User-Generated Content Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.63 Billion |

| Market Size (2031) | USD 43.92 Billion |

| Growth Rate (2026 - 2031) | 28.32% CAGR |

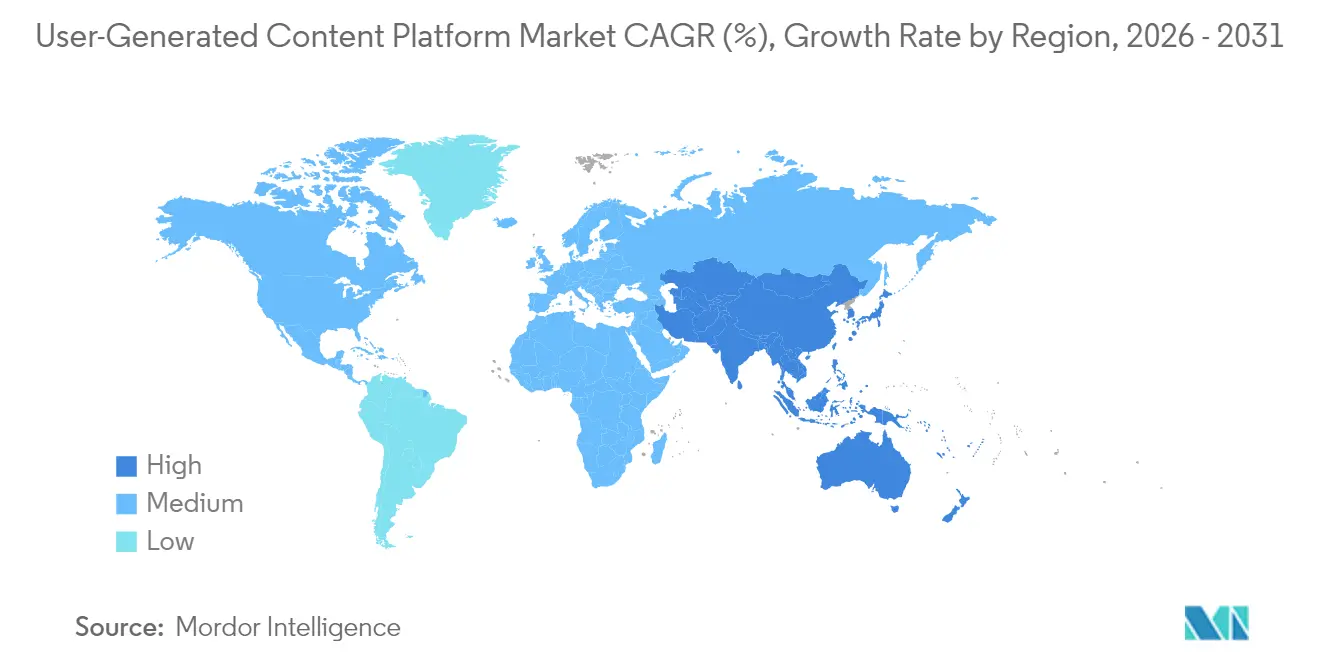

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

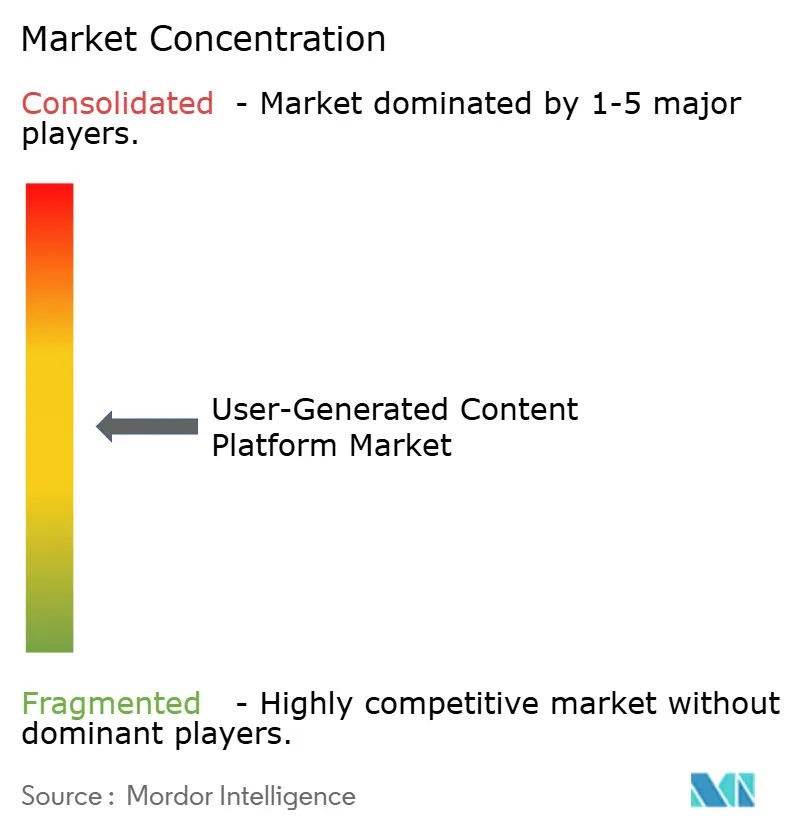

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

User-Generated Content Platform Market Analysis by Mordor Intelligence

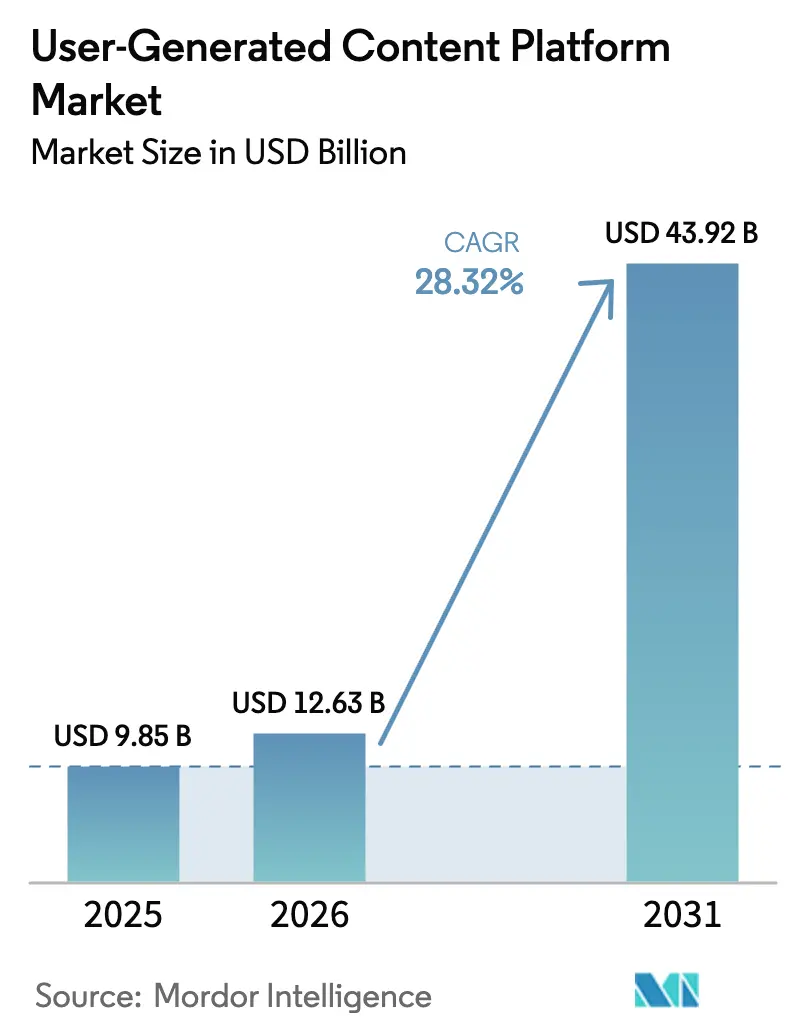

The user-generated content platform market size is expected to grow from USD 9.85 billion in 2025 to USD 12.63 billion in 2026 and is forecast to reach USD 43.92 billion by 2031 at 28.32% CAGR over 2026-2031. This dynamic growth comes as brands pivot from traditional advertising to community-driven storytelling that delivers 6.9 times higher engagement than branded content. Influencer-commerce momentum, short-form video proliferation, and AI-powered creator tools are steadily reshaping how enterprises capture authentic consumer voices. Platform providers are prioritizing cloud-native architectures that streamline scalable, real-time moderation while lowering entry barriers for small and medium enterprises. Meanwhile, regulatory scrutiny is steering investment toward privacy-preserving analytics and automated compliance capabilities that differentiate offerings across the user-generated content platform market.

Key Report Takeaways

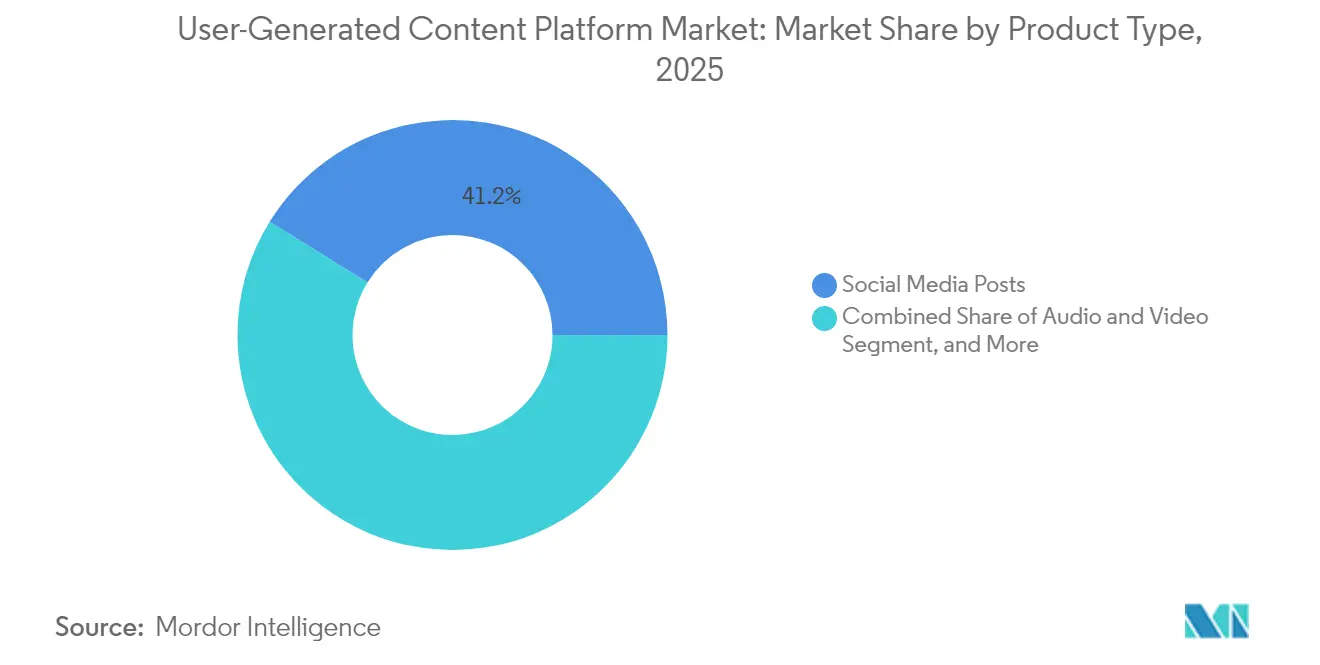

- By product type, social media posts led with 41.18% revenue share in 2025 in the user-generated content platform market, whereas live-streaming is advancing at a 30.12% CAGR through 2031.

- By end-user segment, large enterprises commanded 43.21% of the 2025 user-generated content platform market share, while SMEs are projected to grow at 30.25% CAGR to 2031.

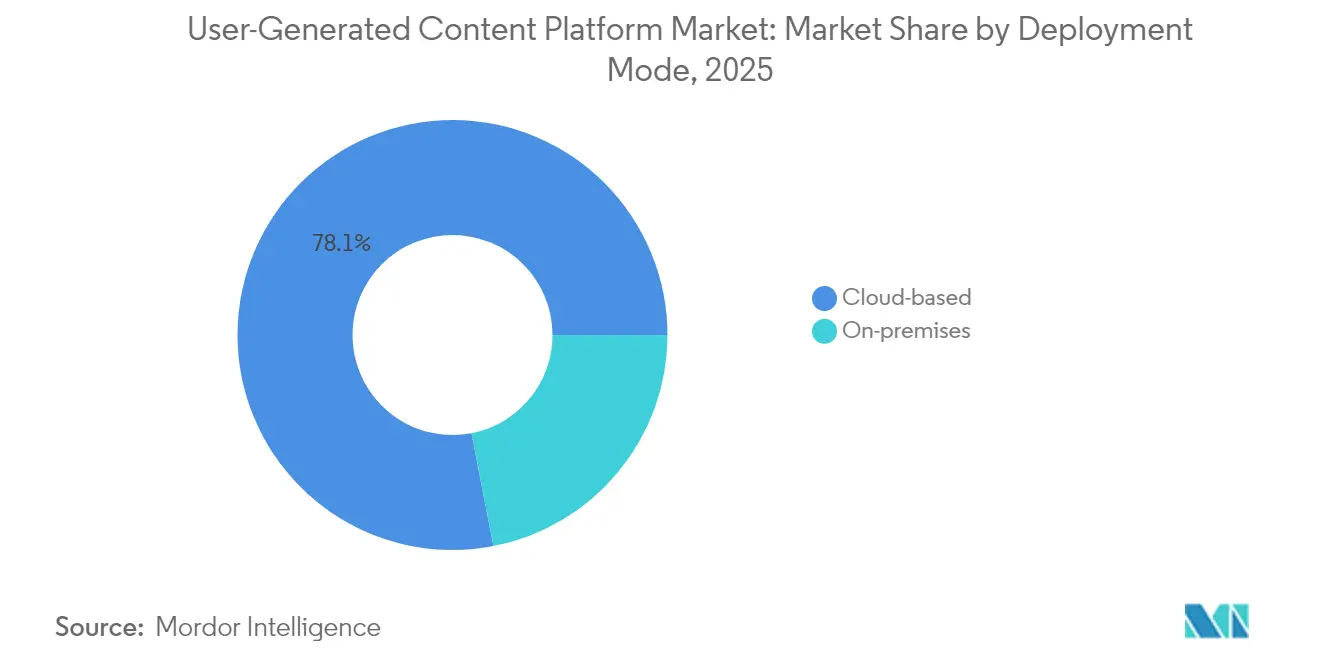

- By deployment mode, cloud-based solutions accounted for 78.05% of the user-generated content platform market size in 2025 and are set to rise at a 31.02% CAGR over the forecast horizon.

- By revenue model, the advertising-supported approach retained 61.15% share in 2025 in the user-generated content platform market; freemium offerings show the fastest climb at 30.86% CAGR through 2031.

- By geography, North America contributed 38.12% of 2025 revenue in the user-generated content platform market, but the Middle East and Africa region is poised for a 30.08% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global User-Generated Content Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Influencer-driven commerce acceleration | +8.2% | Global, with concentration in North America and APAC | Medium term (2-4 years) |

| Short-form video platforms fueling UGC volumes | +7.8% | Global, led by APAC and North America | Short term (≤ 2 years) |

| Social-commerce integrations by major retailers | +6.4% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Generative-AI-assisted content creation | +5.9% | Global, early adoption in North America and EU | Long term (≥ 4 years) |

| Web3 token-based creator monetisation models | +4.3% | Global, strongest in APAC and North America | Long term (≥ 4 years) |

| Privacy-centric first-party data advantages | +3.7% | EU and North America, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Influencer-Driven Commerce Acceleration

Brands fusing creator networks with integrated checkout features are shortening purchase funnels and driving measurable ROI improvements. Influencer marketing platforms generated USD 21 billion in 2024 revenue, with micro-influencers producing 60% higher engagement than macro creators. Enterprise demand for scalable identification of niche creators is propelling investment in AI-based discovery engines. Shoppable content integrations are eliminating an average of 2.3 customer touchpoints, reinforcing the strategic imperative for real-time UGC activation. Updated FTC endorsement guidelines are encouraging platforms that automate disclosure compliance, boosting trust and reinforcing growth across the user-generated content platform market.

Short-Form Video Platforms Fueling UGC Volumes

Platforms processed more than 720,000 video hours daily in late 2024.[1]“Video Content Surge Drives Platform Infrastructure Investment,” Financial Times, ft.com This surge increases the need for intelligent curation systems that surface relevant clips for brands drowning in content abundance. Vertical-video formats optimized for mobile use now deliver 40% higher engagement, prompting platforms to redeploy recommendation algorithms. Meta’s September 2024 AI studio rollout accelerated creator productivity and preserved hallmark authenticity, fueling additional demand for analytics that validate performance while filtering deceptive content. These forces collectively expand platform stickiness and monetization opportunities inside the user-generated content platform market.

Social-Commerce Integrations by Major Retailers

Retailers embedding UGC into product pages experience tangible gains: Walmart reported 28% higher conversions and 15% fewer returns during 2024 when showcasing customer videos. Complex rights management, speedy moderation, and unified analytics requirements are driving platform consolidation as merchants favor end-to-end solutions. Privacy laws such as GDPR inform consent workflows and data portability features that are now core purchasing criteria. Providers delivering turnkey integrations that respect privacy and support omnichannel merchandising continue to outpace generic offerings within the user-generated content platform market.

Generative-AI-Assisted Content Creatio

Meta’s Movie Gen announcement in October 2024 underscored how text-to-video tools can lower production barriers while introducing authenticity concerns. Early detection frameworks boast 94% accuracy in flagging synthetic clips, reducing misinformation risks and elevating trust. Fragmented global regulation, EU mandates explicit AI labeling, whereas U.S. rules concentrate on preventing deception, creates compliance complexity that only technology-rich platforms can manage. Long-term, generative AI is likely to expand creator pools and diversify content formats, lifting engagement and revenue across the user-generated content platform market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Brand-safety and content-moderation costs | -4.8% | Global, highest impact in EU due to DSA requirements | Short term (≤ 2 years) |

| Rising regulatory scrutiny on data use | -3.2% | EU and North America, expanding globally | Medium term (2-4 years) |

| Decline of third-party cookies reducing ad yields | -2.1% | Global, most severe in North America and EU | Short term (≤ 2 years) |

| Generative-AI misinformation risks | -1.7% | Global, regulatory focus in EU and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Brand-Safety and Content-Moderation Costs

Industry-wide moderation spend surpassed USD 25 billion in 2024, with more than 1 million human moderators supplementing AI filters. The EU Digital Services Act heightened obligations, forcing sophisticated classification and 24-hour takedown windows that add USD 2.8 billion in annual compliance expenses for dominant firms. AI tools trim per-item costs by 35%, yet nuanced contextual evaluation still demands human oversight, especially for enterprise campaigns where a single unsafe placement can void contracts. These operating burdens temper profitability and slow near-term expansion in the user-generated content platform market.

Rising Regulatory Scrutiny on Data Use

The demise of third-party cookies reduced advertising yield by 20-30% on major networks, spurring urgent pivots toward first-party data strategies.[2]Privacy Regulations Impact on Digital Advertising,” Financial Times, ft.com GDPR, CCPA, and emerging state statutes oblige continuous investment in consent orchestration and auditing infrastructure. Smaller platforms, lacking dedicated legal teams, face proportionally heavier fixed costs, elevating barriers to entry. Cross-border data transfer uncertainty further complicates architecture decisions, nudging some providers toward localization that fragments scale advantages and constrains margin expansion inside the user-generated content platform market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Social Media Posts Sustain Leadership, Live-Streaming Rises

Social media posts contributed 41.18% of 2025 revenue, underscoring their entrenched role in brand storytelling. Live-streaming boasts the highest 30.12% CAGR through 2031, reflecting consumer appetite for real-time interaction and tipping-based monetization. Gaming-centric broadcasts produced USD 4.2 billion in creator revenue during 2024. Audio-video hybrids continue steady growth as production kits become affordable. Ratings and reviews remain foundational trust signals, especially when embedded in e-commerce checkouts. Blogs, while mature, are regaining momentum through AI-enhanced multimedia inserts.

Cloud-native AI tagging systems ensure compliance with evolving classification standards set by the EU’s Digital Services Act, reducing manual workload. Vertical video algorithms optimized for smartphones are lifting dwell times and click-throughs. As these mobile-first experiences proliferate, providers capable of cross-format orchestration gain share, sustaining the user-generated content platform market expansion.

By End-User: Enterprise Dominance, SME Acceleration

Large enterprises held 43.21% of 2025 revenue, leveraging integrations with CRM and martech stacks to measure full-funnel ROI. SMEs, however, post a 30.25% CAGR to 2031 as subscription tiers remove upfront investment hurdles. Authentic customer photos and videos drive 45% higher SME engagement than brand-authored assets, closing performance gaps with larger competitors.

Enterprise buyers demand robust brand-safety dashboards and API-level data transfers for attribution modeling. SMEs prioritize quick onboarding, guided workflows, and bundled rights management. Platforms offering tiered configurations appease both cohorts, broadening the user-generated content platform market addressable base.

By Deployment Mode: Cloud Ascendancy

Cloud deployments represented 78.05% of the 2025 user-generated content platform market size, advancing at 31.02% CAGR on scalability and instant global reach advantages. Elastic resource provisioning accommodates viral content spikes without service degradation. Hybrid architectures are emerging where sensitive data remains on-premise while compute-heavy rendering and moderation shift to cloud edge nodes.

Edge acceleration lowers latency for live-streams and delivers uniform quality in bandwidth-constrained geographies. Region-specific clouds address data sovereignty, boosting adoption among privacy-minded enterprises. Collectively, these factors cement cloud’s dominance within the user-generated content platform market.

By Revenue Model: Advertising Holds Sway, Freemium Accelerates

Advertising-supported platforms captured 61.15% share in 2025, leveraging mature targeting ecosystems. Freemium models grow fastest at 30.86% CAGR, as illustrated by Character.AI’s pivot that quadrupled active users without revenue dilution. Subscription tiers anchor predictable enterprise cash flows, while transaction fees tie platform gains to merchant success.

Hybrid monetization now prevails: ad-funded reach underpins creator discovery, whereas premium analytics or exclusive content drive incremental upsells. Contextual advertising and first-party audience pools mitigate cookie deprecation, sustaining revenue resilience across the user-generated content platform market.

Geography Analysis

North America’s user-generated content platform market size benefited from USD-denominated brand budgets and broad enterprise SaaS penetration, sustaining higher average revenue per user. The region’s stringent brand-safety demands foster advanced moderation tooling, elevating barrier-to-entry for smaller competitors. Ongoing state privacy bills create parallel compliance tracks that platforms must harmonize without sacrificing agility.

Asia-Pacific’s explosive content volume and creator population underpin a vibrant competitive field. Localized payment rails and super-app ecosystems catalyze micro-transactions within live-streams, driving monetization innovation. Government support programs in South Korea and Indonesia subsidize digital-skills training, expanding the creator base and demand for platform services. However, content censorship guidelines require adaptable classification engines to avert takedowns.

The Middle East and Africa records the highest forecast CAGR, propelled by smartphone affordability and carrier-backed zero-rating of social platforms that amplify reach. E-commerce rollouts across Gulf Cooperation Council states integrate shoppable UGC feeds, translating social discovery into purchase at unprecedented speed. Local languages and dialects challenge global AI filters, incentivizing regional partnerships that supply contextual training data. Collectively, divergent regional dynamics reinforce the heterogeneity of the global user-generated content platform market.

Competitive Landscape

Consolidation is redefining vendor standings as Getty Images combined with Shutterstock in a USD 3.7 billion deal, creating a multimedia behemoth blending stock and real-time UGC. Disney’s USD 1.5 billion stake in Epic Games embeds metaverse storytelling tools that marry entertainment franchises with creator-built worlds. Meanwhile, blockchain-native upstarts like The Sandbox secured USD 20 million to pursue decentralized creator monetization, challenging centralized incumbents with tokenized revenue sharing.

AI leadership now differentiates offerings: predictive performance scoring, automated rights clearance, and real-time harmful-content detection augment brand confidence. Platforms excelling at privacy-compliant first-party data capture gain negotiating leverage with advertisers grappling with signal loss. Conversely, legacy providers anchored to on-premise codebases confront modernization urgency as cloud-native entrants iterate faster.

White-space opportunities persist in regulated verticals, healthcare, finance, education, where bespoke compliance logic deters horizontal providers. Vendors crafting domain-specific ontologies and auditable content trails position for premium pricing and sticky enterprise contracts. Against this backdrop, providers balancing rapid feature shipping with escalating compliance demands secure share within the evolving user-generated content platform market.

User-Generated Content Platform Industry Leaders

Grin Technologies Inc.

Bazaarvoice Inc.

CrowdRiff Inc.

Monotype Imaging Holdings Inc.

Yotpo Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Meta unveiled Movie Gen, an AI video generator that converts text prompts into high-quality clips, heralding a new era of AI-assisted UGC workflows.

- September 2024: Perplexity AI tabled a USD 50 billion offer for TikTok’s U.S. operations, spotlighting geopolitical risk and strategic UGC value.

- August 2024: Getty Images finalized its USD 3.7 billion merger with Shutterstock, consolidating visual UGC and AI creation capabilities.

- July 2024: Disney invested USD 1.5 billion in Epic Games to advance metaverse-integrated UGC experiences.

Global User-Generated Content Platform Market Report Scope

A User-Generated Content Platform is an online website or platform that enables users to create, upload, share, and interact with various types of content. User-generated content consists of original, brand-specific content created by users and published on social media or other channels. Many types of UGC are included, such as images, videos, reviews, testimonials, or even podcasts.

The user-generated content platform market is segmented by product type (blogs, websites, advertising and promotions, social media, audio and video, and others), by end-user (individual, enterprises), and by geography.

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Blogs |

| Social Media Posts |

| Audio and Video |

| Ratings and Reviews |

| Live-Streaming |

| Individuals |

| Small and Medium Enterprises |

| Large Enterprises |

| Cloud-based |

| On-premise / Private Cloud |

| Advertising-supported |

| Subscription / SaaS |

| Freemium and Transaction-based |

| North America |

| South America |

| Europe |

| Asia-Pacific |

| Middle East and Africa |

| By Product Type | Blogs |

| Social Media Posts | |

| Audio and Video | |

| Ratings and Reviews | |

| Live-Streaming | |

| By End-user | Individuals |

| Small and Medium Enterprises | |

| Large Enterprises | |

| By Deployment Mode | Cloud-based |

| On-premise / Private Cloud | |

| By Revenue Model | Advertising-supported |

| Subscription / SaaS | |

| Freemium and Transaction-based | |

| By Geography | North America |

| South America | |

| Europe | |

| Asia-Pacific | |

| Middle East and Africa |

Key Questions Answered in the Report

How large is the user-generated content platform market in 2026?

The market is valued at USD 12.63 billion in 2026 and is projected to hit USD 43.92 billion by 2031 at a 28.32% CAGR.

Which product segment is growing fastest?

Live-streaming leads with a 30.12% CAGR to 2031, reflecting heightened demand for real-time creator-audience interaction.

Why are SMEs adopting UGC platforms so rapidly?

Cloud-based subscription tiers lower entry costs and deliver 45% higher engagement from authentic customer content compared with branded assets.

How does regulation affect platform growth?

EU and U.S. privacy laws increase compliance spending and push providers toward first-party data strategies that preserve targeting effectiveness.

What region offers the highest growth potential?

The Middle East and Africa region is forecast to grow at 30.08% CAGR through 2031, driven by mobile-first adoption and expanding social commerce.

Page last updated on: