Vegan Cookies Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

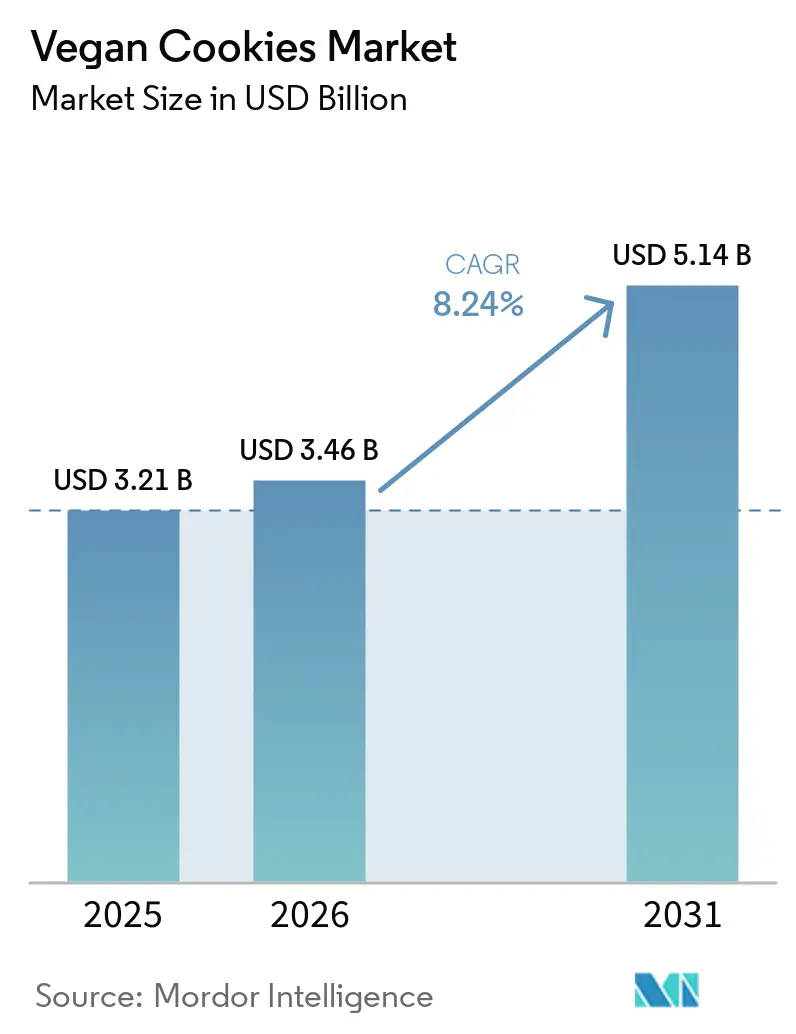

| Market Size (2026) | USD 3.46 Billion |

| Market Size (2031) | USD 5.14 Billion |

| Growth Rate (2026 - 2031) | 8.24% CAGR |

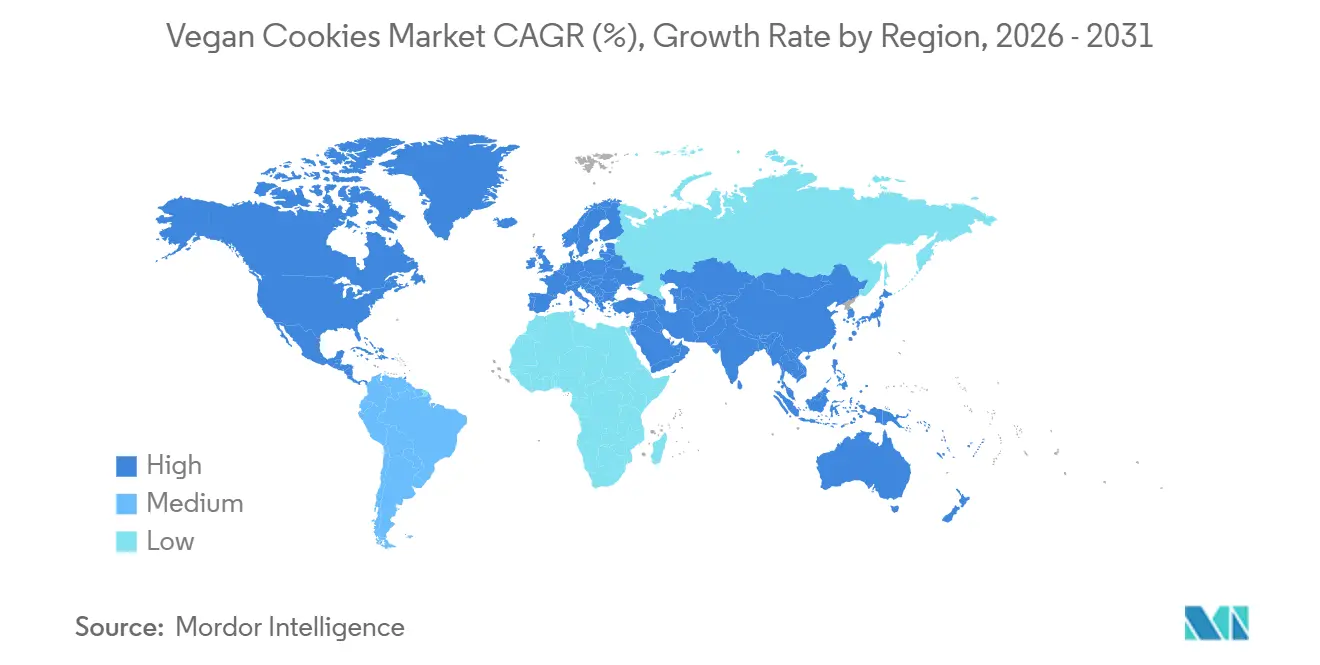

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vegan Cookies Market Analysis by Mordor Intelligence

The vegan cookies market size is expected to grow from USD 3.21 billion in 2025 to USD 3.46 billion in 2026 and is forecast to reach USD 5.14 billion by 2031 at 8.24% CAGR over 2026-2031. Consumers' growing health consciousness, environmental advocacy, and consistent investor focus on alternative proteins are driving this growth trajectory. Furthermore, packaging policies increasingly favoring recyclables are accelerating this trend. Companies are introducing innovations such as protein-rich nuts, precision-fermented fats, and eco-friendly single-serve packs to improve the taste, texture, and shelf life of cookies. Brand owners actively leverage AI-driven formulations and implement transparent supply chains to strengthen consumer trust. Flexitarian consumers are expanding the market's reach, prompting retailers to enhance their omnichannel strategies and position plant-based snacks as mainstream options. Regulatory changes, particularly the EU's mandate requiring 65% recycled content in plastic packaging by 2040, are actively supporting market growth while encouraging sustainable packaging innovations that align with the preferences of vegan consumers.

Key Report Takeaways

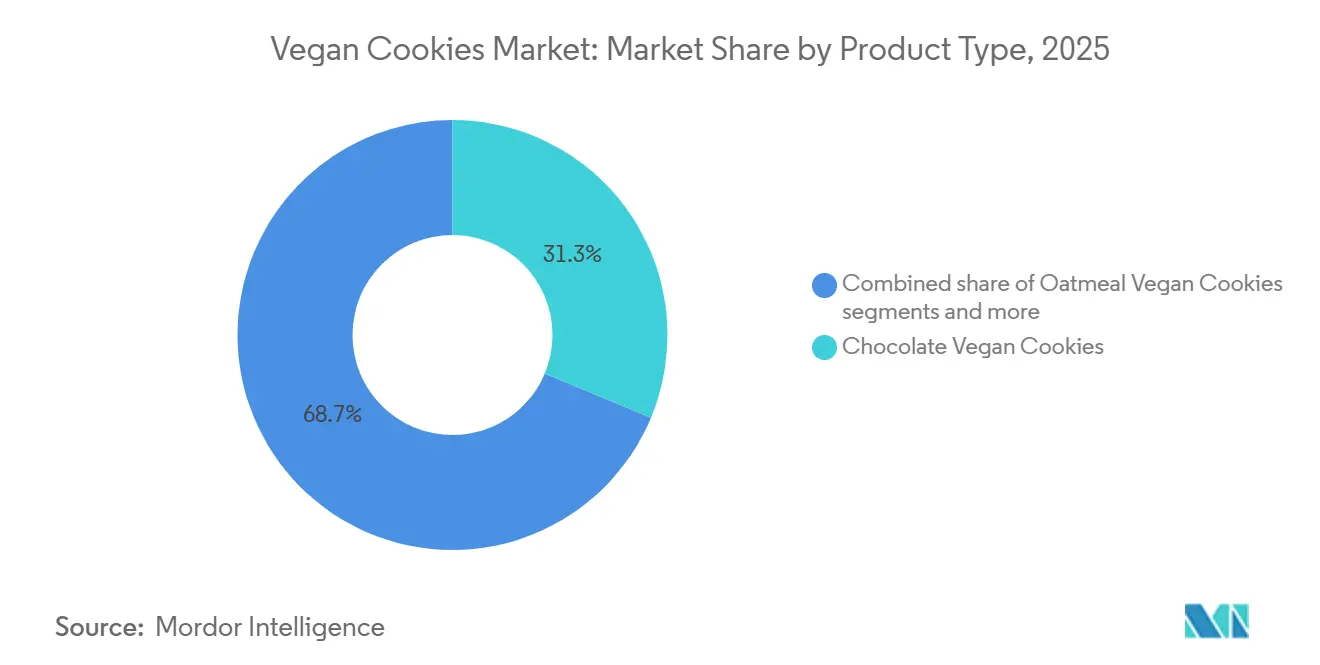

- By product type, chocolate led with 31.29% revenue share in 2025, while peanut butter is projected to advance at a 9.01% CAGR through 2031.

- By ingredient type, nut- and seed-based recipes accounted for 34.58% share in 2025, whereas wheat-based formats are on track for a 9.31% CAGR during 2026-2031.

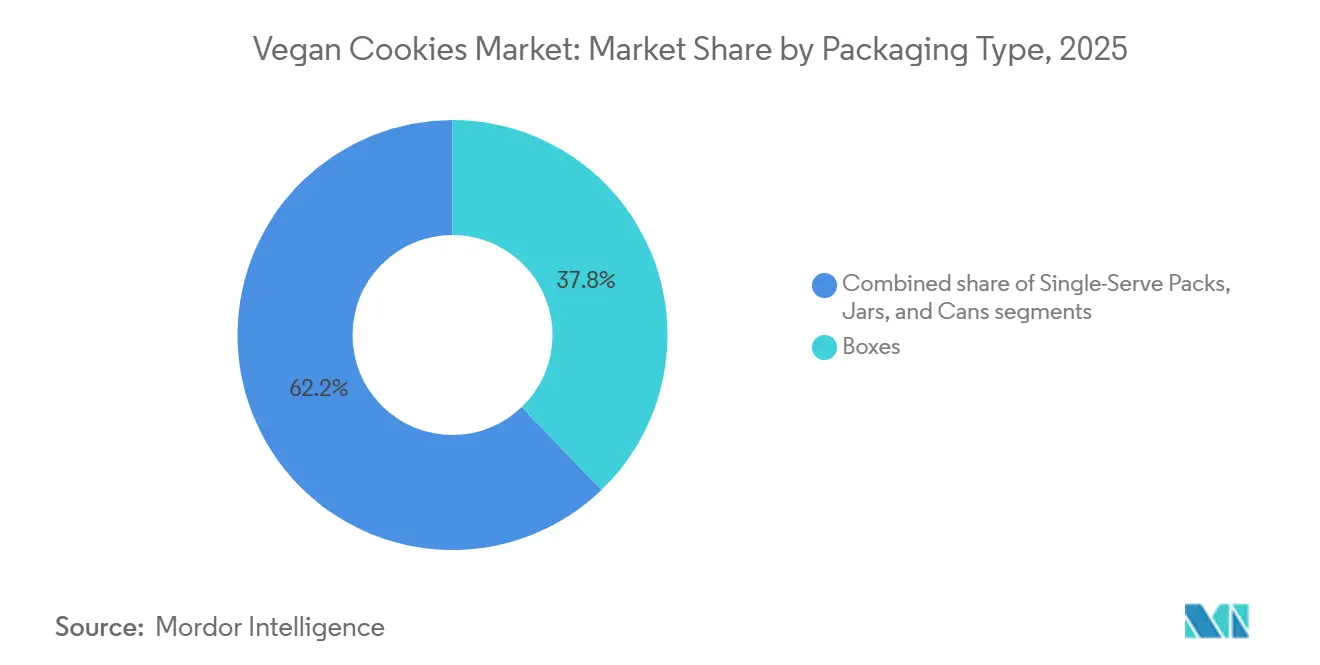

- By packaging type, boxes captured 37.81% share in 2025; single-serve packs are forecast to grow at a 9.51% CAGR during 2026-2031.

- By distribution channel, supermarkets and hypermarkets held 39.11% share in 2025, yet online retail is expanding at a 10.25% CAGR through 2031.

- By geography, North America commanded 34.21% share in 2025, while Asia-Pacific is the fastest-growing region with a 9.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vegan Cookies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising vegan and plant-based lifestyle adoption globally | +2.1% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Increasing demand for clean-label and allergen-free snacks | +1.8% | North America and Europe lead; emerging in Asia-Pacific urban centers | Short term (≤ 2 years) |

| Growing lactose intolerance and dairy allergy cases | +1.5% | Global, highest in Asia-Pacific (70-90% prevalence), South America, and Africa | Long term (≥ 4 years) |

| Expansion of health-conscious snacking trends | +1.3% | Global, particularly North America and Europe; Gen Z-driven in all regions | Medium term (2-4 years) |

| Rising popularity of ethical and cruelty-free food products | +0.9% | Europe and North America core; spillover to urban Asia-Pacific and Latin America | Long term (≥ 4 years) |

| Increasing innovation in ingredients (oat, almond, coconut-based cookies) | +1.2% | Global, with research and development hubs in North America and Europe; adoption in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising vegan and plant-based lifestyle adoption globally

Rising vegan and plant-based lifestyle adoption globally is significantly driving the growth of the vegan cookies market. Consumers are increasingly shifting toward plant-based diets due to health consciousness, sustainability concerns, and ethical considerations related to animal welfare. This transition is no longer limited to niche consumer groups, as plant-based food consumption has entered mainstream eating habits. For instance, according to the Good Food Institute, 53% of Americans reported consuming plant-based meat at some point in 2024, highlighting the widespread penetration of plant-based products into everyday diets[1]Source: Good Food Institute (GFI), “Plant-Based Meat in the United States”, gfi.org. In addition, around 60% of U.S. households purchased some type of plant-based food in 2024, reflecting strong and sustained consumer adoption across categories[2]Source: Good Food Institute, “U.S. retail market insights for the plant-based industry”, gfi.org. This growing acceptance is encouraging manufacturers to expand vegan bakery offerings, including cookies made without dairy, eggs, or other animal-derived ingredients.

Increasing demand for clean-label and allergen-free snacks

Increasing demand for clean-label and allergen-free snacks is a major driver of the vegan cookies market. Consumers are increasingly seeking products with simple, recognizable ingredients and minimal artificial additives, preservatives, or synthetic chemicals. This shift is strongly influenced by rising health awareness and growing concerns about food sensitivities and intolerances. Vegan cookies, which are naturally free from dairy and eggs, are well-positioned to meet this demand for allergen-free alternatives. According to research by CBI, Ministry of Foreign Affairs, clean-label products are projected to constitute over 70% of product portfolios in 2025 and 2026, rising significantly from 52% in 2021[3]Source: CBI Ministry of Foreign Affairs, “Which trends offer opportunities”, cbi.eu. This reflects a strong industry-wide shift toward transparency and healthier food formulations. Manufacturers are responding by reformulating products and introducing vegan cookies with organic, non-GMO, and minimally processed ingredients.

Growing lactose intolerance and dairy allergy cases

Growing lactose intolerance and dairy allergy cases are significantly supporting the expansion of the vegan cookies market. A rising share of the global population is experiencing difficulty digesting lactose, which leads to discomfort and restricts consumption of conventional dairy-based bakery products. Alongside this, increasing prevalence of milk protein allergies among children and adults is further encouraging the shift toward dairy-free alternatives. Vegan cookies, formulated without milk, butter, or other animal-derived dairy ingredients, provide a suitable substitute for these consumers. This has broadened the appeal of vegan cookies beyond strict vegan consumers to include health-sensitive and allergy-conscious individuals. Manufacturers are increasingly focusing on allergen-free formulations and clear dairy-free labeling to cater to this demand. Growing awareness of food intolerances and dietary-related health issues is further reinforcing this trend.

Expansion of health-conscious snacking trends

Expansion of health-conscious snacking trends is playing a major role in shaping the growth of the vegan cookies market. Consumers are increasingly shifting away from traditional high-sugar and high-fat snacks toward healthier alternatives that offer better nutritional value. This change is being driven by rising awareness of obesity, diabetes, and other lifestyle-related health conditions. Vegan cookies are gaining popularity as they are often perceived as a healthier option due to their plant-based ingredients and cleaner formulations. Manufacturers are responding by introducing cookies with reduced sugar, high fiber content, whole grains, and natural sweeteners. The demand for functional snacks that provide both taste and nutrition is also increasing among working professionals and younger consumers. Additionally, fitness-oriented consumers are actively seeking plant-based snacks that align with their wellness goals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher product cost compared to conventional cookies | -1.4% | Global, most acute in price-sensitive markets (South America, rural North America, developing Asia-Pacific) | Short term (≤ 2 years) |

| Limited availability in rural and low-income markets | -0.8% | Rural North America, South America, Sub-Saharan Africa, rural Asia-Pacific | Medium term (2-4 years) |

| Taste and texture perception differences compared to traditional cookies | -0.7% | Global, particularly in markets with low plant-based familiarity (Middle East, Eastern Europe, rural Asia) | Medium term (2-4 years) |

| Regulatory and labeling compliance challenges | -0.5% | Europe (EU labeling directives), North America (FDA/CFIA), Asia-Pacific (fragmented standards) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher product cost compared to conventional cookies

Higher product cost compared to conventional cookies remains a key challenge affecting the growth of the vegan cookies market. Vegan cookies are often priced at a premium due to the use of specialized plant-based ingredients such as almond flour, oat milk, coconut oil, and natural sweeteners. These ingredients are generally more expensive than traditional dairy, butter, and refined flour used in conventional cookies. In addition, small-batch production processes and limited economies of scale further contribute to elevated manufacturing costs. Supply chain complexities associated with sourcing high-quality vegan and organic raw materials also add to overall pricing pressure. As a result, vegan cookies are often perceived as less affordable, particularly in price-sensitive markets and developing economies. This cost disparity can limit mass-market adoption despite growing health and ethical awareness.

Limited availability in rural and low-income markets

Limited availability in rural and low-income markets is restricting the broader expansion of the vegan cookies market. Distribution networks for vegan and specialty bakery products are often concentrated in urban areas with well-developed retail infrastructure. In contrast, rural regions typically have limited access to supermarkets, specialty health stores, and premium bakery outlets where vegan cookies are commonly sold. Additionally, lower awareness of plant-based diets in these regions reduces consumer demand for such products. Logistical challenges and higher distribution costs further discourage manufacturers from expanding aggressively into these markets. Price sensitivity in low-income regions also makes premium vegan cookies less accessible to a large portion of consumers. As a result, market penetration remains uneven across different geographic areas. This limited reach continues to slow down the overall growth potential of the vegan cookies industry globally.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Chocolate Dominance Meets Protein-Dense Disruption

The chocolate segment accounted for the largest share of the global vegan cookies market in 2025, contributing 31.29% of total revenue. The strong position of this segment is primarily driven by high consumer preference for chocolate-based bakery snacks across both developed and emerging markets. Vegan chocolate cookies have gained widespread popularity due to continuous product innovation involving dark chocolate, cocoa nibs, chocolate chips, and reduced-sugar formulations. Leading brands are increasingly introducing indulgent yet plant-based cookie variants to attract flexitarian and health-conscious consumers. The segment also benefits from strong retail visibility across supermarkets, convenience stores, specialty vegan stores, and e-commerce platforms.

The peanut butter segment is projected to register the fastest CAGR of 9.01% during the forecast period through 2031. Growth in this segment is largely supported by increasing consumer demand for protein-rich and nutrient-dense snack products. Peanut butter vegan cookies are gaining traction among fitness-focused consumers due to their association with plant protein, healthy fats, and satiety benefits. Manufacturers are also introducing gluten-free, high-fiber, and organic peanut butter cookie variants to strengthen product differentiation in the market. Rising popularity of functional snacking and clean-label ingredients is further accelerating consumer adoption of peanut butter-based vegan cookies.

By Ingredient Type: Nut Supremacy Challenged by Wheat Renaissance

Nut- and seed-based formulations accounted for the largest share of the global vegan cookies market in 2025, representing 34.58% of total revenue. The dominance of this segment is primarily driven by rising consumer preference for nutrient-rich and plant-based snack ingredients. Almonds, cashews, peanuts, chia seeds, flaxseeds, sunflower seeds, and pumpkin seeds are increasingly being used in vegan cookies to enhance protein, fiber, and healthy fat content. Consumers are also showing strong interest in clean-label and minimally processed bakery products made with natural ingredients. Manufacturers are expanding their portfolios with nut- and seed-based cookie variants to target health-conscious, fitness-oriented, and flexitarian consumers.

The wheat-based segment is projected to register the fastest CAGR of 9.31% during the forecast period from 2026 to 2031. Growth of this segment is supported by the widespread use of wheat flour as a cost-effective and versatile ingredient in commercial vegan cookie production. Manufacturers are increasingly developing innovative wheat-based vegan cookies with improved textures, flavors, and fortified nutritional profiles to attract a broader consumer base. Rising demand for convenient and affordable plant-based snacks is also contributing to segment expansion globally. Additionally, advancements in whole wheat, multigrain, and fortified wheat formulations are helping brands position their products as healthier alternatives within the bakery sector.

By Packaging Type: Single-Serve Surge Amid Snackification

Boxes accounted for the largest share of the global vegan cookies market in 2025, capturing 37.81% of total revenue. The dominance of this packaging segment is largely attributed to its strong suitability for retail shelf placement, bulk packaging, and premium product presentation. Box packaging is widely preferred by manufacturers because it offers better product protection, extended shelf appeal, and improved branding opportunities. Consumers also favor boxed vegan cookies for family consumption, gifting purposes, and multi-pack purchases. In addition, supermarkets and hypermarkets prominently stock boxed cookie products due to easier storage, stacking, and display advantages. The growing demand for premium, organic, and assorted vegan cookie varieties is further supporting the continued expansion of box-based packaging formats across global markets.

Single-serve packs are projected to register the fastest CAGR of 9.51% through 2031. Growth of this segment is primarily driven by rising consumer demand for convenient, portable, and portion-controlled snack options. Busy lifestyles, increasing on-the-go consumption, and growing preference for healthy snacking are encouraging manufacturers to expand their single-serve vegan cookie offerings. These packaging formats are particularly popular among working professionals, students, fitness-focused consumers, and travelers seeking quick snack solutions. Brands are also utilizing single-serve packs to introduce trial-sized products and expand consumer accessibility through convenience stores, vending machines, and online retail platforms.

By Distribution Channel: E-Commerce Disrupts Supermarket Hegemony

Supermarkets and hypermarkets accounted for the largest share of the global vegan cookies market in 2025, representing 39.11% of total revenue. The strong dominance of this distribution channel is driven by extensive product availability, high consumer footfall, and strong visibility of vegan snack products across organized retail chains. These retail formats offer consumers access to a wide range of vegan cookie brands, flavors, packaging sizes, and promotional discounts under a single location. Manufacturers also prioritize supermarkets and hypermarkets because they provide strong shelf exposure and support impulse purchasing behavior. In-store product placements, promotional campaigns, and dedicated health food sections further contribute to higher sales volumes within this channel.

Online retail is projected to register the fastest CAGR of 10.25% through 2031. The rapid growth of this segment is primarily supported by increasing digital shopping adoption and rising consumer preference for convenient home delivery services. E-commerce platforms provide consumers with easy access to a broad portfolio of vegan cookie products, including premium, organic, gluten-free, and specialty variants that may have limited offline availability. Online retail channels also enable brands to directly engage with consumers through subscription models, personalized recommendations, and targeted digital marketing strategies. Growing smartphone penetration, expanding internet accessibility, and secure digital payment systems are further accelerating online vegan snack purchases globally.

Geography Analysis

North America accounted for the largest share of the global vegan cookies market in 2025, contributing 34.21% of total revenue. The region’s dominance is primarily driven by high consumer awareness regarding plant-based diets, clean-label foods, and health-focused snacking trends. The United States and Canada have witnessed strong demand for vegan bakery products due to the growing vegan, vegetarian, and flexitarian population base. Major food manufacturers and emerging plant-based brands are continuously launching innovative vegan cookie products with organic, gluten-free, and allergen-free formulations to meet evolving consumer preferences. The strong presence of organized retail chains, specialty health food stores, and advanced e-commerce infrastructure further supports market growth across the region.

Asia-Pacific is projected to register the fastest CAGR of 9.44% through 2031. Rapid urbanization, changing dietary habits, and increasing health consciousness among consumers are major factors driving market expansion in the region. Countries such as China, India, Japan, South Korea, and Australia are witnessing rising adoption of plant-based and dairy-free food products among younger consumer groups. Growing disposable incomes and expanding middle-class populations are also supporting higher spending on premium and specialty snack products, including vegan cookies. Manufacturers are increasingly expanding their regional presence through new product launches, online retail partnerships, and localized flavor innovations tailored to Asian consumer preferences.

Europe represents a significant market for vegan cookies due to strong consumer preference for sustainable, organic, and plant-based food products. Countries such as Germany, the United Kingdom, France, and the Netherlands have witnessed substantial growth in vegan bakery consumption supported by rising environmental awareness and clean-label food trends. South America is gradually emerging as a promising market, driven by increasing urbanization, expanding retail infrastructure, and growing interest in healthier snack alternatives among younger consumers. In the Middle East and Africa, market growth is supported by increasing exposure to international food trends, rising health awareness, and expanding availability of vegan products across supermarkets and specialty retail stores.

Competitive Landscape

The global vegan cookies market exhibits a highly fragmented competitive landscape characterized by the presence of numerous multinational food companies, regional bakery brands, emerging plant-based startups, and specialty vegan snack manufacturers. Market competition is intensifying as companies increasingly focus on product innovation, premium ingredient formulations, and clean-label positioning to strengthen their market presence. Leading players are actively introducing new flavors, gluten-free variants, high-protein formulations, and allergen-free products to cater to evolving consumer preferences. The market is also witnessing strong competition from artisanal and niche vegan bakery brands that emphasize organic ingredients, sustainability, and small-batch production.

Major companies operating in the vegan cookies market are increasingly investing in strategic partnerships, product launches, mergers, acquisitions, and geographic expansion initiatives to strengthen their competitive positioning. Companies are focusing on ingredient innovation involving oat flour, almond flour, coconut sugar, plant protein, and natural sweeteners to enhance nutritional value and product differentiation. Manufacturers are also prioritizing sustainable packaging solutions and ethical sourcing practices to align with rising consumer demand for environmentally responsible products.

Established bakery and snack companies are entering the vegan segment through brand diversification strategies to capitalize on the rapidly growing plant-based food industry. Additionally, aggressive digital marketing campaigns, influencer collaborations, and social media-based brand promotions are becoming important competitive tools for attracting younger and health-conscious consumers. The increasing availability of vegan cookies across mainstream retail outlets is also encouraging companies to strengthen supply chain efficiency and large-scale production capabilities.

Vegan Cookies Industry Leaders

Lenny & Larry's, LLC

Flowers Foods, Inc.

Partake Foods, Inc.

Mondelez International, Inc.

Lotus Bakeries NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Rubicon launched its new vegan chocolate chip cookies at Whole Foods Market, directly addressing the increasing demand for premium vegan treats among mainstream consumers. By introducing the product in Whole Foods, Rubicon showcased the growing acceptance of vegan products in the mainstream market and emphasized the importance of clean ingredient lists to meet consumer expectations.

- June 2025: Lidl, under its Tower Gate brand, introduced BN-style vegan biscuits in “Chocolate Creamy” and “Vanilla Creamy” flavors. These cookies, designed to replicate traditional sandwich-style biscuits, were made entirely plant-based, making them suitable for a wider range of consumers. This launch reflected Lidl’s strategic response to the growing popularity of private-label vegan bakery products and the increasing consumer preference for plant-based options.

- February 2025: Doughlicious expanded its plant-based snack portfolio with the launch of a new range of ready-to-eat vegan soft-baked cookies targeting the growing on-the-go snacking segment. The company introduced four flavors, including Double Chocolate Chip, Salted Caramel, Chocolate Chip, and Banana Good Granola, strengthening product diversification within the vegan bakery category.

- January 2025: Girl Scouts expanded their vegan cookie offerings for the 2025 season, retaining favorites like Thin Mints and Caramel Chocolate Chip with certified vegan formulations. These cookies now feature improved recipes, including gluten-free and allergen-friendly variants.

Global Vegan Cookies Market Report Scope

Vegan cookies are plant-based baked snack products made without the use of any animal-derived ingredients such as milk, butter, eggs, honey, or other dairy-based components. The vegan cookies market is segmented by product type, ingredient type, packaging type, distribution channel and geography. Based on product type, the market is segmented into chocolate vegan cookies, oatmeal vegan cookies, peanut butter vegan cookies, sandwich and creme-filled cookies and other Vegan cookies. By ingredient type, the market is segmented into nut andseed-based, wheat-based and other ingredient type. By packaging type, the market is segmented into single-serve packs, boxes, jars and cans. By distribution channel, the market is segmented into supermarkets/hypermarkets, specialty stores, online retail stores and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasting have been done in value terms (USD million).

| Chocolate Vegan Cookies |

| Oatmeal Vegan Cookies |

| Peanut Butter Vegan Cookies |

| Sandwich and Creme-filled Cookies |

| Other Vegan Cookies |

| Nut- & Seed-based |

| Wheat-based |

| Other Ingredient Type |

| Single-Serve Packs |

| Boxes |

| Jars |

| Cans |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Chocolate Vegan Cookies | |

| Oatmeal Vegan Cookies | ||

| Peanut Butter Vegan Cookies | ||

| Sandwich and Creme-filled Cookies | ||

| Other Vegan Cookies | ||

| By Ingredient Type | Nut- & Seed-based | |

| Wheat-based | ||

| Other Ingredient Type | ||

| By Packaging Type | Single-Serve Packs | |

| Boxes | ||

| Jars | ||

| Cans | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the vegan cookies market today?

The vegan cookies market size reached USD 3.46 billion in 2026 and is on course to hit USD 5.14 billion by 2031.

What is the expected growth rate for vegan cookies over 2026-2031?

The market is projected to post an 8.24% CAGR through 2031.

Which product type sells the most vegan cookies?

Chocolate variants dominated with a 31.29% share of sales in 2025.

Which region is growing the fastest?

Asia-Pacific is set to grow at about 9.44% CAGR through 2031, fueled by large lactose-intolerant populations and urban plant-based adoption.

Why are single-serve packs gaining popularity?

Consumers seeking portion control and on-the-go snacks are driving a 9.51% CAGR for single-serve formats.

Page last updated on: