Pasty Products Filling Machine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

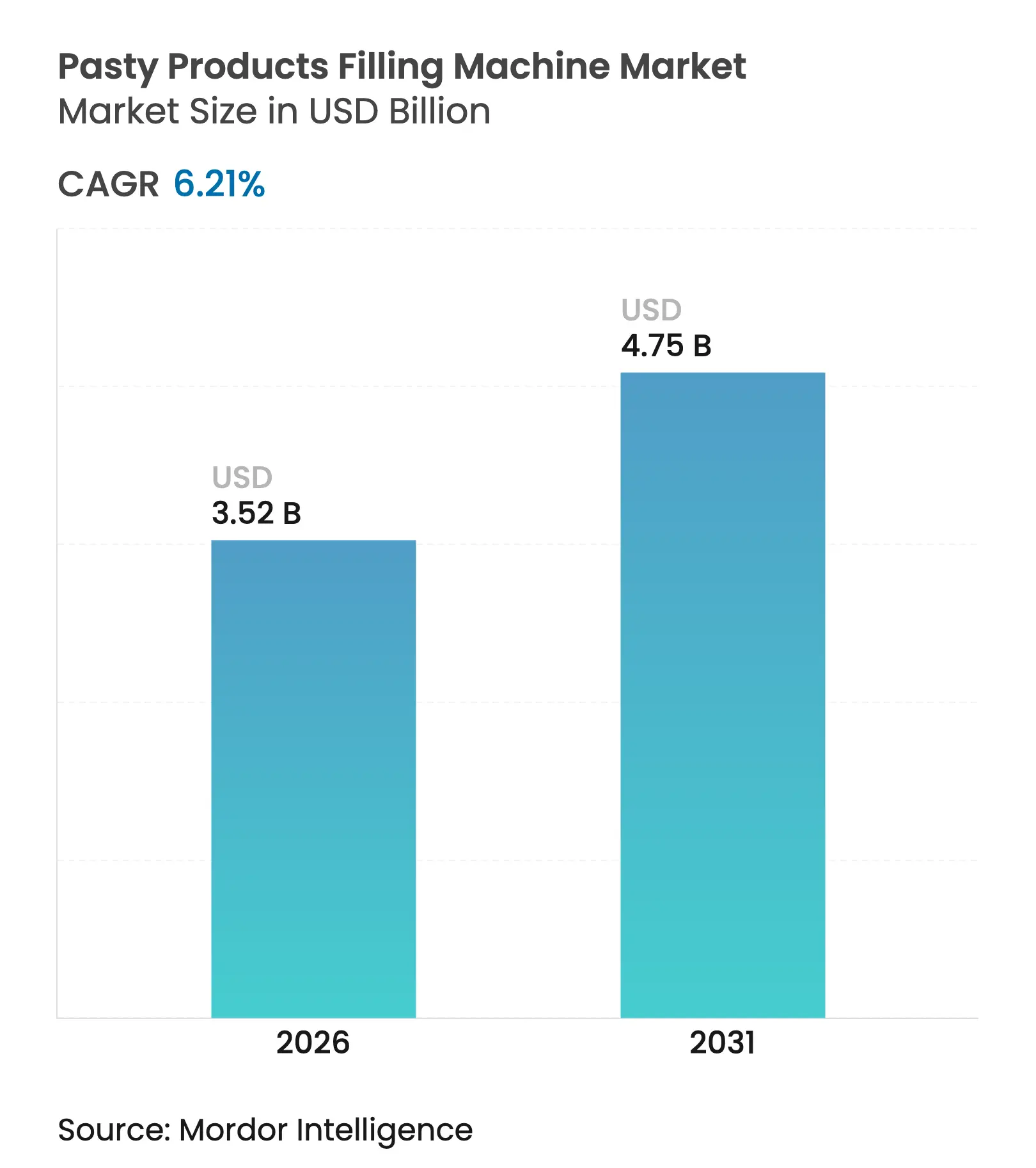

| Market Size (2026) | USD 3.52 Billion |

| Market Size (2031) | USD 4.75 Billion |

| Growth Rate (2026 - 2031) | 6.21 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Pasty Products Filling Machine Market Analysis by Mordor Intelligence

The pasty products filling machine market size was valued at USD 3.31 billion in 2025 and estimated to grow from USD 3.52 billion in 2026 to reach USD 4.75 billion by 2031, at a CAGR of 6.21% during the forecast period (2026-2031). Elevated regulatory scrutiny of aseptic processing, rising adoption of single-dose packaging in foodservice, and EU circular-economy mandates for cosmetics packaging collectively create sustained equipment demand. European subsidy programs that offset roughly one-third of capital expenditure encourage artisan food producers to reshore capacity, while pharmaceutical fill-finish suites migrate toward closed-system automation to satisfy the FDA’s September 2024 draft guidance. Brand owners also favor high-speed rotary piston fillers capable of more than 180 cycles per minute to support portion-controlled formats, especially in quick-service restaurants facing labor constraints. Meanwhile, contract packers in emerging economies are scaling linear volumetric lines to accommodate diverse SKUs, underscoring the market’s dual pull toward both ultra-high-speed and highly flexible equipment.

Key Report Takeaways

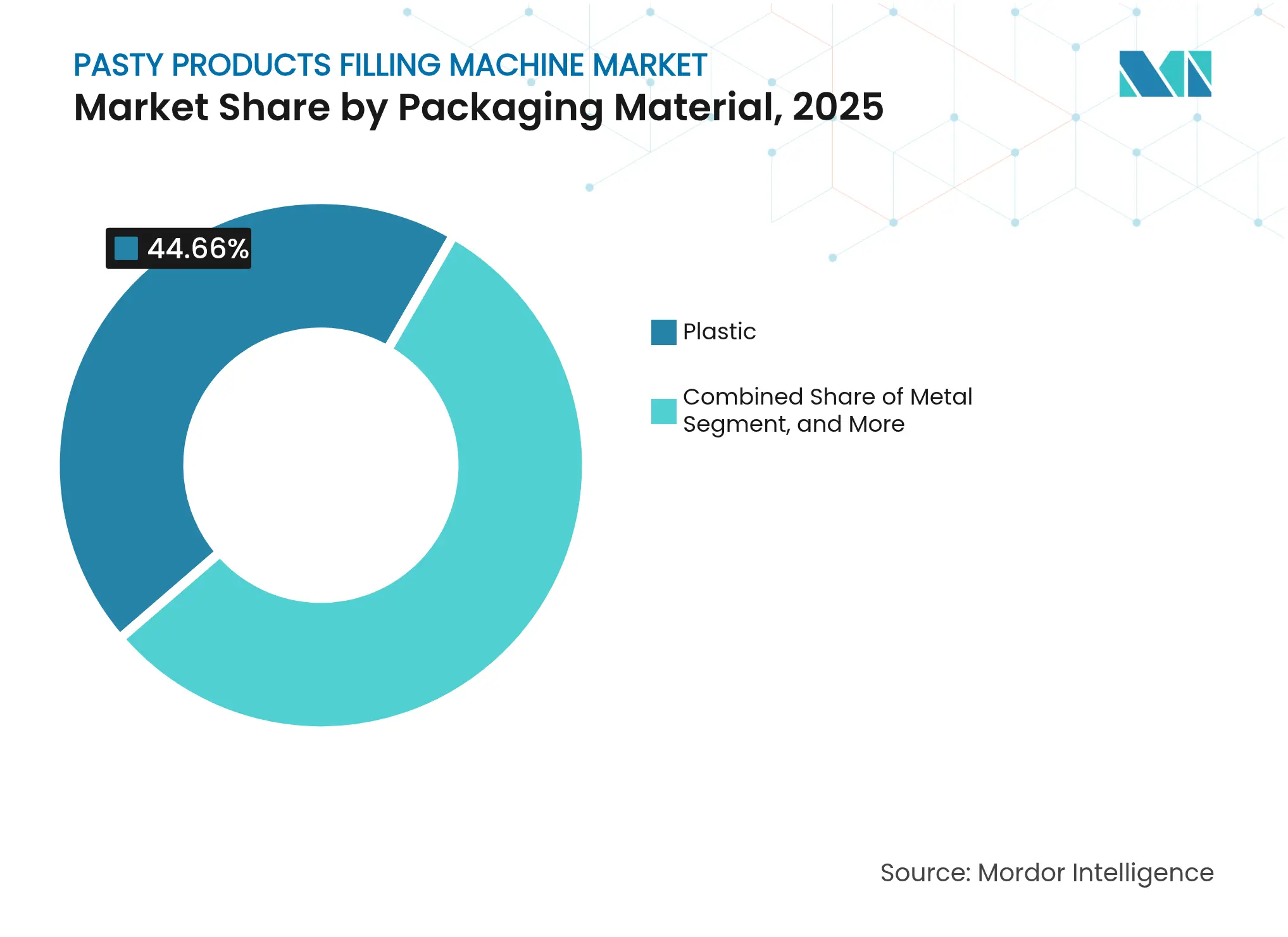

- By packaging material, plastic captured 44.66% of the pasty products filling machine market share in 2025.

- By end-user, the pasty products filling machine market size for pharmaceutical applications is forecast to advance at a 7.89% CAGR through 2031.

- By filling technology, rotary piston systems captured 38.52% of the pasty products filling machine market share in 2025.

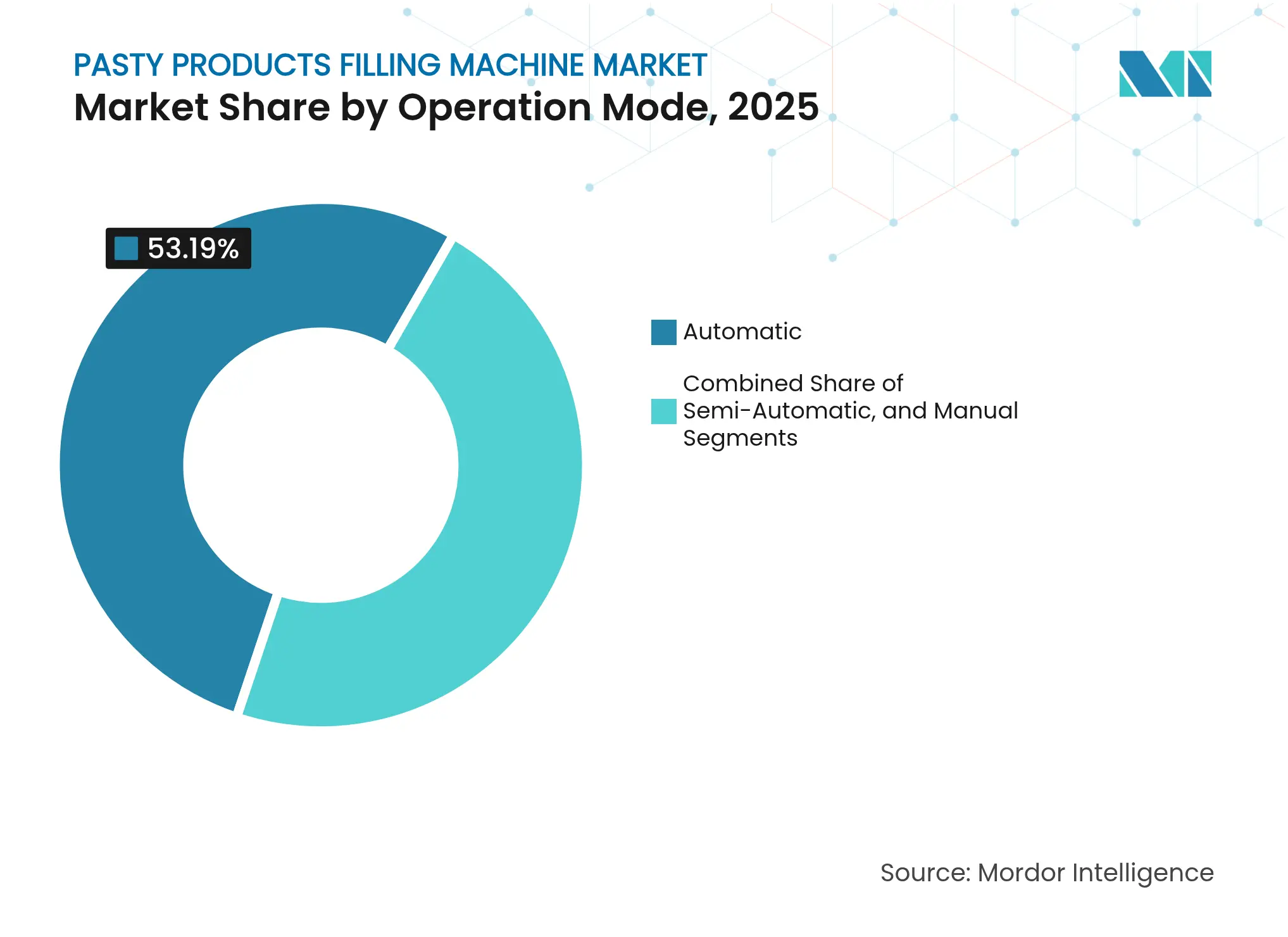

- By operation mode, the pasty products filling machine market size for semi-automatic units is forecast to advance at a 7.46% CAGR through 2031.

- By production speed, the 61-180 CPM segment captured 46.62% of the pasty products filling machine market share in 2025.

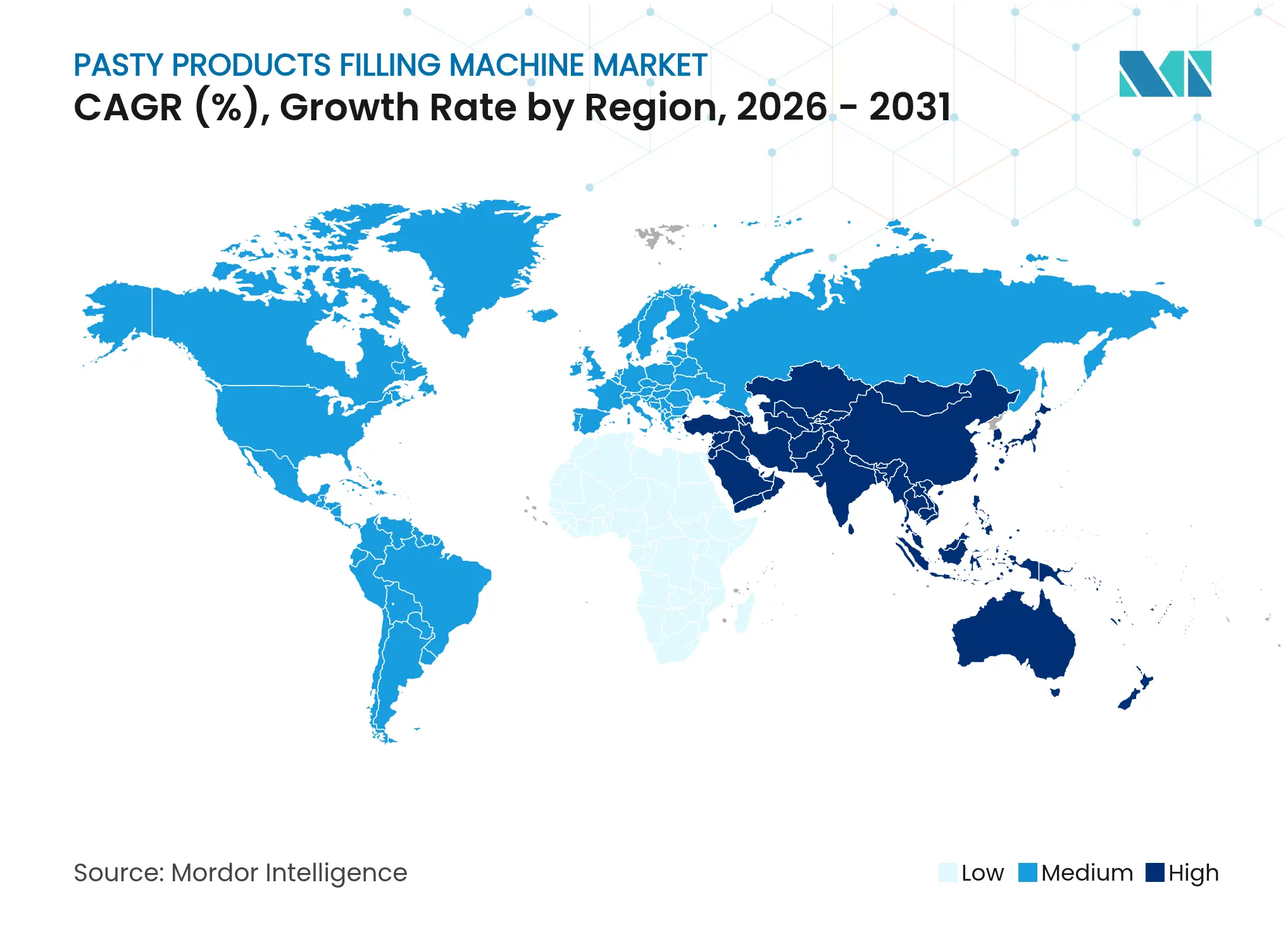

- By geography, the pasty products filling machine market size for Asia-Pacific is forecast to advance at an 8.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pasty Products Filling Machine Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rapid adoption of Industry 4.0 enabled filling lines Rapid adoption of Industry 4.0 enabled filling lines | +1.2% | Global, led by Germany, United States, Japan, South Korea | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:Global, led by Germany, United States, Japan, South Korea | Impact Timeline:Medium term (2-4 years) |

Surge in demand for single-dose sachet formats in foodservice Surge in demand for single-dose sachet formats in foodservice | +0.9% | North America and Europe, with spillover to Asia-Pacific quick-service chains | Short term (≤ 2 years) | |||

Growth of eco-design plastic tubes for cosmetics Growth of eco-design plastic tubes for cosmetics | +0.8% | Europe and North America | Long term (≥ 4 years) | |||

Compliance-driven automation in pharma fill-finish Compliance-driven automation in pharma fill-finish | +1.3% | United States, European Union, Japan | Medium term (2-4 years) | |||

Expansion of contract packing in emerging economies Expansion of contract packing in emerging economies | +1.0% | Asia-Pacific, Latin America, Middle East | Long term (≥ 4 years) | |||

Re-shoring of artisan food production in Europe Re-shoring of artisan food production in Europe | +0.7% | France, Germany, Italy, Austria | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rapid Adoption of Industry 4.0 Enabled Filling Lines

Manufacturers are integrating real-time analytics, predictive maintenance, and digital twins to compress batch release times and raise overall equipment effectiveness. Krones’ Dynafill employs AI-based control to process 80,000 containers per hour, reducing its footprint by 50% and demonstrating how machine learning optimizes piston velocity in real-time.[1]Krones AG, “Dynafill AI-Based Filling,” krones.com Beckhoff’s XTS Hygienic transport system synchronizes rotary indexing and piston actuation at sub-millisecond intervals via EtherCAT, illustrating the precision gains achievable with PC-based motion control. Siemens’ TIA Portal example for linear filling utilizes virtual axis mapping to reduce changeovers, thereby enhancing SKU agility. Open-architecture standards, such as OMAC PackML, enable multi-vendor equipment to exchange production data, thereby reducing integration bottlenecks.[2]OMAC, “PackML Standard,” omac.org Together, these technologies reduce validation cycles and support the rapid development of products in the cosmetics and nutraceutical industries.

Surge in Demand for Single-Dose Sachet Formats in Foodservice

Quick-service restaurants are transitioning from bulk dispensers to pre-portioned sachets to enhance hygiene and reduce labor costs. SIG’s Motion Servo Series produces up to 240 pouches per minute, meeting commissary throughput targets. ProMach’s Bartelt MAG-R, introduced for PACK EXPO 2025, integrates multi-lane rotary piston dosing to handle viscous sauces at similar speeds. Pre-measured units simplify allergen tracking under menu-labeling laws, while labor-scarce kitchens gain consistent portion control. North American and European operators adopt these formats the fastest, but franchise expansions in the Asia-Pacific region are amplifying downstream equipment orders. As sachet volumes rise, demand concentrates on high-speed horizontal form-fill-seal and servo piston technology that maintains ±0.5% fill accuracy even with shear-sensitive condiments.

Growth of Eco-Design Plastic Tubes for Cosmetics

The EU Packaging and Packaging Waste Regulation mandates 30% recycled content by 2030, prompting cosmetics brands to adopt post-consumer resin tubes. L’Oréal’s pledge to reach 100% recycled or bio-based plastics intensifies equipment retrofits for ultrasonic sealing and in-line vision systems that detect micro-cracks in recycled substrates. ALPMA’s FreshPack platform shows how controlled-atmosphere filling extends shelf life in eco-designed packaging. These initiatives require material-traceability software in filler controls to satisfy extended producer responsibility audits. Although recycled HDPE increases oxygen transmission, tube-filler suppliers are refining seal geometries and inert-gas purging to protect oxidation-sensitive actives such as retinol.

Compliance-Driven Automation in Pharma Fill-Finish

The FDA’s September 2024 draft guidance elevates requirements for environmental monitoring and media-fill validation, accelerating investment in closed-system isolator lines. Syntegon’s Versynta FFP integrates robotic depyrogenation, in-line weighing, and automated stopper placement to minimize human intervention. Watson-Marlow’s Flexicon units maintain ±0.5% accuracy from 0.5 to 250 ml, which is essential for high-value biologics where overfilling erodes margins. EMA Annex 1, revised in 2022, reinforces the importance of real-time particulate monitoring, nudging suppliers to embed Industry 4.0 sensor arrays. These combined pressures make validated, robotic fill-finish platforms an imperative rather than a capital luxury.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High CAPEX for servo-driven rotary fillers High CAPEX for servo-driven rotary fillers | -0.6% | Global, most severe for SMEs in emerging markets | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.6% | Geographic Relevance:Global, most severe for SMEs in emerging markets | Impact Timeline:Short term (≤ 2 years) |

Viscosity-induced accuracy challenges at high RPM Viscosity-induced accuracy challenges at high RPM | -0.4% | Global, impacting pharma and cosmetics | Medium term (2-4 years) | |||

Limited skilled workforce for PLC-based maintenance Limited skilled workforce for PLC-based maintenance | -0.5% | Asia-Pacific, Latin America, Middle East and Africa | Medium term (2-4 years) | |||

Bi-directional contamination risks with recycled PCR packaging Bi-directional contamination risks with recycled PCR packaging | -0.3% | Europe and North America | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High CAPEX for Servo-Driven Rotary Fillers

Precision rotary fillers cost USD 500,000-1,500,000, a hurdle for SMEs, especially when banks demand 30-40% down payments and charge interest rates several hundred basis points above those in developed markets.[3]Jornen Machinery, “NF60A Tube Filler,” jornen.com Leasing options are emerging, yet lessors bear the residual-value risk amid rapid technological obsolescence. Chinese vendors price their equipment 40-60% below that of European counterparts, but buyers often sacrifice access to global support networks. ProMach’s 2024 acquisition spree signals likely consolidation around proprietary control platforms, possibly increasing switching costs.

Limited Skilled Workforce for PLC-Based Maintenance

Advanced fillers rely on multi-axis motion controllers, smart sensors, and cloud gateways; however, emerging-market plants often lack technicians conversant with these systems. Downtime linked to PLC diagnostics or Industry 4.0 protocols reduces line availability and increases reliance on OEM service contracts, which are scarce in rural areas. Governments in India and Brazil have launched vocational grants, but the throughput of certifications still lags behind installed-base growth by an estimated 15%. Without skilled labor, ultrahigh-speed fillers risk suboptimal utilization, which reduces ROI.

Segment Analysis

By Packaging Material: Circular Mandates Pressure Plastic Leadership

Plastic held the largest share of the pasty products filling machine market at 44.66% in 2025, buoyed by cost-effectiveness and compatibility with rotary piston systems. Other materials are forecast to post an 8.52% CAGR, the quickest among the group, as bio-based polyethylene, hybrid laminates, and compostable films gain traction. EU recycled-content rules intensify the shift, prompting fillers to integrate material-traceability and ultrasonic sealing upgrades. The pasty products filling machine market size linked to bio-based substrates is thus set for outsized expansion. Nevertheless, lingering validation issues around PCR contamination keep metal and glass tubes relevant for oxygen-sensitive formulations.

As luxury cosmetics adopt aluminum for premium aesthetics and pharmaceutical ointments favor metal’s barrier properties, equipment suppliers are refining crimping modules to accommodate mixed-material portfolios. Glass remains a niche material, dedicated to inert, sterile applications where breakage mitigation requires specialized handling. The sustainability narrative, coupled with consumer preference for low-carbon packaging, positions new-generation fillers with fuse-weld seals and adaptive torque control as pivotal to future revenue streams.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Pharma Automation Outpaces Food Volume

Food applications dominated with a 36.43% share in 2025, thanks to high-throughput condiment and spread lines. Still, pharmaceutical users are projected to log the highest growth at an 7.89% CAGR through 2031 as aseptic regulations tighten. This shift will increase the market size of pasty products filling machines attributable to pharma lines, even though absolute unit volumes remain lower than those for food. Compliance investments include isolators, nested-syringe platforms, and inline weigh systems that guarantee ±0.5% accuracy, reducing overfill in high-value biologics.

Food producers continue retrofitting legacy lines for single-serve formats, but margin pressure constrains capital outlay. Cosmetics, nutraceuticals, and household products form a mid-sized cohort, driving demand for versatile tube fillers that can handle post-consumer resin packaging. Contract packers serving these segments favor modular designs that shorten changeovers, thereby reinforcing the uptake of linear volumetric systems.

By Filling Technology: Linear Volumetric Gains on Flexibility

Rotary piston systems captured a 38.52% share in 2025, favored for validated pharmaceutical and cosmetics lines where repeatability is paramount. Linear volumetric machines are rising at a 7.23% CAGR, propelled by contract manufacturers managing short runs across diverse SKUs. Advanced PLC software that stores recipe-specific cam profiles reduces setup time to under 15 minutes, a compelling proposition for markets with seasonal or promotional production.

Vacuum and pressure fillers occupy specialist niches, such as mayonnaise or aerated creams, where foaming must be minimized. Peristaltic solutions address micro-batch biologics, albeit at lower throughput. As brand owners pursue SKU proliferation tied to digital marketing campaigns, the flexibility premium will sustain linear volumetric momentum despite rotary piston incumbency.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Operation Mode: Semi-Automatic Systems Ride Artisan Resurgence

Automatic units accounted for a 53.19% share in 2025, driven by pharmaceutical and multinational food installations. Semi-automatic platforms, however, are forecast to post a 7.46% CAGR as European artisan producers leverage subsidies covering a third of capex. These fillers accommodate batch sizes of 500-5,000 units without expensive format parts, meeting provenance-driven consumer demand for local products.

Automatic isolator lines remain the preferred choice for sterile pharmaceuticals and high-volume cosmetics, where human intervention risks contamination. Manual fillers persist in R&D and pilot plants, supporting formulation screening and limited-edition runs. The pasty products filling machine industry, therefore, spans a continuum from manual benchtop models to robotic, closed-system islands capable of 80,000 units per hour.

Note: Segment shares of all individual segments available upon report purchase

By Production Speed: Ultra-High-Speed Lines Serve Pharma and QSR

Machines operating at 61-180 cycles per minute held a 46.62% share in 2025, striking a balance between speed and cost for mainstream applications. Units exceeding 180 cycles are forecast to grow at an 8.03% CAGR as pharma fill-finish and foodservice sachet demand escalates. AI-driven control loops maintain accuracy with shear-thinning pastes, addressing a historical bottleneck above 180 RPM. Artisan producers and contract packers in emerging markets maintain demand for models with ≤60 cycles that minimize capital burn while supporting niche flavors and limited editions.

Viscosity-induced accuracy challenges intensify at ultra-high speeds, pushing OEMs to introduce real-time rheology compensation modules. Where those upgrades remain cost-prohibitive, time-pressure fillers with adaptive dwell control offer a middle ground, preserving cycle rates without compromising dose uniformity.

Geography Analysis

The Asia-Pacific led the pasty products filling machine market with a 33.96% share in 2025 and is expected to expand at an 8.12% CAGR through 2031. Production-linked incentives in India, growing cosmetics exports from South Korea and Japan, and food processing investments in China underpin this trajectory. Domestic OEMs, such as Jornen and Shanghai CrossQ, supply low-cost, servo-driven equipment, thereby widening adoption among SMEs. Cloud-enabled sensors deployed in Japanese and Korean facilities maximize batch yields by detecting micro-stoppages before they escalate.

Europe ranks second, buoyed by pharmaceutical fill-finish reshoring, subsidy-backed artisan food plants, and early compliance with EU recycled-content mandates. France, Germany, Italy, and Spain host dense clusters that shorten lead times and enable rapid prototyping. Zalkin’s 2024 expansion in France illustrates localized capacity investment to meet new tethered-cap rules. The region also pioneers circular-economy packaging, spurring demand for fillers with advanced seal integrity checks.

North America maintains a sizable installed base driven by FDA guidance-led pharma upgrades and foodservice sachet rollouts. ProMach’s multi-brand roll-up strategy and JBT’s acquisition of Marel enhance turnkey line availability for local buyers. Labor shortages intensify the adoption of automation, especially in quick-service restaurants that are migrating to touch-free condiments. Latin American growth is anchored in contract packing in Brazil and Mexico, while investments in halal-certified production in the Middle East add new demand layers, notably from the UAE and Saudi Arabia.

Competitive Landscape

Market Concentration

The pasty products filling machine market remains moderately fragmented. European specialists IMA, Syntegon, and Coesia dominate pharma and cosmetics niches with validated, high-speed platforms. Chinese vendors, such as Shanghai CrossQ and Jornen, compete on price, capturing the food and household segments with servo upgrades. ProMach’s eight-brand acquisition streak from 2024-2025 positions it as a global turnkey supplier spanning fillers, cappers, labeling, and end-of-line solutions. JBT’s 2025 merger with Marel broadens reach into protein processing and liquid filling, enabling cross-selling across shared accounts.

Innovation pivots on servo motion, AI-driven control, and material compatibility. Krones’ Dynafill and Beckhoff’s XTS exemplify AI- and PC-based motion ecosystems that reduce footprints while increasing throughput. Emerging disruptors from Taiwan and mainland China are embracing open-source PLCs to mitigate vendor lock-in. Niche players, such as Watson-Marlow, address micro-batch biologics with peristaltic fill accuracies of ±0.5%, carving out defensible slots where product value outweighs line speed.

Pasty Products Filling Machine Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: ProMach unveiled the Bartelt MAG-R rotary horizontal form-fill-seal pouch machine, reaching 240 pouches per minute for viscous sauces.

- January 2025: JBT closed its USD 3.6 billion acquisition of Marel, expanding its protein processing and liquid filling footprint.

- October 2024: ProMach bought HMC Products, bolstering horizontal form-fill-seal capability for sachets.

- July 2024: ProMach acquired MBF to enhance wine and spirits filling solutions.

Table of Contents for Pasty Products Filling Machine Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rapid Adoption of Industry 4.0 Enabled Filling Lines

- 4.2.2Surge in Demand for Single-Dose Sachet Formats in Foodservice

- 4.2.3Growth of Eco-Design Plastic Tubes for Cosmetics

- 4.2.4Compliance-Driven Automation in Pharma Fill-Finish

- 4.2.5Expansion of Contract Packing in Emerging Economies

- 4.2.6Re-shoring of Artisan Food Production in Europe

- 4.3Market Restraints

- 4.3.1High CAPEX for Servo-Driven Rotary Fillers

- 4.3.2Viscosity-Induced Accuracy Challenges at High RPM

- 4.3.3Limited Skilled Workforce for PLC-Based Maintenance

- 4.3.4Bi-directional Contamination Risks with Recycled PCR Packaging

- 4.4Industry Value Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitute Products

- 4.7.5Intensity of Competitive Rivalry

- 4.8The Impact of Macroeconomic Factors on the Market

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Packaging Material

- 5.1.1Plastic

- 5.1.2Metal

- 5.1.3Glass

- 5.1.4Other Packaging Materials

- 5.2By End-User Industry

- 5.2.1Food

- 5.2.2Household and Cosmetics

- 5.2.3Pharma

- 5.2.4Other End-User Industries

- 5.3By Filling Technology

- 5.3.1Rotary Piston Fillers

- 5.3.2Linear Volumetric Fillers

- 5.3.3Vacuum and Pressure Fillers

- 5.4By Operation Mode

- 5.4.1Automatic

- 5.4.2Semi-Automatic

- 5.4.3Manual

- 5.5By Production Speed

- 5.5.1Up to 60 CPM

- 5.5.261-180 CPM

- 5.5.3Above 180 CPM

- 5.6By Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2South America

- 5.6.2.1Brazil

- 5.6.2.2Argentina

- 5.6.2.3Rest of South America

- 5.6.3Europe

- 5.6.3.1Germany

- 5.6.3.2France

- 5.6.3.3United Kingdom

- 5.6.3.4Italy

- 5.6.3.5Spain

- 5.6.3.6Russia

- 5.6.3.7Rest of Europe

- 5.6.4Asia-Pacific

- 5.6.4.1China

- 5.6.4.2Japan

- 5.6.4.3India

- 5.6.4.4South Korea

- 5.6.4.5Australia

- 5.6.4.6Rest of Asia-Pacific

- 5.6.5Middle East and Africa

- 5.6.5.1Middle East

- 5.6.5.1.1Saudi Arabia

- 5.6.5.1.2United Arab Emirates

- 5.6.5.1.3Turkey

- 5.6.5.1.4Rest of Middle East

- 5.6.5.2Africa

- 5.6.5.2.1South Africa

- 5.6.5.2.2Egypt

- 5.6.5.2.3Nigeria

- 5.6.5.2.4Rest of Africa

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1IMA S.p.A.

- 6.4.2Syntegon Technology GmbH

- 6.4.3Coesia S.p.A.

- 6.4.4JBT Corporation

- 6.4.5ProMach Inc.

- 6.4.6Chabot Delrieu Associes

- 6.4.7ALPMA Alpenland Maschinenbau GmbH

- 6.4.8Shanghai CrossQ Automation Equipment Co., Ltd.

- 6.4.9Dongguang Sammi Packing Machine Co., Ltd.

- 6.4.10Jornen Machinery Co., Ltd.

- 6.4.11Nima Erreti Packaging S.r.l.

- 6.4.12Neostarpack Co., Ltd.

- 6.4.13WALDNER Dosomat GmbH and Co. KG

- 6.4.14Wenzhou Hofen Packing Machinery Co., Ltd.

- 6.4.15Hunan Grand Packaging Co., Ltd.

- 6.4.16Accutek Packaging Equipment Company, Inc.

- 6.4.17Filamatic Inc.

- 6.4.18Watson-Marlow Fluid Technology Group

- 6.4.19Shemesh Automation Ltd.

- 6.4.20Oystar USA Technologies, Inc.

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1White-Space and Unmet-Need Assessment

Global Pasty Products Filling Machine Market Report Scope

The scope of the Pasty Products Filling Machine Market report encompasses an examination of equipment designed for filling viscous, semi-solid, and paste-like products across various industries, including food, cosmetics, pharmaceuticals, chemicals, and related sectors. The report outlines the key machine types used in the handling of high-viscosity materials, including automatic, semi-automatic, rotary, piston-based, servo-driven, and volumetric filling systems. The study describes the operational characteristics, accuracy requirements, hygiene standards, and technological capabilities associated with pasty product filling solutions.

The Pasty Products Filling Machine Market Report is Segmented by Packaging Material (Plastic, Metal, Glass, Other Packaging Materials), End-User (Food, Household and Cosmetics, Pharma, Other End-Users), Filling Technology (Rotary Piston Fillers, Linear Volumetric Fillers, Vacuum and Pressure Fillers), Operation Mode (Automatic, Semi-Automatic, Manual), Production Speed (Up to 60 CPM, 61-180 CPM, Above 180 CPM), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).