E-learning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

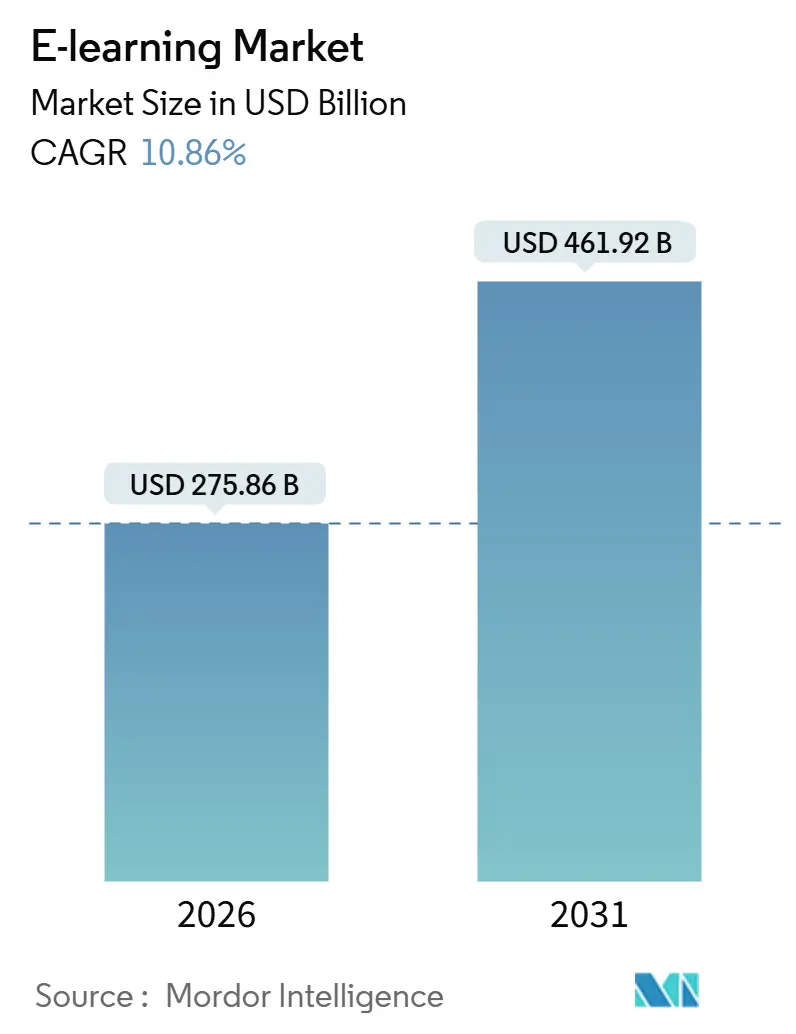

| Market Size (2026) | USD 275.86 Billion |

| Market Size (2031) | USD 461.92 Billion |

| Growth Rate (2026 - 2031) | 10.86% CAGR |

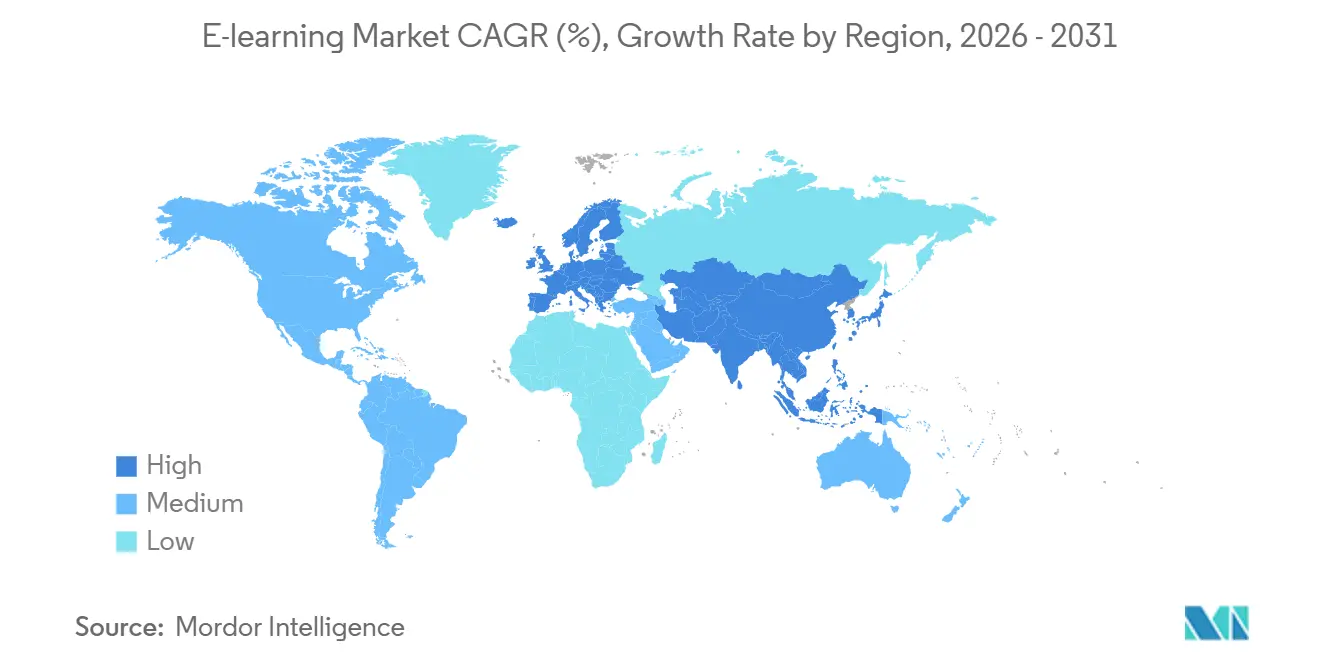

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

E-learning Market Analysis by Mordor Intelligence

The global e-learning market size is projected to grow from USD 275.86 billion in 2026 to USD 461.92 billion by 2031, reflecting a robust compound annual growth rate (CAGR) of 10.86% over the five years. This expansion is fueled by organizations leveraging skills intelligence to align learning with job roles, with 61% of corporate L&D professionals identifying skill gap closure as their top training goal, according to Exploding Topics data cited in Continu’s 2025 corporate eLearning statistics report. Academic institutions are increasingly formalizing micro-credentials to address employability gaps, supported by UNESCO IESALC findings that 81% of executives believe these credentials ease hiring decisions. Among youth aged 18–24, smartphone penetration has reached 98%, enabling widespread mobile access to learning platforms. In the United States, over half of students now enroll in at least one online course, spanning both K–12 and higher education. Public-sector mandates and privacy frameworks, such as GDPR and institutional data protection policies, continue to shape platform design and compliance standards across nearly all e-learning programs.

Key Report Takeaways

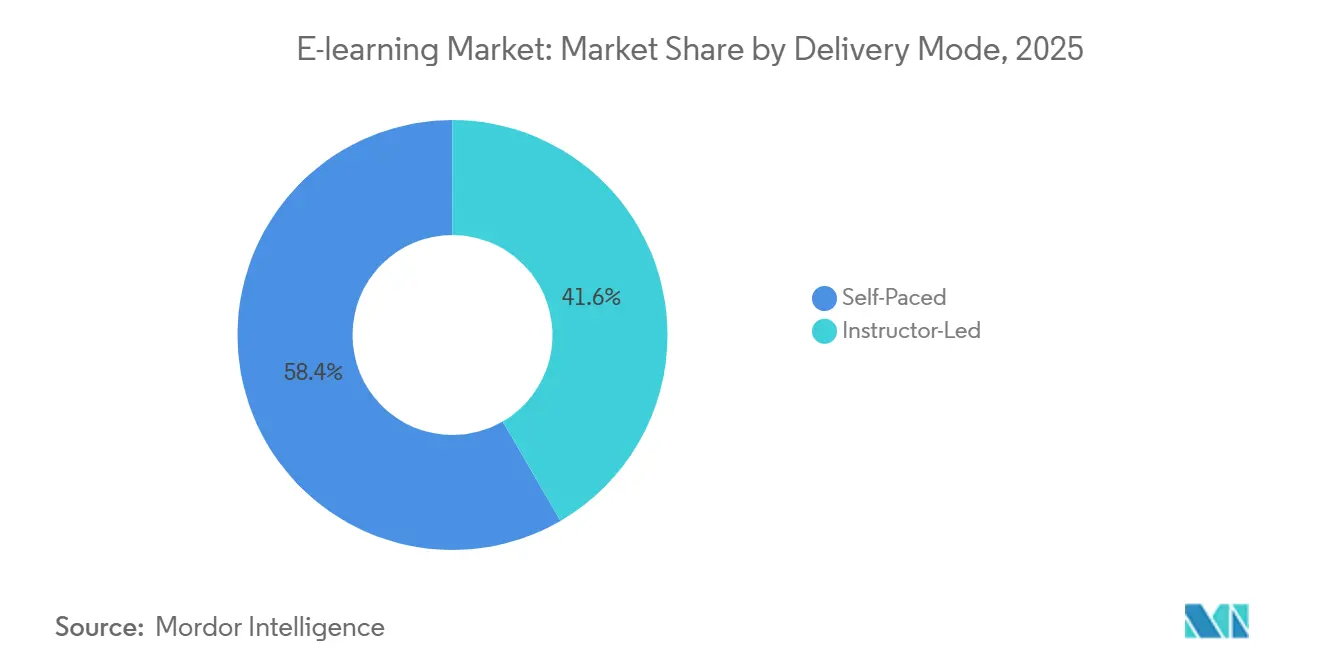

- By delivery mode, self-paced formats led with 58.37% of the e-learning market share in 2025, while instructor-led offerings are forecast to expand at a 12.76% CAGR through 2031.

- By deployment, cloud-based delivery held 54.37% of the e learning market share in 2025 and is forecast to grow at an 11.77% CAGR through 2031.

- By technology, online e-learning retained a 43.39% of the e-learning market share in 2025, while mobile e-learning is projected to record the highest growth at a 15.73% CAGR through 2031.

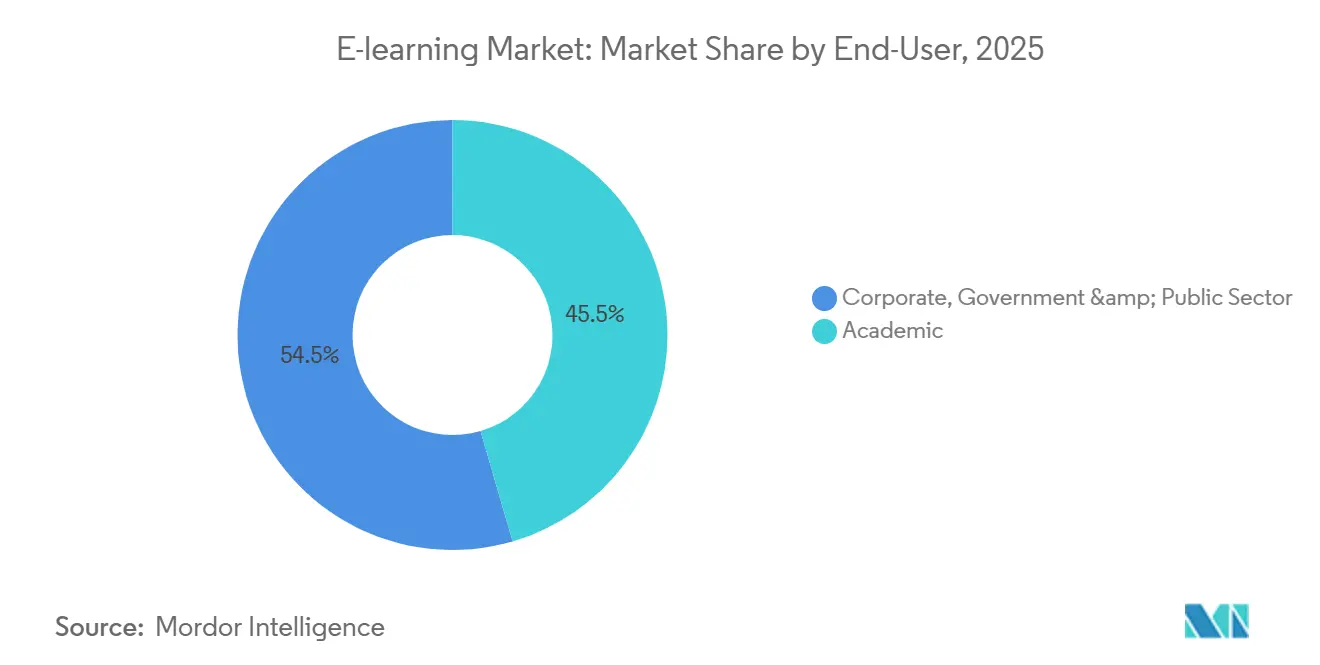

- By end-user, academic institutions accounted for 45.48% of the e-learning market share in 2025, while the corporate segment is projected to grow at a 10.38% CAGR through 2031.

- By geography, North America held 34.74% of the e learning market share in 2025, while Asia-Pacific is forecast to grow at an 8.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global E-learning Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing penetration of smartphones & high-speed internet | +2.3% | Global, strongest in Asia-Pacific, and rural North America | Short term (≤ 2 years) |

| Corporate up-skilling demand amid digital transformation | +3.1% | North America, Europe, Asia-Pacific core | Medium term (2-4 years) |

| Government initiatives for digital education | +1.8% | Europe, India, Canada, the Middle East | Long term (≥ 4 years) |

| Cost advantages over classroom training | +1.5% | Global, particularly emerging markets | Short term (≤ 2 years) |

| Rise of micro-credential partnerships between universities & Big Tech | +1.6% | North America, Europe, and early adopters in the Asia-Pacific | Medium term (2-4 years) |

| EdTech venture funding shifts toward emerging markets | +0.8% | South America, Southeast Asia, and MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Penetration of Smartphones and High-Speed Internet

Mobile access and better connectivity are reshaping how people engage with online learning and skills development. According to OECD PISA 2022 data, 98% of 15-year-olds across OECD countries own a smartphone, and 96% have access to a desktop, laptop, or tablet at home, lowering barriers to video lessons, tutoring, and coursework outside school hours. At the same time, 79 education systems worldwide, representing 40% of global systems, have implemented smartphone restrictions or bans in classrooms by the end of 2024 to protect attention and learning outcomes, per UNESCO monitoring, while permitting after-school use for homework and supplemental learning [1]UNESCO, “Smartphones in School: Only When They Clearly Support Learning,” UNESCO, unesco.org. The coexistence of classroom restrictions and strong out-of-school mobile use pushes providers to invest in features like offline modes, low-bandwidth formats, and content that fits short sessions. This environment helps the e-learning market extend reach among learners who have smartphones but inconsistent broadband, especially in rural districts and emerging markets where mobile-first strategies carry the most impact.

Corporate Up-Skilling Demand Amid Digital Transformation

Labor markets in 2026 prioritize speed-to-skill, making structured, outcomes-based programs central to enterprise learning roadmaps. A survey conducted by edX in 2025 found that most working-age adults considering training intended to act within months, pointing to concrete timelines that learning leaders must meet with scalable programs that align with job requirements. Public education systems are shifting to formalize AI literacy and practice through required professional learning days and resources that guide safe, effective classroom use. For instance, Ontario’s Ministry of Education mandated AI as a topic for Professional Activity Days in 2025-26, requiring educators to discuss AI’s role in teaching, explore approved tools for writing and critical thinking, and align with the Ontario Trustworthy AI Framework and cybersecurity policies[2]Government of Ontario, “Mandatory Professional Activity Days for 2025–26,” Ontario Ministry of Education, ontario.ca. National strategies to address digital talent gaps in the public sector are driving evergreen training plans with explicit AI components, such as the UK Cabinet Office’s One Big Thing 2025 initiative, which will train all civil servants on AI essentials, practical applications for streamlining work, and innovation in public services starting in autumn 2025. These efforts expand addressable demand for platforms that deliver role-aligned learning at government scale.

Government Initiatives for Digital Education

Policy is organizing a durable foundation for digital teaching and learning, from connectivity and devices to digital pedagogy and safe technology use. In the European Union, the Digital Education Action Plan for 2021-2027 focuses on building resilient learning systems, closing readiness gaps for educators, and setting shared goals for digital capacity, which improves certainty for institutions procuring platforms and content. Complementing this, UNESCO and UNICEF advanced a Charter for Public Digital Learning Platforms to guide government decision-making on public-interest platforms, interoperability, and trusted governance, which sets expectations for openness, inclusion, and long-term support. National programs to build digital and AI skills across civil services are formalizing curricula, training pathways, and operating models for continuous learning, giving platforms clear frameworks to address public-sector needs.

Cost Advantages Over Classroom Training

Organizations adopt e-learning to reduce delivery costs at scale, with studies showing 50-70% savings compared to classroom training by eliminating travel, venues, and instructor fees, such as Dow Chemicals cutting per-learner costs from USD 95 to USD 11. This standardizes quality and accelerates update cycles, as e-learning requires 40-60% less time than in-person sessions while boosting retention by 25-60%. Enterprise subscription models and skills pathways offered by leading platforms illustrate how buyers translate these efficiencies into continuous programs that map to job roles and certifications across large user bases. Vendors are embedding AI tutors, coaching, and practice simulations to raise engagement and improve completion without increasing live-instructor hours, which helps balance outcomes and budget in sustained programs. As evidence builds across enterprise deployments, the e-learning market continues to monetize the scalability and time-to-value advantages of digital delivery, especially in distributed workforces and regulated sectors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low completion rates & learner-engagement challenges | -1.4% | Global, particularly acute in self-paced MOOCs | Medium term (2-4 years) |

| Digital divide in rural & low-income areas | -1.2% | Rural United States, Sub-Saharan Africa, rural Asia-Pacific, South America | Long term (≥ 4 years) |

| Content-localization barriers for multilingual markets | -0.6% | Emerging markets with linguistic diversity (India, MEA, South America) | Medium term (2-4 years) |

| Data-privacy regulatory complexity | -0.7% | Europe (GDPR), India (DPDP Rules), California (CPRA) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Low Completion Rates and Learner-Engagement Challenges

Completion remains the most persistent challenge for at-scale online formats, especially in programs built entirely around self-paced experiences. Many providers counter this with live touchpoints, coaching, and social learning features designed to sustain motivation and reinforce accountability through milestones. Across formal education, comparative completion data illustrate how many students require more time than the theoretical duration of their programs, which points to structural and support needs that also apply to online programs. The e-learning market is responding with AI tutors, progress dashboards, and practice environments that shorten feedback loops and help learners build momentum with targeted assistance. Enterprise implementations also leverage manager enablement and projects tied to job outcomes, which can improve persistence by linking coursework to near-term performance goals. As expectations around demonstrable outcomes grow, providers continue to invest in engagement mechanics that make completion more likely at scale.

Digital Divide in Rural and Low-Income Areas

Access disparities limit the addressable base for online learning in regions where fixed or mobile broadband speeds lag, even as device access improves. OECD data reveals persistent gaps, with fixed broadband speeds in metropolitan areas 44% higher than in remote regions in 2024, widening from 22 Mbps to 58 Mbps between 2019-2024, and mobile speeds 37% faster in cities (74.5 Mbps) versus rural areas (54.3 Mbps). Global monitoring shows over 20% of primary schools lack electricity, drinking water, or sanitation, with more than half missing electricity and two-thirds without digital tools in the least developed countries, restricting digital content integration. Studies of unlimited data plans suggest these offerings can meaningfully expand access to education content in low-income and rural households by removing marginal cost constraints on data usage. Meanwhile, potential shifts in telecom funding mechanisms can introduce uncertainty for subsidized connectivity and community anchor institutions that serve learners in underserved areas. The e-learning market continues to adapt with offline modes, low-bandwidth design, and asynchronous formats to keep learning accessible where connectivity remains inconsistent.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Delivery Mode: Instructor-Led Momentum Builds Alongside Self-Paced Dominance

Self-paced learning accounts for 58.37% of the market in 2025, reflecting a strong preference for flexible, on-demand access that supports self-directed practice. Instructor-led formats are projected to grow at a 12.76% CAGR through 2031, driven by enterprises blending live coaching with asynchronous content to enhance confidence and completion rates. Managers increasingly request role-specific simulations, such as Udemy's October 2025 AI Role Play launch with over 10,000 simulations tied to certifications and feedback sessions, reducing performance risks. Platforms integrating AI assistance achieve 76% efficiency gains, as per Didask benchmarks, complementing instructor time and scaling live support across languages for large learner groups.

Corporate and public-sector buyers are formalizing AI up-skilling and digital literacy requirements, using live sessions to align teams with responsible practices and organizational frameworks. This shift strengthens hybrid designs, where instructor-led touchpoints introduce tools, assess readiness, and standardize workflows, while asynchronous content addresses knowledge gaps. Over the forecast period, the e-learning industry is expected to sustain both modes as complementary channels serving distinct objectives. Live formats will remain essential for onboarding, leadership, and soft skills, while self-paced modules will anchor knowledge acquisition and practice.

By Deployment: Cloud Infrastructure Captures and Sustains Leadership

Cloud-based deployment, holding 54.37% of the base in 2025, is projected to grow at an 11.77% CAGR through 2031. Enterprises favor faster updates, elastic capacity, and multi-tenant architecture for simplified administration. The e-learning market supports this shift by focusing on security, regional hosting, and compliance integrations for regulated industries. Cloud platforms enable features like AI coaching and analytics without on-premises maintenance, ensuring continuous improvement and uptime for global users. Subscription models illustrate how enterprises scale across teams and geographies while reducing costs and consolidating vendors. As institutions standardize on fewer platforms, cloud-first strategies enhance speed and lower the total cost of ownership compared to on-premises solutions.

On-premises implementations will remain in defense and sensitive environments requiring network isolation. However, the e-learning market increasingly prioritizes cloud features. Product roadmaps emphasize privacy controls, consent management, and accessibility to meet institutional and student protection requirements, boosting confidence in hosted solutions. Cloud-native analytics link course activity to skill signals and credentials, proving outcomes and supporting career mobility. Procurement frameworks focusing on data protection and AI transparency favor cloud platforms with certifications and regional coverage. These factors position cloud deployment as the foundation of the e-learning industry through 2031.

By Technology: Mobile E-Learning Sprints Ahead as AI Refactors Online Platforms

Online e-learning held a 43.39% share in 2025, highlighting the importance of web-based courses, virtual classrooms, and recorded lectures. Mobile e-learning is projected to grow at a 15.73% CAGR through 2031, driven by widespread youth smartphone access in developed economies and increasing availability in emerging markets. Providers design mobile experiences for short sessions and offline use, with micro-learning improving retention by 20% over traditional methods. Coursera's October 2025 partnership with Anthropic expands AI-driven content for soft skills training, integrating simulated practice into mobile platforms to support credential progress. This shift aligns with user preferences for bite-sized modules and continuous skill updates across job roles.

Virtual classrooms, learning management systems, and rapid authoring tools enable real-time instruction, compliance reporting, and faster course creation by experts. The mobile e-learning market benefits from device penetration and platform features that encourage participation. Policies limiting smartphone use during class hours create a split, with mobile learning thriving outside K-12 settings and gaining traction in higher education and enterprises. Combining mobile, web, and live instruction ensures flexibility and supports outcomes. AI tools across web and mobile are expected to refine content discovery, personalize practice, and streamline credentialing, deepening engagement in the e-learning market.

By End-User: Corporate Acceleration Complements a Mature Academic Base

Academic institutions accounted for 45.48% of the e-learning market in 2025, reflecting the sustained adoption of digital learning in K-12, higher education, and vocational training. The corporate segment is projected to grow at a 10.38% CAGR through 2031, driven by employers formalizing AI and data skills pathways that link learning to productivity and talent mobility. Leading platforms report that organizations are scaling role-aligned learning through subscriptions and structured journeys. High-demand skills like generative AI, cybersecurity, and data analysis dominate enrollments, supporting recurring investments in content and assessments aligned with job outcomes. These trends position the e-learning market to address both institutional curricula and workforce transformation at scale.

Public-sector buyers are codifying AI-readiness and digital literacy, increasing demand for platforms that meet data-protection standards and offer content mapped to civil-service roles. Academic systems align professional development and student experiences with responsible AI frameworks, using virtual learning environments and ministry resources to guide adoption. While academic institutions will maintain a significant market share, corporate demand is growing faster due to job-change velocity and shorter planning cycles. Providers integrating with human capital and student information systems will gain preference by reducing operational friction. As cross-sector needs converge on outcomes, evidence, and credential portability, the e-learning market will diversify its revenue streams.

Geography Analysis

North America held a 34.74% market share in 2025, supported by a strong ecosystem of platforms, content partners, and enterprise buyers sustaining digital learning post-pandemic. Institutional and government actions in 2026 are reinforcing digital literacy and responsible AI practices in schools and public services, driving long-term adoption. United States and Canadian initiatives to build AI-ready workforces are increasing demand for certifications, structured learning pathways, and compliance-ready vendors. Private-sector buyers are expanding subscriptions and role-based learning programs integrated with enterprise systems, committing to multi-year digital training. Rural connectivity gaps and potential telecom funding shifts create uncertainties for subsidized broadband, affecting community institutions. Growth in this mature market is tied to AI-native features, micro-credentials, and evidence.

Europe continues implementing the EU Digital Education Action Plan in 2026, advancing educator readiness, system resilience, and digital transformation goals in schools and higher education. Policies addressing digital skills and teacher support bridge readiness gaps and secure multi-year budgets for infrastructure, content, and platforms across member states. Procurement prioritizes privacy, safety, and accessibility, favoring platforms compliant with EU frameworks and national guidelines. Multilingual content and localization influence adoption across diverse language communities. As hybrid models and learning analytics become embedded, steady procurement cycles and cross-border partnerships align credentials with labor market needs. AI literacy and responsible use strengthen the case for AI-native platforms in higher education and enterprise contexts.

Asia-Pacific is projected to grow at an 8.87% CAGR through 2031, driven by internet access gains, mobile-first learning behavior, and policy pushes for digital skills in schools and workplaces. Governments and employers are investing in AI and data capability programs, expanding demand for role-aligned courses and professional certificates. Mobile access and offline capabilities shape product choices in rural and peri-urban areas. Privacy and safety mandates guide platform design, while partnerships with universities and large employers anchor market strategies.

Competitive Landscape

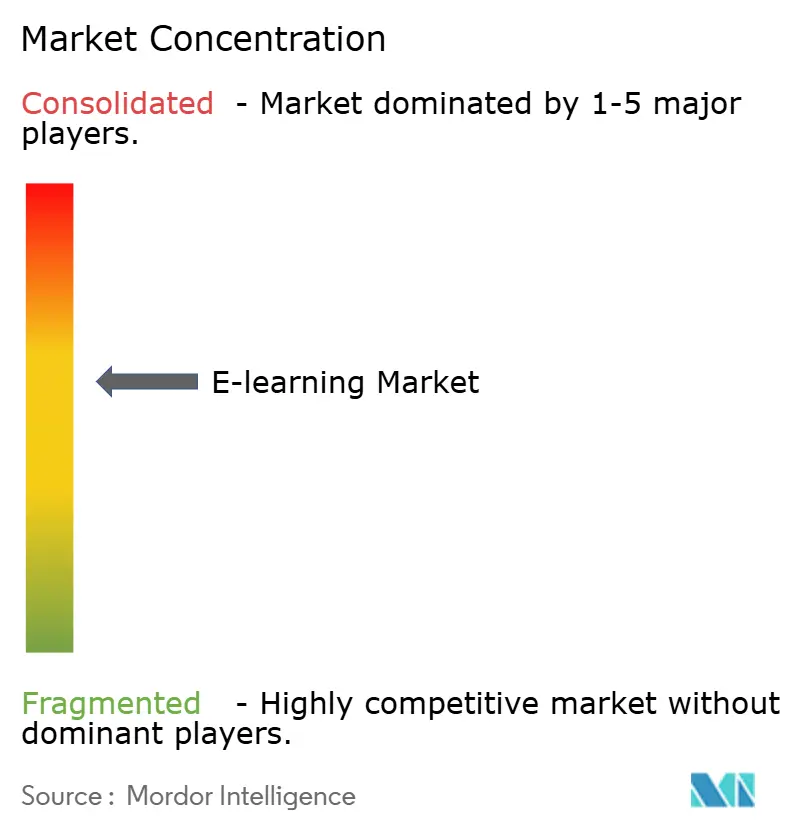

The e-learning market remains moderately fragmented, with scaled platforms and specialized providers addressing diverse domains, languages, and enterprise needs. In December 2025, Coursera and Udemy announced plans to merge, pending regulatory and shareholder approvals. This merger aims to unify learner communities, enterprise customer bases, and course catalogs, focusing on AI-driven features, skills intelligence, and efficient market engagement with universities and employers. Integration with AI assistants and apps has enhanced content discovery and engagement, creating new acquisition channels and cross-platform learning experiences. Platforms connecting learning to credentials, hiring signals, and measurable workforce outcomes at scale gain a competitive edge.

In the enterprise sector, vendors compete through personalization, role-specific journeys, and embedded practices that validate skills. Udemy emphasizes simulations and certification-aligned journey designs, reporting improved learner conversion and monetization within enterprise groups. Skillsoft launched an AI-driven platform and is reviewing its instructor-led training business, signaling a shift toward scalable digital experiences and university-led content partnerships. Platforms integrating with human capital systems, offering job-role analytics, and updating content to meet evolving tools and compliance needs are favored. With enterprise learning budgets prioritizing AI and cybersecurity, providers demonstrating measurable outcomes and faster competency timelines are poised to gain market share.

Degree and executive education models are evolving due to challenges faced by legacy operators. In 2025, 2U realigned its operations and portfolio, reflecting an industry-wide focus on capital efficiency, product-market fit, and outcome validation[3]edX, “Economic Pressures Propel Workers Towards Upskilling: 2025 Survey,” edX, edx.org. University-industry partnerships are driving micro-credentials and enterprise pathways, linking learners to recognized credentials and in-demand roles, enhancing platform relevance in corporate and academic contexts. Regulatory and privacy frameworks influence vendor selection, promoting security, accessibility, and trustworthy AI features aligned with institutional risk standards. These factors sustain competitive intensity while encouraging consolidation and specialization in the e-learning market.

E-learning Industry Leaders

Coursera Inc.

Udemy Inc.

LinkedIn Learning

edX (2U Inc.)

Skillsoft

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Coursera and Udemy announced an all-stock merger expected to close by the second half of 2026, creating a combined entity with over USD 1.5 billion in pro forma annual revenue, 273 million registered learners, and 15,000-plus enterprise customers, with an implied equity value of approximately USD 2.5 billion and expected USD 115 million in annual run-rate cost collaboration within 24 months.

- December 2025: Skillsoft announced a strategic review of its Global Knowledge segment and launched the next-generation Percipio Platform, positioned as an AI-native skills intelligence platform, while signing initial enterprise customers for the new offering.

- May 2025: Udemy launched AI Role Play with more than 10,000 simulations, introduced Career Journeys, and reported improved subscription conversion through partnerships, including certification pathways with Pearson.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global eLearning market as every paid digital learning service or content license that is delivered over public or private internet networks to academic institutions, corporate learners, and government bodies, including self-paced modules, instructor-led virtual classes, mobile micro-learning, learning management system access, and assessment engines, all valued in USD at end-user spend.

Scope exclusion: hardware devices, stand-alone conferencing tools, and informal open-video tutorials lie outside this valuation.

Segmentation Overview

- By Delivery Mode

- Self-Paced

- Instructor-Led

- By Deployment

- Cloud

- On-Premise

- By Technology

- Online e-learning

- Learning Management System (LMS)

- Mobile e-learning

- Rapid e-learning

- Virtual Classroom

- By End-User

- Academic

- Corporate

- Government & Public Sector

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- Rest of Asia-Pacific

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East & Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Discussions with platform executives, LMS architects, university digital officers, and learning and development heads across North America, Europe, Asia-Pacific, the Gulf, and Latin America validate pricing ladders, completion rates, and regional content preferences that secondary material only hints at. The interviews also refine our forecast drivers and vet early model outputs.

Desk Research

Mordor analysts first compile supply and demand cues from tier-1 open datasets such as the UNESCO Institute for Statistics, International Telecommunication Union, OECD Education at a Glance, the U.S. National Center for Education Statistics, and regional telecom regulators.

Company 10-Ks, investor decks, patent abstracts, and education ministry tenders round out adoption signals.

Subscription resources, including Dow Jones Factiva for news flow and D&B Hoovers for provider revenues, help chart competitive footprints.

These sources anchor baseline enrollment pools, connectivity levels, and average digital course pricing; many additional references were consulted beyond the illustrative list above.

Market-Sizing and Forecasting

A top-down spend per learner build starts with formal enrollment numbers and corporate headcount pools, which are then multiplied by verified penetration rates and average subscription fees.

Results are cross-checked through selective bottom-up samples of leading vendor revenues and channel checks to tune anomalies.

Key variables include smartphone penetration, broadband subscriptions, corporate HR tech spend per employee, course completion ratios, and annual license price shifts.

Multivariate regression, supported by scenario overlays, extends the series to 2030 while allowing sensitivity tests around economic growth and policy shifts.

Gaps in bottom-up data are bridged using regional analogs approved by our subject experts.

Data Validation and Update Cycle

Every model passes a multi-step peer review; anomaly dashboards flag outliers, and senior reviewers sign off only after reconciling variances with fresh news and filings.

We refresh each dataset annually and trigger interim updates when policy, M&A, or technology shocks materially sway market fundamentals.

Why Mordor's Global E-Learning Revenue Baseline Commands Reliability

Published estimates often diverge because firms pick different service mixes, price anchors, and refresh rhythms.

Key gap drivers include the inclusion of hardware or pure content bundles by some publishers, conservative ASP progressions by others, and infrequent primary validation.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 248.84 B (2025) | Mordor Intelligence | |

| USD 366 B (2025) | Global Consultancy A | Counts corporate training services and niche hardware, relies on single-step top-down model |

| USD 352.59 B (2025) | Industry Analyst B | Uses historical exchange rates without inflation parity, limited primary interviews |

| USD 342.4 B (2024) | Trade Journal C | Older base year and quarterly news extrapolation instead of structured demand variables |

The comparison shows that, by selecting a well-defined service scope, updating inputs yearly, and blending model approaches, Mordor's figures present a balanced, traceable baseline that decision-makers can reproduce with publicly available facts and minimal assumptions.

Key Questions Answered in the Report

What is the global e-learning market size and growth outlook to 2031?

The e-learning market size is USD 275.86 billion in 2026 and is projected to reach USD 461.92 billion by 2031 at a 10.86% CAGR.

Which delivery mode is growing fastest in the e-learning market through 2031?

Instructor-led formats are forecast to grow at a 12.76% CAGR, even as self-paced learning remains the largest mode by 2025 share.

What technologies are leading adoption in the e-learning market?

Online e-learning holds the largest 2025 share, while mobile e-learning is projected to grow the fastest at a 15.73% CAGR, thanks to mobile-first behavior and better connectivity.

How is cloud deployment influencing the e-learning market?

Cloud-based delivery held a 54.37% share in 2025 and is expected to grow at an 11.77% CAGR, driven by faster updates, integration, and lower overhead at scale.

Which regions are expected to lead growth in the e-learning market to 2031?

North America held the largest 2025 share, while Asia-Pacific is projected to post the fastest growth with an 8.87% CAGR through 2031.

How are enterprises shaping demand in the e-learning market?

Employers are prioritizing role-aligned learning and micro-credentials, which is why the corporate segment is projected to grow at a 10.38% CAGR, and vendors emphasize AI-native, skills-based pathways.

Page last updated on: