Market Overview

| Study Period | 2021 - 2031 |

|---|---|

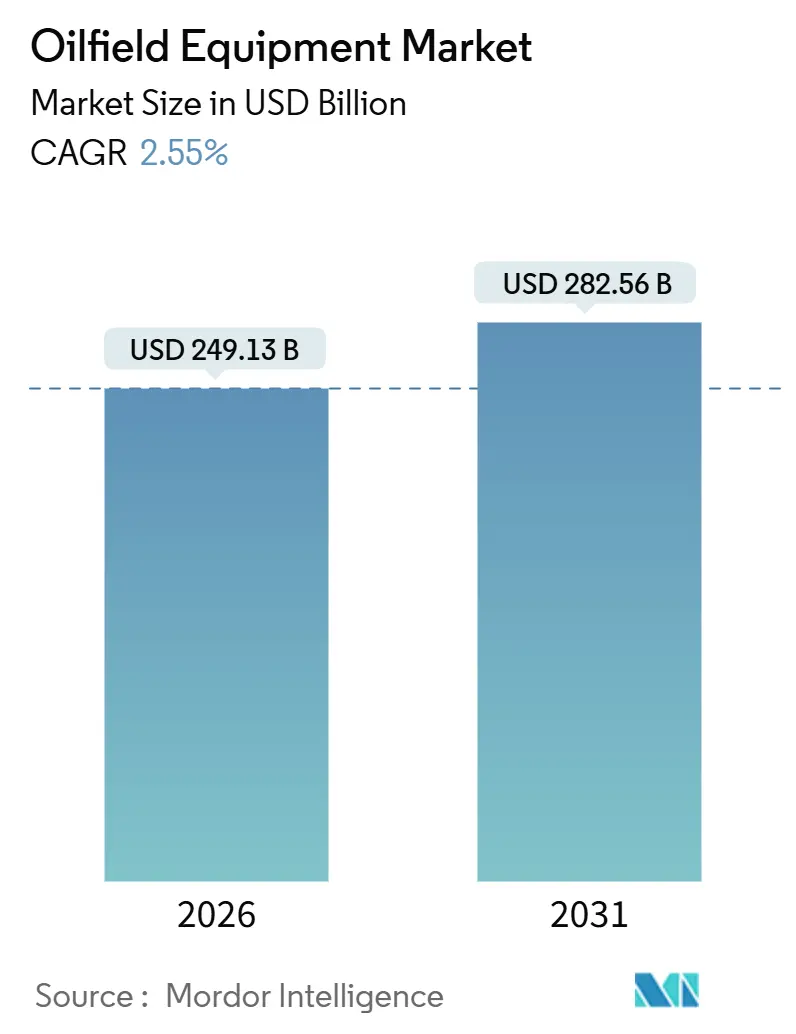

| Market Size (2026) | USD 249.13 Billion |

| Market Size (2031) | USD 282.56 Billion |

| Growth Rate (2026 - 2031) | 2.55% CAGR |

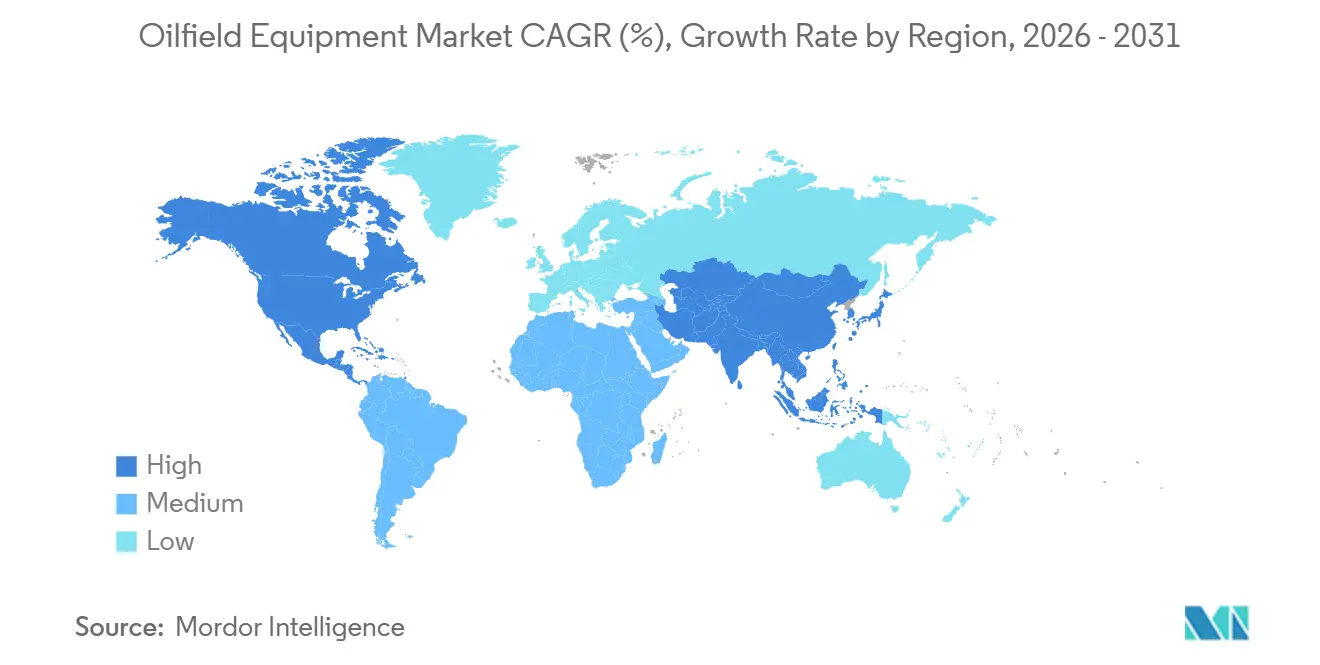

| Fastest Growing Market | North America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oilfield Equipment Market Analysis by Mordor Intelligence

The Oilfield Equipment Market size is estimated at USD 249.13 billion in 2026, and is expected to reach USD 282.56 billion by 2031, at a CAGR of 2.55% during the forecast period (2026-2031).

Capital is gravitating toward higher-quality reservoirs, so operators are channeling budgets into ultra-deepwater developments, long-lateral shale wells, and retrofit programs that comply with methane emission rules. Longer lead times and larger upfront CAPEX characterize offshore projects, yet payback improves when Brent trades in the USD 70-85 range, a dynamic that convinced majors to approve deepwater schemes in Guyana, Brazil, and West Africa. In North America, shale producers are drilling laterals that average 3.2 km, which raises demand for heavy-duty completion gear and higher-pressure blowout preventers. Simultaneously, the U.S. Environmental Protection Agency’s methane rule, effective in 2025, accelerates replacement cycles for pneumatic controllers and legacy wellhead assemblies.

Key Report Takeaways

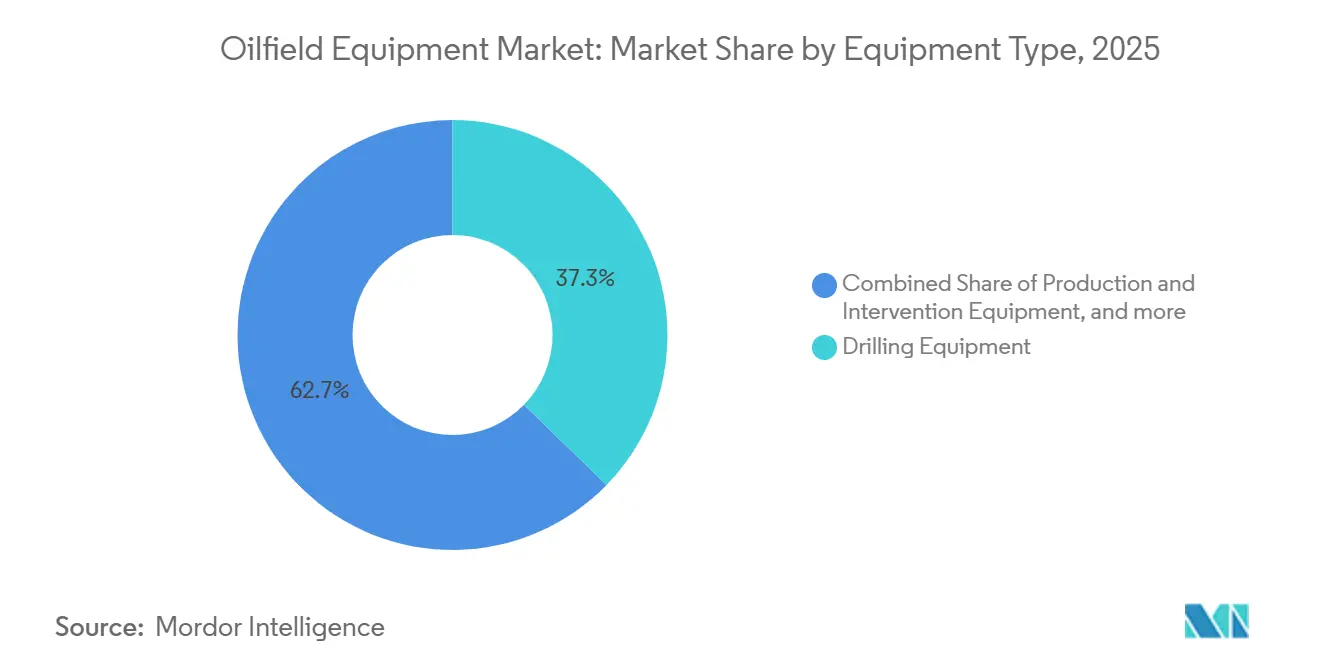

- By equipment type, drilling equipment captured 37.3% of the oilfield equipment market share in 2025 and is projected to expand at a 2.6% CAGR to 2031.

- By location, onshore operations held 66.3% of the oilfield equipment market size in 2025, while offshore operations showed the highest growth at 3.9% through 2031.

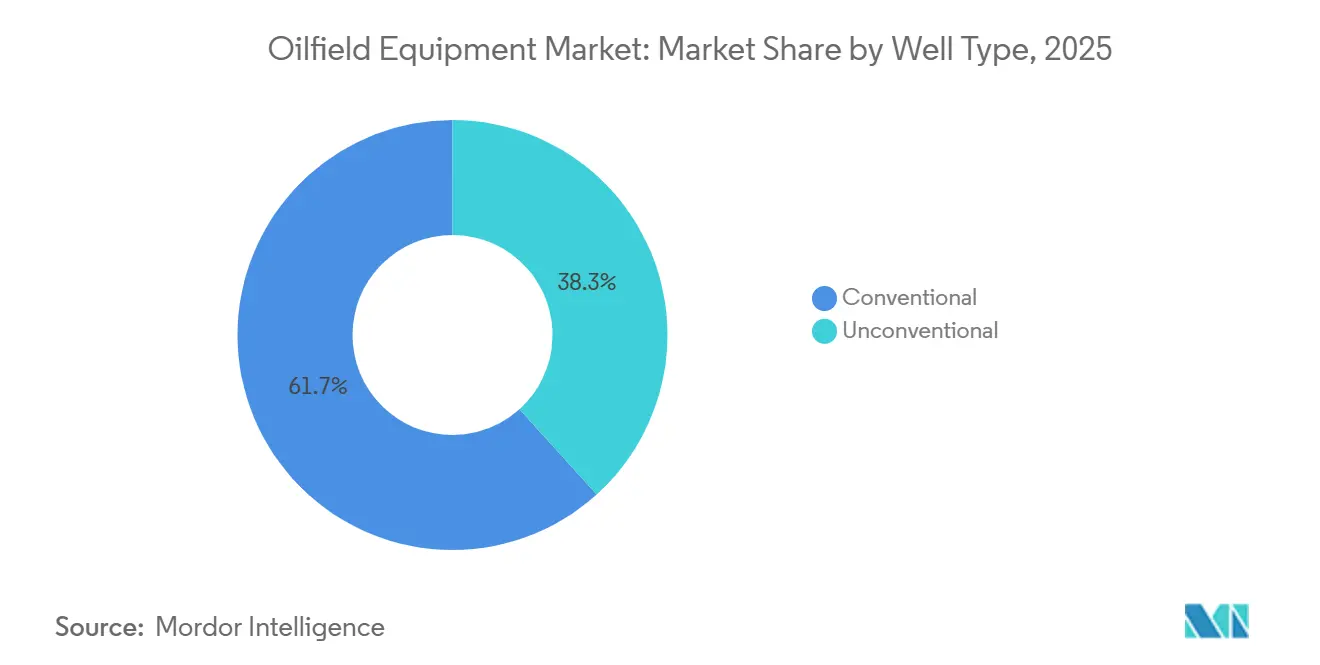

- By well type, conventional wells commanded 61.7% of the oilfield equipment market size in 2025; unconventional wells are advancing at a 3.7% CAGR through 2031.

- By geography, North America led with 36.3% revenue share in 2025, and it also records the strongest regional CAGR at 3.4% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Oilfield Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising deep- & ultra-deepwater project pipeline | 0.8% | Global, concentrated in Brazil, Guyana, West Africa, Gulf of Mexico | Medium term (2-4 years) |

| CAPEX recovery and rig-count rebound post-2024 | 0.7% | North America, Middle East, with spillover to APAC | Short term (≤ 2 years) |

| Methane-leak rules accelerating demand for low-emission BOPs | 0.5% | North America & EU, early adoption in Australia | Medium term (2-4 years) |

| Surging APAC energy demand feeding new field developments | 0.6% | APAC core (China, India, ASEAN), spillover to Australia | Long term (≥ 4 years) |

| Expansion of shale & tight-oil drilling activity | 0.6% | North America (Permian, Eagle Ford, Bakken), Argentina (Vaca Muerta), China (Sichuan Basin) | Short term (≤ 2 years) |

| Tariff-led reshoring & localization of OCTG/valves manufacturing | 0.4% | North America (US, Mexico, Canada), selective impact in EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Deep- & Ultra-Deepwater Project Pipeline Propels Subsea Equipment Demand

Final investment decisions for 18 deepwater projects over USD 1 billion each were reached in 2024-2025, double the tally from the prior two-year period. Brazil’s pre-salt developments, such as Búzios 9 and Mero 4, alone require 64 subsea trees and extensive flexible risers, sustaining large orders for high-specification production hardware. Guyana’s Stabroek Block added Hammerhead, Pluma, and Pickerel, all demanding sixth-generation drillships and 20,000 psi BOPs that only a handful of suppliers can provide. West Africa re-entered the queue with TotalEnergies’ USD 6 billion Kaminho project that relies on subsea tiebacks to FPSOs, which curbs breakeven to USD 35 per barrel. Regulatory influence is rising; Norway now mandates dual-shear-ram BOPs for wells deeper than 1,500 m, a benchmark insurers increasingly require worldwide.

CAPEX Recovery and Rig-Count Rebound Post-2024 Unlock Pent-Up Equipment Orders

Global upstream CAPEX climbed to USD 525 billion in 2025, a 14% jump from 2024, ending a five-year contraction.[1]International Energy Agency, “World Energy Investment 2025,” iea.org North American land-rig counts averaged 621 in 2025, up 9%, while floater utilization rose to 84%, driving day rates for ultra-deepwater drillships above USD 450,000. National Oilwell Varco’s drilling-equipment backlog hit USD 2.1 billion at year-end 2025, covering BOPs and top-drive systems scheduled through 2027. Producers increasingly select automated pipe-handling and real-time downhole sensors that shorten well-construction timelines by up to 20%. Middle-East NOCs ordered 52 new land rigs in 2025 to meet gas development goals, reinforcing demand for high-specification rig packages.

Methane-Leak Rules Accelerating Demand for Low-Emission BOPs and Wellhead Systems

The U.S. EPA’s methane rule obliges operators to eliminate routine flaring by 2030 and to install continuous leak detection on every well by 2027, spawning a retrofit market covering around 180,000 legacy wells.[2]United States Environmental Protection Agency, “Final Methane Rule Factsheet,” epa.gov The European Union’s analogous regulation applies to imported gas, forcing exporters to upgrade equipment or risk losing market access. Baker Hughes introduced the Aptara low-emission BOP in June 2025, using electric actuators that remove hydraulic leaks and cut maintenance by 40%. Weatherford’s zero-emission wellhead system, launched in September 2025, integrates real-time pressure monitoring, aligning with tighter leak-detection mandates. Regulators in Australia now require monthly Scope 1 reporting, nudging operators toward early equipment upgrades.

Surging APAC Energy Demand Feeding New Field Developments and Equipment Orders

Asia Pacific oil demand is projected to rise 2.1% annually through 2031, sustaining a wave of exploration and development.[3]International Energy Agency, “Oil Market Report 2025,” iea.org CNOOC sanctioned four South China Sea projects in 2025 that together need 48 subsea trees and three wellhead platforms. ONGC ordered 12 offshore rigs for the Krishna-Godavari Basin to exploit prospective gas volumes topping 1 TCF. ASEAN participation is led by the USD 3.5 billion Kasawari gas scheme in Malaysia, which incorporates subsea compression to lengthen field life. Australia’s Scarborough gas project reached FID in 2024 and requires floating production units plus 430 km of pipelines that must satisfy carbon-capture readiness standards. China now insists that all new offshore platforms include carbon-capture provisions, lifting equipment CAPEX by 5-7% but securing future emissions-trading revenues.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oil-price volatility undermining E&P budgets | -0.6% | Global, acute in North America shale and marginal offshore fields | Short term (≤ 2 years) |

| Rising environmental-compliance costs | -0.3% | Global, most stringent in EU, North America, Australia; emerging in APAC | Medium term (2-4 years) |

| High offshore equipment CAPEX & long payback cycles | -0.4% | Offshore-focused regions: North Sea, West Africa, deepwater Gulf of Mexico | Medium term (2-4 years) |

| Semiconductor/alloy supply-chain bottlenecks delaying deliveries | -0.3% | Global, acute in markets dependent on Asian semiconductor supply and specialty alloy imports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Oil-Price Volatility Undermining E&P Budgets and Project Sanctioning

Brent crude ranged from USD 68 to USD 88 in 2025, with swings above 15% each quarter that compressed planning horizons and delayed 22% of global FIDs during the second quarter when prices dipped below USD 70.[4]U.S. Energy Information Administration, “Short-Term Energy Outlook 2025,” eia.gov Permian operators idle rigs quickly when margins narrow, creating uneven demand for completion gear. Deepwater ventures require oil above USD 60 to yield 15% returns, and volatility can defer sanction decisions by up to 18 months, dragging equipment orders with them. TechnipFMC reported that 30% of its 2025 subsea backlog contained price-contingent clauses allowing delivery deferral when Brent falls below thresholds. Smaller independents cut exploration budgets by 18% on average in 2025, reducing seismic and drilling activity.

High Offshore Equipment CAPEX and Long Payback Cycles Constraining Investment

A sixth-generation drillship costs USD 650-750 million, and a four-well subsea tieback averages USD 180 million, making offshore developments three to four times as capital-intensive as onshore wells. Payback typically stretches 7-10 years, which is unattractive when interest rates push the weighted average cost of capital above 9%. North Sea capital spending fell 11% in 2025 despite stable oil prices because aging assets and decommissioning liabilities deterred new investment. Angola and Nigeria lost operator interest in deepwater blocks due to fiscal regimes that do not cover equipment CAPEX and risk premiums. Suppliers respond with modular templates that can be relocated, cutting fabrication time by 30%, and with leasing models for ROVs and subsea tools that shift spending from CAPEX to OPEX. Norway offers tax incentives that offset some of the cost burden, whereas Brazil’s local-content rules raise sourcing complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Automation Gives Drilling Equipment an Edge

Drilling equipment accounted for 37.3% of the oilfield equipment market in 2025 and is projected to grow at 2.6% through 2031, propelled by automated rig-floor systems that cut non-productive time. High-pressure, high-temperature wells in the Gulf of Mexico and the North Sea require 20,000 psi BOPs that carry price tags of USD 8-12 million higher than 15,000 psi units, supporting premium margins for certified suppliers. Production and intervention tools benefit from aging wells that need artificial lift, coiled tubing, and workover rigs, while completion equipment gains from dissolvable materials that remove cleanout runs and shave USD 200,000-400,000 per well. Competitive pressure is rising from Asian fabricators, yet premium connections and corrosion-resistant alloys allow Western mills to secure 15-20% price premiums in sour-gas environments.

Electric submersible pumps, intelligent rotary steerable systems, and real-time drilling analytics illustrate how digitalization is moving from pilot phase to standard practice. Operators report 12-18% reductions in drilling days when machine-learning platforms optimize bit weight and rotary speed, savings that compound over multi-well pad developments. The oilfield equipment market continues to reward manufacturers that embed digital interfaces and remote-monitoring capabilities into hardware, positioning drilling equipment for the highest growth among the major categories.

By Location: Offshore Momentum Outruns Onshore Scale

Onshore assets still dominate with 66.3% of revenue in 2025, yet offshore posts the fastest 3.9% CAGR to 2031 as Brazil, Guyana, and Mozambique underpin multi-billion-dollar floater programs. Petrobras plans to add 11 FPSOs between 2025-2029, each ordering subsea systems worth USD 400-600 million. Guyana’s Hammerhead FPSO, sanctioned in 2025, signals how integrated subsea-to-surface packages are becoming the procurement norm.

Onshore activity remains robust in the Permian, which averaged 11,200 wells per year during 2024-2025, translating into large orders for fracturing fleets, wellheads, and artificial-lift systems. Canada’s Montney and Duvernay basins gained momentum after new pipelines eased takeaway constraints, pushing drilling up 14% in 2025. Middle-East onshore fields are investing in enhanced oil recovery, demanding specialized pumps and separators. Differing regulations matter: Norway enforces subsea isolation valves on all new offshore wells, while U.S. onshore rules vary by state, complicating supply-chain planning.

By Well Type: Unconventional Wells Narrow the Gap

Conventional wells held 61.7% of revenue in 2025, yet the unconventional segment is growing at 3.7% annually, powered by long-lateral shale drilling in the United States and by rising hydraulic-fracturing adoption in Argentina and China. The oilfield equipment market size for unconventional wells is projected to rise as electric fracturing fleets cut fuel costs by 40% and remove diesel emissions, meeting both economic and ESG goals.

Argentina’s Vaca Muerta field secured a USD 2.5 billion drilling program for 180 horizontal wells scheduled through 2027, anchoring local demand for proppant logistics, plug-and-perf tools, and intelligent completion systems. China’s Sichuan Basin lifted shale-gas output 16% in 2025, aided by domestically produced fracturing pumps priced 30% below Western equivalents. In parallel, Middle-East giants are fitting intelligent well completions and downhole fiber optics on conventional wells to maximize recovery factors, which sustains a high baseline of equipment purchases.

Geography Analysis

North America generated 36.3% of 2025 revenue and shows the strongest 3.4% CAGR through 2031, supported by Permian consolidation, Gulf of Mexico lease auctions that yielded USD 382 million in high bids, and an uptick in Canadian oil sands drilling. The U.S. operated 621 active land rigs in 2025, while offshore output averaged 1.9 million bpd amid infrastructure upgrades that move breakevens toward USD 40-50 per barrel. Canada’s pipeline expansions unlocked incremental drilling in the Montney and Duvernay, and Mexico’s Zama field approaches peak output of 165,000 bpd in 2027, necessitating subsea kits and FPSO capacity.

The Middle East and Africa follow, buoyed by USD 80 billion in combined annual upstream investment from Saudi Aramco and ADNOC, including 40 new offshore rigs and significant gas-processing expansions. Nigeria and Angola struggle with fiscal terms that depress deepwater economics, yet the Niger Delta onshore projects carry on under improved security. Technology demand shifts toward modular rigs and aggressive digitalization as NOCs chase efficiency gains.

Asia Pacific is the fastest-moving consumer market, driven by China’s four new offshore schemes and India’s 12-rig procurement to accelerate Krishna-Godavari exploration. Malaysia’s Kasawari gas project and Australia’s Scarborough development strengthen regional subsea equipment orders, while Japan and South Korea invest in floating LNG regasification units requiring high-pressure pumps and mooring systems. South America rests on Brazil’s pre-salt plan for 64 subsea trees between 2025-2027, whereas Argentina’s Vaca Muerta pushes unconventional purchases. Europe shows divergence: UK North Sea spending fell 11% in 2025, but Norway approved 15 new developments outfitted with electrified platforms that reduce carbon intensity.

Competitive Landscape

The top five service majors, Schlumberger, Halliburton, Baker Hughes, Weatherford, and National Oilwell Varco, controlled about 48% of global revenue in 2025, but regional manufacturers in Asia and the Middle East offer 15-20% cost advantages on standardized equipment, pressuring margins. Digital acquisitions headline corporate strategy; Schlumberger paid USD 430 million for Aucerna in January 2025 to deepen its subsurface-software stack, while Halliburton rolled out the iCruise intelligent rotary steerable system that blends real-time formation data with automated drilling control.

Cost-focused challengers such as China’s Jereh Oilfield Services and India’s Aban Offshore win bids by underpricing Western counterparts on completion tools and workover rigs, especially in Asia and Africa. The legacy U.S. well count exceeds 1.8 million, yet only 12% have installed methane-abating hardware, signaling multiyear retrofit upside for providers with certified low-emission product lines. Technology partnerships grow: SparkCognition and Baker Hughes deployed AI-driven predictive maintenance that shortened unplanned downtime by 25%, improving equipment utilization.

Consolidation continues. Weatherford bought Altus Intervention to enlarge its well-intervention portfolio, and TechnipFMC merged subsea activities with Aker Solutions in a joint venture owning a USD 3.2 billion backlog. Suppliers must maintain API Specification 16A and ISO 13628 certifications, which elevate entry barriers and favor incumbents with global compliance footprints.

Oilfield Equipment Industry Leaders

Schlumberger Limited

Baker Hughes Company

Halliburton Company

Weatherford International PLC

National Oilwell Varco Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Baker Hughes (BKR), an energy technology firm, secured a multi-year contract with the Kuwait Oil Company (KOC). Under this agreement, Baker Hughes will supply advanced artificial lift systems, such as electrical submersible pumps (ESPs) and intelligent automation tools (FusionPro, Leucipa).

- November 2025: SLB (formerly known as Schlumberger) unveiled Tela, an advanced AI platform. Tela is engineered to automate and refine upstream energy tasks, such as interpreting well logs and forecasting drilling challenges. Functioning as a collaborative AI assistant, Tela spans the entire energy lifecycle, aiming to boost both productivity and safety.

- March 2025: The International Financial Services Centers Authority (IFSCA) announced plans to introduce oilfield equipment leasing in GIFT City, Gujarat, India. This initiative seeks to broaden the current leasing framework, which already covers ships and aircraft, to include oilfield equipment.

- October 2024: Petrobras awarded Baker Hughes Co. substantial contracts to deliver 77 km of flexible pipe systems for Brazil's pre-salt fields. This multi-year endeavor encompasses risers and flowlines essential for hydrocarbon extraction, as well as gas and water injection.

Global Oilfield Equipment Market Report Scope

Oilfield equipment refers to tools and machinery that are primarily useful in upstream operations such as exploration, drilling, and production processes. These are used in developing oilfield projects, both onshore and offshore. Oilfield equipment is chosen according to the application and offers precision.

The global oilfield equipment market is segmented by equipment type, location, well type, and geography. By equipment type, the market is segmented into drilling equipment, production and intervention equipment, completion equipment, and other equipment types. By location, the market is segmented into onshore and offshore. By well type, the market is segmented into conventional and unconventional. By geography, the market is segmented into North America, Europe, Asia Pacific, South America, and the Middle East and Africa. The report also covers the market sizes and forecasts for the global oilfield equipment market across major countries within each of these regions. For all segments, the market sizing and forecasts have been conducted on the basis of value (USD).

By Equipment Type

| Drilling Equipment |

| Production and Intervention Equipment |

| Completion Equipment |

| Other Equipment Types |

By Location

| Onshore |

| Offshore |

By Well Type

| Conventional |

| Unconventional |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Norway |

| United Kingdom | |

| Russia | |

| Netherlands | |

| Germany | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Iran | |

| Nigeria | |

| South Africa | |

| Rest of Middle East and Africa |

| By Equipment Type | Drilling Equipment | |

| Production and Intervention Equipment | ||

| Completion Equipment | ||

| Other Equipment Types | ||

| By Location | Onshore | |

| Offshore | ||

| By Well Type | Conventional | |

| Unconventional | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Norway | |

| United Kingdom | ||

| Russia | ||

| Netherlands | ||

| Germany | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Iran | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the oilfield equipment market in 2026 and how fast is it growing?

The market size stands at USD 249.13 billion in 2026 and is on course to reach USD 282.56 billion by 2031, expanding at a 2.55% CAGR.

Which equipment type holds the biggest revenue share?

Drilling equipment leads with a 37.3% share in 2025, benefiting from automation that cuts well-construction time and boosts safety.

Which region shows the highest growth momentum through 2031?

North America records the fastest regional 3.4% CAGR, underpinned by Permian shale activity and Gulf of Mexico deepwater leasing.

What driver most influences future spending on oilfield gear?

Rising deep- and ultra-deepwater projects, particularly in Brazil and Guyana, add +0.8% to forecast CAGR by expanding subsea equipment demand.

How are methane rules affecting equipment demand?

U.S. and EU methane regulations spur immediate retrofits of pneumatic controllers, low-emission BOPs, and real-time monitoring systems across about 180,000 wells.

Page last updated on: