Vapor Recovery Units Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

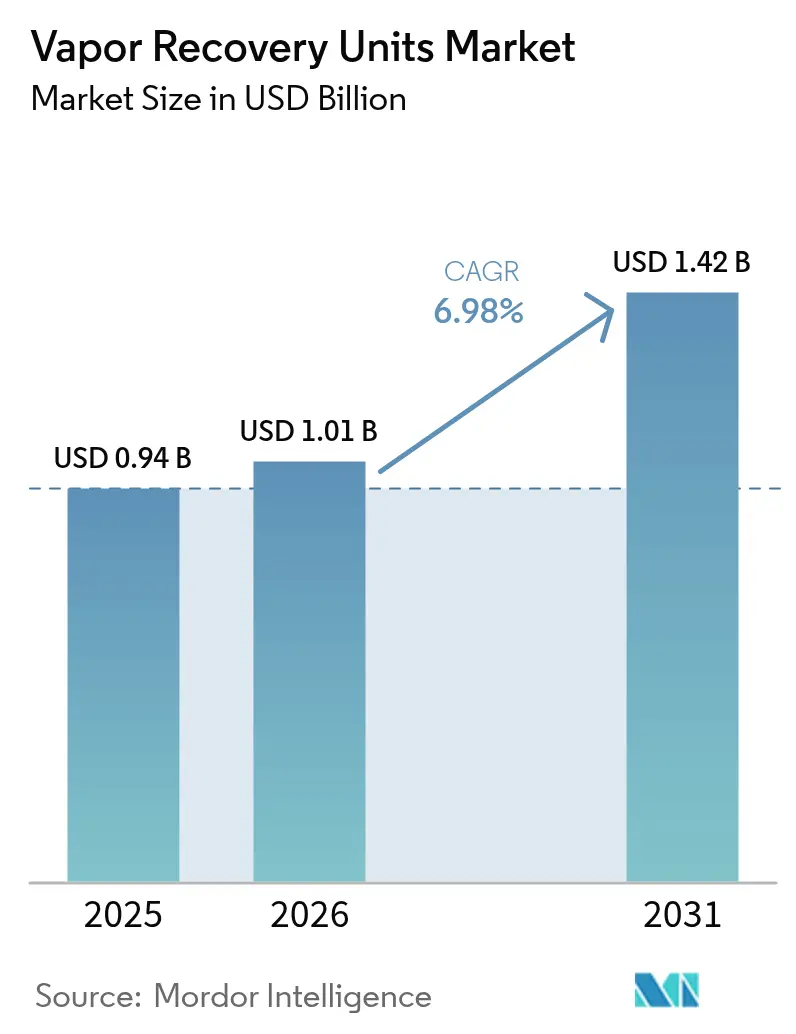

| Market Size (2026) | USD 1.01 Billion |

| Market Size (2031) | USD 1.42 Billion |

| Growth Rate (2026 - 2031) | 6.98% CAGR |

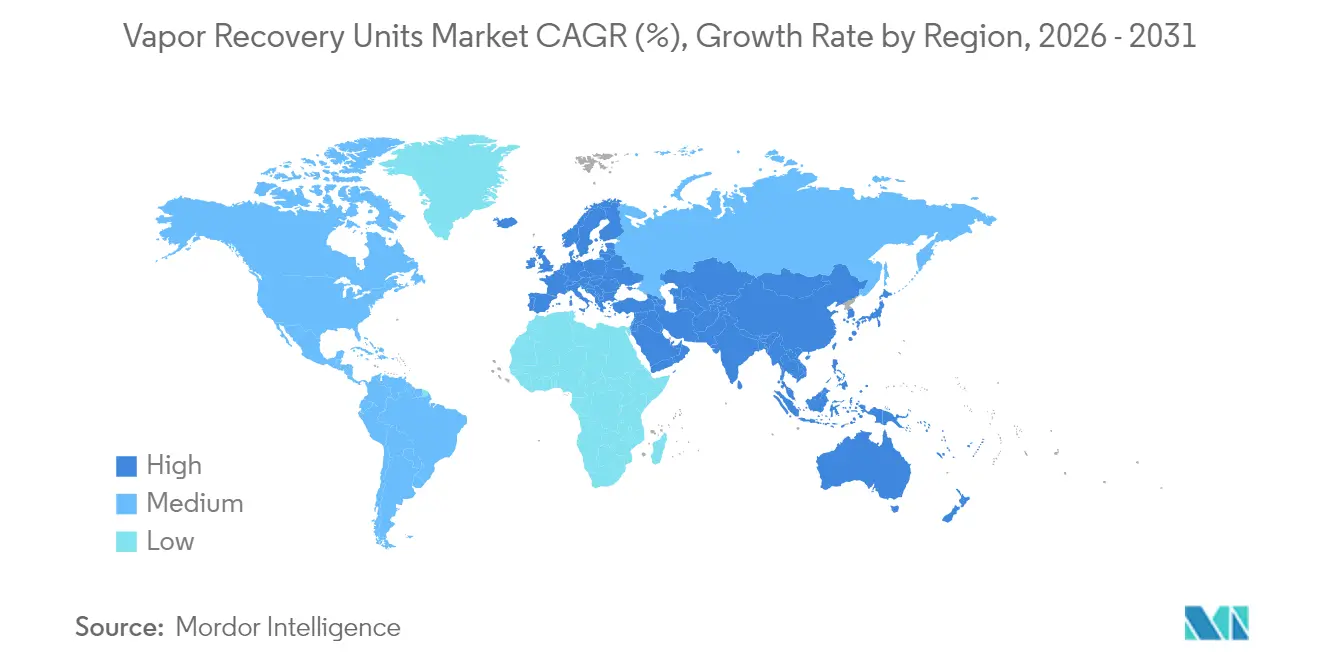

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vapor Recovery Units Market Analysis by Mordor Intelligence

Vapor Recovery Units Market size in 2026 is estimated at USD 1.01 billion, growing from 2025 value of USD 0.94 billion with 2031 projections showing USD 1.42 billion, growing at 6.98% CAGR over 2026-2031.

Heightened enforcement of the United States Environmental Protection Agency’s new methane rule, combined with the escalating Methane Waste Emissions Charge, is placing a clear economic value on capturing previously vented vapors. Uptake is propelled by zero-routine-flaring commitments, real-time monitoring innovations, and premium pricing for high-BTU recovered gas streams. At the same time, rapid breakthroughs in membrane science are shortening payback timelines and reducing life-cycle costs for operators that must meet increasingly stringent leak-detection and repair thresholds. Competitive activity is increasingly defined by digital twin deployments that trim downtime and modular offerings aimed at shallow-decline wells where capital discipline is tight.

Key Report Takeaways

- By product type, compression-based units held 45.55% of the vapor recovery units market share in 2025, while membrane separation units are forecasted to post the fastest growth rate of 8.34% from 2025 to 2031.

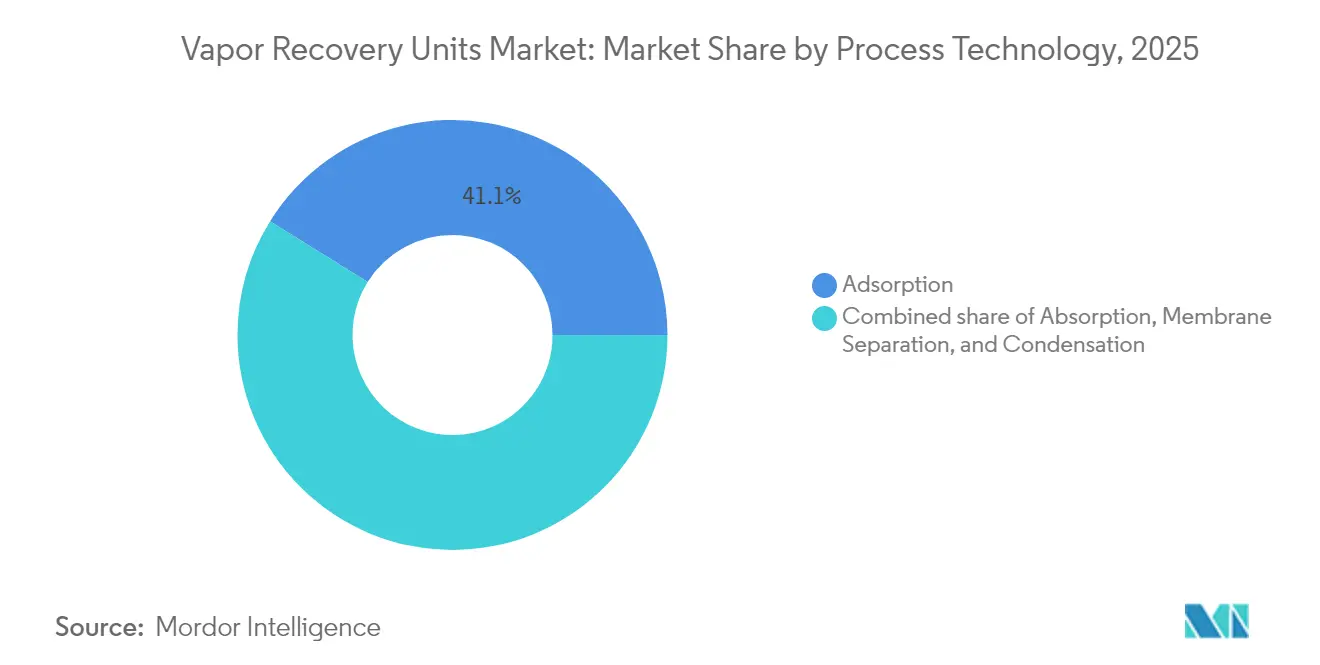

- By process technology, adsorption captured 41.12% of the vapor recovery units market size in 2025; membrane separation is projected to advance at a 12.15% CAGR to 2031.

- By flow-rate capacity, the 200-500 Mscfd band is poised for the quickest 7.12% CAGR, overtaking the 50-200 Mscfd segment, which led with a 38.62% share in 2025.

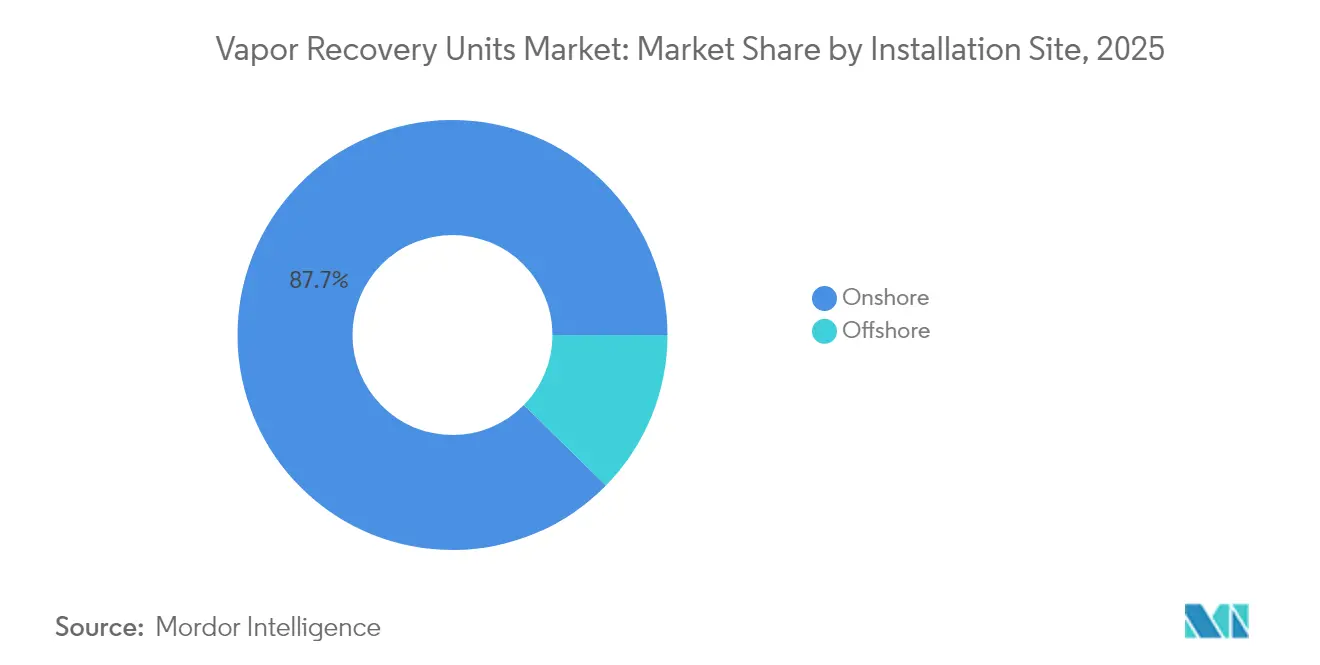

- By installation site, onshore projects accounted for 87.65% of the 2025 spend, whereas offshore deployments are growing at an 7.74% CAGR amid a rebound in FPSO investments.

- By application, storage tanks generated 37.85% of revenue in 2025; flaring-gas recovery is set to climb at a 7.36% CAGR through 2031.

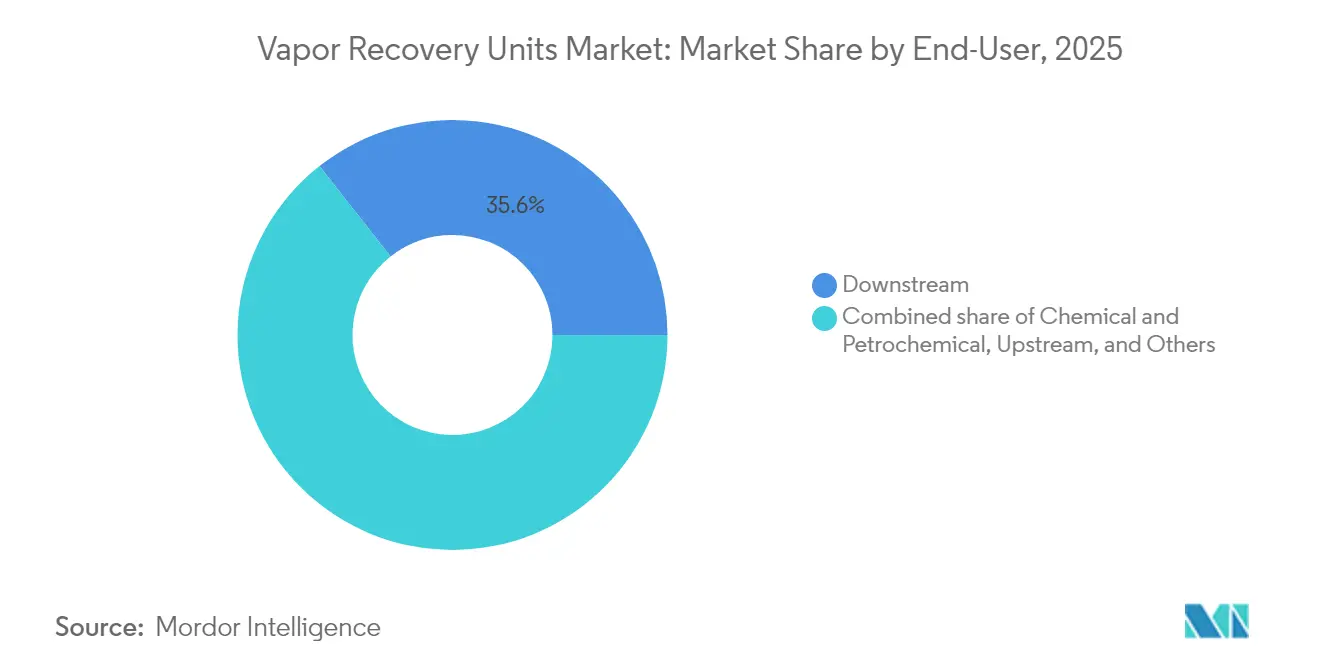

- By end-user, downstream facilities retained a 35.62% share in 2025; however, chemical and petrochemical plants are forecasted to record a 7.28% CAGR through 2031.

- By geography, North America accounted for 38.25% of the vapor recovery units market share in 2025; the Asia-Pacific region is projected to expand at an 8.07% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vapor Recovery Units Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|---|

| Tightening methane-fee & LDAR regulations | +2.1% | Global, with North America & Europe leading | Short term (≤ 2 years) | |

| Economic pay-back from recovered rich gas | +1.8% | Global, particularly North America shale regions | Medium term (2-4 years) | |

| Stricter gasoline terminal vapor rules (Asia) | +1.2% | APAC core, spill-over to MEA | Medium term (2-4 years) | |

| Up-stream zero-routine flaring targets | +0.9% | Global, with Middle East & Africa focus | Long term (≥ 4 years) | |

| Digital-twin uptime optimisation | +0.7% | Global, with early adoption in North America & Europe | Medium term (2-4 years) | |

| Voluntary crude carbon-intensity scoring | +0.5% | Global, with emphasis on ESG-focused regions | Long te | |

| Source: Mordor Intelligence | ||||

Tightening Methane-Fee & LDAR Regulations

The EPA rule mandating 95% reductions for new and modified oil and gas sources took effect on May 7, 2024, and is reinforced by a Super Emitter Program that obliges operators to remediate plumes exceeding 100 kg/h within prescribed time windows. Canada’s analogous framework, effective March 26, 2025, will apply to 434 petroleum facilities and reduce 488,000 tonnes of VOCs through 2045.(1)Environment and Climate Change Canada, “Reduction in the Release of Volatile Organic Compounds Regulations,” canada.ca Coupled with a Methane Waste Emissions Charge that rises from USD 900 per ton in 2024 to USD 1,500 per ton by 2026, these measures make prompt vapor capture financially rational even at marginal wells. Third-party satellite, drone, and OGI surveillance heightens non-compliance risk, thereby accelerating demand for vapor recovery units.(2)Source: Trihydro Corporation, “EPA’s Super Emitter Program,” trihydro.com

Economic Pay-Back from Recovered Rich Gas

Recovered vapors typically exceed pipeline-quality BTU specifications and often contain monetizable NGL fractions, delivering project revenues of USD 132,000 against installed costs of USD 100,000 with nine-month payouts in shale plays. Field studies indicate that 94.9% of methane losses at gas-processing facilities can be abated profitably, collectively valued at USD 8.4 million annually. Rising spot gas prices, escalating carbon penalties, and attractive liquids credits are forging a triple dividend that fortifies the vapor recovery units market.

Stricter Gasoline Terminal Vapor Rules (Asia)

China’s oil and gas methane output expanded eightfold between 1990 and 2022, prompting the development of a national action plan centered on high-frequency monitoring and the implementation of best-available controls. South Korea’s Clean Air Conservation Act now directs real-time benzene tracking at terminals handling volatile cargoes, pushing operators to adopt high-efficiency VRUs that meet 550 ppmv TOC limits for new facilities. The alignment of regional rules with MARPOL Annex VI for marine loading is opening routes for global suppliers, underpinning Asia-Pacific’s outsize 8.4% CAGR within the vapor recovery units market.

Up-Stream Zero-Routine Flaring Targets

The World Bank and IOC's pledges to eliminate routine flaring by 2030 translate into field-level retrofits, where flare-gas recovery yields internal rates of return above 20% compared with vent-and-burn practices. Offshore FPSOs sanctioned in 2024 integrate variable-speed compression, ejector boosters, and CO₂ capture as baseline utilities, demonstrating that near-zero-flaring designs are commercially viable.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for compression skids | -1.4% | Global, particularly affecting marginal operations | Short term (≤ 2 years) |

| Corrosive sour-gas service issues | -0.8% | Regional, concentrated in sour gas production areas | Medium term (2-4 years) |

| Off-grid power constraints at shale pads | -0.6% | North America shale regions, remote offshore locations | Short term (≤ 2 years) |

| Cheap flaring credits in carbon markets | -0.4% | Global, with regional variations in carbon pricing | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX for Compression Skids

Compression-dominant systems, which account for nearly half of 2024 revenue, require upfront expenditures exceeding USD 100,000 per site, a hurdle that could shut in up to 300,000 US marginal wells producing 15 bbl/day or less.(3)Source: Flogistix, “Vapor Recovery Units | VRU,” flogistix.com Vendors ease the burden through rental fleets and lease-to-own structures, while ejector-based packages eliminate the need for rotating machinery, thereby curtailing capex and maintenance.

Corrosive Sour-Gas Service Issues

H₂S-rich streams mandate stainless alloys, special elastomers, and upgraded seals, inflating the total cost of ownership relative to sweet-gas duty. Membrane elements are prone to accelerated degradation in sour service unless protected by new chemistries, such as polyimide-graphene blends. Adsorption beds, on the other hand, require frequent carbon change-outs. Research on resilient materials is underway, but adoption in highly sour fields remains tentative, tempering the growth of vapor recovery units in those locales.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Compression Dominance Meets Membrane Innovation

Compression packages accounted for 45.55% of 2025 sales in the vapor recovery units market, reflecting reliability across tank, pipeline, and terminal sites. Membrane VRUs, however, are growing at an 8.34% CAGR and benefit from fuel-free operation and compact footprints that allow skid mounting on congested pads. The vapor recovery units market size for membrane systems is projected to reach USD 281 million by 2031, driven by graphene-enhanced modules that reduce energy consumption by more than 50%. Ejector/Venturi units are carving a niche at low-pressure remote leases where pneumatic power is readily available, and cryogenic VRUs thrive in NGL-rich plays that justify deeper cooling cycles.

Continued materials progress, ranging from mixed-matrix membranes to scroll compressors with variable-frequency drives, has narrowed OPEX gaps against legacy compression. Digital twin models optimize set points in real-time, extending component life and reducing unplanned downtime by up to 30%. These technology inflections shift customer evaluations toward life-cycle economics over first cost, accelerating membrane traction within the vapor recovery units market.

By Process Technology: Adsorption Leadership Under Membrane Pressure

Activated-carbon adsorption accounted for 41.12% of 2025 revenue, thanks to near-unity recovery efficiencies that meet 95% VOC rules. The vapor recovery units market share for membrane separation remains lower today but is climbing fastest at a 12.15% CAGR, driven by polymer-of-intrinsic-microporosity films that post permeabilities above 10,000 GPU. Absorption towers remain relevant in benzene-rich service, while condensation units thrive where phase-change economics make chilling more attractive.

Operators weigh the energy draw against the complexity of maintenance. Adsorption demands periodic carbon regeneration, whereas membranes avoid cycle downtime but must contend with fouling. Emerging AI-enabled monitors flag feed-quality excursions early, allowing operators to rotate skids rather than shut down, thereby boosting system uptime and further driving the growth of the vapor recovery units market.

By Flow-Rate Capacity: Mid-Range Momentum Drives Market Evolution

Units rated 50-200 Mscfd generated 38.62% of 2025 turnover as they match the production curves common to multi-well pads. Yet the 200-500 Mscfd class is forecast to show the strongest 7.12% CAGR, propelled by central processing hubs that pool vapors from satellite sites. Economies of scale drive the cost per recovered Mcf downward, thereby bolstering the market size for vapor recovery units in the mid-range systems segment. Below 50 Mscfd solutions pivot to modular designs, while above 500 Mscfd mega-VRUs serve LNG pre-treatment and large refinery projects.

Software-driven load balancing enables variable-speed compressors to track fluctuating feed rates without experiencing surge events, thereby enhancing fuel efficiency. Combined with predictive analytics, these features tighten the economic case at mid-scale, underpinning growth in this bandwidth of the vapor recovery units market.

By Installation Site: Onshore Stability Versus Offshore Innovation

Onshore projects captured 87.65% of 2025 revenue due to mature pipeline grids and easier logistics. Offshore, however, is adding installations at an 7.74% CAGR as Brazil and Guyana sanction deepwater FPSOs equipped with zero-routine-flaring packages. The vapor recovery units market size for offshore applications is expected to exceed USD 163 million by 2031, driven by space-saving scroll compression modules and robust seawater-cooled membranes. Harsh service demands stainless housings, explosion-proof drives, and remote-access diagnostics, which raise ticket prices but also increase margins for specialized vendors.

Onshore operators focus on modularity and quick tie-ins to storage tank roofs, while offshore engineers seek integrated skid designs that combine vapor and fuel-gas conditioning. This bifurcation shapes R&D spending and regional procurement channels across the vapor recovery units market.

By Application: Storage Tank Leadership Meets Flaring Recovery Growth

Storage tanks contributed 37.85% of 2025 revenue as EPA rules require 95% VOC control for vessels emitting more than 6 tons annually. Flaring-gas recovery is the fastest-growing sector, with a 7.36% CAGR; higher carbon fees render previously uneconomic flare streams profitable to capture. The vapor recovery units market size tied to flare capture could surpass USD 300 million by the end of the decade, as paybacks of under two years become commonplace in high-liquids formations.

Processing plants, loading racks, and gathering-line boosters round out demand. Continuous H₂S monitoring and auto-start blowers now couple with VRUs to prevent atmospheric bypass in upset conditions, smoothing compliance and reinforcing uptake across the vapor recovery units market.

By End-User: Downstream Dominance Challenged by Chemical Sector Expansion

Refineries and terminals accounted for 35.62% of the 2025 spend, primarily driven by long-standing vapor balancing and gasoline loading mandates. Chemical and petrochemical complexes are experiencing a 7.28% CAGR, as synthetic organic chemical standards stipulate 95% capture, and as fenceline benzene monitoring triggers corrective action. Upstream shale plays generate significant growth upside, but budget-constrained independent operators still tend to gravitate toward rental programs. Emerging segments, such as biofuels and pharmaceuticals, add incremental volume, thereby widening the user base of the vapor recovery units market.

Digital-twin adoption by multinational chemical firms enables a 65% reduction in solvent use under pollution-prevention alternatives, highlighting vapor recovery as a cost-effective compliance lever.

Geography Analysis

North America led the vapor recovery units market with 38.25% share in 2025, powered by rigorous EPA mandates and prolific shale output that yields high-value condensate vapors. Canada’s 2025 VOC rule, covering 434 sites, reinforces a regulatory bulwark that sustains capital flows even as marginal wells wrestle with compliance economics. Robust service networks, abundant gas takeaway, and active digital-tech pilots keep the region at the center of innovation.

The Asia-Pacific region is the pace-setter, with an 8.07% CAGR projected to 2031. China’s methane surge to 4 Tg in 2022 has triggered nationwide monitoring schemes, while South Korea’s benzene controls and India’s clean-fuel policies are expanding the addressable demand. Regional integration into global supply chains means ports and terminals must match international standards, further enlarging the vapor recovery units market.

Europe maintains solid demand through decarbonization targets and refinery revamps, whereas the Middle East & Africa progress is anchored by zero-routine-flaring pledges from NOCs and by Sour-Gas VRU retrofits on giant onshore fields. South America’s FPSO wave amplifies offshore prospects, with Brazil alone accounting for the majority of floating production orders through 2028. Collectively, converging methane strategies spotlight vapor recovery as a universal mitigation lever.

Competitive Landscape

The vapor recovery units market is moderately fragmented, with a long tail of regional fabricators and a clutch of global brands specializing in combustion, vapor capture, and after-market services. John Zink Hamworthy, Zeeco, and Flogistix offer integrated packages that combine VRUs with vapor combustor or burner flare solutions, while membrane pure-plays specialize in energy-efficient separation niches. Digital twin platforms, often sourced from third-party software houses, are now bundled with hardware to ensure 10-30% reductions in downtime and maintenance spend.

Disruptive entrants such as ZEVAC leverage compressed-air drive systems to sidestep electrical infrastructure and permitting, offering ready-fit kits for Subpart OOOOb compliance. Membrane innovators commercialize graphene and mixed-matrix modules capable of achieving a 53-fold CO₂/N₂ selectivity, thereby slashing compression horsepower and redefining cost curves. As carbon pricing spreads, portfolio breadth, rapid-response service, and compliance advisory services become competitive assets within the vapor recovery units market.

Vapor Recovery Units Industry Leaders

John Zink Company

Zeeco

BORSIG Membrane Technology

Flogistix

Cimarron Energy Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Canada enforced VOC storage-and-loading rules targeting a 488,000 t reduction by 2045.

- January 2025: ANDRITZ introduced polymer-carrier membranes operating at 50–60 °C with minimal footprint.

- October 2024: EPA finalized 98% VOC limits for tanks above 20,000 gallons and 0.25 psia TVP.

- July 2024: EPA issued gasoline-terminal standards setting 550 ppmv TOC caps for new builds.

Global Vapor Recovery Units Market Report Scope

The vapor recovery units market report includes:

| Compression-based VRU |

| Ejector/Venturi VRU |

| Membrane Separation VRU |

| Condensation/Cryogenic VRU |

| Absorption (Carbon) VRU |

| Adsorption |

| Absorption |

| Condensation |

| Membrane Separation |

| Below 50 Mscfd |

| 50 to 200 Mscfd |

| 200 to 500 Mscfd |

| Above 500 Mscfd |

| Onshore |

| Offshore |

| Processing Plants |

| Storage Tanks |

| Loading and Unloading |

| Pipelines and Gathering |

| Flaring Gas Recovery |

| Upstream Oil and Gas |

| Downstream (Refining, Terminals) |

| Chemical and Petrochemical |

| Others (Biofuels, Pharma) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Product Type | Compression-based VRU | |

| Ejector/Venturi VRU | ||

| Membrane Separation VRU | ||

| Condensation/Cryogenic VRU | ||

| Absorption (Carbon) VRU | ||

| By Process Technology | Adsorption | |

| Absorption | ||

| Condensation | ||

| Membrane Separation | ||

| By Flow-rate Capacity | Below 50 Mscfd | |

| 50 to 200 Mscfd | ||

| 200 to 500 Mscfd | ||

| Above 500 Mscfd | ||

| By Installation Site | Onshore | |

| Offshore | ||

| By Application | Processing Plants | |

| Storage Tanks | ||

| Loading and Unloading | ||

| Pipelines and Gathering | ||

| Flaring Gas Recovery | ||

| By End-User | Upstream Oil and Gas | |

| Downstream (Refining, Terminals) | ||

| Chemical and Petrochemical | ||

| Others (Biofuels, Pharma) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the global value of the vapor recovery units market in 2026?

The vapor recovery units market size is USD 1.01 billion in 2026.

How fast is the vapor recovery units market expected to grow?

It is forecast to post a 6.98% CAGR between 2026 and 2031.

Which region will expand the quickest?

Asia-Pacific is projected to record the fastest 8.07% CAGR through 2031.

Why are membrane VRUs gaining traction?

Membrane units cut energy use by more than 50% and avoid carbon-bed regeneration downtime, giving them the highest 8.34% CAGR among product types.

What regulatory driver is most significant in North America?

The EPA methane rule enforces 95% VOC and GHG reductions and couples with an escalating Waste Emissions Charge that rises to USD 1,500 t-¹ by 2026.

How do VRUs create economic returns?

A single installation can yield annual revenues of roughly USD 132,000 from recovered rich gas against typical capex of USD 100,000, delivering sub-one-year paybacks.

Page last updated on: