Hermetic Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

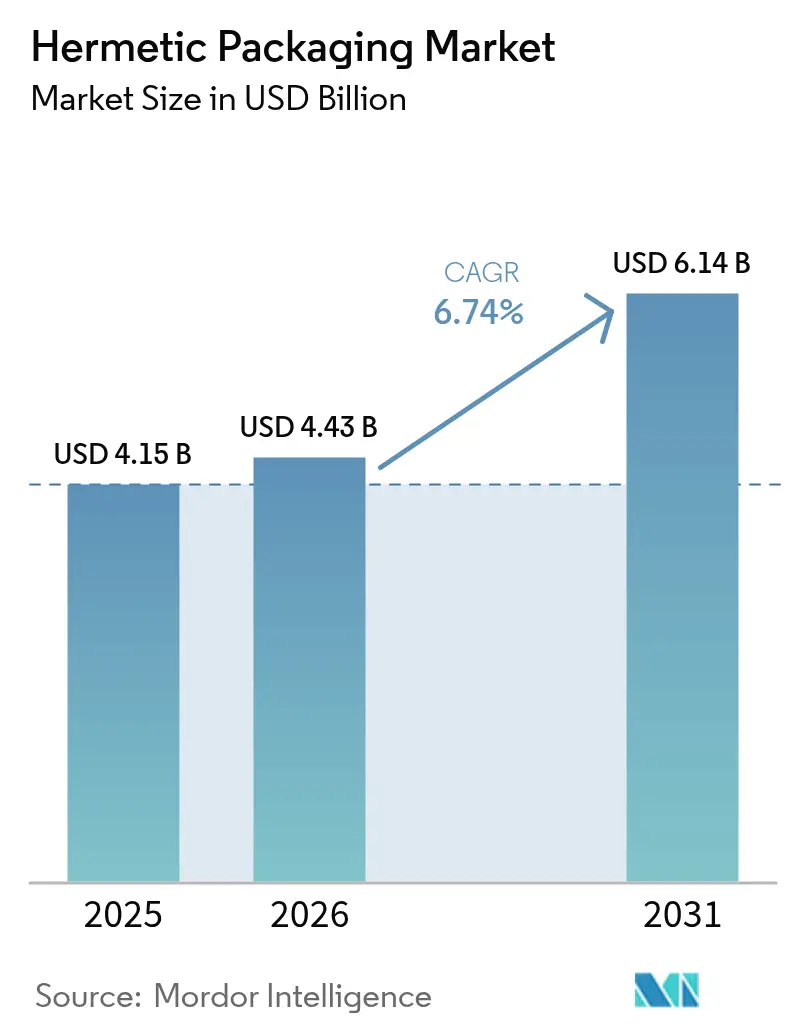

| Market Size (2026) | USD 4.43 Billion |

| Market Size (2031) | USD 6.14 Billion |

| Growth Rate (2026 - 2031) | 6.74% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hermetic Packaging Market Analysis by Mordor Intelligence

The hermetic packaging market size was valued at USD 4.15 billion in 2025 and estimated to grow from USD 4.43 billion in 2026 to reach USD 6.14 billion by 2031, at a CAGR of 6.74% during the forecast period (2026-2031). Escalating demand for fault-tolerant electronics in aerospace updates, 5G base-station rollouts, and high-density electric-vehicle sensors is shifting volumes from legacy defense procurements toward high-throughput commercial lines. Device designers are tightening helium-leak limits to the 1 × 10⁻⁹ atm-cc-s threshold, which privileges ceramic-to-metal seals over glass-to-metal interfaces in automotive safety actuators. Pressed-ceramic carriers optimized for quantum-computing cryostats and millimeter-wave radar modules are capturing new sockets that traditionally defaulted to metal cans. Meanwhile, defense primes and medical-device OEMs continue to lock in multiyear supply agreements to mitigate raw-glass and kovar-alloy bottlenecks that emerged in 2024.

Key Report Takeaways

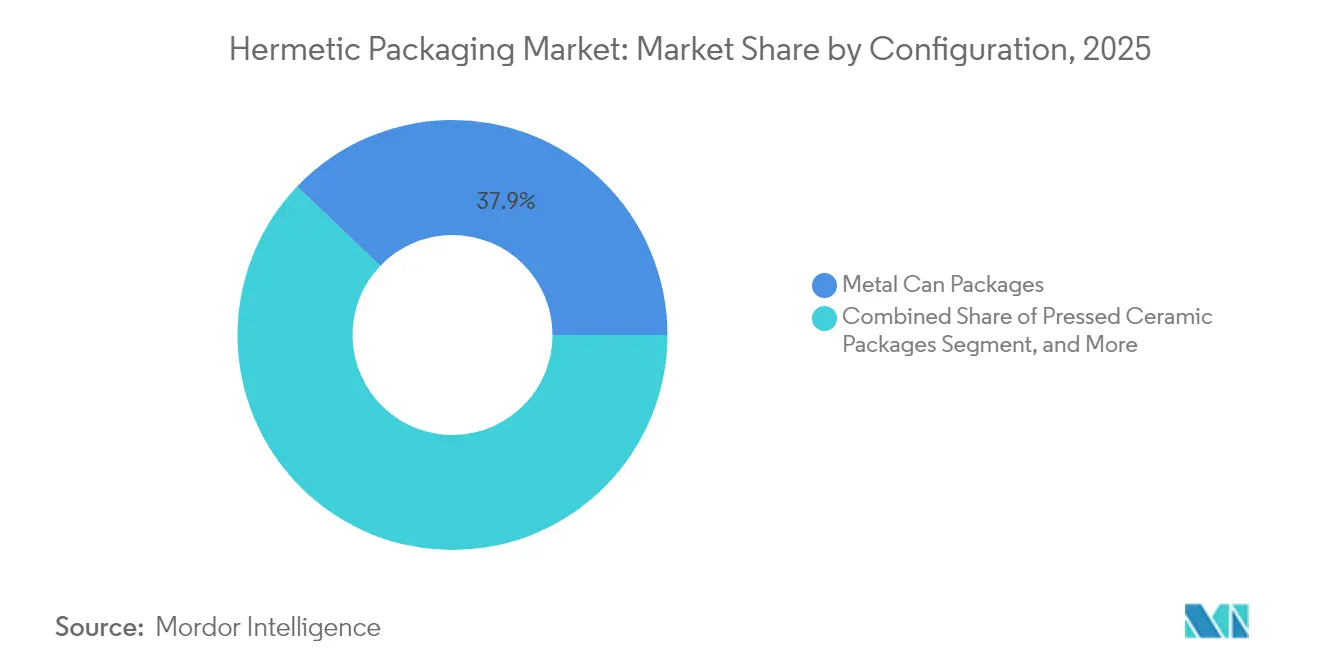

- By configuration, metal cans accounted for 37.86% of the hermetic packaging market share in 2025, whereas pressed-ceramic formats are expected to advance at an 8.12% CAGR through 2031.

- By type, ceramic-to-metal sealing held 28.10% of the hermetic packaging market share in 2025 and is forecast to expand at an 8.05% CAGR.

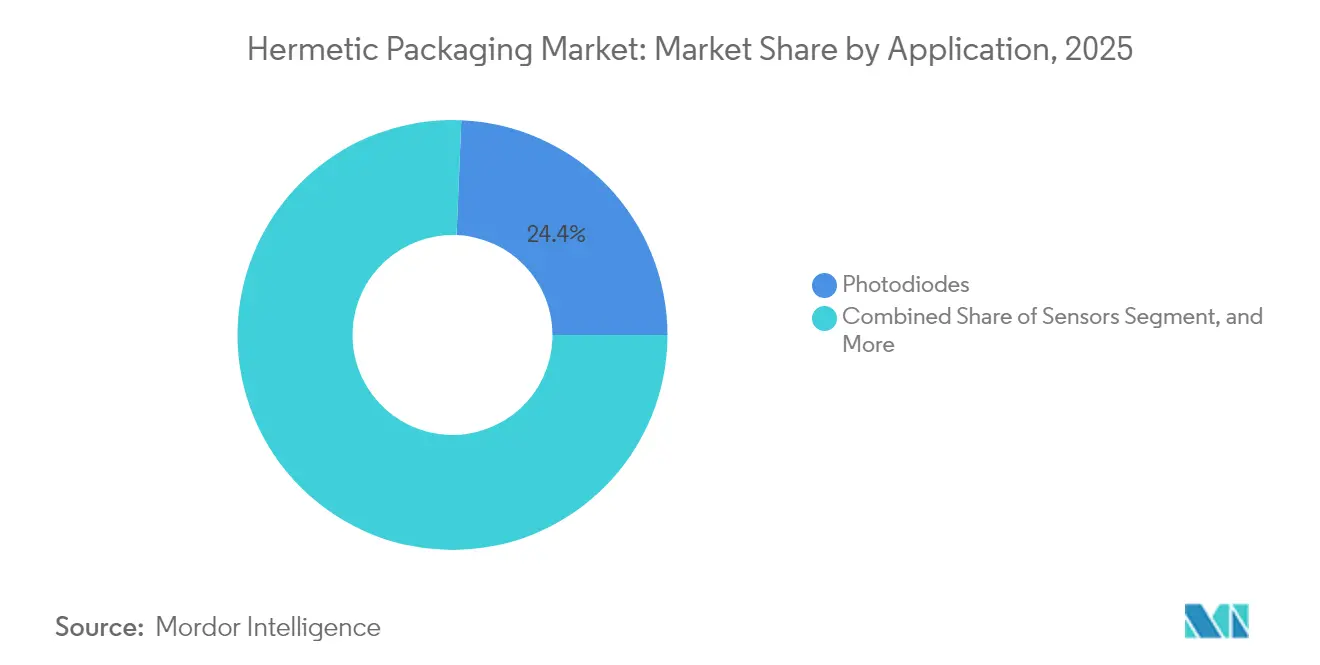

- By application, photodiodes led the hermetic packaging market with 24.35% of the market share in 2025, while MEMS switches represented the fastest-growing niche at a 9.18% CAGR from 2026 to 2031.

- By end-user, the automotive sector accounted for 31.95% of the hermetic packaging market share in 2025; however, the aerospace and defense sector is expected to post the highest CAGR of 9.04% across the outlook window.

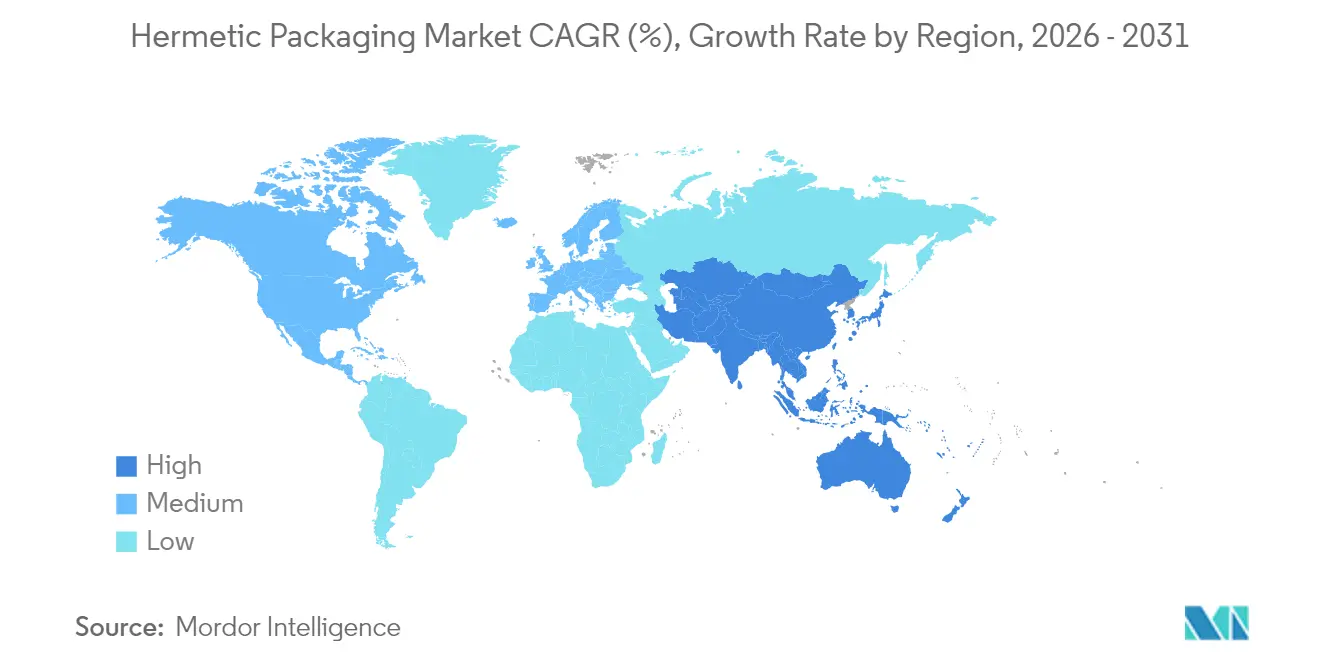

- By geography, North America contributed 39.65% of the revenue in 2025, although the Asia-Pacific region is projected to register a 8.82% CAGR, thanks to the acceleration of 5G and EV supply-chain localization.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hermetic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand for High-Reliability Electronics in Aerospace and Defense | +1.2% | North America, Europe, Asia-Pacific defense corridors | Medium term (2-4 years) |

| Growing Adoption of Electric Vehicles with Safety-Critical Sensors | +1.5% | Global, with concentration in China, Europe, North America | Short term (≤ 2 years) |

| Expansion of 5G Infrastructure Driving Hermetic RF Packages | +1.1% | Asia-Pacific core, spill-over to Middle East and Africa | Short term (≤ 2 years) |

| Growth of Medical Implants Requiring Long-Term Encapsulation | +0.9% | North America, Western Europe, Japan | Long term (≥ 4 years) |

| Miniaturization of Quantum-Computing Cryogenic Devices | +0.6% | North America, select European research hubs | Long term (≥ 4 years) |

| Mandatory Reliability Standards for NewSpace Small-Satellite Constellations | +0.8% | Global, led by North America and emerging launch markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for High-Reliability Electronics in Aerospace and Defense

Distributed low-Earth-orbit constellations expose components to cumulative ionizing doses beyond 100 kilorads, forcing program managers to specify helium-fine-leak test limits at 1 × 10⁻⁸ atm-cc-s or better.[1]National Aeronautics and Space Administration, “NASA Electronic Parts and Packaging Program,” nepp.nasa.gov Sealed Kovar-lid packages also protect gallium-nitride radar amplifiers whose junctions routinely exceed 200 °C in flight. U.S. fiscal-year 2025 space-system funding of USD 33.9 billion doubles the satellite lot purchases recorded in 2023, directly enlarging the qualified-supplier funnel for hermetic housings. European defense agencies are meeting these requirements through the Eurofighter radar upgrade, maintaining resilient demand despite cost inflation. Because plastic encapsulation suffers rapid moisture uptake under orbital temperature cycling, the hermetic packaging market continues to defend premium pricing in this vertical.

Growing Adoption of Electric Vehicles with Safety-Critical Sensors

Battery electric vehicles incorporate hermetically sealed pressure, inertial, and battery-management sensors that must withstand AEC-Q100 high-temperature operating conditions of up to 150 °C. Tesla shipped 1.81 million units in 2024, each equipped with an average of 18 hermetic sensors, equivalent to more than 32 million units from one automaker alone.[2]Tesla Inc., “2024 Annual Report,” ir.tesla.com Airbag ignitors utilize ceramic-to-metal feedthroughs to eliminate moisture pathways that could degrade pyrotechnic pellets over the vehicle's 15-year lifespan. Government crash-test protocols require flawless deployment across a temperature range of -40 °C to +125 °C, highlighting the adoption gap versus plastic encapsulation. As Chinese and European EV platforms transition to centralized zonal architectures, a single node failure can compromise safety functions, further enhancing the value proposition of hermetic packages

Expansion of 5G Infrastructure Driving Hermetic RF Packages

China Mobile activated 1.9 million 5G base stations in 2024, each hosting up to 256 transceiver elements that rely on hermetic RF relays to maintain insertion loss below 0.5 dB across the temperature range of -40 °C to +85 °C.[3]China Mobile Limited, “Sustainability Report 2024,” chinamobileltd.com Millimeter-wave small cells increase the component count per square kilometer, driving a multiplier effect on hermetic volumes compared to the 4G era. Operators in the Middle East and Africa are following suit, adapting IP67 requirements that epoxy-molded packages cannot meet without secondary sealing. Reliability clauses in multiyear tower-leasing contracts stipulate 99.999% uptime, making hermetic integrity a non-negotiable requirement. Component OEMs respond by integrating ceramic heat spreaders within package floors to tame self-heating in 64T64R antenna arrays.

Growth of Medical Implants Requiring Long-Term Encapsulation

ISO 14708-1 caps moisture ingress at 1 × 10⁻⁹ atm-cc-s for implantable pulse generators, a level unattainable with conformally coated plastics. Medtronic shipped 850,000 rhythm-management devices in 2024, each enclosed in a titanium shell brazed to a glass-to-metal feedthrough. The FDA’s 2024 guidance on wireless implants emphasized electromagnetic compatibility under MRI fields up to 4 tesla, which is easier to achieve when the housing acts as a Faraday cage. Western Europe’s aging population is expected to raise the annual pacemaker implantation rate, supporting long-tail demand through 2030. As neurostimulator therapies for chronic pain and depression scale, developers specify ultra-thin titanium lids yet still require leak rates in the 10⁻¹⁰ atm-cc-s decade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Hermetic Materials and Processes | -1.3% | Global, acute in price-sensitive consumer segments | Short term (≤ 2 years) |

| Availability of Low-Cost Plastic Encapsulation Alternatives | -0.9% | Asia-Pacific manufacturing hubs, consumer electronics | Medium term (2-4 years) |

| Skilled Labor Shortage for Precision Seal Manufacturing | -0.7% | North America and Western Europe, spill-over to high-wage Asia-Pacific | Medium term (2-4 years) |

| Supply Chain Vulnerability for High-Purity Glass Powders | -0.5% | Global, concentrated impact on medical implant and optical segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Hermetic Materials and Processes

Unit economics range from USD 2 to USD 50 per packaged device, versus USD 0.10 to USD 2 for plastic QFN equivalents. Kovar alloy averaged USD 35/kg in 2024, while high-purity alumina exceeded USD 150/kg, inflating the bill of materials for mid-volume programs. Laser-seam welders cost more than USD 500,000 per line, and cycle times typically last around 20 seconds, quadrupling the takt relative to transfer-molding presses. Wage pressure for leak-test technicians surpasses USD 25 per hour in the United States, further widening the pricing gulf. Consumer electronics brands, therefore, prefer plastic overmolds unless functional-safety or lifetime warranties override cost concerns.

Availability of Low-Cost Plastic Encapsulation Alternatives

Outsourced assembly houses in Malaysia, Vietnam, and the Philippines offer molded BGAs at USD 0.15 to USD 0.80, leveraging JEDEC MSL-3 qualified epoxies that tolerate 85 °C–85% RH for 168 hours without delamination. Parylene and silicone coatings shrink moisture uptake, allowing plastics to meet five-year service targets in wearables and industrial IoT. System-in-package architectures pack multiple dies under a single epoxy dome, sidestepping the footprint penalties that legacy metal cans impose. Unless specifications invoke MIL-STD-883 or ISO 14708, project managers often opt for the cheaper route. This substitution effect restrains the hermetic packaging market, especially in midrange automotive infotainment and consumer health gadgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Configuration: Pressed-Ceramic Packages Capture Quantum and RF Growth

Pressed-ceramic formats are projected to clock an 8.12% CAGR from 2026 to 2031 as quantum processors and millimeter-wave front-ends migrate toward low-outgassing substrates that stabilize electrical parameters below 100 millikelvin. Pressed ceramics accounted for 21.14% of the hermetic packaging market size in 2025, narrowing the historic gap with metal cans.

IBM’s 1,121-qubit Condor processor demonstrates that a single pressed-ceramic carrier can host high-density superconducting routing while meeting a 1 × 10⁻¹⁰ atm-cc-s leak limit. Satellite OEMs favor the same technology for compact chip-on-board assemblies that shave mass by 35% compared with TO-style cans. Automotive radar modules operating at 77 GHz integrate ceramic heat spreaders to dissipate heat, thereby raising demand among tier-one suppliers in Germany and Japan. Although multilayer-ceramic packages still dominate Ka-band payloads, their multi-co-fired fabrication stretches lead times beyond 12 weeks, prompting designers to pivot toward single-fire pressed options. As defense primes localize supply chains, U.S. and South Korean fabs are installing new sintering furnaces that raise pressed-ceramic throughput to 25 million units annually.

By Type: Ceramic-to-Metal Sealing Strengthens Harsh-Environment Foothold

Ceramic-to-metal seals captured 28.10% of the revenue in 2025 and are projected to grow at an 8.05% CAGR, outpacing glass-to-metal alternatives as OEMs seek to achieve coefficient of thermal expansion parity under -40 °C to +150 °C cycles. Ceramic-to-metal devices represented 17.55% of the hermetic packaging market size for airbag ignitors in 2025, and their share is poised to rise as European safety regulators increase deployment-reliability thresholds.

Modern kovar-sheathed feedthroughs withstand mechanical shock at 40,000 g, a specification that is challenging to meet with glass interfaces, which can microcrack during automotive cold soak. Medical-device makers still specify borosilicate glass for titanium housings, but are increasingly trialing thin-film alumina inserts to lower X-ray attenuation in MRI-compatible implants. Reed-glass and transponder-glass segments remain small, serving magnetic switches and livestock RFID tags where unit economics outweigh the need for extreme reliability. Passivation glass overcoats on analog die curb mobile-ion drift, yet they supplement rather than replace ceramic lids in petrochemical plant controllers. The competitive field, therefore, concentrates on high-yield ceramic-to-metal brazing lines capable of 180 ppm part-per-million leak performance under helium bombing.

By Application: MEMS Switches Accelerate on 5G Beam-Forming Demands

MEMS RF switches are on track for a 9.18% CAGR, the quickest among application clusters, as 5G massive-MIMO antennas adopt electrostatically actuated relays that deliver sub-0.2 dB insertion loss. MEMS devices accounted for 11.88% of the hermetic packaging market share in 2025, and design wins at Chinese and U.S. base-station makers suggest a double-digit share by 2030.

Photodiodes still account for 24.35% of 2025 revenue, thanks to the hyperscale move toward 800 GbE optical links, where indium-gallium-arsenide detectors must remain stable in 85 °C data center aisles. VCSEL and DFB laser diodes require hermetic lids to prevent facet oxidation, thereby preserving a 250-mW output over a 25,000-hour service life. High-G shock sensors on oil-drill heads rely on robust sealing to maintain calibration in environments containing hydrogen sulfide. Airbag ignitors continue to ship in the hundreds of millions, but volume growth is moderating as mature markets plateau light-vehicle production. Overall demand patterns imply widening diversity rather than single-segment dominance, a trend that rewards suppliers with broad design libraries.

By End-User Industry: NewSpace Drives a Shift Toward Defense-Grade Volumes

The automotive sector maintained a 31.95% revenue share in 2025, while the aerospace and defense sector is expected to register the fastest growth of 9.04% CAGR, as thousands of low-orbit satellites require radiation-hardened modules that can operate beyond 15 years without onsite servicing. The hermetic packaging market size for satellite electronics approached USD 810 million in 2025, underpinned by the Starlink fleet surpassing 5,000 active spacecraft.

Electric-vehicle makers remain vital, but their average sensor count plateaus once Level-3 autonomy stabilizes. Medical-implant consumption rises steadily with demographic aging in OECD nations, while petrochemical and energy producers add down-hole pressure and temperature probes that must withstand temperatures of up to 175 °C for 10,000 hours. Industrial automation segments adopt hermetically sealed encoders to avert coolant ingress on CNC machinery. These overlapping demand waves diversify revenue sources, cushioning suppliers from cyclical shocks in any single domain.

Geography Analysis

North America retained 39.65% of global revenue in 2025, anchored by defense primes, cardiac-device OEMs, and legacy aerospace corridors from California to Florida. The United States Department of Defense earmarked USD 33.9 billion for space-system procurements in fiscal 2025, funneling orders to hermetic providers qualified under MIL-STD-883 and AS9100. Boston Scientific, Abbott, and Medtronic shipped more than 2 million implantable devices from their regional plants, thereby preserving domestic demand even as some consumables are shifted offshore. Canadian satellite suppliers contribute high-density feedthrough assemblies for the Lightspeed constellation, while Mexican maquiladoras manufacture airbag ignitors that supply platforms in Detroit. A culture of design for reliability keeps unit margins above global averages, ensuring North American fabs operate at favorable capacity utilization.

Asia-Pacific is poised for a 8.82% CAGR between 2026 and 2031, outstripping every other region as China, Japan, and South Korea accelerate semiconductor self-reliance. China Mobile’s record 1.9 million 5G towers translate to tens of millions of hermetic RF filters shipped annually, and BYD’s 3.6 million EVs embed battery-management feedthroughs in every pack. Kyocera’s fiscal 2024 reporting highlighted 12% year-over-year growth in semiconductor components, driven by ceramic substrate exports to European automotive radar lines. Samsung Electro-Mechanics is retrofitting cleanrooms in Gumi to co-package hermetic lids on premium smartphone image sensors, while India and Vietnam court back-end assembly investments that de-risk single-country exposure.

Europe generated approximately 14.68% of the 2025 global revenue, with Germany’s Bosch, Continental, and ZF purchasing over 150 million hermetic automotive sensors for safety systems. Airbus delivered 735 aircraft, each stuffed with flight-control computers that must withstand 30-year pressurization cycles. SCHOTT AG logged EUR 400 million (USD 450 million) in hermetic packaging sales, leveraging in-house glass powder furnaces to protect against supply shocks. France’s missile and satellite programs maintain a robust vendor qualification pipeline, and the United Kingdom’s Surrey Satellite Technology specifies ceramic flat packs for Earth observation payloads. Although the Middle East and Africa, as well as South America, together accounted for less than 9.85% of 2025 revenue, oil-and-gas automation upgrades and South African mining robotics show incremental uptake for hermetic sensors, hinting at future upside tied to infrastructure investment cycles.

Competitive Landscape

The hermetic packaging market is moderately consolidated, with the top five suppliers controlling roughly 45% of global revenue; however, no single vendor exceeds a 15% share. SCHOTT, Kyocera, NGK, AMETEK, and Materion dominate the market for Kovar-brazed ceramic housings, leveraging vertically integrated glass-powder synthesis and alloy-stamping lines to buffer material volatility. Smaller entrants, such as Complete Hermetics and Willow Technologies, carve out niches in cryogenic quantum-bit carriers and titanium neural-implant feedthroughs, competing on agility and rapid prototyping speed.

Technology differentiation centers on sub-nanoleak performance; tier-one players advertise routine screening down to 1 × 10⁻¹⁰ atm-cc-s through helium bombing, residual-gas analysis, and automated micro-CT inspection. Additive-manufactured titanium shells with integrated cooling microchannels reduce design cycles for high-power radar amplifiers, while low-temperature co-fired ceramic packages achieve dielectric-loss tangents below 0.001 at 77 GHz, making them suitable for automotive radar modules.

Strategic moves underscore a tilt toward capacity expansion: SCHOTT’s USD 56 million Mitterteich line upgrade raised medical-implant feedthrough output by 30%; AMETEK injected USD 25 million into Connecticut connector lines; and Teledyne’s USD 180 million Micross acquisition introduced radiation-hardened flat-pack expertise. Suppliers maintain ISO 13485, AS9100, and IATF 16949 credentials to secure multiyear contracts that newcomers struggle to penetrate. Continuous investment in leak-test automation and ceramic-powder purity safeguards competitive moats as cost pressures mount from the use of plastic encapsulation.

Hermetic Packaging Industry Leaders

SCHOTT AG

AMETEK Inc.

Teledyne Technologies Incorporated

Materion Corporation

Micross Components Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: AMETEK signed a five-year contract valued at USD 75 million to supply hermetic connectors and feedthroughs for SpaceX Starlink Gen2 satellites, securing priority allocation for high-pin-count assemblies.

- August 2025: SCHOTT AG introduced its HectoSeal ultra-low-leak glass-ceramic series, rated to 1 × 10⁻¹⁰ atm-cc-s, with pilot production underway at the Mitterteich facility to serve emerging quantum-computing modules.

- April 2025: Kyocera invested USD 30 million to open a research and development center in Phoenix, Arizona, focused on additive-manufactured ceramic-to-metal hermetic packages for aerospace and quantum-computing applications.

- February 2025: NGK Insulators completed a new ceramic feedthrough production line at its Nagoya plant, expanding annual capacity for electric-vehicle sensor packages by 20% following a USD 18 million equipment upgrade.

Global Hermetic Packaging Market Report Scope

Hermetic packaging refers to the sealing of electronic components to protect them from environmental factors such as moisture, dust, and other contaminants, ensuring their reliability and longevity. This type of packaging is widely used in industries where high-performance and durability are critical.

The Hermetic Packaging Market Report is Segmented by Configuration (Multilayer Ceramic Packages, Pressed Ceramic Packages, Metal Can Packages), Type (Passivation Glass, Reed Glass, Transponder Glass, Glass-to-Metal Sealing, Ceramic-to-Metal Sealing), Application (Sensors, Photodiodes, Lasers, MEMS Switches, Airbag Ignitors), End-User Industry (Aerospace and Defense, Automotive, Healthcare, Petrochemical, Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Multilayer Ceramic Packages |

| Pressed Ceramic Packages |

| Metal Can Packages |

| Passivation Glass |

| Reed Glass |

| Transponder Glass |

| Glass-to-Metal Sealing |

| Ceramic-to-Metal Sealing |

| Sensors |

| Photodiodes |

| Lasers |

| MEMS Switches |

| Airbag Ignitors |

| Aerospace and Defense |

| Automotive |

| Healthcare |

| Petrochemical |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Nigeria | ||

| Rest of Africa | ||

| By Configuration | Multilayer Ceramic Packages | ||

| Pressed Ceramic Packages | |||

| Metal Can Packages | |||

| By Type | Passivation Glass | ||

| Reed Glass | |||

| Transponder Glass | |||

| Glass-to-Metal Sealing | |||

| Ceramic-to-Metal Sealing | |||

| By Application | Sensors | ||

| Photodiodes | |||

| Lasers | |||

| MEMS Switches | |||

| Airbag Ignitors | |||

| By End-User Industry | Aerospace and Defense | ||

| Automotive | |||

| Healthcare | |||

| Petrochemical | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What CAGR is forecast for the hermetic packaging market through 2031?

The hermetic packaging market is projected to register a 6.74% CAGR between 2026 and 2031.

Which configuration type is expanding the fastest?

Pressed-ceramic packages are advancing at an 8.12% CAGR owing to quantum-computing and millimeter-wave radar demand.

Why are ceramic-to-metal seals gaining share over glass-to-metal seals?

Better thermal-expansion matching under -40 °C to +150 °C cycles reduces leak risk in automotive and defense applications.

Which region offers the highest growth potential to 2031?

Asia-Pacific is forecast to post a 8.82% CAGR as China, Japan, and South Korea localize advanced packaging capacity.

How do plastic alternatives affect hermetic packaging adoption?

Low-cost plastic BGAs and conformal coatings undercut pricing, limiting uptake in consumer electronics where ultimate reliability is not mandated.

Page last updated on: