these systems, creating positive feedback that extends beyond pure compliance and cements long-term demand in the polymer emulsions market.

OEM Automotive Demand for Eco-Friendly Scratch-Resistant Finishes

Vehicle assemblers in North America and Europe now specify water-borne primer-surfacer and clear-coat packages that match solvent durability while cutting carbon footprints. Formulators employ hybrid polyurethane–acrylic matrices with self-cross-linking blocks to achieve hardness and mar resistance. Sun Chemical’s WATERSOL AC line illustrates this progress with coatings that deliver high gloss and low micro-scratch while eliminating up to 90% VOCs. With mainstream performance hurdles removed, brand-owners market sustainability credentials, accelerating volume growth across global auto plants.

EU Bans on Solvent-Borne Adhesives Boosting Packaging Emulsion Uptake

The European Green Deal restricts toluene- and xylene-based laminating adhesives, forcing converters toward acrylic emulsions and polyurethane dispersions. New water-borne grades reach bond strengths comparable to butyl hot-melts at lower coat-weights, lowering material cost and improving recyclability. Avery Dennison documents drop-in success for flexible food packs where cold-fill resistance and transparency are mandatory[2]Avery Dennison, “Using High Performance Emulsion Adhesives for Building and Construction,” performancepolymers.averydennison.com. Because packaging lines run high volumes, the change materially shifts global resin demand and provides reference installations that de-risk adoption in other sectors.

Increased Textile and Paper Industry Usage

Functional barrier coatings for paperboard replace fluorine-based treatments with water-borne styrene-acrylate emulsions that resist grease and vapor. Simultaneously, textile mills adopt biodegradable polyurethane dispersions showcased by Covestro at Techtextil 2025. Improved stretch recovery, color fastness, and breathable membranes open new revenue channels, particularly in sportswear and single-use food service articles. The twin push from two large process industries secures a long-run demand floor.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Market | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Butadiene and Acrylate Monomer Pricing | -1.20% | Global, with pronounced effect in Asia-Pacific | Short term (≤ 2 years) |

| Performance Gap vs. Solvent-borne Coatings in Heavy-Duty Uses | -0.80% | North America and Europe | Medium term (2-4 years) |

| VAM Supply Disruptions in Europe | -0.60% | Europe, with ripple effects in global supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Butadiene and Acrylate Monomer Pricing

Rapid feedstock swings compress latex producer margins, especially for styrene-butadiene grades tied to fluctuating naphtha costs. Contract formulas rarely adjust faster than quarterly, exposing suppliers during spikes. Firms diversify procurement and explore sugar-based acrylics to stabilize input budgets, but near-term volatility continues to weigh on profitability and may delay capital upgrades.

Performance Gap versus Solvent-Borne Coatings in Heavy-Duty Uses

Water-borne chemistries still trail solvent epoxies in chemical immersion, high-heat, and ultra-fast cure shop primers. Croda addresses the gap with reactive surfactants that build internal crosslinks and raise barrier properties[3]Croda Industrial Specialties, “Sustainable Solutions for Coatings,” crodaindustrialspecialties.com. Progress is measurable, yet end-users in marine, oil-and-gas, and food-processing segments adopt conservatively, limiting total addressable volume until next-generation polymers prove lifecycle parity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Acrylic Leadership Continues amid Polyurethane Momentum

Acrylic resins controlled 44.40% of 2025 volume and generated USD 12.93 billion in 2025. The segment benefits from broad compatibility, solid weatherability, and rapid regulatory approvals, cementing its role as the default platform across decorative paints, sealants, and pressure-sensitive labels. Celanese’s EcoVAE grades combine low odor with Class A scrub resistance, satisfying green-building schemes. Styrene-butadiene latex remains a cost-efficient choice for paper coating and carpet backing, though growth is modest as recycled fiber quality improves. Vinyl acetate polymers sustain steady demand in plaster and putty compounds where flexibility is essential. The “Others” cluster, including silicone-modified and bio-derived emulsions, expands selectively in high-margin niches such as medical films. Polyurethane dispersions, however, advance fastest at 6.78% CAGR, fueled by premium automotive, flexible packaging, and specialty floor-finish applications where toughness, clarity, and hydrolysis resistance justify higher prices. Collectively, product diversification anchors resilience in the polymer emulsions market.

The push for lower embodied carbon spurs investment in surfactant-free photoinitiated processes that tame foaming and cut VOCs. Laboratory work shows stable lattices at 55% solid without traditional soap systems, which can simplify compliance and effluent treatment. Suppliers integrating these methods stand to capture early-mover premiums. As bio-acrylic and sugar-route butadiene scale, life-cycle impact scores should fall further, aligning with scope-3 targets of major downstream brands and reinforcing the sustainability narrative driving the polymer emulsions industry.

By Application: Regulations Redefine Usage Patterns

Paints and coatings consumed 45.70% of 2025 demand, equal to USD 13.31 billion in 2025. Stringent VOC caps encourage conversion of decorative, protective, and automotive systems to water-borne platforms. Lamberti’s direct-to-metal acrylic, which matches solvent corrosion protection at 120 µm dry film, exemplifies how performance parity unlocks heavy-duty adoption. Adhesives and carpet backing record the fastest 6.95% CAGR as flexible packaging and construction tapes phase out solvent acrylics. Water-borne pressure-sensitives now withstand freezer storage and UV exposure, broadening their function set.

Paper and paperboard remain steady but are undergoing qualitative change. Water-based barriers incorporating vinyl ester of Versatic acid improve moisture and oil resistance, allowing substitution of polyethylene-extruded cups and trays with single-material structures. Textile, leather, and emerging 3-D printing binders fill the diverse “Others” bucket. Across segments, digital color-matching and inline viscosity control systems reduce batch variability, further normalizing water-borne use and lifting the polymer emulsions market trajectory.

By End-User Industry: Construction Dominates while Automotive Accelerates

The building and construction sector represented 37.60% of revenue in 2025, equal to USD 10.95 billion. Demand scales with megaprojects in Asia, retrofit programs in Europe, and stimulus-supported housing in North America. Latex polymers improve water resistance and crack bridging in cementitious mortars, with recent studies confirming enhanced compressive strength under chloride-sulfate exposure. Automotive and transportation register a 7.29% CAGR as original equipment manufacturers commit to water-borne clear-coats that satisfy Class-A appearance and 10-year corrosion warranties. Packaging, wood, and furniture sustain dependable volumes, each benefiting from low-odor indoor finishes that support brand sustainability claims. Chemical processing and general manufacturing round out diverse specialist uses and adopt emulsions when curing energy, odor control, or food-contact compliance matter. Collectively, evolving end-use profiles underpin robust demand across the polymer emulsions market.

By Solid Content: Performance–Regulation Balance Evolves

Formulations below 45% solid captured 42.50% of the 2025 volume, thanks to easier pumpability and wide familiarity among formulators. Medium solids (45-55%) grades record the highest 7.26% CAGR, striking the sweet spot between finish hardness, reduced drying time, and regulatory compliance. Producers employ reactive surfactants and chain-transfer agents to maintain stability at these higher solids. High-solid emulsions above 55% hold specialty positions in radiation-curable wood coatings and fast-dry OEM metal primers, where every gram of water removed slashes oven energy. Continuous technical progress nudges overall solids higher, reducing transportation emissions and supporting downstream scope 3 objectives, thereby reinforcing the long-term competitiveness of the polymer emulsions market.

Geography Analysis

Asia-Pacific commanded 40.85% of revenue in 2025, equivalent to USD 11.90 billion, and is projected to grow at 7.11% CAGR through 2031. Building booms in China, India, Indonesia, and Vietnam consume vast volumes of architectural latex, while regional automakers apply scratch-resistant water-borne topcoats. Capacity additions by multinational suppliers in China and emerging hubs such as Vietnam shorten lead times and shield buyers from freight swings. Japan and South Korea concentrate on high-performance niches—optical films, conductive coatings, and eco-friendly leather finishes—where domestic research and development depth secures premium pricing.

North America sits as the second-largest region. The United States drives water-borne adoption in remodeling, infrastructure, and EV manufacturing. Demand for low odor and rapid-dry formulations pushes suppliers to roll out next-generation acrylic-PU hybrids. Canada maintains healthy consumption in wood finishes and packaging grades. Mexico’s fast-expanding appliance and automotive assembly plants lift local demand, aided by near-shoring trends that draw coatings supply chains southward.

Europe remains a pivotal market shaped by the EU’s aggressive solvent-reduction mandates. Germany, France, the United Kingdom, and Italy implement national green-building codes that accelerate switch-overs in decorative paints and industrial maintenance products. The bloc’s ban on solvent-borne laminating adhesives propels swift uptake of water-borne chemistries in flexible packaging lines. Meanwhile, feedstock constraints from periodic VAM outages underscore supply-security concerns, pushing converters to qualifying dual sourcing in Eastern Europe and the Middle East.

South America and the Middle East and Africa hold smaller shares yet exhibit notable momentum. Brazil benefits from infrastructure and housing programs that expand latex mortar use. The Middle East leverages feedstock advantage; new acrylic emulsion plants in Saudi Arabia and the UAE export to Europe and Asia, altering trade flows. South Africa anchors African consumption with government-backed road and housing projects that call for durable low-VOC coatings. Across these emerging regions, governments increasingly reference the World Health Organization indoor air guidelines, aligning local regulations with global norms and ensuring sustained demand for the polymer emulsions market.

Competitive Landscape

Market structure remains moderately consolidated. Global majors─BASF, Dow, Arkema, DIC CORPORATION, and Synthomer plc─compete with regional specialists for share across acrylic, vinyl acetate, styrene-butadiene, and polyurethane families. Competitive intensity is rising as customers prioritize cradle-to-gate carbon footprints alongside cost and performance. Producers invest in bio-acrylic routes, mass-balance certifications, and recycled wastewater loops to differentiate sustainability credentials.

Strategic moves align with this agenda. Arkema champions open innovation partnerships around bio-sourced monomers and recyclable latex packaging, raising its profile at European and US coatings forums. Lubrizol committed USD 20 million to expand polyurethane dispersion capacity and support premium packaging clients seeking hot-stamp holographic performance without solvent odor. BASF pilots AI-driven formulation platforms that model polymer microstructure, shortening development cycles for low-carbon grades. Startups exploit white space, targeting niche bio-latex and high-solid photopolymer markets that incumbents address slower.

Digitalization gains importance across the polymer emulsions market. Inline near-infrared sensors optimize particle-size distribution, lowering off-grade rates, while blockchain tools document renewable content for downstream auditors. Midsize players adopt licensed process packages to leapfrog older reactors. The convergence of green chemistry and smart manufacturing tightens the competitive race and benefits buyers through broader choice and faster customization.

Polymer Emulsions Industry Leaders

BASF

Dow

Arkema

DIC CORPORATION

Synthomer plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Lamberti has introduced ESACOTE AC 509, a water-based acrylic emulsion designed specifically for direct-to-metal (DTM) applications. This innovative binder offers exceptional adhesion and corrosion resistance, making it ideal for industrial and metal coating formulations.

- April 2024: Lubrizol has announced a USD 20 million investment to enhance its acrylic emulsion manufacturing capabilities at its Gastonia, North Carolina facility. This strategic expansion aims to increase production capacity and improve operational efficiency to meet the growing demand for high-performance coatings.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the polymer emulsions market as the total value of water-borne dispersions produced through emulsion polymerization, encompassing acrylics, styrene-butadiene latex, vinyl-acetate polymers, polyurethane dispersions, and similar chemistries that are sold in liquid form to coatings, adhesives, paper, and other downstream formulators.

Scope exclusion: dry powders, solvent-borne resins, and redispersible latexes are outside the frame.

Segmentation Overview

- By Product Type

- Acrylics

- Styrene-Butadiene (SB) Latex

- Vinyl Acetate Polymers

- PVA Homopolymer

- Other Vinyl Acetates

- Polyurethane (PU) Dispersions

- Others

- By Application

- Paints and Coatings

- Adhesives and Carpet Backing

- Paper and Paperboard

- Others

- By End-User Industry

- Building and Construction

- Automotive and Transportation

- Packaging

- Wood and Furniture

- Textile and Apparel

- Others (Chemicals and General Manufacturing)

- By Solid Content

- High Solids (more than 55 %)

- Medium Solids (45-55 %)

- Low Solids (less than 45 %)

- Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed raw-material suppliers, binder formulators, paint makers, adhesive converters, and paper coaters across Asia-Pacific, Europe, North America, and the Middle East. These discussions clarified average selling prices, solids levels, and likely substitution trends, thereby closing gaps that desk work alone could not bridge.

Desk Research

We began with government and multilateral datasets such as UN Comtrade shipment codes for styrene-butadiene and acrylic lattices, the U.S. EPA and European Chemicals Agency VOC directives, China's Ministry of Ecology & Environment coating standards, and construction output data from the World Bank. Trade-association yearbooks from the American Coatings Association, World Paint & Coatings Industry Association, and Adhesive & Sealant Council supplied end-use demand clues. Company 10-Ks, investor decks, and news from Dow Jones Factiva added supplier-side revenue splits, while patent mining on Questel highlighted technology diffusion rates. This list is illustrative; a wider pool of open and paid sources was reviewed before numbers were locked.

Market-Sizing & Forecasting

We first sized regional demand through a top-down build that combines architectural paint output, adhesive production indices, global paper coating volumes, and average polymer solids to reconstruct latex consumption pools. We then converted tonnage to revenue using region-specific ASPs. Bottom-up cross-checks, supplier roll-ups, and channel checks tempered each total. Key variables include building permit growth, automotive OEM paint usage, VAM and butadiene cost curves, and tightening VOC thresholds. A multivariate regression model, stress-tested by scenario analysis, generates 2025-2030 forecasts; gaps where plant-level data were thin were smoothed with tested penetration coefficients.

Data Validation & Update Cycle

Outputs run through variance scans against historical ratios, peer benchmarks, and live trade data. Senior analysts review anomalies, and we re-contact sources when swings exceed preset bands. Reports refresh annually, with interim updates after big regulatory or capacity shocks, ensuring clients always access a freshly vetted baseline.

Why Mordor's Polymer Emulsions Baseline Earns Trust

Published estimates often diverge because firms adopt different product mixes, pricing ladders, and update rhythms.

Key gap drivers typically stem from whether vinyl-acetate redispersibles are folded in, how aggressively future ASP compression is modeled, the cadence at which construction indicators are refreshed, and the extent of primary validation.

Mordor's disciplined scope, yearly refresh, and dual-track validation keep our baseline balanced and decision-ready.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 29.13 B (2025) | Mordor Intelligence | - |

| USD 32.02 B (2023) | Global Consultancy A | Broader latex family included; minimal primary checks; older baseline |

| USD 30.96 B (2024) | Trade Journal B | Uses ex-factory prices only; currency conversions not harmonized |

| USD 28.80 B (2022) | Industry Association C | Excludes PU dispersions; applies fixed CAGR forward without scenario testing |

The comparison shows that figures swing when scope, price basis, or validation depth shifts. By anchoring values to transparent variables and refreshing them yearly, Mordor Intelligence provides a dependable starting point for planners and investors.

Key Questions Answered in the Report

What is the current size of the polymer emulsions market?

The polymer emulsions market size is USD 30.99 billion in 2026 and is forecast to reach USD 42.21 billion by 2031.

Which product type holds the largest market share?

Acrylic emulsions account for 44.40% of revenue in 2025, leading due to versatility and regulatory acceptance.

Which region is growing fastest?

Asia-Pacific is projected to expand at a 7.11% CAGR from 2026 to 2031, driven by construction and automotive demand.

What are the main growth drivers?

Tighter VOC rules, EU bans on solvent adhesives, capacity additions in the Middle East, and rising automotive demand for eco-friendly finishes together add more than 5% to the projected CAGR.

How are producers addressing raw-material volatility?

Strategies include bio-based monomer development, diversified sourcing, and vertical integration to stabilize margins against butadiene and acrylate price swings.

Page last updated on: