Semi-Automatic And Manual Filling Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

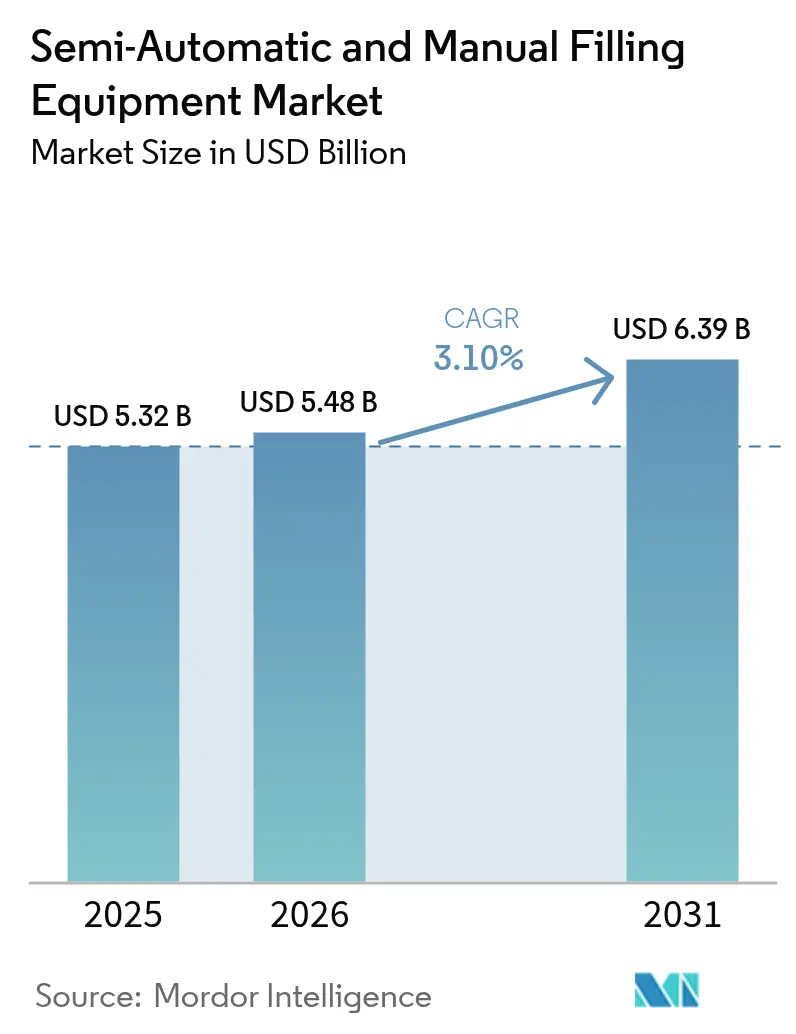

| Market Size (2026) | USD 5.48 Billion |

| Market Size (2031) | USD 6.39 Billion |

| Growth Rate (2026 - 2031) | 3.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Semi-Automatic And Manual Filling Equipment Market Analysis by Mordor Intelligence

The Semi-Automatic and Manual filling equipment market size in 2026 is estimated at USD 5.48 billion, growing from 2025 value of USD 5.32 billion with 2031 projections showing USD 6.39 billion, growing at 3.10% CAGR over 2026-2031. Current expansion hinges on steady demand for adaptable, lower-capital-expenditure machinery that helps manufacturers align throughput with fluctuating order volumes while complying with tightening food and drug regulations. Semi-automatic systems hold 86.43% of the 2024 Semi-Automatic and Manual filling equipment market share because they combine modest automation benefits with quick format changeovers that suit mid-scale enterprises. Craft beverage growth, personalized pharma batches, and modular upgrades that create incremental capacity all reinforce purchasing activity. Competitive intensity remains high as European incumbents and emerging Asian vendors offer modular designs and built-in data logging to satisfy electronic batch record rules.

Key Report Takeaways

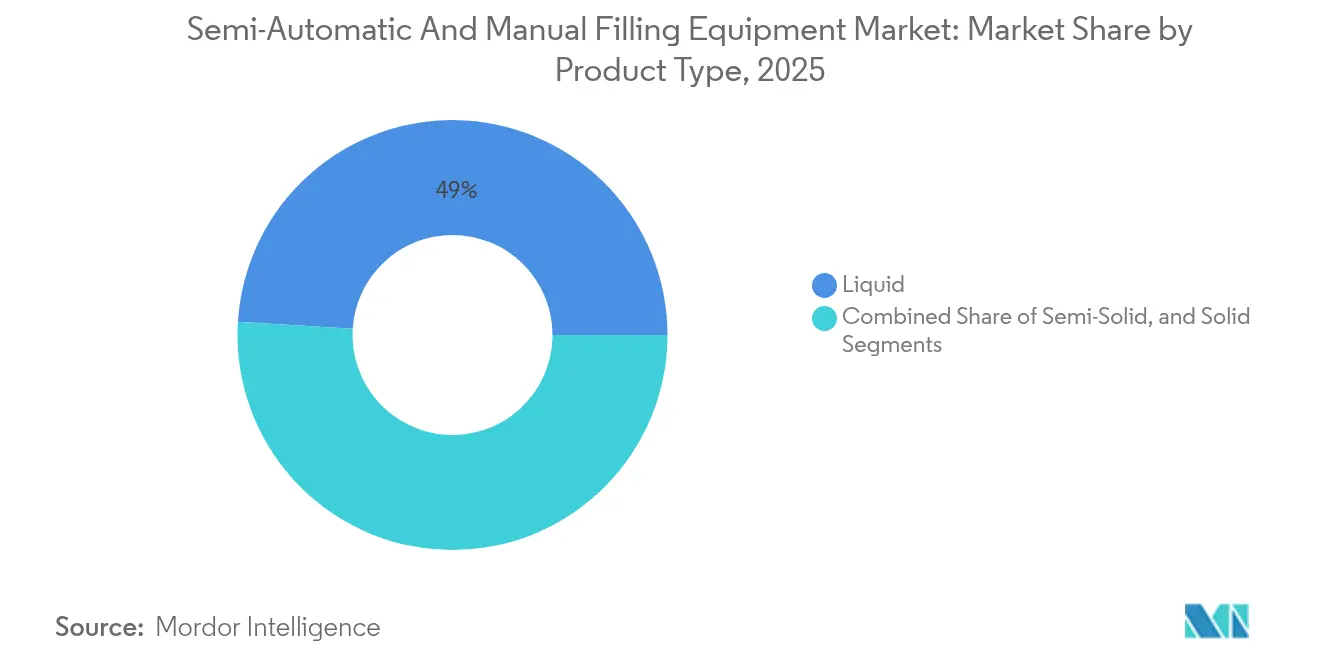

- By product type, liquid applications captured 49.02% of the semi-automatic and manual filling equipment market share in 2025.

- By end-user industry, the market size for food processing is forecast to advance at a 4.12% CAGR through 2031.

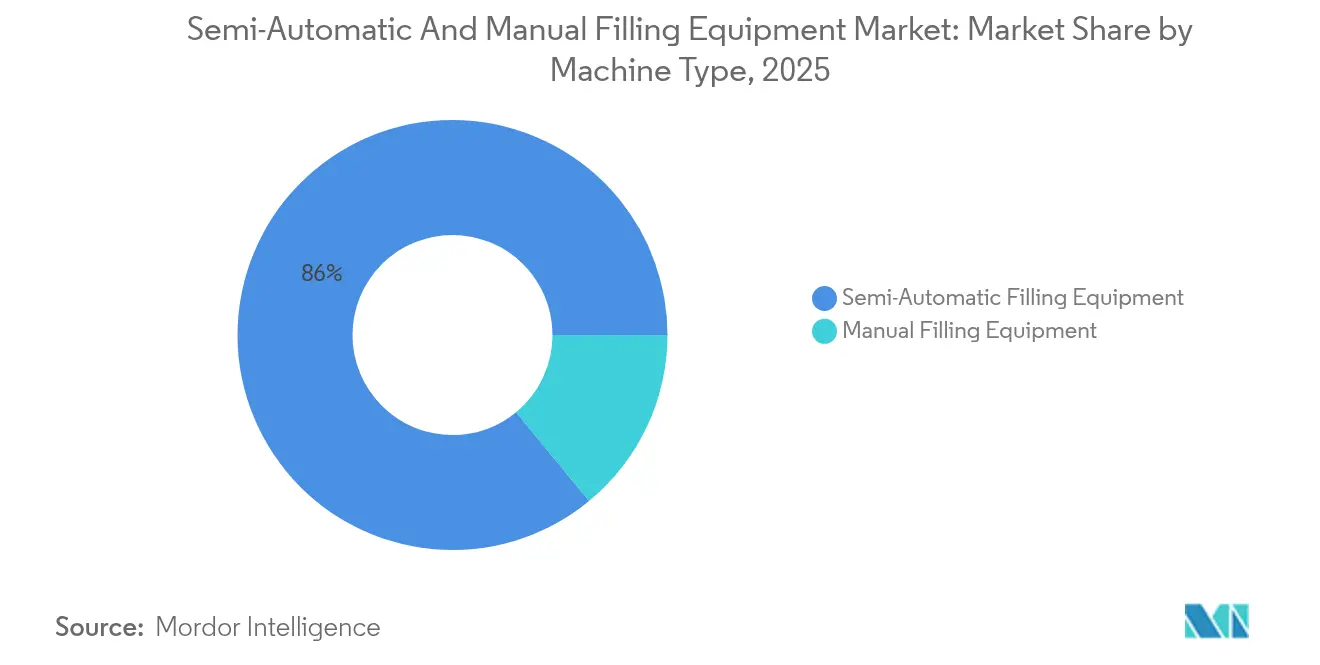

- By machine type, semi-automatic systems captured 85.96% of the semi-automatic and manual filling equipment market share in 2025.

- By container type, the market size for pouches and sachets is forecast to advance at a 3.78% CAGR through 2031.

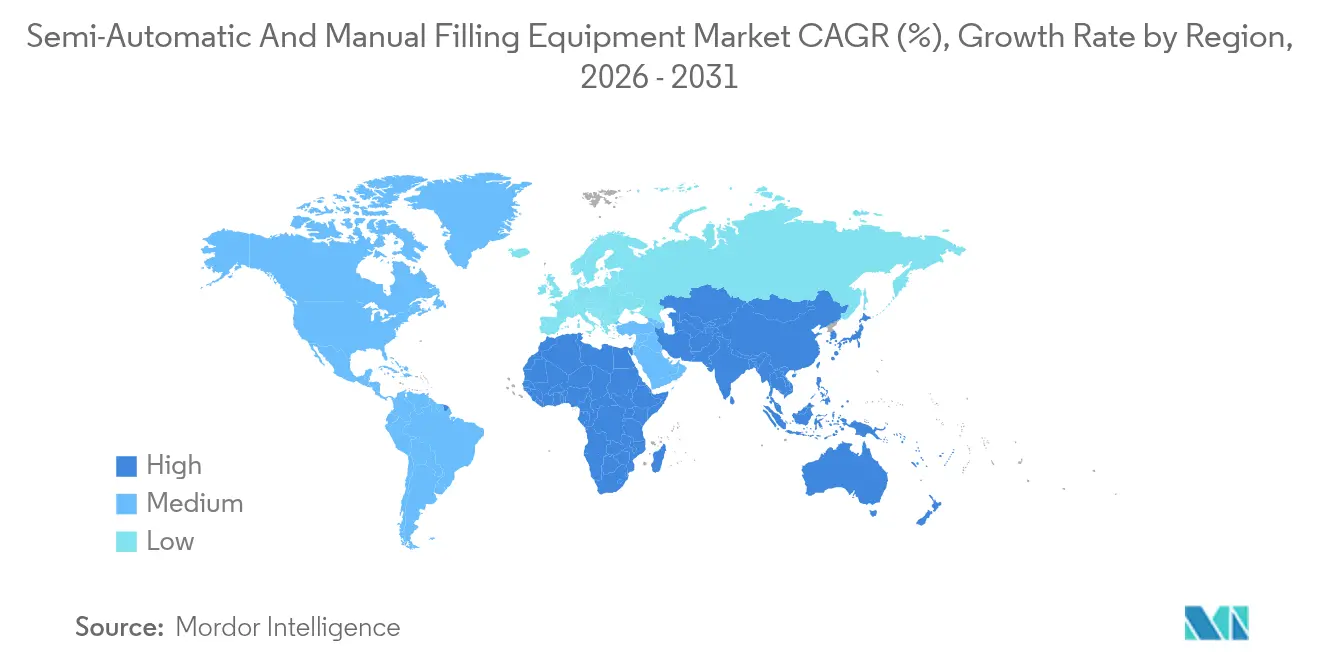

- By geography, Asia-Pacific captured 43.12% of the semi-automatic and manual filling equipment market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Semi-Automatic And Manual Filling Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Adoption of Modular Semi-Automatic Lines by SME Food Processors | +0.8% | Global, early gains in Asia-Pacific and North America | Medium term (2-4 years) |

| Surge in Low-Volume Personalised Pharma Production Needing Manual Fillers | +0.6% | North America and EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Expansion of Craft Beverage Brands Demanding Flexible Filling Solutions | +0.5% | North America core, spill-over to EU and APAC | Short term (≤ 2 years) |

| Regulatory Push for E-Batch Records Spurring Smart Semi-Automatic Retrofits | +0.4% | Global, led by FDA and EU compliance regions | Medium term (2-4 years) |

| Retail Refill-Station Boom Boosting Portable Manual Fillers | +0.3% | EU & North America, emerging urban Asia-Pacific | Long term (≥ 4 years) |

| Micro-Factory Growth in Emerging Economies Favouring Low-CAPEX Manual Kits | +0.4% | APAC core, expanding to MEA and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Adoption of Modular Semi-Automatic Lines by SME Food Processors

Small and mid-size food companies are investing in modular semi-automatic equipment that permits stepwise scale-up while meeting preventive-control mandates under 21 CFR Part 117.[1]U.S. Food and Drug Administration, “Advanced Manufacturing,” FDA.gov Plug-and-play fillers minimize installation downtime, let processors run seasonal stock-keeping units without extensive retooling, and support the Semi-Automatic and Manual filling equipment market by extending machine life through incremental module swaps. Equipment houses are bundling cloud-based monitoring to capture production data that auditors now request at line-level granularity. Modular skid frames also facilitate relocation when processors move to new food-grade premises, thereby preserving earlier capital investments.

Surge in Low-Volume Personalised Pharma Production Needing Manual Fillers

The move toward patient-specific treatments has increased demand for manual and semi-automatic fillers with precise dose control, suitable for batches that rarely exceed several thousand units. FDA guidance on advanced manufacturing highlights equipment agility over sheer speed. Manual fillers support clinical trial lots and orphan-drug runs where changeovers are frequent and stringent cleaning verification is mandatory. Vendors are integrating closed-loop weight checks and single-use product paths to reduce the risk of cross-contamination. This niche solidifies the Semi-Automatic and Manual filling equipment market, as pharmaceutical buyers favor flexible skids over fixed-format, high-speed lines.

Expansion of Craft Beverage Brands Demanding Flexible Filling Solutions

Alcohol and Tobacco Tax and Trade Bureau data indicate continued growth in licensing among small breweries, cideries, and ready-to-drink cocktail producers.[2]Alcohol and Tobacco Tax and Trade Bureau, “Annual Statistical Report,” TTB.gov Craft players need fillers that shift between bottle sizes, can ends, or keg units in minutes, and semi-automatic variants satisfy this agility gap. Machine builders answer with universal clamps, servo-driven capping heads, and recipe storage for carbonated or nitrogen-infused products. The craft wave thus keeps the Semi-Automatic and Manual filling equipment market vibrant in North America and increasingly in Europe and Asia, where local specialty brands follow similar business models.

Regulatory Push for E-Batch Records Spurring Smart Semi-Automatic Retrofits

FDA 21 CFR Part 211 and parallel EU rules press companies to capture real-time batch data. Retrofitting legacy semi-automatic stations with sensors for temperature, volume, torque, and time stamps provides compliance without scrapping useful hardware. Suppliers now bundle edge-device gateways and validation packs that directly map into electronic batch record platforms. These upgrades extend equipment lifecycles, strengthen audit readiness, and support incremental digitalization, feeding continued purchasing within the Semi-Automatic and Manual filling equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Maintenance and Downtime Costs for Semi-Automatic Machines | -0.7% | Global, particularly affecting emerging markets | Short term (≤ 2 years) |

| Skilled-Operator Shortages in Developing Regions | -0.5% | APAC emerging markets, MEA, and South America | Medium term (2-4 years) |

| Global Phase-Out of Legacy Pneumatics Inflating Retrofit Spend | -0.4% | Global, higher impact in established regions | Long term (≥ 4 years) |

| Volatile Food-Grade Lubricant Pricing Raising Total Cost of Ownership | -0.3% | Global, with raw-material price swings | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Maintenance and Downtime Costs for Semi-Automatic Machines

Semi-automatic fillers introduce pneumatics, servo drives, and PLCs that need scheduled servicing and skilled troubleshooting. Replacement parts for proprietary valves or sensors can be costly, and unplanned stoppages disrupt delivery timetables. ISO/TC 313 prescribes preventive protocols that smaller firms sometimes defer, compounding wear and increasing mean-time-to-repair.[3]International Organization for Standardization, “ISO/TC 313 Packaging Machinery,” ISO.org Resulting OPEX concerns temper purchasing decisions in cash-constrained enterprises within the Semi-Automatic and Manual filling equipment market.

Skilled-Operator Shortages in Developing Regions

Plant expansions in APAC and MEA outpace vocational-training capacity, leaving a gap in technicians able to calibrate nozzles, set torque limits, or run validation cycles. Vendors have begun shipping video-guided maintenance modules and smartphone AR overlays, yet adoption is gradual where internet bandwidth is limited. Skills scarcity curbs utilization rates and slows new deployments in those regional slices of the Semi-Automatic and Manual filling equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Diversified Material Handling Expands Revenue Potential

Liquid formats generated 49.02% of the revenue in 2025, illustrating an enduring alignment between standard nozzle designs and throughput for beverages, pharmaceuticals, and cosmetics. That share anchors the Semi-Automatic and Manual Filling Equipment market, as high-viscosity pumps and CIP-enabled manifolds keep productivity steady. Semi-solid products, although a minority, chart a 3.92% CAGR on the back of premium skincare balms and topical medicines that demand air-free pistons for precise dosing. Vendors bundle heated jackets and vacuum-assist modules to manage viscosity fluctuations, protecting dose repeatability. Solid dosing remains a specialized field that involves capsule filling, seasoning sachets, or vitamin powder sticks, which rely on gravimetric augers versus volumetric pistons. Growth here hinges on the popularity of nutraceuticals rather than mass throughput.

Regulatory attention spans every product class. FDA food-contact rules, as outlined in 21 CFR Part 177, require stainless steel wetted components and gaskets to be rated for high-temperature sanitation. The same rules also apply to cosmetic and OTC factories that share equipment between edible and topical SKUs. For solids and semi-solids, single-use contact kits simplify cleaning and demonstrate to auditors that batch segregation is airtight.

By End-User Industry: Beverage Strength Holds While Food Accelerates

Beverages accounted for 24.41% revenue in 2025, reflecting entrenched bottle-and-can infrastructure and sustained craft-brew licensing expansion. Carbonated drink reformulations, hard seltzers, and functional waters continue to require accurate degassing or foam-control modules, which are typically found in semi-automatic lines. Food processing, however, is on pace for a 4.12% CAGR as SME snack and sauce producers convert home-grown processes into commercial volumes. Compliance with the Preventive Controls rule encourages them to purchase pre-validated fillers for allergen changeovers, thereby nudging penetration higher. Pharmaceuticals maintain incremental gains through personalized medicine and orphan-drug policies, which increase demand for flexible, small-footprint skids. Cosmetics and household goods, although smaller slices, leverage brand premiumization utilizing glass droppers, airless pumps, and recyclable aluminum to justify equipment retrofits that support non-traditional containers.

Cross-industry commonalities lie in audit expectations, including batch traceability, hygienic design, and minimized product loss. The Semi-Automatic and Manual filling equipment market, therefore, favors designs that replicate similar hygienic baselines while offering tooling quick swaps for divergent product viscosities.

By Machine Type: Semi-Automatic Architecture Retains Primacy

Machine-type segmentation shows semi-automatic variants with an 85.96% stake and a 3.26% CAGR outlook. Control PLCs paired with manual oversight create the sweet spot for output per capital dollar, which is critical for mid-tier processors. Servo-driven pistons hit up to 40 cycles per minute while retaining hand-fed flexibility for specialty runs. Manual stations continue to sell into bespoke applications vial filling in clinical research, barrel-aged craft ales, or startup condiment lines, where operators require tactile control and visual feedback. Manual models also serve as pilot platforms preceding higher-throughput investments, ensuring a persistent, if niche, addressable pocket within the broader Semi-Automatic and Manual filling equipment market.

Safety regulations amplify the divergence. EU Machinery Directive 2006/42/EC obliges OEMs to integrate guards, e-stops, and interlocks, which can be more easily built into semi-automatic frames. Buyers appreciate the pre-certified CE badges that accelerate factory approvals and reduce insurance premiums.

By Container Type: Flexible Packages Gain Ground Without Displacing Rigid Leaders

Rigid bottles and jars comprised 39.22% receipts in 2025, capitalizing on mature glass and PET supply chains plus consumer familiarity. Semi-automatic monoblocs with rotary turrets manage both carbonated and still liquids, ensuring continued factory reliance. Yet pouches and sachets are projected to grow at a 3.78% CAGR, driven by portability, e-commerce mailing efficiencies, and lower material footprints. Tube applications bring incremental upside for premium skincare and prescription creams, where airless dosing extends shelf life. Cans stay stable, tied to ready-to-drink spirit cocktails and energy drinks, fields that value metal’s barrier properties. The Semi-Automatic and Manual Filling Equipment market consequently sustains a spectrum of tooling kits, ranging from vacuum-grip spouts for doypacks to nitrogen-purge injectors that preserve the headspace of craft beer.

Standards such as 21 CFR Part 177 regulate resin migration, prompting OEMs to utilize UV-resistant polycarbonate shields and quick-release seals to facilitate allergen sanitation. Flexible packaging handling introduces mechanical challenges, including pouch neck support and crease avoidance, which spur R&D budgets and drive competitive IP filings.

Geography Analysis

The Asia-Pacific region held 43.12% of the revenue in 2025 and is projected to advance at a 4.55% CAGR through 2031, making it both the largest and fastest-growing region within the Semi-Automatic and Manual filling equipment market. China’s National Medical Products Administration modernized dossier requirements, prompting pharma line refurbishments that favor data-logging fillers. Simultaneously, ASEAN snack brands are expanding their export footprints and adopting semi-automatic fillers that are compatible with halal and HACCP directives. Government grants for Industry 4.0 upgrades in South Korea and Singapore further subsidize smart retrofits.

North America’s mature base incrementally replaces legacy machines to embed electronic batch records and CIP manifolds. Craft beverage start-ups in the United States and Canada, buoyed by simplified licensing in several states, continue to make brisk manual filler purchases until scale justifies investments in servo-driven cappers. Food-safety litigation risk also motivates U.S. processors to prefer fillers with hygienic certifications, thereby sustaining the aftermarket revenue of the Semi-Automatic and Manual filling equipment market.

Europe matches North American maturity but channels spending toward sustainability, lightweighting bottle projects, and refill kiosk pilots largely in the Benelux and Nordic countries. CE-marked equipment enjoys streamlined customs processing, facilitating EU manufacturers' exports to Middle East hubs. Meanwhile, European Union digital product-passport deliberations are steering capital toward traceability-enabled machines.

South America and the Middle East-Africa cluster trail in absolute terms, yet show rising micro-factory activity. Local snack flavors, herbal extracts, and artisanal household cleaners are entering domestic supermarkets, driving demand for entry-level manual kits. Currency volatility occasionally delays larger capex, but donor-financed food-security programs often bundle semi-automatic fillers into turnkey lines.

Competitive Landscape

The Semi-Automatic and Manual filling equipment market remains fragmented. European stalwarts such as IMA Group, Syntegon Technology, Coesia, and GEA continue to command premium, compliance-ready portfolios. Asian challengers, particularly those from China and South Korea, offer cost-efficient modular frames, thereby narrowing the price gaps. U.S.-based ProMach and JBT Corporation rely on M&A to acquire niche technologies, such as craft-beer mobile fillers or vacuum-assisted tube fillers.

Strategic priorities cluster around Industry 4.0 features, predictive maintenance, OPC-UA connectivity, and AI-assisted anomaly detection. Patent races target quick-release tooling, servo-driven multi-format turrets, and real-time inline weight verification. Sustainability differentiators include low-energy pneumatic circuits and designs optimized for handling post-consumer-recycled resin. Pricing pressure persists, but post-sale service agreements and validation documentation add revenue resilience for established vendors.

Regional service hubs are proliferating in India, Thailand, and Mexico, thereby reducing lead times for parts and on-site technicians. Partnerships with local system integrators help Western brands adapt to domestic voltage standards and language interfaces. Meanwhile, emerging refill-station specialists provide boutique competition, though many license core valve technology from larger OEMs.

Semi-Automatic And Manual Filling Equipment Industry Leaders

IMA Group

Robert Bosch GmbH (Syntegon Technology GmbH)

ProMach Inc.

Coesia S.p.A.

GEA Group AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: IMA Group opened a pharmaceutical filling-equipment plant in Singapore, lifting Asia-Pacific capacity 40% to meet personalized medicine demand and local regulatory filings.

- December 2024: Syntegon Technology secured FDA clearance for a smart filler equipped with real-time batch analytics that satisfy 21 CFR Part 211 electronic record rules.

- November 2024: JBT Corporation bought a boutique manual filler firm geared to craft beverage brands, adding portable tabletop units aimed at seasonal production cycles.

- October 2024: Coesia introduced a modular semi-automatic platform for SME food processors that scales via plug-in dosing heads and complies out-of-box with FSMA.

Global Semi-Automatic And Manual Filling Equipment Market Report Scope

The Semi-Automatic and Manual Filling Equipment provide filling packaging process of solid, semi-solid and liquid products in various container types, vacuum bags, etc, for end users such as in foods, beverages, pharma, cosmetics, etc.

| Solid |

| Semi-Solid |

| Liquid |

| Food |

| Beverage |

| Pharmaceutical |

| Cosmetics and Household |

| Other End-User Industries |

| Semi-Automatic Filling Equipment |

| Manual Filling Equipment |

| Bottles and Jars |

| Pouches and Sachets |

| Cans |

| Tubes |

| Other Container Types |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Solid | ||

| Semi-Solid | |||

| Liquid | |||

| By End-User Industry | Food | ||

| Beverage | |||

| Pharmaceutical | |||

| Cosmetics and Household | |||

| Other End-User Industries | |||

| By Machine Type | Semi-Automatic Filling Equipment | ||

| Manual Filling Equipment | |||

| By Container Type | Bottles and Jars | ||

| Pouches and Sachets | |||

| Cans | |||

| Tubes | |||

| Other Container Types | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the Semi-Automatic and Manual filling equipment market by 2031?

The market is forecast to reach USD 6.39 billion by 2031, reflecting a 3.10% CAGR over 2026-2031.

Which region shows the fastest demand growth for filling equipment?

Asia-Pacific leads with a 4.55% CAGR through 2031, driven by pharmaceutical and food-processing expansion.

Why do semi-automatic machines dominate over manual alternatives?

Semi-automatic systems provide higher throughput and built-in safety features while remaining more affordable than full automation, capturing 85.96% share in 2025.

Which end-user segment is expanding quickest?

Food processing is advancing at a 4.12% CAGR as SME processors adopt compliant, flexible lines.

How are electronic batch record rules influencing equipment design?

Regulators now expect real-time batch data, prompting retrofits with sensors and connectivity to satisfy 21 CFR Part 211 and EU equivalents.

What container trend is reshaping filler specifications?

Demand for pouches and sachets is rising at a 3.78% CAGR, spurring development of pouch-support modules and low-waste dosing valves.

Page last updated on: