Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

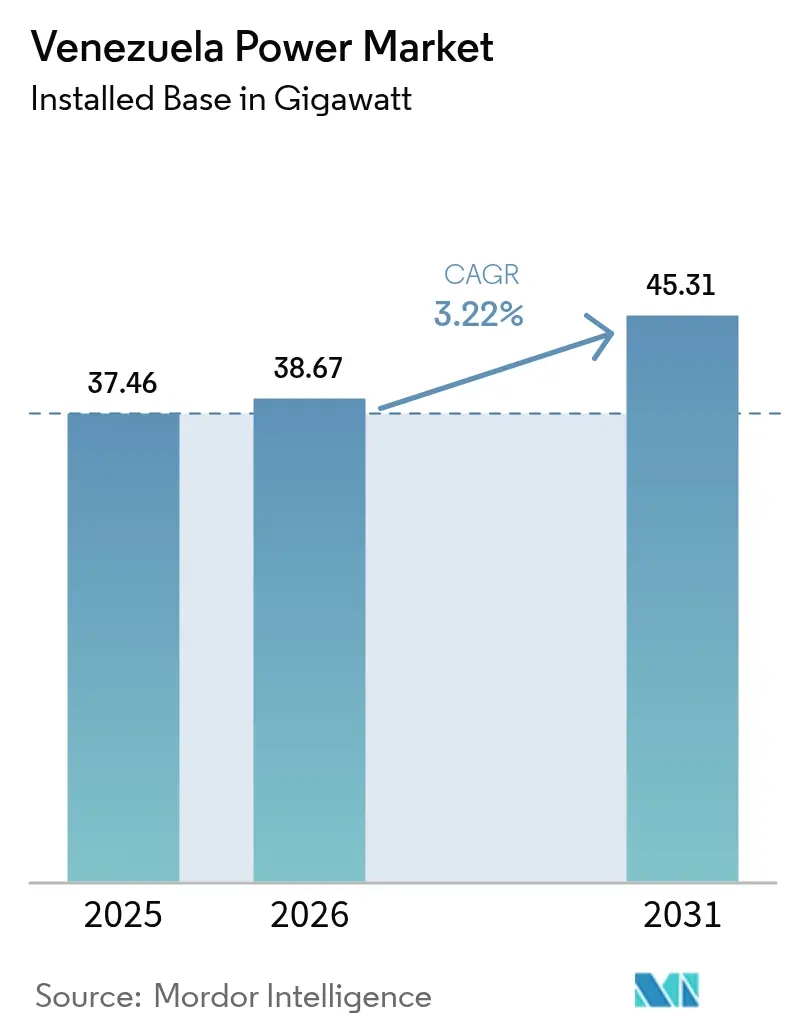

| Base Year Market Size (2025) | 37.46 gigawatt |

| Market Volume (2026) | 38.67 gigawatt |

| Market Volume (2031) | 45.31 gigawatt |

| Growth Rate (2026 - 2031) | 3.22% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Venezuela Power Market Analysis by Mordor Intelligence

The Venezuela Power Market size was valued at 37.46 gigawatt in 2025 and estimated to grow from 38.67 gigawatt in 2026 to reach 45.31 gigawatt by 2031, at a CAGR of 3.22% during the forecast period (2026-2031).

This outlook hides stark structural contrasts: abundant hydro resources counterbalanced by chronic fuel shortages, hyperinflation running at 180.0% for 2025, and renewed U.S. sanctions that restrain procurement for thermal fleets.[1]U.S. Department of the Treasury, “General License 44A,” home.treasury.gov Capacity factors for hydro assets slide below 40%, thermal plants operate at roughly one-quarter of nameplate, and the Venezuela power market endures a recurring generation deficit of 1,600-1,800 MW at peak demand. Rehabilitation of the 10,200 MW Guri complex, a 3,000 MW Andean solar program, and dual-fuel retrofits of thermal stations anchor near-term supply additions, while distributed solar and micro-grids reshape demand in outage-prone regions. Competitive intensity remains low: CORPOELEC’s statutory monopoly crowds out private entrants and forces foreign OEMs into narrow rehabilitation niches. Still, white-space opportunities in self-generation, electric-mobility charging, and hybrid micro-grids keep the Venezuela power market on investors’ watchlists despite macro-political headwinds.

Key Report Takeaways

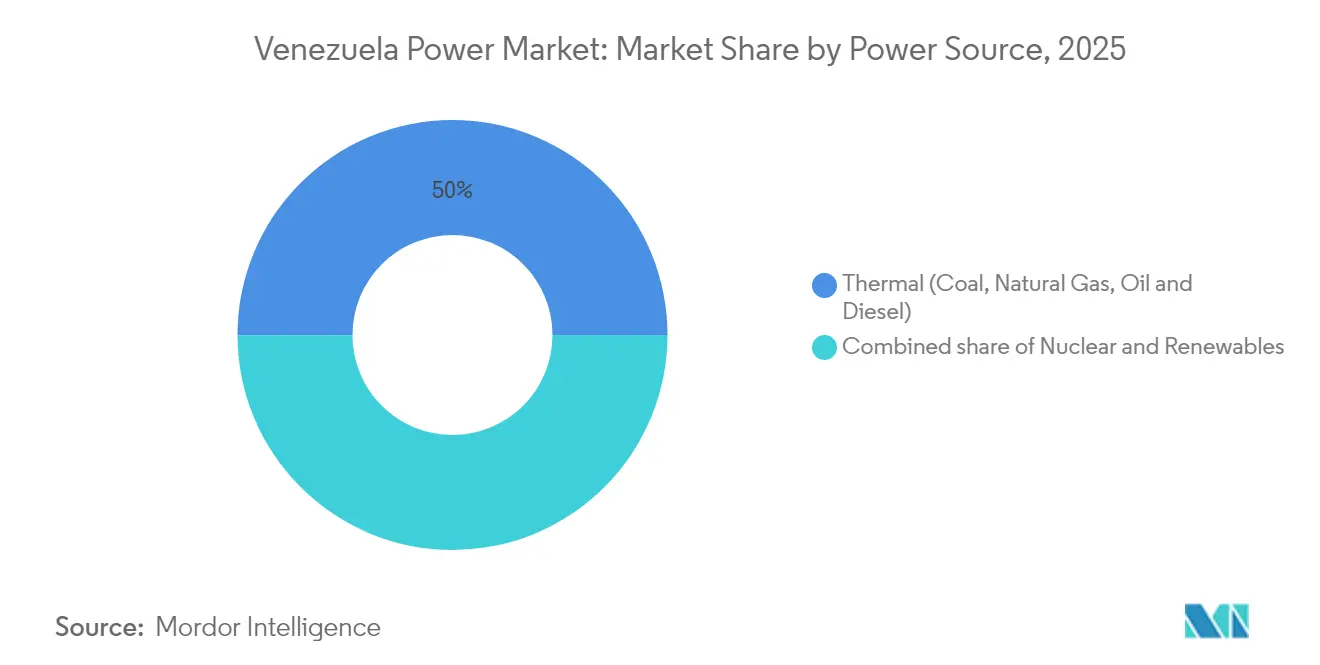

- By power source, thermal generation led with 50.02% of the Venezuela power market share in 2025, yet renewables are forecast to expand at a 5.55% CAGR through 2031.

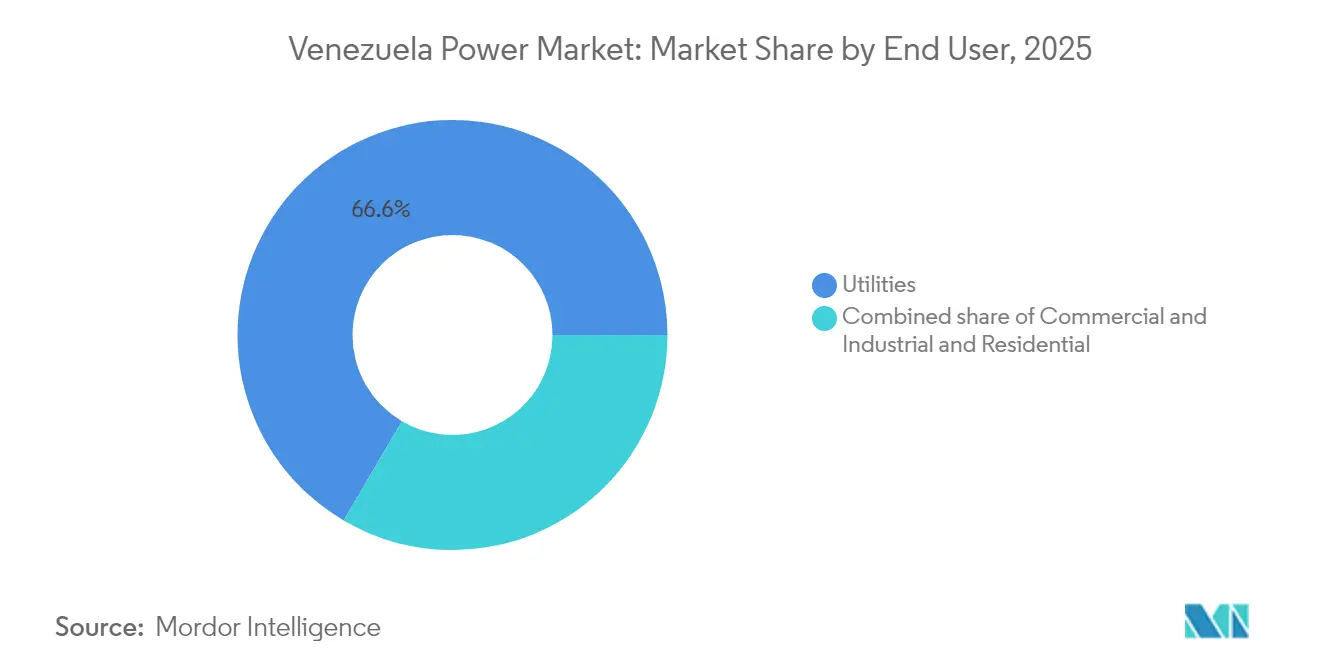

- By end user, utilities commanded a 66.55% share of the Venezuela power market size in 2025 and are projected to grow at a 6.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Venezuela Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Abundant hydropower potential & refurbishment of Guri Dam | +0.8% | National, concentrated in Bolívar state (Guri) and Caroní basin | Medium term (2-4 years) |

| Government renewable-diversification targets amid oil-price volatility | +1.2% | National, with early gains in Mérida, Táchira, Trujillo (Andes solar), Paraguaná (wind) | Long term (≥ 4 years) |

| Rehabilitation & dual-fuel conversion of ageing thermal fleet | +0.6% | National, priority in Zulia (Termozulia, Ramón Laguna), Bolívar (Sidor) | Medium term (2-4 years) |

| Gradual economic stabilisation driving electricity-demand rebound | +0.9% | National, with spillover to cross-border trade (Colombia, Brazil) | Short term (≤ 2 years) |

| Untapped cross-border interconnection capacity (Colombia & Brazil) | +0.4% | Border regions, particularly Zulia (Colombia), Bolívar (Brazil), with national grid benefits | Long term (≥ 4 years) |

| Growing micro-grid initiatives in remote Orinoco & Amazonas regions | +0.3% | Remote areas in Orinoco Basin, Amazonas state, Delta Amacuro | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Abundant Hydropower Potential & Refurbishment of Guri Dam

Venezuela’s technical hydro potential approaches 20,000 MW, yet actual output hovers near 30% of that ceiling.[2]Chambers & Partners, “Energy & Natural Resources Guide Venezuela 2025,” chambers.com The 10,200 MW Guri complex anchors the Caroní cascade, but deferred maintenance, sedimentation, and drought have eroded performance. Refurbishment campaigns, focused on turbine overhauls, valve modernization, and sediment control, could reclaim 800-1,000 MW, erasing the structural deficit without green-field construction.[3]International Energy Agency, “Hydropower Market Report 2023,” iea.org Financing relies on oil-for-infrastructure agreements with Chinese policy banks, while technical execution rotates among Andritz, Voith, and Siemens Energy under Ministry supervision.

Government Renewable-Diversification Targets Amid Oil-Price Volatility

At COP29 (Nov 2024), Caracas pledged to source 30% of electricity from photovoltaics and unveiled a 3,000 MW solar roadmap for the Andes states. This pivot shields exportable hydrocarbons and hedges against fuel-supply shocks that routinely idle thermal plants. Early projects include a 50 MW facility in Mara, Zulia, and a twin 50 MW site in El Vigía, Mérida. Execution leans on turnkey EPC contracts with Chinese, Indian, and Turkish suppliers, yet the stalled Renewable and Alternative Energy (RAE) Bill still clouds power-purchase agreement (PPA) design and tariff certainty.

Rehabilitation & Dual-Fuel Conversion of Ageing Thermal Fleet

Thermal assets such as the 770 MW Termozulia station and the 660 MW Ramón Laguna plant run at 25% utilization or remain dormant. Dual-fuel retrofits allow switching between scarce gas and imported diesel, raising availability when associated-gas flows fluctuate—an acute risk since the 2024 Muscar gas-complex explosion. Contracts center on Siemens Energy and Wärtsilä for burner re-engineering and digital controls, but OFAC licensing and bolívar depreciation inflate costs and elongate delivery cycles.

Gradual Economic Stabilization Driving Electricity-Demand Rebound

GDP grew 5.3% in 2024, yet is projected to contract 4.0% in 2025 as hyperinflation persists. Still, activity in refining, petrochemicals, and mining propels localized demand, particularly in Orinoco Belt operations operated by Chevron and Eni under specific licenses. Distributed solar installers, 13 at last count, and 5,000 EVs show latent elasticity in commercial and mobility segments, offering buffers against grid instability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged political instability & US sanctions limiting FDI | -1.1% | National, with acute effects on oil/gas-dependent regions (Zulia, Anzoátegui, Monagas) | Long term (≥ 4 years) |

| Hyper-inflation and bolívar volatility inflating project costs | -0.6% | National, most severe impact on import-dependent projects and hard-currency financing | Short term (≤ 2 years) |

| Ageing T&D infrastructure causing chronic outages & losses | -0.7% | National, most severe in eastern states, Margarita Island, and peripheral distribution networks | Medium term (2-4 years) |

| Skilled-worker exodus constraining O&M capacity | -0.5% | National, particularly affecting CORPOELEC operations and specialized maintenance at Guri, thermal plants | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prolonged Political Instability & U.S. Sanctions Limiting FDI

General License 44A (Apr 2024) reinstated sectoral sanctions, curbing equipment imports and deterring multiyear finance. Although Chevron, Repsol, and Maurel & Prom hold narrow exemptions, sovereign default status and governance risks elevate Venezuela’s cost of capital well above regional peers. The IEA notes that Venezuela captured none of the USD 185 billion in Latin American power-sector inflows during 2024.

Ageing T&D Infrastructure Causing Chronic Outages & Losses

Service-failure rates leapt from 25.9% in 2022 to 61.9% in 2023 as corroded conductors, overloaded transformers, and weak protection schemes induced cascading blackouts. CORPOELEC’s consolidation of 14 regional utilities has not reversed attrition of skilled labor, and technical plus non-technical losses soak up revenue needed for capital replacement. A World Bank extra-high-voltage upgrade remains undisbursed, underscoring lender reluctance.[4]World Bank, “Venezuela Extra High Voltage Transmission Project,” worldbank.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Source: Hydro Dominance Masks Fuel-Supply Fragility

Hydro supplied 62,516 GWh of 2022 generation and remains the backbone of the Venezuela power market. The hydro-heavy mix commands 49.98% of the Venezuela power market size, while thermal assets account for the remaining 50.02% yet contribute disproportionately less energy because of fuel bottlenecks. Renewables excluding legacy hydro are set to grow at a 5.55% CAGR through 2031, led by the 3,000 MW Andean solar cluster and incremental wind at Paraguaná. The Venezuela power industry faces concentration risk from the single 10,200 MW Guri plant: a repeat of 2020-2021 drought conditions could slice national output by double digits. Dual-fuel conversions promise partial mitigation but hinge on reliable diesel imports or flared-gas capture, both vulnerable to sanctions drag.

Solar, at merely 5 MW in 2023, will acquire a toehold through 100 MW of approved projects and distributed rooftops. Wind’s 40-50 MW addition in July 2024 augurs further coastal build-outs if logistics hurdles ease. Biomass and geothermal stay embryonic, the former stymied by feedstock aggregation costs and the latter by vague tariff signals under the shelved RAE Bill.

By End User: Utilities Dominate Amid Industrial Self-Generation Surge

Utilities controlled 66.55% of installed capacity in 2025 and will expand at a 6.18% CAGR as state-led solar plants funnel into the grid. The Venezuela power market size for utilities equates to roughly 24.9 GW today and rises to 35.7 GW by 2031. Commercial and industrial users, facing outages up to 12 hours daily in eastern regions, ramp up self-generation with rooftop solar, diesel gensets, and nascent battery storage. The Venezuela power market share held by this segment remains below 30%, but growth outpaces the grid as miners and refiners in the Orinoco Belt deploy captive gas turbines exempt from CORPOELEC tariffs. Residential adoption of rooftop PV lags because of high dollar-denominated costs and absent net-metering, yet pilot programs in Caracas and Nueva Esparta suggest a slow climb if financing tools emerge. EV charging loads, now trivial, could add 50-100 MW by 2030, contingent on grid resilience and a modest acceleration in electric mobility.

Geography Analysis

Bolívar state hosts the 10,200 MW Guri complex plus a cascade of smaller dams totaling 16,829 MW, making it the keystone of the Venezuela power market. Drought volatility and sedimentation cut capacity factors below 40% in recent years. Zulia, once a thermal powerhouse, now imports power via vulnerable extra-high-voltage lines that often trip, exposing Maracaibo to frequent curtailments. The Andean trio of Mérida, Táchira, and Trujillo will house the 3,000 MW solar program, leveraging 5.35 kWh/m² of average global horizontal irradiance and proximity to load centers.

Eastern states, Anzoátegui, Monagas, and Sucre, depend on thermals running on associated gas, yet the Muscar explosion cut supply, demonstrating fragility. Coastal Falcón benefited from 38 new wind turbines in 2024, signaling a diversification path. Cross-border interconnections with Colombia and Brazil remain underutilized; price disparities and political risk stall expansion. Remote Orinoco and Amazonas communities rely on diesel and micro-hydro pilot projects; solar-plus-storage could gradually displace liquid fuels pending concessional finance and streamlined permits.

Competitive Landscape

The Venezuela power market is highly concentrated: CORPOELEC monopolizes transmission and distribution and dominates generation under a state-ownership rule requiring a 60% stake in any joint venture. Siemens Energy, ABB, Schneider Electric, Andritz, Voith, and Chinese state-owned EPC contractors engage mainly via legacy maintenance agreements, turbine rehabilitation, or turnkey solar EPCs financed through oil-for-infrastructure swaps. Dual-fuel retrofits at Termozulia and Ramón Laguna place Wärtsilä and Siemens Energy as front-runners, while Andritz retains a service franchise on Guri’s Francis turbines.

White-space revolves around solar micro-grids in Orinoco and Amazonas, EV charging by Swing Energy, and Verdi’s electric taxi fleet. Barriers stem from OFAC compliance, bolívar convertibility, and the absence of bankable PPA templates. Digitalization of hydro dispatch and thermal controls offers incremental gains; Siemens Energy’s T-3000 control retrofit at Termozulia delivers early evidence of efficiency lift. New entrants gravitate toward distributed solar and storage to skirt transmission bottlenecks rather than contest CORPOELEC’s grid hegemony.

Venezuela Power Industry Leaders

CORPOELEC

PDVSA Electricidad

Enel Green Power LATAM

Eletronorte

Siemens Energy (O&M contracts)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Venezuela's government unveiled its latest Nationally Determined Contribution (NDC), committing to a 20% reduction in greenhouse gas (GHG) emissions by 2035, relative to a business-as-usual (BAU) scenario spanning 2024 to 2030. The nation plans to allocate over USD 18.4 billion towards its mitigation efforts, predominantly channeling funds into transportation (USD 10 billion) and electricity (USD 7.8 billion).

- August 2025: Venezuela inaugurated its inaugural solar park in El Vigía, located in Mérida state. This move underscores the nation's commitment to weaving solar energy into its power grid. With a capacity of 1.5 megawatts (MW), the solar park can energize around 2,000 homes in El Vigía.

- June 2024: The government approved a 50 MW solar park in Mara, Zulia, with a 10-month build schedule.

Venezuela Power Market Report Scope

Power is generated through various primary sources such as coal, hydro, solar, thermal, etc. In utilities, it's a step before its delivery to its end users. Then the process is followed by Transmission and distribution. Under this, the power generated is distributed via high-voltage lines (transmission lines) and low-voltage lines (distribution lines) as per the requirement of the end user.

The Venezuela power market report is segmented by power sources and end-user. By power sources, the market is segmented into thermal (Coal, Natural Gas, Oil, and Diesel), nuclear, renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal). By end-user, the market is segmented into utilities, commercial and industrial, and residential. The market sizing and forecasts have been done based on electricity generation capacity (GW).

By Power Source

| Thermal (Coal, Natural Gas, Oil and Diesel) |

| Nuclear |

| Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal) |

By End User

| Utilities |

| Commercial and Industrial |

| Residential |

By T&D Voltage Level (Qualitative Analysis only)

| High-Voltage Transmission (Above 230 kV) |

| Sub-Transmission (69 to 161 kV) |

| Medium-Voltage Distribution (13.2 to 34.5 kV) |

| Low-Voltage Distribution (Up to 1 kV) |

| By Power Source | Thermal (Coal, Natural Gas, Oil and Diesel) |

| Nuclear | |

| Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal) | |

| By End User | Utilities |

| Commercial and Industrial | |

| Residential | |

| By T&D Voltage Level (Qualitative Analysis only) | High-Voltage Transmission (Above 230 kV) |

| Sub-Transmission (69 to 161 kV) | |

| Medium-Voltage Distribution (13.2 to 34.5 kV) | |

| Low-Voltage Distribution (Up to 1 kV) |

Key Questions Answered in the Report

What is the current size of the Venezuela power market?

Installed capacity reached 38.67 GW in 2026 and is forecast to climb to 45.31 GW by 2031.

Which segment supplies most electricity in Venezuela?

Hydropower, led by the 10,200 MW Guri Dam, accounted for 62,516 GWh of the 2022 output.

How fast are renewables growing?

Non-hydro renewables are expected to rise at a 5.55% CAGR between 2026 and 2031 under the 3,000 MW Andean solar program.

Why do blackouts persist despite adequate capacity?

Ageing transmission and distribution assets drive outages, with failure rates affecting 61.9% of households in 2023.

How do U.S. sanctions affect the sector?

Sanctions restrict equipment imports, financing, and foreign participation, reducing inflows and slowing rehabilitation projects.

Where are investment opportunities emerging?

Distributed solar, micro-grids in Orinoco and Amazonas, and EV charging infrastructure offer niches insulated from state monopoly risk.

Page last updated on: