Educational Consulting And Training Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

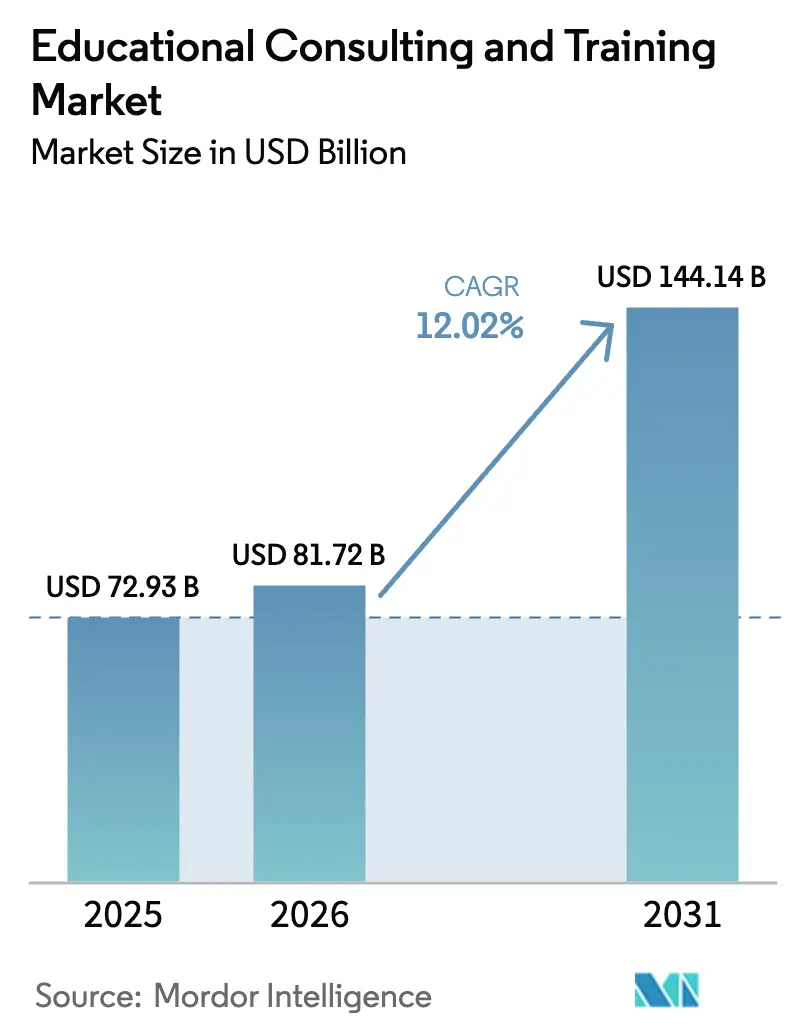

| Market Size (2026) | USD 81.72 Billion |

| Market Size (2031) | USD 144.14 Billion |

| Growth Rate (2026 - 2031) | 12.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Educational Consulting And Training Market Analysis by Mordor Intelligence

Educational Consulting and Training market size in 2026 is estimated at USD 81.72 billion, growing from 2025 value of USD 72.93 billion with 2031 projections showing USD 144.14 billion, growing at 12.02% CAGR over 2026-2031. To sustain that pace, public-sector agencies, higher-education systems, and large employers are shifting away from ad-hoc workshops toward multiyear, outcome-based engagements that tie invoices to clearly defined learning or employment metrics. Buyers of Educational Consulting and Training market services now demand integrated solutions that cover needs analysis, program design, technology deployment, instructor enablement, and post-training analytics in one contract, eroding the historic distinction between strategy consultants and content providers [1]HM Treasury, “Spring Budget 2024,” gov.uk . Artificial-intelligence tooling has become the lever that compresses development cycles by generating adaptive content and real-time feedback loops, allowing providers to charge premium fees for personalization at scale while improving completion rates and learner satisfaction. At the same time, tightening privacy regulations and new professional-licensure rules oblige institutions to demonstrate auditable compliance, channelling additional demand toward firms that can bundle instructional expertise with legal and cybersecurity capabilities.

Key Report Takeaways

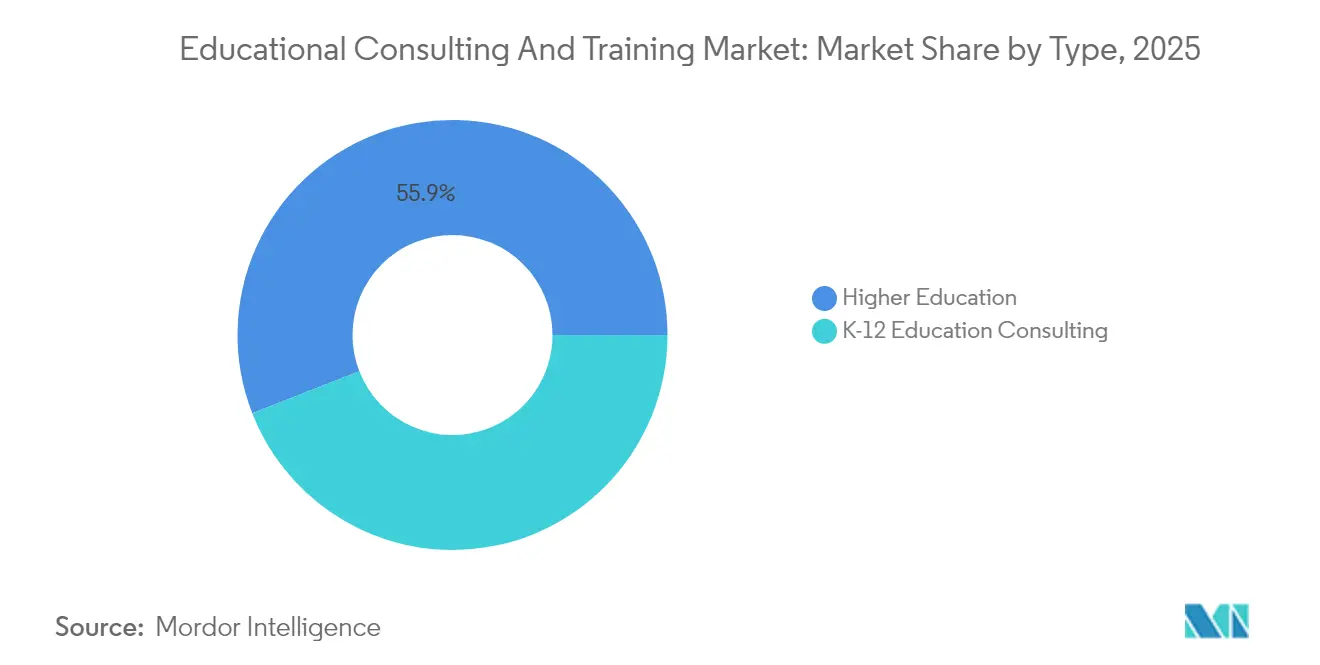

- By type, Higher Education held 55.92% of the educational consulting and training market share in 2025, whereas K-12 is expanding at an 13.1% CAGR through 2031.

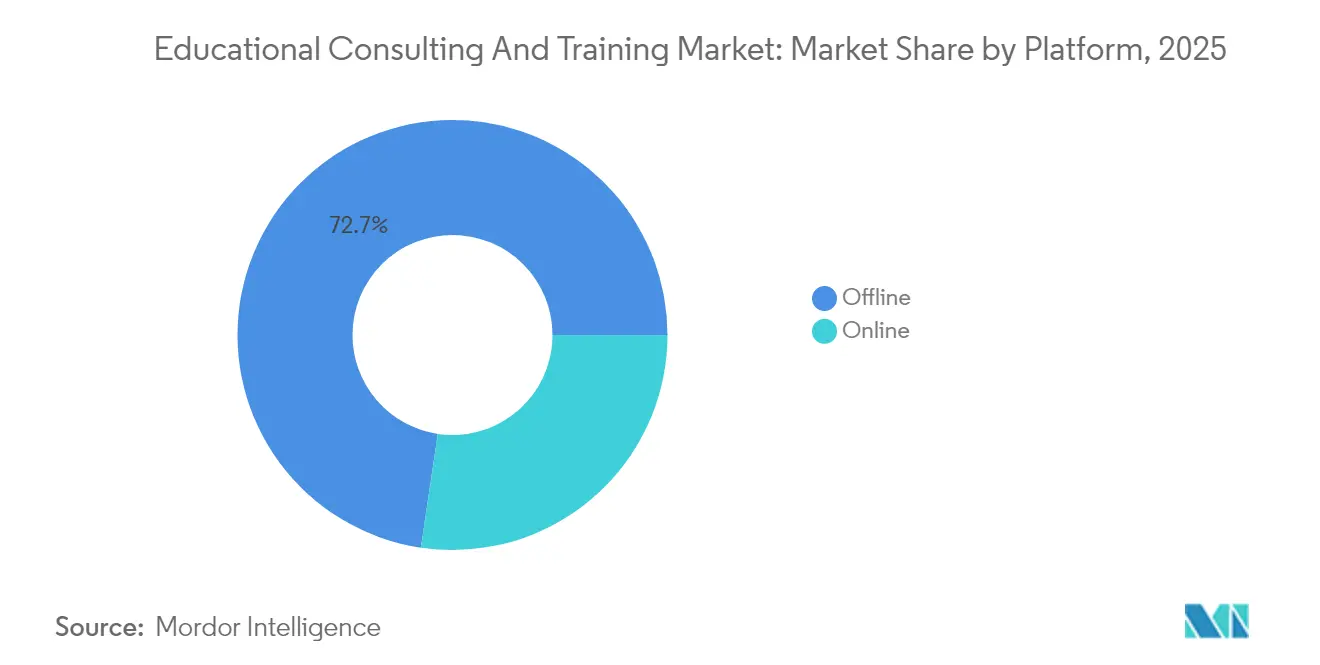

- By platform, offline solutions accounted for 72.65% of the educational consulting and training market share in 2025, while online modalities are forecast to grow at a 19.2% CAGR to 2031.

- By service offering, teacher professional development captured 36.12% of the educational consulting and training market share in 2025; AI-assisted instructional design is projected to surge at a 19.75% CAGR through 2031.

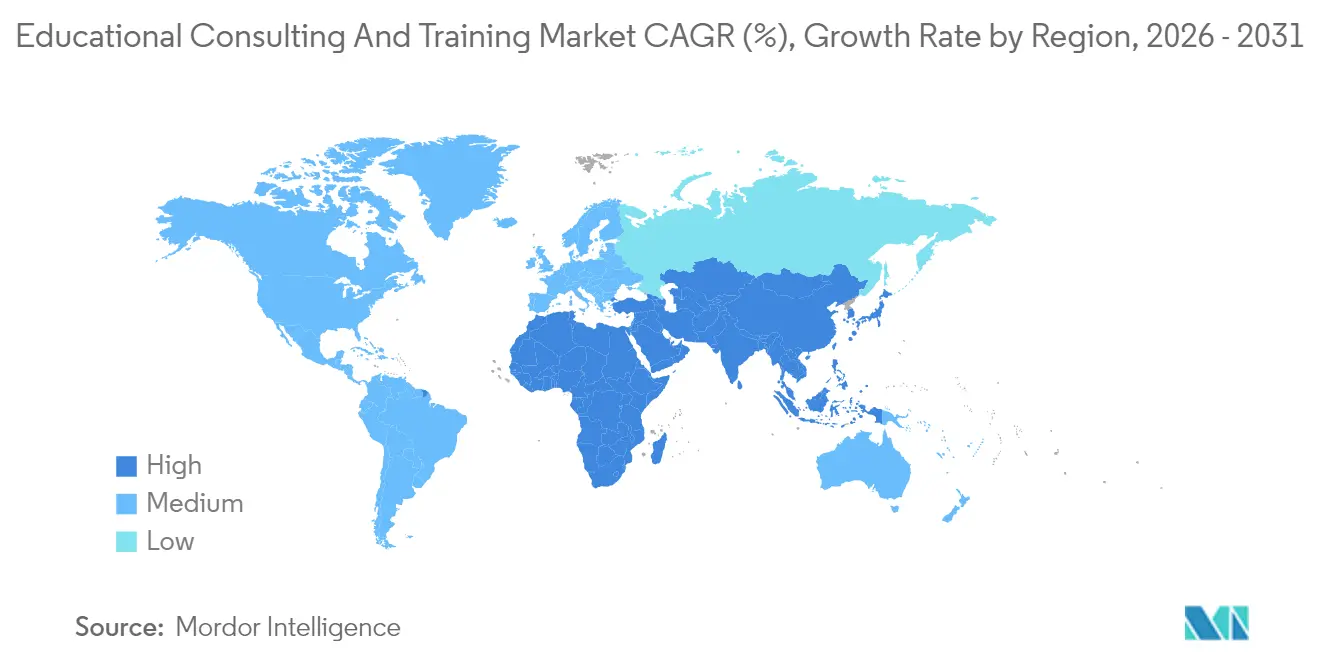

- By geography, North America led with a 38.95% of the educational consulting and training market share in 2025, but Asia-Pacific is set to post the fastest 14.62% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Educational Consulting And Training Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid digital-learning adoption (post-pandemic) | +2.8% | Global, with concentrated impact in North America & Europe | Medium term (2-4 years) |

| Government upskilling initiatives & funding | +2.1% | Global, strongest in Asia-Pacific and North America | Long term (≥ 4 years) |

| Rising corporate L&D budgets for reskilling | +1.9% | North America & Europe core, expanding to APAC | Medium term (2-4 years) |

| Growing demand for outcome-based consulting | +1.6% | Global, led by North America and Western Europe | Short term (≤ 2 years) |

| AI-assisted instructional design outsourcing | +1.4% | North America & Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Demand for ESG-linked workforce training | +1.2% | Europe leading, North America following, APAC emerging | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Digital-Learning Adoption Drives Platform Transformation

Hybrid delivery has become institutional policy rather than a contingency plan, which materially enlarges the Educational Consulting and Training market as clients seek partners who can unify pedagogy, technology, and change management. The United Kingdom appropriated USD 3.14 billion (GBP 2.5 billion) for national digital-skills development running through 2025[2]New Jersey Department of Labor & Workforce Development, “Future of Work Task Force Update,” nj.gov . In 2024, Singapore's SkillsFuture initiative expanded its portfolio of online learning modules and introduced a requirement for outcome-tracking dashboards as a prerequisite for grant funding. This strategic move aims to enhance accountability and measure the effectiveness of funded programs. Such mandates shift consulting scopes from basic platform selection to enterprise-wide learner analytics integration, faculty enablement, and credential architecture. Corporations mirror this urgency by migrating legacy content into cloud-based learning-experience platforms that embed adaptive algorithms, thereby feeding a virtuous cycle in which data-rich environments help consultants demonstrate ROI and unlock follow-on assignments.

Government Upskilling Initiatives Reshape Market Demand

Governments now treat workforce skilling as macroeconomic policy. New Jersey’s USD 50 million Workforce Development Initiative, launched in 2024, requires grantees to partner with external specialists for curriculum design and employer outreach[3]Journal of Interactive Media in Education, “The Importance of Offline Options for Online Learners,” jime.open.ac.uk . Queensland's Skills Strategy allocates co-investment grants to training consortia designed to align with industry requirements. These consortia are mandated to deliver annual impact reports, which undergo audits conducted by independent third-party consultants to ensure accountability and transparency. Similarly, Canada's Future Skills Centre has prioritized funding for experimental training pilots, with disbursement contingent upon the adoption of comprehensive and rigorous evaluation frameworks. These strategic initiatives are driving growth in the Educational Consulting and Training market, as a significant portion of colleges, vocational institutions, and employer coalitions lack the internal resources and expertise necessary to comply with the increasingly stringent evidence-based policy standards.

Corporate L&D Budget Expansion Fuels Reskilling Demand

Enterprise training budgets have rebounded sharply as boards link skill currency to risk mitigation. In 2024, technology firms across North America demonstrated a strategic shift by increasing their per-employee learning investments. Notably, over 50% of these expenditures were allocated to skill development in critical areas such as cloud computing, artificial intelligence, and cybersecurity, reflecting a focused approach to addressing evolving technological demands. Consulting opportunities span needs analysis, curriculum co-development with original-equipment manufacturers, and post-program analytics that map learning to operational KPIs—a holistic mandate that few pure-play content vendors can satisfy. As a result, the Educational Consulting and Training market increasingly rewards full-stack providers capable of advising on technology roadmaps, sourcing adjunct faculty, and integrating learning telemetry into enterprise data warehouses.

Outcome-Based Consulting Models Gain Traction

In 2025, several U.S. university systems released RFPs that incorporated performance-bond requirements specifically for retention-focused projects. This development reflects a growing emphasis on financial accountability and measurable outcomes, such as improved graduation rates and higher certification pass rates. Consequently, consulting firms are allocating resources toward advanced baseline diagnostics, rigorous control-group design, and the establishment of secure data rooms to meet the demands of third-party verification processes. These measures have significantly increased entry barriers, favoring established players with substantial financial stability. This shift underscores a broader trend in the Educational Consulting and Training market, where scalability and robust balance sheets are becoming critical competitive advantages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget constraints in educational institutions | -1.8% | Global, most acute in North America post-ESSER | Short term (≤ 2 years) |

| Talent shortage of specialized consultants | -1.2% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Data-privacy compliance costs (GDPR, etc.) | -0.9% | Europe is leading, expanding globally | Long term (≥ 4 years) |

| Client fatigue from point-solution sprawl | -0.7% | North America & Europe primarily | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Budget Constraints Challenge Institutional Spending

The wind-down of Elementary and Secondary School Emergency Relief funding forces U.S. districts to trim discretionary services just as pandemic-related learning loss persists. Higher-education institutions confront flat tuition revenue and declining public appropriations, compelling CFOs to favor incremental, modular consulting scopes over transformational megaprojects. Providers seeking to defend their share of the Educational Consulting and Training market must therefore embed ROI calculators, flexible payment milestones, and grant-writing assistance into proposals.

Specialized Consultant Talent Shortage Limits Growth

The North American market is witnessing a pronounced gap between the demand for and supply of professionals with expertise in pedagogy, data science, and cloud architecture. This talent shortage has driven up average salary packages for senior learning analytics roles, reflecting the premium placed on these specialized skills. The resulting capacity constraints are causing extended delivery lead times, which, in turn, are delaying revenue recognition across the Educational Consulting and Training market. To mitigate these challenges, key market players are implementing strategic initiatives, including the establishment of internal academies and the formation of partnerships with universities. These efforts are designed to build a sustainable talent pipeline of credentialed designers, enabling organizations to enhance scalability, improve operational efficiency, and meet growing market demands effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Higher Education Dominance Amid K-12 Acceleration

In 2025, Higher Education engagements accounted for 55.92% of the Educational Consulting and Training market share. This performance was attributed to universities prioritizing strategies to address declining enrolment rates, develop stackable micro-credential programs, and align academic curricula with labour-market trends and data-driven insights. Typical statements of work span diagnostic analytics, program-portfolio rationalization, and registrar-system integration. K-12, although representing a smaller share, will log an 13.1% CAGR, marking it the fastest-moving component of the Educational Consulting and Training market through 2031. State literacy mandates, science-of-reading implementations, and federally backed tutoring consortia anchor demand for professional-development sessions, coaching cycles, and curriculum mapping. District buyers favour short, grant-aligned projects, yet the cumulative volume of those engagements generates sizeable addressable revenue for regional specialists able to scale delivery across multiple school systems.

Higher Education clients typically sign multiyear master services agreements that cover enterprise resource planning, data-warehouse upgrades, and enrollment-marketing optimization, preserving high visibility for service revenue. Conversely, K-12 boards operate on annual budgets, driving providers to adopt modular toolkits and cost-sharing consortium models. Cross-selling potential emerges as higher-education consultancies downshift adjacent services, such as graduate-tracking dashboards, into K-12 markets, thereby expanding the Educational Consulting and Training market footprint without large marketing overhead.

By Platform: Offline Persistence Despite Online Surge

Offline engagement still delivered 72.65% of the Educational Consulting and Training market size in 2025, mainly because leadership institutes, lab-based technical training, and compliance audits demand face-to-face observation. Yet online modalities will absorb nearly all incremental spend, accelerating at 19.2% CAGR as synchronous virtual classrooms, AI-chat tutors, and mobile micro-learning apps mature. Institutions increasingly favour hybrid “click-and-campus” blueprints whereby foundational theory appears in asynchronous modules and higher-order practice unfolds in facilitated workshops. Consultants must therefore design content that travels seamlessly between platforms, institute data pipelines that blend LMS logs with in-person observation rubrics, and certify facilitators in both virtual and live delivery. Providers excelling at this orchestration will gain a disproportionate share of the Educational Consulting and Training market.

Operational economics vary significantly depending on the modality. Digital programs achieve higher gross margins, particularly after the completion of platform amortization, whereas travel-intensive workshops tend to operate with comparatively lower gross margins. However, offline pathways maintain higher client-retention rates and generate ancillary revenue from facility rentals and executive-education lodging. The optimal portfolio for Educational Consulting and Training industry leaders, therefore, balances margin-rich digital catalogs with relationship-anchoring in-person residencies, supported by unified credential frameworks.

By Service Offering: Professional Development Leadership

Teacher Professional Development accounted for 36.12% of the Educational Consulting and Training market share in 2025, reflecting legislative pressure linking educator effectiveness to student-achievement metrics. Key contract themes revolve around the implementation of culturally responsive pedagogy, the adoption of project-based assessment methodologies, and the organization of workshops aimed at enhancing educational technology integration. The AI-assisted Instructional Design market is projected to grow at a CAGR of 19.75%. This growth is driven by the increasing utilization of generative AI technologies, which facilitate the development of personalized learning sequences designed to meet the unique requirements of diverse learner demographics. The integration of such advanced AI tools is expected to significantly transform instructional methodologies, enabling more effective and inclusive educational outcomes. Consultants sell subscription-style retainers that combine design sprints, model-drift monitoring, and ethical-AI audits—services that command double-digit margin premiums.

Strategic & Operational Consulting keeps steady momentum by guiding institutions through structural reform, shared-services adoption, and partnership brokering with employers. Student Assessment & Support Services exhibit moderate expansion as early-warning analytics and success coaching become essential to retention targets. Collectively, these offerings reinforce the breadth requirement for players seeking to lead the Educational Consulting and Training industry.

Geography Analysis

North America generated 38.95% of 2025 revenue, owing to substantial federal and state funds aligned to workforce programs and digital-infrastructure upgrades. The Infrastructure Investment and Jobs Act earmarked multibillion-dollar grants for community-college modernization, while state initiatives such as California’s Strong Workforce Program stipulate mandatory third-party evaluations. Consulting engagements often encompass platform migration, workforce reskilling, and economic impact evaluations. These integrated service offerings contribute to an increase in the average size of deals, reflecting the growing demand for comprehensive and value-driven solutions in the market. Canadian provinces deploy stackable credential pilots and Indigenous education initiatives that further expand the Educational Consulting and Training market.

Asia-Pacific is projected to clock a 14.62% CAGR, fuelled by government digitization drives and demographic tailwinds. China’s regional governments roll out AI-literacy certifications linked to industrial policy, forcing vocational institutes to seek external curriculum partners. India’s National Education Policy mandates multidisciplinary curriculum conversion across colleges, generating sustained consulting demand for syllabus mapping, faculty coaching, and accreditation logistics. Southeast Asian ministries of education, notably Vietnam and Indonesia, allocate ed-tech subsidies aimed at English proficiency and STEM capacity, positioning foreign consultants as valued implementation guides.

Europe posts mid-single-digit growth on the strength of GDPR compliance projects and ESG-skills mandates. The Corporate Sustainability Reporting Directive requires companies to track employee competence in climate-impact topics, spawning specialized instructional-design engagements at. Nordic countries pilot lifelong-learning vouchers redeemable on approved course catalogs, necessitating audit mechanisms often outsourced to consultants. Mediterranean economies leverage EU cohesion funds to modernize vocational centers, creating cross-border collaboration opportunities that enlarge the Educational Consulting and Training market footprint. The Middle East & Africa show smaller but accelerating demand as Gulf states pivot to knowledge-economy strategies and African Union members prioritize teacher-capacity building, though budget volatility tempers near-term scale.

Competitive Landscape

The Educational Consulting and Training market remains moderately concentrated: the top five providers control one-fourth of worldwide revenue. Multinational professional-services firms leverage their audit and IT-integration arms to secure multi-tower engagements, exemplified by Accenture’s 2024 purchase of Udacity that fused nano-degree catalogs with global change-management muscle. Big Four competitors replicate the strategy by bundling cloud alliances, analytics dashboards, and instructional-design studios, making it harder for smaller firms to win enterprise accounts.

Private equity accelerates consolidation, viewing SaaS learning platforms as recurring-revenue anchors around which service revenue can be layered. Bain Capital's acquisition of PowerSchool exemplifies a strategic approach by integrating a well-established base of school districts with the potential of an emerging AI assistant. This combination is positioned to drive growth opportunities through professional development offerings, leveraging the AI assistant to enhance value and expand market reach. Nonetheless, meaningful whitespace persists for specialists in learning analytics implementation, accessibility compliance, and bilingual curriculum design—areas where domain depth trumps scale.

Talent scarcity shapes competitive dynamics: firms that establish internal academies enjoy faster project mobilization and tighter delivery quality. Partnerships also proliferate; for example, mid-tier consultancies ally with cloud hyperscalers to access pre-built AI models, reducing development cost and accelerating deployment cycles. As regulatory frameworks tighten, credibility in data-governance certification becomes a decisive differentiator in the Educational Consulting and Training industry.

Educational Consulting And Training Industry Leaders

Accenture

Deloitte

PwC

Pearson

McKinsey & Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Bain Capital entered into a USD 5.6 billion agreement to purchase PowerSchool, securing a K-12 SaaS platform that reaches 55 million learners.

- March 2025: Franklin Covey unveiled an AI-augmented leadership-coaching suite to address corporate demand for scalable executive development.

- March 2024: Accenture finalized its Udacity acquisition, forming LearnVantage to deliver AI and data analytics reskilling programs at enterprise scale.

- May 2024: Skillsoft launched micro-credential pathways mapped to industry certifications, signaling continued movement toward competency-based learning.

Global Educational Consulting And Training Market Report Scope

Educational consulting and training encompass guiding schools, universities, and other educational institutions on various matters, including curriculum enhancement, educator development, and strategic initiatives. The educational consulting and training market forecast is segmented by type, platform, and geography. By type, the market is segmented into higher education consulting and K-12 education consulting. By platform, the market is segmented into online and offline. By geography, the market is segmented into Asia-Pacific, North America, Europe, South America, the Middle East and Africa, and the Rest of the World. The reports offer the market size and forecasts for the educational consulting and training market in value (USD) for all the above segments.

| Higher Education Consulting |

| K-12 Education Consulting |

| Online |

| Offline |

| Strategic & Operational Consulting |

| Curriculum & Instructional Design |

| Teacher Professional Development & Training |

| Student Assessment & Support Services |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Type | Higher Education Consulting | |

| K-12 Education Consulting | ||

| By Platform | Online | |

| Offline | ||

| By Service Offering | Strategic & Operational Consulting | |

| Curriculum & Instructional Design | ||

| Teacher Professional Development & Training | ||

| Student Assessment & Support Services | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the Educational Consulting and Training market be in 2031?

Forecasts indicate it will reach USD 144.14 billion, expanding from USD 72.93 billion in 2025 to USD 81.72 billion in 2026 at a 12.02% CAGR.

Which segment represents the greatest share of current consulting revenue?

Higher Education engagements hold 55.92% of 2025 revenue, driven by enrolment, digital-transformation, and workforce-alignment initiatives.

Which delivery platform is growing fastest?

Online and hybrid modalities are projected to scale at a 19.2% CAGR, absorbing most incremental spending through 2031.

Why is AI-assisted instructional design accelerating?

Generative-AI tools cut course-development cycles while enabling personalization, propelling this service line at a 19.75% CAGR.

What regional market will record the quickest growth?

Asia-Pacific is set to pace the field with a 14.62% CAGR, supported by government digitization programs and rising middle-class enrolment demand.

How are consulting fee structures evolving?

Institutions and enterprises increasingly insist on outcome-based contracts that link consultant payments to measurable learning or employment metrics.

Page last updated on: