Vertical Lift Module (VLM) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.95 Billion |

| Market Size (2031) | USD 3.08 Billion |

| Growth Rate (2026 - 2031) | 9.58% CAGR |

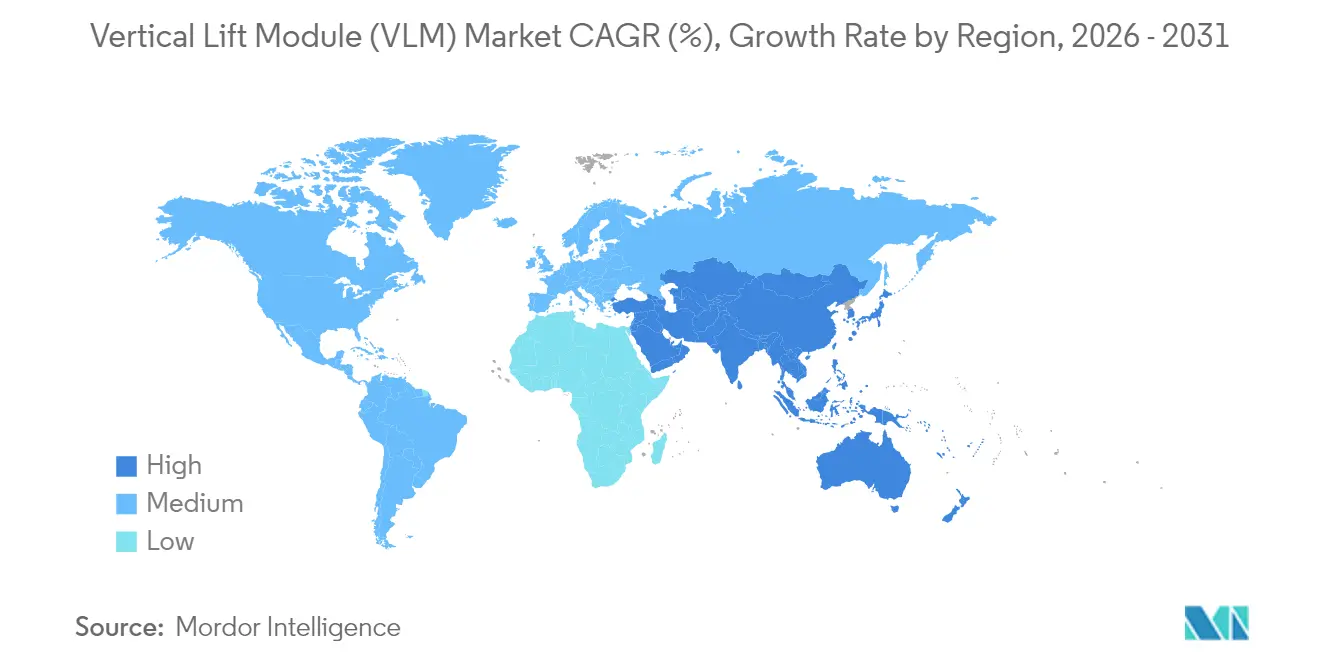

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vertical Lift Module (VLM) Market Analysis by Mordor Intelligence

The vertical lift module market size was valued at USD 1.78 billion in 2025 and estimated to grow from USD 1.95 billion in 2026 to reach USD 3.08 billion by 2031, at a CAGR of 9.58% during the forecast period (2026-2031). Demand accelerates as e-commerce firms replace bulky pallet racking with goods-to-person systems that compress fulfillment cycles from days to hours. Automakers add automated buffer storage to sustain just-in-time production rhythms, while life-sciences cleanrooms adopt enclosed modules that meet traceability and contamination-control mandates. Cold-chain operators view energy-efficient dual-drive motors as a route to ROI in less than 24 months, and predictive-maintenance software packages open an after-sales revenue stream for equipment makers.

Key Report Takeaways

- By type, single-level delivery systems held 56.65% of the vertical lift module market share in 2025, whereas dual-level delivery is projected to grow at an 11.74% CAGR to 2031.

- By load capacity, 20-50 ton units accounted for 42.55% of the vertical lift module market size in 2025; above-50-ton units are poised to expand at a 12.42% CAGR through 2031.

- By application, storage and buffering contributed 47.25% of deployments in 2025, while order-picking and kitting is advancing at a 13.18% CAGR to 2031.

- By end-user, automotive operations represented 23.60% revenue share in 2025; e-commerce fulfillment is the fastest-growing end-user segment at a 14.32% CAGR.

- By region, Europe commanded a 35.70% share of the vertical lift module market in 2025; Asia-Pacific is the fastest-growing region at a 12.14% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vertical Lift Module (VLM) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce-led micro-fulfillment expansion | 2.10% | Global, concentrated in North America & EU urban centers | Medium term (2-4 years) |

| Accelerating VLM adoption in urban warehouses | 1.80% | APAC core, spill-over to MEA | Short term (≤ 2 years) |

| OEM push for fully automated, closed-loop spare-parts storage in European automotive sector | 1.40% | Europe; expansion to North America | Medium term (2-4 years) |

| Compliance-driven traceability needs in U.S. life-sciences cleanrooms | 1.20% | North America; regulatory adoption in EU | Long term (≥ 4 years) |

| Rising labor-cost differentials in South-East Asia driving AS/RS retrofits | 0.90% | APAC, particularly Southeast Asia | Short term (≤ 2 years) |

| Energy-efficient dual-drive motors enabling ROI < 24 months in cold-storage facilities | 0.80% | Global; early adoption in North America | Medium term (2-4 years) |

| AI-enabled predictive-maintenance bundles from VLM OEMs boosting after-sales revenues | 0.60% | Global; led by developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce-led micro-fulfillment expansion

Retailers are shifting from regional distribution centers to automated micro-fulfillment nodes located inside or adjacent to existing stores. More than 7,300 automated micro-fulfillment centers are expected to be operational worldwide by 2030, almost half of them in the United States, creating sustained demand for compact, high-density modules that fit within 10,000 square-foot footprints . VLMs integrate with robotic pickers to achieve 99.99% order-accuracy rates while reducing labor needs by up to 66% . Although supply-chain constraints have slowed some retailer roll-outs, early adopters demonstrate rapid payback by compressing last-mile delivery lead times.

Accelerating VLM adoption in urban warehouses

Industrial rents in key Asian capitals outpace regional averages, forcing operators to reclaim vertical space. VLMs that reach ceiling heights of 98 feet quadruple storage density while shifting work from travel to picking, essential where labor is scarce and expensive. Daifuku’s new manufacturing plant in India was commissioned to satisfy this surge in urban automation demand. Real-estate constraints and wage inflation thus act in tandem to move VLM investments higher on management priority lists.

OEM push for fully automated, closed-loop spare-parts storage in European automotive sector

Automotive OEMs embed VLMs in parts centers to maintain production rhythm and reduce inventory. Emil Frey Logistik boosted storage capacity 300% and secured 99.76% uptime after implementing an AutoStore-based solution. Stellantis targets 40% manufacturing cost cuts by 2030 through automation, underscoring management commitment to digital logistics. Closed-loop traceability also supports quality audits and warranty management.

Compliance-driven traceability needs in U.S. life-sciences cleanrooms

Modules provide sealed environments, integrate air-particle monitoring, and maintain audit trails compliant with FDA 21 CFR Part 11. Beckman Coulter’s MET ONE 3400+ counter links directly to storage systems, automating batch documentation. ASYS Group delivers GMP-compatible handling units that synchronize with manufacturing-operations platforms, reinforcing the vertical lift module market’s appeal in regulated spaces.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Facility roof-height limitations in brownfield European sites | -1.30% | Europe; industrial legacy sites | Short term (≤ 2 years) |

| High up-front investment vs. multi-shuttle alternatives in APAC tier-2 cities | -1.10% | APAC tier-2 cities; emerging markets | Medium term (2-4 years) |

| Power-quality variations in emerging African logistics hubs | -0.70% | Sub-Saharan Africa; select MEA markets | Long term (≥ 4 years) |

| Limited retrofit-ready ERP/WMS interfaces in SME segments | -0.90% | Global SME markets; developing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Facility roof-height limitations in brownfield European sites

Many European plants built before 1990 lack the 25-foot clear height that unlocks peak VLM efficiency. Retrofitting involves floor reinforcement and structural checks that inflate project costs; in some locations, heritage rules bar vertical alterations. AutoStore estimates that 65% of its European installs occur in such retrofit scenarios, highlighting both opportunity and constraint

High up-front investment vs. multi-shuttle alternatives in APAC tier-2 cities

Operators in secondary Asian metros often favor shuttle-based systems that scale gradually. Budget uncertainties stem from fluctuating e-commerce penetration and the need for simultaneous facility upgrades. Limited payback visibility therefore delays some vertical lift module market deployments despite long-term throughput advantages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Single-level delivery dominates traditional applications

Single-level systems captured 56.65% of 2025 revenue, a reflection of their compatibility with existing building heights and straightforward operations. Typical throughput averages 250 items per hour, adequate for medium-velocity environments. Dual-level variants, however, post an 11.74% CAGR through 2031. They hit 350 items per hour by allowing simultaneous extraction and presentation trays, making them a preferred choice when brownfield sites possess sufficient vertical clearance. Kardex has upgraded controller firmware to harmonize either configuration within the same WMS, giving operators flexibility to mix system types as order profiles evolve. The vertical lift module market continues to tilt toward dual-level investments as facilities chase higher picks-per-square-foot.

A modular design framework lowers engineering costs and accelerates installation. OEMs now offer plug-and-play conveyor docks and robotic interfaces, allowing single-level modules to serve as buffers for adjacent high-throughput zones while dual-level units handle fast movers. This hybrid strategy ensures continuity during seasonal spikes without oversizing equipment for average demand, reinforcing the vertical lift module market’s value proposition for balanced capex planning.

By Load Capacity: Mid-range systems balance versatility and performance

Units rated for 20-50 tons held 42.55% market share in 2025, reflecting their suitability for boxed automotive parts, tote-handled e-commerce inventory, and pharmaceutical payloads that rarely exceed 1,000 pounds per tray. These systems form the backbone of multi-industry deployments because they require no special flooring or crane assistance. Above-50-ton modules record a 12.42% CAGR, fueled by aerospace and heavy-machinery suppliers consolidating oversized components into single storage points. Conversely, sub-20-ton machines occupy niche roles in electronics and medical device assembly lines where cleanliness and precision outweigh weight metrics.

Schaefer’s LOGIMAT illustrates the trend, offering capacities up to 1 ton per tray with ERP connectors that reduce integration times by 30%. As Industry 4.0 spreads, facilities select load classes based on digital-twin simulations rather than generic rules of thumb. Consequently, procurement cycles extend to include data modeling, yet adoption momentum sustains because the vertical lift module market size aligns closely with quantifiable productivity gains.

By Application: Storage transitions to dynamic fulfillment

Storage and buffering still account for 47.25% of deployments, a legacy of early projects that replaced traditional shelving. Yet order-picking and kitting shows a 13.18% CAGR to 2031 as omnichannel retailers prioritize throughput. The vertical lift module market size attributed to fulfillment functions gains from integrated pick-to-light, ergonomic lift tables, and AMR hand-offs that cut labor travel distance to zero. Spare-parts handling remains steady, underpinned by automotive and industrial OEM service networks that demand serialized traceability for warranty audits.

Modules now ship with embedded APIs that link picker data to customer-facing dashboards, shortening promised lead times. Flaschenpost’s automated beverage fulfillment center achieved more than 2,000 robot movements per hour by pairing VLM storage with shuttle bots. The outcome demonstrates how application evolution pivots the vertical lift module market toward real-time, order-driven logic rather than static stocking.

By End-User Industry: Automotive leadership faces e-commerce challenge

Automotive plants held 23.60% share in 2025, leveraging modules for kit-sequencing lines and warranty parts hubs. The vertical lift module market share in this segment reflects strict uptime targets and mature MES interfaces. E-commerce-centric retailers, however, register the fastest expansion at 14.32% CAGR through 2031. They treat VLMs as micro-fulfillment engines that slash urban delivery windows to same-hour benchmarks. Life-sciences cleanrooms, electrical assembly, and food logistics maintain consistent uptake as industry-specific variants gain certifications such as GMP or ISO 14644.

Interstate Cold Storage documented 35% energy savings after integrating VFD-equipped hoist motors, proving relevance for temperature-controlled goods. As climate-controlled logistics proliferate, end-user diversification helps insulate the vertical lift module industry from cyclical shocks in any single sector.

Geography Analysis

Europe leads with 35.70% revenue share in 2025, anchored by automotive manufacturing corridors in Germany, Spain, and France. Brownfield retrofits dominate because many facilities predate modern ceiling-height norms. OEM mandates for traceability and energy-footprint reduction, combined with strict worker-safety codes, keep the regional vertical lift module market growing even when new-build projects slow. Germany’s Tier-1 suppliers integrate AI-based motor diagnostics to prevent unscheduled line stops, a feature now embedded in most European purchase specifications.

Asia-Pacific posts the fastest 12.14% CAGR through 2031. China deploys VLMs in greenfield smart factories where cell-based manufacturing needs compact point-of-use stores. India’s logistics automation spending is climbing as new industrial corridors receive public funding for integrated supply-chain parks, reinforcing regional appetite for high-density vertical storage. Japan and South Korea apply modules to alleviate labor shortages caused by aging demographics. The region’s scale and greenfield nature mean suppliers sell complete ecosystems—VLM hardware, WMS, and AMR fleets—in one turnkey package, bolstering the vertical lift module market size across the decade.

North America maintains a steady expansion track. Retailers retrofit suburban outlets with micro-fulfillment nodes, and life-sciences clusters in the U.S. Northeast adopt GMP-compliant modules for biologics. Cold-storage operators in the U.S. Midwest and Canada appreciate dual-drive hoist efficiencies that curb utility bills during peak tariffs. Latin America and the Middle East & Africa are emerging but uneven. Brazil’s contract-logistics firms explore leasing models to bypass capex barriers, while South African distributors face power-quality issues that necessitate voltage-regulation add-ons, a factor that suppresses near-term vertical lift module market penetration.

Competitive Landscape

The market remains moderately fragmented. Kardex, Hänel, and Modula retain legacy brand equity, yet cross-segment entrants such as AutoStore and SSI SCHAEFER challenge incumbents by bundling cube storage or shuttle systems with VLM offerings. Product differentiation now centers on software. Kardex’s tie-up with Berkshire Grey integrates robotic picking to achieve 99.99% accuracy without teach-in periods, underscoring a shift toward AI-enabled workflows .[1]Kardex, “Berkshire Grey Announces Formal Partnership with Kardex; Powering Robotic Picking and AutoStore,” kardex.com Likewise, SPARETECH’s parts-identification platform leverages a 10-million-item database to cut spare-parts inventory costs, extending value beyond physical equipment .[2]SPARETECH, “Spare Parts on Demand – Transparency & Availability Instead of High Inventories,” sparetech.io

Energy-optimized drives and predictive diagnostics serve as additional battlegrounds. Modula’s next-gen controller employs load-adaptive acceleration curves that trim electricity use by 15%, addressing ESG scorecard pressures . AutoStore’s Thai robot plant doubles production capacity, shrinking lead time to 20 weeks and giving the firm supply-chain resilience that competitors lack .[3]“AutoStore Debuts New Modular Robot Factory to Support Global Market Expansion,” autostoresystem.com Regional manufacturing footprints also influence total landing cost, a factor that favors vendors with diversified assembly locations such as Daifuku and SSI SCHAEFER. Pricing tactics vary: some suppliers bundle long-term service agreements at discounted rates to lock in annuity revenue, while others offer modular service tiers targeting SME budgets.

Vertical Lift Module (VLM) Industry Leaders

-

Kardex Group

-

Hänel Storage Systems

-

Ferretto Group S.p.a

-

Modula Inc.(System Logistics)

-

AutoCrib Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: SPARETECH launched an automated spare-parts platform built on more than 10 million SKUs SPARETECH.

- February 2025: Infosys began a global SAP S/4HANA program with Kardex covering 30+ countries Infosys.

- January 2025: AutoStore opened a new modular robot factory in Rayong Province, Thailand, doubling robot capacity to 15,000 units within 18 months AutoStore.

- January 2025: Bertel O. Steen quadrupled storage capacity after implementing AutoStore automation, achieving 99.7% uptime AutoStore.

Global Vertical Lift Module (VLM) Market Report Scope

A vertical lift module (VLM) is a closed system with an inserter and an extractor in the middle. This makes it easy for stored trays to be found and taken out automatically.When stored items were brought to the operator, the search time was cut by a lot, which increased productivity by 66%.

The studied market divides VLM into groups based on the end-user industries, such as automotive, food and beverage, and retail, and gives a detailed analysis of specific use cases and application areas. Also, the analysis of geography leaves out major countries in North America, Europe, and the Asia-Pacific region.

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Single-Level Delivery |

| Dual-Level Delivery |

| Up to 20 Tons |

| 20 - 50 Tons |

| Above 50 Tons |

| Storage and Buffering |

| Order-Picking and Kitting |

| Spare-Parts Handling |

| Automotive |

| Metal and Machinery |

| Electrical and Electronics |

| Retail / Distribution and E-commerce |

| Life-Sciences (Pharma Medical Devices) |

| Food and Beverage |

| Other Industries |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Turkey |

| Saudi Arabia | |

| South Africa | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Type | Single-Level Delivery | |

| Dual-Level Delivery | ||

| By Load Capacity | Up to 20 Tons | |

| 20 - 50 Tons | ||

| Above 50 Tons | ||

| By Application | Storage and Buffering | |

| Order-Picking and Kitting | ||

| Spare-Parts Handling | ||

| By End-User Industry | Automotive | |

| Metal and Machinery | ||

| Electrical and Electronics | ||

| Retail / Distribution and E-commerce | ||

| Life-Sciences (Pharma Medical Devices) | ||

| Food and Beverage | ||

| Other Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Turkey | |

| Saudi Arabia | ||

| South Africa | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the vertical lift module market?

The vertical lift module market size is valued at USD 1.95 billion in 2026 and is projected to reach USD 3.08 billion by 2031 at a 9.58% CAGR.

Which segment holds the largest vertical lift module market share?

Single-level delivery systems hold the largest share at 56.65% of 2025 revenue.

Which application area is growing fastest?

Order-picking and kitting applications are expanding at a 13.18% CAGR through 2031 as retailers push for rapid fulfillment.

Why is Asia-Pacific the fastest-growing region?

Robust e-commerce growth and greenfield smart-factory investments drive a 12.14% CAGR for Asia-Pacific through 2031.

Page last updated on: