Flare Gas Recovery System Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.97 Billion |

| Market Size (2031) | USD 5.84 Billion |

| Growth Rate (2026 - 2031) | 8.07% CAGR |

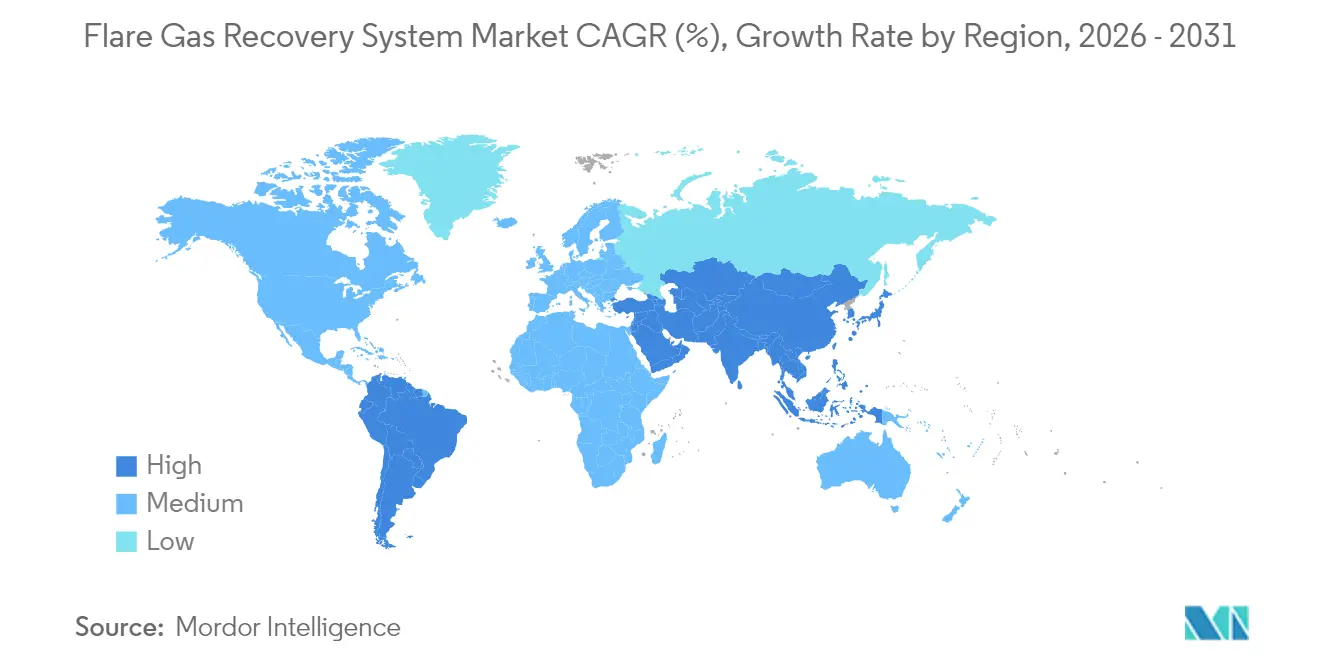

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

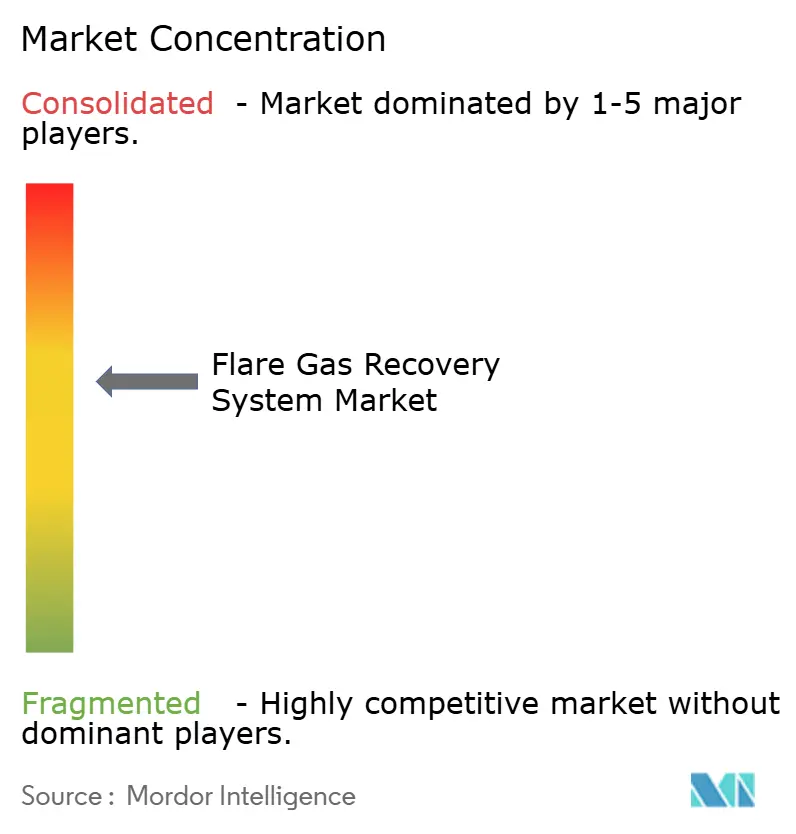

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flare Gas Recovery System Market Analysis by Mordor Intelligence

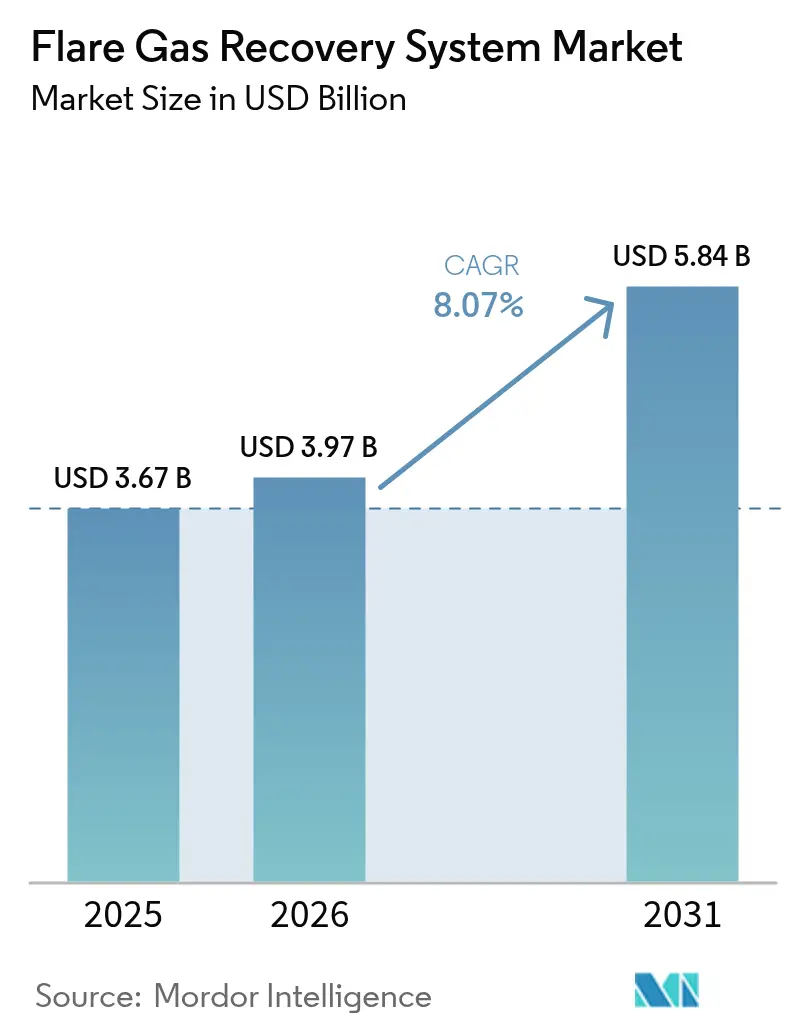

Flare Gas Recovery System market size in 2026 is estimated at USD 3.97 billion, growing from 2025 value of USD 3.67 billion with 2031 projections showing USD 5.84 billion, growing at 8.07% CAGR over 2026-2031.

The expansion is underpinned by regulatory penalties that can reach USD 40,000 per day for methane‐emission breaches in California, creating strong economic incentives for immediate investment.[1]California Air Resources Board, “Low Carbon Fuel Standard Regulation Amendments,” arb.ca.gov Operators no longer view recovery units as compliance add-ons. They treat them as revenue assets that generate carbon credits, fuel for blue-hydrogen production, and high-value natural gas liquids. Digitization, modular designs, and new membrane materials shorten payback periods across facility sizes, while national oil companies (NOCs) embed flare-reduction clauses in production contracts to accelerate technology deployment.

Key Report Takeaways

- By technology, compression-only units accounted for 45.60% of the flare gas recovery system market size in 2025, while membrane separation is progressing at a 12.18% CAGR to 2031.

- By component, compressors and blowers held 39.60% revenue share in 2025; instrumentation and control systems are advancing at 12.05% CAGR to 2031.

- By capacity, above-15 MMSCFD systems captured 42.60% of the flare gas recovery system market size in 2025; systems below 1 MMSCFD are expanding at a 9.85% CAGR between 2026-2031.

- By application, downstream refineries and petrochemicals contributed 39.70% of the flare gas recovery system market size in 2025, whereas LNG and gas-processing plants are forecast to expand at 10.95% CAGR through 2031.

- By geography, North America led with 38.70% of the flare gas recovery system market share in 2025, whereas Asia-Pacific is forecast to register the fastest regional CAGR of 11.35% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Flare Gas Recovery System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter global methane-emission penalties | 1.80% | Global; early enforcement in North America & EU | Short term (≤ 2 years) |

| Rising LNG liquefaction & FLNG projects | 1.60% | Asia-Pacific core; spill-over to Middle East | Medium term (2-4 years) |

| Carbon-pricing schemes linking flare credits to ESG funding | 1.40% | Global; premium pricing in EU & California | Medium term (2-4 years) |

| Integration with small-scale blue-hydrogen units | 1.20% | North America & EU; expanding to Asia-Pacific | Long term (≥ 4 years) |

| Mandatory flare-reduction targets in NOC production-sharing contracts | 1.00% | Middle East & Africa; selective Latin America | Medium term (2-4 years) |

| AI-enabled predictive vent-gas routing | 0.80% | Global; early adoption in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter global methane-emission penalties

Regulators shifted from voluntary guidelines to binding rules with escalating fees. The US EPA’s NSPS OOOOb requires methane fees of USD 900-1,500 per metric ton, while the EU mandates quarterly leak-detection reports.[2] [3]US Environmental Protection Agency, “Final Rule: Standards of Performance for Crude Oil and Natural Gas,” epa.gov European Commission, “Regulation on Methane Emissions Reductions,” eur-lex.europa.eu California’s amendments add a USD 40,000-per-day liability for repeat infractions, ensuring that flare gas recovery system market uptake now occurs during project design rather than after violations. Investors use methane intensity metrics in equity valuations, making recovery units essential for capital access.

Rising LNG liquefaction & FLNG projects

Asia-Pacific LNG capacity is expanding rapidly. Qatar’s Joint Boil-Off Gas project integrates recovery units to reach 99.5% gas utilization.[4]QatarEnergy, “North Field Sustainability Project Overview,” qatareenergy.qa Modular “Fast LNG” plants from New Fortress Energy process 0.5-2.0 MMSCFD of waste gas, proving economically viable for small fields. Twelve FLNG vessels sanctioned in 2024 require compact, offshore-rated membranes and compressors, anchoring long-term demand.

Carbon-pricing schemes linking flare credits to ESG funding

Voluntary carbon markets crossed USD 1.4 billion in 2024; engineered methane credits trade at USD 15-25 per ton CO₂e, well above forestry offsets. New “core carbon principles” favor industrial abatement. Operators monetize credits upfront through carbon-backed loans, de-risking capital outlays. Price swings of 40-60% prompted insurers to launch floor contracts that stabilise project cash flows.

Integration with small-scale blue-hydrogen units

ExxonMobil’s Baytown complex converts recovered gas into 1,000 t/day of blue hydrogen with 90% CO₂ capture. Modular 1-10 MW reactors process flare streams as low as 0.5 MMSCFD. HNO International’s EcoFlare Power targets data centres that value low-carbon backup power. Projects tap three revenue lines, penalty avoidance, hydrogen sales, and carbon credits, yet require advanced process control and higher capital.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX vs. low associated-gas value in ultra-mature fields | -2.40% | Global; acute in North Sea & Gulf of Mexico | Short term (≤ 2 years) |

| Limited cryogenic-grade gas quality in shale plays | -1.80% | North America shale basins; select global plays | Medium term (2-4 years) |

| Uncertain carbon-credit price floors | -1.60% | Global; volatility in voluntary markets | Medium term (2-4 years) |

| Scarcity of retrofit space on ageing offshore platforms | -1.40% | North Sea, Gulf of Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX vs. low associated-gas value in ultra-mature fields

Late-life offshore platforms face declining production and modest gas prices, making USD 2-5 million small-scale units hard to justify. Space constraints often double installation costs. Joint-platform sharing schemes ease the burden but rely on complex commercial agreements and short remaining asset lives.

Limited cryogenic-grade gas quality in shale plays

Permian gas can contain 5-15% nitrogen and elevated CO₂, challenging membrane selectivity and raising processing costs. Bakken streams vary widely, forcing customised designs that erode standardisation benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Membrane innovation drives market evolution

Compression-only systems retained 45.60% of the flare gas recovery system market share in 2025, owing to proven reliability and lower upfront costs. Membrane separation, however, is estimated to record a 12.18% CAGR, the fastest among technologies. The shift stems from tighter pipeline specifications and the ability of next-generation polymers to withstand sour-gas streams. Cryogenic condensation is a niche in ultra-high-purity applications but suffers from elevated energy demand. Absorption and adsorption maintain steady uptake in H₂S-rich fields.

Hybrid solutions blending compression and membranes are gaining traction because operators optimize capex while achieving higher recovery yields. MTR’s FuelSep™ system, deployed in the Eagle Ford in 2024, demonstrated 20% lower energy use than legacy skids while capturing C₃+ liquids for resale. The flare gas recovery system market size for hybrid units is forecast to expand above the overall 8.07% baseline through 2031 as manufacturers introduce modular cartridges adaptable to changing gas quality.

By Component: Digitization transforms control systems

Compressors and blowers dominated 39.60% of revenue in 2025, reflecting their indispensable role in creating suction and discharge pressure. Yet instrumentation and control systems will post the highest 12.05% CAGR to 2031 as facilities migrate from manual valves to autonomous loops governed by cloud analytics. Baker Hughes’ flare.IQ enables operators to verify 98% combustion efficiency in real time, a capability now mandatory in several jurisdictions. Vapour recovery towers and knock-out drums follow market growth, while heat exchangers face substitution by energy-efficient chiller packages in low-temperature climates.

By Capacity Range: Scale polarization reflects market dynamics

Above-15 MMSCFD plants held a 42.60% share in 2025 because integrated refineries and gas hubs favor economies of scale. Systems below 1 MMSCFD will grow at a 9.85% CAGR as skid-mounted packages let remote producers monetize gas previously vented. Operators appreciate plug-and-play modules that scale through parallel trains, though per-unit costs are higher. Mid-range 1-5 MMSCFD and 5-15 MMSCFD installations track the overall flare gas recovery system market.

By Application: LNG expansion drives processing-plant growth

Downstream refineries and petrochemicals accounted for 39.70% revenue in 2025, thanks to existing utilities and a steady waste-gas supply. LNG and gas-processing facilities are forecast to record an 10.95% CAGR as developers integrate recovery skids directly into main process trains. QatarEnergy’s North Field expansion and US Gulf Coast projects highlight how recovered gas feeds liquefaction or NGL extraction units, turning a liability into feedstock. Upstream operations still generate the largest volume of flare gas but face economic headwinds in mature basins.

Geography Analysis

North America holds 38.70% of the flare gas recovery system market size, supported by EPA rules, shale infrastructure, and readily available service networks. However, intermittent negative gas prices in the Permian Basin during 2024 prompted some operators to flare rather than sell, underlining the need for stricter enforcement. Canada’s Clean Electricity Regulations and Mexico’s emerging shale resources present incremental upside, though timelines diverge.

Asia-Pacific is the fastest-growing region at 11.35% CAGR. China is retrofitting refineries with carbon-capture and flare-recovery units, while India invests in gasification and LNG terminals. Southeast Asian FLNG projects and Japan and South Korea’s compact-system innovations underpin sustained momentum. Government policies offering tax breaks for methane abatement further reduce payback times.

Europe shows steady uptake driven by the EU methane strategy and carbon pricing. Operators in the North Sea weigh retrofit costs against decommissioning obligations, yet many proceed because EU ETS allowances now represent a significant revenue stream. Germany’s THG quota system for transport fuels creates another value pathway for recovered gas.

Middle East & Africa record selective growth. Saudi Arabia and UAE bundle flare-recovery requirements into concession agreements, ensuring early-phase deployment. Nigeria’s updated commercialization programme and Iraq’s GGIP establish large capture volumes. Nevertheless, financing and local-content mandates can slow procurement.

Competitive Landscape

The flare gas recovery system market remains moderately fragmented. Legacy combustion specialists John Zink Hamworthy and Zeeco leverage decades of experience and global installed bases. Equipment majors such as Honeywell UOP and Baker Hughes are pivoting towards digital service models. Software-centric entrants offer AI optimisation overlays atop any vendor’s hardware, capturing high-margin analytics revenue.

Competition now centres on turnkey packages that pair skid equipment with remote monitoring, predictive maintenance, and carbon-credit advisory. Patent filings around high-selectivity membranes, low-bleed pneumatics, and machine-learning algorithms rose markedly in 2024. Strategic alliances, BP with Baker Hughes and SOCAR with Honeywell, illustrate how firms combine domain expertise to win multi-facility rollouts. Moderate M&A activity is expected as traditional mechanical firms acquire digital startups to fill capability gaps.

Flare Gas Recovery System Industry Leaders

John Zink Hamworthy Combustion LLC

Gardner Denver holdings Inc

Honeywell International Inc

Zeeco Inc.

Wärtsilä Oyj Abp

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: TotalEnergies launched the final phase of Iraq’s Gas Growth Integrated Project, capturing 600 MMSCFD of associated gas for power generation and export.

- February 2025: HNO International launched EcoFlare Power to convert flare gas into hydrogen-fueled electricity for data centres and Bitcoin mines, opening a non-traditional customer base.

- January 2025: Kathairos and Kimray introduced a zero-emissions pneumatic control suite adopted at 2,000 sites across North America, eliminating 200,000 t CO₂e.

- March 2024: Baker Hughes expanded the flare.IQ deployments with SOCAR and EGPC, delivering real-time emission quantification across multiple offshore assets.

Global Flare Gas Recovery System Market Report Scope

The flare gas recovery system market report includes:

| Compression-only Systems |

| Membrane Separation |

| Cryogenic Condensation |

| Absorption/Adsorption |

| Hybrid (e.g., Compression + Membrane) |

| Compressors and Blowers |

| Vapour Recovery Towers |

| Knock-Out Drums and Separators |

| Heat Exchangers/Chillers |

| Instrumentation and Control Systems |

| Below 1 MMSCFD |

| 1 to 5 MMSCFD |

| 5 to 15 MMSCFD |

| Above 15 MMSCFD |

| Upstream (Onshore and Offshore) |

| Downstream (Refineries and Petrochemicals) |

| LNG and Gas-processing Plants |

| Others (Gas Storage, Terminals) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Technology | Compression-only Systems | |

| Membrane Separation | ||

| Cryogenic Condensation | ||

| Absorption/Adsorption | ||

| Hybrid (e.g., Compression + Membrane) | ||

| By Component | Compressors and Blowers | |

| Vapour Recovery Towers | ||

| Knock-Out Drums and Separators | ||

| Heat Exchangers/Chillers | ||

| Instrumentation and Control Systems | ||

| By Capacity Range | Below 1 MMSCFD | |

| 1 to 5 MMSCFD | ||

| 5 to 15 MMSCFD | ||

| Above 15 MMSCFD | ||

| By Application | Upstream (Onshore and Offshore) | |

| Downstream (Refineries and Petrochemicals) | ||

| LNG and Gas-processing Plants | ||

| Others (Gas Storage, Terminals) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Egypt | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving the flare gas recovery system market growth?

Stricter methane regulations, expanding LNG capacity, and monetisation opportunities such as carbon credits and blue hydrogen sales are pushing an 8.07% CAGR through 2031.

Which region will grow the fastest?

Asia-Pacific is forecast to post an 11.35% CAGR to 2031, powered by LNG projects and supportive emission-reduction policies.

How large is the flare gas recovery system market size today?

The market reached USD 3.97 billion in 2026 and is projected to rise to USD 5.84 billion by 2031.

Which technology segment leads the market?

Compression-only systems held 45.60% of 2025 revenue, but membrane separation is the fastest-growing at 12.18% CAGR.

What share do compressors and blowers command?

They accounted for 39.60% of 2025 component revenue, reflecting their critical role in any recovery skid.

Are small-scale recovery units viable?

Yes. Systems below 1 MMSCFD are forecast to grow at 9.85% CAGR owing to modular designs that suit remote or marginal fields.

Page last updated on: