Veterinary Infusion Pumps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

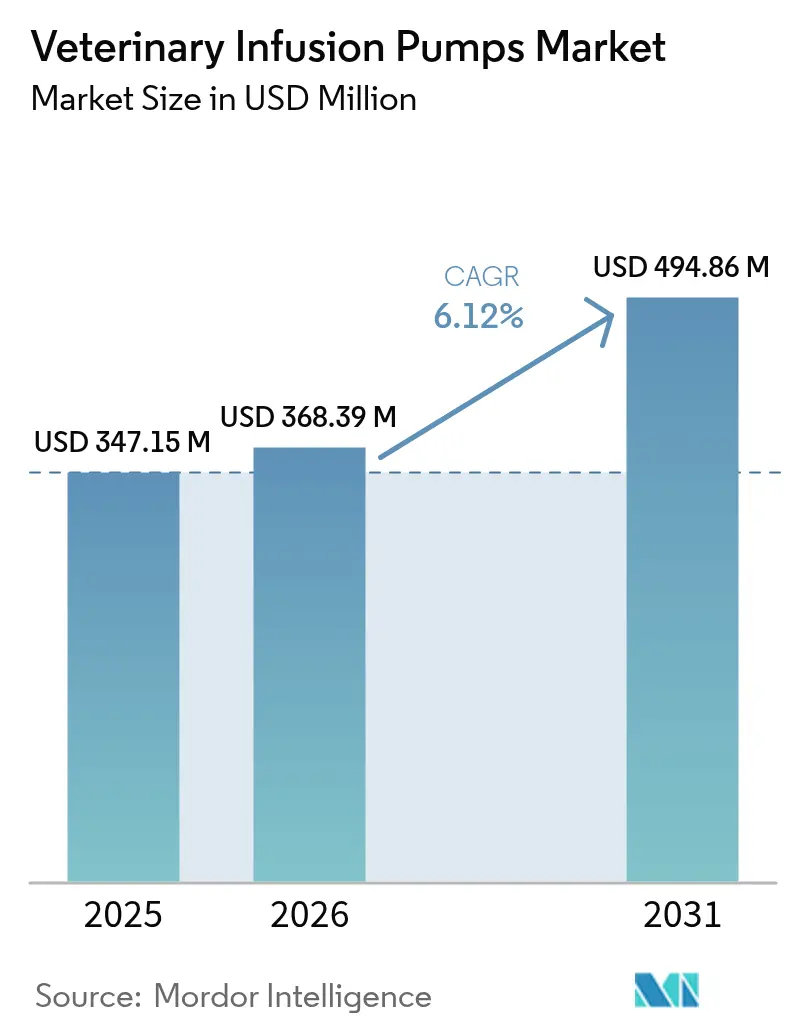

| Market Size (2026) | USD 368.39 Million |

| Market Size (2031) | USD 494.86 Million |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Infusion Pumps Market Analysis by Mordor Intelligence

The Veterinary Infusion Pumps market size is expected to grow from USD 347.15 million in 2025 to USD 368.39 million in 2026 and is forecast to reach USD 494.86 million by 2031 at 6.12% CAGR over 2026-2031.

Uptake is propelled by the humanisation of pets, rapid specialty-clinic expansion, and the migration of human-grade smart-pump technology into animal health settings. Growing chronic-disease prevalence in dogs and cats, tighter dosing-accuracy regulations, and AI-enabled devices that auto-adjust flow rates are further accelerating adoption. At the same time, supply-chain localisation, especially for semiconductors and PTFE tubing, is reinforcing manufacturers’ capital outlays, while stringent FDA recall activity is reshaping product-launch timelines. Competitive differentiation now revolves around integrated drug libraries, remote-monitoring connectivity and veterinary-specific user interfaces, features that are fast becoming baseline rather than premium.

Key Report Takeaways

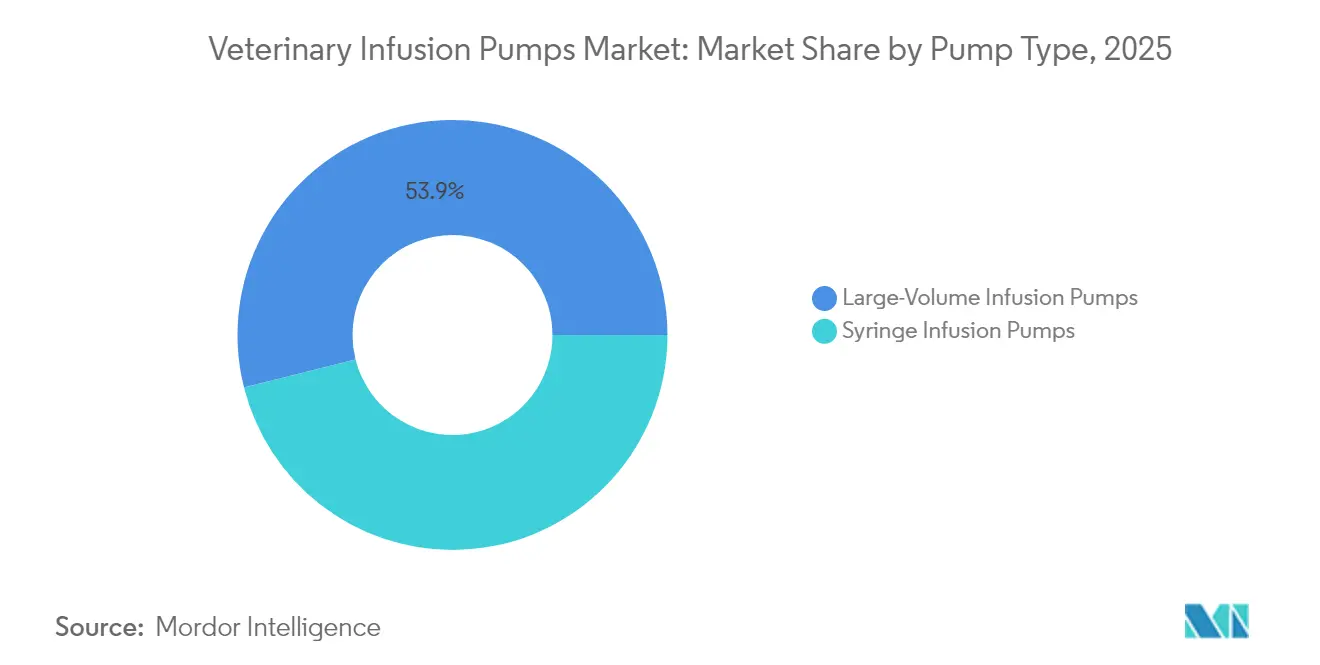

- By pump type, large-volume devices commanded 53.92% of the veterinary infusion pumps market share in 2025, whereas syringe pumps are poised to grow at 8.78% CAGR through 2031.

- By animal type, companion animals led with 56.15% revenue share of the veterinary infusion pumps market in 2025; the same segment is projected to advance at a 9.62% CAGR to 2031.

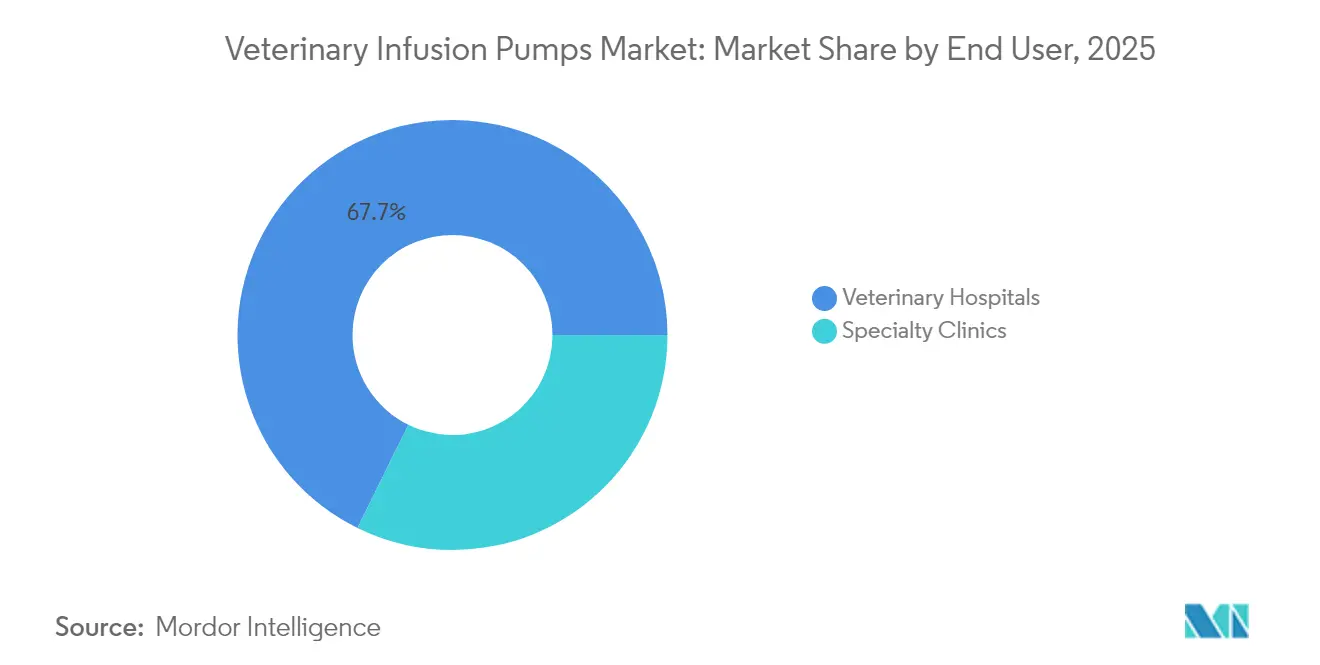

- By end user, veterinary hospitals held 67.72% share of the veterinary infusion pumps market size in 2025, while specialty clinics record the fastest forecast CAGR at 10.62%.

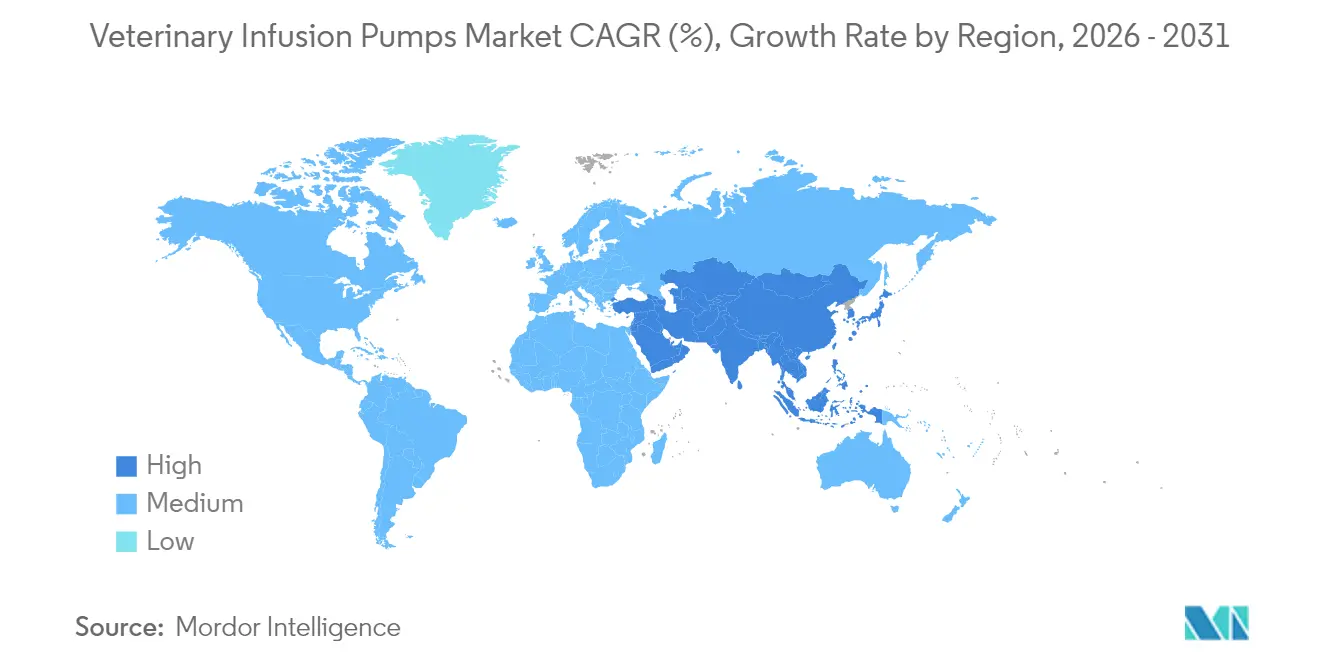

- By geography, North America retained 38.89% share of the veterinary infusion pumps market in 2025; Asia-Pacific is on track for the highest regional CAGR of 13.48% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Infusion Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising companion animal ownership & health spend | +1.8% | North America, Europe | Medium term (2-4 years) |

| Increasing incidence of chronic & critical conditions | +1.2% | Global | Long term (≥ 4 years) |

| Technological advances in pump design | +1.5% | North America, Europe, expanding to APAC | Short term (≤ 2 years) |

| Growth of specialty veterinary clinics | +1.1% | North America, Europe | Medium term (2-4 years) |

| Adoption of remote monitoring & telehealth | +0.7% | North America, emerging APAC | Medium term (2-4 years) |

| Shift to minimally invasive, home-based therapy | +0.3% | Developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Companion Animal Ownership and Health Spending

Pet owners now mirror human-health behaviours, channelling record budgets into sophisticated veterinary care. In North America and Europe, insurers increasingly reimburse infusion-based oncology and renal protocols, softening the cost barrier for advanced devices.[1]Food and Drug Administration, “Medical Device Recalls,” fda.gov Demographic shifts toward smaller households intensify emotional bonds with pets, translating into higher willingness to finance long-term treatments delivered via smart pumps. Drug formulary expansion for animals has increased therapy complexity, anchoring the veterinary infusion pumps market in routine practice. Clinics therefore equip multiple treatment rooms with networked pumps to manage a growing caseload of geriatric pets requiring multi-hour drips.

Increasing Incidence of Chronic and Critical Conditions in Animals

Longer lifespans reveal endocrine, oncologic and gastrointestinal diseases that mandate precise multi-day infusions. FDA conditional approval of PANOQUELL-CA1 for canine pancreatitis reinforces intravenous therapy’s role in emergent care. Similar approvals are spurring device upgrades as dose-error-reduction software becomes a compliance necessity. On the livestock front, intensive farming heightens metabolic disorders, elevating demand for rugged, high-volume pumps capable of simultaneous multi-species dosing, a niche that specialised vendors are capturing.

Technological Advancements in Infusion Pump Design

Next-generation devices integrate AI algorithms that modulate flow rates based on real-time vitals, cutting adverse-event risk. Large manufacturers have ported wireless connectivity, drug libraries and occlusion-sensing from human-care portfolios, shrinking learning curves inside clinics. Regulatory insistence on data logs, now required in FDA submissions, accelerates adoption of cloud-enabled pumps. As firmware updates roll out, service contracts create sticky revenue streams, deepening competitive moats in the veterinary infusion pumps market.[2]Terumo Corporation, “Annual Integrated Report 2025,” terumo.com

Growth of Specialty Veterinary Clinics

Emergency and critical-care centres are scaling rapidly; each new build typically budgets 8–12 smart pumps for surgery, ICU and oncology suites. UK-based Dick White Referrals’ GBP 15 million expansion typifies this capital-intensive trend, nearly tripling infusion capacity.[3]Inside Media Limited, “Dick White Referrals Completes £15 Million Expansion,” insidermedia.com Consolidators standardise equipment lists across networks, enabling volume discounts that squeeze independents but lift unit shipments for leading OEMs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial and maintenance costs | -1.2% | Global, especially emerging markets | Short term (≤ 2 years) |

| Limited insurance reimbursement | -0.8% | Global | Medium term (2-4 years) |

| Electronic-component supply disruptions | -0.6% | Global, acute in APAC | Short term (≤ 2 years) |

| Heightened regulatory scrutiny | -0.4% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial and Maintenance Costs

Smart pumps priced at USD 6,000–9,000 place strain on small practices. Annual calibration, software licensing and staff upskilling lift total cost of ownership by 18–22% over five years, slowing penetration in Latin America and Southeast Asia. Vendors are piloting pay-per-infusion models, but uptake remains limited. Capital expenditure requirements for advanced infusion systems create significant barriers for smaller veterinary practices, particularly in emerging markets where practice economics differ substantially from developed regions. The economic pressure intensifies as regulatory compliance requirements drive up manufacturing costs, with FDA Quality Management System Regulation amendments effective February 2026 adding additional compliance burdens that manufacturers will likely pass through to customers.

Lack of Insurance Reimbursement for Veterinary Procedures

With pet-insurance penetration below 5% in most markets, owners shoulder direct costs. Absence of standard reimbursement codes for infusion therapies curbs demand elasticity, particularly in price-sensitive segments. Insurance coverage limitations for advanced veterinary procedures create direct demand constraints for sophisticated medical equipment, as cost-conscious pet owners may opt for less expensive treatment alternatives when facing significant out-of-pocket expenses. The absence of standardized reimbursement protocols for specific infusion therapies reduces predictable revenue streams that typically justify major equipment purchases in human healthcare settings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pump Type: Syringe Pumps Drive Precision Medicine

Syringe devices are projected to log 8.78% CAGR, outpacing large-volume units that held 53.92% share in 2025. Precision dosing for oncology and critical-care boluses is accelerating upgrades, and drug-library integration ensures safe cross-species calculations. Consequently, the veterinary infusion pumps market size for syringe models is set to climb sharply between 2026 and 2031. Large-volume pumps remain indispensable for hydration and total parenteral nutrition, but the innovation spotlight now sits squarely on smart syringe variants embedded with AI-driven flow-control logic.

Flexibility in handling micro-litre flows without compromising accuracy is converting specialist surgeons and internists alike. Meanwhile, refurbished large-volume units are shifting into cost-conscious segments, keeping overall unit volumes stable but constraining premium pricing. Competitive intensity in this slice of the veterinary infusion pumps market remains moderate as firmware ecosystems rather than hardware specs grow to define user preference.

By Animal Type: Companion Animals Fuel Expansion

Companion animals generated 56.15% of 2025 revenue and are on course for 9.62% CAGR, making them the clear locomotive of the veterinary infusion pumps market size through 2031. Millennials perceive pets as family, financing prolonged chemo and renal therapies that depend on continuous infusion. Dogs alone account for nearly two-thirds of procedures requiring pumps, with feline oncology close behind.

Public-health drives to reduce antibiotic use in livestock are nudging farms toward precision dosing delivered via automated pumps, though capital constraints temper uptake. Equine sports medicine is surfacing as a niche where high-pressure syringe units fetch premium prices, diversifying revenue. Overall, the veterinary infusion pumps market share remains tilted toward dogs and cats, yet emerging large-herd applications signal a second growth wave.

By End User: Specialty Clinics Lead Growth Trajectory

Veterinary hospitals held 67.72% share in 2025, yet specialty and emergency clinics will post an 10.62% CAGR to 2031, reflecting case-mix complexity that justifies multi-pump procurement. Corporate chains mandate uniform equipment standards, creating predictable demand spikes each time a new hub opens. Consequently, the veterinary infusion pumps market size for specialty clinics is projected to expand faster than any other end-user group over the forecast horizon.

Teaching hospitals and referral centres embed pumps in anaesthesia, oncology and ICU suites, pushing per-facility installed bases beyond 20 units. Independent practices increasingly lease pumps to preserve cashflow, enabling tier-two OEMs to penetrate via flexible financing. These shifts collectively redeploy market share toward vendors with coordinated service networks and rapid swap-out policies.

Geography Analysis

North America captured 38.89% of 2025 revenue, underpinned by the world’s highest pet-care spend and mature livestock sectors. The United States alone accounts for more than four in every ten pumps sold, driven by widespread insurance adoption and clinical familiarity with human-grade devices. However, growth is tapering to mid-single digits as replacement cycles rather than first-time installs dominate. Canada mirrors these dynamics on a smaller scale, while Mexico is witnessing gradual modernisation of urban clinics.

Asia-Pacific is the fastest-growing theatre with a 13.48% CAGR through 2031, and it is forecast to eclipse Europe in unit shipments before the decade ends. China’s booming middle class treats pets as status symbols, sparking a surge in high-acuity veterinary hospitals fitted with smart pumps. Japan’s ageing pet population requires chronic-disease infusions, and Australia’s well-developed referral network sustains steady upgrades. India’s dairy sector seeks large-volume pumps for mastitis management, pushing diversified demand across species.

Europe sits between the two extremes, maintaining solid but unspectacular growth. Stringent EU animal-welfare regulations, especially on antimicrobial stewardship, necessitate precision dosing in cattle and swine, keeping the veterinary infusion pumps market engaged. Germany, France and the United Kingdom lead procurement, while Eastern European clinics are early in the adoption curve and thus represent a latent upswing. Brexit-related customs friction has marginally lengthened delivery times but is prompting distributors to set up continental inventory hubs, enhancing long-term resilience.

Competitive Landscape

The veterinary infusion pumps market remains moderately consolidated. Human-device giants such as B. Braun and ICU Medical leverage legacy platforms, bundling veterinary consumables to cement client lock-in. Yet repeated FDA recalls have dented confidence, opening channels for niche players like GradyVet that design species-specific cassettes.

Strategic acquisitions define the current chessboard: Patterson Companies’ 2024 purchase of Infusion Concepts instantly boosted its critical-care portfolio in the United Kingdom, signalling broader cross-border consolidation. OEMs are increasingly bundling pumps with cloud analytics, reinforcing aftermarket software revenue. Meanwhile, Asian entrants offer cost-competitive smart pumps, forcing incumbents to defend share through extended warranties and in-clinic training.

Intellectual-property barriers are rising as AI-driven flow-control algorithms become patent protected. Firms with deep software teams gain an edge, while hardware-centric rivals risk commoditisation. The regulatory gauntlet also acts as a moat: companies with ISO-13485-aligned plants can certify revisions faster, translating compliance agility into market agility. Overall, differentiation now hinges on ecosystem breadth rather than standalone hardware specs.

Veterinary Infusion Pumps Industry Leaders

Burtons Medical Equipment Ltd

Heska Corporation

Avante Animal Health

Digicare Biomedical

B. Braun SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Mississippi State University completed USD 18 million expansion of veterinary clinical facilities, including new cattle handling facility, farm animal hospital, and renovated equine hospital with state-of-the-art medical equipment, reflecting continued investment in veterinary education infrastructure.

- November 2024: Scandinavian ChemoTech’s Animal Care division has announced a new milestone with the sale of its vetIQure TSE device and treatment kits to Christoph Sonntag Veterinary Practice in Germany. Specializing in the treatment of domestic animals—particularly dogs and cats—this clinic becomes the latest in Europe to integrate Animal Care’s advanced technology into its services.

- November 2024: National law firm Mills & Reeve has successfully advised Yorkshire-based veterinary supplier Infusion Concepts Ltd. on its acquisition by U.S.-based healthcare distribution leader Patterson Companies Inc. This strategic guidance played a key role in facilitating Infusion Concepts' transition under the ownership of Patterson’s U.K. animal health arm, National Veterinary Services Limited (NVS). The deal enhances Patterson’s infusion and critical care portfolio for veterinary professionals in the U.K. and beyond, while spotlighting Mills & Reeve’s expertise in cross-border M&A transactions in the healthcare sector.

- October 2024: - Patterson Companies, a prominent distributor in the dental and animal health sectors, has announced two significant acquisitions aimed at strengthening its animal health division. The company’s U.K. subsidiary, National Veterinary Services Limited (NVS), is set to acquire Infusion Concepts Ltd., a leading provider of infusion, drainage, and critical care products for veterinary professionals. Simultaneously, Patterson is expanding its footprint in the United States with the acquisition of Mountain Vet Supply, further enhancing its distribution capabilities and product offerings.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the veterinary infusion pumps market as the annual revenue generated from newly manufactured volumetric and syringe pumps that deliver fluids, nutrients, or medications to companion and production animals in clinical settings. According to Mordor Intelligence, the market is valued at USD 347.15 million in 2025 and should reach USD 475.78 million by 2030.

Scope exclusion: laboratory research pumps used solely for rodent experimentation are not counted.

Segmentation Overview

- By Type

- Large-volume Infusion Pumps

- Syringe Infusion Pumps

- By Animal Type

- Companion Animals

- Dogs

- Cats

- Livestock

- Bovine

- Swine

- Poultry

- Other Animal Type

- Companion Animals

- By End User

- Veterinary Hospitals

- Specialty Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed small-animal surgeons, mixed-practice veterinarians, and procurement heads across North America, Europe, and Asia-Pacific. These conversations verified maintenance cycles, feature preferences, and regional price dispersion, filling gaps that secondary sources could not address.

Desk Research

We began with datasets from bodies such as the American Pet Products Association, Eurostat livestock statistics, and USDA Veterinary Services, which clarify the treated-animal pool. Customs HS codes revealed shipment trends, while peer-reviewed articles in the Journal of Veterinary Emergency & Critical Care explained flow-rate norms that influence pump demand. Company 10-Ks, investor decks, and news archives accessed through D&B Hoovers and Dow Jones Factiva added average selling-price clues. These sources illustrate only a portion of the larger document trail tapped for desk work.

Market-Sizing & Forecasting

A top-down construct starts with the treated-animal pool by species, multiplies pump penetration per surgical and critical-care station, and layers customs flow data to approximate global shipments. Supplier channel checks provide a bottom-up roll-up that cross-validates totals before we finalize them. Key variables like companion-animal population growth, elective-surgery incidence, oncology case load, clinic density, and average replacement cycle feed the multivariate regression that projects values through 2030. Where unit data are sparse, repair-revenue ratios gathered during interviews bridge the gaps.

Data Validation & Update Cycle

Outputs pass two analyst reviews; variance rules flag shifts beyond two standard deviations, prompting re-work with fresh calls. Reports refresh annually, with interim revisions triggered by recalls, new regulations, or material M&A. A final pre-publication sweep ensures clients receive our latest view.

Why Mordor's Veterinary Infusion Pumps Baseline Earns Trust

Published estimates often diverge because publishers slice the market by dissimilar regions, exclude certain pump types, or anchor forecasts on static price curves.

For instance, one global study pegs 2024 revenue at USD 279.29 million, while another cites USD 272.48 million for the same year. Such gaps usually stem from narrower coverage, omission of clinic-based smart pumps, and single-source price assumptions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 347.15 million (2025) | Mordor Intelligence | - |

| USD 279.29 million (2024) | Global Consultancy A | Excludes syringe-only devices; limited to three regions |

| USD 384.70 million (2023) | Trade Journal B | Uses shipment counts without ASP normalization; counts refurbished units |

| USD 272.48 million (2024) | Regional Consultancy C | Extrapolates from human pump CAGR; omits home-care usage |

These comparisons show that when scope, variables, and refresh cadence mirror real clinical spend, Mordor's dual-path model delivers a balanced, transparent baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the veterinary infusion pumps market?

The market is worth USD 368.39 million in 2026 and is projected to reach USD 494.86 million by 2031 at a 6.12% CAGR.

Which animal segment dominates demand?

Companion animals account for 56.15% of 2025 revenue and will grow at a 9.62% CAGR, making them both the largest and fastest-expanding segment.

Why are syringe pumps gaining share?

Precision dosing for oncology and critical-care therapies pushes clinics toward smart syringe pumps, which are forecast to post a 8.78% CAGR through 2031.

What restrains adoption in emerging markets?

High upfront costs and limited pet-insurance coverage reduce affordability, while supply-chain shortages lengthen delivery times for advanced models.

Which region offers the strongest growth outlook?

Asia-Pacific leads with a 13.48% CAGR to 2031, fuelled by rising pet ownership in China, Japan and India alongside rapid hospital build-outs.

How will new FDA regulations affect the industry?

Stricter quality-system rules coming in 2026 will lengthen product-development cycles but also elevate entry barriers, favouring companies with strong compliance infrastructure.

Page last updated on: