Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

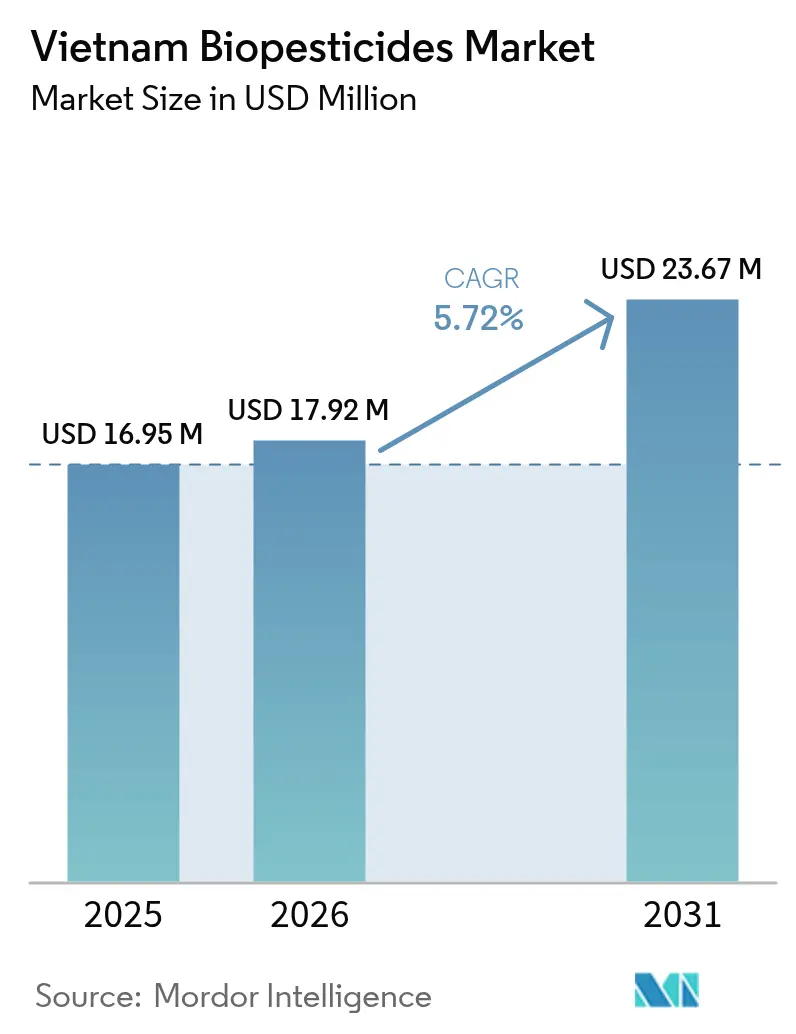

| Base Year Market Size (2025) | USD 16.95 Million |

| Market Size (2026) | USD 17.92 Million |

| Market Size (2031) | USD 23.67 Million |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Biopesticides Market Analysis by Mordor Intelligence

Vietnam biopesticides market size in 2026 is estimated at USD 17.92 million, growing from 2025 value of USD 16.95 million with 2031 projections showing USD 23.67 million, growing at 5.72% CAGR over 2026-2031. Export-oriented horticulture, stronger residue standards in China and the European Union, and government subsidies under Decision 885/QĐ-TTg create sustained demand for biological crop protection. Smallholder dominance keeps the sector fragmented, but cooperative distribution models improve last-mile reach for premium biological inputs. Rising resistance to synthetic pesticides, particularly against fall armyworm in corn and herbicide-resistant weeds in rice, is driving the adoption of microbial solutions. Investment inflows from domestic and foreign players are accelerating the formulation of innovative solutions that address Vietnam’s tropical humidity and limited cold-chain capacity.

Key Report Takeaways

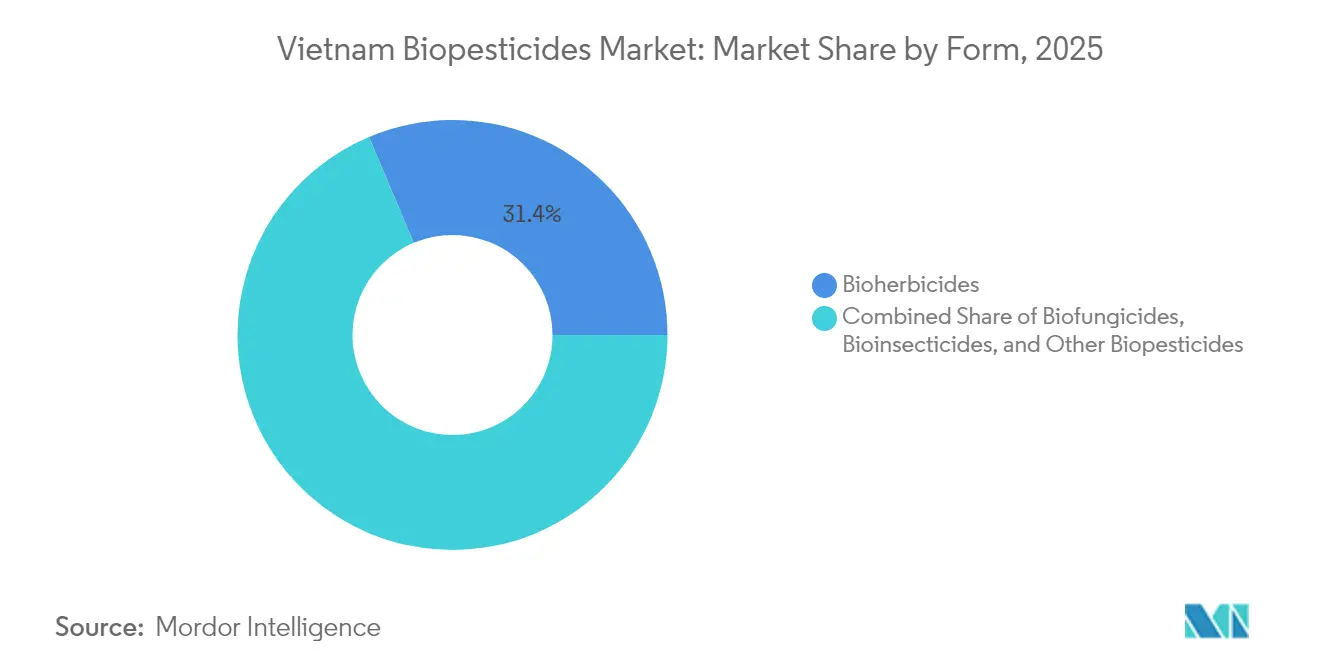

- By form, bioherbicides accounted for 31.35% of the Vietnam biopesticides market size in 2025, while bioinsecticides are projected to expand at a 6.83% CAGR through 2031.

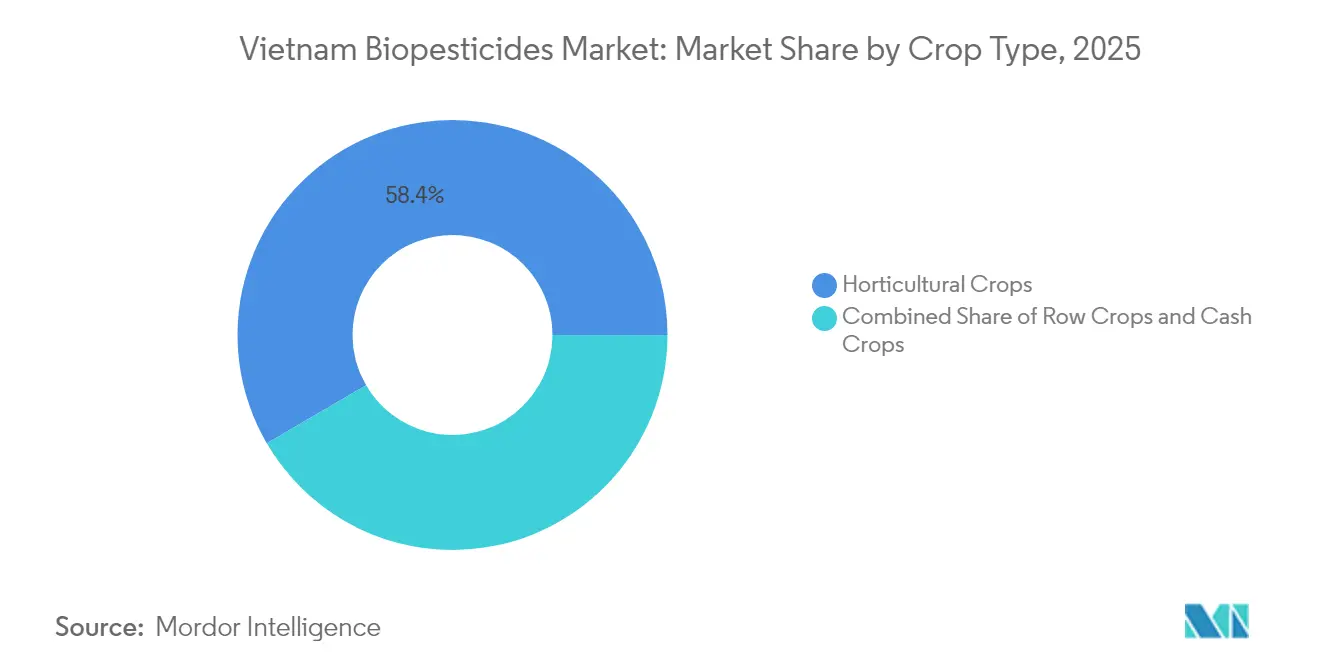

- By crop type, horticultural crops accounted for 58.40% of the Vietnam biopesticides market share in 2025, and cash crops are set to grow at a 5.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Biopesticides Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government subsidies for organic-input adoption | +1.8% | Mekong Delta and Central Highlands | Medium term (2-4 years) |

| Export-driven demand for residue-free horticulture | +1.5% | Nationwide focus on Binh Thuan, Dong Nai, and Dak Lak | Short term (≤ 2 years) |

| Rising resistance to synthetic chemistries | +1.2% | Intensive rice and vegetable zones | Long term (≥ 4 years) |

| Integration of biopesticides into national IPM programs | +1.0% | Pilot provinces with export orientation | Medium term (2-4 years) |

| Expansion of dragon-fruit and durian orchards | +0.8% | Mekong Delta and Central Highlands | Short term (≤ 2 years) |

| European Union carbon-border rules on agro-exports | +0.7% | Coffee and pepper belts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Subsidies for Organic-Input Adoption

Decision 885/QĐ-TTg enlarges direct purchase subsidies, demonstration plots, and certification support for biological inputs, lowering entry costs for smallholders who farm less than 1 hectare[1]Source: Vietnam Agriculture, “Export of Binh Thuan dragon fruit increases more than 20%,” vietnamagriculture.nongnghiep.vn. Extension officers in the Mekong Delta report a 20% rise in biopesticide field trials during 2025, indicating growing confidence in microbial formulations. Subsidy design also encompasses technical training, which helps limit misuse and enhances on-farm efficacy. Unlike neighboring countries that primarily subsidize synthetic inputs, Vietnam allocates funds toward biological alternatives, signaling a strategic policy shift that fosters domestic manufacturing and foreign investment.

Export-Driven Demand for Residue-Free Horticulture

Fruit exports exceeded USD 6 billion in 2024, and importers now impose stricter maximum residue limits that favor biological protections. China warned Vietnamese durian suppliers in June 2025 that non-compliant consignments would be returned, prompting a surge in orders for zero-interval biopesticides[2]Source: WTO Center, “Ensuring quality for sustainable growth of durian exports,” wtocenter.vn . The Standard Technical Barriers to Trade project cut Maximum Residue Limits (MRLs) by 50% for dragon fruit and vegetables, incentivizing growers to replace synthetic sprays with microbial solutions that pass multi-market inspections. Processors pay 8% price premiums for certified biological produce, offsetting the higher upfront cost of biopesticides.

Rising Resistance to Synthetic Chemistries

Fall armyworm resistance pushed biotech corn adoption to 50% of Vietnam’s feed corn acreage, demonstrating growers’ readiness to shift inputs when chemical options fail[3]Source: Long An Portal, “Vietnam emerges as global durian powerhouse,” eng.longan.gov.vn. Research presented at the 2025 International Conference on Biotechnology showed Bacillus subtilis formulations binding effectively to Phytophthora pathogens that threaten pepper and coffee. Weed populations in rice terraces exhibit glyphosate resistance levels exceeding 40%, thereby accelerating the demand for bioherbicides. Biological agents with multiple modes of action curb further resistance, making them integral to sustainable crop protection.

Integration of Biopesticides into National IPM Programs

The Ministry of Agriculture and Rural Development embeds microbial agents as core components rather than ancillaries within Integrated Pest Management (IPM) guidelines, ensuring coordinated procurement through cooperatives and contract farming clusters. Field schools now allocate two of six training modules to biological control, closing knowledge gaps that once discouraged smallholders. Provincial budgets finance monitoring and evaluation, documenting yield gains that reinforce farmer confidence. IPM alignment also creates predictable demand signals for suppliers, enabling them to plan volumes effectively and stabilize prices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low farmer confidence in field-level efficacy | –1.2% | Smallholder regions nationwide | Short term (≤ 2 years) |

| Fragmented distribution and cold-chain gaps | –0.8% | Northern provinces | Medium term (2-4 years) |

| Humidity-driven shelf-life degradation | –0.6% | Tropical climate zones | Long term (≥ 4 years) |

| Inconsistent local bio-efficacy test protocols | –0.4% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low Farmer Confidence in Field-Level Efficacy

Smallholders managing plots of less than 1 hectare depend on predictable yields to secure household incomes below USD 1,000 per hectare, leaving them with little tolerance for performance variability. Variable microbial survival under disparate microclimates undermines trust, especially when synthetic pesticides deliver visible knockdown within hours. Demonstration plots reduce skepticism, yet adoption remains cautious. Provincial extension agents note that a single failed biopesticide application can deter an entire village, highlighting the delicate nature of reputation in tightly knit farm communities.

Fragmented Distribution and Cold-Chain Gaps

Vietnam’s cold storage capacity is anticipated to reach only 1.7 million pallets by 2028, with facilities clustering near Ho Chi Minh City, leaving northern hubs with limited refrigeration. Most input retailers operate without temperature-controlled rooms, forcing biological products into unstable ambient conditions during transit. Electricity interruptions increase operating costs through increased generator fuel consumption, discouraging small distributors from stocking microbial formulations. The distribution mosaic inflates last-mile prices by as much as 15% compared with synthetic pesticides, eroding the cost advantage of subsidies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Bioherbicides Dominate, Bioinsecticides Accelerate

Bioherbicides accounted for 31.35% of the Vietnam biopesticides market share in 2025, driven by glyphosate-resistant weed outbreaks in rice paddies. Bacillus-based formulations are compatible with existing sprayer equipment, facilitating substitution without requiring new capital expenditures. Yet bioinsecticides post the fastest 6.83% CAGR through 2031, propelled by fall armyworm damage that caused yield losses up to 30% in non-treated corn fields. Formulators advance wettable powders and oil dispersions that withstand high humidity, preserving potency during field application.

Meanwhile, biofungicides are gaining traction in durian orchards as Phytophthora infections surge. However, regulatory hurdles are slowing the approval of new active ingredients. Other categories, such as bionematicides, remain niche yet attractive for pepper and coffee growers wrestling with root-knot nematodes. Intensive research and development activities signal a widening product menu that will broaden the Vietnam biopesticides market over the forecast horizon.

By Crop Type: Horticulture Leads, Cash Crops Gain Momentum

Horticultural crops held 58.40% of 2025 revenue, reflecting the export focus on dragon fruit, durian, and vegetables destined for China and the European Union. Residue-free certification premiums widen income differentials, allowing growers to absorb higher biological input costs. The Vietnam biopesticides market share for horticulture is anticipated to remain dominant through 2031, as orchard acreage continues to expand.

Cash crops, mainly coffee and pepper, register the highest 5.95% CAGR driven by European Union carbon policies that reward low-emission supply chains. The Vietnam biopesticides market size for cash crops is projected to increase, driven by processor mandates. Rice and maize growers adopt biopesticides selectively, constrained by tight margins despite subsidy offsets. Producers in contract-farming schemes, however, benefit from aggregator financing that spreads costs across larger volumes. This dualism requires suppliers to tailor portfolio and pricing strategies by crop economics, balancing high-margin specialty products with volume-driven staples.

Geography Analysis

The Mekong Delta contributes the largest revenue slice because it concentrates 30% of the durian orchards and houses most of the fruit-packing and cold-storage infrastructure. Proximity to Can Tho and Ho Chi Minh ports reduces logistics costs, enabling rapid replenishment of temperature-sensitive stocks. Provincial governments co-fund IPM field schools, generating peer-to-peer diffusion that speeds adoption. The Central Highlands exhibits the fastest growth as new durian and coffee plantings rise on fertile red basalt soils. Cooperatives in Dak Lak secure bulk procurement contracts that cut input prices 12% below retail, expanding reach among smallholders.

Northern provinces trail due to limited cold storage and fragmented distribution. Nonetheless, vegetable farmers near Hanoi shift to biological controls because supermarkets impose strict residue ceilings. Pilot projects in Bac Giang have demonstrated a 15% yield increase when biofungicides replace synthetic fungicides during humid summers. These successes spur replication grants, yet infrastructure gaps persist. Coastal regions add incremental demand from shrimp-rice rotation systems where microbial nematicides reduce soil pathogen loads.

Government program intensity varies by region. Southern provinces receive priority funding tied to export revenue targets, and northern provinces rely more on donor-supported demonstration plots. Suppliers therefore deploy a hub-and-spoke distribution system, staging inventory in southern hubs and shipping smaller lots northward under insulated packaging. Such flexibility cushions regional demand swings caused by weather or trade policy shifts, assuring nationwide coverage of the Vietnam biopesticides market.

Competitive Landscape

The top five companies controlled only a limited share of 2024 sales, underscoring fragmentation that favors niche entrants. Vietnam Pesticide Joint Stock Company leads with the strength of localized production and 2,300 retail outlets. Marrone Bio Innovations, Inc., follows, leveraging proprietary strains and joint ventures with provincial cooperatives for last-mile delivery. Domestic start-ups leverage public-sector lab research to develop cost-competitive formulations, benefiting from import duty exemptions on fermentation equipment.

Competitive focus tilts toward formulation engineering rather than novel actives because tropical heat and humidity accelerate microbial decay, making it challenging to maintain product stability. Seipasa’s Furity liquid technology extends the shelf life of Bacillus up to 15 months under ambient conditions of 35 °C. UPL Ltd., pursues sachet packaging that dissolves in tank mixes, simplifying handling for smallholders. Corteva Agriscience LLC and local NGO partners train farmers in Central Highlands provinces, building brand loyalty through service rather than price wars.

Merger and acquisition prospects rise as foreign players seek regulatory expertise and distribution scale. Domestic firms with provincial registration expertise become attractive targets, promising an accelerated route to market for global actives waiting in the pipeline. At the same time, strict local content rules encourage contract manufacturing, giving Vietnamese formulators leverage in negotiations over technology transfer royalties. Overall, competition remains cooperative rather than combative because the market still struggles to convert conventional pesticide users, leaving ample whitespace for all participants in the Vietnam biopesticides market.

Vietnam Biopesticides Industry Leaders

Vietnam Pesticide Joint Stock Company

Marrone Bio Innovations, Inc. (Bioceres Crop Solutions Corp.)

UPL Ltd.

Sumitomo Chemical Co., Ltd.

Corteva Agriscience LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The Food and Agriculture Organization (FAO) and Vietnam’s Plant Protection Department launched a National Plan for Integrated Plant Health Management (IPHM). This initiative aims to enhance biological solutions for crop protection, focusing on pest risk management in the context of climate change and the adoption of digital technologies. The plan also seeks to incorporate IPHM into agricultural training programs across the country.

- October 2023: Bayer introduced its first bio-fungicide product, SERENADE SC, in Vietnam. The product is based on the patented Bacillus subtilis strain QST 713 and provides broad-spectrum disease control, short quarantine periods, and residue-free crops, aligning with stringent export standards. It is certified by OMRI and ECOCERT for use in organic farming. Additionally, Bayer signed a Memorandum of Understanding (MoU) with PepsiCo to promote sustainable farming practices in Vietnam.

Vietnam Biopesticides Market Report Scope

Biopesticides are substances derived from natural or biological sources, used to manage pests such as insects, weeds, fungi, and other harmful organisms. They are designed to minimize environmental impact and risks to human health. Biopesticides include microbial pesticides, plant-derived pesticides, and biochemical agents that support sustainable crop protection. The Vietnam Biopesticides Market Report is Segmented by Form: Biofungicides, Bioherbicides, Bioinsecticides, and Other Biopesticides; by Crop Type: Cash Crops, Horticultural Crops, and Row Crops. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Form

| Biofungicides |

| Bioherbicides |

| Bioinsecticides |

| Other Biopesticides |

Crop Type

| Cash Crops |

| Horticultural Crops |

| Row Crops |

| Form | Biofungicides |

| Bioherbicides | |

| Bioinsecticides | |

| Other Biopesticides | |

| Crop Type | Cash Crops |

| Horticultural Crops | |

| Row Crops |

Market Definition

- AVERAGE DOSAGE RATE - The average application rate is the average volume of biopesticides applied per hectare of farmland in the respective region/country.

- CROP TYPE - Crop type includes Row crops (Cereals, Pulses, Oilseeds), Horticultural Crops (Fruits and vegetables) and Cash Crops (Plantation Crops, Fibre Crops and Other Industrial Crops)

- FUNCTION - The Crop Protection function of agirucultural biological include products that prevent or control various biotic and abiotic stress.

- TYPE - Biopesticides prevent or control various pests, including insects, diseases, and weeds, from causing crop damage and yield loss.

| Keyword | Definition |

|---|---|

| Cash Crops | Cash crops are non-consumable crops sold as a whole or part of the crop to manufacture end-products to make a profit. |

| Integrated Pest Management (IPM) | IPM is an environment-friendly and sustainable approach to control pests in various crops. It involves a combination of methods, including biological controls, cultural practices, and selective use of pesticides. |

| Bacterial biocontrol agents | Bacteria used to control pests and diseases in crops. They work by producing toxins harmful to the target pests or competing with them for nutrients and space in the growing environment. Some examples of commonly used bacterial biocontrol agents include Bacillus thuringiensis (Bt), Pseudomonas fluorescens, and Streptomyces spp. |

| Plant Protection Product (PPP) | A plant protection product is a formulation applied to crops to protect from pests, such as weeds, diseases, or insects. They contain one or more active substances with other co-formulants such as solvents, carriers, inert material, wetting agents or adjuvants formulated to give optimum product efficacy. |

| Pathogen | A pathogen is an organism causing disease to its host, with the severity of the disease symptoms. |

| Parasitoids | Parasitoids are insects that lay their eggs on or within the host insect, with their larvae feeding on the host insect. In agriculture, parasitoids can be used as a form of biological pest control, as they help to control pest damage to crops and decrease the need for chemical pesticides. |

| Entomopathogenic Nematodes (EPN) | Entomopathogenic nematodes are parasitic roundworms that infect and kill pests by releasing bacteria from their gut. Entomopathogenic nematodes are a form of biocontrol agents used in agriculture. |

| Vesicular-arbuscular mycorrhiza (VAM) | VAM fungi are mycorrhizal species of fungus. They live in the roots of different higher-order plants. They develop a symbiotic relationship with the plants in the roots of these plants. |

| Fungal biocontrol agents | Fungal biocontrol agents are the beneficial fungi that control plant pests and diseases. They are an alternative to chemical pesticides. They infect and kill the pests or compete with pathogenic fungi for nutrients and space. |

| Biofertilizers | Biofertilizers contain beneficial microorganisms that enhance soil fertility and promote plant growth. |

| Biopesticides | Biopesticides are natural/bio-based compounds used to manage agricultural pests using specific biological effects. |

| Predators | Predators in agriculture are the organisms that feed on pests and help control pest damage to the crops. Some common predator species used in agriculture include ladybugs, lacewings, and predatory mites. |

| Biocontrol agents | Biocontrol agents are living organisms used to control pests and diseases in agriculture. They are alternatives to chemical pesticides and are known for their lesser impact on the environment and human health. |

| Organic Fertilizers | Organic fertilizer is composed of animal or vegetable matter used alone or in combination with one or more non-synthetically derived elements or compounds used for soil fertility and plant growth. |

| Protein hydrolysates (PHs) | Protein hydrolysate-based biostimulants contain free amino acids, oligopeptides, and polypeptides produced by enzymatic or chemical hydrolysis of proteins, primarily from vegetal or animal sources. |

| Biostimulants/Plant Growth Regulators (PGR) | Biostimulants/Plant Growth Regulators (PGR) are substances derived from natural resources to enhance plant growth and health by stimulating plant processes (metabolism). |

| Soil Amendments | Soil Amendments are substances applied to soil that improve soil health, such as soil fertility and soil structure. |

| Seaweed Extract | Seaweed extracts are rich in micro and macronutrients, proteins, polysaccharides, polyphenols, phytohormones, and osmolytes. These substances boost seed germination and crop establishment, total plant growth and productivity. |

| Compounds related to biocontrol and/or promoting growth (CRBPG) | Compounds related to biocontrol or promoting growth (CRBPG) are the ability of a bacteria to produce compounds for phytopathogen biocontrol and plant growth promotion. |

| Symbiotic Nitrogen-Fixing Bacteria | Symbiotic nitrogen-fixing bacteria such as Rhizobium obtain food and shelter from the host, and in return, they help by providing fixed nitrogen to the plants. |

| Nitrogen Fixation | Nitrogen fixation is a chemical process in soil which converts molecular nitrogen into ammonia or related nitrogenous compounds. |

| ARS (Agricultural Research Service) | ARS is the U.S. Department of Agriculture's chief scientific in-house research agency. It aims to find solutions to agricultural problems faced by the farmers in the country. |

| Phytosanitary Regulations | Phytosanitary regulations imposed by the respective government bodies check or prohibit the importation and marketing of certain insects, plant species, or products of these plants to prevent the introduction or spread of new plant pests or pathogens. |

| Ectomycorrhizae (ECM) | Ectomycorrhiza (ECM) is a symbiotic interaction of fungi with the feeder roots of higher plants in which both the plant and the fungi benefit through the association for survival. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.