KSA Private K-12 Education Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

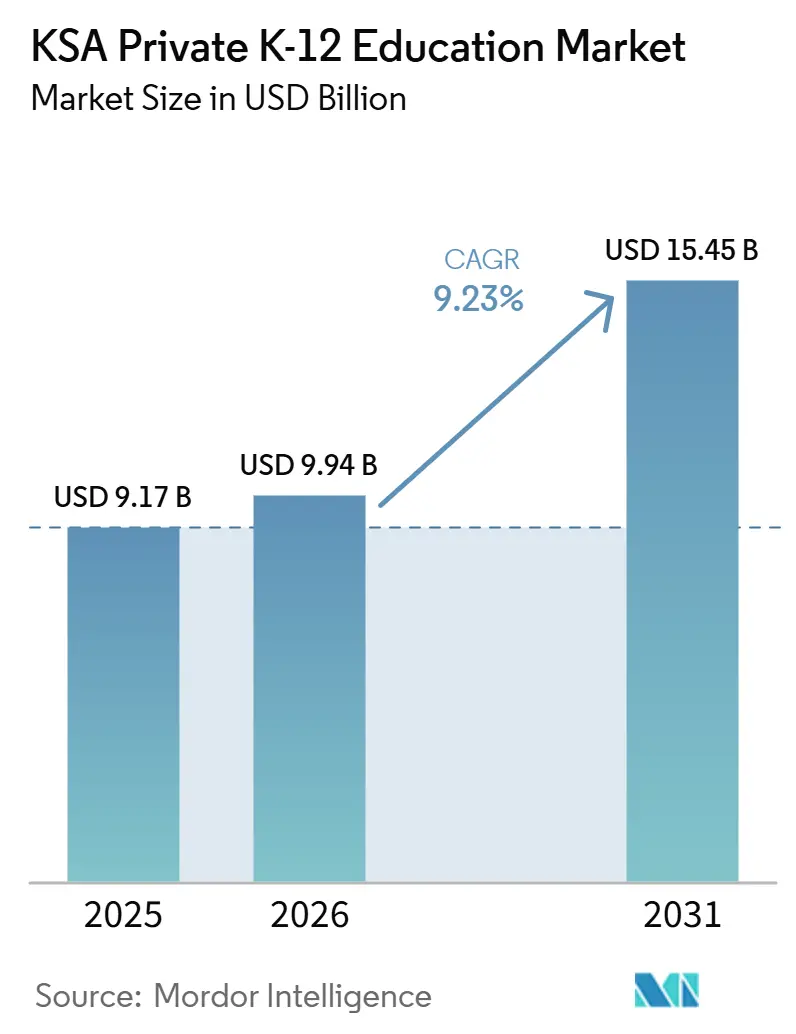

| Base Year Market Size (2025) | USD 9.17 Billion |

| Market Size (2026) | USD 9.94 Billion |

| Market Size (2031) | USD 15.45 Billion |

| Growth Rate (2026 - 2031) | 9.23% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

KSA Private K-12 Education Market Analysis by Mordor Intelligence

The KSA Private K-12 Education Market size is expected to grow from USD 9.17 billion in 2025 to USD 9.94 billion in 2026 and is forecast to reach USD 15.45 billion by 2031 at 9.23% CAGR over 2026-2031. Demographic expansion, Vision 2030 human-capital mandates, and rising expatriate inflows collectively underpin resilient enrolment demand that sustains new-build campuses and drives higher seat utilization ratios. Aggressive public-private partnership (PPP) programs now funnel fresh capital toward greenfield projects while risk-sharing models lower upfront financial hurdles for operators and accelerate time-to-market for new schools. Mandatory kindergarten enrolment beginning in 2025 further enlarges the addressable learner base, especially for providers that can quickly scale early-years capacities without compromising quality benchmarks mandated by the Ministry of Education. Intensifying curriculum diversification, epitomized by British, American, and hybrid offerings, positions premium operators to capture fee uplifts as parents prioritize global academic pathways.

Key Report Takeaways

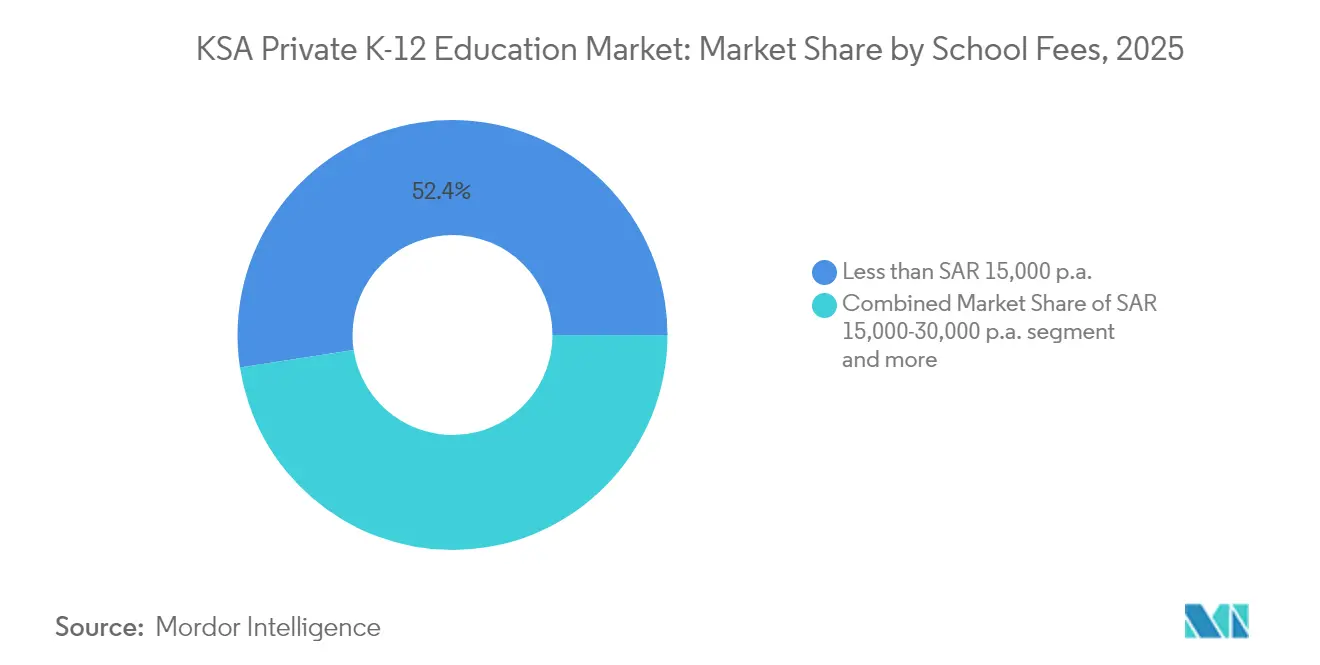

- By school fees, less than SAR 15,000 p.a. led with a 52.41% KSA private K-12 education market share in 2025, whereas above SAR 80,000 p.a. is advancing at a 15.74% CAGR through 2031.

- By curriculum, British programs accounted for 32.94% of the KSA private K-12 education market size in 2025, while American curricula posted the fastest 11.24% CAGR to 2031.

- By nationality, the expat students accounted for 72.88% of the KSA private K-12 education market size in 2025, while local students are expected to register the fastest growth rate of about 13.74% between 2026-2031.

- By region, the Riyadh area captured 36.12% of the KSA private K-12 education market share in 2025, and the other regions of KSA are expanding at a 7.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

KSA Private K-12 Education Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Population-led surge in school-age cohort | +3.2% | National, high density in Central and Western regions | Long term (≥ 4 years) |

| Ambitious Vision 2030 human-capital targets | +2.8% | Kingdom-wide, priority in major cities | Medium term (2-4 years) |

| K-12 privatization & PPP initiatives | +2.1% | Nationwide roll-out, early traction in Riyadh, Jeddah, Makkah | Medium term (2-4 years) |

| Rising preference for international curricula | +1.8% | Central and Western expatriate clusters | Short term (≤ 2 years) |

| Mandatory kindergarten from 2025 | +1.5% | National implementation | Short term (≤ 2 years) |

| AI-enabled personalised learning demand | +0.9% | Urban technology-forward campuses | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Population-led Surge in School-Age Cohort

Saudi Arabia’s school-age population is increasing 2.5% annually and is projected to hit 7.2 million by 2030, an expansion that requires 1.2 million additional seats to avoid overcrowding pressures that already strain high-demand urban districts [1]Ministry of Education, “Minister of Education: Our goal is to position Saudi Arabia among the top 20 educational systems worldwide,” MOE.gov.sa . Private providers are expected to supply these places, driving investors to expedite land acquisition and prefabricated construction efforts to maintain a competitive edge in meeting enrolment demands. The dominance of expatriates within the urban population is driving demand for private K-12 education in Saudi Arabia. Operators in this market benefit from offering globally recognized diplomas, which attract premium tuition fees. These revenues are strategically reinvested into upgrading facilities and enhancing extracurricular programs, strengthening their competitive positioning. Simultaneously, Saudi families now prize differentiated pedagogy and bilingual instruction as pathways to international university admissions, shifting enrolment from public to private classrooms. Sustained birth-rate momentum, coupled with extended life expectancy under Vision 2030’s healthcare agenda, ensures that classroom demand will remain buoyant well beyond the current forecast horizon.

Ambitious Vision 2030 Human-Capital Targets

A dedicated Business Centre now streamlines licensing, trims approval times, and packages incentives such as subsidized land leases, VAT relief, and foreign-ownership guarantees that entice premium global operators. Fourteen months of recruitment campaigns have already attracted thirteen international school brands to Riyadh, reinforcing the KSA private K-12 education market as a regional magnet for quality foreign educators and curriculum providers. Thirty-seven performance indicators, ranging from teacher-student ratios to STEM proficiency benchmarks, create an accountability matrix that elevates classroom outcomes while reassuring investors about regulatory predictability. Collectively, these measures deepen private-sector penetration and align graduate skill sets with the Kingdom’s shift toward knowledge-based economic activity.

K-12 Privatization & PPP Initiatives Gain Pace

The National Centre for Privatization has earmarked more than 200 education-sector projects, including large-scale PPP bundles that reduce sovereign capital outlays yet preserve state oversight through long-term service contracts [2]Ministry of Education, “Tuition Fee Regulations-Private Education,” MOE.gov.sa . Wave 1 and Wave 2 school projects already deliver 120 campuses in Jeddah, Makkah, and Medina, each secured by 20-year offtake agreements that ensure predictable cash flows for operators and financiers. The KSA private K-12 education market benefits from this risk-mitigated framework because project finance lenders perceive lower default probability, which cuts weighted average cost of capital and frees incremental resources for instructional technology. The Ministry’s inaugural privatization tender in 2024 signals a structural shift from single-asset procurement toward holistic service partnerships that bundle construction, operations, maintenance, and learning-outcome guarantees. Replicable PPP templates now enable rapid geographic replication, expediting market penetration in secondary cities that previously lacked bankable project structures.

Rising Preference for International Curricula

British curriculum programs dominate the KSA private K-12 education market with a 33.38% slice in 2024, but American tracks are compounding faster at 11.13% annually as parents target admissions to U.S. universities. Premium international schools charge between SAR 10,000 and SAR 30,000 per year (USD 2,600–8,000), a tariff multiple that funds specialist labs, leadership development modules, and expatriate teacher packages that smaller Arabic-medium schools cannot match. Regulatory amendments in 2017 eliminated foreign-ownership caps, unleashing direct investment from established chains that now proliferate hybrid models blending Saudi history and geography with Cambridge-aligned science syllabi. Such hybrids pacify regulators while satisfying parental appetite for globally recognized credentials, thereby widening total addressable tuition revenue. Market entrants, therefore, calibrate facility design, teacher recruitment, and extracurricular line-ups around internationally benchmarked learning outcomes that yield competitive advantage in scholarship awards and global league-table placements.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tuition-fee caps & licensing hurdles | −1.8% | Nationwide, stricter enforcement in top metros | Short term (≤ 2 years) |

| Shortage of qualified bilingual teachers | −1.2% | National, acute in remote provinces | Medium term (2-4 years) |

| Socio-economic sensitivity to expat outflows | −0.9% | Central and Western expatriate clusters | Short term (≤ 2 years) |

| Limited availability of large urban plots | −0.7% | Riyadh, Jeddah, Dammam metropolitan corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tuition-Fee Caps & Licensing Hurdles

Oversight committees must pre-approve every tuition adjustment, evaluating facility adequacy, teacher-compensation frameworks, and quality metrics before granting raises, thereby constraining agile price resets that reflect inflation or program enhancements. Non-compliance risks a fine of up to SAR 500,000 (USD 133,000), creating financial exposure that particularly burdens smaller proprietors lacking regulatory affairs departments. Further friction arises from multi-layer approvals involving local education directorates, the Technical and Vocational Training Corporation, and, where foreign staff are employed, the Ministry of Human Resources. Capital-light entrants, therefore, confront elongated gestation periods that erode first-mover advantages in newly liberalized districts. Resultant pressure accelerates consolidation, as well-capitalized groups absorb subscale schools seeking shelter from compliance volatility.

Shortage of Qualified Bilingual Teachers

Bilingual educators proficient in international pedagogy remain scarce, particularly for STEM subjects where global demand outstrips supply. Competitive remuneration packages, often including housing allowances, airfare, and child-education subsidies, inflate operating costs, tightening cap-rate spreads on newly built campuses. Government teacher-preparation reforms emphasize digital fluency and student-centred methods, yet training pipelines lag immediate classroom requirements, especially outside major metros. Schools increasingly deploy AI-powered tutor modules and peer-mentorship ladders to mitigate instructor shortages, but adoption curves vary by operator sophistication. Until supply equilibrates, the expansion pace in the KSA private K-12 education market will hinge on creative talent-sourcing alliances with overseas recruitment agencies and domestic scholarship-for-service bonds that lock graduates into multi-year teaching commitments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By School Fees: Less than SAR 15,000 p.a. Hods Dominance

The less than SAR 15,000 p.a. segment of the market was valued at USD 6.95 billion in 2025. It is expected to reach USD 14.19 billion by 2031, registering a growth rate of 12.64% during the forecast period.

The education landscape in Saudi Arabia is undergoing a significant transformation and is poised for rapid growth. Bolstered by substantial investments and a clear governmental focus on educational enhancements, the sector stands on a robust foundation for expansion.

With Vision 2030 advocating for increased private sector participation, the outlook for private education in Saudi Arabia is optimistic. Furthermore, the Tadarruj scheme's new regulations have paved the way for larger private entities to engage in mergers and acquisitions (M&A), especially as smaller players find meeting the latest compliance standards challenging.

Kindergarten and primary school fees in Saudi Arabia typically hover below SAR 15,000 annually.

By Curriculum: British Pre-eminence Confronts American Acceleration

British programs held 32.94% of the KSA private K-12 education market share in 2025, buoyed by historical ties to UK higher-education pathways and a reputation for rigorous assessment regimes. American tracks, expanding at 11.24% CAGR, are narrowing the gap by offering Advanced Placement and dual-enrolment options that appeal to globally mobile families targeting North American universities. Curriculum hybridity has emerged as a strategic lever with operators embedding Saudi history and geography modules to secure licensure while retaining alignment with Cambridge or College Board standards, thus satisfying both regulatory compliance and parental expectations. Fee stratification mirrors curriculum differentiation, as British and American schools command premium tuition brackets that finance expatriate faculty salaries and state-of-the-art STEM labs. Emerging International Baccalaureate programs carve niche positioning, appealing to parents seeking holistic competency frameworks and broad university recognition.

Investment inflows track curriculum demand signals; for instance, British International School Riyadh’s Al Waha campus and Ellesmere College Riyadh exemplify large-format projects that bundle advanced sports complexes with performing-arts theatres to reinforce experiential learning value propositions. American-curriculum entrants leverage partnerships with U.S. universities to inject college-readiness counselling and scholarship pipelines that boost brand cachet. Operators competing on curriculum quality increasingly deploy AI-enabled adaptive assessments to personalize instruction and document mastery, thereby differentiating beyond brand heritage alone. The KSA private K-12 education market size enjoys a lift as curriculum diversity widens the prospective parent base, moving the decision set from binary public-versus-private to a multi-tiered choice architecture defined by global pedagogical benchmarks. Regulatory obliges that all international schools teach Arabic and Islamic studies; seasoned providers integrate these content areas seamlessly, preventing schedule overload and sustaining co-curricular balance.

By Nationality: Saudi Arabia: Vision 2030 Drives National Education Transformation

Expatriate learners filled 72.88% of private-school seats in 2025, but the demographic balance is shifting as Vision 2030 commits to raising the quality and accessibility of nongovernment education for citizens. The Madaris platform identifies 70 investment opportunities aimed at enhancing supply. With private education currently capturing only a limited share of the Kingdom's student population, significant potential for market expansion exists. The 2024 national budget allocates significant resources toward infrastructure development and the integration of digital learning initiatives, including the implementation of mandatory artificial intelligence modules starting from primary education levels. EFG Hermes signalled investor confidence by launching a USD 300 million Saudi Education Fund that acquired a seven-school portfolio focused mainly on Saudi families. Mandatory Arabic and Islamic studies classes continue to safeguard cultural alignment across British, American, and IB pathways.

Saudi students are forecast to grow at a 13.74% CAGR through 2031, the steepest rise in the Gulf, as public policy removes foreign ownership caps and accelerates school licensing. Sharia-compliant sukuk structures are widening the investor base, bringing pension funds and Islamic banks into campus development projects. Parallel mega-projects such as NEOM and ROSHN sustain expatriate inflows, ensuring that dual-segment demand continues even as local participation rises. Collectively, these moves position Saudi Arabia as a diversified and sustainable private-education market.

Geography Analysis

The Central region accounted for 36.12% of the KSA private K-12 education market size in 2025, anchored by Riyadh’s concentration of governmental bodies, multinational headquarters, and higher-income households. Location advantages, such as proximity to embassies and the new King Salman Park district, enable schools to command premium fees while maintaining high occupancy rates driven by expatriate professionals. The educational landscape in the western region benefits from Jeddah's strategic trade connectivity and Makkah's religious prominence. This advantage is further strengthened by 179 government-supported educational initiatives, implemented through PPP structures, aimed at increasing student capacity . Eastern corridors around Dammam and Khobar derive stability from oil-sector employment, attracting investors like Al-Khalej Training and Education Company, which opened a new international complex in 2025. Land scarcity inside Tier-1 metros incentivizes vertical campus designs and pushes greenfield development toward suburban plots along emerging public transit lines.

Northern provinces deliver the fastest 7.08% CAGR by 2031 as Vision 2030 pivots toward balanced development that de-concentrates economic activity away from legacy hubs. NEOM and ancillary mega-projects fuel population inflows of skilled workers who demand high-quality schooling, thereby creating blue-ocean territory for first-mover operators with modular campus solutions. Competitive intensity is lower than in the Central and Western regions, offering healthier pricing power and room for differentiated curriculum positioning. Southern locales remain constrained by rugged topography and lower household incomes, yet government infrastructure upgrades could spark latent demand beyond the forecast window. Regionally nuanced go-to-market strategies, covering land acquisition models, teacher recruitment pipelines, and transportation logistics, determine success rates inside the geographically diverse KSA private K-12 education market.

Competitive Landscape

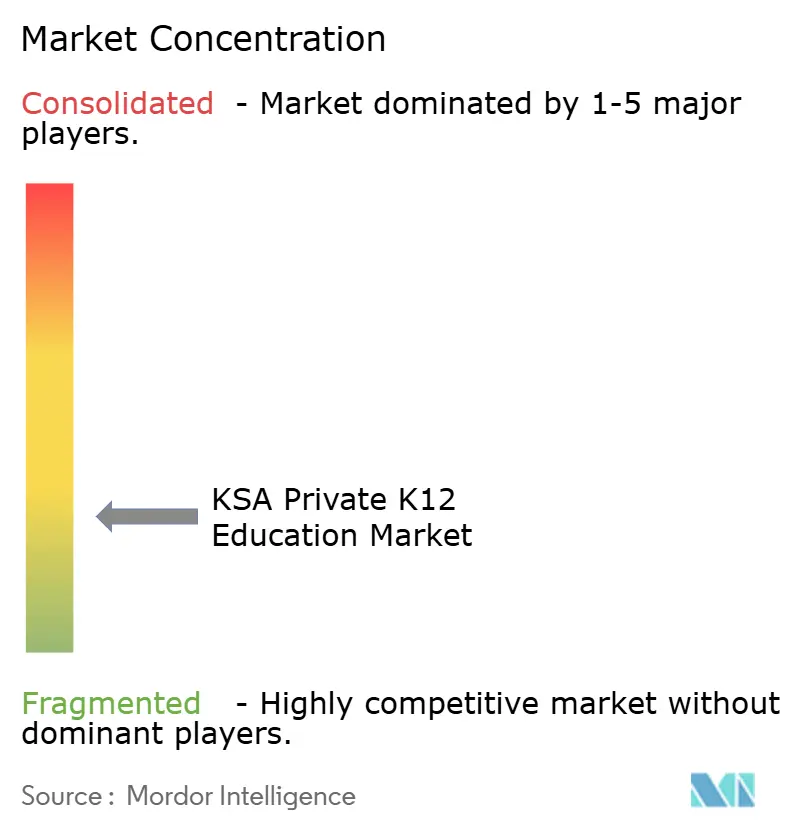

Fragmentation defines the KSA private K-12 education market, where the top five operators held less than one-fourth of 2024 revenues, translating to a market concentration score of 3 and leaving expansive headroom for acquisition-driven scale building. Maarif Education, operating as a consolidator, utilized capital pools to acquire Ibn Khaldoun Education Company. This acquisition has driven total enrolment figures to exceed a notable benchmark, reflecting a strategic focus on regional roll-ups aimed at achieving procurement efficiencies and fostering brand integration. EFG Hermes’ USD 300 million Saudi Education Fund exemplifies the influx of institutional finance chasing predictable tuition cash flows tied to demographic fundamentals; its purchase of the Britus Education portfolio positions the fund as a rising multi-geography contender. Technology partnerships illustrate another axis of rivalry, as evidenced by McGraw-Hill’s exclusive content deal with Maarif integrates adaptive learning engines across ten campuses, raising the performance bar that peers must match to remain competitive [4]McGraw Hill, “McGraw Hill, Maarif Education forge exclusive partnership to boost hybrid learning,” McGrawHill.com .

Emerging disruptors diversify the field by deploying virtual-school models and AI-centric pedagogy, evidenced by Ataa Educational’s memorandum with Semanoor to launch the Kingdom’s first fully online K-12 platform. Such innovations cater to transient expatriate families and gifted Saudi students seeking accelerated pathways without geographical tethering, thereby adding elasticity to the KSA private K-12 education market size. Mid-tier local operators differentiate via niche value propositions such as STEAM labs, bilingual theatre programs, or faith-integrated leadership curricula that capture specific parent segments unwilling to pay premium international fees yet demanding higher quality than legacy Arabic-only schools. Regulatory scrutiny over tuition caps and facility specifications functions as both hurdle and moat: while compliance demands lift cost bases, adept players transform adherence into marketing proof of quality assurance.

Geographic expansion remains a salient competitive tactic; chains that entered early into Northern and Eastern regions enjoy first-mover advantage as those corridors ramp economic output and resident affluence. Vertical integration across kindergarten to secondary stages smooths enrolment funnels and magnifies lifetime revenue per family, enabling aggressive scholarship campaigns that attract high-performing students who elevate standardized-test league tables. EdTech ecosystems continue to reshape instructional design, and partnerships with research institutions like KAUST feed continuous innovation loops that smaller schools struggle to replicate. Despite heightened rivalry in mature districts, the overall KSA private K-12 education market continues to deliver double-digit growth, preserving space for both scale-seekers and specialized boutiques to flourish under Vision 2030’s pro-private stance.

KSA Private K-12 Education Industry Leaders

Ataa Educational Company

Ma’arif for Education & Training

GEMS Education KSA

Al-Khaleej Training & Education (Ajyal)

Al-Rowad International Schools

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Spark Education Platform has acquired a controlling interest in Qimam El Hayat International School, located in Riyadh. This acquisition has enabled the school to expand its capacity substantially by transitioning to a larger campus.

- November 2024: Maarif Education completed the takeover of Ibn Khaldoun Education Company, creating the Kingdom’s largest K-12 operator with enrolment exceeding 36,000 students.

- November 2024: EFG Hermes launched a USD 300 million Saudi Education Fund and simultaneously acquired the Britus Education portfolio of seven GCC schools with 12,000 seats, signaling an aggressive roll-up strategy in the region.

- August 2024: Ataa Educational opened Buckswood School Riyadh and shifted Al Wasat National School to a new complex, raising total capacity from 1,400 to 2,590 seats and introducing British curriculum with IB options.

KSA Private K-12 Education Market Report Scope

The Ministry of Education is responsible for overseeing the Saudi Arabian K-12 educational system. Public schools typically teach more religious subjects than private institutions. Additionally, there are several international schools, particularly for foreigners.

The KSA Private K12 Education Market is segmented Segmented By School Fees (Less Than Sar 15000 P.A., Sar 15,000 To 30,000 P.A., Sar 30,000 To 80,000 P.A., and Above Sar 80,000 P.A.), By Curriculum (American, British, Arabic, CBSE, and Other curriculum), and By Region (Riyadh, Jeddah, Eastern Province, and Other Regions). The report offers market size and forecasts for KSA Private K12 Education Market in value (USD Million) for all the above segments.

| Less Than SAR 15,000 P.A. |

| SAR 15,000 to 30,000 P.A. |

| SAR 30,000 to 80,000 P.A. |

| Above SAR 80,000 P.A. |

| American |

| British |

| Arabic |

| CBSE |

| Other Curriculum |

| Expat Students |

| Local Students |

| Riyadh |

| Jeddah |

| Eastern Province |

| Other Region |

| By School Fees | Less Than SAR 15,000 P.A. |

| SAR 15,000 to 30,000 P.A. | |

| SAR 30,000 to 80,000 P.A. | |

| Above SAR 80,000 P.A. | |

| By Curriculum | American |

| British | |

| Arabic | |

| CBSE | |

| Other Curriculum | |

| By Nationality | Expat Students |

| Local Students | |

| By Region (KSA) | Riyadh |

| Jeddah | |

| Eastern Province | |

| Other Region |

Key Questions Answered in the Report

How large is the KSA private K-12 education market in 2026?

The KSA Private K-12 Education Market is valued at USD 9.94 billion in 2026 and is on track to reach USD 15.45 billion by 2031.

What is driving enrolment growth in Saudi private schools?

Demographic expansion, Vision 2030 human-capital targets, mandatory kindergarten, and rising demand for international curricula collectively sustain double-digit enrolment growth.

Which curriculum holds the largest share among Saudi private schools?

British programs lead with a 32.94% share in 2025, although American tracks are growing fastest at 11.24% CAGR.

Why are PPP models important for school construction?

PPPs reduce sovereign capital burdens while granting operators secure 20-year contracts, delivering predictable cash flows that attract institutional investors.

How fragmented is the competitive field?

The top five operators control less than one-fourth of revenues, signalling ample room for mergers, acquisitions, and greenfield expansion.

What role does AI play in Saudi classrooms?

Government-backed funding and university partnerships are accelerating adoption of adaptive learning platforms, improving test scores and addressing teacher shortages.

Page last updated on: