Personal Care Contract Manufacturing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

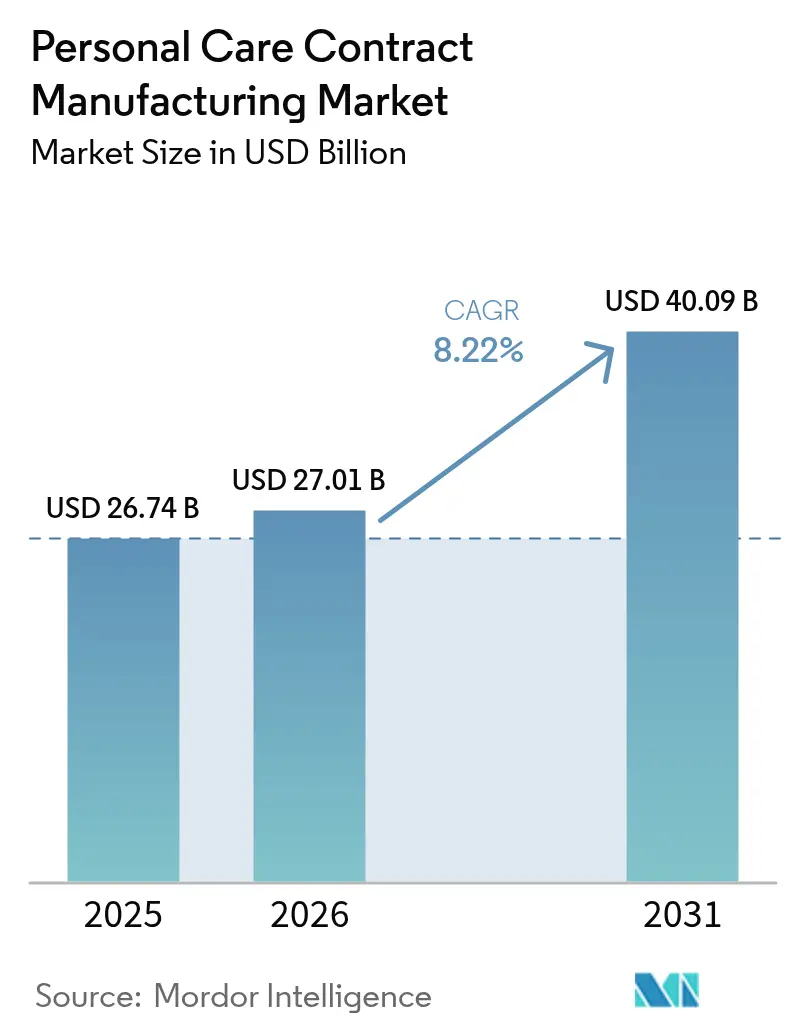

| Market Size (2026) | USD 27.01 Billion |

| Market Size (2031) | USD 40.09 Billion |

| Growth Rate (2026 - 2031) | 8.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Personal Care Contract Manufacturing Market Analysis by Mordor Intelligence

The personal care contract manufacturing market size is projected to expand from USD 26.74 billion in 2025 and USD 27.01 billion in 2026 to USD 40.09 billion by 2031, registering a CAGR of 8.22% between 2026 and 2031. Brand owners are scaling back capital-intensive plants and leaning on external partners for formulation know-how, faster compliance, and speedier product rollouts. Manufacturing services still generate most revenue, yet full-service and turnkey engagements are accelerating as venture-backed direct-to-consumer labels demand bundled solutions. Asia-Pacific anchors capacity expansion because South Korean and Chinese vendors marry low labor costs with vast ingredient ecosystems, allowing them to quote aggressive lead times. Simultaneously, regulatory shifts in Europe on refillable packaging are steering brands toward contract manufacturers that can redesign both formula and primary pack in one engagement.

Key Report Takeaways

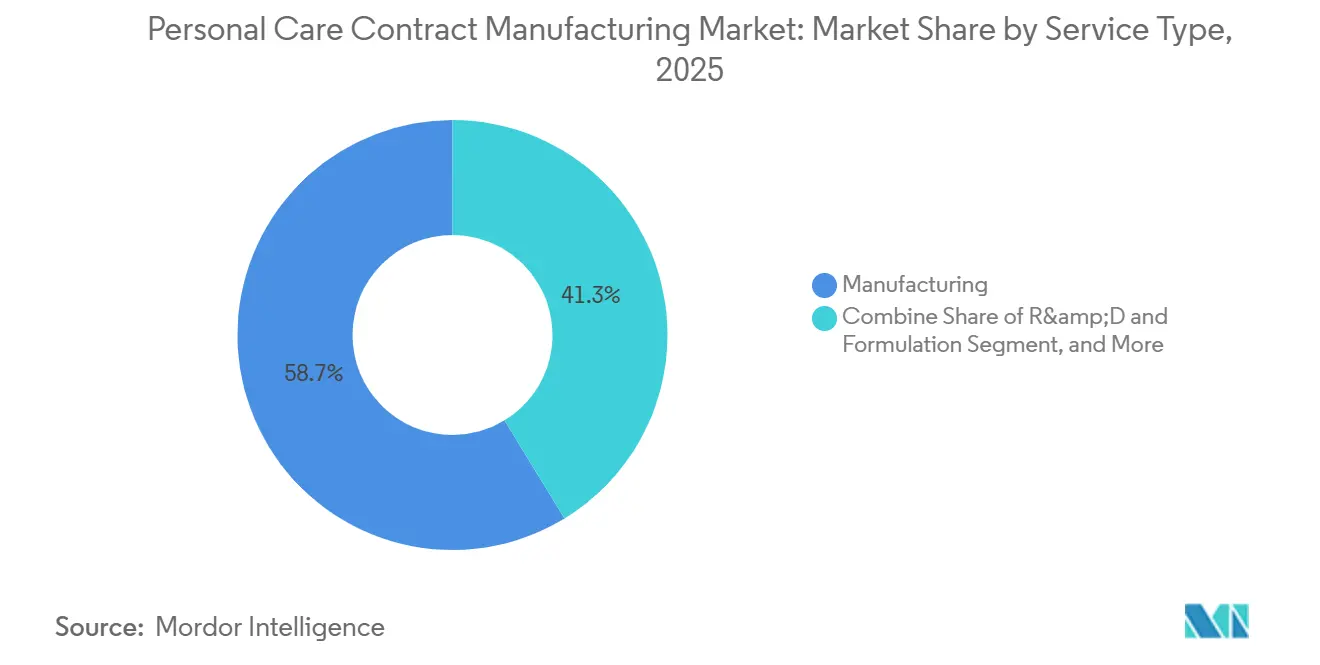

- By service type, manufacturing services led with 58.72% of personal care contract manufacturing market share in 2025, while turnkey and full-service contracts are forecast to rise at an 8.52% CAGR through 2031.

- By product type, skin care commanded 38.18% revenue share in 2025; hair care is projected to grow at an 8.76% CAGR through 2031.

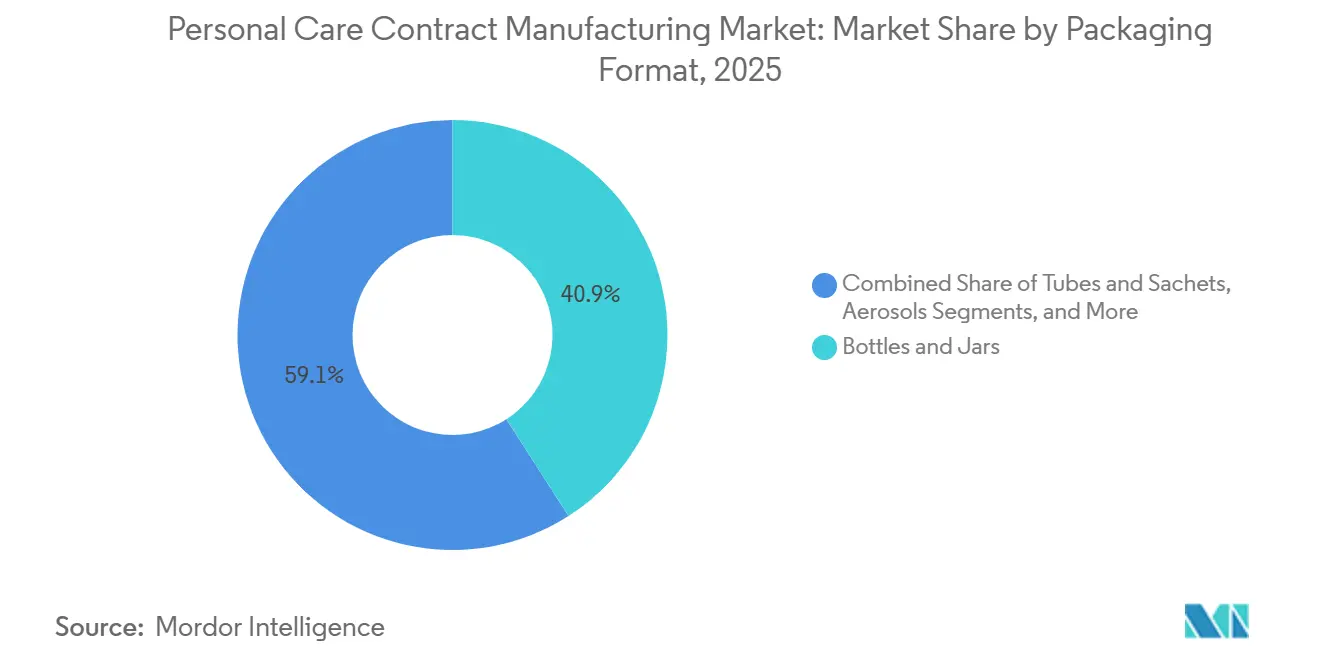

- By packaging format, bottles and jars held 40.93% share in 2025, yet tubes and sachets will deliver the fastest growth at an 8.93% CAGR under European refillability rules.

- By contract manufacturing model, OEM captured 55.64% share in 2025, whereas ODM is expected to expand at an 8.41% CAGR as indie brands license ready-made recipes.

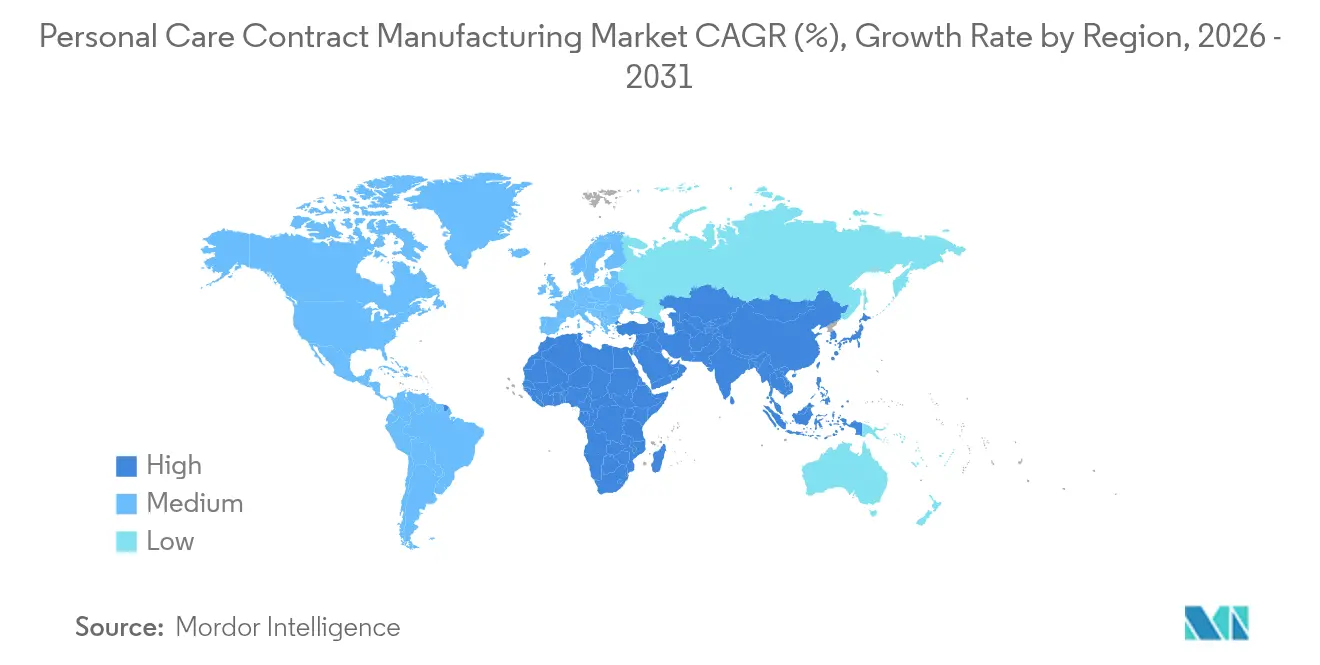

- By geography, Asia-Pacific accounted for 36.91% of personal care contract manufacturing market share in 2025 and should advance at a 9.11% CAGR through 2031 on the back of South Korean and Chinese capacity build-outs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Personal Care Contract Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Evolution of service offerings enables outsourcing focus | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Localization of manufacturing for lead-time and cost advantage | +1.5% | APAC core, spill-over to North America and Europe | Medium term (2-4 years) |

| Surge of indie/DTC brands outsourcing production | +1.6% | North America and Europe, expanding to APAC | Short term (≤ 2 years) |

| Demand for organic and natural formulations | +1.2% | Global, strongest in Europe and North America | Long term (≥ 4 years) |

| AI-driven rapid formulation platforms | +1.4% | North America, Europe, South Korea, Japan | Medium term (2-4 years) |

| Refillable-packaging mandates requiring specialised CM | +1.0% | Europe (primary), North America (emerging) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Evolution of Service Offerings Enables Outsourcing Focus

Contract manufacturers now provide R&D, regulatory filing, and packaging under one roof, freeing brands to invest in marketing instead of fixed assets. The turnkey model compresses launch cycles from a year to only months and transfers working-capital risk to the supplier. Maesa’s Magic Incubator illustrates the appeal, granting USD 35,000 plus lab access to startup brands that have since crossed USD 100 million in annual sales.[1]Maesa, “Magic Incubator 2026 Cohort Announcement,” maesagroup.com ISO 22716 certification and FDA MoCRA registration handled by the vendor shield young labels from compliance pitfalls. As a result, full-service contracts are pacing 8.52% CAGR, well above standalone toll manufacturing.

Surge of Indie and DTC Brands Outsourcing Production

Thousands of venture-funded cosmetic labels launched during the e-commerce boom now hit volume thresholds where outsourcing beats building captive lines. Minimum runs of 5,000–10,000 units align neatly with contract manufacturers’ pilot facilities, sparing founders multimillion-dollar capex. KDC/ONE’s purchase of Maesa’s EMEA arm broadened its small-batch and clean-beauty toolkit, luring digitally native brands that iterate rapidly. The ODM pathway, with a 8.41% CAGR, lets new entrants license proven recipes and swap fragrances or actives to differentiate, shrinking concept-to-shelf times to 6 months.

Localization of Manufacturing for Lead-Time and Cost Advantage

Tariffs, freight hikes, and pandemic-era shipping chaos persuaded brands to nearshore. Kolmar Korea opened a 17,805-square-meter Pennsylvania plant in 2025, cutting U.S. replenishment cycles from 90 to 30 days and dodging 25% tariffs on China-made goods. COSMAX broke ground in Thailand to serve Southeast Asia, aiming to reach 230 million units annually by 2026. Boston Consulting Group calculated that localized production reduces landed cosmetic costs by 8%-15% once freight, tariffs, and inventory carrying charges are factored in.

AI-Enabled Rapid Formulation Platforms

L’Oréal and IBM unveiled a generative-AI engine in 2025 that predicts ingredient interactions and regulatory flags, slicing development timelines from 18 months to under six.[2]L’Oréal, “L’Oréal and IBM Launch AI Platform for Beauty Innovation,” loreal.com Contract manufacturers adopting similar systems win briefs from prestige houses seeking speed without sacrificing safety. Nouryon followed with its BeautyCreations simulator, letting brands model sensorial profiles before lab batches. The result is shorter innovation cycles and lower R&D spend, nudging more projects toward external partners.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory and counterfeit concerns | -1.1% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Raw-material price and supply-chain volatility | -1.3% | Global, with acute pressure in APAC and Europe | Short term (≤ 2 years) |

| In-house capacity expansion by mega beauty brands | -0.9% | North America and Europe | Medium term (2-4 years) |

| Blockchain-based traceability and disclosure pressures | -0.6% | Europe (primary), North America (emerging) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory and Counterfeit Concerns

The FDA’s 2026 draft guidance demands real-time electronic batch records, a heavy IT lift for small and midsize vendors.[3]U.S. Food and Drug Administration, “Draft Guidance for Industry: Access to Records,” fda.gov The agency’s new recall authority, finalized in 2025, further increases liability, nudging some suppliers out of sunscreens and eye-area products. Parallel reforms in Europe banned 23 additional CMR substances, forcing costly reformulations. Counterfeits muddy trust: the WHO estimated that fake cosmetics accounted for 10% of global trade in 2024, and when packaging is copied, legitimate contract manufacturers bear the reputational fallout.

Raw-Material Price and Supply-Chain Volatility

Feedstock swings-exemplified by Dow’s USD 0.05 per pound glycol-ether increase effective January 2025-compress margins and complicate quotation validity. Contract manufacturers must hedge solvent and surfactant exposure or accept periodic re-pricing clauses, a shift that strains downstream relationships. Port congestion and political tensions are creating spot shortages of fragrance oils, palm-derived fatty acids, and glass droppers. Factories without multiple approved vendors risk line stoppages, prompting a strategic pivot toward dual sourcing, buffer inventories, and vendor-managed stocking agreements across the personal care contract manufacturing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type – Turnkey Models Capture Outsourcing Momentum

Manufacturing services contributed 58.72% of personal care contract manufacturing market share in 2025. However, turnkey contracts are scaling fastest, indexing to an 8.52% CAGR as brands off-load formulation, regulatory, and packaging in a single deal. This reallocation lightens working-capital pressure for labels that prioritize influencer campaigns over capital equipment. R&D outsourcing is also up as clean-beauty claims demand sophisticated preservative systems. Platforms such as Nouryon’s BeautyCreations AI demonstrate how predictive modeling trims bench work, a capability that is pulling mid-tier brands toward external labs.

Turnkey suppliers exploit scale by bundling bottles, pumps, and secondary packaging with liquid filling, which enlarges average order values and broadens margin. The personal care contract manufacturing market size derived from full-service contracts is set to widen each year through 2031 as startups and multinational innovation teams alike pivot to variable-cost supply chains. In contrast, pure toll manufacturing grows slowly because it offers limited differentiation and places inventory liability on the brand. ISO and cGMP compliance costs continue to tilt small clients toward partners that already maintain validated systems.

By Product Type: Skin Care Leadership Meets Hair Care Innovation

Skin care dominated revenue with 38.18% in 2025, anchored by prestige serums using encapsulated actives. Hair care is expected to post an 8.76% CAGR, the quickest clip among categories, on the back of sulfate-free cleansers and scalp-serum launches. Unilever, for instance, shifted several shampoo lines to Asian ODMs specializing in coconut-derived surfactants to meet clean-label pledges. Color cosmetics lag due to minimalist makeup trends, yet specialized contract manufacturers still book seasonal palettes for luxury houses.

The personal care contract manufacturing market for hair care is set to expand as peptide-rich scalp tonics cross over from skin care technologies. Contract partners with micro-biome testing labs stand to win those programs. Fragrance and deodorants remain steady but mature; growth skews toward aluminum-free sticks, which require new wax-gel chemistries. Oral care outsourcing stays niche because giants like Colgate-Palmolive largely self-manufacture at scale.

By Packaging Format: Tubes and Sachets Lead Sustainability Transition

Bottles and jars held 40.93% of shipments in 2025, yet tubes and sachets are tracking an 8.93% CAGR through 2031 as European and Californian laws push refill systems. France’s AGEC statute and the EU Packaging and Packaging Waste Regulation obligate 10% reusable cosmetic packs by 2030. Contract manufacturers with in-house extrusion and lamination capabilities land those projects because brands prefer a single partner for both formula and pack engineering.

The personal care contract manufacturing market share expected from tubes and sachets therefore rises in tandem with mandates. Airless pumps grow among preservative-free serums needing oxygen barriers, though their cost keeps them skewed to premium. Aerosols confront propellant and recycling scrutiny but stay essential for dry shampoos. New paperboard sticks debut in solid perfumes and deodorants, calling for filling lines that handle lower-heat substrates.

By Contract Manufacturing Model – ODM Gains Favor With Speed-First Brands

OEMs still accounted for 55.64% of contracts in 2025 because heritage brands control their IP and outsource only production. ODM is growing 8.41% because celebrity labels and influencer startups value six-month launch cycles and pre-validated stability data. Kolmar Korea disclosed that ODM exceeded 60% of its total sales in 2024. COSMAX posted similar ratios, allowing clients to tweak active levels rather than build new emulsions from scratch.

As ODM expands, personal care contract manufacturing market size linked to royalty-bearing formulations becomes more predictable for vendors, allowing better capacity planning. OBM and private-label programs with retailers offer volume but thinner margins. Toll manufacturing remains a fallback for brands undergoing plant shutdowns, yet its strategic value declines because it delivers neither speed nor R&D leverage.

Geography Analysis

Asia-Pacific accounted for 36.91% of the personal care contract manufacturing market share in 2025 and is forecast to grow at a 9.11% CAGR through 2031. South Korea’s COSMAX recorded KRW 319.8 billion (USD 240 million) Q3 2024 revenue, up 15.1% year over year, leveraging libraries that cut development times to six months. Chinese ODM specialists ride domestic demand from Perfect Diary and Florasis, while India attracts new factories to serve the Middle East and Africa. Japan remains niche but premium, focusing on probiotic skin care, whereas Australia emphasizes botanicals native to its biomes.

North America and Europe together generated roughly half of global turnover in 2025. The United States heads revenue, but growth moderates as brands consolidate their vendor footprint. Kolmar Korea’s Pennsylvania plant added 120 million-unit capacity in 2025, slicing replenishment times for East Coast labels. Europe tightens the regulatory screws with refillable-packaging quotas and ingredient bans, nudging contract manufacturers toward investment in mold engineering and high-barrier mono-material packs. Germany leads in natural cosmetics, France in prestige fragrance, and Italy in color-cosmetic compacts.

South America, the Middle East, and Africa remain smaller but rising. Brazil’s domestic houses rely on local fillers for lotions suited to humid climates, while multinationals eye Gulf Cooperation Council hubs for fragrance blending. South Africa’s market is dominated by ethnic hair care lines produced at contract sites near Johannesburg. Nigeria’s potential is sizable, though import dependencies and uneven power infrastructure temper growth.

Competitive Landscape

Innovation and Adaptability Drive Future Success

The top 10 vendors account for about 40% of global revenue, indicating moderate fragmentation. Scale advantages hinge on three assets: a broad formulation catalog, vertical integration into packaging or ingredients, and deep regulatory teams versed in FDA MoCRA and EU CMR lists. Intercos pursued a USD 100-200 million acquisition in 2025 to deepen its hair and skin competencies. KDC/ONE integrated Maesa’s EMEA division, gaining access to clean-beauty test rooms and agile filling lines for influencer launches.

Technology capabilities increasingly split winners from also-rans. L’Oréal’s generative-AI formulation tool sets a new clock speed that contract partners must match or risk losing briefs. COSMAX hired a new vice chairman in 2025 with a remit to scale AI labs and Southeast Asian plants, underscoring the pivot to data-driven innovation.

Mid-tier firms without proprietary tech or ingredient verticality face squeezed margins as mega brands intermittently insource to balance capacity. White-space opportunities persist in scalp health, refillable formats, and Indian nearshoring, arenas where regulatory barriers are still settling and incumbent share is low.

Personal Care Contract Manufacturing Industry Leaders

Fareva Group

COSMAX Inc.

Intercos S.p.A

Kolmar Korea Co., Ltd.

kdc/one

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The FDA released draft guidance mandating instant electronic batch-record access during inspections.

- December 2025: Ashland agreed to buy Pharmachem Laboratories for USD 660 million, adding specialty hair-care actives.

- December 2025: The FDA finalized recall authority that empowers cosmetic product seizures without voluntary corporate cooperation.

- September 2025: Intercos began due diligence on a USD 100–200 million U.S. skin-care asset to widen its stateside reach.

Global Personal Care Contract Manufacturing Market Report Scope

Contract manufacturing in the personal care industry involves companies outsourcing design, formulation, manufacturing, packaging, and related services. This approach allows small business owners to market their personal care products without the hefty investment required to build and operate a manufacturing plant. The report tracks and analyzes the demand for outsourced services ranging from manufacturing and formulation to research and packaging within the personal care industry, all while considering current market trends and dynamics.

The Personal Care Contract Manufacturing Market Report is Segmented by Service Type (R&D and Formulation, Manufacturing, Packaging and Allied Services, and Turnkey/Full-Service Manufacturing), Product Type (Skin Care, Hair Care, Color Cosmetics, Fragrance and Deodorants, Oral Care, and Other Product Type), Packaging Format (Aerosols, Bottles and Jars, Tubes and Sachets, Pumps and Dispensers, Sticks and Roll-ons, and Other Packaging Format), Contract Manufacturing Model (OEM, ODM, OBM/Private Label, and Toll Manufacturing), and Geography (North America, Europe, South America, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| R&D and Formulation |

| Manufacturing |

| Packaging and Allied Services |

| Turnkey / Full-Service Manufacturing |

| Skin Care |

| Hair Care |

| Color Cosmetics |

| Fragrance and Deodorants |

| Oral Care |

| Other Product Type |

| Aerosols |

| Bottles and Jars |

| Tubes and Sachets |

| Pumps and Dispensers |

| Sticks and Roll-ons |

| Other Packaging Format |

| OEM |

| ODM |

| OBM / Private Label |

| Toll Manufacturing |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Service Type | R&D and Formulation | |

| Manufacturing | ||

| Packaging and Allied Services | ||

| Turnkey / Full-Service Manufacturing | ||

| By Product Type | Skin Care | |

| Hair Care | ||

| Color Cosmetics | ||

| Fragrance and Deodorants | ||

| Oral Care | ||

| Other Product Type | ||

| By Packaging Format | Aerosols | |

| Bottles and Jars | ||

| Tubes and Sachets | ||

| Pumps and Dispensers | ||

| Sticks and Roll-ons | ||

| Other Packaging Format | ||

| By Contract Manufacturing Model | OEM | |

| ODM | ||

| OBM / Private Label | ||

| Toll Manufacturing | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is the personal care contract manufacturing market expected to grow through 2031?

It is projected to register an 8.22% CAGR from 2026 to 2031, climbing to USD 40.09 billion by the end of the period.

Which segment is expanding quickest within outsourced services?

Turnkey and full-service contracts, advancing at an 8.52% CAGR as brands favor end-to-end solutions.

Why are tubes and sachets gaining popularity in beauty packaging?

European and Californian reuse mandates push brands toward refillable and single-dose packs, driving tubes and sachets at an 8.93% CAGR.

What drives the surge in outsourcing by indie beauty labels?

Indie and direct-to-consumer brands outsource to save capex and because ODM libraries let them launch new products in six months.

Which region leads growth in contract manufacturing capacity?

Asia-Pacific, projected to rise at a 9.11% CAGR, powered by South Korean and Chinese suppliers scaling ODM lines.

Page last updated on: