Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | 15.97 gigawatt |

| Market Volume (2026) | 17.6 gigawatt |

| Market Volume (2031) | 28.66 gigawatt |

| Growth Rate (2026 - 2031) | 10.23% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Colombia Renewable Energy Market Analysis by Mordor Intelligence

Colombia Renewable Energy Market size in 2026 is estimated at 17.6 gigawatt, growing from 2025 value of 15.97 gigawatt with 2031 projections showing 28.66 gigawatt, growing at 10.23% CAGR over 2026-2031.

This advance mirrors the government’s USD 40 billion socio-ecological transition portfolio and the national target for renewables to provide 15% of power generation by 2025.[1]OECD Economic Outlook Unit, “Colombia Economic Outlook April 2025,” OECD, oecd.org Hydropower continues to anchor the system, yet aggressive build-outs in wind and solar signal a decisive diversification away from hydrocarbons. Technology cost declines, improved auction design, and multilateral climate-finance inflows attract new capital, while corporate power-purchase agreements (PPAs) from miners and hyperscale data center operators create a parallel demand channel. Execution risk persists in the Colombia renewable energy market, notably due to grid congestion in La Guajira, lengthy environmental licensing processes, and currency headwinds; however, policy momentum and transmission upgrades underpin a robust growth runway through 2030.

Key Report Takeaways

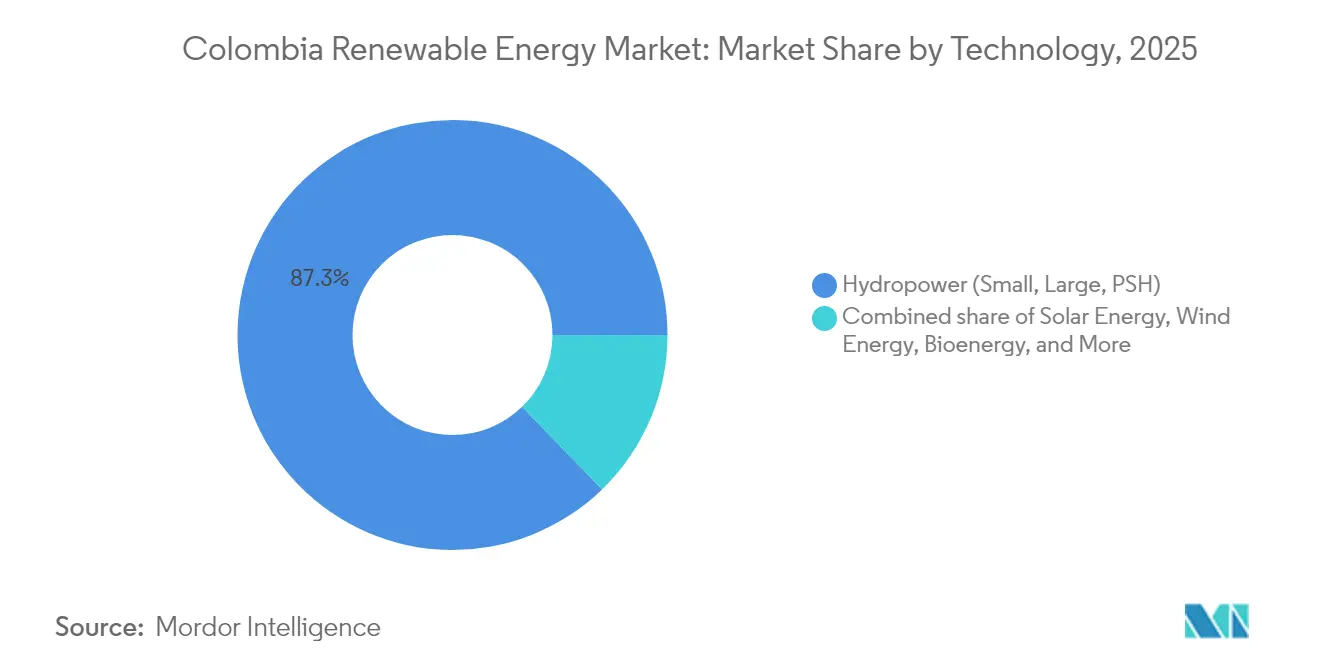

- By technology, hydropower held an 87.25% Colombia renewable energy market share in 2025; onshore wind capacity is projected to expand at an 82.9% CAGR between 2026 and 2031.

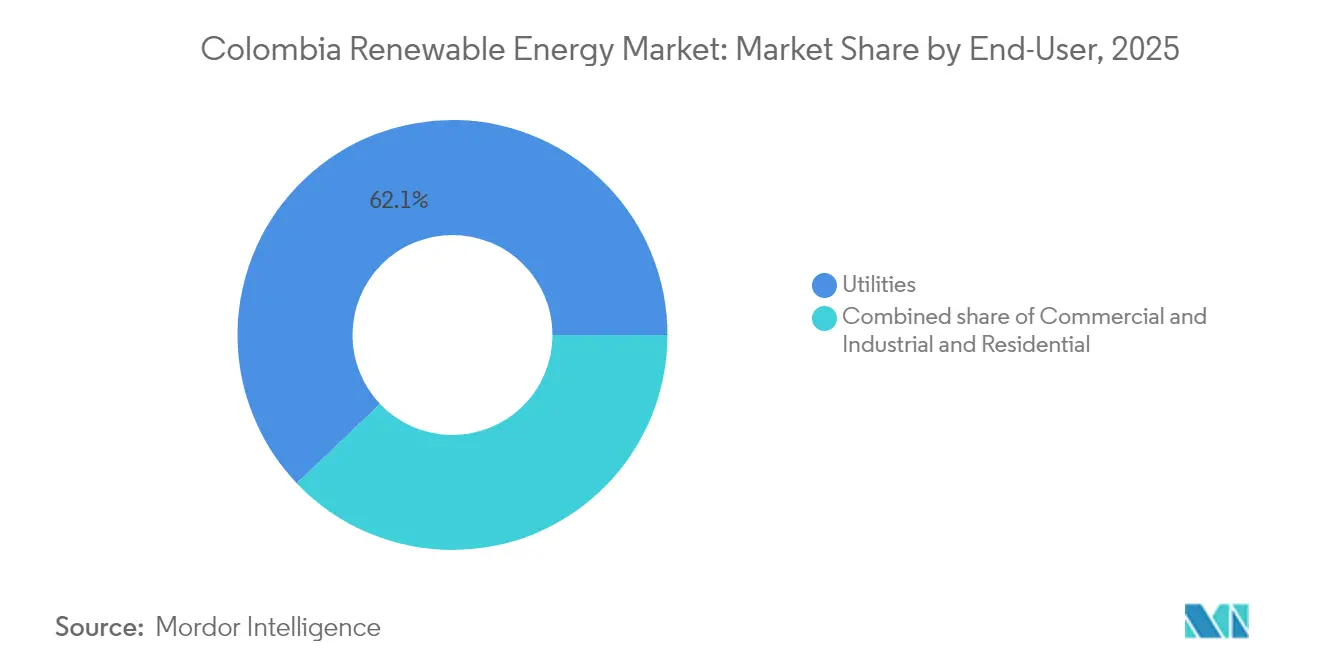

- By end-user, utilities accounted for 62.10% of Colombia's renewable energy market size in 2025, while the commercial and industrial segment is forecast to grow at a 16.15% CAGR through 2031.

- Enel Colombia, Ecopetrol-AES, and Statkraft-Enerfín controlled 34.60% of national solar capacity in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Colombia Renewable Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renewable-energy auctions boost project pipeline | +2.1% | National, with concentration in La Guajira, Atlántico, Tolima | Medium term (2-4 years) |

| Declining LCOE for solar & wind technologies | +1.8% | National, with early gains in Caribbean coast, Andean regions | Short term (≤ 2 years) |

| Access to multilateral climate finance | +1.4% | National, with priority in rural and indigenous territories | Long term (≥ 4 years) |

| National transmission-expansion plan (Plan de Expansión) | +1.2% | La Guajira to central grid, Caribbean interconnection | Medium term (2-4 years) |

| Corporate PPAs from mining & data-center sector | +0.9% | Antioquia, Cundinamarca, mining regions | Short term (≤ 2 years) |

| Green-hydrogen co-location opportunity | +0.7% | La Guajira, Valle del Cauca, El Atlántico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Renewable-energy auctions boost project pipeline

Colombia’s 2024 auction awarded 4.4 GW of solar PV at long-term fixed prices, deepening the development queue and lowering perceived market risk.[2]John Silk, “Colombia Awards 4.4 GW of Solar PV in Renewables Auction,” PV Tech, pv-tech.org The mechanism’s reliability-charge feature secures revenue during low-irradiance hours and improves debt-service coverage ratios. Yet, regulatory volatility resurfaced when Decree 570 was annulled, delaying the financial close of 1.21 GW of projects. A Special Follow-Through Commission now oversees remediation, though its success hinges on re-establishing quorum at the Commission of Energy and Gas Regulation (CREG). Despite setbacks, auctions remain central to scaling the Colombia renewable energy market by standardizing contracts and attracting first-time investors.

Declining LCOE for solar & wind technologies

Utility-scale solar prices are now on par with thermal generation, as illustrated by Enel’s 486.7 MW Guayepo complex, which cleared financing based on merchant revenues. AI-enabled predictive maintenance cuts PV operating costs by 40% and extends asset life, favoring developers with strong digital competencies. Wind economics benefit from an average speed of 9 m/s in La Guajira, but confront social-licence premiums that elevate risk. Offshore prospects along the Caribbean shelf promise further cost declines once supply-chain learning effects emerge. Overall, technology deflation enlarges the Colombia renewable energy market and cushions projects against currency depreciation.

Access to multilateral climate finance

IDB Invest’s USD 113 million package for the 201 MW Shangri-La plant and the European Investment Bank’s USD 300 million framework loan to Enel Colombia illustrate the use of concessional capital in bridging financing gaps.[3]IDB Invest Press Office, “IDB Invest, Bancolombia and Atlas Renewable Energy Announce Investment to Boost Colombia’s Energy Transition,” idbinvest.org Loan covenants mandate gender equity and community-benefit programs that enhance social acceptance. Domestic green-bond issuance by Epsa signals growing local appetite for sustainable assets, though access still skews toward large sponsors. Multilateral funding remains a pivotal accelerator for the Colombia renewable energy market, lowering the weighted-average cost of capital and expanding the bankability of new technologies.

National transmission-expansion plan

The delayed 500 kV Colectora line, due mid-2025, will unlock 900 MW of stranded wind projects and relieve La Guajira’s congestion. Grid operator ISA has earmarked 71% of a USD 1.4 trillion investment pipeline for renewable energy integration, deploying modular static-series synchronous compensation (M-SSSC) devices to enhance power flow flexibility. Smart Wires’ second project with ISA TRANSELCA validates rapid-deployment grid-tech solutions. While coordination gaps between national and regional planners persist, the Plan de Expansión’s staged tenders improve investor visibility in the Colombia renewable energy market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid congestion & curtailment risk in La Guajira | -1.9% | La Guajira, Caribbean coast transmission corridors | Short term (≤ 2 years) |

| Lengthy environmental licensing process | -1.6% | National, with acute impact in La Guajira, Amazon regions | Medium term (2-4 years) |

| Indigenous Wayuu community opposition | -1.3% | La Guajira, offshore wind development areas | Long term (≥ 4 years) |

| Peso depreciation inflating imported CAPEX | -0.8% | National, with higher impact on import-intensive technologies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Grid congestion & curtailment risk in La Guajira

Transmission lags expose projects to curtailment penalties that erode returns and delay senior-debt drawdowns. The Inter-American Development Bank identifies first-mover disadvantage, as early entrants monopolize finite capacity while later projects face output caps.[4]Inter-American Development Bank Energy Division, “The Challenge of Renewable Energy Curtailment,” iadb.org Weather correlation increases simultaneous generation peaks, straining the 220 kV corridor toward the Caribbean hub. Smart-grid controls and 100 MW-class battery systems can mitigate curtailment but require joint investment across generation and transmission actors. Until Colectora energizes, congestion remains the primary brake on the Colombia renewable energy market.

Lengthy environmental licensing process

Full environmental impact assessments add roughly 18 months and inflate financing costs, prompting exits by firms such as EDF Renewables. Overlapping agency mandates result in sequential instead of parallel reviews, while indigenous consultations often lack standardized protocols. Fast-track geothermal rules hint at potential reform, yet broader streamlining faces political resistance over environmental safeguards. Prolonged permitting tilts the Colombia renewable energy market toward well-capitalized players and slows technology diversification.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Wind Surge Challenges Hydropower Dominance

Hydropower commanded 87.25% of installed capacity in 2025, but onshore wind is forecast to post an 82.9% CAGR through 2031 as La Guajira's 15 GW resource base moves into construction. AES Colombia's 1,087 MW Jemeiwaa Ka'I cluster exemplifies the potential for scale, while the upcoming offshore wind round targets Caribbean leases with superior capacity factors. Solar capacity crossed 1.3 GW in 2024 and is projected to supply 20.80% of new installations by 2031. Colombia's renewable energy market size for wind is expected to hit 2.45 GW by 2031, compared with 16.7 GW for hydropower. Bioenergy and geothermal add dispatchable diversity: palm-oil waste alone offers 50.2 × 10^6 GJ annual energy, and geothermal blocks totaling 1.17 GW enter auction in late 2025.

Grid resilience drives hybrid deployments that pair PV and wind with lithium-iron-phosphate storage to cut curtailment and provide ancillary services. Concentrated solar power remains nascent but offers future peaking potential. Ocean-energy pilots in tidal estuaries seek tariff support to reach commercial scale. Together, these advances broaden the technology stack and reduce rainfall-driven hydropower volatility within the Colombia renewable energy market.

By End-User: Commercial & Industrial Demand Redraws Procurement

Utilities retained 62.10% capacity share in 2025 yet face stiff competition from direct-sourcing corporates. The commercial-and-industrial (C&I) segment is on track for a 16.15% CAGR, driven by miners hedging price volatility and data-center operators pursuing 24/7 clean-energy credentials. Scala Data Centers' long-term PPA with Serena Energia illustrates how hyperscale demand accelerates new builds. Private-wire PPAs and behind-the-meter solar arrays allow industrial buyers to avoid grid fees and improve power-quality metrics.

Colombia's renewable energy market share for commercial and industrial (C&I) offtake is projected to increase to 29.35% by 2031. Utilities respond by expanding renewable portfolios and offering sleeved PPAs to retain key accounts. Residential uptake lags, but public programs such as "Colombia Solar" aim to mobilize USD 10 billion to subsidize rooftop systems for low-income households, signaling future diffusion into the mass market. The evolving end-user mix underscores a broader shift toward decentralized procurement and customer choice in the Colombia renewable energy industry.

Geography Analysis

La Guajira hosts Latin America’s best onshore wind regime, with average speeds topping 9 m/s and technical potential near 15 GW. Yet community opposition from the Wayuu people and delayed transmission lines have slowed execution, leading to cancellations such as Enel’s 200 MW Windpeshi project. Offshore blocks along the Caribbean shelf extend resource headroom but must also address the impacts on fisheries and the complex permitting requirements. The Andean departments of Cundinamarca and Tolima captured 73% of solar additions expected in 2025, leveraging proximity to Bogotá’s load center and avoiding La Guajira’s social-licence hurdles. Biomass clusters line the Magdalena River valley, where 26% internal rates of return entice agro-industrial investors into rice-husk cogeneration.

Geothermal prospects are concentrated in volcanic zones, including Nevado del Ruiz (206 MW), Azufral (82 MW), and Paipa (22 MW). These baseload resources complement intermittent renewables, improving system inertia. Pacific and Amazon territories rely on micro-grids that integrate solar, small hydro, and biodigesters to electrify remote communities. Transmission build-outs, such as Colectora and the Caribbean 500 kV reinforcement, will rebalance regional disparities by integrating coastal renewables with interior demand and expanding the Colombia renewable energy market.

Regulatory Landscape

Colombia renewable energy regulation continues to center on long-term contracting, grid access, and system flexibility, led by Ministerio de Minas y Energia (MinMinas), CREG (Comision de Regulacion de Energia y Gas), and UPME. In March 2026, MinMinas issued Resolution 40178 of 2026 to define general rules for long-term clean energy procurement mechanisms. This reinforces the policy push to use standardized, bankable contracts for non-conventional renewables and complementary resources.

In 2026, the framework also expanded to address connection bottlenecks and flexibility assets. UPME issued Resolution 000358 of 2026 to regulate and expedite transmission-capacity allocation for generation projects, while CREG issued measures such as Resolution 101 098 of 2026 on technical and operational requirements for shared transmission-asset connections in the SIN. CREG also issued Resolution 101 113 of 2026, incorporating guidelines for battery energy storage systems (SAEB) to support frequency regulation, voltage support, and peak-demand reduction. On the distributed side, Decree 972 of 2025 created the Colombia Solar program to enable solar autogeneration for residential users in strata 1, 2, and 3, broadening the policy toolkit beyond utility-scale auctions.

Competitive Landscape

The market exhibits moderate concentration. Enel Colombia controls 35% of its solar capacity through the Guayepo, La Loma, and Fundación plants, leveraging scale and concession. Ecopetrol's pivot includes a 49% stake in AES-Ka'IJemeiwaa Ka'I and a USD 3.6 billion purchase of 51.4% of ISA, creating a vertically integrated generation-to-grStatkraft's. Statkraft's sale of Enerfín Colombia to Ecopetrol in 2025 highlights consolidation and foreign exit trends.

Digitalization is emerging as a key differentiator, as AI-powered asset monitoring, digital substations, and hybrid storage raise availability factors and reduce O&M costs. International developers partner with local EPC firms to navigate social license processes, while smaller independents focus on rural electrification niches, financed by blended-finance vehicles. Currency volatility, indigenous consultations, and curtailment risks elevate execution hurdles, favoring players with diversified portfolios and robust treasury operations. Competitive intensity is increasing as utilities, oil majors, and tech-centric entrants vie for bankable sites in the Colombia renewable energy market.

Colombia Renewable Energy Industry Leaders

Celsia SAESP

DNV GL AS

Enel Green Power SpA

EDP Renovaveis SA

Ventus Ingeniería S.R.L

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Long-term contracting and hybridization create identifiable whitespace in utility-scale solar, wind, and storage configurations, particularly for projects that can deliver firmed energy and grid services during peak periods. MinMinas Resolution 40208 of 2026 launched a long-term auction that includes renewable generation, storage, and hybrid systems, with 15-year contracts designed to start in 2030 and awards targeted by July 31, 2026. Because grid congestion and connection queues remain binding constraints, UPME’s transmission-capacity allocation rules (Resolution 000358 of 2026) and CREG guidance on shared-asset connections and storage integration support project designs that combine generation with BESS. This approach helps reduce curtailment exposure and increases dispatchability in the SIN.

Transmission expansion and regional integration then drive a second opportunity layer along the Caribbean corridor, where enabling infrastructure affects how quickly La Guajira and nearby departments translate resource quality into connected capacity. The Connected Caribbean grid development program, described as a US$1.7 billion commitment, targets reinforcements including synchronous compensators and STN transformers to support around 6 GW of new wind and solar capacity, aligning network upgrades with developer pipelines. A third opportunity area is early-stage geothermal, where MinMinas granted the first geothermal exploration permit for the El Barranquero area in July 2026, backed by an investment of more than COP 38,556 million. This establishes a new dispatchable renewable track alongside hydro variability, even though exploration runs on a multi-year timeline. Execution gaps persist, as MinMinas cited in May 2026 that 52% of renewable projects were stalled due to regulatory and administrative delays, which raises the value of sponsors and EPCs that can manage permitting, consultation, and interconnection milestones.

Recent Industry Developments

- July 2026: Ministerio de Minas y Energia granted the first geothermal exploration permit for the El Barranquero area, supporting studies and exploration with an investment of more than COP 38,556 million. The decision operationalizes geothermal as a new dispatchable renewable pathway within Colombia's transition agenda and expands the technology pipeline beyond wind and solar.

- December 2025: EDP Renovaveis initiated an ICSID arbitration claim against the Republic of Colombia, seeking about USD 600 million tied to disputes around its Alpha and Beta wind projects in La Guajira. The filing raised perceived regulatory and contract-risk premiums for large wind developments and sharpened scrutiny of the reliability-charge and permitting framework among international investors.

- August 2024: Celsia started construction of three solar farms totaling 59.7 MW in Valledupar, Cesar. The build-out added near-term EPC and interconnection activity in an interior solar corridor and supported the scale-up of Celsia's operating and development renewables platform.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Colombia renewable energy market is defined as the country level installed renewable power capacity that is connected or counted as operational within the power system, tracked in gigawatts and aggregated across renewable technologies.

Scope exclusions: We do not count fossil fuel power capacity or nuclear power capacity in the renewable total, even if they appear in wider power sector dashboards.

Segmentation Overview

- By Technology

- Solar Energy (PV and CSP)

- Wind Energy (Onshore and Offshore)

- Hydropower (Small, Large, PSH)

- Bioenergy

- Geothermal

- Ocean Energy (Tidal and Wave)

- By End-User

- Utilities

- Commercial and Industrial

- Residential

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base for Colombia power capacity additions, technology mix, and the policy and auction pipeline that influences renewable commissioning. We typically start with public and official references such as UPME publications, XM system operation updates, DANE energy and industry statistics, and IRENA renewable capacity series, then cross-check them against global power datasets from sources such as the IEA and the World Bank.

To keep assumptions realistic, we also reviewed company filings and investor presentations for project level timelines and grid connection milestones, along with association websites and reputable press for regulatory changes that can shift COD dates. In a few cases, paid subscriptions for company financials and news intelligence, patent databases, and an import and export shipment level database were used to sanity-check equipment arrival timing and supplier activity signals. These desk sources are illustrative only, and many other references were also used to collect data, validate it, and clarify open questions.

Primary Interviews and Surveys

Primary work was used to pressure-test what is visible on paper versus what is actually expected to be commissioned, delayed, or re-scoped. We spoke with a mix of developers, EPC and O&M participants, equipment and service providers, lenders and advisors, and large power buyers, and then aligned findings across Colombia with the most relevant supply and financing touchpoints.

Given how transmission readiness, permitting, and community engagement affect renewable project schedules in Colombia, these discussions helped us finalize timing assumptions and a realistic year-by-year capacity ramp, instead of relying only on announced plans.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 12% | |

| Mid tier: 48% | Functional/Unit leaders: 42% | |

| Smaller Players: 18% | Managers: 46% |

Market-Sizing & Forecasting

Market sizing is built from a top-down reconstruction of Colombia renewable installed capacity, where reported system totals are split by technology and then extended using the visible project pipeline and expected commissioning dates. To keep the final number grounded, we corroborate it with selective bottom-up checks, including sampling major projects, applying typical project size distributions, and validating the implied annual additions against equipment delivery and grid connection signals.

A few inputs that consistently mattered in the model were annual renewable capacity additions (GW), technology mix shifts between hydro, bioenergy, and other renewables, grid expansion and substation readiness, auction and PPA award volumes, and the average delay factor between announced COD and actual commissioning. When some project details were missing, the gap was handled with conservative assumptions based on similar projects in Colombia, then re-checked through interview feedback.

For forecasting, scenario analysis was used because commissioning is driven by discrete project milestones and policy and transmission events. The base case assumptions were adjusted only after they were validated with expert consensus on likely delays, financing tightness, and near-term grid constraints.

Data Validation & Update Cycle

Before sign-off, outputs are triangulated against independent signals, including public capacity statistics, grid operator updates, and the implied pace of annual commissioning versus what the pipeline can realistically deliver. When a large variance is observed, we review it in a second pass, where technology splits, timing assumptions, and conversion logic are re-checked, and follow-up calls are triggered when a key project or policy change could materially shift the trajectory.

Reports are refreshed annually, and interim updates are made when material events occur, such as a major auction outcome, a transmission delay, or a large project cancellation. Right before delivery, we perform a fresh review so clients receive the most current view that can be supported by traceable inputs.

Mordor Intelligence's Colombia Renewable Energy Market Size Versus Other Published Estimates

Published estimates for Colombia renewable energy often differ because the unit of measurement changes, the counted technologies differ, and the timing of what is considered operational is applied differently. Some sources also blend market value and capacity in the same narrative, which can complicate comparisons even when both numbers are correct within their own definitions.

The main gap comes from whether large hydropower is included in the renewable total and whether only operational capacity is counted, where Mordor Intelligence keeps large hydro inside the renewable installed-capacity total and uses consistent commissioning cutoffs instead of mixing announced and under-construction projects.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.97 B (2025) | |

| Trade Journal A | USD 2.55 B (2025) | This figure reflects only non-conventional renewables such as solar and wind and explicitly excludes large hydropower, which makes the scope narrower than a total renewables capacity view. |

| Global Consultancy B | USD 8.90 B (2024) | This estimate is reported in value terms for a broader renewable ecosystem and uses a different base year, so it can move independently from installed capacity expansion in a single year. |

The spread in the table is mainly explained by unit choice (USD value versus capacity tracking), base year alignment, and whether hydropower is treated as part of renewables or left out. By keeping the sizing steps tied to clear definitions and re-checking year-by-year commissioning reality with multiple signals, the result stays easier to reproduce and reconcile over time.

Key Questions Answered in the Report

What capacity has the Colombia renewable energy market reached in 2026?

Installed renewable capacity stands at 17.6 GW in 2026 and is projected to grow to 28.66 GW by 2031.

Which technology is expanding quickest in Colombia?

Onshore wind leads, with an expected 82.9% CAGR for 2026-2031 as La Guajira and Caribbean offshore zones develop.

How significant are corporate PPAs for new projects?

Corporate offtake is the fastest-growing end-user category at a 16.15% CAGR, providing long-term revenue certainty for developers.

Which Colombian regions offer the best renewable resources?

La Guajira excels in wind, while Cundinamarca and Tolima dominate solar additions thanks to grid proximity and high irradiation.

What are the main barriers to renewable deployment?

Grid congestion in La Guajira and an 18-month average environmental licensing cycle are the most critical execution hurdles.

How will new transmission lines influence growth?

Commissioning of the 500 kV Colectora line in 2025 will unlock 900 MW of wind capacity and reduce curtailment risk across the northern corridor.

Page last updated on: