Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

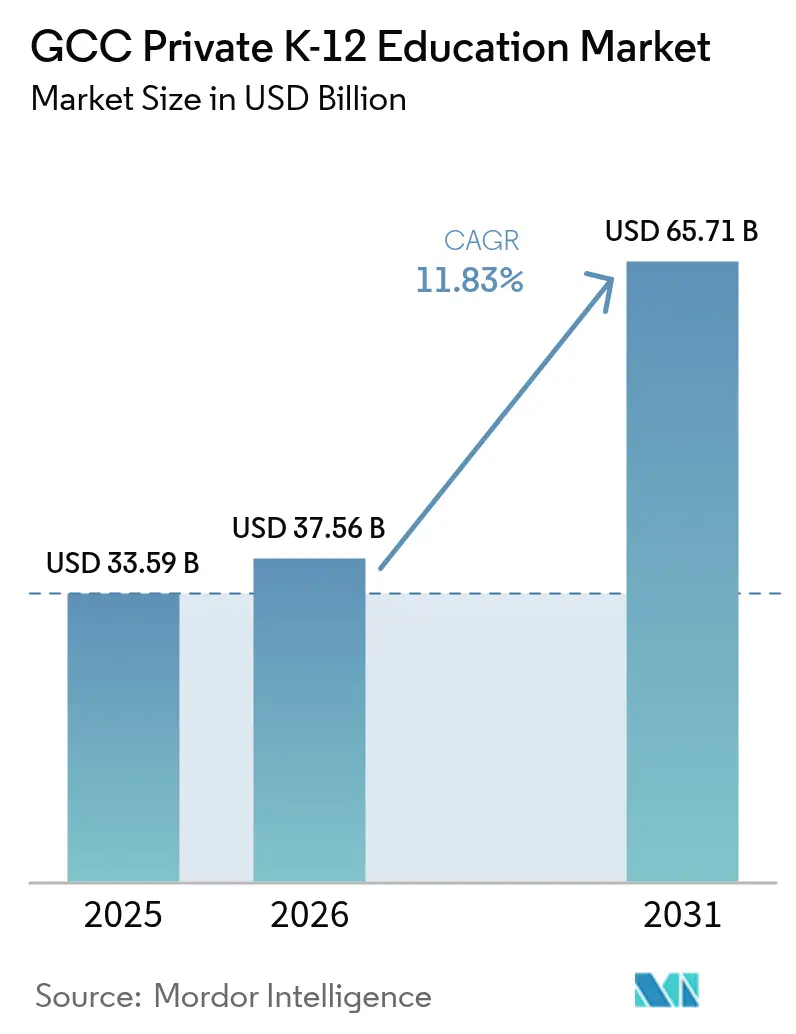

| Base Year Market Size (2025) | USD 33.59 Billion |

| Market Size (2026) | USD 37.56 Billion |

| Market Size (2031) | USD 65.71 Billion |

| Growth Rate (2026 - 2031) | 11.83% CAGR |

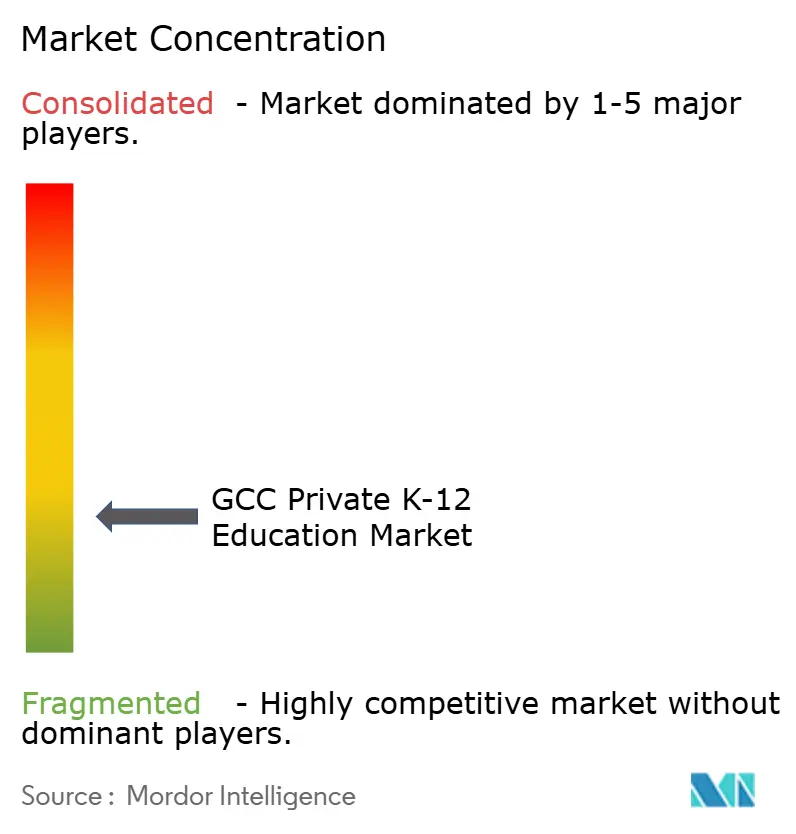

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Private K-12 Education Market Analysis by Mordor Intelligence

The GCC private K-12 education market size is expected to grow from USD 33.59 billion in 2025 to USD 37.56 billion in 2026 and reach USD 65.71 billion by 2031, with a CAGR of 11.83% during 2026-2031. Government funding, regulatory reforms encouraging foreign investment, and public-private partnerships are driving supply growth and quality improvements across Saudi Arabia, the UAE, Qatar, Oman, Bahrain, and Kuwait. Increased public budgets in 2025 and 2026 align with national strategies focused on skills and employability, sustaining demand for diverse curricula and long enrollment periods. Expatriate families contribute to a steady demand for British, American, and CBSE curricula, offering globally recognized qualifications and bilingual options. Infrastructure concessions and asset-light models are improving access across price points, helping operators manage rising construction costs and regulatory fee controls while maintaining academic standards.

Key Report Takeaways

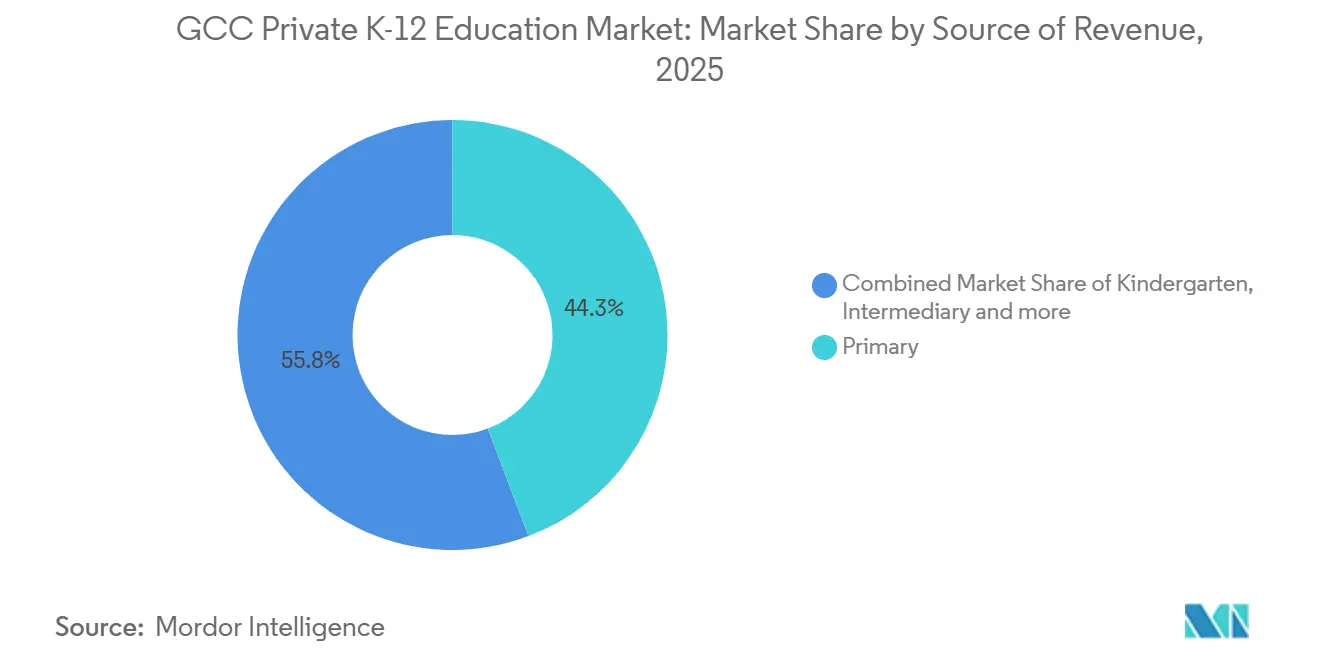

- By source of revenue, Primary programs accounted for 44.25% of the GCC private K‑12 education market in 2025, while Kindergarten is projected to expand at a 12.14% CAGR through 2031.

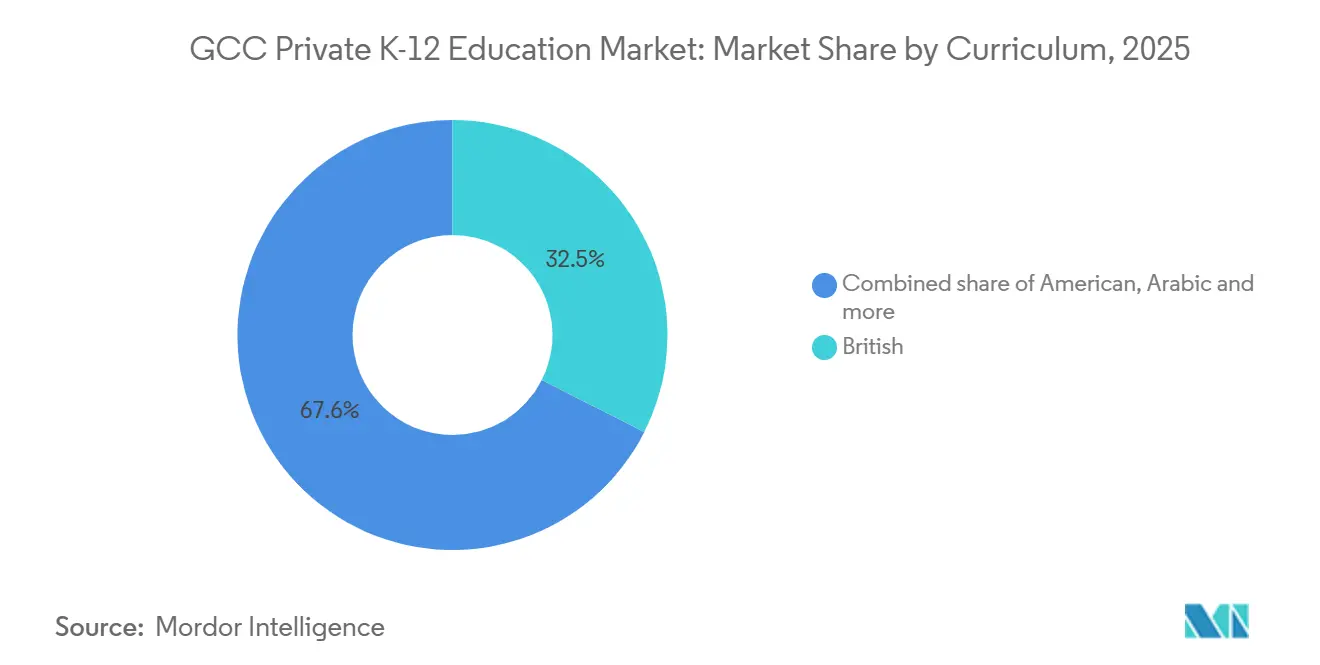

- By curriculum, British programs captured 32.45% of the GCC private K‑12 education market size in 2025, and CBSE is forecast to grow at a 13.05% CAGR through 2031.

- By nationality, expatriate students accounted for 82.95% of the GCC private K‑12 education market size in 2025, while local students are projected to grow at a 7.31% CAGR through 2031.

- By geography, Saudi Arabia accounted for 37.05% of the GCC private K‑12 education market in 2025, and Qatar is set to record a 12.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Private K-12 Education Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong government reforms and elevated education budgets are accelerating sector momentum | +2.8% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| A growing influx of expatriates is sharply increasing demand for international curricula | +3.1% | UAE, Qatar, Kuwait | Short term (≤ 2 years) |

| Higher household purchasing power is driving the uptake of premium‑fee schooling | +1.7% | Riyadh, Dubai, Doha | Long term (≥ 4 years) |

| Wider integration of EdTech solutions is improving learning quality and delivery | +2.2% | UAE, Saudi Arabia | Medium term (2-4 years) |

| Large‑scale PPP school‑infrastructure initiatives are opening new avenues for private investment | +1.4% | Saudi Arabia, Qatar | Long term (≥ 4 years) |

| Expanded access to Sharia‑compliant financing is attracting a broader base of investors | +0.7% | Saudi Arabia, UAE, Bahrain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strong government reforms and elevated education budgets are accelerating sector momentum

Saudi Arabia’s SAR 202 billion (USD 53.82 billion) education budget for 2026 reflects its ongoing efforts to enhance teaching standards, facilities, and student services in the GCC private K-12 education market. Vision 2030’s privatization program supports private capital investment in school infrastructure, ensuring long-term seat expansion. The UAE allocated AED 10.9 billion (USD 2.97 billion) for education in its 2025 federal budget, with PPP initiatives increasing capacity while balancing affordability and quality. Qatar’s 2026 education budget prioritizes improved outcomes and access, supported by private delivery models. Regulatory measures, including foreign ownership permissions, attract international brands with multi-curriculum expertise to the GCC market.

A growing influx of expatriates is sharply increasing demand for international curricula

Foreign nationals form a significant share of residents in several GCC countries, driving demand for internationally recognized credentials in the private K-12 education market. The Indian diaspora supports CBSE pathway enrollments, ensuring steady progression from early years to senior grades. The CBSE Global Curriculum, launching in April 2026, aligns with host country standards and enhances student mobility within and beyond the region. British and American curricula remain popular among families seeking bilingual proficiency and university admission pathways. This sustains seat utilization in established schools and encourages new school proposals in areas with growing expatriate populations[1]Times of India, “CBSE to Introduce Global Curriculum Across UAE and Other Countries from April 2026,” Times of India, timesofindia.indiatimes.com.

Wider integration of EdTech solutions is improving learning quality and delivery

Operators in the GCC private K-12 education market are integrating adaptive learning platforms, robotics, and immersive content to enhance teaching methods and differentiate offerings. Education groups use student information systems and classroom analytics to personalize instruction and enable early interventions, improving outcomes and parent engagement. Campuses are investing in AI-equipped labs and maker spaces to align with national digital strategies and prepare students for data-driven careers. Collaborations with technology firms and innovation accelerators expand access to curated content and startup ecosystems, enriching classroom learning. Building digital skills among teachers remains essential to achieving instructional and operational improvements[2]Education Middle East, “GCC Education Suppliers Join the AI Adoption Race,” Education Middle East, educationmiddleeast.com.

Large‑scale PPP school‑infrastructure initiatives are opening new avenues for private investment

Saudi Arabia's privatization framework integrates private operators into school delivery while retaining state curriculum oversight, enabling capacity growth without fully burdening public budgets in the GCC private K-12 education market. In the UAE, initiatives like Dubai Schools add thousands of seats with fee caps to ensure affordability and support mid-market enrollment. Qatar's budget approvals and tenders assign operational responsibilities to experienced non-public partners under long-term agreements, ensuring service continuity. Asset-light contracts and long leases reduce capital requirements, aligning with investor preferences and accelerating scaling. Quality assurance measures and inflation-indexed reimbursements enhance predictable cash flows, attracting global education platforms.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent shortages of qualified teachers are constraining school operations | -1.2% | UAE, Saudi Arabia, Qatar | Short term (≤ 2 years) |

| Rising land and construction costs are inflating campus development expenses | -0.9% | Dubai, Abu Dhabi | Medium term (2-4 years) |

| Imposed tuition‑fee caps are compressing school profit margins | -0.6% | Dubai | Short term (≤ 2 years) |

| Market saturation of premium schools in Dubai and Abu Dhabi is limiting growth potential | -0.8% | Dubai, Abu Dhabi | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent shortages of qualified teachers are constraining school operations

Vacancy postings are outpacing domestic teacher supply in high-growth areas, increasing recruitment cycles and onboarding costs in the GCC private K-12 education market. Flexible policies on ownership and investment are attracting international brands with global talent networks. However, bilingual and specialist roles still rely on expatriate educators. Education groups are developing internal academies and certifications to improve digital pedagogy and leadership skills, enhancing classroom quality and inspection outcomes. Professional development requires sustained investment in coaching, resources, and career pathways to retain skilled teachers. Recruitment challenges will persist until more locally trained graduates join the profession.

Rising land and construction costs are inflating campus development expenses

Land scarcity and high construction costs in the GCC private K-12 education market extend project timelines and increase breakeven thresholds for new schools. Operators are adopting asset-light strategies, separating operations from real estate ownership to safeguard returns and expand seat capacity. Public-Private Partnership (PPP) concessions with capped fees and minimum service commitments reduce construction risks and align payments with enrollments. Selective property acquisitions near flagship campuses help incrementally increase capacity while maintaining standards. Stabilizing construction costs, along with phased development and partnership models, is expected to support balanced growth and affordability in the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source of Revenue: Early Childhood Surges as Operators Lock Lifetime Value

Primary programs accounted for 44.25% of the GCC private K-12 education market share in 2025. Kindergarten is expected to grow at a compound annual growth rate (CAGR) of 12.14% through 2031. Public budgets and reforms in Saudi Arabia are expanding preschool access, enabling earlier enrollment and longer educational cycles. Operators are enhancing early years networks and integrating nurseries to capture value, extending into primary and secondary education. Public-private partnerships (PPPs) are boosting entry-level demand by adding capacity with affordability measures, encouraging structured pathways at younger ages. In Oman, Vision 2040 has clarified investment permissions and project pipelines, driving capacity growth in areas with rising early childhood enrollments.

Intermediary and secondary segments represent the remaining revenue share, benefiting from higher fees linked to examination stages, specialized facilities, and counseling services. Saudi education groups are introducing bilingual tracks to meet demand for Arabic and global credentials. In the UAE, inspection frameworks and quality oversight are driving investments in teacher development and advanced facilities. Operators are aligning electives with national priorities in technology and entrepreneurship, emphasizing career readiness. Integrated campuses are expected to sustain strong utilization and retention across student cohorts.

By Curriculum: CBSE Gains as British Brands Defend Share Through Premium Differentiation

British programs represented 32.45% of enrollments in 2025, remaining a key choice for families pursuing established university pathways. The CBSE curriculum is projected to grow at 13.05% through 2031, driven by the region's Indian diaspora and its strong progression from primary to senior grades. The CBSE Global Curriculum, launching in April 2026, will align with host country requirements, including Arabic and Islamic studies, while ensuring credential portability for tertiary admissions. Multi-curriculum groups are expanding British and CBSE offerings to meet demand, integrating digital tools to personalize instruction and streamline assessments. American and IB pathways retain strength in senior years, supporting diverse academic options across income segments[3]Interval Edu, “CBSE Global Curriculum to Launch in UAE 2026,” Interval Edu, intervaledu.com.

Portfolio strategies focus on resilient demand pools and balanced pricing, supporting utilization across income groups. Operators emphasize transparent reporting of exam results, university placements, and enrichment programs to build brand equity. In Saudi Arabia, bilingual pathways are increasingly relevant as families seek strong Arabic instruction alongside international credentials. In the UAE, schools invest in faculty and facilities to secure regulatory support for fee adjustments. Curriculum optimization and measured expansions are expected to balance access and academic excellence over the forecast period.

By Nationality: Expatriate Dominance Persists as Golden Visas Lengthen Enrollment Tenures

Expatriate students made up 82.95% of enrollments in 2025. Local student enrollments are expected to grow at 7.31% annually through 2031, driven by government efforts to increase citizen participation in private schooling. Reforms emphasizing cultural preservation and bilingual instruction are building confidence among national families, especially when private schools align with state curricula in language and civics. In the UAE, non-citizens can enroll in public schools on a paid basis up to a set cap, which provides an alternative but does not significantly reduce demand for private international programs. Voucher and subsidy programs in some countries are directing citizen enrollments to approved private providers, ensuring stable seat utilization and affordability.

Education operators are improving admissions, parent engagement, and alumni pathways to reduce mid-year attrition and ensure continuity during key transitions. In Saudi Arabia, bilingual and international options are attracting national families seeking Arabic proficiency and global readiness. Clear inspection and licensing frameworks in the UAE provide operational stability for schools managing diverse student populations. Aligning curricula with labor market needs remains critical to sustaining participation. Consistent quality standards and targeted support are expected to reduce performance gaps while preserving educational choices for expatriate and national families[4]Education Saudi, “Saudi Arabia Education Trends – K12 Private Schools,” Education Saudi, education-saudi.com.

Geography Analysis

Saudi Arabia held 37.05% of revenues in 2025, supported by its privatization program, which expands school capacity while maintaining state oversight and curriculum standards. Education budgets remain a priority, with the 2026 allocation focusing on equipping students with skills aligned with economic transformation goals. International operators are introducing multi-curriculum offerings in major cities to attract expatriate and national families. New British schools, such as Sherborne School Jeddah, reflect growing demand in regions with rising middle- and upper-income populations.

The UAE continues to serve as a hub due to its scale, regulatory clarity, and experienced operators expanding capacity and curricula. Federal education budgets and emirate-level public-private partnership (PPP) initiatives support enrollment growth in entry- and mid-market segments. Groups like Taaleem and Aldar are increasing capacity through greenfield projects and acquisitions across British, American, IB, French, and bilingual pathways. Projects emphasizing technology and innovation enhance pedagogy and student experience. Capacity additions in new residential areas are expected to ease saturation in established zones. Qatar combines stable budget allocations with structured tenders directing delivery to non-public partners, ensuring pipeline visibility. British, American, and CBSE curricula attract families seeking global readiness and bilingual proficiency, supporting existing schools and guiding new proposals.

Oman’s Vision 2040 supports growth through full foreign ownership and PPP-driven school development. The curriculum mix includes a significant British presence, with new projects, such as international schools in Muscat’s knowledge corridors, meeting demand for diverse offerings.Bahrain and Kuwait sustain interest through stable policy frameworks and demand from expatriate communities. Expansion efforts often use asset-light or partnership models to manage capital intensity while addressing market needs.

Competitive Landscape

The GCC private K-12 education market includes large platforms and independent schools. Consolidation is visible in higher-priced segments, while mid-market price points remain fragmented. Operators such as GEMS Education, Taaleem, Aldar Education, Nord Anglia Education, and Cognita are expanding through new campuses, program diversification, and acquisitions. Their strategies emphasize broad curricula, bilingual tracks, and innovation-driven learning environments aligned with national skills agendas and parental expectations. Larger operators benefit from professional development and inspection readiness, while asset-light models and public-private partnerships (PPPs) provide flexibility in capital allocation. New entries from British brands are increasing competition for skilled teachers and senior leadership roles.

Recent transactions highlight institutional interest in regulated K-12 platforms across the GCC. A consortium led by EQT acquired Nord Anglia Education, with follow-on investment from Mubadala, positioning GCC capital in international school expansion strategies. Brookfield’s financing package for GEMS Education supports advanced campuses and digital learning initiatives. Taaleem has expanded through acquisitions in early childhood and French curriculum segments, enhancing its portfolio and supporting pipeline conversions. Cognita has grown through partnerships in Saudi Arabia, Oman, and Qatar, leveraging global curricula and teacher development systems.

Technology and innovation are key in the GCC private K-12 education market. Schools invest in AI-ready facilities, adaptive platforms, and entrepreneurship programs. Collaborations with technology providers enable scaling of best practices and improve data-driven instruction. Inspection frameworks in the UAE and aligned regional processes encourage continuous improvement, rewarding investments in quality, pastoral care, and inclusion. Campuses integrating early years through post-16 programs improve retention and operational efficiency through consistent pedagogy and shared facilities. Operators with balanced portfolios, strong teacher pipelines, and advanced digital capabilities are well-positioned to meet steady demand across income tiers in the GCC private K-12 education market.

GCC Private K-12 Education Industry Leaders

GEMS Education

Taaleem

Aldar Education

National Company for Learning & Education

SABIS Educational Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Dubai Holding Investments and Nord Anglia Education announced a partnership to establish and manage K-12 schools in Dubai. Dubai Holding Asset Management will develop facilities, while Nord Anglia will operate them. A British-curriculum school in Dubai Production City is planned, pending KHDA approval, to serve Jumeirah Golf Estates, Emirates Living, and Tilal Al Ghaf. Additional schools are planned in other Dubai Holding developments.

- February 2026: Apollo-managed funds invested USD 1 billion in subordinated hybrid notes issued by Aldar Properties PJSC, marking their fifth investment in Aldar since 2022. This brings total commitments to USD 2.9 billion. The funds will support Aldar's growth plans, including landbank replenishment, expanding its develop-to-hold portfolio (such as Aldar Education's 58,000-seat K-12 platform), and strategic acquisitions, representing significant foreign direct investment in Abu Dhabi's private sector.

- April 2025: Mubadala Investment Company made a USD 600 million investment to acquire a minority stake in Nord Anglia Education. This acquisition was carried out as part of a consortium led by EQT.

- April 2025: GEMS Education launched the Next Billion Innovation startup fund with a USD 1 million investment to foster student entrepreneurship at the School of Research and Innovation in Dubai.

GCC Private K-12 Education Market Report Scope

The GCC private K‑12 education market includes privately operated schools offering American, British, Arabic, CBSE, and other curricula to expatriate and local students. The market is segmented by revenue source (Kindergarten, Primary, Intermediary, Secondary), curriculum (American, British, Arabic, CBSE, Others), nationality (expatriate and local students), and country (Saudi Arabia, UAE, Qatar, Oman, Bahrain, Kuwait). Key drivers include government reforms, expatriate inflows, rising incomes, EdTech adoption, PPP initiatives, and Sharia-compliant financing. Restraints involve teacher shortages, rising costs, tuition fee caps, and school saturation. The report covers regulatory frameworks, technology trends, supply chains, and competition using Porter’s Five Forces. It provides market size, forecasts in USD, company profiles, and opportunities like bilingual schools and AI-driven learning platforms.

By Source of Revenue

| Kindergarten |

| Primary |

| Intermediary |

| Secondary |

By Curriculum

| American |

| British |

| Arabic |

| CBSE |

| Other |

By Nationality

| Expat Students |

| Local Students |

By Country

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Oman |

| Bahrain |

| Kuwait |

| By Source of Revenue | Kindergarten |

| Primary | |

| Intermediary | |

| Secondary | |

| By Curriculum | American |

| British | |

| Arabic | |

| CBSE | |

| Other | |

| By Nationality | Expat Students |

| Local Students | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Oman | |

| Bahrain | |

| Kuwait |

Key Questions Answered in the Report

What is the current size and growth outlook for the GCC private K-12 education market?

The GCC Private K-12 Education Market is currently valued at USD 33.59 billion in 2025, expected to grow to USD 37.56 billion in 2026, and is forecast to reach USD 65.71 billion by 2031 at a 11.83% CAGR over 2026–2031, indicating strong expansion and sustained demand across the region.

Which curricula are expanding fastest in the GCC private K-12 education market?

CBSE is projected to grow at 13.05% through 2031, while British programs retain the largest enrollment base among international pathways.

Which segments lead by source of revenue within the GCC private K-12 education market?

Primary programs led with 44.25% in 2025, while Kindergarten is the fastest growing stage with a 12.14% CAGR through 2031.

Which countries anchor demand in the GCC private K-12 education market through 2031?

Saudi Arabia led with a 37.05% revenue share in 2025, and Qatar is projected to grow fastest at a 12.03% CAGR through 2031.

What factors are shaping investment in the GCC private K-12 education market?

High government budgets, PPP models, expatriate demographics, and EdTech adoption are key drivers, while teacher shortages and land costs are important constraints.

How are leading operators differentiating in the GCC private K-12 education market?

Major groups are scaling multi curriculum portfolios, expanding early years capacity, and investing in AI ready learning environments and professional development to support outcomes and inspection readiness.

Page last updated on: