Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

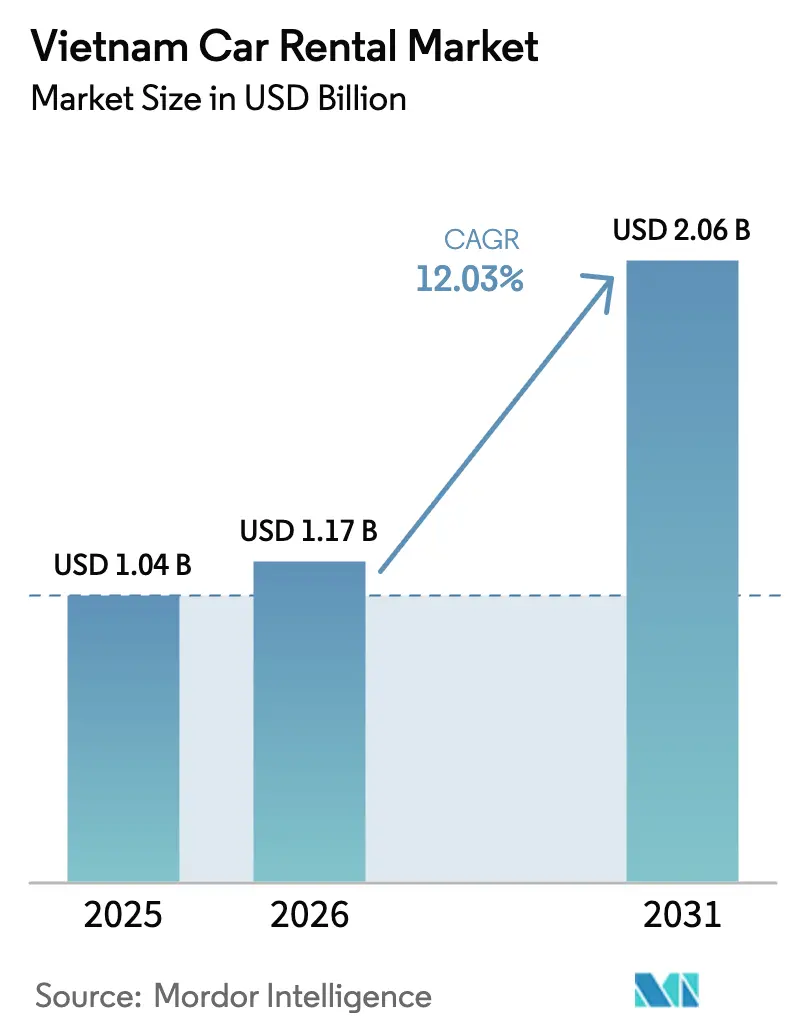

| Base Year Market Size (2025) | USD 1.04 Billion |

| Market Size (2026) | USD 1.17 Billion |

| Market Size (2031) | USD 2.06 Billion |

| Growth Rate (2026 - 2031) | 12.03% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Car Rental Market Analysis by Mordor Intelligence

The Vietnam Car Rental Market size is projected to be USD 1.04 billion in 2025, USD 1.17 billion in 2026, and reach USD 2.06 billion by 2031, growing at a CAGR of 12.03% from 2026 to 2031. In recent years, international tourist arrivals have shown significant recovery, supported by a growing middle-class disposable income reaching notable levels. At the same time, policy measures have accelerated the adoption of battery-electric vehicles (BEVs), reshaping the dynamics of rental demand. App-based platforms have effectively leveraged widespread mobile payment adoption, capturing bookings that traditionally went to walk-in counters. Operators are increasingly leveraging BEV cost efficiency to align with premium leisure pricing. This shift is further supported by substantial foreign direct investment (FDI) inflows, creating a rapidly expanding corporate leasing opportunity. The competitive landscape is transitioning from a focus on fleet size to prioritizing digital reach, data-driven dynamic pricing, and integrated multi-service ecosystems.

Key Report Takeaways

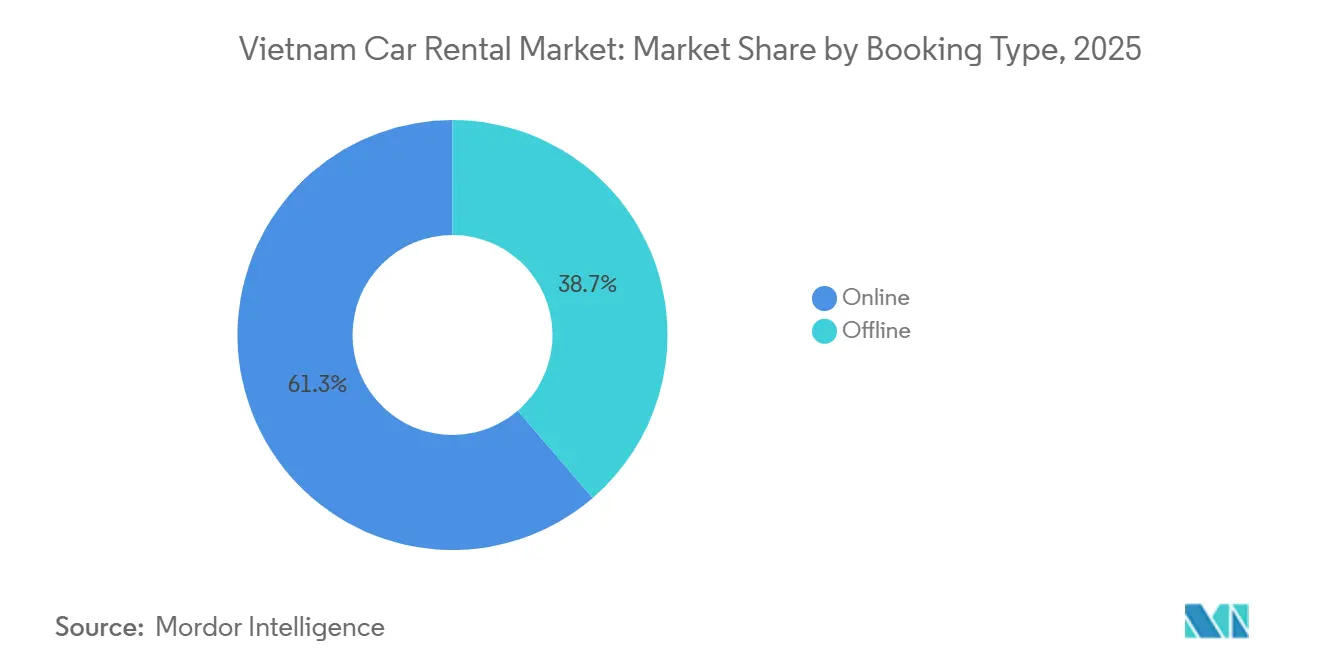

- By booking type, online channels accounted for 61.32% of the Vietnam car rental market share in 2025 and are forecast to grow at a 12.07% CAGR through 2031.

- By rental duration, short-term contracts accounted for 63.48% of the Vietnam car rental market in 2025, while long-term corporate agreements are projected to expand at a 12.16% CAGR during 2026-2031.

- By application, tourism and leisure accounted for 73.18% of revenue share in 2025; corporate and expat mobility is advancing at a 12.19% CAGR through 2031.

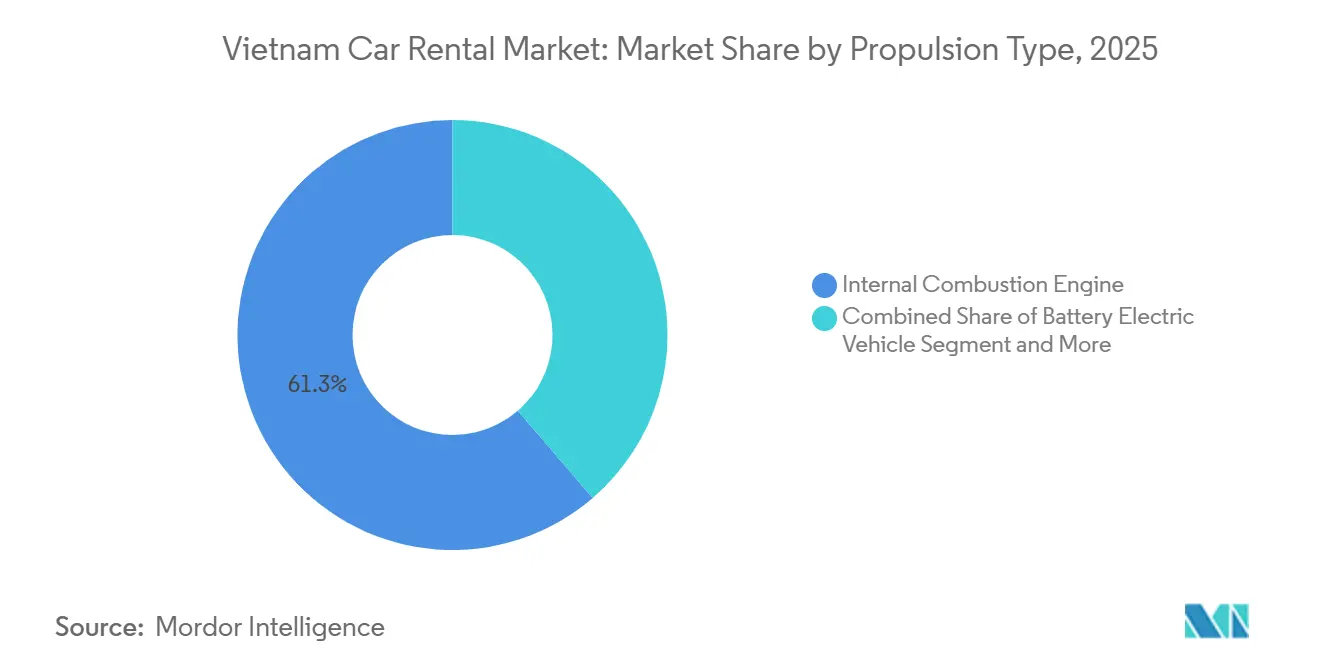

- By propulsion, ICEs accounted for 61.27% of the market in 2025; battery-electric vehicles are forecast to outpace internal-combustion models with a 12.09% CAGR from 2026 to 2031.

- By end user, individuals accounted for 68.73% of the 2025 value, yet corporate customers are projected to grow at a 12.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Car Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tourism Rebound Drives Leisure Rentals | +2.1% | National, with peaks in Hanoi, Da Nang, Nha Trang, HCMC | Short term (≤ 2 years) |

| Rising Disposable Incomes Among Middle Class | +1.8% | National, strongest in urban Hanoi and HCMC | Medium term (2-4 years) |

| Shift Toward App-Based and Online Bookings | +1.5% | National, led by Hanoi and HCMC, spreading to Tier-2 cities | Short term (≤ 2 years) |

| Electrification Push Via Green-and-Smart Mobility | +1.3% | Hanoi and HCMC core, gradual rollout to Da Nang, Can Tho | Long term (≥ 4 years) |

| Corporate Fleet Outsourcing Post-IFRS 16 | +1.0% | Hanoi, HCMC, Binh Duong, Dong Nai industrial zones | Medium term (2-4 years) |

| Government Smart-Mobility Sandbox Projects | +0.7% | Hanoi (ITS pilot), HCMC (smart parking), Da Nang (EV zones) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tourism Rebound Drives Leisure Rentals

Vietnam hosted 21.2 million international visitors in 2025, up 20.4% year on year, and visa-free policies for 25 countries fostered 3- to 7-day multi-province itineraries [1]“International Visitor Arrivals 2025,” Vietnam National Administration of Tourism, vnat.gov.vn . Korean and Indian travelers, together accounting for more than 6.9 million arrivals, increasingly rented self-drive SUVs to reach emerging destinations such as Phong Nha caves and the Central Highlands coffee belt. The Long Thanh International Airport, opening partially in late 2026, will add 25 million annual seats near Ho Chi Minh City, widening leisure catchments. Seasonality remains pronounced: Lunar New Year and the June-to-August peaks account for 60% of annual leisure revenue, prompting operators to flex capacity through peer-to-peer tie-ups.

Rising Disposable Incomes Among Middle Class

GDP growth of 8.02% in 2025 lifted per-capita income to USD 5,026, creating a 45-million-strong middle class that now values experiential road travel over asset ownership [2]“Socio-Economic Situation 2025,” General Statistics Office, gso.gov.vn . Weekend trips to Da Lat and Sa Pa surged, with app data showing 38% of domestic bookings from users aged 25-35. Car prices averaging USD 25,000-40,000—equal to 5-8 years of median earnings—keep ownership aspirational, positioning rentals as both trial and status substitute. Friday evening to Monday morning pick-ups doubled across 2024-2025, affirming rentals as a hedge against high depreciation.

Shift Toward App-Based and Online Bookings

Digital Payment use reached three-fourths of urban transactions in 2025, enabling apps to secure 61.32% of bookings [3]“Cashless Payment Report 2025,” State Bank of Vietnam, sbv.gov.vn . Grab inserted a car-rental module in Q2 2025, monetizing idle taxis and underpricing traditional fleets by up to 20% on leisure routes. Domestic aggregator Thuexe.vn logged 1.2 million downloads and credits 70% of growth to instant confirmations within two hours. Regulatory Circular 12/2025 obliges operators to display live rates and insurance terms, leveling transparency and accelerating migration from walk-ins.

Electrification Push Via Green-Mobility Mandates

Decision 876 aims for a significant share of electric vehicles (EVs) in new vehicle sales by 2030, mandating full electrification for buses and taxis by the same deadline. In recent years, VinFast has delivered a substantial number of EVs and established a large network of charging ports, primarily concentrated in Hanoi and Ho Chi Minh City, helping to address urban range anxiety. Green & Smart Mobility has introduced a notable fleet of EVs and proprietary chargers, while also securing battery-swap agreements with Hyundai and BYD, significantly reducing downtime. With electricity priced competitively, the energy cost per kilometer is considerably lower than gasoline, narrowing the total cost of ownership gap within a few years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dominance of Low-Cost Ride-Hailing and Motorbikes | -1.4% | National, most acute in Hanoi and HCMC | Short term (≤ 2 years) |

| High Vehicle Import Tariffs and Registration Fees | -1.1% | National | Medium term (2-4 years) |

| Urban Congestion and Limited Parking | -0.9% | Hanoi, HCMC, Da Nang | Short term (≤ 2 years) |

| Sparse EV-Charging Network Outside Tier-1 Cities | -0.6% | Secondary cities: Can Tho, Hai Phong, Hue, Nha Trang | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Dominance of Low-Cost Ride-Hailing and Motorbikes

Grab dominates the ride-hailing scene with a commanding market share, enticing customers with affordable short-distance trips. This pricing strategy allows Grab to significantly undercut hourly rentals. In Vietnam, where motorbikes are a prevalent mode of transportation, their low operating costs solidify their status as a cost-effective and nimble choice for daily transportation.

High Vehicle Import Tariffs and Registration Fees

Operators face a significant increase in the landed cost of completely built-up cars due to high tariffs and an additional consumption tax. To achieve profitability within a reasonable timeframe, they need to maintain high fleet utilization, which drives a preference for tax-advantaged VinFast models, despite concerns over residual-value depreciation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Booking Type: Digital Channels Reshape Access

Online platforms accounted for 61.32% of 2025 revenue, growing at a 12.07% CAGR, as the Vietnam car rental market tilts toward transparent pricing and instant confirmation. Airports and hotels still rely heavily on offline counters, especially for face-to-face services catering to older tourists and contract clients. Grab's peer-to-peer model capitalizes on idle taxis, offering discounted rates for weekend leisure. Meanwhile, regulatory requirements mandate real-time price disclosures, giving app ecosystems an edge.

Online bookings in Vietnam's car rental market are expected to grow significantly in the coming years. In contrast, offline channels are expected to grow more slowly. This shift is largely influenced by the widespread adoption of mobile payments. Younger users show the strongest loyalty to platforms. Additionally, aggregator apps have set a new standard with guaranteed quick urban vehicle handovers, a feat that offline competitors find challenging to replicate.

By Rental Duration: Short-Term Dominance Masks Corporate Shift

Short-term bookings accounted for 63.48% of volume and will continue to expand at a 12.16% CAGR as visa-free tourists drive 3-to-7-day multi-province trips. Long-term rentals, however, are gaining relevance as corporate buyers exploit IFRS 16 to avoid capital lock-up.

Short-term bookings generate most of the annual revenue during peak holiday windows, forcing operators to over-fleet or partner with peer-to-peer platforms to smooth utilization. Long-term contracts deliver 2.3 times higher lifetime value per vehicle and are expected to add USD 200 million to the Vietnam car rental market by 2031, contingent on managed-fleet capabilities.

By Application Type: Tourism Leads, Corporate Accelerates

Tourism and leisure produced 73.18% of the 2025 turnover on the back of 21.2 million international arrivals. Corporate and expatriate mobility, growing at a 12.19% CAGR, benefits from manufacturing FDI around Hanoi and Ho Chi Minh City that requires predictable fleet availability.

Leisure demand emphasizes SUVs and dynamic pricing, while corporate clients negotiate all-inclusive monthly packages covering insurance, maintenance, and driver training. Daily commuting remains marginal as Grab and motorbikes offer cheaper, quicker intra-city trips, though congestion-pricing could shift the calculus for future decisions.

By Vehicle Propulsion: ICE Incumbency Meets BEV Momentum

Internal-combustion engines accounted for 61.27% of fleet value in 2025, yet BEVs are slated to grow fastest at a 12.09% CAGR following Decision 876 incentives. By the end of the forecast period, hybrid vehicles, caught in a strategic bind without full tax relief and facing high entry prices, might yield ground to purely electric models or more efficient internal combustion engine (ICE) variants.

As electricity prices remain significantly lower than gasoline costs and VinFast broadens its network, the market for battery electric vehicles (BEVs) in Vietnam's car rental sector is expected to experience substantial growth. Yet, operators are limiting the BEV fleet's share to a small proportion until pricing in the secondary market stabilizes, especially given that older BEVs are currently fetching noticeably lower values than their ICE counterparts.

By End-User: Individual Leisure Versus Corporate Contracts

Individuals accounted for 68.73% of the 2025 value, driven by aspirational weekend road trips and social media culture. Corporate users will expand steadily at a 12.11% CAGR, driven by managed fleets displacing ownership, especially among FDI manufacturers.

Daily rate hikes significantly impact individual bookings due to their elastic demand. In contrast, corporate contracts benefit from budget protection and tax deductibility. If fleet management adoption among domestic conglomerates aligns with regional standards, corporate leasing's share in Vietnam's car rental market could grow substantially in the coming years.

Geography Analysis

In 2025, Southern Vietnam led the charge in tourism demand, with Ho Chi Minh City accounting for a significant share of international arrivals at Tan Son Nhat Airport. While the Mekong Delta and Vung Tau see spikes in weekend leisure traffic, the provinces of Binh Duong and Dong Nai, known for their industrial base, are becoming hotspots for long-term corporate leasing. However, with limited peak speeds and high hourly parking fees, the allure of self-driving within the city diminishes. This scenario has paved the way for Grab to dominate short-distance commutes. Looking ahead, the partial inauguration of Long Thanh Airport is set to redistribute tourist traffic. This shift will likely extend average rental durations towards regional heritage sites, reducing the need for returns through Ho Chi Minh City.

Northern Vietnam strikes a balance between business and heritage tourism. While Ha Long Bay and Sa Pa stretch the average rental duration, government contractors in Hanoi lean towards long-term packages. VinFast has strategically concentrated its chargers in the capital, bolstering intra-city BEV rentals. Yet, the sparse highway coverage limits electric vehicle options for those eyeing multi-province journeys. Notably, Chinese tourist arrivals have been increasing, favoring self-drive SUVs to access attractions like the Dong Van Karst Plateau. This trend has introduced weekday demand to fleets typically buoyed by weekend leisure.

Central Vietnam is emerging as the fastest-growing segment in the tourism landscape. Da Nang, with its favorable average speeds and abundant beachfront parking, boasts a car-rental penetration rate that's significantly higher per capita than Hanoi. The UNESCO corridors connecting Hue, Hoi An, and My Son are extending average rental contracts. While Da Nang's EV Priority Zone has successfully increased BEV bookings, the region's limited number of fast chargers across Central provinces still restricts electric vehicle adoption on popular routes like Nha Trang to Dalat. The completion of the North-South Expressway has significantly reduced the drive time from Hanoi to Da Nang. Furthermore, with plans to expand the airport to accommodate a much larger number of passengers in the coming years, demand is set to surge beyond the coastal hubs.

Competitive Landscape

In Vietnam's car rental market, competition remains moderate, with no single operator holding a significant share. Digital-native entrants are leveraging dynamic pricing and in-app insurance, allowing them to undercut traditional taxi fleets that are retrofitting telematics. Green & Smart Mobility stands out by operating a substantial number of EVs and chargers, utilizing a battery-swap model that significantly reduces downtime. Meanwhile, Mai Linh, with its extensive fleet, is shifting its focus to managed corporate fleets, reporting a notable increase in near-term contract wins.

Vinasun, once the frontrunner in Ho Chi Minh City, is now adopting peer-to-peer sharing to compete with Grab. Grab is set to launch its rental service soon, offering prices that undercut traditional operators during leisure weekends. While international giants like Avis, Hertz, and Sixt maintain airport concessions, their limited presence in provincial areas leaves room for domestic aggregators, such as Thuexe.vn, to dominate leisure corridors.

There's a notable opportunity in long-term corporate leasing, a segment that's highly valued in the market. This is underscored by the fact that only a small percentage of enterprises currently hold formal fleet contracts. However, technology disparities are evident: GSM’s proprietary telematics achieve a considerable reduction in energy use, yet many smaller firms depend on generic software that lacks EV-specific analytics. The introduction of Circular 12/2025, which mandates live pricing, is catalyzing a wave of mergers and partnerships among aggregators. This is largely driven by traditional operators' urgency to align with digital standards, especially with ISO-aligned telematics benchmarks set for the near future.

Vietnam Car Rental Industry Leaders

Grab Holdings Inc.

Green & Smart Mobility JSC

Vietnam Sun Corporation (Vinasun)

Mai Linh Group

Avis Budget Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: VinFast launched a wedding-centric electric car rental service. The service offers three unique packages, priced from 1.26 to 7.19 million VND, to address diverse usage requirements.

- May 2024: In a strategic move, Lotte Rental made its debut in Vietnam's long-term personal car rental market, aiming to grow its fleet to 10,000 vehicles by 2028.

Vietnam Car Rental Market Report Scope

The scope of the report includes Booking Type (Online and Offline), Rental Duration (Short-Term and Long-Term), Application Type (Tourism and Leisure and More), Vehicle Propulsion (ICE and More), End-User (Individual and Corporate), and Geography.

By Booking Type

| Online |

| Offline |

By Rental Duration

| Short-term |

| Long-term |

By Application Type

| Tourism and Leisure |

| Daily Commuting |

| Corporate and Expat Mobility |

By Vehicle Propulsion

| Internal-Combustion Engine (ICE) |

| Battery-Electric Vehicle (BEV) |

| Hybrid Electric Vehicle (HEV/PHEV) |

By End-user

| Individual |

| Corporate |

| By Booking Type | Online |

| Offline | |

| By Rental Duration | Short-term |

| Long-term | |

| By Application Type | Tourism and Leisure |

| Daily Commuting | |

| Corporate and Expat Mobility | |

| By Vehicle Propulsion | Internal-Combustion Engine (ICE) |

| Battery-Electric Vehicle (BEV) | |

| Hybrid Electric Vehicle (HEV/PHEV) | |

| By End-user | Individual |

| Corporate |

Key Questions Answered in the Report

How fast is revenue growing in the Vietnam car rental market?

Revenue is projected to increase from USD 1.17 billion in 2026 to USD 2.06 billion by 2031, reflecting a 12.03% CAGR.

Which booking channel leads demand?

Online platforms captured 61.32% of 2025 bookings and are expanding quickly due to 75% mobile-payment penetration and regulatory support for transparent pricing.

What is driving BEV adoption in rental fleets?

Decision 876 incentives, VinFast’s 150,000 urban chargers, and operating costs one-third that of gasoline are pushing BEV fleet share toward 15% by the end of the decade.

Why are corporate long-term leases gaining importance?

IFRS 16 accounting changes make rentals more liquid than ownership, and FDI manufacturers now source 50-200 vehicles through managed services to avoid depreciation and maintenance complexity.

Which region is the fastest growing for rentals?

Central Vietnam, with Da Nang and Nha Trang, shows the strongest expansion as coastal tourism and better traffic conditions lift rental penetration 40% above Hanoi.

Who are the key competitors?

Green & Smart Mobility, Mai Linh, Vinasun, Grab’s new rental arm, and airport-focused international brands such as Avis and Hertz headline a field where no player exceeds 12% share.

Page last updated on: