Servo Motor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

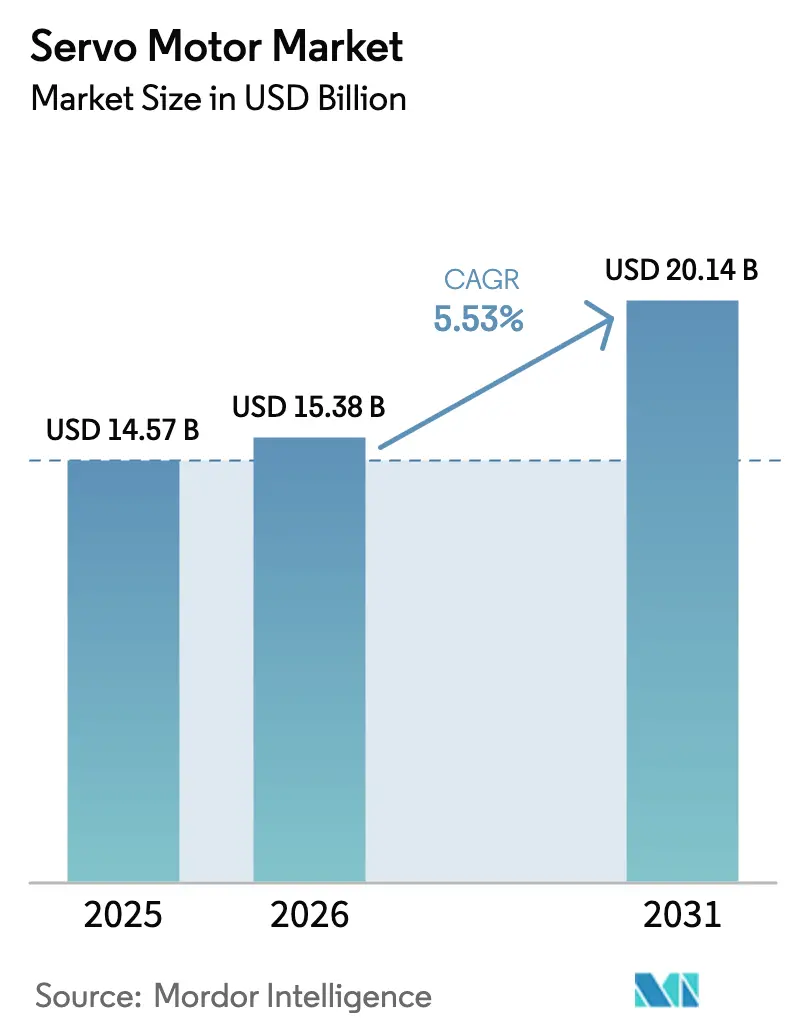

| Market Size (2026) | USD 15.38 Billion |

| Market Size (2031) | USD 20.14 Billion |

| Growth Rate (2026 - 2031) | 5.53% CAGR |

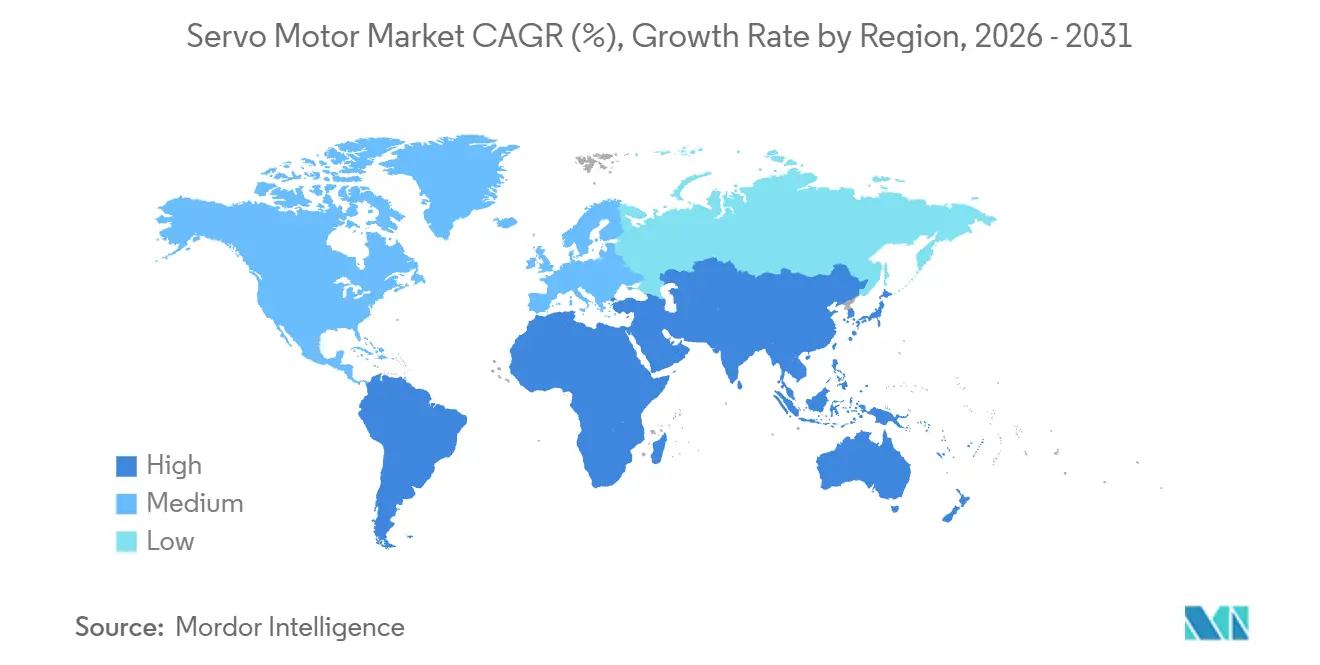

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

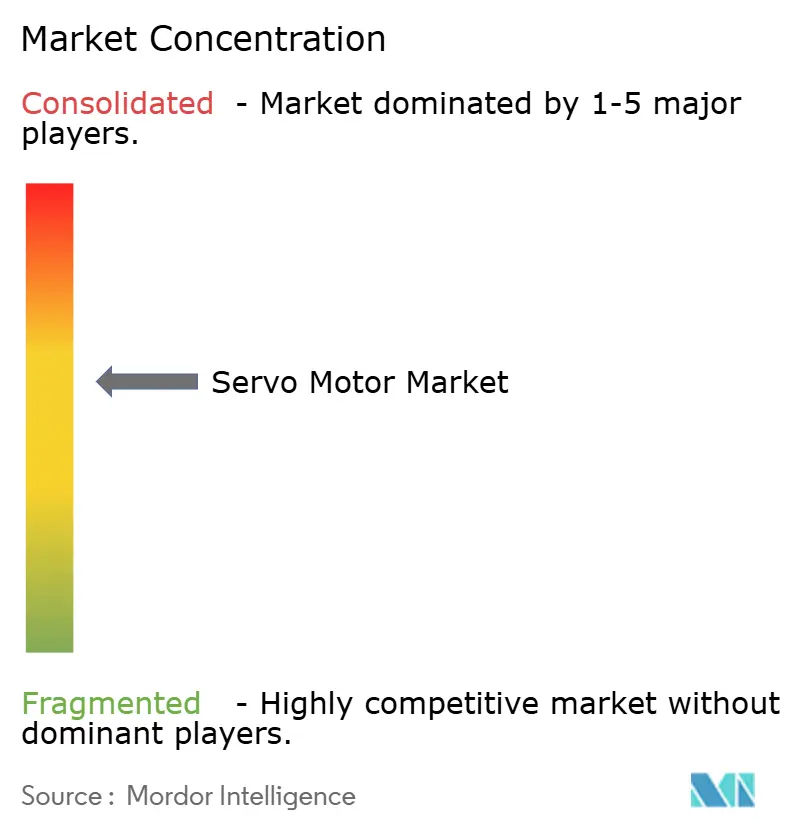

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Servo Motor Market Analysis by Mordor Intelligence

The Servo Motor Market size is expected to increase from USD 14.57 billion in 2025 to USD 15.38 billion in 2026 and reach USD 20.14 billion by 2031, growing at a CAGR of 5.53% over 2026-2031. This expansion is driven by a shift from volume-led installations to precision, digitally networked motion-control platforms, which carry higher unit prices. Tighter efficiency mandates introduced by IEC 61800-9-2:2025 are catalyzing the replacement of legacy drives with premium IE4 and IE5-rated units, while real-time diagnostics and energy compliance have overtaken upfront cost as the primary purchase criteria. High-volume electronics assembly in Asia Pacific, rising cobot deployments, and the integration of edge AI analytics are driving further reinforcement of demand, even as supply-chain risks surrounding rare-earth magnets and cybersecurity continue to shadow growth prospects.

Key Report Takeaways

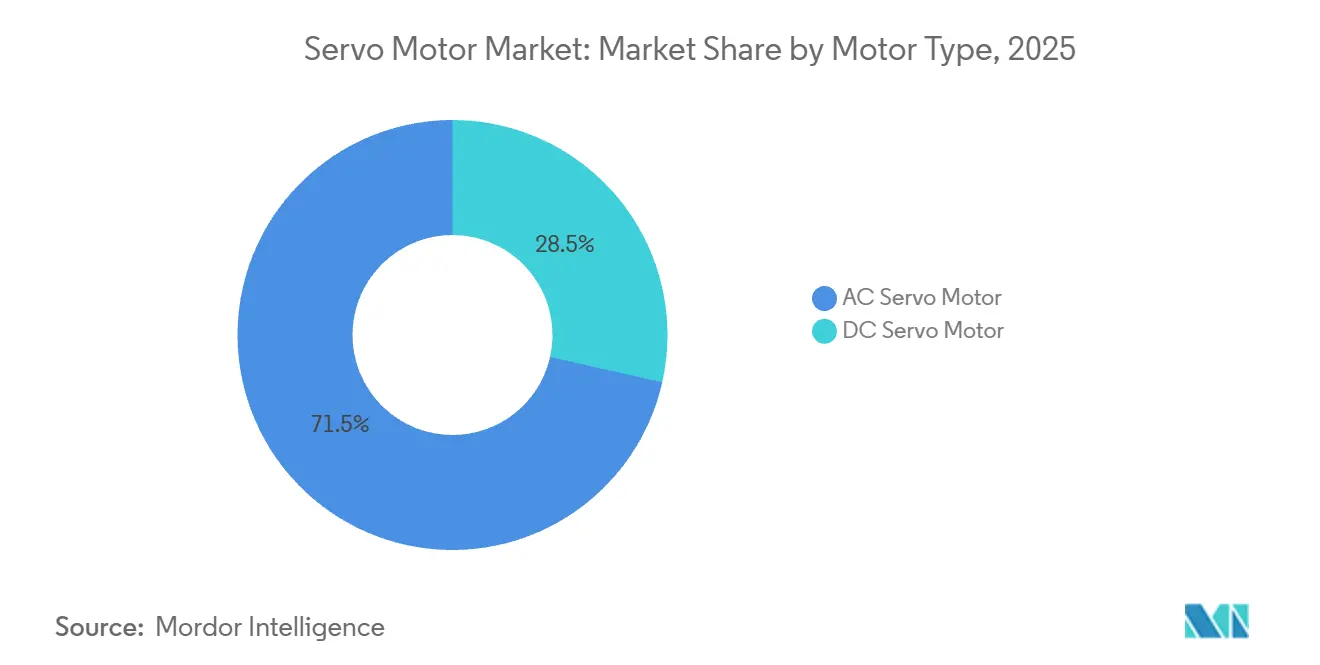

- By motor type, AC servo motors led with 71.47% revenue share in 2025; brushless DC variants are projected to expand at a 6.47% CAGR through 2031.

- By axis configuration, single-axis systems accounted for 63.41% of the servo motor market share in 2025, whereas multi-axis solutions are forecast to post a 7.32% CAGR.

- By power rating, the 750-watt to 2-kilowatt band held a 38.27% share of the servo motor market size in 2025, while units above 2 kilowatts are advancing at an 8.12% CAGR.

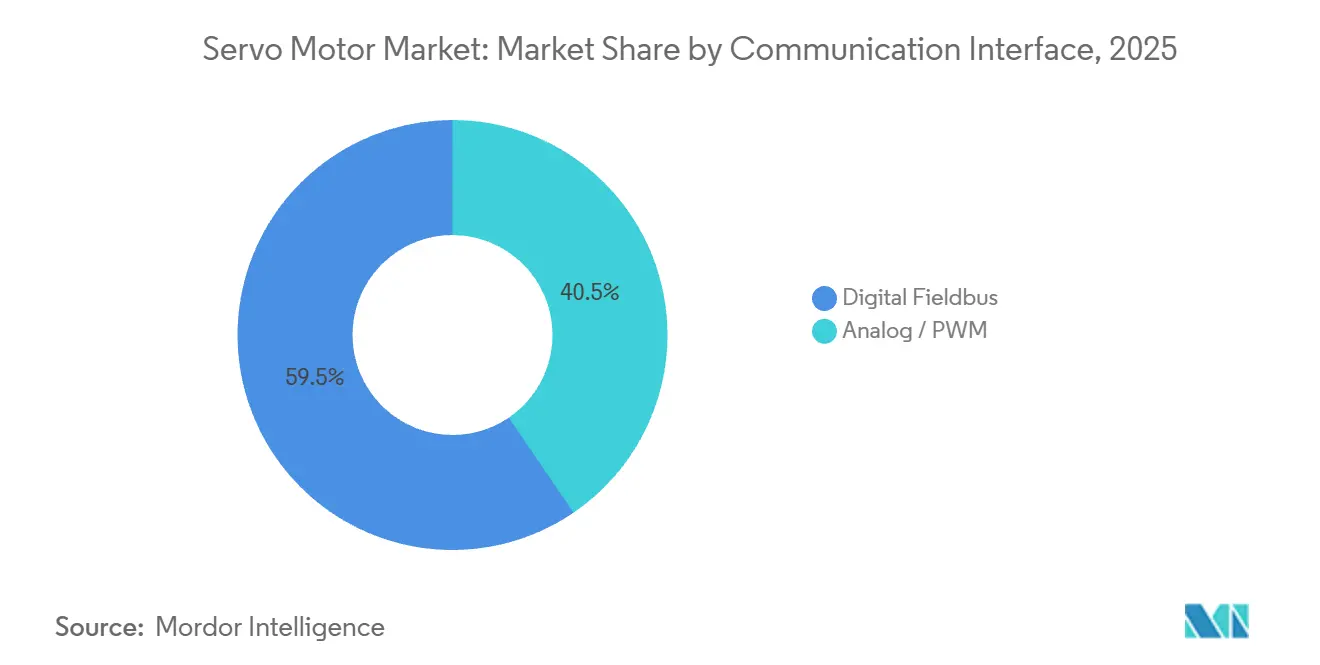

- By communication interface, digital fieldbus networks captured 59.53% of 2025 installations; at 6.32% CAGR, they remain the fastest-growing connectivity option.

- By end-user industry, automotive represented 24.63% of 2025 demand, yet electronics and semiconductor manufacturing is set to grow at an 8.13% CAGR to 2031.

- By geography, the Asia Pacific commanded 43.74% of global revenue in 2025, whereas Africa is expected to log the highest 8.13% CAGR during the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Servo Motor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of International Energy-Efficiency Standards | +0.9% | Europe, Asia Pacific, North America | Medium term (2-4 years) |

| Industry-Wide Drive Toward Smart and Flexible Automation | +1.2% | Global, with concentration in Asia Pacific and Europe | Long term (≥4 years) |

| Rising Deployment of Industrial and Collaborative Robots | +1.1% | Asia Pacific, North America, Europe | Medium term (2-4 years) |

| Integration of Servo Drives with Edge AI Chips for On-motor Analytics | +0.7% | North America, Europe, Asia Pacific (Japan, South Korea) | Long term (≥4 years) |

| Miniaturized Servo Solutions for Medical Exoskeletons | +0.3% | North America, Europe, Japan | Long term (≥4 years) |

| High-Torque Servo Use in Autonomous Agricultural Equipment | +0.5% | North America, Europe, Brazil, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adoption Of International Energy-Efficiency Standards

IEC 61800-9-2:2025 established IE4 and IE5 benchmarks, forcing vendors to redesign windings, magnets, and firmware to lower drivetrain losses. EU member states are expected to embed the standard in public procurement rules by mid-2025, triggering large-scale retrofits in municipal water networks. Japan and South Korea linked tax credits to compliance, accelerating adoption across automotive paint shops and semiconductor fabs. The rule also mandates the disclosure of full-load efficiency curves, shifting competition from sticker price to life-cycle operating costs. North America is lagging but is likely to catch up as the U.S. Department of Energy references the standard in its 2027 rulemaking.[1]U.S. Department of Energy, “Notice of Intent for 2027 Appliance Efficiency Rulemaking,” energy.gov

Industry-Wide Drive Toward Smart And Flexible Automation

Manufacturers are abandoning hard-tooled transfer lines for reconfigurable work-cells equipped with servo-driven gantries and cobots connected over deterministic Ethernet. Operational industrial robots reached 4.28 million units by the end of 2023. EtherCAT penetration among German machine builders reached 62% in 2024, underscoring the shift toward distributed-clock motion networks. Edge AI chips mounted on drives are predicting bearing failures up to 30 days in advance, cutting unplanned stoppages by 40% in pilot lines. The servo motor market, therefore, benefits not only from mechanical precision but from data-driven uptime improvements.

Rising Deployment Of Industrial And Collaborative Robots

Robot installations hit 541,302 units in 2023, with cobots expanding 28% year-on-year. Each cobot integrates four to six synchronized servo axes capable of sub-millisecond loop closure, driving multi-axis drive demand. Japan earmarked USD 450 million in subsidies for SME cobot adoption, provided installations use servo-driven joints. Semiconductor back-end lines now achieve 120 placements per minute thanks to high-speed servo delta robots, roughly doubling pneumatic throughput. The performance delta is locking in servos as the default actuation technology for precision assembly.

Integration Of Servo Drives With Edge AI Chips For On-Motor Analytics

Embedding inference processors directly on drives eliminates cloud latency and secures operational data on-premise, aligning with IEC 62443 cybersecurity zones. Siemens and Rockwell Automation plan to ship drives carrying NVIDIA Jetson Thor modules from 2026 onward. German supplier Synapticon already delivered 15,000 AI-enabled drives in 2025 to packaging OEMs, auto-tuning PID gains as product weight varies. Analog Devices’ mixed-signal controller integrates PWM generation and TensorFlow Lite, opening sub-1-kilowatt servos to AI features. Competitive focus is pivoting from torque density to software-defined adaptability, expanding the addressable value pool for the servo motor market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Low-Cost Stepper and BLDC Alternatives | -0.6% | Asia Pacific, South America, Africa | Short term (≤2 years) |

| High Upfront Capital Expenditure for Multi-Axis Servo Systems | -0.5% | Global, acute in South America and Africa | Medium term (2-4 years) |

| Rare-Earth Magnet Supply Risks Amid Geopolitical Tensions | -0.7% | Global, with acute impact in North America and Europe | Long term (≥4 years) |

| Cyber-Security Concerns in Networked Motion Control | -0.3% | North America, Europe, Asia Pacific (Japan, South Korea) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation Of Low-Cost Stepper And BLDC Alternatives

Open-loop stepper and sensor-based BLDC motors cost 40-60% less than servo systems, a gap that appeals to price-sensitive buyers in Africa and South America. Chinese suppliers shipped over 12 million steppers in 2024, primarily for use in servicing 3D printers, CNC routers, and textile machinery. Texas Instruments’ USD 5 encoder IC blurs the line by adding closed-loop feedback to BLDC motors. As a result, servo adoption is deferred in cost-elastic markets by up to three years.

Rare-Earth Magnet Supply Risks Amid Geopolitical Tensions

China processes roughly 90% of the global neodymium and dysprosium, and the tightening of export quotas in mid-2024 led to a 35% increase in dysprosium prices. Western manufacturers responded by stockpiling magnets and financing recycling plants; however, supply security remains tenuous until domestic mines scale up after 2028.[2]U.S. Geological Survey, “Mineral Commodity Summaries – Rare Earths,” usgs.gov Torque-dense ferrite and reluctance designs are under evaluation, but they lag behind permanent-magnet servos by 15-20% in power density, hindering near-term substitution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Motor Type: Brushless DC Gains Momentum Amid Miniaturization Needs

Brushless DC motors accounted for the fastest-growing share within the servo motor market, advancing at a 6.47% CAGR as medical, agricultural, and mobile-robot OEMs prioritize compact form factors. AC counterparts still dominated with 71.47% revenue share in 2025, reflecting their hold on heavy industrial processes that tap three-phase grids. Battery-powered surgical robots and exoskeletons favor frameless BLDC units, while silicon-carbide inverters narrow the efficiency gap to legacy induction platforms.

AC designs nonetheless retain an advantage in regenerative energy recovery, a decisive feature in vertical-axis CNC and high-bay crane applications. Vendors such as Yaskawa integrated 23-bit encoders and silicon-carbide drives into next-gen AC platforms, extending mean time between failures to 100,000 hours and reinforcing their presence in the servo motor market.

By Axis Configuration: Multi-Axis Solutions Ride The Cobot Wave

Single-axis systems still accounted for 63.41% of installations in 2025, primarily used for conveyor indexing and valve actuation tasks. Yet, multi-axis architectures are expanding at a 7.32% CAGR, propelled by cobots that require six coordinated joints. EtherCAT and PROFINET backbones deliver sub-microsecond synchronization across axes, enabling compliant motion without the need for cages.

Automotive welding lines are transitioning from fixed spot guns to multi-axis gantries that adapt in real-time to panel distortion. Siemens launched turnkey packages integrating vision guidance with multi-axis drives, reducing programming labor by 60% and deepening penetration of the servo motor market.

By Power Rating: High-Power Band Accelerates On Autonomous Equipment

The 750 W–2 kW class remained the largest slice at 38.27% of the servo motor market size in 2025, though >2 kW units are accelerating at 8.12% CAGR. Autonomous tractors employ 5 kW servos to maintain down-force in variable soil, illustrating the torque demands in precision farming. High-tonnage metal presses and injection-molding machines likewise favor liquid-cooled 10-kW drives that meet IE5 efficiency with silicon-carbide inverters.

Thermal management challenges escalate above 2 kW, prompting the adoption of water-cooled designs that carry a 15-20% price premium yet deliver lifecycle savings through lower electricity consumption. Sub-750 W motors, by contrast, thrive in exoskeletons and lab automation where inertia and footprint drive selection.

By Communication Interface: Digital Fieldbus Becomes De-Facto Standard

Digital fieldbus protocols held a 59.53% share in 2025 and are growing at a rate of 6.32% annually, reflecting the demand for deterministic multi-axis coordination. EtherCAT processes frames on the fly, synchronizing 100 axes within 1 ms, a prerequisite for semiconductor wafer handling.[3]SEMI, “Semiconductor Equipment Market Statistics,” semi.org PROFINET’s backward compatibility with legacy PROFIBUS networks eases migration.

Analog and PWM lines persist in low-complexity tasks but face obsolescence as IEC 62443 security rules require encrypted traffic that analog cannot provide. Rockwell’s 2025 launch of a drive verifying position commands via digital signatures underscores how cybersecurity accelerates fieldbus uptake.

By End-User Industry: Electronics And Semiconductor Leapfrog Automotive

Automotive held 24.63% of demand in 2025; however, electronics and semiconductor plants are expanding at a segment-best 8.13% CAGR, as sub-10 nm nodes and advanced packaging push precision requirements upward. Lithography steppers utilize nanometer-level stages driven by high-torque servos, accounting for approximately 18% of wafer-fabrication equipment costs.

Surface-mount lines in China, South Korea, and Taiwan utilize servo delta robots, achieving 120 placements per minute, which far outpaces pneumatic pickers and secures higher ASPs for servo vendors. Mature verticals, such as oil and gas, remain hydraulic-centric, although pilot retrofits show 15-20% energy savings with servo drives on centrifugal pumps.

Geography Analysis

Asia Pacific generated 43.74% of 2025 revenue, anchored by China’s dominance in smartphone assembly and South Korea’s USD 44 billion semiconductor CAPEX wave. Government subsidies in India under the Production-Linked Incentive scheme reimburse 25% of automation spend, accelerating servo adoption across automotive and pharma lines.[3]

Africa, although only a small portion of the current servo motor market, is forecast to expand at an 8.13% CAGR through 2031, driven by South Africa’s EV program, Nigerian food-processing upgrades, and Kenyan textile exports. Limited grid reliability and servicing expertise, however, keep low-cost stepper alternatives in contention, tempering upside.

North America and Europe remain mature but show pockets of double-digit growth in medical devices and aerospace, segments willing to pay premiums for IP69K stainless motors or DO-178-certified software stacks. South America lags as macro volatility lifts imported-equipment costs, although Brazil’s automotive sector could reaccelerate once borrowing costs retreat below 10%. The Middle East, led by Saudi Arabia's Vision 2030, is selectively installing servo-driven CNC and additive manufacturing cells in new industrial zones.

Competitive Landscape

The servo motor market exhibits moderate concentration, with the top five suppliers accounting for approximately 52% of the 2025 revenue; no single firm exceeds 15%. Incumbents defend their share through the vertical integration of motor cores, encoders, and silicon-carbide drives, exemplified by Yaskawa’s Sigma-7 series, which integrates 23-bit absolute encoders and achieves a 100,000-hour MTBF.

Chinese entrants, such as Estun Automation, leverage local rare-earth supply and low labor costs to undercut prices but lag behind in encoder resolution and cybersecurity features. Siemens filed 47 motion-control patents in 2024, with 60% aimed at encrypted fieldbus communication, emphasizing alignment with IEC 62443.[4]Siemens AG, “Motion-Control Patent Filings 2024,” siemens.com

White-space opportunities center on edge AI; fewer than 5% of installed drives run on-motor inference, exposing incumbents to software-first disruptors. Nevertheless, entrenched service contracts and proprietary programming environments create switching costs that slow the erosion of market share, suggesting continued but incremental rebalancing.

Servo Motor Industry Leaders

Yaskawa Electric Corporation

Mitsubishi Electric Corp.

Siemens AG

Rockwell Automation Inc.

Delta Electronics Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Siemens launched the Sinamics S210 drive with integrated edge AI processors for real-time vibration analytics, reporting 35% maintenance-cost cuts in pilot lines.

- September 2025: Yaskawa committed USD 180 million to expand its Kitakyushu plant, adding 2 million servo units of annual capacity.

- August 2025: ABB acquired Codian Robotics for USD 95 million, folding delta robots into its packaging portfolio.

- July 2025: Mitsubishi Electric debuted the Melservo-J5 brushless DC line, which spans ratings of 50 W–750 W, for use in medical and laboratory automation.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the global servo-motor market as revenue generated from the sale of new, standalone AC and DC rotary servo-motors that deliver closed-loop control of position, speed, or torque across industrial, commercial, and selected medical devices. Motors are tracked at factory gate prices before freight and taxes, and demand is mapped to the first point of installation geography.

Out-of-scope: integrated motor-drive packages, linear servo drives, and aftermarket repair services.

Segmentation Overview

- By Motor Type

- AC Servo Motor

- DC Servo Motor

- By Axis Configuration

- Single-Axis

- Multi-Axis

- By Power Rating

- <750 W

- 750 W – 2 kW

- >2 kW

- By Communication Interface

- Analog / PWM

- Digital Fieldbus (CANopen, EtherCAT, PROFINET)

- By End-User Industry

- Oil and Gas

- Chemical and Petrochemical

- Power Generation

- Water and Wastewater

- Metal and Mining

- Food and Beverage

- Discrete Industries

- Automotive

- Electronics and Semiconductor

- Packaging

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview motor OEM executives, automation-system integrators, and distribution partners in Asia-Pacific, Europe, and the Americas. These conversations validate shipment shares, typical margins, and emerging applications (for example, exoskeletons and EV battery lines), and they reconcile regional ASP differences highlighted during desk work.

Desk Research

We begin with public statistics, UN Comtrade shipment codes for electric motors, the International Federation of Robotics robot-density data set, Eurostat PRODCOM, and the US Census' Current Industrial Reports, because these establish unit flow and baseline pricing across regions. Trade-association yearbooks such as the Japan Electrical Manufacturers Association and the National Electrical Manufacturers Association help us detail power-rating splits. Company filings and investor decks supply average selling prices and mix shifts, which are then complemented with patent trends from Questel and financial snapshots from D&B Hoovers. Dow Jones Factiva screens industry news for capacity additions and policy moves. The sources cited above are illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down demand pool is constructed from industrial production indices, new robot installations, and machine-tool shipments; volumes are multiplied by verified servo penetration rates and calibrated ASP tiers. Results are corroborated through selective bottom-up supplier roll-ups and distributor channel checks. Key variables inside the model include robot density per 10,000 workers, global EV assembly lines commissioned, rare-earth magnet price index, capital-goods PMI, and national energy-efficiency mandates. Forecasts use multivariate regression augmented with scenario analysis to capture commodity-price or policy shocks, and missing bottom-up data points are bridged with region-specific triangulation factors agreed upon by interviewed experts.

Data Validation & Update Cycle

Outputs pass two analyst reviews, anomaly screens, and currency/PPP sanity checks before sign-off. The study is refreshed every twelve months, with interim revisions triggered by material events such as tariff changes or large capacity announcements. A final pre-publication sweep ensures clients always receive the latest view.

Credibility anchor: why our Servo Motor baseline commands reliability

Published estimates rarely align because each publisher tweaks scope, currency year, or ASP logic.

Key gap drivers include differing treatment of small-frame motors, whether drives are bundled, forecast refresh cadence, and the currency conversion method applied to Asia-origin data. Our study keeps scope tight, refreshes annually, and publicizes every assumption, which raises confidence for strategic planning.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 14.57 B | Mordor Intelligence | - |

| USD 14.44 B | Global Consultancy A | Excludes sub-50 W units, relies on 2024 shipment inventory only |

| USD 17.16 B | Industry Association B | Bundles servo drives with motors, inflating total value |

| USD 9.59 B | Research Boutique C | Counts AC models only and omits retrofit demand |

The comparison shows that when scope creep or omission is removed, our balanced, clearly documented approach delivers a dependable baseline that decision-makers can retrace and stress-test with minimal effort.

Key Questions Answered in the Report

How large is the servo motor market in 2026?

The servo motor market size was USD 15.38 billion in 2026.

What CAGR is expected for servo motors to 2031?

The market is projected to register a 5.53% CAGR through 2031.

Which motor type is growing fastest?

Brushless DC servo motors are forecast to expand at 6.47% CAGR.

Which region is anticipated to grow quickest?

Africa is predicted to post the highest 8.13% CAGR through 2031.

Why are digital fieldbus interfaces gaining share?

They enable deterministic multi-axis coordination and meet IEC 62443 cybersecurity requirements, driving 6.32% CAGR adoption.

What is the main supply-chain risk for servo manufacturers?

Dependence on rare-earth magnets, with China controlling about 90% of global refining capacity, poses significant supply risk.

Page last updated on: