Chemicals & Materials

7th MayStrategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

The Opacifiers Report is Segmented by Type (Titanium Dioxide, Opaque Polymers, Zinc Oxide, Cerium Oxide, and Other Types), Form (Powder, Dispersion, Masterbatch), Application (Paints and Coatings, Ceramics, Paper, Personal Care, Plastics, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

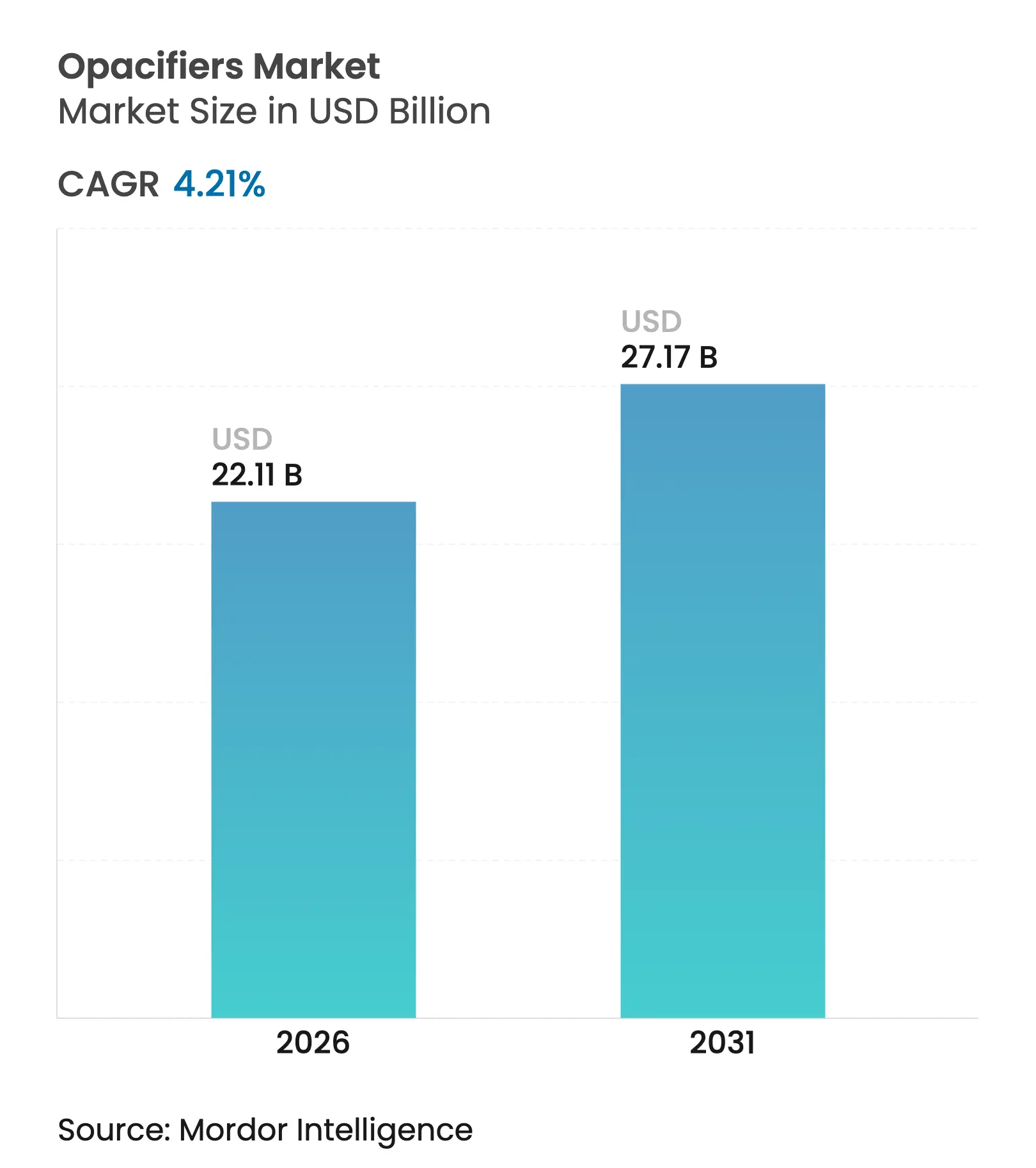

| Market Size (2026) | USD 22.11 Billion |

| Market Size (2031) | USD 27.17 Billion |

| Growth Rate (2026 - 2031) | 4.21 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Opacifiers market size in 2026 is estimated at USD 22.11 billion, growing from 2025 value of USD 21.22 billion with 2031 projections showing USD 27.17 billion, growing at 4.21% CAGR over 2026-2031. Rising infrastructure activity, personal-care reformulation pressures, and technical ceramics innovation are collectively reinforcing steady demand, while regulatory scrutiny of titanium dioxide is nudging formulators toward hybrid or alternative systems. Paints and coatings remain the anchor application, but the fastest incremental volumes are coming from personal-care lines that must balance opacity with clean-beauty mandates. Asia-Pacific dominates both scale and velocity, thanks to its integrated mineral extraction, pigment conversion, and downstream manufacturing base, although Europe sets the pace on regulatory change that shapes global product development. Together, these dynamics position the opacifiers market for measured but resilient expansion through 2030.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Surging infrastructure-led demand in paints and coatings

Surging infrastructure-led demand in paints and coatings

| +1.2% | Global, led by APAC and MEA | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

Global, led by APAC and MEA

|

Impact Timeline

:

Medium term (2-4 years)

|

Expanding ceramics output in developing economies

Expanding ceramics output in developing economies

| +0.8% | APAC core; spill-over to LATAM | Long term (≥4 years) | |||

Growing personal-care formulation complexity

Growing personal-care formulation complexity

| +0.6% | North America and EU; expanding to APAC | Short term (≤2 years) | |||

Regulatory push toward titanium-oxide-free alternatives

Regulatory push toward titanium-oxide-free alternatives

| +0.5% | EU and North America | Medium term (2-4 years) | |||

3-D-printed technical ceramics need tailored opacifiers

3-D-printed technical ceramics need tailored opacifiers

| +0.4% | North America, EU, Japan | Long term (≥4 years) | |||

| Source: Mordor Intelligence | ||||||

Surging Infrastructure-Led Demand in Paints and Coatings

Infrastructure programmes are generating sustained coatings consumption that requires robust hiding power coupled with low-VOC compliance. Projects under China’s Belt and Road Initiative have similar opacity-performance specifications, favouring surface-treated rutile grades that deliver UV stability. At the same time, geopolitical tension around critical minerals is prompting producers to lock in ilmenite and zircon sources, ensuring that coatings formulators receive consistent whiteness and tinting strength. As mega-infrastructure pipelines extend across emerging markets, paints and coatings will continue to anchor volume for the opacifiers market.

Expanding Ceramics Output in Developing Economies

Developing economies are moving up the value curve, investing in technical ceramics for electronics, aerospace, and renewable-energy assemblies that demand opacity at sintering temperatures exceeding 1,700 °C. HRL Laboratories’ light-curable ceramic resins prove that appropriately engineered opacifiers can survive both photopolymerisation and high-temperature densification. Kyocera’s additive-manufacturing push with alumina and zirconia illustrates how tailored refractive indices and particle morphologies enable intricate lattice structures. Cerium and zinc oxides are benefiting from these trends by providing alternative whiteness without compromising dielectric properties. As Latin American nations replicate these production models, long-run demand for high-temperature opacifiers is set to widen the application spectrum of the opacifiers market.

Growing Personal-Care Formulation Complexity

Clean-beauty standards require opacifiers that simultaneously supply whiteness, UV protection, and elegant sensory profiles. The EU Cosmetics Regulation mandates a six-month advance notification for any nanomaterial, forcing formulators to vet every particle dimension and surface treatment[1]“Regulation 1223/2009 Cosmetic Products,” EUR-Lex, eur-lex.europa.eu . Polymer–zinc-oxide composites now allow water-based sunscreen gels that avoid the greasy feel typical of legacy systems while meeting SPF targets. Biodegradable starch and natural wax opacifiers are gaining traction in rinse-off products, though their hiding power lags titanium dioxide benchmarks. With personal-care brands racing to publish full ingredient transparency, the opacifiers market is evolving toward multifunctional mineral platforms that can be registered quickly across multiple jurisdictions.

Regulatory Push Toward Titanium-Oxide-Free Alternatives

The European Food Safety Authority’s 2024 opinion has accelerated the search for replacements in more than 100,000 medicinal SKUs, yet no single chemistry duplicates titanium dioxide’s opacity and inertness[2]European Federation of Pharmaceutical Industries and Associations, “TiO₂ and Alternatives Industry Final Report to QWP EMA 2024,” efpia.eu. Pharmaceutical reformulation budgets are swelling, and projected timelines stretch seven to twelve years for complex dosage forms. Calcium carbonate, iron oxides, and hybrid polymeric beads are being trialled, but each introduces performance trade-offs ranging from discoloration to moisture sensitivity. Cosmetics companies are taking a preventative route by shifting toward cerium and zinc systems ahead of any formal ban. The opacifiers market, therefore, faces both risk and opportunity as industries balance compliance deadlines with technical feasibility.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Tightening health and environmental rules on titanium

oxide

Tightening health and environmental rules on titanium

oxide

| −0.7% | EU and North America | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

−0.7%

|

Geographic Relevance

:

EU and North America

|

Impact Timeline

:

Medium term (2-4 years)

|

Volatile feedstock prices (ilmenite, zircon, antimony)

Volatile feedstock prices (ilmenite, zircon, antimony)

| −0.6% | Global, Asia supply focus | Short term (≤2 years) | |||

Sustainability shift to clear/bio-based materials

Sustainability shift to clear/bio-based materials

| −0.3% | Global, led by developed markets | Long term (≥4 years) | |||

| Source: Mordor Intelligence | ||||||

Tightening Health and Environmental Rules on Titanium Oxide

EU authorities have questioned titanium dioxide’s safety profile, forcing pharmaceutical and food-supplement players to evaluate costly overhauls. Cosmetics brands face an added disclosure layer for nano-forms, increasing administrative burdens and elongating time-to-market. Because no direct substitute matches TiO₂’s opacity and neutrality, formulators either accept downgraded whiteness or combine multiple pigments at higher dosage, escalating cost and complexity. These headwinds shave growth momentum within the opacifiers market, particularly in regions with active hazard labelling debates.

Sustainability Shift to Clear/Bio-Based Materials

Microplastics bans and consumer preference for ingredient transparency are guiding research and development toward biodegradable or transparent solutions. Roquette’s starch-based system now enables paper opacification without mineral loading, helping converters meet eco-label criteria. European ink makers are switching to vegetable-oil vehicles, thereby curbing traditional pigment demand. Personal-care labels celebrate translucent gels that showcase naturally derived actives, lowering opacity requirements. These shifts gradually erode volume in established segments of the opacifiers market while opening exploratory niches for bio-compatible chemistries.

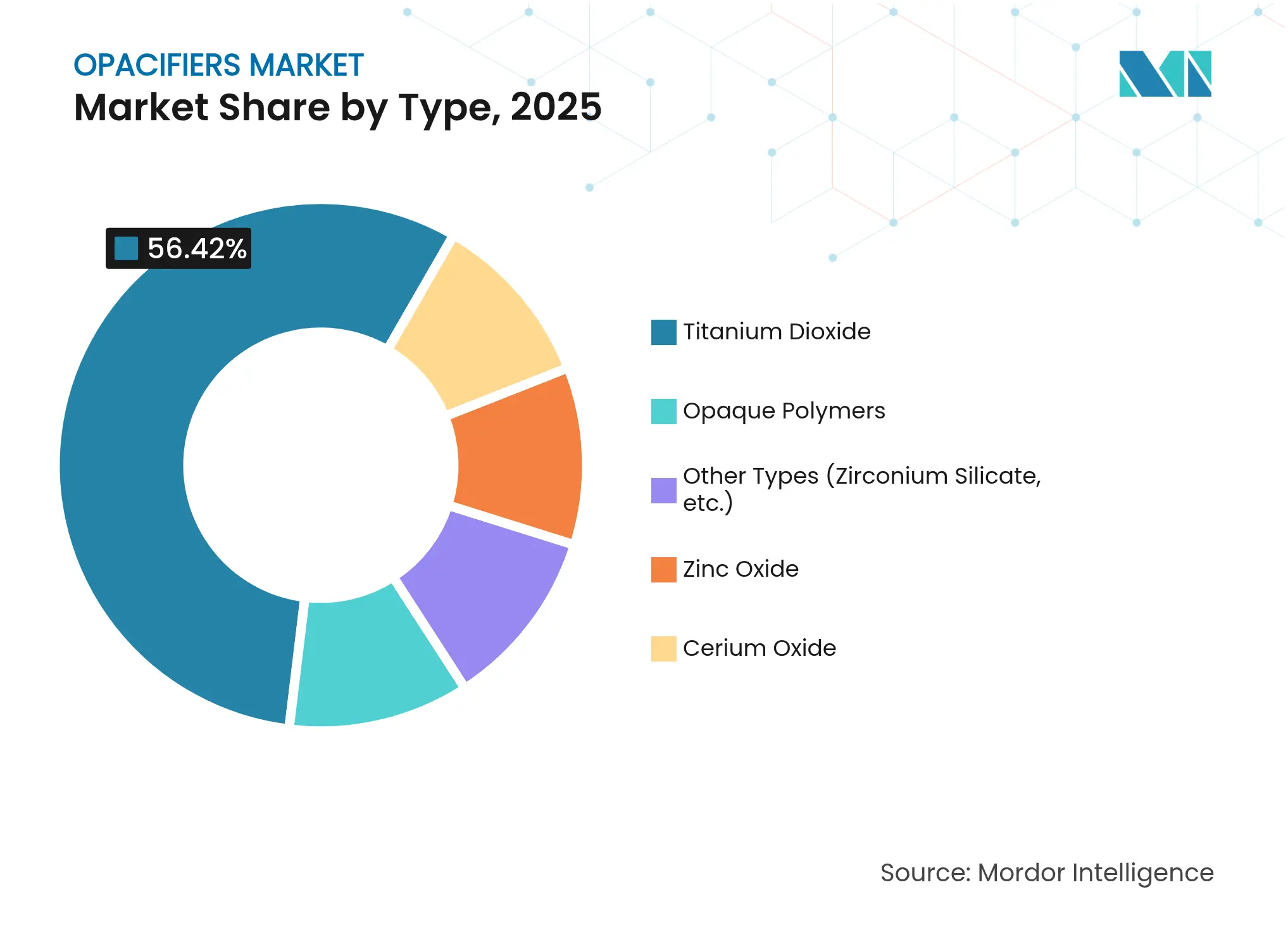

By Type: Titanium Dioxide Dominance Faces Alternative Innovation

Titanium dioxide held a 56.42% opacifier market share in 2025, thanks to its superior hiding power and cost efficiency. Demand remains robust across architectural coatings and plastics, but regulatory attention fosters experiments with cerium, zinc, and polymeric replacements. Opaque polymers are the fastest-growing category at 5.08% CAGR, bolstered by water-based formulation compatibility and lower density that improves yield. Zinc-oxide composites increasingly serve multifunctional sunscreens, illustrating how a pigment can merge opacity and UV defence in a single mineral package.

Alternative minerals nevertheless face technical and economic hurdles. Calcium carbonate struggles with tint strength; iron oxides add unwanted hues; barium sulfate pushes density and cost. Consequently, hybrid formulating is becoming routine, and suppliers with broad portfolios capture incremental wallet share. TiO₂ producers respond by introducing surface-modified grades such as Chemours’ Ti-Pure TS-6706, a TMP- and TME-free variant targeting low-VOC coatings. The dynamic underscores how type diversification reshapes competitive strategy across the opacifiers market.

Note: Segment shares of all individual segments available upon report purchase

By Form: Masterbatch Processing Gains Momentum

Powder remains the primary form, representing 61.85% of the opacifiers market size in 2025. Its versatility, easy storage, and established metering infrastructure suit batch and continuous processes. Masterbatch, however, delivers the strongest growth at 4.92% CAGR because it simplifies dispersion, cuts dust, and supports compounders seeking leaner inventories. Polymer-coated TiO₂ masterbatches reduce dispersion defects in extrusion and injection moulding, boosting finished-part gloss.

Development focus is shifting toward customised form factors that match downstream processing conditions. For additive manufacturing, slurry viscosity and photo-reactivity dictate pigment morphology; pigment suppliers now offer ready-to-print pastes tailor-made for 385 nm laser curing. In compound plastics, pelletised concentrates lower energy requirements by shortening melt-mix cycles. These innovations deepen partnerships between pigment makers and masterbatchers, broadening the value proposition inside the opacifiers market.

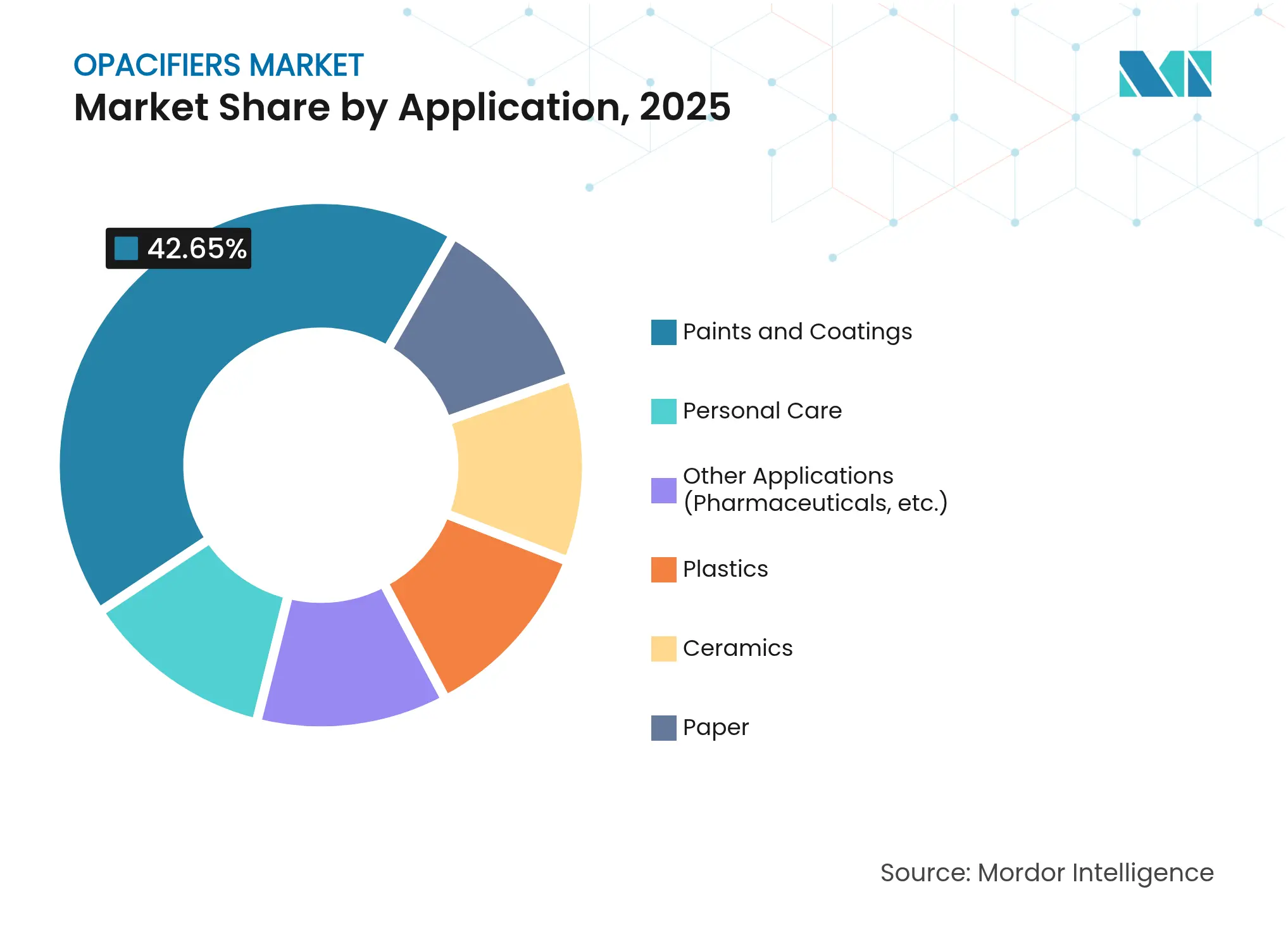

By Application: Personal Care Complexity Drives Innovation

Paints and coatings dominated the opacifiers market size at 42.65% in 2025, reflecting their scale in infrastructure and OEM segments. Yet personal care, with a forecast 5.03% CAGR, is strategically critical because it drives additive functionality and regulatory scrutiny. Sunscreens, colour cosmetics, and skincare demand particles that mask base-colour variability, deliver SPF, and disperse smoothly in water or oil phases. Clean-beauty badges spur interest in mineral or bio-based systems, accelerating zinc and starch-derived solutions. Ceramics, including additive-manufactured parts, continue to grow, especially for aerospace heat shields that require opacity at extreme temperatures.

Regulatory convergence forces cross-application learning. Pharmaceutical dosage forms must retain tablet whiteness without titanium dioxide, an outcome still technologically elusive. Personal-care formulators therefore function as pilot users for new chemistries, incentivising fast iteration cycles that later migrate to other end uses. The interaction between high-volume commodity coatings and high-growth, high-margin personal care exemplifies the balanced demand matrix that stabilises the opacifiers market.

Note: Segment shares of all individual segments available upon report purchase

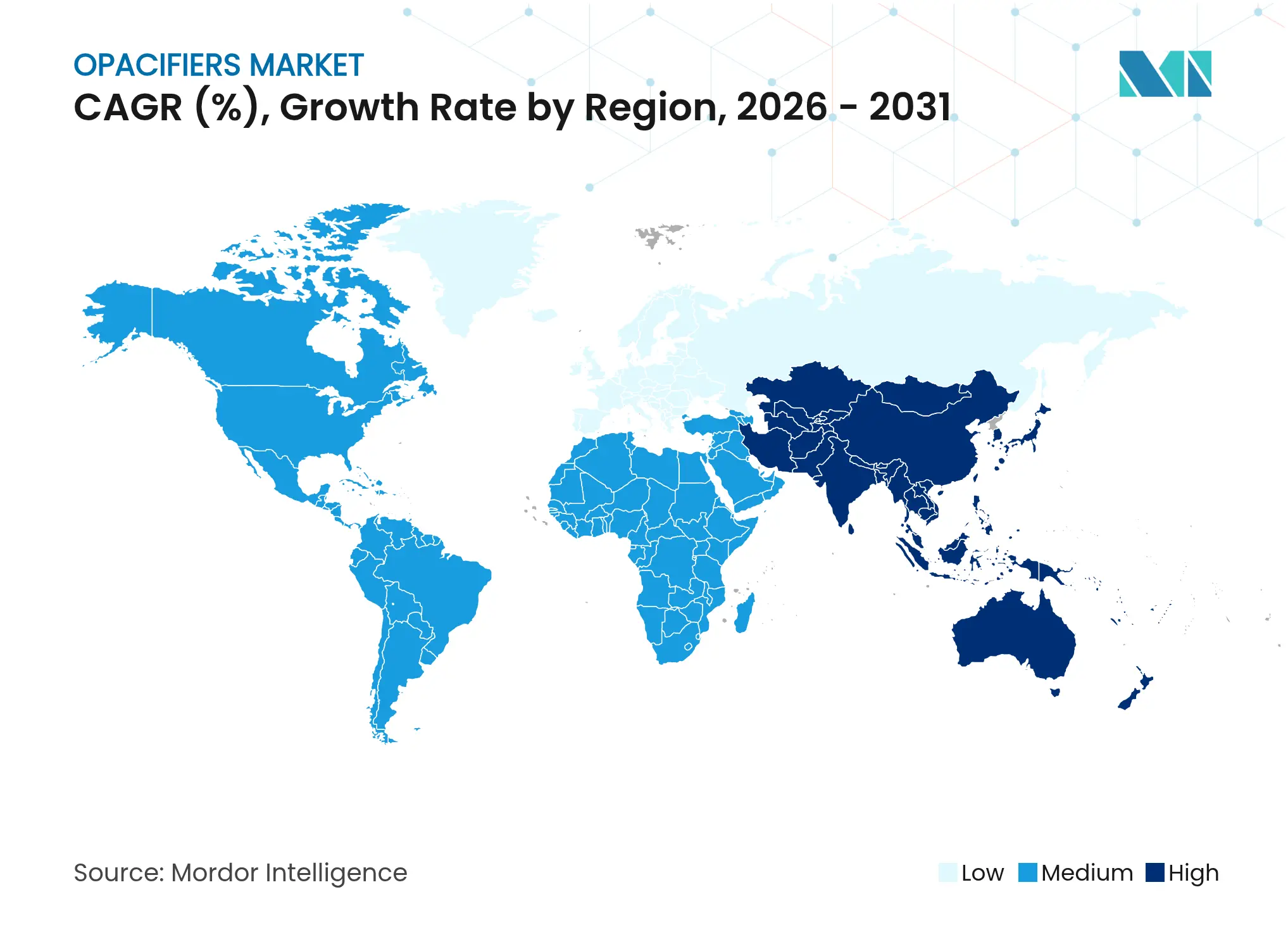

Asia-Pacific retained 45.98% of the global opacifiers market share in 2025 and is projected to post a 4.88% CAGR to 2031. China drives scale through integrated TiO₂ complexes, but supply risk surfaced when Beijing restricted antimony exports, causing a triple-digit price leap that reverberated through pigments and battery metals simultaneously. The region’s cost-competitive extraction and conversion base underpins its leadership, yet dependence on critical mineral logistics remains a strategic vulnerability.

North America reflects a mature but innovation-centric theatre. Pharmaceutical reformulation following TiO₂ scrutiny dominates laboratory pipelines, and personal-care firms adopt mineral-only claim strategies that favour zinc and cerium systems. The United States is reassessing domestic antimony mining after two decades of inactivity, aiming to insulate strategic supply chains.

Europe navigates the strictest regulatory landscape. Nanomaterial disclosure rules under EC 1223/2009 and sustainable-ink directives have already nudged converters toward bio-derived or transparent solutions, marginally reducing overall mineral intensity.

South America, and the Middle East and Africa deliver incremental volume through infrastructure and packaging expansion, but supply-chain constraints and evolving standards temper immediate upside. Across regions, regulatory cadence and resource security set the tempo for growth trajectories within the opacifiers market.

Market Concentration

The opacifiers market features moderate fragmentation as leading players pursue mine-to-pigment integration to shelter margins from volatile ores. Innovation pipelines span surface-modified rutile grades that lift hiding efficiency by up to 15%, polymer-composite zinc-oxide systems offering SPF without greasiness, and nanoscale cerium-oxide dispersions for UV-stable plastics. Patent filings at the USPTO underscore fresh approaches to improve paint hiding with lower pigment-volume concentration, saving formulators raw-material costs. Technical-ceramics and additive-manufacturing niches tilt toward partnership models in which pigment suppliers co-develop formulations with printer OEMs and end-use engineers. Collectively, these patterns affirm a landscape where scale, resource security, and research and development dexterity jointly define long-term positioning.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts (Value)

6. Competitive Landscape

7. Market Opportunities and Future Outlook

The opacifiers market report includes:

Strategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

Unlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

Wealth Management Intelligence for the Middle East

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.