Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

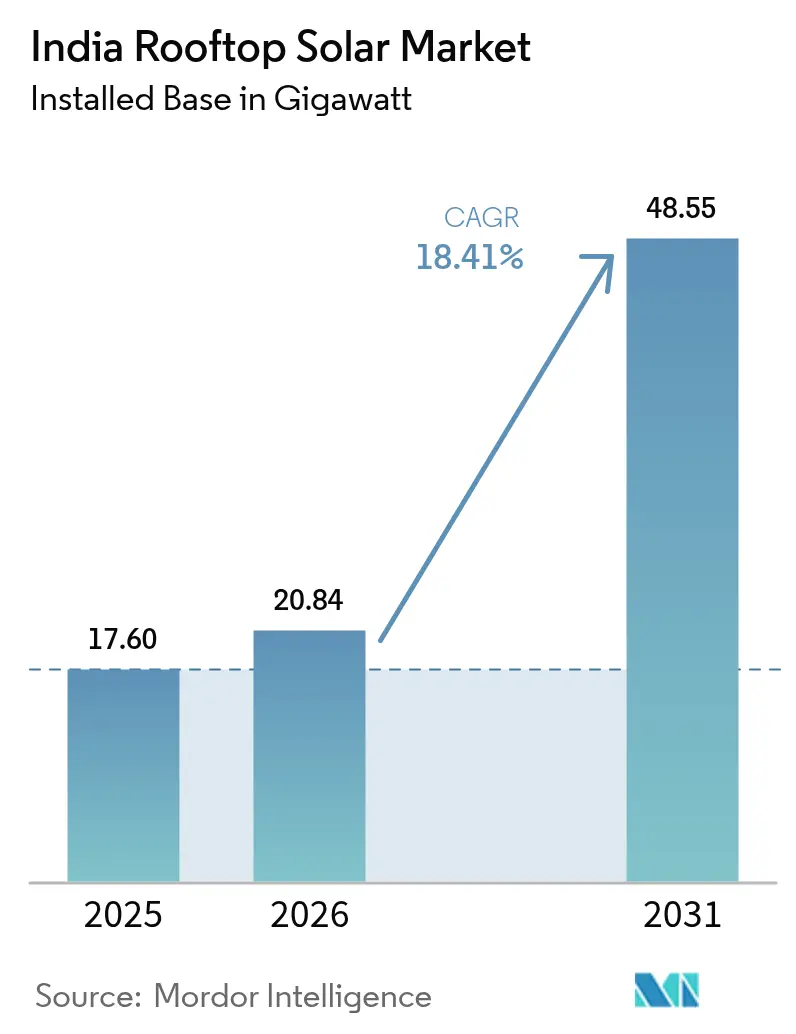

| Base Year Market Size (2025) | 17.60 gigawatt |

| Market Volume (2026) | 20.84 gigawatt |

| Market Volume (2031) | 48.55 gigawatt |

| Growth Rate (2026 - 2031) | 18.41% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Rooftop Solar Market Analysis by Mordor Intelligence

India Rooftop Solar Market size in 2026 is estimated at 20.84 gigawatt, growing from 2025 value of 17.60 gigawatt with 2031 projections showing 48.55 gigawatt, growing at 18.41% CAGR over 2026-2031.

India's renewable energy landscape has witnessed a remarkable transformation, driven by technological advancements and declining costs in the solar installation sector. According to the International Renewable Energy Agency (IRENA), the total average installed costs in the residential rooftop solar PV sector decreased by over 80% between 2010 and 2022, making solar installations increasingly accessible to various consumer segments. The integration of advanced technologies like smart inverters and monitoring systems has enhanced the efficiency and reliability of rooftop solar installations. The country's commitment to renewable energy is evident in its achievement of reaching 81.81 GW of total solar power system capacity as of March 2024, with grid-connected rooftop solar capacity accounting for 11.87 GW.

The market is experiencing a significant shift towards distributed generation, particularly in urban and semi-urban areas. Mumbai's climate action plan exemplifies this trend, identifying the potential for generating approximately 1.72 GW through rooftop solar power plants across commercial, industrial, and residential segments. The adoption of net metering policies across various states has created a more favorable environment for consumers, with states like Rajasthan raising the limit for net metering from 500 kW to 1 MW for rooftop solar installations in March 2024. These policy reforms have made rooftop solar installations more financially attractive for consumers while contributing to grid stability.

The integration of battery energy storage systems (BESS) with rooftop solar installations has emerged as a crucial trend, particularly in regions with unreliable grid power. The decreasing cost of batteries, which fell to USD 151 per kilowatt-hour in 2022, has made hybrid solar-plus-storage systems more economically viable. This integration enables consumers to maximize self-consumption of solar energy system power and maintain a reliable power supply during grid outages, addressing one of the key challenges in India's power sector.

The market is witnessing innovative financing models and implementation approaches, particularly in rural and semi-urban areas. Healthcare facilities have emerged as significant adopters of rooftop solar solutions, with successful implementations in government hospitals providing both environmental and economic benefits. The introduction of virtual net metering and peer-to-peer energy trading concepts has opened new possibilities for community solar projects and shared solar installations. For instance, in January 2024, Karnataka's draft plan to enable peer-to-peer trading of solar energy through blockchain technology represents a significant step towards modernizing the rooftop solar ecosystem and creating more flexible energy-sharing models.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Rooftop Solar Market Trends and Insights

Government Emphasis Toward Rooftop Solar Integration

The Indian government has demonstrated a strong commitment to rooftop solar integration through comprehensive policy frameworks and financial incentives. In February 2024, the government announced plans to increase the subsidy for rooftop solar installations to approximately 60% under the new Pradhan Mantri Suryoday Yojana. Additionally, the Ministry of New and Renewable Energy unveiled draft guidelines for the PM Surya Ghar: Muft Bijli Yojana initiative, aimed at facilitating rooftop solar installations in 10 million households with central government subsidy assistance. The program specifically targets households consuming up to 300 units of electricity per month, with implementation planned through March 31, 2027.

State governments have also introduced significant initiatives to promote residential solar adoption. For instance, in February 2024, the Uttar Pradesh government launched an ambitious program to install solar rooftop systems on 25,000 households in Varanasi within a two-month period. Similarly, in November 2023, the Haryana New and Renewable Energy Department introduced the 'Haryana Solar Power Policy, 2023,' which emphasizes various solar initiatives and targets the installation of 1,600 MW through rooftop solar installations by 2030. The government has also streamlined the installation process through the National Portal launched in September 2023, enabling residential consumers nationwide to apply for solar installation and receive subsidies directly in their bank accounts.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Demand in the Commercial & Industrial Sector

The commercial and industrial sector has emerged as a significant driver of India's rooftop solar market, with solar panels offering a levelized cost of power as low as INR 2-3 per kWh over their 25-year lifespan, compared to much higher grid tariffs of INR 7-9 for industrial power. This substantial cost difference has resulted in average payback periods of just over three years, making solar installation financially attractive for businesses. The sector's growth is further supported by recent technological advancements and innovative financing solutions, particularly for the MSME segment, where several rooftop solar financers have recently formulated MSME-focused lending plans allowing collateral-free loans.

Recent developments demonstrate the sector's growing adoption of commercial solar solutions. In March 2024, Gensol Engineering completed the installation of a 10.6-megawatt rooftop solar project at Trident Ltd's Budhni textile unit in Madhya Pradesh, featuring nearly 20,000 solar modules and offsetting approximately 11,000 tons of carbon dioxide emissions annually. The project ranks among the top five largest rooftop solar projects globally, covering a rooftop area exceeding 70,000 square meters. Additionally, emerging trends such as battery energy storage, virtual net-metering, and peer-to-peer energy trading are expected to boost electricity generation from solar rooftop power plants in the commercial & industrial sectors, with battery costs having decreased significantly from USD 1,220 per kilowatt hour in 2010 to USD 151 per kilowatt hour in 2022.

Segment Analysis

Industrial Segment in India Rooftop Solar Market

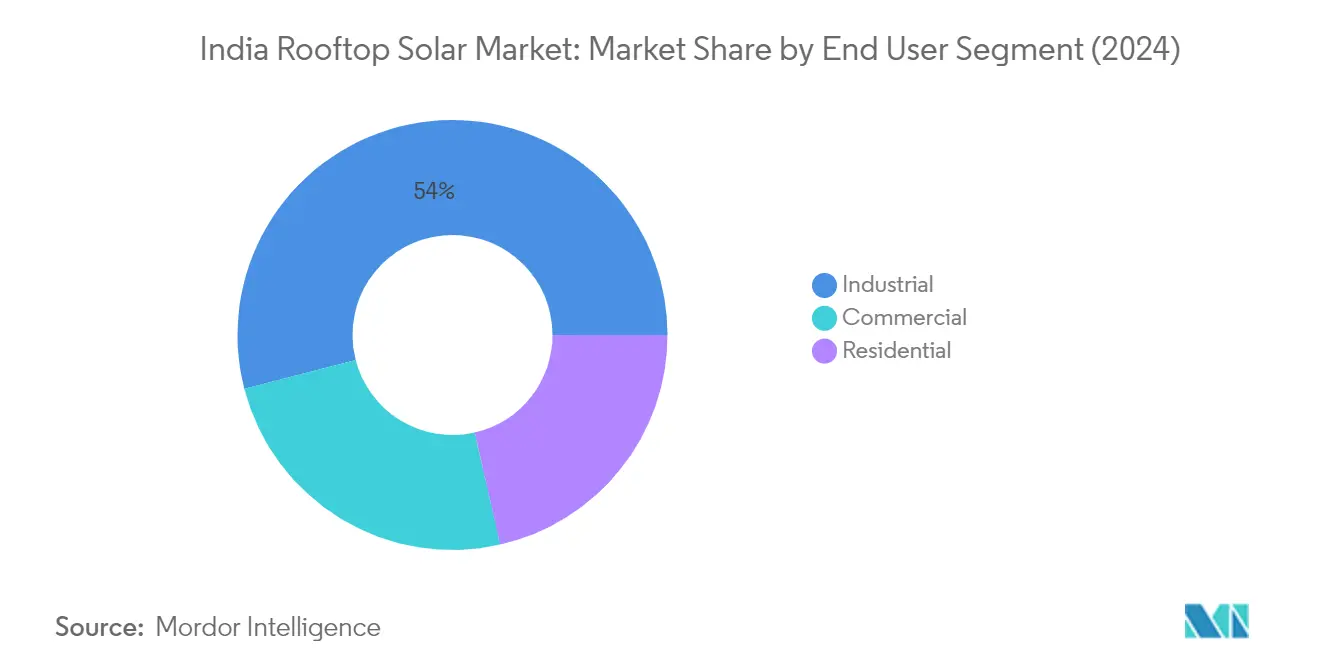

The industrial segment continues to dominate the India rooftop solar market, holding approximately 53.60% of the total market share in 2025, with an installed capacity of around 9,402 MW. This significant market position is primarily driven by the sector's high electricity consumption patterns and the increasing focus on reducing operational costs through renewable energy adoption. The segment's growth is further supported by various government initiatives and policies promoting solar installation in industrial sectors, particularly focusing on MSMEs (Micro, Small, & Medium Enterprises). Industrial consumers are increasingly adopting rooftop solar solutions due to the attractive cost economics, with solar panels offering a levelized cost of power as low as INR 2-3 per kWh over their 25-year lifespan, compared to the much higher grid tariffs of INR 7-9 for industrial power. The sector's dominance is also reinforced by the availability of larger roof spaces in industrial facilities, making them ideal for high-capacity solar array installations.

Residential Segment in India Rooftop Solar Market

The residential solar segment is emerging as the fastest-growing sector in the India rooftop solar market, projected to expand at a CAGR of approximately 22.26% during 2025-2031. This remarkable growth trajectory is primarily driven by increasing government support through initiatives like the Pradhan Mantri Suryoday Yojana, which offers substantial subsidies for residential solar installations. The segment's growth is further accelerated by rising electricity tariffs in residential sectors across various states, prompting homeowners to seek cost-effective alternatives. The implementation of simplified procedures for residential solar installations through the national portal, coupled with the availability of Central Financial Assistance (CFA) of around 40% for systems up to 3 kW and 20% for systems between 3-10 kW, has made solar adoption more accessible to residential consumers. Additionally, the increasing awareness about renewable energy benefits and the growing focus on energy independence among households are contributing to the segment's rapid expansion.

Commercial Segment in India Rooftop Solar Market

The commercial solar segment, including public sector installations, represents a significant portion of the India rooftop solar market, offering unique opportunities and growth potential. This segment benefits from the availability of large rooftop areas in commercial buildings such as malls, hospitals, educational institutions, and office complexes, making them suitable for medium to large-scale solar energy system installations. The segment's growth is supported by various state-specific incentives and net metering policies, particularly in states like Gujarat, Maharashtra, and Karnataka. Commercial establishments are increasingly adopting rooftop solar solutions to offset high commercial electricity tariffs and demonstrate their commitment to sustainability. The segment also benefits from innovative financing options and power purchase agreements (PPAs) that make solar adoption more feasible for commercial entities.

Segment Analysis: Grid Type

On-Grid Segment in India Rooftop Solar Market

The on-grid segment dominates the India rooftop solar market, holding approximately 80% market share in 2024, with an installed capacity of 11,869.63 MW. This significant market position is primarily driven by the government's Grid Connected Solar Rooftop Scheme and various supportive policies aimed at achieving 40,000 MW from grid-connected rooftop solar projects by March 2026. The segment's growth is further bolstered by the implementation of net metering policies across various states, with Maharashtra and Rajasthan recently increasing their net metering limits to enhance adoption. The Central Financial Assistance (CFA) scheme, offering substantial subsidies for residential installations, has also played a crucial role in driving the segment's expansion. Additionally, the launch of the National Portal in 2023 has streamlined the online process for consumers to install rooftop solar panels and receive subsidies directly in their bank accounts, making grid-connected systems more accessible and attractive to potential adopters. The segment is projected to grow at around 20% annually from 2024 to 2029, reflecting the strong market fundamentals and continued policy support.

Off-Grid Segment in India Rooftop Solar Market

The off-grid segment represents approximately 20% of the India rooftop solar market in 2024, serving as a crucial solution for areas with limited or no grid connectivity. This segment has gained significant traction through various government initiatives, including the Off-grid Solar Applications Programme run by the MNRE and private sector participation from companies like TATA Power. The segment's growth is particularly notable in rural electrification projects, healthcare facilities, and remote industrial applications. Recent programs like the Pradhan Mantri Janjati Adivasi Nyaya Maha Abhiyan (PM JANMAN) have allocated substantial funding for solar power implementation in tribal areas, demonstrating the government's commitment to off-grid solutions. The segment's development is also supported by technological advancements in battery storage systems and decreasing component costs, making off-grid solutions more economically viable for end-users. Furthermore, the implementation of schemes like PM KUSUM has created additional opportunities for off-grid installations in agricultural applications, contributing to the segment's steady expansion in the market.

Competitive Landscape

Top Companies in India Rooftop Solar Market

The Indian rooftop solar market is characterized by a mix of established players and emerging companies driving innovation and market expansion. Companies are increasingly focusing on developing integrated solar power systems that combine panel manufacturing, installation services, and financing options to provide end-to-end customer solutions. Strategic partnerships with banks and financial institutions have become a key trend to facilitate easier financing options for residential and commercial customers. Market players are also investing in research and development to improve solar module efficiency and develop smart monitoring systems. The industry has witnessed a shift towards offering customized solutions for different customer segments, with many companies establishing specialized divisions for residential, commercial, and industrial installations. Additionally, companies are expanding their geographical presence through dealer networks and strategic partnerships while also focusing on after-sales service and maintenance support to build long-term customer relationships.

Dynamic Market with Strong Growth Potential

The Indian rooftop solar market exhibits a balanced mix of both domestic and international players, with local companies having a strong presence in solar installation and maintenance services while global players dominate the solar power equipment manufacturing segment. The market structure is relatively fragmented with numerous regional players operating alongside established national companies, creating a competitive environment that drives innovation and price competitiveness. Recent years have witnessed significant merger and acquisition activities, particularly with international renewable energy companies acquiring stakes in Indian solar companies to establish their presence in the growing market. Private equity firms and international investors have shown increasing interest in the sector, leading to capital infusion and consolidation among smaller players.

The competitive landscape is evolving with the entry of traditional power companies diversifying into the solar sector, bringing their expertise in utility-scale projects to the rooftop segment. Companies are increasingly focusing on vertical integration, with many manufacturers expanding into project development and EPC services to capture higher margins and maintain better control over the value chain. The market has also seen the emergence of specialized players focusing on specific customer segments or geographical regions, creating niche markets within the broader industry. This specialization has led to improved service quality and more targeted solutions for different customer needs.

Innovation and Adaptation Drive Market Success

Success in the Indian rooftop solar market increasingly depends on companies' ability to offer innovative financing solutions and maintain technological leadership while managing costs effectively. Market leaders are strengthening their positions by developing proprietary technologies, establishing strong distribution networks, and building strategic partnerships with component suppliers and financial institutions. Companies are also focusing on digitalization, incorporating smart monitoring systems and predictive maintenance capabilities to enhance their service offerings. The ability to navigate complex regulatory environments across different states while maintaining compliance with quality standards has become crucial for sustained growth.

For new entrants and smaller players, success lies in identifying and serving underserved market segments, particularly in tier-2 and tier-3 cities where competition is less intense. Companies need to focus on building strong local relationships, offering specialized solutions for specific industries, and maintaining operational efficiency to compete effectively. The increasing focus on domestic manufacturing under government initiatives presents opportunities for companies to establish manufacturing capabilities and reduce dependence on imports. Additionally, developing expertise in emerging technologies like storage solutions and smart grid integration will be crucial for future growth. Companies must also prepare for potential regulatory changes, particularly around net metering policies and quality standards, while maintaining flexibility in their business models.

India Rooftop Solar Industry Leaders

Tata Power Solar Systems Limited

Amplus Solar Power Private Limited

Clean Max Enviro Energy Solutions Pvt. Ltd

Orb Energy Pvt. Ltd

Sunsource Energy Pvt. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: Apple announced forming a joint venture with renewable energy developer CleanMax to invest in six rooftop solar projects to power its operations in India. The solar project is expected to have a total capacity of 14.4 MW and, when operational, will provide a local solution to power the company’s offices and two retail stores in Mumbai and New Delhi.

- March 2024: GAIL (India) announced an invitation for bids regarding a rooftop solar project. This project is expected to involve designing, supplying, installing, testing, and commissioning a grid-tied rooftop solar PV (photovoltaic) system. Additionally, this initiative includes a comprehensive 5-year Annual Maintenance Contract (AMC) to supply electricity generated by the project to the Krishna Godavari Basin area.

India Rooftop Solar Market Report Scope

Rooftop solar PV is a photovoltaic system with electricity-generating solar panels mounted on the rooftop of a commercial or residential building. It captures the sun's energy and converts it into electrical energy.

The Indian rooftop solar market is segmented by end user and grid type. By end user, the market is segmented into commercial, industrial, and residential. By grid type, the market is segmented into on-grid and off-grid. For each segment, the market sizing and forecasts were made based on installed capacity.

End-user

| Industrial |

| Commercial (Including Public Sector) |

| Residential |

Grid Type (Qualitative Analysis Only)

| On-grid |

| Off-grid |

| End-user | Industrial |

| Commercial (Including Public Sector) | |

| Residential | |

| Grid Type (Qualitative Analysis Only) | On-grid |

| Off-grid |

Key Questions Answered in the Report

How big is the India Rooftop Solar Market?

The India Rooftop Solar Market size is expected to reach 20.84 gigawatt in 2026 and grow at a CAGR of 18.41% to reach 48.55 gigawatt by 2031.

What is the current India Rooftop Solar Market size?

In 2026, the India Rooftop Solar Market size is expected to reach 20.84 gigawatt.

Who are the key players in India Rooftop Solar Market?

Tata Power Solar Systems Limited, Amplus Solar Power Private Limited, Clean Max Enviro Energy Solutions Pvt. Ltd, Orb Energy Pvt. Ltd and Sunsource Energy Pvt. Ltd are the major companies operating in the India Rooftop Solar Market.

What years does this India Rooftop Solar Market cover, and what was the market size in 2025?

In 2025, the India Rooftop Solar Market size was estimated at 20.84 gigawatt. The report covers the India Rooftop Solar Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the India Rooftop Solar Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: