Reservoir Analysis Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 10.09 Billion |

| Market Size (2031) | USD 12.84 Billion |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

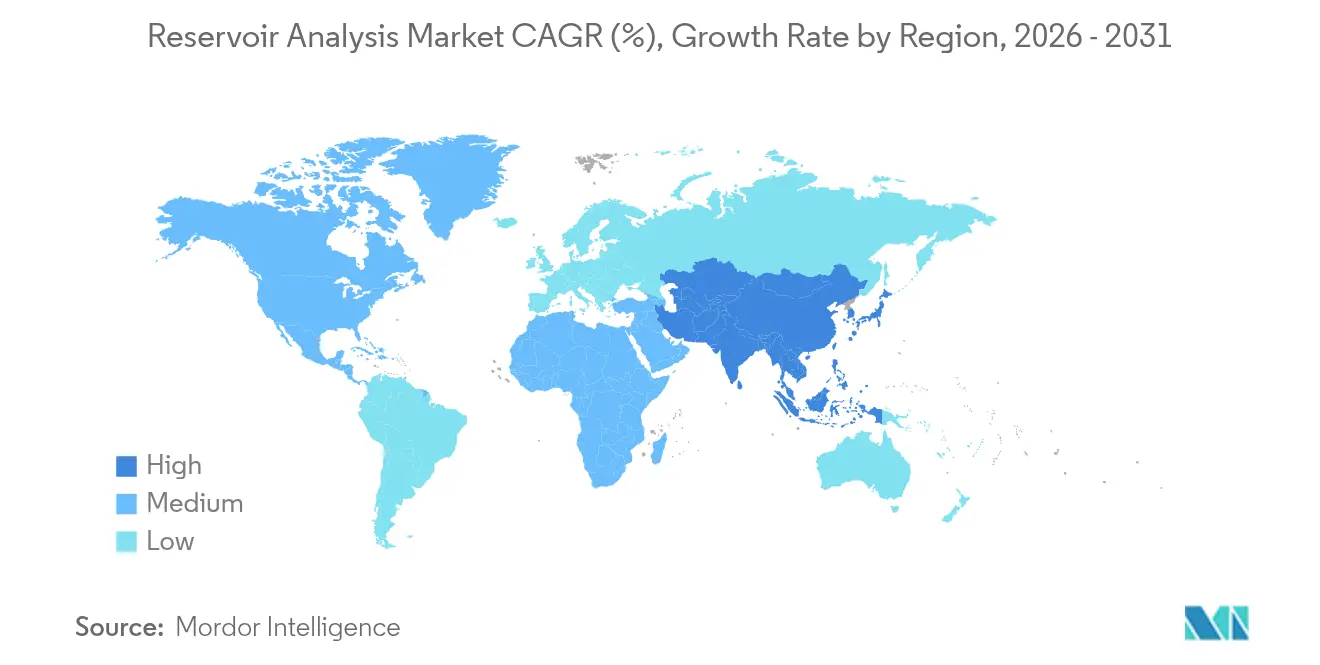

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

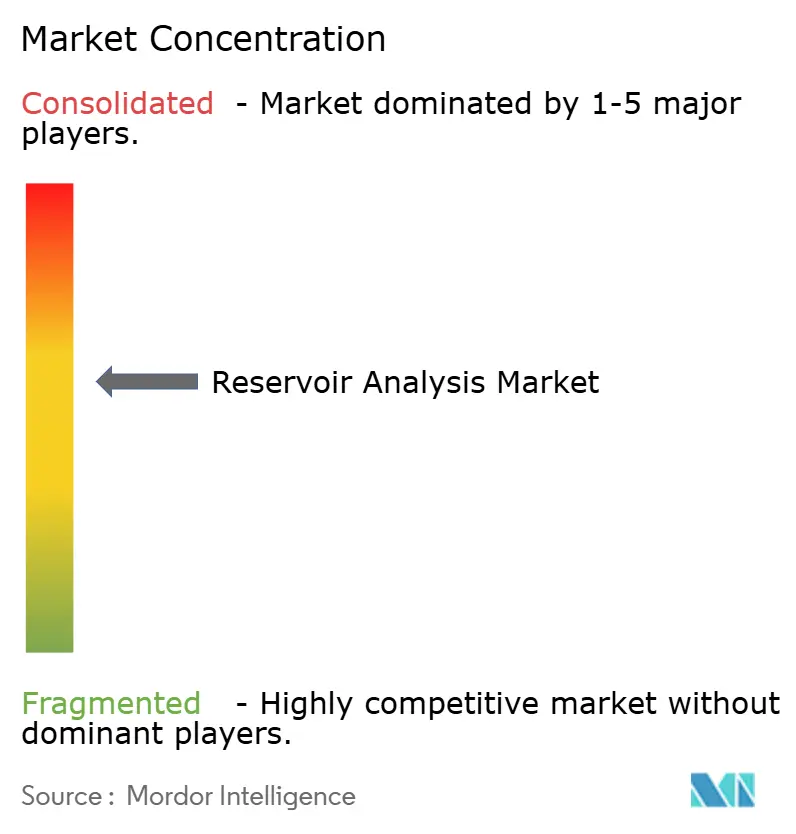

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Reservoir Analysis Market Analysis by Mordor Intelligence

The Reservoir Analysis Market size is expected to grow from USD 9.62 billion in 2025 to USD 10.09 billion in 2026 and is forecast to reach USD 12.84 billion by 2031 at 4.92% CAGR over 2026-2031.

This growth trajectory reflects the industry's strategic shift toward data-driven reservoir optimization, as operators face increasing pressure to maximize recovery rates while minimizing environmental impact. The reservoir analysis sector has become the critical nexus where traditional subsurface engineering converges with advanced analytics, positioning it as an essential enabler for both conventional field optimization and emerging energy transition initiatives. The competitive landscape reflects consolidation dynamics as major service providers integrate AI capabilities through strategic acquisitions and partnerships. Market concentration intensifies as operators demand integrated solutions that span reservoir characterization through production optimization, creating barriers for smaller, specialized providers.

Key Report Takeaways

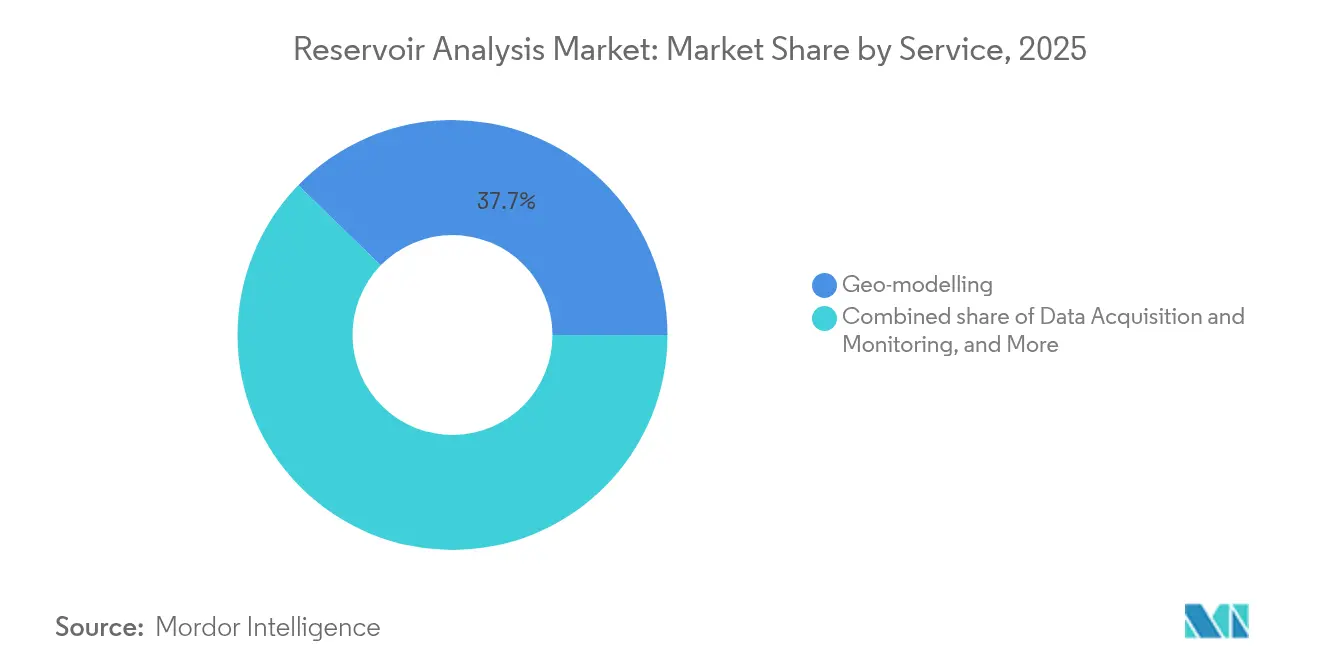

- By service, geo-modeling captured 37.74% of the reservoir analysis market share in 2025. Reservoir simulation is forecasted to expand at a 6.35% CAGR between 2026 and 2031.

- By technology, wireline logging led with 42.98% revenue share in 2025. Machine-learning-assisted analytics is projected to record a 6.88% CAGR through 2031.

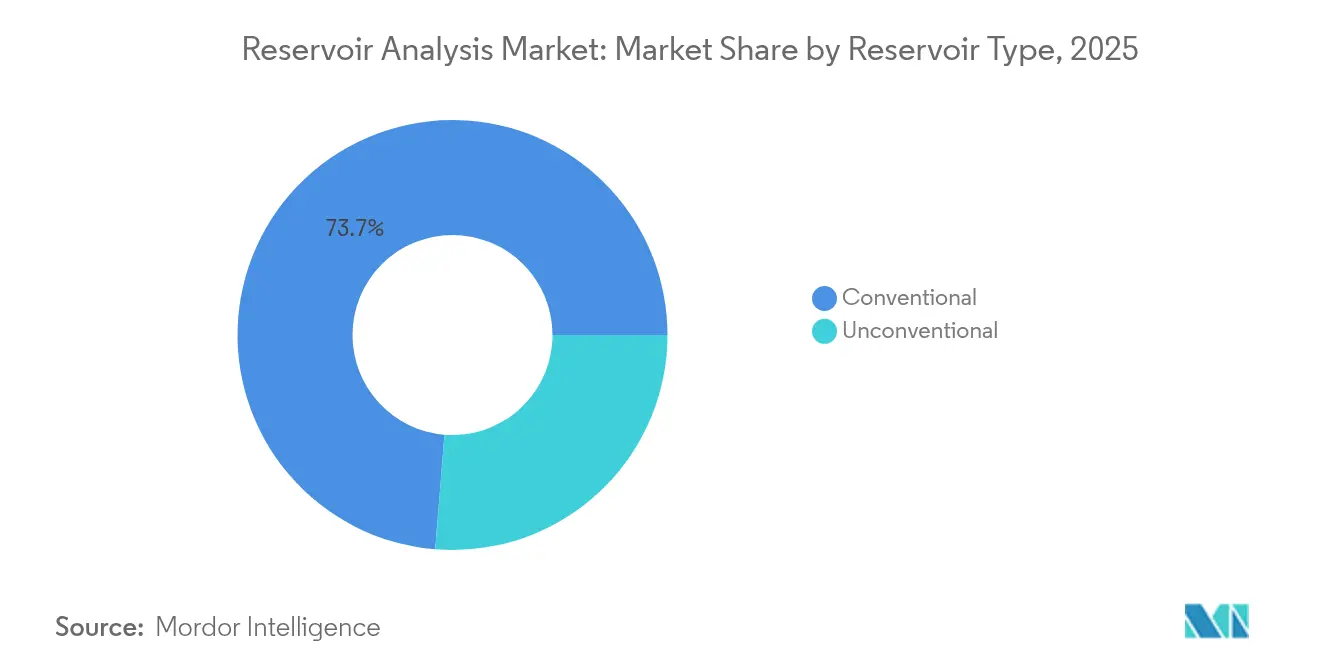

- By reservoir type, conventional assets contributed 73.72% of the reservoir analysis market size in 2025. Unconventional reservoirs are advancing at a 7.06% CAGR to 2031.

- By application, onshore projects held a 67.95% share of the reservoir analysis market size in 2025. Offshore deep- and ultra-deepwater developments are expected to grow at an 7.74% CAGR during the forecast period.

- By geography, North America commanded a 40.52% revenue share in 2025, while the Asia-Pacific is forecasted to register the fastest growth at a 7.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Reservoir Analysis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising unconventional hydrocarbon development | +1.20% | North America core; expanding in APAC & MEA | Medium term (2-4 years) |

| Digital-oilfield adoption & advanced analytics integration | +0.80% | Global; North America & Europe leading | Short term (≤2 years) |

| Increasing offshore deep- / ultra-deepwater E&P spending | +0.60% | Gulf of Mexico, North Sea, Brazil | Long term (≥4 years) |

| Cloud-based collaborative reservoir models | +0.50% | Early uptake in North America & Middle East | Medium term (2-4 years) |

| Mandatory CCUS reservoir suitability studies | +0.40% | Europe & North America; spreading globally | Long term (≥4 years) |

| Geothermal repurposing of depleted fields | +0.30% | Europe & North America; emerging in APAC | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising unconventional hydrocarbon development

Rapid unconventional growth reshapes analytical requirements because shale reservoirs display multiphase flow regimes and artificial fracture networks that evade traditional models. Extra Trees machine-learning algorithms achieved an R² value of 0.81 while forecasting Duvernay shale production, doubling the accuracy compared with legacy decline-curve techniques. Driven completion workflows enable operators to fine-tune fluid volumes and proppant concentration, often doubling early-life output. Such demonstrable gains fuel demand for advanced reservoir characterization, lifting the reservoir analysis market as unconventional assets mature.

Digital-oilfield adoption & advanced analytics integration

Edge AI, IoT sensors, and real-time platforms enable reservoir analysis to shift from episodic studies to continuous optimization. In Ecuador’s Shushufindi Field, SLB’s Agora edge AI prevented 12,000 barrels of deferred oil by predicting injection system failures.(1)SLB, “Agora Edge AI Prevents Deferred Oil in Shushufindi,” slb.comAutomated fracture-stage evaluation now attains 99.7% event-detection accuracy, permitting on-the-fly pumping adjustments. These operational wins accelerate digital oilfield rollouts, reinforcing the steady expansion of the reservoir analysis market.

Increasing offshore deep- / ultra-deepwater E&P spending

Deepwater wells require multidisciplinary data synthesis to derisk investments of USD billions. SLB’s USD 800 million services pact with Petrobras spans 100 wells and leverages Ora intelligent testing for real-time fluid mapping. High-pressure, high-temperature environments enhance analytical rigor through the integration of seismic, petrophysical, and dynamic models, which safeguard well placement. These complexities elevate offshore demand, sustaining value growth in the reservoir analysis market.

Cloud-based collaborative reservoir models

Cloud platforms mobilize global asset teams around a living reservoir model that ingests real-time data. SLB’s 10-year pact with TotalEnergies builds Delfi-enabled AI workflows to automate history matching and predictive maintenance. Continuous updating counters volatile production behavior and accelerates decision cycles. Embracing cloud collaboration further underpins market expansion as operators rationalize software licensing and hardware costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oil-price volatility dampening E&P CAPEX | -0.70% | Global; acute in North America shale & offshore projects | Short term (≤2 years) |

| High service cost for HPHT & ultra-deepwater | -0.50% | Gulf of Mexico, North Sea, West Africa | Medium term (2-4 years) |

| Data-sovereignty & cybersecurity concerns | -0.30% | Europe, China, national oil companies | Medium term (2-4 years) |

| Shrinking pool of experienced professionals | -0.20% | North America & Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Oil-price volatility dampening E&P CAPEX

Despite firmer prices, producers maintain strict capital discipline, which prioritizes short-cycle studies over long-cycle ones. The Dallas Federal Reserve reports that companies are redirecting cash toward debt reduction and dividends rather than exploration budgets. Deferred projects shrink near-term spending on comprehensive reservoir studies, tempering the growth of the reservoir analysis market.

High service cost for HPHT & ultra-deepwater

HPHT projects exceeding 20,000 psi and 400 °F require bespoke metallurgy and sensors, which doubles the service prices relative to conventional work.(2)J. Smith, “Automated Stage-Wise Analysis Reaches 99.7% Accuracy,” OnePetro, onepetro.org Limited supplier pools add oligopolistic premiums, pushing some operators to postpone studies until cash flows stabilize. Elevated costs thus constrain uptake in the reservoir analysis industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Simulation Advances Amid Geo-Modeling Primacy

The reservoir analysis market size for geo-modeling reached its highest point in 2025, capturing a 37.74% share, due to its foundational role in field planning. Simulation, however, is forecast to post a 6.35% CAGR through 2031 as dynamic modelling supersedes static frameworks in unconventional settings. Operators leverage neural networks that outperform decline-curve forecasts by R² margins exceeding 0.80 in Eagle Ford evaluations. Integrated reservoir management is gaining traction because single-vendor solutions reduce interface risk and shorten decision-making loops.

Data acquisition remains resilient as permanent downhole gauges enable continuous surveillance. Sampling services persist for fluid PVT quality control, although non-invasive spectroscopic tools are reducing the need for core-based tests. Emerging “others” services, digital twins, and automated inversion signal the next wave of analytics, reinforcing the reservoir analysis market as a strategic platform for multi-disciplinary optimisation.

By Technology: Machine Learning Challenges Wireline Dominance

Wireline logging retained a 42.98% share of the reservoir analysis market size in 2025, thanks to decades of field use. Machine-learning-assisted analytics, although smaller, are expected to accelerate at a 6.88% CAGR through 2031, as convolutional networks automate lithology classification. Hybrid workflows integrate gamma-ray, resistivity, and acoustic logs with AI models, reducing the interpretation cycle time by 60%. Fiber-optic distributed sensing, coupled with 4D seismic, furnishes real-time fracture diagnostics that augment completion design.

Operators value the fusion of trusted measurement and predictive intelligence, prompting service players to bundle AI software with legacy hardware. Baker Hughes’ SureCONNECT FE fiber-optic wet-mate system, launched in January 2025, exemplifies this integration by enabling continuous monitoring in deepwater. This convergence feeds sustained value creation within the reservoir analysis market.

By Reservoir Type: Unconventional Momentum Confronts Conventional Scale

Conventional resources accounted for 73.72% of the reservoir analysis market share in 2025, driven by mature giant fields and established workflows. Unconventional assets, however, expand at a 7.06% CAGR because optimized fracturing and AI-enabled analytics expose new cash-flow opportunities. Digital rock analysis, combined with machine learning, now predicts core properties without the need for physical plugs, thereby trimming lab time and costs.

Investment trade-offs increasingly reward unconventional plays where rapid payout offsets shorter decline curves. Consequently, service providers tailor simulators to match the complexity of hydraulic fractures, broadening the reservoir analysis industry beyond classical Darcy-flow paradigms.

By Application: Offshore Upswing Outpaces Onshore Scale

Onshore fields contributed 67.95% of 2025 revenue, underlining their vast well count and lower entry barriers. Offshore projects, particularly deepwater, register the fastest 7.74% CAGR to 2031 because elevated revenue per barrel justifies premium services. Complex pressure regimes, fault compartmentalization, and multi-contact fluids necessitate an integrated analysis that spans geophysics to dynamic modeling.

New fiber-optic solutions that can withstand water depths of 10,000 feet provide real-time production insights, which are crucial for optimizing life-of-field efficiency. The cross-applicability of offshore innovations to shale plays further multiplies the addressable demand, supporting the sustained expansion of the reservoir analysis market.

Geography Analysis

North America retains its leadership position with a 40.52% revenue share in 2025, driven by prolific shale drilling and the early adoption of digital oilfield technologies. Operators embed machine learning in every phase from completion design to decline diagnostics, reinforcing regional dominance. Collaborative efforts, such as the SLB-Nabors automation program, illustrate the ongoing technology upgrades that keep the reservoir analysis market vibrant in the region. Regulatory incentives for carbon capture and storage also stimulate new evaluation campaigns across the Gulf Coast.

The Asia-Pacific region posts a 7.31% CAGR, the fastest worldwide, driven by ambitious national energy security targets. China surpassed 400 million tons of oil and gas output in 2024, a milestone underpinned by advanced reservoir analytics that unlocked tight gas and deep carbonate resources. Australia’s gas projects and India’s CBM expansions further accelerate demand for simulation, seismic inversion, and production monitoring. Large-scale CCUS projects such as BP’s Tangguh UCC in Indonesia add a parallel data stream focused on storage integrity.

Europe sustains a balanced market as operators extract more barrels from aging North Sea fields while pioneering the use of CO₂ sequestration. Meanwhile, the Middle East and Africa channels capex into gas monetisation and offshore frontier plays, respectively. National oil companies in the region are increasingly stipulating integrated reservoir frameworks that bundle AI simulation with real-time surveillance, thereby widening the customer base for reservoir analysis market providers.

Competitive Landscape

The reservoir analysis market is moderately concentrated, with SLB, Halliburton, and Baker Hughes holding the majority share through integrated portfolios that span wireline, seismic, analytics, and production solutions. SLB’s USD 7.1 billion purchase of ChampionX in July 2025 enhances its artificial-lift and chemical offerings, creating an end-to-end asset optimization suite. Halliburton’s TrueSync hybrid ESP motor and OCTIV Auto Frac underline a strategic focus on embedding reservoir understanding directly into downhole hardware.

Competitive differentiation now hinges on the depth of AI capability, cloud delivery, and partnership ecosystems, rather than solely on price. Emerging specialists such as Resoptima and Ikon Science leverage digital twins and rock-physics analytics to secure niche positions. Market entry barriers rise because operators prefer vendors who can guarantee measurable production improvements under outcome-based contracts. As a result, consolidation momentum is set to continue, reinforcing scale advantages for incumbents within the reservoir analysis industry.

Reservoir Analysis Industry Leaders

Schlumberger Limited

Halliburton Company

Baker Hughes Company

Weatherford International PLC

CGG SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: SLB (formerly Schlumberger) and TotalEnergies have formed a 10-year partnership to co-develop AI-powered digital solutions for subsurface workflows using SLB's Delfi platform.

- April 2025: Halliburton and Nabors Industries achieved the first fully automated surface and subsurface execution of rotary and slide drilling operations in Oman.

- February 2025: Halliburton and Sekal have deployed the world's first automated on-bottom drilling system for Equinor's North Sea operations. This innovative system integrates Halliburton's LOGIX automation with Sekal's DrillTronics and the rig automation control system.

- January 2025: Baker Hughes has introduced the SureCONNECT FE fiber-optic wet-mate system to enhance deepwater reservoir monitoring.

Global Reservoir Analysis Market Report Scope

Reservoir Analysis develops subsurface data to integrate analysis of rocks, pores, and fluids from various reservoirs. In addition, it calculates dynamic rock and fluid properties and gives reservoir model indirect measurements.

The Reservoir Analysis Market is segmented by application, reservoir type, service, and geography. By applications, the market is segmented into onshore and offshore. By reservoir type, the market is segmented into conventional and unconventional. By service, the market is segmented into geo modeling, reservoir simulation, data acquisition and monitoring, reservoir sampling, and others. The report also covers the market size and forecasts for the reservoir analysis market across the major region. For each segment, the market sizing and forecasts have been done based on revenue (USD billion).

| Geo-modelling |

| Reservoir Simulation |

| Data Acquisition and Monitoring |

| Reservoir Sampling |

| Integrated Reservoir Management |

| Others |

| Wireline Logging |

| 3-D/4-D Seismic Imaging |

| Fiber-Optic Distributed Sensing |

| Machine-Learning Assisted Analytics |

| Conventional |

| Unconventional |

| Onshore |

| Offshore |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Service | Geo-modelling | |

| Reservoir Simulation | ||

| Data Acquisition and Monitoring | ||

| Reservoir Sampling | ||

| Integrated Reservoir Management | ||

| Others | ||

| By Technology | Wireline Logging | |

| 3-D/4-D Seismic Imaging | ||

| Fiber-Optic Distributed Sensing | ||

| Machine-Learning Assisted Analytics | ||

| By Reservoir Type | Conventional | |

| Unconventional | ||

| By Application | Onshore | |

| Offshore | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the reservoir analysis market?

The market generated USD 10.09 billion in 2026 and is projected to reach USD 12.84 billion by 2031.

Which region dominates reservoir analysis spending?

North America leads with 40.52% 2025 revenue share, driven by mature shale plays and advanced digital-oilfield adoption.

What segment is growing fastest in the reservoir analysis market?

Machine-learning assisted analytics is projected to post a 6.88% CAGR through 2031, making it the fastest-expanding technology segment.

How are unconventional reservoirs influencing demand?

Unconventional assets are expected to grow at a 7.06% CAGR as AI-enabled completion design improves recovery, driving higher demand for dynamic simulation and real-time monitoring services.

What impact does CCUS have on reservoir analysis?

Mandatory CO₂ storage assessments in Europe and North America are creating new workflows focused on reservoir suitability and long-term monitoring, expanding the addressable market beyond traditional hydrocarbon applications.

Who are the key players in the reservoir analysis industry?

SLB, Halliburton, and Baker Hughes hold the largest shares, while specialists such as Ikon Science and Resoptima provide niche analytics solutions, especially in digital twins and rock-physics areas.

Page last updated on: