Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

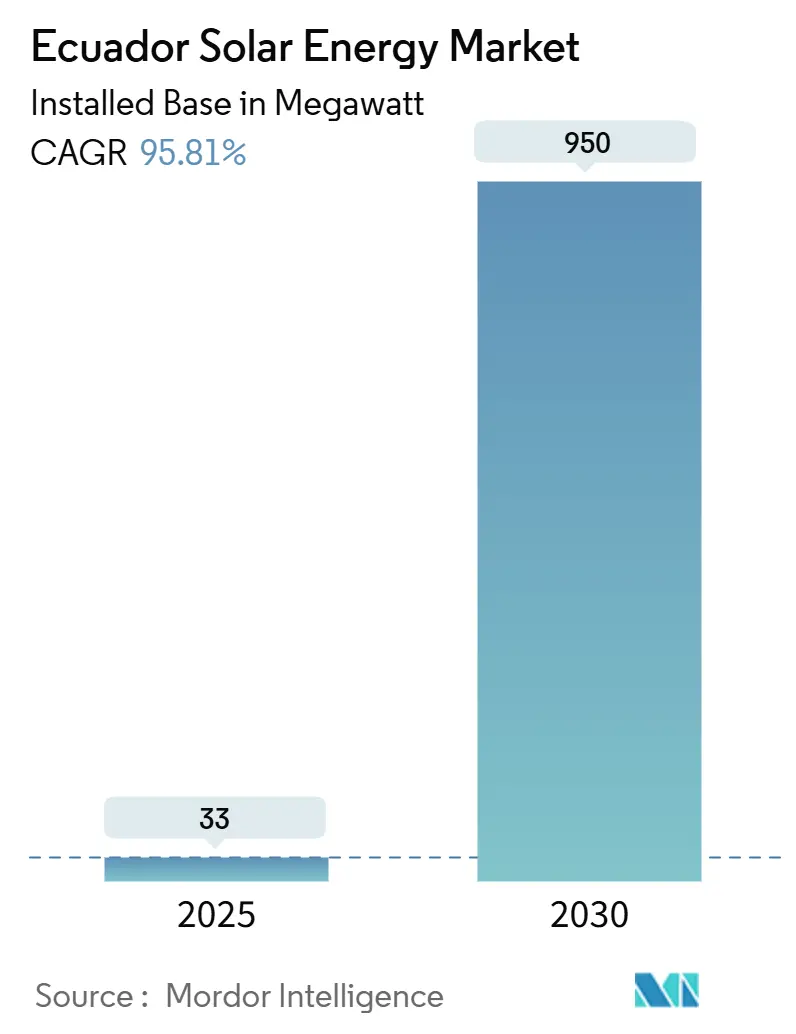

| Market Volume (2025) | 33 megawatt |

| Market Volume (2030) | 950 megawatt |

| Growth Rate (2025 - 2030) | 95.81% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ecuador Solar Energy Market Analysis by Mordor Intelligence

The Ecuador Solar Energy Market size in terms of installed base is expected to grow from 33 megawatt in 2025 to 950 megawatt by 2030, at a CAGR of 95.81% during the forecast period (2025-2030).

A shift away from hydro reliance, record‐high irradiation of 4.3–5.0 kWh/m²/day, and a USD 913 million public investment program are accelerating capacity additions. The 2024 energy crisis, which led to blackouts lasting up to 14 hours a day, pushed policymakers to streamline licensing for projects up to 100 MW, expand utility-scale auctions, and offer tax incentives for self-generation. Falling module prices have lowered the solar LCOE to USD 40-50 per MWh, undercutting hydro peaking costs and encouraging private developers to pursue mid-scale plants in provinces with available transmission. International concessional finance from the Inter-American Development Bank and Agence Française de Développement further reduces the cost of capital, while strong corporate decarbonization targets are lifting demand for rooftop systems in export-oriented agro-processing clusters.

Key Report Takeaways

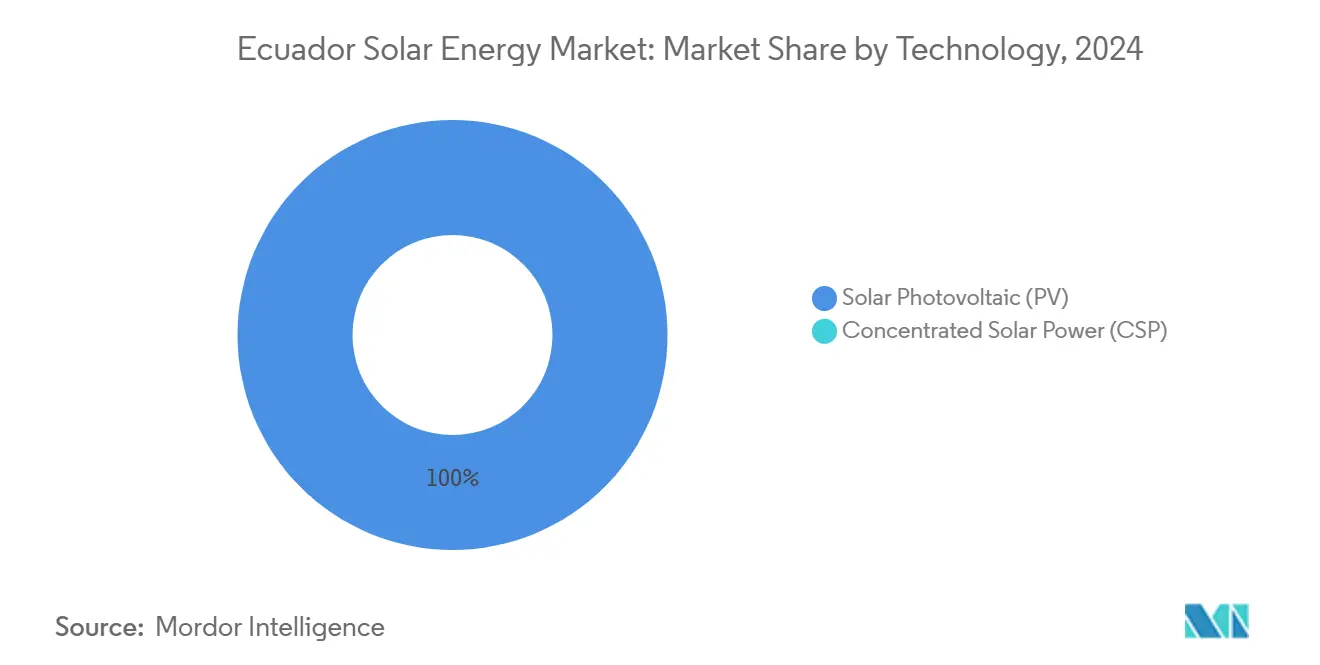

- By technology, photovoltaic (PV) captured 100% of the Ecuador solar energy market share in 2024 and is forecast to grow at a 95.8% CAGR through 2030.

- By grid type, on-grid systems held 95.8% of the Ecuador solar energy market share in 2024; the segment is projected to expand at a 98.3% CAGR to 2030.

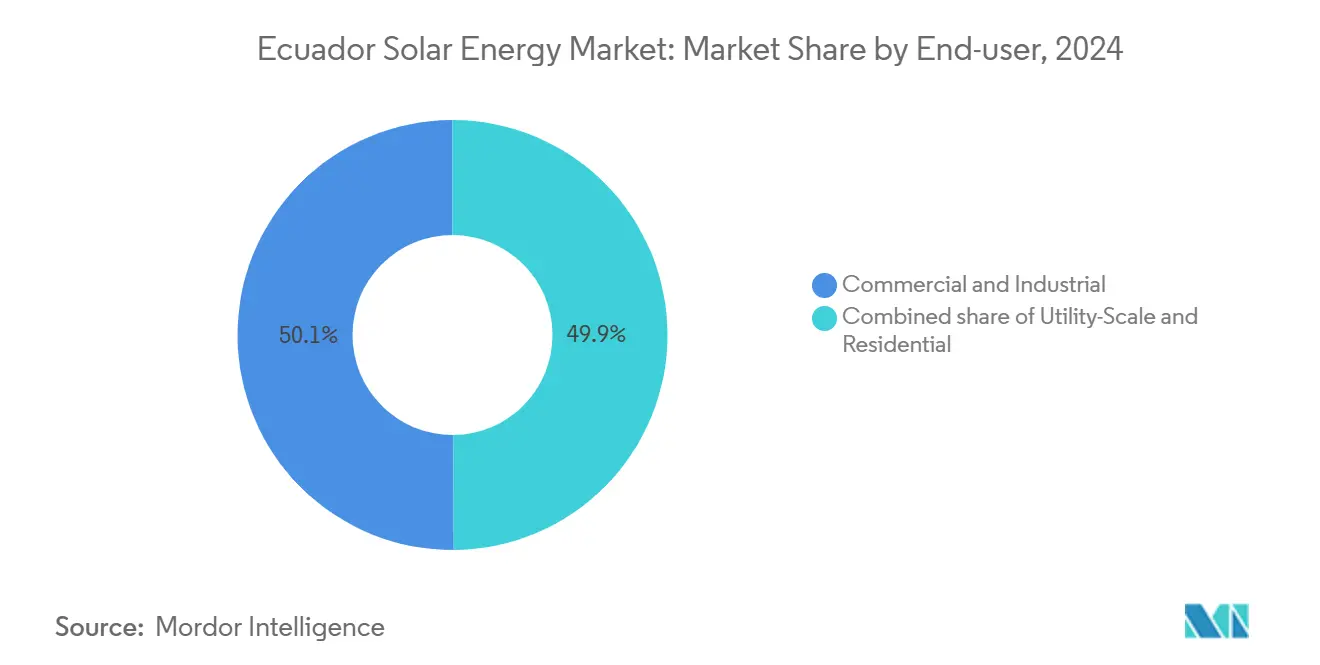

- By end-user, the utility-scale segment is poised to advance at a 125.5% CAGR between 2025 and 2030, while the commercial-and-industrial (C&I) segment led with 50.1% share of the Ecuador solar energy market size in 2024.

Ecuador Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government utility-scale auction program | +28.50% | Loja, Manabí, Guayas | Medium term (2-4 years) |

| Falling module and BOS costs | +22% | Nationwide, early gains in Loja and Imbabura | Short term (≤2 years) |

| High year-round irradiation and 12-hour daylight | +18% | Southern highlands and coastal Manabí | Long term (≥4 years) |

| Seasonal hydro deficits creating capacity payments | +15% | Nationwide, pronounced during El Niño periods | Medium term (2-4 years) |

| International concessional finance pipeline | +20% | Sites promoted by CELEC EP | Medium term (2-4 years) |

| Mining and agro-processing self-generation mandates | +12% | Azuay, Zamora-Chinchipe, Guayas, El Oro | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Falling Module and Balance-of-System Costs Narrow the LCOE Gap

Average global module prices fell to USD 0.10 per W in 2024, allowing the national solar LCOE to drop toward USD 40 per MWh. At this level, PV undercuts new hydro peaking projects priced at USD 60-80 per MWh and competes with combined-cycle gas. Zero import duty on panels has accelerated utility-scale pipelines, whereas a 12% VAT on inverters adds USD 5-8 per MWh to hybrid systems, reinforcing the popularity of pure grid-tied arrays. As BOS prices decline further, the economic advantage is expected to reach off-grid microgrids serving the Amazon and Galápagos by 2027.

High Year-Round Irradiation and 12-Hour Daylight Enhance Capacity Factors

Equatorial geography gives Ecuador consistent daily sunlight, yielding 16-17% capacity factors for fixed-tilt plants and up to 21% for tracking systems. Loja posts the highest irradiation in the country, prompting CELEC GENSUR to launch the 200 MW La Ceiba project in January 2025. Developers are favoring high-efficiency bifacial modules that reduce land needs by 15-20%, a critical benefit for mountainous sites with limited flat terrain.

Seasonal Hydro Deficits Create Capacity Payments for Solar Firming

Hydro generated 71.68% of electricity in 2023, but output drops 30-40% in dry periods, forcing expensive diesel peaking at USD 120-150 per MWh. CENACE is piloting an ancillary-services market that would let solar-plus-battery projects earn USD 10-15 per MWh in capacity fees, improving project IRRs by as much as 3 percentage points.

Government Utility-Scale Auction Program Drives Capacity Additions

The ministry awarded the 200 MW El Aromo project under a 310 MW tender and, in January 2024, identified seven new sites totaling 1.58 GW, positioning state utility CELEC EP as the anchor of future PPAs.(1)CELEC EP, “Generación Solar Portfolio,” celec.gob.ec Legislative reform in October 2024 lifted the private-project threshold to 100 MW, removing the requirement for competitive bidding and attracting independent producers keen to fast-track projects in provinces where existing transmission is adequate. Successful Colombian auctions in 2019 offer a regional precedent, reinforcing investor confidence that Ecuador can secure financial close for 50–100 MW plants by 2026.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy environmental and indigenous consultation | -12% | Amazon and highland territories | Medium term (2-4 years) |

| Weak transmission in high-solar provinces | -10% | Loja, Imbabura, Carchi | Long term (≥4 years) |

| Import tariffs and VAT on inverters and storage | -6% | Nationwide | Short term (≤2 years) |

| Expiry of preferential feed-in tariffs | -8% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lengthy Environmental and Indigenous Consultation Delays Projects

Projects exceeding 1 MW require an environmental impact assessment and, when located on ancestral land, a prior consultation under ILO 169. This sequence often extends beyond 18 months, as illustrated by the 200 MW El Aromo plant still awaiting full permits in early 2025. Developers now budget USD 0.5-1 million for upfront community agreements, trading higher soft costs for shorter overall timelines.

Weak Transmission in High-Solar Provinces Constrains Grid Integration

Loja and Imbabura offer irradiation above 5.0 kWh/m²/day but lack sufficient 230 kV lines to move supply toward Quito and Guayaquil. TRANSELECTRIC plans USD 150 million in upgrades by 2027; however, right-of-way challenges mean several corridors will not be energized before 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: PV Monopolizes the Pipeline

Installation data show that PV commanded 100% of the Ecuador solar energy market share in 2024 and is projected to maintain dominance through 2030 on a 95.8% CAGR. The Ecuador solar energy market size attributable to PV is set to jump from 33 MW in 2025 to 950 MW in 2030 as no CSP plants appear in the national registry.(2)International Renewable Energy Agency, “Renewable Power Generation Costs 2024,” irena.org Capital expenditure for fixed-tilt PV averages USD 800-900 per kW compared with USD 3,500-4,500 per kW for CSP, an 80% cost advantage that accelerates financial close. Bifacial modules supplied by Trina Solar and Canadian Solar deliver 10-15% energy gains by harvesting albedo, reducing land requirements in mountainous regions where flat parcels carry premium prices.

Continuous module-efficiency gains, such as JinkoSolar’s N-type Tiger Neo reaching 25.8% in 2024, allow developers to boost capacity within existing substation limits.(3)JinkoSolar, “Tiger Neo N-type Module Datasheet,” jinkosolar.com The absence of high direct-normal-irradiance zones makes CSP economically unattractive, a reality confirmed by feasibility studies from NREL showing DNI below 1,500 kWh/m²/year nationwide. As auctions stipulate least-cost bids, PV’s cost leadership leaves CSP sidelined for the foreseeable future.

By Grid Type: On-Grid Capacity Surges with Transmission Upgrades

On-grid projects held 95.8% of the Ecuador solar energy market share in 2024 and will grow at a 98.3% CAGR to 2030 as CELEC EP’s 1.58 GW portfolio feeds the National Interconnected System. Around 200 MW of new capacity, including La Ceiba and El Aromo, is scheduled for financial close in 2025-2026. Grid-tied economics are helped by zero import duty on modules and established PPA frameworks overseen by CENACE.

Off-grid systems account for just 4.2 MW but play a vital social role by powering Amazon schools, clinics, and the Galápagos Islands. The ministry’s rural electrification program deployed 60 MW of self-consumption capacity by mid-2025 and cut diesel use by up to 70%. Nevertheless, as grid extensions reach isolated provinces, off-grid growth will moderate in favor of net-metered rooftops under ARCERNNR Regulation 008/23.

By End-User: Utility-Scale Leads Future Additions

Commercial and Industrial (C&I) rooftops led demand in 2024 with 50.1% of installed capacity, but the utility-scale segment is forecast to post a 125.5% CAGR from 2025 to 2030 as auctioned plants reach COD. The Ecuador solar energy market size for utility-scale assets is expected to exceed 700 MW by 2030, driven by transmission-ready sites in Manabí, Loja, and Guayas. Mid-tier developers are flocking to projects under 100 MW that now bypass the auction process, speeding timelines by at least six months.

C&I economics remain compelling, with rooftop LCOE near USD 0.12 per kWh against retail tariffs of USD 0.156 per kWh, offering 5-7 year paybacks for exporters in the banana, cacao, and shrimp sectors. Residential uptake lags due to subsidized tariffs at USD 0.093 per kWh and limited access to long-term finance. Subsidy reform is politically sensitive and unlikely before the 2027 legislative cycle, capping household adoption near 2% of national installations.

Geography Analysis

Loja, Manabí, and Guayas make up the primary deployment corridor and together represent more than 60% of installed and planned megawatts. Loja’s average irradiation of 5.7 kWh/m²/day and the launch of the 200 MW La Ceiba project secure the province’s leadership through 2030. Manabí hosts the 200 MW El Aromo plant near Portoviejo, where flat terrain simplifies construction and coastal proximity shortens logistics chains.

Guayas, home to Guayaquil and 35% of national demand, added 150 MW of distributed projects under Regulation 013/2021, taking advantage of ample commercial rooftops and nearby substations. Imbabura and Carchi post irradiation above 4.8 kWh/m²/day yet face bottlenecks until the 230 kV line extension scheduled for 2028. Once energized, the corridor could unlock 300 MW of currently stalled projects.

The Amazon provinces of Sucumbíos and Orellana rely on PV-diesel microgrids; 60 MW had been deployed by June 2025 under the rural electrification program, delivering uninterrupted power to clinics and schools. The Galápagos Islands target 100% renewable electricity by 2030; the 1.5 MW Baltra plant commissioned in 2024 demonstrates technical viability in a protected environment.(4)UNESCO, “Galápagos Renewable Energy Initiative,” unesco.orgSecondary provinces such as Azuay and El Oro are poised to attract solar-plus-storage tied to mining and agro-processing loads once the IDB-funded transmission upgrades reach completion.

Competitive Landscape

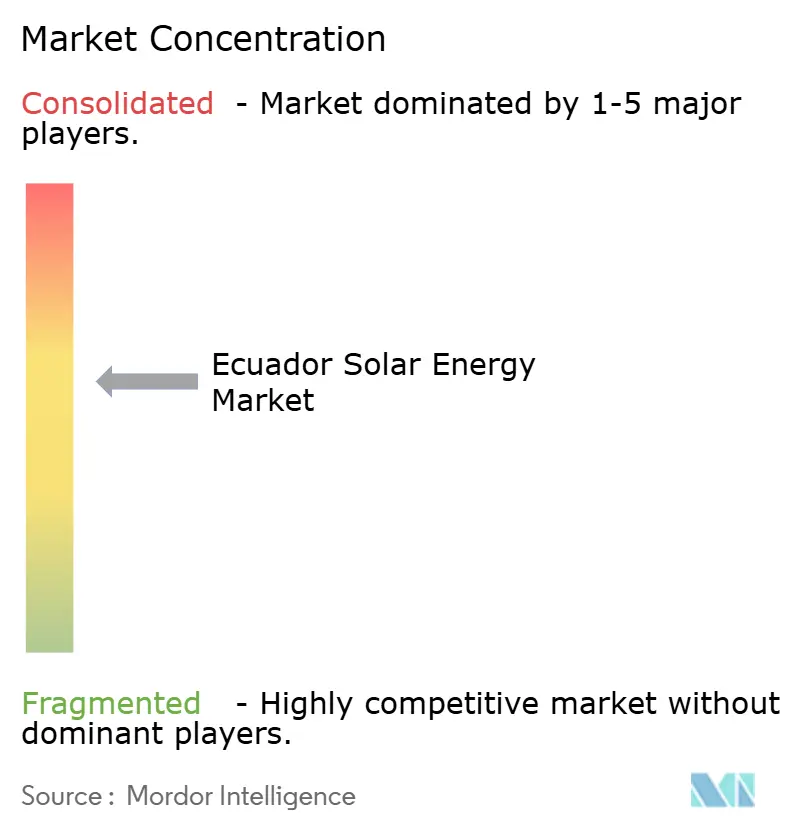

State-owned CELEC EP is the dominant developer, controlling a 1.58 GW pipeline financed by AFD and IDB and acting as off-taker for auctioned projects. Moderate concentration prevails because legislative changes now allow private developers to build up to 100 MW without bidding, a condition that is expected to dilute CELEC’s share beyond 2027. International EPC firms Acciona Energía and Enel Green Power compete for turnkey contracts, while local installers Renovaenergia, GoSolar Ecuador, and Solergy Ecuador focus on sub-1 MW rooftops empowered by Regulation 013/2021.

The equipment supply chain is dominated by Chinese brands such as JinkoSolar, Trina Solar, Canadian Solar, Huawei Digital Power, and Sungrow Power, whose zero-duty panels and competitive inverter pricing reduce capex. High-efficiency N-type and bifacial modules are gaining ground as developers seek to maximize output within limited land envelopes. Risen Energy and LONGi are increasing shipments, expanding choice for upcoming tenders.

Financing trends favor concessional loans blended with local-currency tranches; the DREX platform launched by IDB in 2024 connects SMEs with financing for 50-500 kW systems, lowering transaction costs. Market entrants that can combine EPC capability with structured finance and community relations expertise stand to win share as provincial governments insist on local employment clauses.

Ecuador Solar Energy Industry Leaders

Renovaenergia SA

Solergy Ecuador C.ltda.

Enercity SA

Acciona SA

Arausol Gmbh

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: ARCERNNR authorized 643 MW of distributed-energy projects, including 450 MW of commercial and industrial rooftop solar and 193 MW of utility-scale self-consumption systems. The approvals reflect accelerating adoption under Regulation 013/2021, which permits systems below 1 MW for self-consumption.

- January 2025: CELEC EP initiated the 200 MW La Ceiba solar project in Loja province, leveraging AFD concessional finance and targeting commissioning in late 2027. The project will anchor CELEC GENSUR's generation portfolio and serve mining load centers in southern Ecuador, reducing reliance on diesel peaking plants during hydro deficits.

- October 2024: Ecuador's National Assembly approved the "No More Blackouts" law, introducing tax incentives for self-generation and streamlining environmental permitting for renewable projects below 50 MW. The legislation responds to the 2024 energy crisis, which imposed blackouts of up to 14 hours daily and exposed the grid's vulnerability to hydro seasonality.

- October 2024: The Ecuadorian government raised the private-project threshold from 10 MW to 100 MW, eliminating competitive-bidding requirements for mid-scale solar developments. The reform is expected to attract independent power producers and accelerate financial close for projects in provinces where CELEC EP lacks capital for grid reinforcement.

Ecuador Solar Energy Market Report Scope

Solar power means using the sun's energy to produce electricity, either directly as thermal energy (heat) or indirectly through photovoltaic cells in solar panels and clear photovoltaic glass.

The Ecuador solar energy market is segmented by technology, grid type, end-user, and component type. By technology, the market is segmented into solar photovoltaic (PV) and concentrated solar power (CSP). By grid type, the market is segmented into on-grid and off-grid. By end-user, the market is segmented into utility-scale, commercial and industrial, and residential. By component, the market is segmented into solar modules, inverters, mounting and tracking systems, balance-of-system and electricals, energy storage, and hybrid integration.

The report also covers the market size and forecasts for the Ecuador solar energy market. For each segment, market sizing and forecasts have been done based on installed capacity.

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Key Questions Answered in the Report

How fast is solar capacity expected to grow in Ecuador by 2030?

Installed photovoltaic capacity is forecast to climb from 33 MW in 2025 to 950 MW in 2030, a 95.81% CAGR.

Which provinces are likely to receive the most new solar projects?

Loja, Manabí, and Guayas lead the pipeline thanks to high irradiation and better grid access, with more than 60% of planned megawatts.

What policy change most benefits private solar developers?

The October 2024 reform that raised the private-project threshold to 100 MW removes the need for competitive bidding and shortens licensing timelines.

Why is PV favored over CSP in Ecuador?

PV costs USD 800-900 per kW versus USD 3,500-4,500 per kW for CSP, and national direct-normal-irradiance levels are below CSP economic thresholds.

How do current solar electricity costs compare with hydro peaking costs?

Solar LCOE ranges from USD 40-50 per MWh, while new hydro peaking plants stand at USD 60-80 per MWh, making PV the cheapest marginal option.

What incentives exist for commercial rooftop installations?

Regulation 013/2021 allows systems under 1 MW to net-meter surplus power and qualify for five-to-seven-year paybacks at current retail tariffs.

Page last updated on: