Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

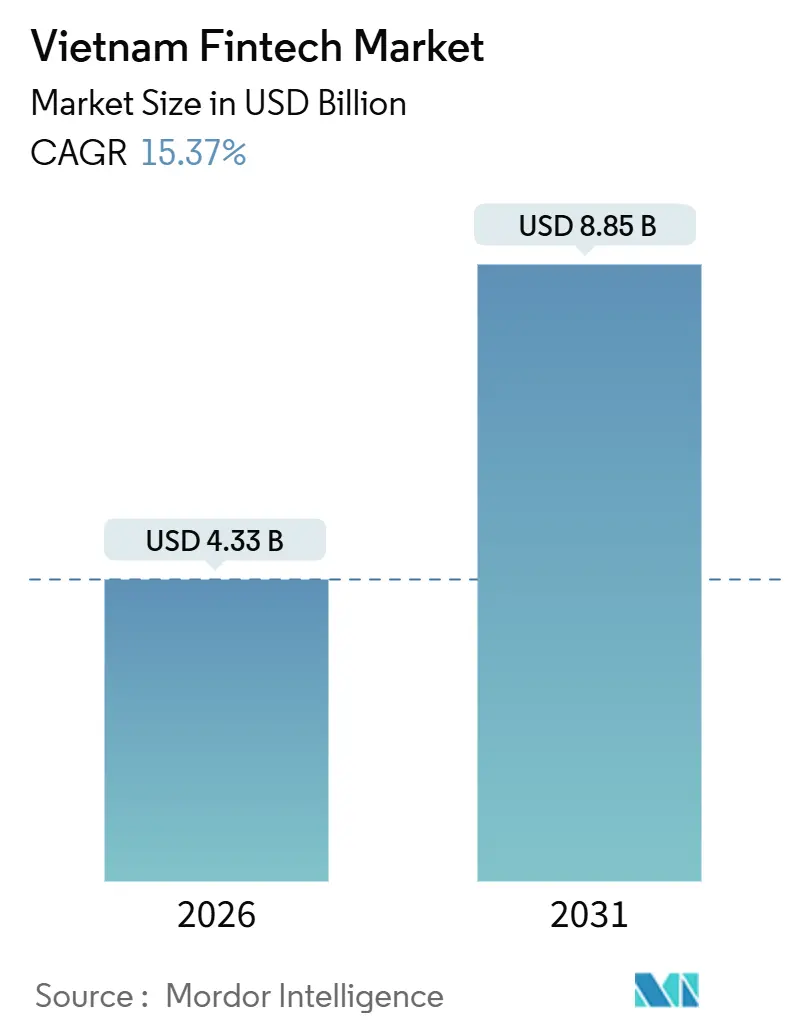

| Market Size (2026) | USD 4.33 Billion |

| Market Size (2031) | USD 8.85 Billion |

| Growth Rate (2026 - 2031) | 15.37% CAGR |

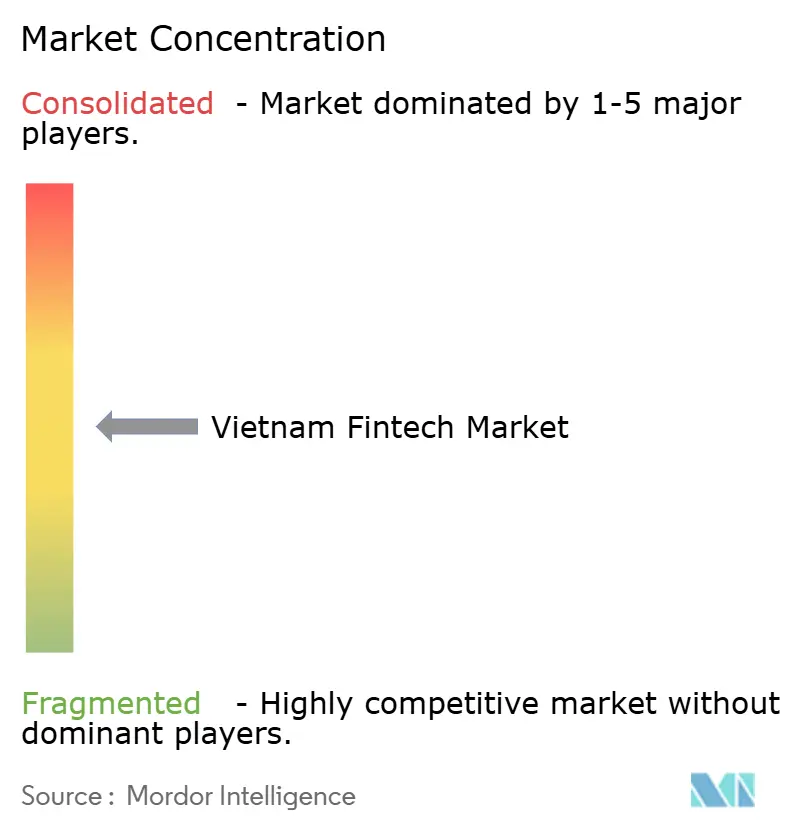

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Fintech Market Analysis by Mordor Intelligence

The Vietnam fintech market size is USD 4.33 billion in 2026 and is projected to reach USD 8.85 billion by 2031 at a 15.37% CAGR. This growth is fueled by a robust domestic digital payment ecosystem, which saw significant year-on-year expansion. Vietnam introduced a fintech sandbox, allowing innovative financial products to scale in a controlled environment. The shift toward cashless payments is evident, with 5.5 billion cashless transactions recorded in Q1 2025, facilitated by NAPAS 247's real-time QR infrastructure that lowers merchant acceptance costs and expands digital use cases. [1]International Monetary Fund, “The Impact of Central Bank Digital Currency on Payments Competition,” elibrary.imf.org. Expanding financial inclusion has also contributed to market growth, as more individuals gain access to bank accounts. Digital platforms and banks have further accelerated adoption by providing accessible and user-friendly fintech solutions. The market is strengthened by growing consumer trust in digital payments, supported by secure and well-regulated systems. Overall, Vietnam’s fintech landscape is poised for sustained growth, driven by technology adoption, regulatory support, and a broadening financial infrastructure.

Key Report Takeaways

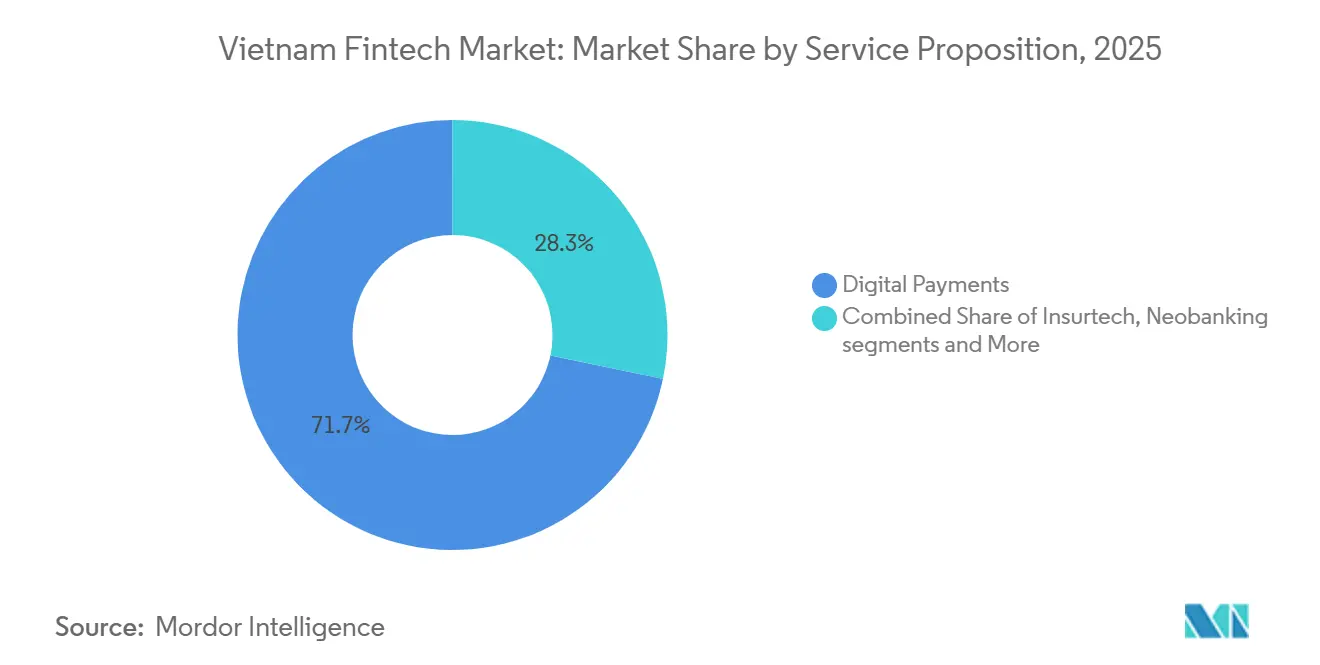

- By service proposition, digital payments held 71.73% of the Vietnam fintech market share in 2025, while insurtech is forecasted to expand at a 31.28% CAGR through 2031.

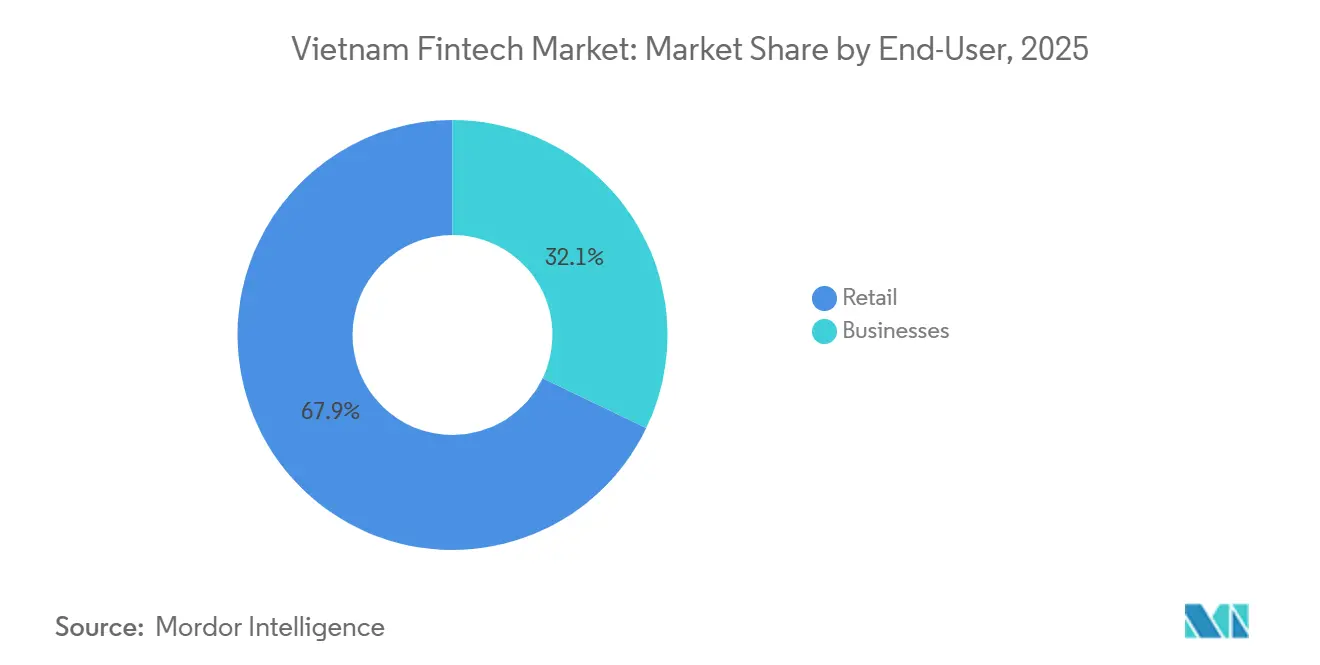

- By end-user, retail accounted for 67.88% of the Vietnam fintech market share in 2025, and business users are projected to record a 24.38% CAGR through 2031.

- By user interface, mobile applications captured 79.28% of the Vietnam fintech market share in 2025, while POS and IoT devices are set to grow at a 28.35% CAGR through 2031.

- By geography, Southern Vietnam accounted for 47.75% of the Vietnam fintech market share in 2025, while Central Vietnam is projected to grow at an 18.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Fintech Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High smartphone and internet penetration, enabling mass mobile-first fintech adoption | +2.8% | Global, particularly urban centres in Northern and Southern Vietnam | Short term (≤ 2 years) |

| The government's cashless roadmap and the National Digital Transformation Program are accelerating the digital payment infrastructure | +3.5% | National, with accelerated implementation in Ho Chi Minh City and Hanoi | Medium term (2-4 years) |

| Rising middle-class demand for convenient, low-cost financial services | +2.1% | National, concentrated in urban areas across all three regions | Long term (≥ 4 years) |

| Expansion of NAPAS 247 real-time QR rail, reducing merchant acceptance costs | +2.3% | National | Short term (≤ 2 years) |

| Regulatory sandbox for P2P lending and open banking, enabling innovation pilots | +1.6% | National, with sandbox zones in Ho Chi Minh City and Da Nang | Medium term (2-4 years) |

| Cross-border e-commerce remittance inflows are driving multi-currency wallet demand | +1.4% | Southern Vietnam hub, expanding to Northern provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Smartphone & Internet Penetration

Smartphone and internet penetration are a structural advantage for the Vietnam fintech market, with widespread connectivity enabling mobile-first service delivery across payments, lending, investments, and insurance. The Ministry of Information and Communications has driven household fiber and 4G coverage to high levels, which has reduced access friction for real-time transactions and account onboarding. National planning targets 5G availability at scale by 2030, which supports the next wave of low-latency fintech use cases like instant credit decisioning and dynamic QR payments. Platform growth shows the effect of this base, as leading wallets and bank apps scaled rapidly on the back of digital infrastructure and user readiness. As participation widens, hybrid models that blend digital channels with local agent support continue to expand reach in areas where digital literacy is still maturing, keeping the Vietnam fintech market inclusive while sustaining growth.

Government Cashless Roadmap & National Digital Transformation Program

The cashless roadmap and the National Digital Transformation Program have accelerated the Vietnam fintech market by pushing digital payments into the mainstream of commerce and public services. Fiscal and administrative measures, including requirements that link deductions and benefits to non-cash evidence, have created persistent incentives for businesses to digitize payment flows and record-keeping. National database integration prioritized by the government is improving the quality of identity, tax, and credit data that underpin digital onboarding, underwriting, and fraud control. Banks have reinforced these gains by rolling out biometric ID-based authentication at scale, which has improved security outcomes and reduced fraud exposure alongside compliance with new verification rules. As payroll, pensions, and subsidy distribution migrate to digital channels through local pilots, consumer switching costs rise, and platform lock-in strengthens, supporting durable adoption across the Vietnam fintech market.

Rising Middle-Class Demand for Convenient Financial Services

An expanding middle class is creating sustained demand for simple, convenient, and affordable financial services that are accessible on mobile devices across savings, credit, payments, and protection. Digital investment platforms that offer fractional investing and automated advisory features have grown their user bases by addressing entry barriers, including minimum balances and onboarding friction. Insurers and distributors are responding by embedding micro-insurance and on-the-go protection within everyday applications, which better fits customer preferences for convenience and transparency. Banks and wallets are also adopting personalization through AI-driven prompts and rewards that nudge users toward responsible credit and savings behavior, reinforcing engagement at low incremental cost. Together, these shifts strengthen retail-led monetization for the Vietnam fintech market, while opening new cross-sell opportunities as incomes rise and customer needs diversify.

Expansion of NAPAS 247 Real-Time QR Rail

The expansion of NAPAS 247 has been pivotal for the Vietnam fintech market, since interoperable QR and instant transfers reduce acceptance costs and increase merchant coverage across formal and informal retail. Rail interoperability allows any participating bank app or wallet to scan standardized codes, which removes silos in acceptance and supports broader use cases like delivery, on-demand transport, and utilities. Leading acquirers have gained share by coupling dynamic QR capabilities with merchant services, enhancing collections and reconciliation for e-commerce and logistics partners at scale. Faster and cheaper payments diminish the incremental benefits a retail CBDC might offer in the near term, since a public fast payment system is already delivering high-speed clearing and settlement nationwide. Network resilience remains a focus in more remote provinces, where connectivity limitations can slow confirmations, reinforcing the need for telco-fintech collaboration on service continuity for the Vietnam fintech market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low financial literacy and trust gaps outside Tier-1 cities are limiting product adoption | -1.9% | Rural areas nationwide, particularly the Northern highlands and the Mekong Delta | Long term (≥ 4 years) |

| Fragmented multi-agency KYC rules are increasing onboarding friction and compliance costs | -1.4% | National | Medium term (2-4 years) |

| Unsustainably high customer acquisition cost from cashback wars eroding unit economics | -1.2% | Urban centres in Southern and Northern Vietnam | Short term (≤ 2 years) |

| Limited cloud availability zones and latency issues are constraining real-time fraud detection | -0.9% | National, with an acute impact in Central and rural provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low Financial Literacy & Trust in Rural Areas

Over 70% of the population lives outside the largest cities, which means the Vietnam fintech market depends on outreach models that address gaps in confidence, awareness, and product understanding. [2]International Finance Corporation, “Digital Finance to Drive Viet Nam’s Economic Growth,” ifc.org. Government programs focused on financial inclusion and digital transformation continue to push acceptance infrastructure and e-services deeper into rural districts. Payment providers, banks, and agents are testing hybrid delivery that combines mobile onboarding with local assistance to bridge literacy constraints and build trust. Greater coverage of identity services, including chip-based IDs and biometric verification, is also reducing fraud risk and improving confidence in digital channels. A sustained focus on education, grievance redressal, and agent quality is likely to determine how quickly advanced products like investments and insurance scale beyond major urban corridors in the Vietnam fintech market.

Fragmented KYC Rules Across Ministries

KYC and data protection regulations are spread across multiple statutes and agencies, which complicates digital user onboarding and increases compliance costs for non-bank fintechs. Recent requirements for biometric verification of corporate representatives have prompted banks to implement both in-app and in-branch biometric options. Fintechs without banking licenses must rely on partnerships with licensed institutions to access credit data and identity services, creating third-party dependencies and potential revenue-sharing challenges. New frameworks in emerging financial centers are introducing sandbox pathways that could simplify rules for pilot participants, but this may result in inconsistent onboarding experiences across different regions until national standards are harmonized. Addressing this regulatory fragmentation is expected to shorten time-to-market for new products, reduce user drop-off during onboarding, and directly improve unit economics in the Vietnam fintech sector. [3]VietnamPlus, “Banks Accelerate Digitalisation, Non-cash Payments,” vietnamplus.vn.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Proposition: Payments Lead, Insurtech Accelerates

Digital payments held a commanding 71.73% share in 2025, while insurtech is forecast to be the fastest-growing service line at a 31.28% CAGR through 2031, underscoring the depth and breadth of the Vietnam fintech market. In parallel, the regulatory sandbox enables controlled pilots in P2P lending, credit scoring, and open APIs, which will support lending and data-led models as they transition from proof of concept to scaled deployment. Neobanking is advancing through bank-backed digital brands and partnerships with technology players that shorten the path from customer acquisition to product activation. Digital investments are expanding through fractional equity and automated saving tools, as platforms adapt to rising retail wealth and the need for low-barrier entry. Insurtech’s growth is leveraging embedded distribution and digital channels, which aligns with the policy environment that has supported greater foreign investment into the sector and modernization of distribution.

From a growth-composition perspective, the Vietnam fintech market is set to evolve as payments mature and other verticals accelerate from a smaller base. Digital payments are likely to sustain mid-teen rates as account ownership nears saturation, while new use cases in merchant acquiring and B2B payments keep activity healthy. Insurtech’s acceleration reflects a catch-up dynamic, as carriers pivot toward embedded models and consumer-grade digital experiences. Lending and financing are positioned to benefit from open-banking integration, improved credit data, and better verification, which together reduce default risk and increase addressable demand. These dynamics indicate a broader shift from a payments-led to a multi-product Vietnam fintech industry, which is likely to broaden revenue pools and diversify monetization.

By End-User: Retail Dominates, Business Surges

Retail accounted for 67.88% of value in 2025, reflecting the breadth of wallet usage, QR acceptance, and investment adoption among mass and mass-affluent consumers in the Vietnam fintech market. Business users are projected to expand at a 24.38% CAGR, as SMEs integrate embedded finance, supplier payments, collections, and working-capital solutions that improve cash conversion and reduce friction. Given that SMEs constitute the overwhelming majority of registered enterprises, the digitization of invoicing and merchant finance materially expands the serviceable opportunity. As APIs proliferate and enterprise systems connect with bank platforms, switching costs rise, and early movers consolidate share through account lock-in and workflow depth. Bank-fintech models that couple merchant services with short-term credit are gaining traction, underscoring the rising importance of B2B flows in the Vietnam fintech market.

Across the cycle, retail growth has been consumption-led, while business growth correlates with investment cycles and public-spending execution. Open banking standards are creating a cleaner environment for treasury connectivity, reconciliation, and embedded lending, which strengthens the business case for digitization. As more SMEs adopt ERP, e-commerce, and FinOps tools, data exhaust improves underwriting, which reduces collateral reliance and expands B2B credit access. These trends reinforce a gradual rebalancing from retail-only growth toward a more even split between consumer and enterprise flows in the Vietnam fintech market. The result is a broader and more resilient revenue base that is less sensitive to short-term changes in consumer spend.

By User Interface: Mobile Reigns, POS/IoT Devices Surge

Mobile applications captured 79.28% in 2025, reflecting a mobile-first adoption curve built on high smartphone use and low-friction onboarding among leading players in the Vietnam fintech market. POS and IoT devices show the highest growth at 28.35% CAGR, as soft POS has turned smartphones into contactless acceptance terminals for small merchants and service providers. Web and browser interfaces remain relevant for corporate banking, treasury dashboards, and higher-consideration advisory flows, where larger screens and controls are preferred. Platform integrations with transport and delivery services have pulled digital payments into daily mobility and food use cases across new provinces, broadening coverage outside metro cores. With mobile usage near saturation, further gains in the Vietnam fintech market are likely to come from deeper merchant acquiring in tier-2 and tier-3 cities through low-cost POS and IoT deployments.

Adoption patterns suggest mobile will continue to lead daily transacting, while POS and IoT fill acceptance gaps in long-tail retail and services. As banks and processors deploy tap-to-phone and QR solutions with unified reporting, the merchant value proposition strengthens through lower hardware costs and faster settlement. Enhanced API connectivity across channels and devices keeps user experiences consistent, which supports loyalty and higher frequency. This multi-interface progression helps the Vietnam fintech market move beyond core bill-pay and P2P into richer acquiring and B2B flows. Over time, cross-channel analytics and AI will add personalization that tightens engagement without raising variable cost.

Geography Analysis

Southern Vietnam accounted for 47.75% of activity in 2025, anchored by Ho Chi Minh City’s financial and commercial base and the emergence of its International Financial Centre framework. The region benefits from a dense ecosystem of banks, wallets, and merchant partners that continue to expand acceptance and embedded finance into retail and services. Ho Chi Minh City is targeting a USD 120 billion economy in 2025, with logistics and trade infrastructure that support payments and lending volume across supply chains. The concentration of financial services and technology talent has also enabled faster product testing and partnerships that feed the Vietnam fintech market. As digital-payments penetration increases, growth shifts from new-to-digital use cases to deeper monetization across merchant services and credit.

Northern Vietnam is an administrative and innovation center that aims to lift the digital economy’s contribution with policy support and ecosystem initiatives involving universities and research hubs. The region’s growth in manufacturing and services continues to draw investment, which sustains payment flows for payroll, procurement, and trade. Leading banks headquartered in Hanoi have deepened digital offerings but continue to operate hybrid models that combine branch strength with upgraded mobile and web platforms. Mobility platforms are expanding northward and bringing payments to new provinces, which extends acquiring and consumer finance to more districts. These shifts balance the Vietnam fintech market by adding regional diversity to growth drivers.

Central Vietnam is the fastest-growing region with an 18.87% projected CAGR, as Da Nang advances sandbox activity linked to green finance, blockchain, and cross-border flows under the International Financial Centre framework. The city is collaborating with international partners to build expertise and run controlled pilots, which support trade finance and tourism-related payments aligned with its logistics position. As infrastructure and regulatory pilots converge, Central Vietnam can attract new capital and specialized talent, while reinforcing nationwide initiatives on data and interoperability. Over the forecast horizon, the Vietnam fintech market should see a more balanced geographic contribution to growth as Central projects scale and Northern adoption deepens. This balancing makes the overall opportunity less dependent on one metropolitan region and more resilient to localized shocks.

Competitive Landscape

The Vietnam fintech market exhibits a moderately concentrated structure, with major players holding strong positions while competition remains active through bank-led digital brands and new foreign-backed entrants. Some digital wallets have achieved profitability by balancing scale, merchant reach, and disciplined spending, showing that network effects can offset acquisition costs as products mature. Other wallets leverage extensive social networks to enhance QR payment adoption, engagement, and user retention. Super-app ecosystems are integrating payments with commerce and mobility, increasing transaction frequency and creating opportunities for lending and insurance. Bank-backed neobanks are intensifying competition by combining deposit services with seamless digital experiences, reducing friction, and enabling cross-selling. Overall, the market demonstrates a dynamic balance between established leaders and innovative challengers, shaping the adoption of digital financial services.

Incumbent banks are investing heavily in data platforms, analytics, and cloud infrastructure to improve personalization, fraud detection, and operational efficiency. Generative AI is being deployed in customer service and lead allocation to accelerate response times and improve conversion, while biometric requirements enhance baseline security across the system. Partnerships between wallets and banks are expanding product offerings within super-apps, strengthening embedded finance through shared data and risk. New entrants are focusing on AI-driven credit solutions that shorten approval times and serve underbanked customers with limited or no credit history. The competitive emphasis is shifting toward quality underwriting, cross-sell potential, and operational efficiency rather than purely acquisition-driven strategies. In 2024, ZaloPay reinforced its position as a leading payment platform by expanding payment options, merchant networks, and QR solutions that support cross-platform and international use, while also adding financial services like savings, loans, and installment plans to deepen engagement. [4]VNG Corporation, “ZaloPay 2024: Hành Trình Mới và Mở,” vng.com.vn.

The International Financial Centre frameworks in Ho Chi Minh City and Da Nang are attracting global institutions with clear pilot mechanisms and incentives, increasing competitive intensity. Banks are extending their ecosystems into insurance and wealth management, creating additional cross-sell opportunities and strengthening customer relationships. Cross-border payment providers are partnering with domestic banks to localize operations, improving speed and reducing costs. As authentication and data standards converge, open-banking use cases are expected to expand, fostering collaboration between fintechs and banks. The emerging market playbook emphasizes regulatory alignment, technology leverage, and ecosystem partnerships as the primary sources of competitive advantage.

Vietnam Fintech Industry Leaders

M_Service (MoMo)

VNPay

ZaloPay (VNG)

ShopeePay

Grab Financial Group VN

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Flywire listed VIB and VPBank as sub-processors for payment and collection partner activities in Vietnam, signaling deeper integration between cross-border processors and domestic banks.

- December 2025: Circle Asia Technologies announced a collaboration with Pismo and Visa to launch Vietnam’s first AI-powered PayLater card with five-minute approval and virtual issuance from early 2026.

- September 2025: The National Assembly formalized the International Financial Centre in Ho Chi Minh City and Da Nang with sandbox mechanisms for fintech, digital assets, and green finance.

- September 2025: dtcpay signed an MoU with the People’s Committee of Da Nang to advance blockchain innovation, digital payments, and sandbox development.

Vietnam Fintech Market Report Scope

Fintech encompasses a range of technologies, including software and mobile applications, designed to enhance and automate conventional financial services for both businesses and consumers.

The Vietnamese fintech market report is segmented by service proposition, end-user, user interface, and geography. By service proposition, the market is segmented into digital payments, digital lending & financing, digital investments, insurtech, and neobanking. By end-user, the market is segmented into retail and businesses. By user interface, the market is segmented into mobile applications, web/browser, and POS/IoT devices. By geography, the market is segmented into Northern Vietnam, Central Vietnam, and Southern Vietnam. The report offers market size and forecasts for the fintech in the Vietnamese market in terms of value (USD) for all the above segments.

By Service Proposition

| Digital Payments |

| Digital Lending & Financing |

| Digital Investments |

| Insurtech |

| Neobanking |

By End-User

| Retail |

| Businesses |

By User Interface

| Mobile Applications |

| Web / Browser |

| POS / IoT Devices |

By Geography

| Northern Vietnam |

| Central Vietnam |

| Southern Vietnam |

| By Service Proposition | Digital Payments |

| Digital Lending & Financing | |

| Digital Investments | |

| Insurtech | |

| Neobanking | |

| By End-User | Retail |

| Businesses | |

| By User Interface | Mobile Applications |

| Web / Browser | |

| POS / IoT Devices | |

| By Geography | Northern Vietnam |

| Central Vietnam | |

| Southern Vietnam |

Key Questions Answered in the Report

What is the size and growth outlook for the Vietnam fintech market through 2031?

The Vietnam fintech market size is USD 4.33 billion in 2026 and is projected to reach USD 8.85 billion by 2031 at a 15.37% CAGR, reflecting robust adoption and supportive policy.

Which segments lead and which are growing fastest in Vietnam’s fintech?

Digital payments led with 71.73% share in 2025, while insurtech is the fastest-growing at a 31.28% CAGR through 2031 on embedded distribution and policy support.

How are regulations shaping competition and innovation in Vietnam fintech?

The SBV sandbox under Decree 94 supports pilots for P2P lending, credit scoring, and open APIs, while biometric KYC and data rules standardize security and data flows.

Which regions are most important for Vietnam’s fintech providers?

Southern Vietnam holds 47.75% of activity, Northern Vietnam is a policy and innovation hub, and Central Vietnam is the fastest-growing region with sandbox momentum.

What are the main restraints facing fintech providers in Vietnam today?

Key constraints include fragmented KYC rules, rural financial literacy gaps, cashback-driven acquisition costs, and limited cloud availability zones that raise latency.

Page last updated on: