Vacuum Fillers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

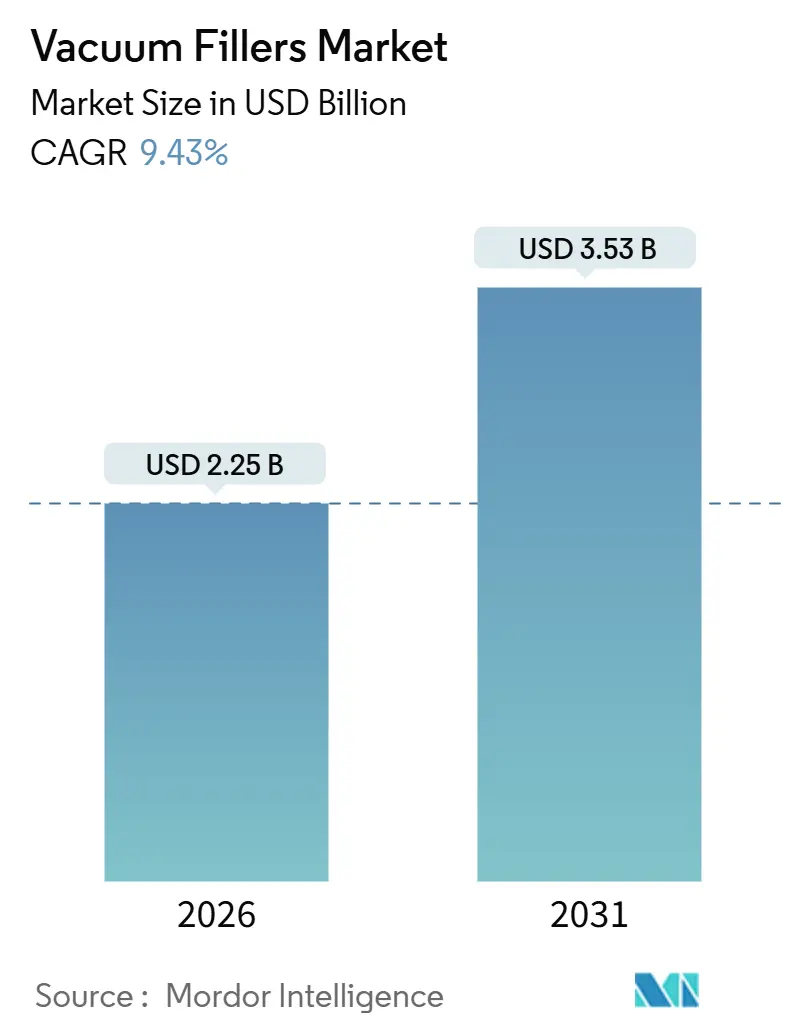

| Market Size (2026) | USD 2.25 Billion |

| Market Size (2031) | USD 3.53 Billion |

| Growth Rate (2026 - 2031) | 9.43% CAGR |

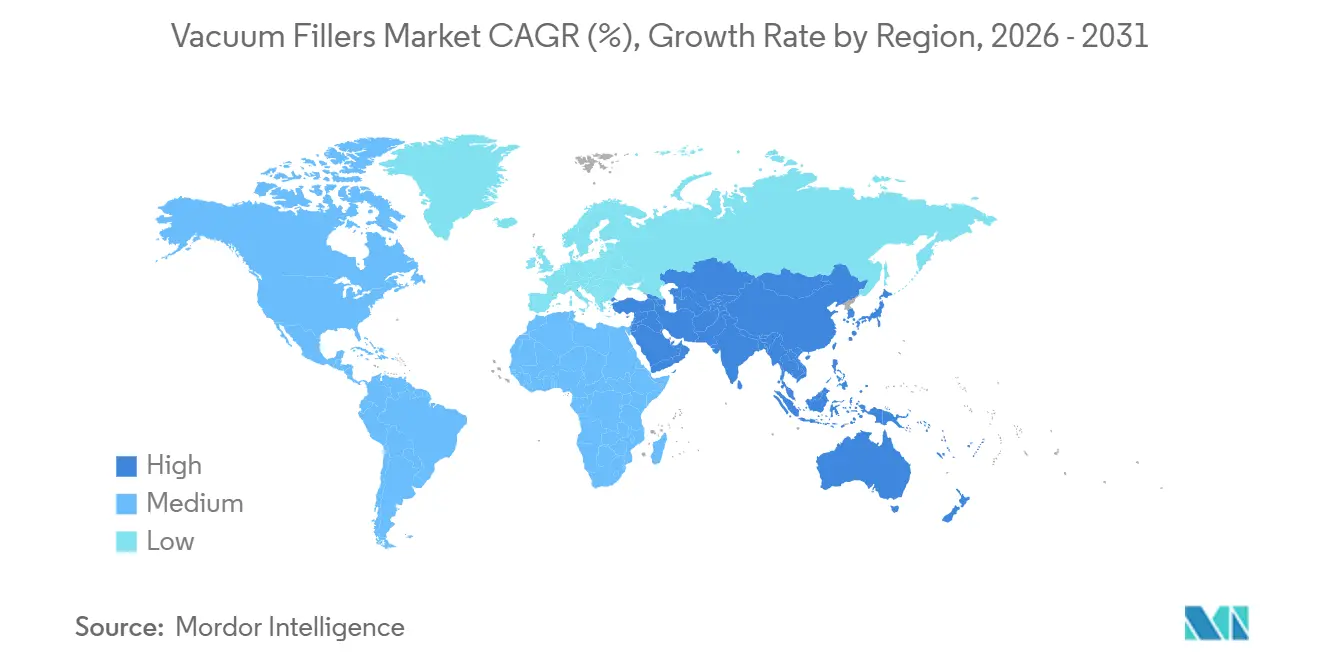

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vacuum Fillers Market Analysis by Mordor Intelligence

The vacuum fillers market size was USD 2.25 billion in 2026 and is projected to reach USD 3.53 billion by 2031, representing a 9.43% CAGR. Strong demand originates from stricter global food-safety rules, rapid automation, and new applications ranging from premium convenience meals to electrolyte dosing in lithium-ion batteries. Rotary systems dominate high-volume food lines, while powder-handling units gain speed in nutraceutical and pharmaceutical plants. Fully automatic equipment outpaces semi-automatic alternatives because connected sensors, machine-learning controls, and predictive maintenance deliver higher line efficiency. Regionally, Europe remains the largest buyer due to its favorable regulatory environment, while the Asia-Pacific region registers the fastest expansion, thanks to the expansion of food processing capacity and a booming EV battery ecosystem. Competitive pressure intensifies as German and Italian firms safeguard their intellectual property and service depth against cost-competitive Asian entrants that specialize in niche machines for the battery and cosmetics industries.

Key Report Takeaways

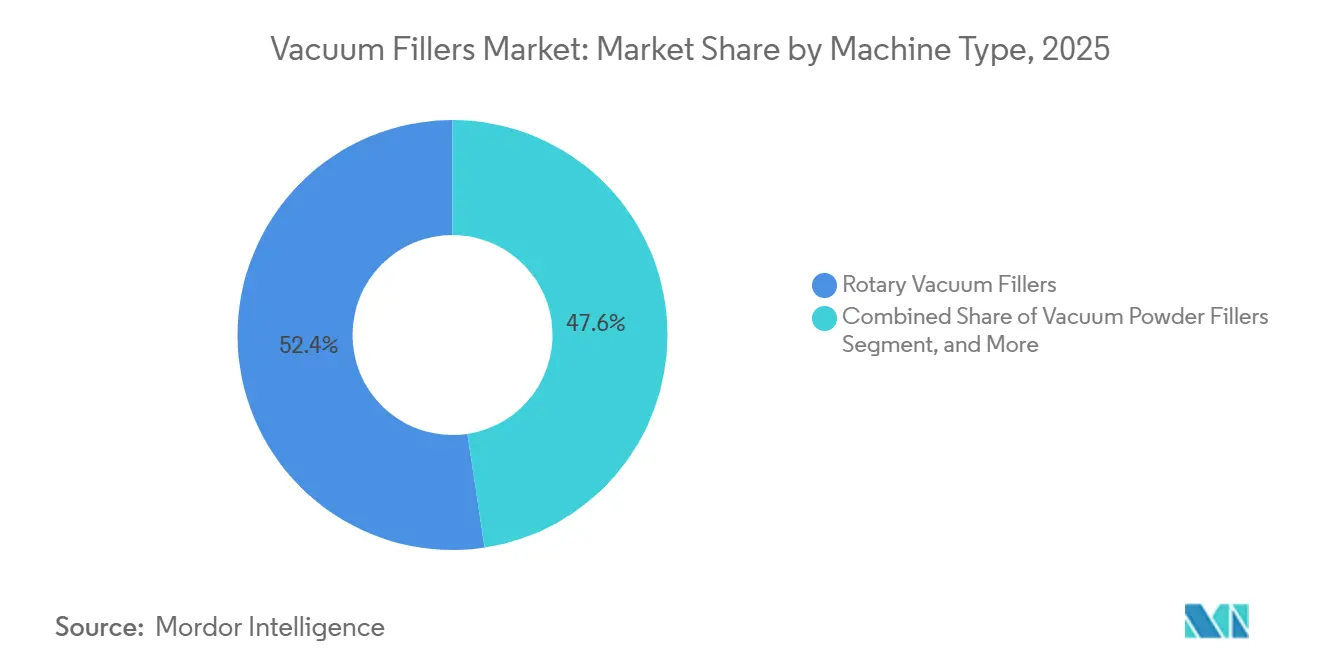

- By machine type, rotary vacuum fillers accounted for 52.38% of the vacuum fillers market share in 2025. However, vacuum powder fillers are forecasted to grow at a 11.67% CAGR during the forecast period.

- By automation level, fully automatic systems held a 68.93% market share of the vacuum fillers market in 2025 and is projected to grow at a 10.93% CAGR between 2026 and 2031.

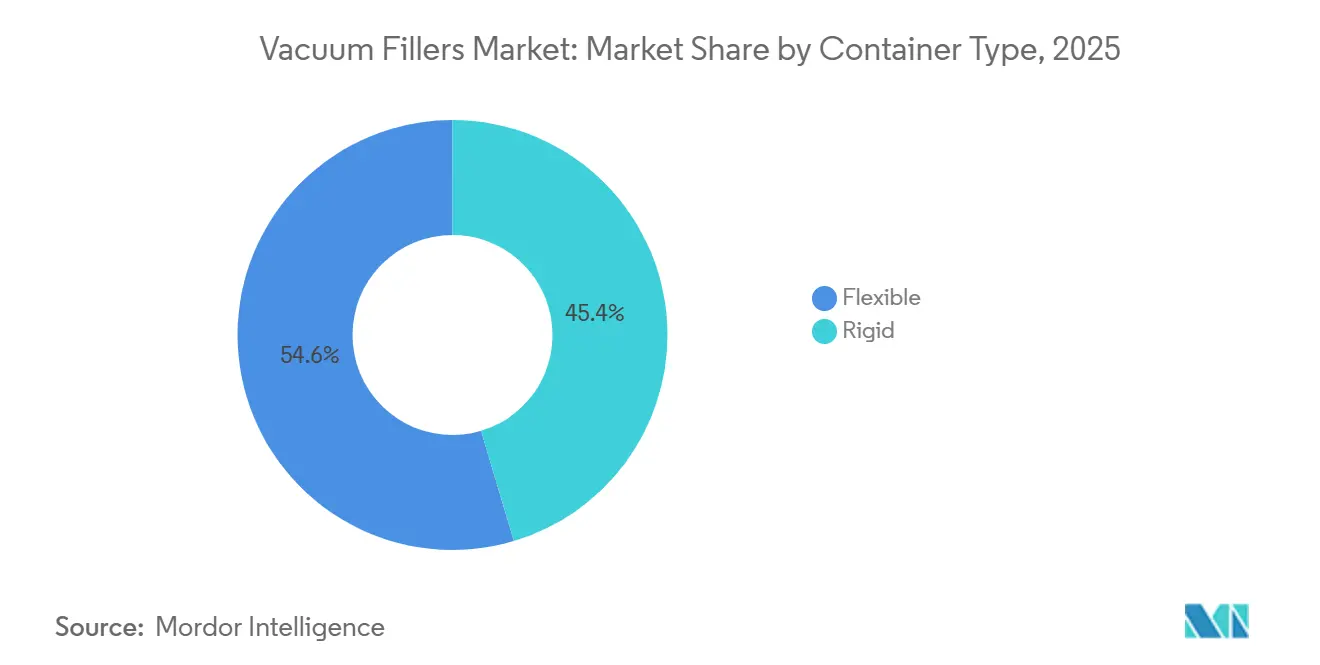

- By container type, the flexible container type captured 45.39% of the vacuum fillers market share in 2025 and is projected to grow at an 11.78% CAGR from 2026 to 2031.

- By end-user industry, food and beverage processors accounted for 48.72% of the market share in the vacuum fillers market. In comparison, the cosmetics and personal care segment is projected to grow at a 11.47% CAGR between 2026 and 2031.

- By geography, Europe captured 34.51% of the vacuum fillers market share in 2025. However, the Asia-Pacific region is projected to post an 11.59% CAGR during the forecast period.

Global Vacuum Fillers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising need to extend shelf life | +2.1% | North America, Europe, global | Medium term (2-4 years) |

| Boom in convenience and ready-meal production | +1.8% | Asia-Pacific urban centers, global | Short term (≤ 2 years) |

| Automation and Industry 4.0 integration | +1.2% | Europe and North America core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Stronger food-safety mandates post-2027 | +0.9% | Developed markets, global | Long term (≥ 4 years) |

| Growth of EV-battery electrolyte filling | +1.1% | Asia-Pacific core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Government Industry 4.0 subsidy programs | +0.4% | Europe and Asia-Pacific, selective in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Need to Extend Shelf Life

Manufacturers adopt vacuum filling because it removes oxygen, which accelerates spoilage, thereby expanding their distribution reach and reducing waste. Lepore Mare’s switch to Darfresh vacuum skin packaging reduced material volume by 50% and extended seafood shelf life by 30% with the help of Sealed Air. Such gains align with the EU Packaging and Packaging Waste Regulation, which aims to minimize space from 2030, creating a clear cost-benefit path for switching to vacuum technology.

Boom in Convenience and Ready-Meal Production

Urban consumers favor ready meals that look fresh and command restaurant-quality presentation. Roughly 59.9% of ready-to-cook meat now uses vacuum or modified-atmosphere methods to preserve color and flavor. Vacuum fillers enable the precise portioning of multi-component meals, eliminate air pockets, and prevent sauces from migrating, which improves shelf visibility and reduces retailer rejections.

Automation and Industry 4.0 Integration of Filling Lines

Factory digitalization accelerates demand for networked vacuum fillers that run predictive maintenance and real-time quality analytics. German mechanical-engineering firms report broad rollouts of such connected systems across the EUR 910 billion machinery sector.[1]German Mechanical Engineering Federation, “Industry Report 2024,” VDMA, vdma.org IoT-equipped fillers track vacuum levels, seal quality, and product viscosity, adjusting parameters on the fly to hold yield losses below 0.3%, while collaborative robots handle tray loading and palletizing tasks.

Growth of EV-Battery Electrolyte Vacuum Filling Demand

High-purity electrolytes are sensitive to air and moisture, making vacuum conditions mandatory. Asia-Pacific battery plants now specify negative-pressure dispensers that can reach up to 3,000 portions per minute. Equipment suppliers retrofit food-grade stainless units with solvent-compatible seals, unlocking an additional multi-million-dollar line opportunity beyond traditional food processing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capital expenditure | -1.3% | Global, sharper in developing markets | Short term (≤ 2 years) |

| Availability of low-cost gravity/piston alternatives | -0.8% | Price-sensitive applications in developing markets | Medium term (2-4 years) |

| Shortage of skilled vacuum-equipment technicians | -0.6% | Global, acute in developed markets | Medium term (2-4 years) |

| Compatibility issues with next-gen eco-packaging films | -0.5% | Europe and North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Expenditure

Fully featured vacuum lines can exceed USD 500,000, and when integration, staff training, and validation are factored in, total cash outlays may exceed USD 700,000 for mid-volume plants. Smaller companies, especially in developing countries, struggle to finance such upgrades and instead extend the life of gravity fillers.

Availability of Low-Cost Gravity / Piston Alternatives

Servo-driven piston machines now achieve accuracy differences of under 0.5 grams compared to vacuum systems, with capital costs often 40-60% lower. Regional suppliers offer in-market services, easing spare parts logistics and delaying the need for vacuum conversion for commodity products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Rotary Systems Drive Volume Production

Rotary vacuum fillers captured a 52.38% share of the vacuum fillers market in 2025, reflecting their suitability for continuous, high-speed production lines for meat, dairy, and ready meals. These systems process up to 57,600 cups per hour and maintain a fill-weight variance of less than 0.2%. Linear fillers and aseptic models serve lower-volume or sterile niches, while vacuum powder filler machines are forecasted to grow at an 11.67% CAGR as nutraceutical makers demand zero-air dosing.

Manufacturers redesign platforms for flexibility. IMA’s Hamba Flexline shifts from four to 12 cups per cycle without stopping the conveyor and integrates UV sterilization in the turret.[2]Kevin Cronin, “IMA Food North America Introduces Cup Fill-Seal System,” Powder & Bulk Solids, powderbulksolids.com Such modularity helps plants consolidate SKUs, reduce changeovers, and increase overall equipment effectiveness to over 85%. Servo drives and recipe-based control software blur old boundaries, allowing one frame to run both paste and particulate soups.

By Automation Level: Full Automation Accelerates

Fully automatic systems held a 68.93% market share of the vacuum fillers market in 2025, with a 10.93% CAGR, surpassing semi-automatic units. Labor scarcity and a median wage increase of more than 5% in the EU food sector are tilting investments toward hands-free lines. Real-time analytics reduce rework and enable remote technical support, resulting in an 18% decrease in unplanned downtime at one Midwest condiment plant.

Government grants for Industry 4.0 further quicken payback. Subsidy guidelines often stipulate machine connectivity, digital twins, and cybersecurity protocols, features that semi-automatic systems rarely offer. Meanwhile, collaborative robots now handle highly viscous or foam-forming products, eliminating repetitive strain injuries and reducing workers' compensation premiums.

By Container Type: Flexible Packaging Gains Momentum

The flexible container type retained a 54.61% share in 2025, but is expected to grow at a 11.78% CAGR as brands reduce material intensity and logistics costs. Vacuum skin packs can halve packaging volume and still extend shelf life, helping seafood brands enter distant markets. Cosmetics brands are adopting airless pouches that preserve active ingredients and provide consumers with controlled dosing, thereby enhancing product efficacy.

New filler heads use gentle vacuum ramps and pulsating inflow to prevent bubbles in flexible fields. Seal-integrity sensors now verify 100% of packages to compensate for the lower rigidity of film structures. The EU’s 2030 minimization rule, which caps space at 50%, reinforces the shift.

By End-user Industry: Food Dominance with Cosmetics Surge

Food and beverage processors accounted for 48.72% of the 2025 equipment demand, driven by investments in ready meals, processed meat, and dairy. Compliance with Hazard Analysis and Preventive Controls drives adoption of hygienic, wash-down designs. Pharmaceutical demand is expanding steadily as generics capacity increases in India and Central Europe.

The cosmetics and personal care segment registers an 11.47% CAGR, fueled by premium serums and air-sensitive formulations that oxidize under gravity filling. A recent Chinese patent describes a negative-pressure filling method for eye cream jars that reduces pump sizes and lowers power consumption. Suppliers add nitrogen-blanket modules and micro-piston dosing for costly actives, lifting the margin per machine.

Geography Analysis

Europe’s leadership rests on a 34.51% revenue share in 2025 and long-standing clusters of precision engineering in Germany and Italy. Multivac, GEA, and Krones utilize extensive supplier networks and adhere to rigorous EN 1672-2 hygiene standards to export high-specification machines worldwide. EU Digital Compass funds encourage factories to digitalize, which sustains demand for connected fillers.

The Asia-Pacific region is projected to post an 11.59% CAGR as urban households expand their chilled and frozen food budgets, and nations accelerate battery production. Chinese overcapacity suppresses average selling prices yet also accelerates domestic demand because turnkey lines become affordable for tier-2 processors. South Korea and India launch “Make-in-Country” incentives, including import-duty rebates on automation components.

North America shows mid-single-digit growth driven by protein processors' reshoring production and beverage companies' shifting to recyclable packs. The Middle East imported EUR 1.3 billion of packaging machinery in 2024, reinforcing long-term growth prospects for vacuum fillers in the halal protein, dairy, and high-temperature desert sectors. South America remains a strategic market, as currency volatility hinders equipment financing; however, agricultural export processors continue to automate in order to meet phytosanitary protocols.

Competitive Landscape

The vacuum fillers market contains a moderate number of global manufacturers alongside dozens of regional specialists. The top five firms account for an estimated 45% collective revenue, leaving room for mid-tier players that innovate in narrow niches. German and Italian brands defend their share through patent portfolios, lifetime service contracts, and integration platforms that tie fillers to weighers, sealers, and X-ray units.

Asian challengers differentiate on cost and rapid customization, especially for battery and cosmetics devices. Mikrouna and Tmax Equipments tailor solvent-compatible seals and Class 100 enclosures for electrolyte lines. European incumbents respond by acquiring pump makers, such as Krones’ purchase of Ampco in 2024, to broaden hygienic handling portfolios.[3]Krones AG Investor Relations, “Annual Report 2024,” Krones, krones.com

The technology race centers on software. Cloud dashboards send live KPIs to secure portals, and AI modules recommend seal-temperature adjustments to prevent leaks from arising. Plants deploying these analytics report scrap reductions of 12% within six months. Suppliers without software capabilities risk relegation to pure hardware vendors, a lower-margin tier.

Vacuum Fillers Industry Leaders

Albert Handtmann Maschinenfabrik GmbH & Co. KG

Vemag Maschinenbau GmbH

Heinrich Frey Maschinenbau GmbH

RISCO S.p.A.

Accutek Packaging Equipment Company, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: IMA Food North America introduced the Hamba Flexline cup fill-seal system, featuring integrated sterilization and a throughput of up to 57,600 cups per hour.

- March 2025: The Marchesini Group exceeded EUR 600 million in turnover for 2024 and set a EUR 1 billion medium-term target, highlighting vacuum-pressure powder fillers at Pharmintech, powered by Ipack-Ima.

- October 2024: IMA Dairy and Food USA showcased the F600 form-fill-seal sachet machine at PACK EXPO International.

- September 2024: The Italian packaging machinery industry reached a turnover of EUR 9.2 billion, with exports accounting for 78.7% of output.

Global Vacuum Fillers Market Report Scope

The scope of the study on the vacuum fillers market encompasses a detailed analysis of machines designed for vacuum-based filling processes, primarily used in the food processing and packaging industries. It covers various equipment types, including high-vacuum fillers, portioning systems, and integrated filling lines for meat, dairy, sauces, and other viscous products.

The Vacuum Fillers Market Report is Segmented by Machine Type (Rotary Vacuum Fillers, Linear Vacuum Fillers, Vacuum Powder Fillers, and High-Vacuum Aseptic Fillers), Automation Level (Manual, Semi-Automatic, and Fully Automatic), Container Type (Rigid, and Flexible), End-user Industry (Food and Beverage, Pharmaceutical, Chemicals, Cosmetics and Personal Care, and Other End-user Industry), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Rotary Vacuum Fillers |

| Linear Vacuum Fillers |

| Vacuum Powder Fillers |

| High-Vacuum Aseptic Fillers |

| Manual |

| Semi-Automatic |

| Fully Automatic |

| Rigid |

| Flexible |

| Food and Beverage |

| Pharmaceutical |

| Chemicals |

| Cosmetics and Personal Care |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Machine Type | Rotary Vacuum Fillers | ||

| Linear Vacuum Fillers | |||

| Vacuum Powder Fillers | |||

| High-Vacuum Aseptic Fillers | |||

| By Automation Level | Manual | ||

| Semi-Automatic | |||

| Fully Automatic | |||

| By Container Type | Rigid | ||

| Flexible | |||

| By End-user Industry | Food and Beverage | ||

| Pharmaceutical | |||

| Chemicals | |||

| Cosmetics and Personal Care | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the vacuum fillers market?

The vacuum fillers market size reached USD 2.25 billion in 2026.

How fast is global demand for vacuum fillers growing?

Demand is projected to rise at a 9.43% CAGR from 2026 to 2031.

Which machine type leads sales?

Rotary vacuum fillers hold 52.38% of 2025 revenue.

Which region is expanding the quickest?

The Asia-Pacific region is forecast to grow at a 11.59% CAGR through 2031.

Why are cosmetics producers adopting vacuum fillers?

Vacuum conditions prevent oxidation, ensure precise dosing, and support premium shelf-life claims, driving an 11.47% CAGR in cosmetics demand.

What factor limits new purchases?

High upfront capital cost remains the chief restraint, especially for small manufacturers.

Page last updated on: