Market Overview

| Study Period | 2020 - 2031 |

|---|---|

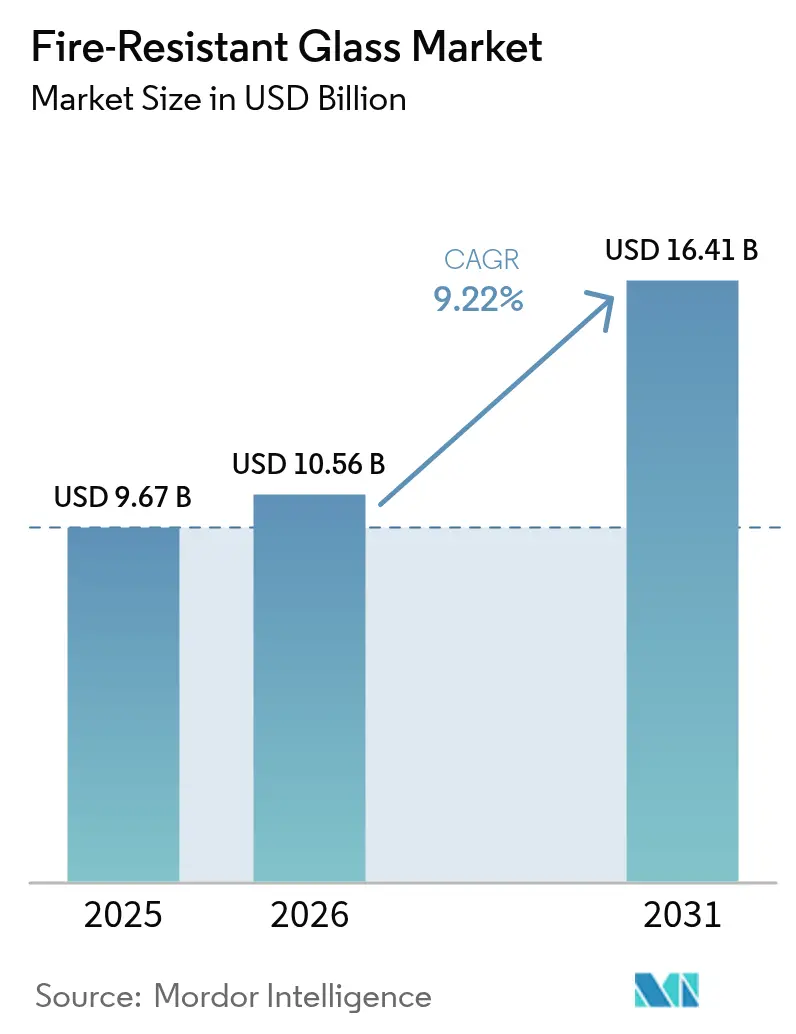

| Market Size (2026) | USD 10.56 Billion |

| Market Size (2031) | USD 16.41 Billion |

| Growth Rate (2026 - 2031) | 9.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fire-Resistant Glass Market Analysis by Mordor Intelligence

The Fire-Resistant Glass Market size is expected to grow from USD 9.67 billion in 2025 to USD 10.56 billion in 2026 and is forecast to reach USD 16.41 billion by 2031 at 9.22% CAGR over 2026-2031. Expanding high-rise construction across Asia-Pacific and the Middle East, the tightening of global fire-safety codes, and the rapid commercialisation of hybrid smart-tint fire-resistant glazing all underpin this growth trajectory. Regulatory momentum, led by China’s GB 55037-2022 standard and the UAE Fire and Life Safety Code 2018, is eliminating non-compliant products and elevating demand for certified solutions. Construction incentives such as Section 179 of the U.S. Internal Revenue Code add a financial pull, while insurance premium discounts for fire-rated glazing continue to unlock retrofit opportunities. On the technology side, manufacturers are moving quickly from single-function panes to value-added laminates that integrate fire protection, daylight control, and energy efficiency—an evolution that widens margins and differentiates supply.

Key Report Takeaways

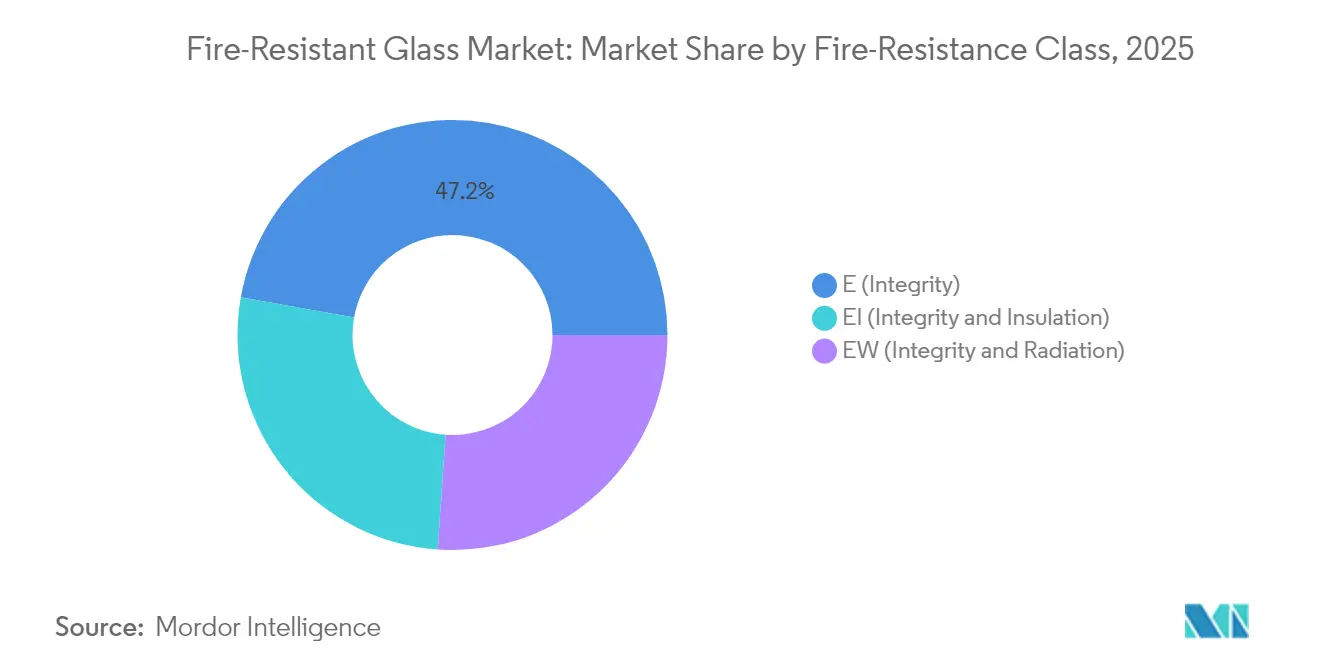

- By fire-resistance class, E (Integrity) glass led with 47.20% revenue share in 2025, while EI (Integrity + Insulation) is poised for a 10.11% CAGR through 2031.

- By product type, ceramic solutions captured 39.20% of the fire-resistant glass market share in 2025, whereas gel-filled variants are forecast to grow at 9.92% CAGR.

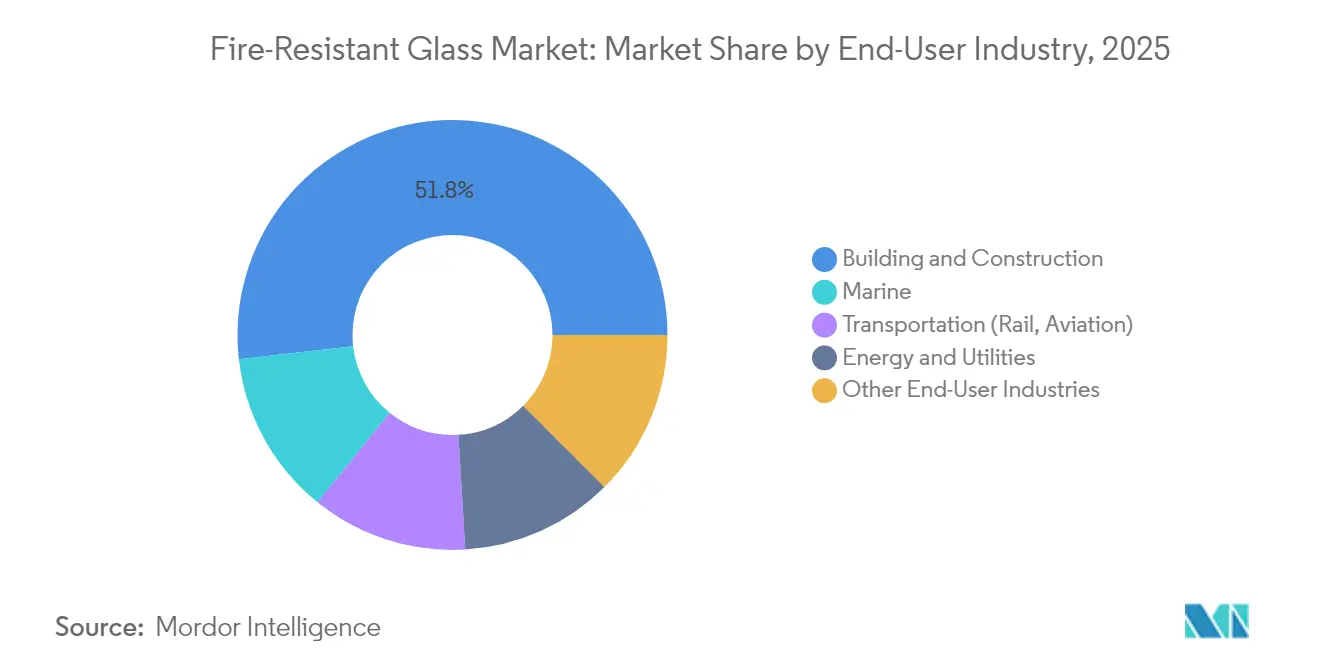

- By end-user industry, building and construction accounted for 51.80% share of the fire-resistant glass market size in 2025; marine applications advance at a 9.38% CAGR to 2031.

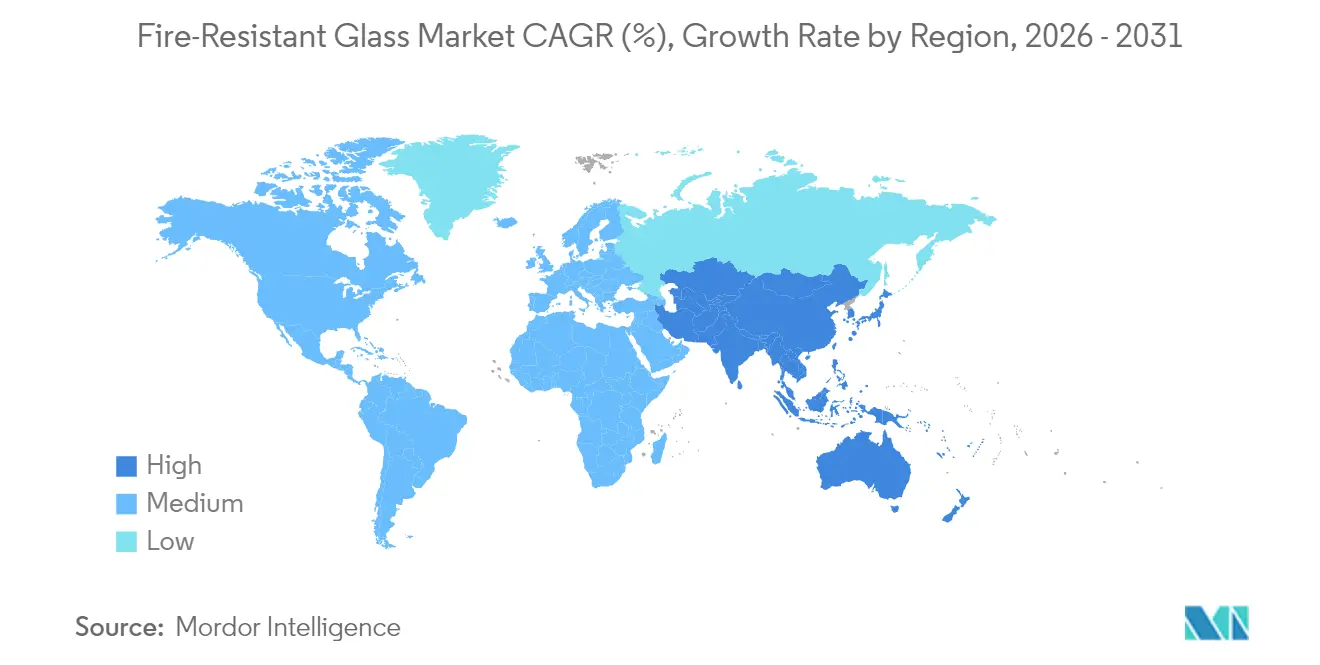

- By geography, North America commanded 31.60% share in 2025, although Asia-Pacific is the fastest-growing region at 9.55% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fire-Resistant Glass Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in high-rise commercial construction in Asia Pacific and Middle East | +2.1% | Asia-Pacific core, Middle East expansion | Medium term (2-4 years) |

| Stricter global fire-safety regulations | +1.8% | Global, with concentration in North America & EU | Short term (≤ 2 years) |

| Insurance incentives for using fire-rated glazing | +0.9% | North America & EU primary markets | Medium term (2-4 years) |

| Hybrid smart-tint and fire-resistant glass innovations | +1.2% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Modular prefab façades need lightweight fire glass | +0.8% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Hydrogen-ready industrial sites demand blast-plus-fire glass | +0.6% | Industrial corridors in North America, EU, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in High-Rise Commercial Construction in Asia-Pacific and Middle East

Rapid vertical urbanisation has elevated fire safety to board-level priority. China’s GB 55037-2022 requires qualified fire-resistant glazing in all new towers above 100 m height, prompting developers to upgrade specification baselines[1]Chinese State Council, “GB 55037-2022 National Fire Prevention Standard,” gov.cn. Dubai’s revised building code, which caps facade glazing area yet demands higher thermal and fire performance, is catalysing premium demand in the Gulf. Developers now seek integrated solutions that meet multiple performance targets in a single pane, enabling suppliers to price above commodity levels while accelerating overall adoption of certified products across the fire-resistant glass market.

Stricter Global Fire-Safety Regulations

The 2024 International Building Code strengthens wall continuity and requires lab-tested glazing assemblies for any rated opening—tightening compliance globally. The UAE “Ten-Point Approach” mandates Civil Defence approvals for facade materials and eliminates lower-grade imports. Similar rule harmonisation in Europe increases cross-border acceptance of certified panes. Together these policies expand the qualified addressable base for the fire-resistant glass market, especially for EI-class products.

Insurance Incentives for Using Fire-Rated Glazing

In North America, insurers are aligning premium schedules with documented life-safety benefits of rated glass. Section 179 allows companies to expense up to USD 1.22 million of qualifying fire-protection equipment in the year of purchase, which improves payback calculations for retrofit projects[2]NFSA, “Section 179 Fire Protection Incentives,” nfsa.org. Insurer-led recognition has moved adoption from reactive compliance toward proactive risk mitigation, creating a retrofit engine that complements new-build demand.

Hybrid Smart-Tint and Fire-Resistant Glass Innovations

Schott’s PYRANOVA Smart combines EI-120 fire performance with switchable tint that modulates daylight and HVAC load, demonstrating where the product roadmap is heading. Developers value reduced glare, lower cooling loads, and code compliance in a single unit, allowing premium price realisation. Similar launches from Saint-Gobain and AGC illustrate a technology arms race that will elevate specification standards in the fire-resistant glass market through 2030.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of certified installers and fabricators | -1.4% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Supply-chain risk for sodium-/boro-silicate feedstock | -0.8% | Global manufacturing hubs | Medium term (2-4 years) |

| Rating-equivalence gaps for multi-material façades | -0.6% | Developed markets with complex building codes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified Installers and Fabricators

Even the most advanced pane loses its rating if incorrectly installed. Rapid construction growth in India, Indonesia, and parts of Africa is outpacing the pool of certified installers, delaying project completions and elevating cost premiums. International suppliers are responding with on-site training programs and turnkey service bundles, yet near-term capacity constraints continue to temper growth in the fire-resistant glass market.

Supply-Chain Risk for Sodium- / Boro-Silicate Feedstock

Borosilicate formulations rely on stable borate supply. Recent consolidation moves—such as Sibelco’s purchase of Strategic Materials in the recycling space—underline the push to secure feedstock and reduce virgin material exposure. Any recurring shortages heighten cost volatility, which in turn leads contractors to delay procurement or seek alternate facade materials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fire-Resistance Class: Integrity Standards Drive Market Evolution

The E class segment headlines the landscape with 47.20% of the fire-resistant glass market size in 2025, firmly positioned as the affordable baseline for compartmentation in office towers and schools. Volume dominance is rooted in simple performance requirements that target flame and smoke containment without thermal-insulation mandates. Upgrading projects often move directly from wired glass to E class panes, ensuring repeat business for incumbents. Yet specification drift toward EI class is accelerating. Post-incident reviews in China and Singapore show that insulation ratings better protect stairwells and refuge floors, nudging architects to embrace EI class despite higher cost.

EI class’s 10.11% CAGR through 2031 reflects this safety-first pivot. As regulatory bodies adopt holistic life-safety metrics, EI-certified panes become indispensable in atria, transportation hubs, and critical infrastructure. Ongoing product innovation such as hydrogel-silicate interlayers that double as acoustic dampers adds multipurpose value, increasing adoption. EW class remains a niche choice where radiant-heat reduction rather than full insulation is required, yet it serves as a mid-price bridge that eases budget constraints on government projects. The upshot is a performance hierarchy that gradually migrates demand from basic to advanced ratings, fortifying the long-term outlook for the fire-resistant glass market.

By Product Type: Ceramic Solutions Lead Technical Innovation

Ceramic glass held 39.20% of the fire-resistant glass market share in 2025 because of its ability to withstand 1 000 °C without optical distortion. Landmark projects such as New York’s super-slender towers rely on transparent ceramics to maintain panoramic views while meeting local fire code. Even so, weight and cost continue to invite alternatives. Laminated systems combine ceramics with intumescent layers to boost impact resistance, edging into security glazing budgets. Tempered solutions remain relevant in less demanding applications but face erosion where EI ratings are mandated.

Gel-filled panes top the growth chart with a 9.92% CAGR outlook. Their 30% weight saving over ceramics is a game changer for unitised prefab facades that aim for zero external mullions. Manufacturers are advancing bio-based gel chemistries that reduce embodied carbon, aligning with green building certifications. Wired glass retains a foothold in institutional retrofits because of familiarity and local code equivalence. Polycarbonate composites address niche transit and defense uses where ballistic resistance and weight are critical. Each material tier occupies clear performance-price coordinates, allowing suppliers to segment the fire-resistant glass market precisely.

By End-User Industry: Construction Dominance Faces Marine Disruption

Building and construction contributed 51.80% to the fire-resistant glass market size in 2025. Code cycles in North America and the EU continuously raise minimum ratings, ensuring ongoing retrofit churn. Hospitals, data centers, and education campuses add steady, specification-driven demand. Energy and utilities remain stable with petrochemical revamps and LNG terminals accounting for periodic spikes. Transportation niches—rail, air, and tunnel segments—value slimline EI-60 panes that combine blast and fire criteria, but overall share stays below 10%.

Marine applications grow fastest at 9.38% CAGR. Offshore platforms, cruise liners, and coastal LNG hubs face stricter SOLAS updates that call for 120-minute integrity with salt-spray durability. California’s revised marine terminal rules require fire-rated glazing in control rooms and cable tunnels, setting a precedent likely to spread to Asia-Pacific yards. Suppliers with Type-approval certificates from class societies are best positioned to capture this upswing, expanding the diversity of the fire-resistant glass market.

Geography Analysis

North America leads the fire-resistant glass market with a 31.60% revenue share in 2025, supported by the 2024 International Building Code, the International Fire Code, and robust insurance incentives. Large retrofit programs in Chicago, New York, and Toronto focus on bringing existing stock to code, while the Section 179 tax deduction sustains private spending on life-safety upgrades. Hybrid smart-tint EI panes are gaining traction as owners pursue both fire and energy targets, raising average selling prices and reinforcing the regional leadership of the fire-resistant glass market.

Europe maintains a mature but innovative profile. Stringent EN 13501 testing, plus the continent’s carbon-pricing regime, steer demand toward low-carbon manufacturing. Saint-Gobain’s hybrid furnace trial that cuts 75% of CO2 emissions exemplifies this alignment and could become a de-facto procurement criterion for EU public projects saint-gobain.com. Niche growth appears in timber-glass composite facades in Scandinavia, which blend fire resistance with renewable materials. European buyers are also early adopters of EI-class plug-and-play curtain wall cassettes, illustrating a preference for complete assemblies versus single panes.

Asia-Pacific is the clear growth engine, expanding at 9.55% CAGR through 2031. China’s national standard, in force since mid-2023, mandates fire-rated glazing for high-rise egress corridors and lift lobbies. India’s National Building Code amendments are following suit, while Indonesia plans to update its 2012 code by 2026. Meanwhile, Dubai and the wider Gulf have raised standard levels after the 2015 Address incident, fuelling demand for EI-120 systems despite hot-climate design challenges. AGC forecasts shipments of high heat-insulating glass to remain resilient in Asia even as overall construction moderates. These developments collectively pull global suppliers toward regional joint ventures and local fabrication, widening the geographic footprint of the fire-resistant glass market.

Competitive Landscape

Competitive intensity is moderate. AGC Inc., Saint-Gobain, and SCHOTT AG command global networks of float lines, coating plants, and distribution hubs. AGC’s architectural glass division posted JPY 329.7 billion net sales in Q3 2024, though profitability slipped in Europe and the Americas because of slower office construction. The firm is pivoting toward Asia-Pacific and specialty EI-class products to restore margins. Saint-Gobain’s 75% CO2-cutting pilot furnace underpins a corporate pledge to become carbon-neutral by 2050, a differentiator in public procurement. SCHOTT continues to invest in borosilicate expertise, promoting PYRANOVA lines that merge acoustic, thermal, and fire performance.

Second-tier players such as Vetrotech Saint-Gobain, Promat, and Pyroguard hold strong regional niches, often specialising in EI-60 and EW-30 ratings tailored to mass-market residential retrofits. Partnerships with facade contractors help them secure early design wins. Start-ups in Europe are testing digital manufacturing for curved EI-glass, while Japanese fabricators experiment with transparent ceramics doped for near-infrared rejection. Overall strategy focuses on integrated performance packages—fire, energy, acoustic, and security—moving the fire-resistant glass market further into premium territory.

Fire-Resistant Glass Industry Leaders

Schott AG

Saint-Gobain

AGC Inc.

Nippon Sheet Glass Co. Ltd

Pyroguard

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Vetrotech, a subsidiary of Saint-Gobain, introduced CONTRAFLAM One at BAU in Munich. The CONTRAFLAM 90-1, part of this range, offers 88% light transmission, is 42% lighter, and reduces emissions by 35% compared to multi-chamber products, setting new industry standards.

- May 2024: AGC Glass Europe, in line with its Carbon Neutrality Roadmap, launched its Low-Carbon Glass range to meet market demand and reduce environmental impact. The company introduced Low-Carbon Pyrobel Glass, a fire-resistant product with significantly lower embodied carbon.

Global Fire-Resistant Glass Market Report Scope

The fire-resistant glass market report includes

By Fire-Resistance Class

| E (Integrity) |

| EW (Integrity and Radiation) |

| EI (Integrity and Insulation) |

By Product Type

| Wired |

| Laminated |

| Ceramic |

| Tempered |

| Gel-filled |

| Polycarbonate and Others |

By End-User Industry

| Building and Construction |

| Marine |

| Transportation (Rail, Aviation) |

| Energy and Utilities |

| Other End-User Industries |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Fire-Resistance Class | E (Integrity) | |

| EW (Integrity and Radiation) | ||

| EI (Integrity and Insulation) | ||

| By Product Type | Wired | |

| Laminated | ||

| Ceramic | ||

| Tempered | ||

| Gel-filled | ||

| Polycarbonate and Others | ||

| By End-User Industry | Building and Construction | |

| Marine | ||

| Transportation (Rail, Aviation) | ||

| Energy and Utilities | ||

| Other End-User Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Fire-Resistant Glass Market size?

The Fire-Resistant Glass Market is valued at USD 10.56 billion in 2026 and is projected to grow steadily through 2031.

Which region leads global demand?

North America holds 31.60% revenue share because of strict code enforcement and retrofit incentives.

Which product segment is growing fastest?

Gel-filled panes are forecast to expand at a 9.92% CAGR between 2026 and 2031.

Why is EI-class glass gaining traction?

EI panes provide both integrity and insulation, aligning with new code requirements for safe evacuation routes in high-rise structures.

Page last updated on: