Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

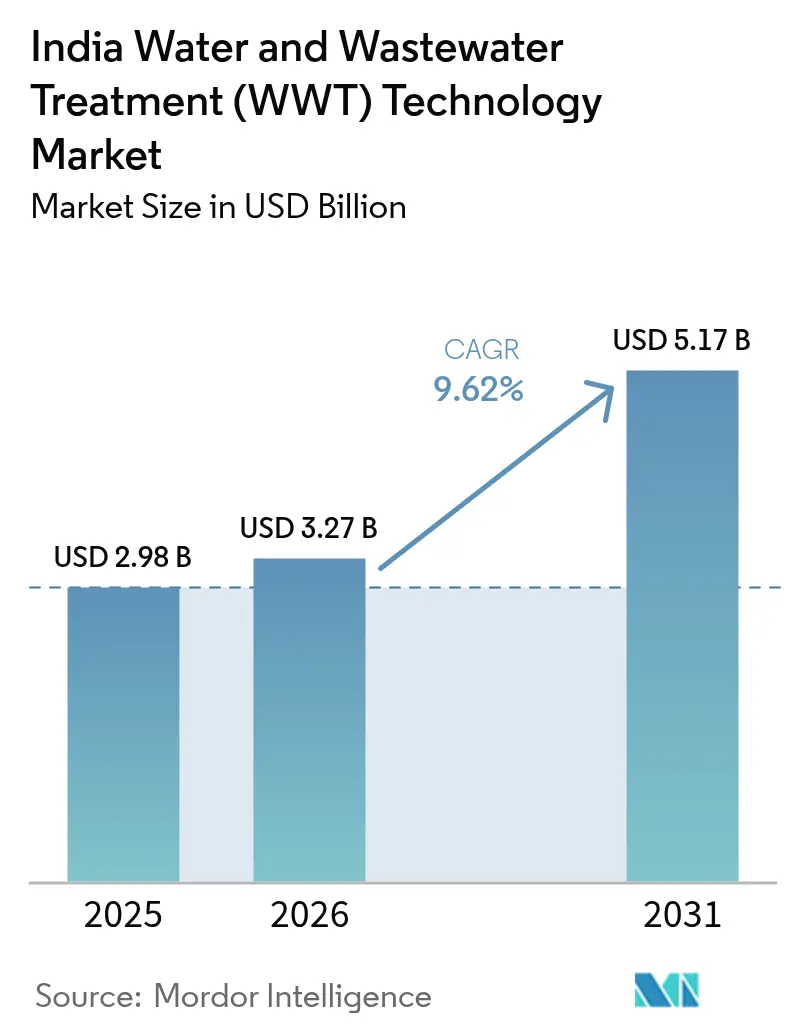

| Base Year Market Size (2025) | USD 2.98 Billion |

| Market Size (2026) | USD 3.27 Billion |

| Market Size (2031) | USD 5.17 Billion |

| Growth Rate (2026 - 2031) | 9.62% CAGR |

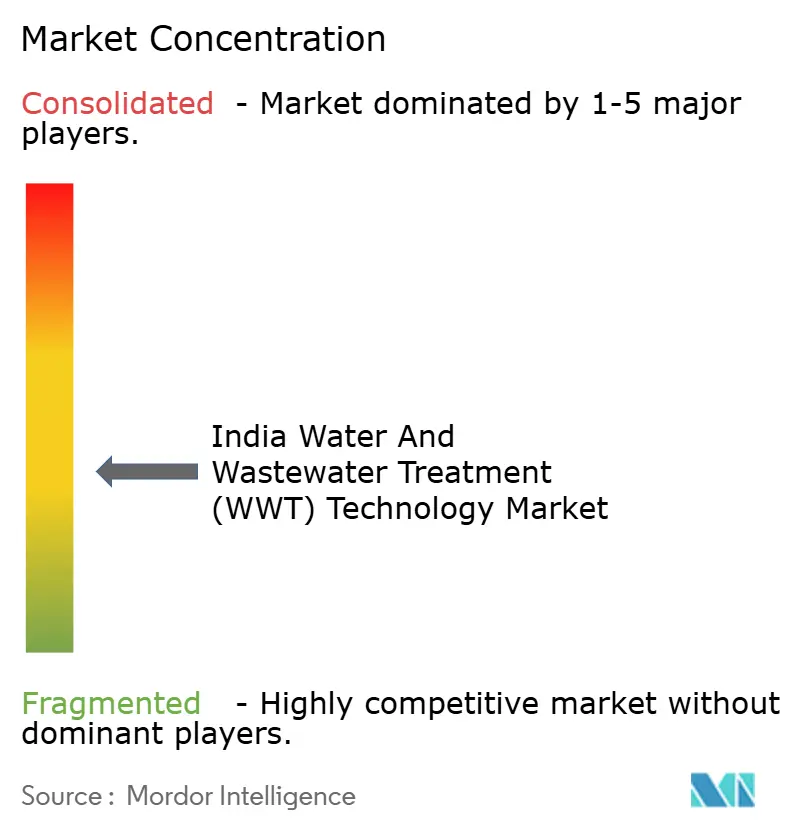

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Water And Wastewater Treatment (WWT) Technology Market Analysis by Mordor Intelligence

The India Water and Wastewater Treatment Technology Market size is projected to be USD 2.98 billion in 2025, USD 3.27 billion in 2026, and reach USD 5.17 billion by 2031, growing at a CAGR of 9.62% from 2026 to 2031. Escalating freshwater scarcity, state-level zero-liquid-discharge (ZLD) penalties, and sovereign programs such as AMRUT 2.0 are steering utilities and industries toward tertiary reuse modules that convert wastewater into an alternative raw-water source, thereby deepening the India water and wastewater treatment technology market across municipal and industrial corridors. Industrial decarbonization timelines tied to ESG-linked green bonds further reinforce this trajectory by monetizing reuse performance and lowering borrowing costs for plants that exceed ZLD benchmarks, a development that raises the addressable India water and wastewater treatment technology market for advanced biological and membrane systems. Semiconductor and green-hydrogen anchor projects in Gujarat and Karnataka demand ultra-pure water specifications that conventional reverse-osmosis (RO) alone cannot meet, which expands the India water and wastewater treatment technology market for polishing, electrodeionization, and brine-management packages. Meanwhile, fragmented municipal procurement and cultural hesitancy toward greywater reuse remain near-term drags, yet rising non-compliance penalties have begun to outweigh these frictions, catalyzing incremental contracts that keep the India water and wastewater treatment technology market on a double-digit growth path.

Key Report Takeaways

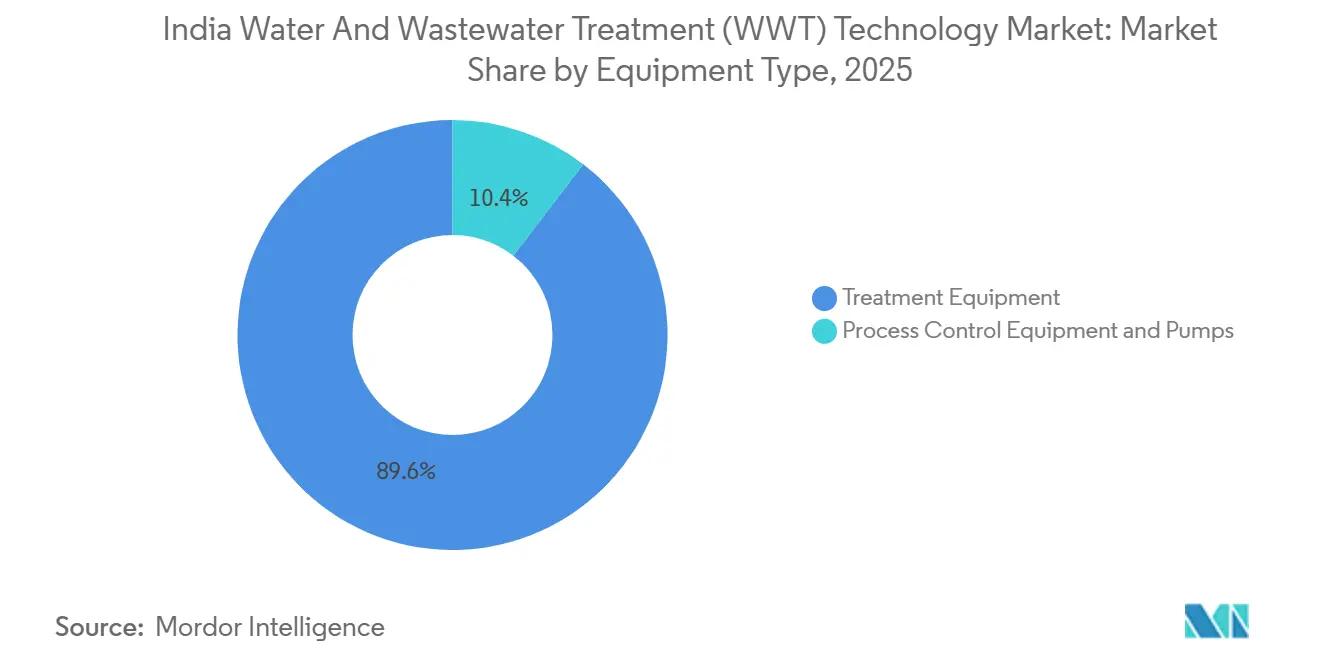

- By equipment type, Treatment Equipment led with 89.59% of the India water and wastewater treatment technology market share in 2025. Process Control Equipment and Pumps are projected to expand at an 11.25% CAGR through 2031, the fastest growth among equipment categories.

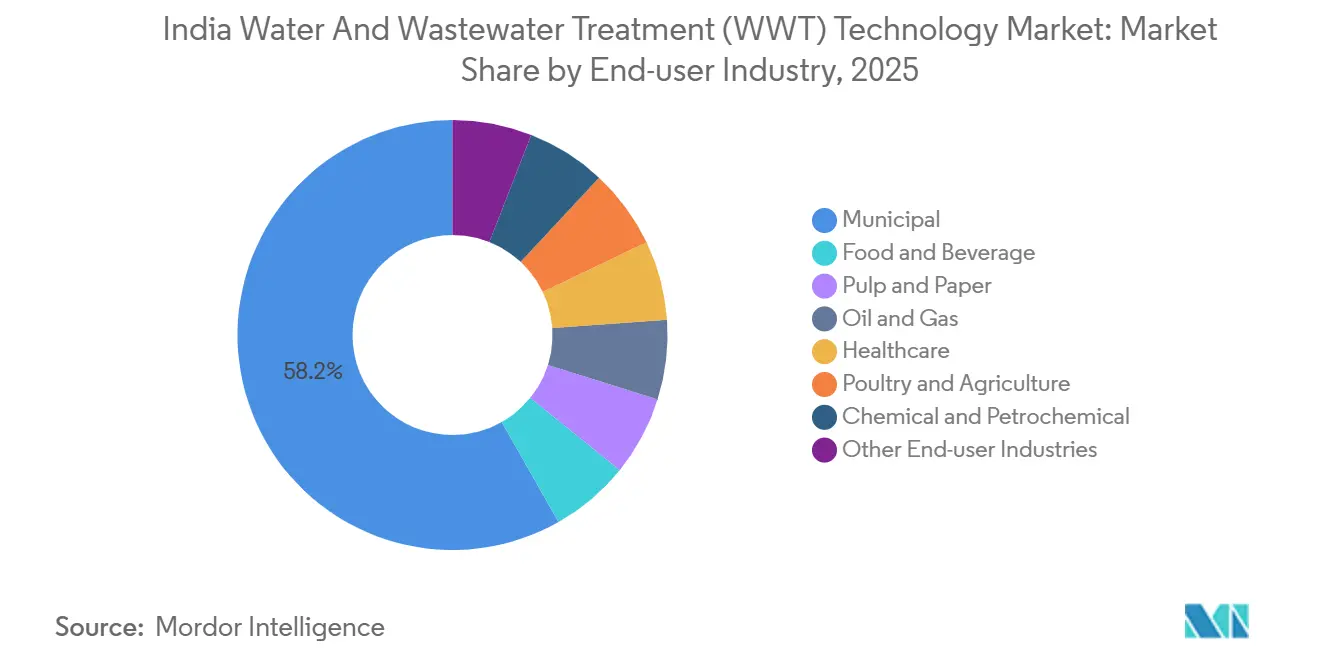

- By end-user industry, Municipal applications held 58.22% share of the India water and wastewater treatment technology market size in 2025. Healthcare end-users are expected to register the quickest 10.72% CAGR between 2026 and 2031 as antibiotic-residue caps tighten.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Water And Wastewater Treatment (WWT) Technology Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying scarcity of per-capita freshwater reserves | +2.1% | National, acute in Gujarat, Rajasthan, Karnataka | Medium term (2-4 years) |

| Stricter Zero-Liquid-Discharge mandates for red industries | +2.5% | Maharashtra, Gujarat, Tamil Nadu industrial belts | Short term (≤ 2 years) |

| Flagship programmes accelerating tertiary-reuse capacity | +2.8% | National, concentrated in AMRUT 2.0 cities | Medium term (2-4 years) |

| Surge in ESG-linked green bonds tied to wastewater-recycling KPIs | +1.3% | Tier-1 cities, municipal corporations with credit ratings | Long term (≥ 4 years) |

| Green-hydrogen and semiconductor projects demanding ultra-pure process water | +1.5% | Gujarat, Karnataka, Telangana industrial corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Scarcity of Per-Capita Freshwater Reserves

In 2025, per-capita freshwater availability dipped below the United Nations' water-stress threshold. This spurred expansions in captive Zero Liquid Discharge (ZLD) plants, which now recycle effluent into process water for sectors like textiles, leather, and pharmaceuticals. The Tiruppur knitwear hub and Kanpur tanneries invested significantly to ensure uninterrupted operations, signaling that scarcity rather than pure compliance now determines budget allocations. Shipments of Reverse Osmosis (RO) membranes for industrial reuse grew significantly year-on-year. This growth notably eclipsed the expansion in municipal wastewater capacity, highlighting a pronounced industrial shift in India's water and wastewater treatment technology landscape. With many major cities facing seasonal rationing, utilities are now emphasizing tertiary modules that enhance resource recovery beyond 60%. This focus has expanded procurement channels for membrane bioreactors and nutrient-recovery systems. While a small percentage of treated wastewater finds its way into agriculture, emerging decentralized biological units designed for peri-urban irrigation are narrowing this gap, further energizing India's water and wastewater treatment technology market.

Stricter Zero-Liquid-Discharge Mandates for Red Industries

In 2024, the Central Pollution Control Board reclassified many sub-sectors into the red category. This move immediately imposed stringent Zero Liquid Discharge (ZLD) obligations on breweries, food processors, and bulk-drug units, influencing equipment demand in the near term[1]Central Pollution Control Board, “Notifications and Guidelines,” cpcb.nic.in. In 2025, Maharashtra set up a real-time monitoring network at industrial outfalls. This network sends pH and flow data every 15 minutes to an auto-penalty dashboard, turning non-compliance from a sporadic issue into a direct financial penalty. Gujarat has placed a moratorium on new water connections in 14 talukas facing high stress. As a result, new applicants are leaning towards closed-loop water strategies. This shift has led to a surge in orders for multi-effect evaporators and mechanical vapor-recompression systems, both of which can reclaim water from brine. Establishing a ZLD plant comes with compliance costs. These high costs are steering small and medium enterprises towards shared treatment facilities. This aggregation of demand for modular skid-mounted units is bolstering the market for water and wastewater treatment technology in India. With penalty triggers set at significant levels, ZLD compliance has transitioned from a mere option to a critical balance-sheet concern, solidifying the optimistic outlook for India's water and wastewater treatment technology market through 2027.

Flagship Programmes Accelerating Tertiary-Reuse Capacity

AMRUT 2.0 has set aside funding for sewerage upgrades through 2026, directing a significant portion of this funding towards tertiary units. These units ensure water meets IS 10500 standards for industrial reuse. In 2025, Jal Jeevan Mission successfully installed village-scale greywater plants. They sidestepped traditional tender challenges, paving the way for decentralized procurement. This move bolstered the water and wastewater treatment technology market, especially in India's non-metro areas. Swachh Bharat Mission 2.0 issued tenders in 2024-2025, targeting new sewage treatment plants. They awarded contracts with viability-gap funding, mitigating equity risks for design-build-operate concessions. In 2025, Ghaziabad Municipal Corporation tapped into the green bond market, raising capital at a competitive coupon rate. This highlighted the financial advantages of ESG labeling for tertiary reuse assets. Together, these initiatives create a robust order backlog, ensuring the resilience of India's water and wastewater treatment technology market, even during investment downturns.

Surge in ESG-Linked Green Bonds Tied to Wastewater-Recycling KPIs

Municipalities in Vadodara, Indore, and Surat issued green bonds between 2024 and 2025. These bonds come with covenants mandating reuse of treated effluent by 2028. This move directly enhances revenue prospects for tertiary equipment suppliers in India's water and wastewater treatment technology market. Private industrial parks, benefiting from sustainability-linked loans, see a reduction in interest spreads when their Zero Liquid Discharge (ZLD) compliance exceeds 95%. This shift transforms treatment plants from mere cost centers to profit-driven assets, justifying investments in higher-spec membranes and advanced sensor packages. In 2025, wastewater projects in India received certifications that attracted European pension-fund capital, offering lower coupons than comparable infrastructure debt, and infusing additional funding into India's water and wastewater treatment technology market. Pilot projects in Rajasthan and Karnataka are trading water-recovery credits, effectively valorizing surplus treated water. This innovative mechanism has the potential to increase revenue per cubic meter for early adopters. However, tier-2 cities continue to depend on sovereign grants, highlighting an uneven landscape that India's water and wastewater treatment technology market must navigate.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and O&M for advanced treatment trains | -1.2% | National, acute in tier-2 and tier-3 municipalities | Medium term (2-4 years) |

| Fragmented municipal procurement and delayed payment cycles | -0.9% | Uttar Pradesh, Bihar, Madhya Pradesh urban local bodies | Short term (≤ 2 years) |

| Cultural resistance to grey-water reuse outside tier-1 cities | -0.6% | Rural and semi-urban areas, northern states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX and Operation and Maintenance for Advanced Treatment Trains

Municipalities grapple with the financial strain of a 100 MLD tertiary plant, which comes with a significant price tag. On top of this, an annual expenditure is needed for membranes, power, and chemicals. This pricing challenge looms large, especially for those with debt-service coverage ratios dipping below 1.5. Meanwhile, industrial Zero Liquid Discharge (ZLD) units inflate operating costs compared to traditional supplies. Such costs become justifiable only when penalties for freshwater usage or premiums due to scarcity surpass this difference. Additionally, membrane fouling can reduce Reverse Osmosis (RO) flux annually. This degradation necessitates chemical cleaning every three to six months and membrane replacement every three to five years. For mid-sized plants, this translates to an added expense. Such financial burdens stifle upgrade cycles, especially in cost-sensitive regions, casting a shadow on the growth of India's water and wastewater treatment technology market. Smaller municipalities, often short-staffed, struggle to operate these advanced systems efficiently. This inefficiency not only diminishes perceived returns but also extends payback periods beyond the five-year mark, a timeline many lenders deem precarious. As a result, these municipalities frequently revert to simpler solutions like trickling filters or lagoons, curtailing the immediate potential of India's water and wastewater treatment technology market[2]Reserve Bank of India, “Municipal Finance Report 2025,” rbi.org.in.

Fragmented Municipal Procurement and Delayed Payment Cycles

Payment delays are inflating working-capital demands for EPC contractors. In response, these contractors are tacking on additional basis points to their bids to counterbalance financing costs. This maneuver is not only artificially inflating project budgets but also leading to a slight contraction of the water and wastewater treatment technology market in certain lagging states of India. The lack of standardized tender templates compels suppliers to craft unique documents for every city. This not only heightens transaction costs but also deters smaller equipment manufacturers from participating in bids. The result is a narrowed competitive landscape and a slowed pace of innovation adoption. Currently, user charges manage to cover only a portion of operational and maintenance expenses. This shortfall leaves concessionaires reliant on municipal budgets, which are often swayed by political cycles. Such dependency hampers the viability of long-term design-build-operate models that are crucial for India's water and wastewater treatment technology market. Furthermore, the need for multi-agency clearances can stretch project timelines significantly. This extended timeline has led some foreign vendors to withdraw from potential opportunities, further limiting the diversity of suppliers. Without significant procurement reforms, the uncertainty in cycle times is poised to continue hindering growth in India's water and wastewater treatment technology market, state by state.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Automation Lifts Process Control Demand

In 2025, Treatment Equipment dominated the Indian water and wastewater treatment technology market, accounting for a 89.59% share of the market. This trend highlights the longstanding prominence of physical, chemical, and biological unit operations. However, looking ahead, Process Control Equipment and Pumps are projected to grow at an 11.25% annual rate until 2031. This surge is driven by operators retrofitting supervisory control and data acquisition (SCADA) platforms, a move mandated by updated consent conditions, signaling a shift towards digitization in India's water and wastewater treatment technology landscape. Within the Treatment Equipment segment, biological nutrient-recovery modules are gaining traction, especially in pharmaceutical and food-processing sectors. Here, struvite precipitation not only recovers phosphorus but also transforms a compliance obligation into a marketable fertilizer precursor, enhancing project profitability. The semiconductor and green hydrogen industries, which require total dissolved solids to be below specific thresholds, are driving demand for advanced solutions. This demand is met by multi-stage RO and nano-filtration stacks, which outpace conventional resins in both efficiency and spatial footprint. Offshore platforms, aiming to meet the discharge limits set in 2024, are now turning to induced-gas flotation for oil-water separation upgrades, further embedding specialty skids into India's treatment technology market. In densely populated metros, where land prices are high, the land-footprint savings from using membrane bioreactors for suspended solids removal become a significant advantage, amplifying the overall project value.

Digitization is revolutionizing the industry, with predictive maintenance capabilities slashing unplanned downtime. This is exemplified by municipal plants utilizing cloud analytics to predict membrane fouling in advance, underscoring the appeal for leaders in process instrumentation. Energy-efficient pumps, equipped with variable-frequency drives, have seen a notable rise in adoption. This shift underscores the industry's sensitivity to power tariffs, which can account for a significant portion of wastewater operation and maintenance expenses. Despite facing an increase in landed costs due to fragmented tender specifications, international suppliers persist in importing membranes and sensors. Their success in winning bids is attributed to the superior lifecycle value they offer. As smart-city initiatives increasingly bundle sensors, pumps, and analytical dashboards, process control emerges as a pivotal force, driving treatment hardware downstream and creating a self-reinforcing cycle that propels growth in India's water and wastewater treatment technology market, bolstered by service-linked annuities.

By End-User Industry: Healthcare Outpaces Municipal Growth

In 2025, municipal utilities held a 58.22% share of India's water and wastewater treatment technology market, thanks to capital allocations from AMRUT 2.0 and the 100% treatment mandates of the Swachh Bharat Mission 2.0. Yet, the most rapid growth is anticipated in the Healthcare sector. Here, stringent antibiotic-residue caps at parts-per-trillion levels are steering facilities towards advanced oxidation and activated-carbon contactors. This trend is set to propel the segment with 10.72% growth through 2031. Meanwhile, Food and Beverage processors invested in Zero Liquid Discharge (ZLD) systems. This investment was aimed at meeting stringent BOD thresholds, converting organic loads into biogas. This biogas not only offsets a portion of the on-site thermal demand but also amplifies interest in energy-positive wastewater solutions. In the Krishna-Godavari basin, Oil and Gas operators are now treating produced water for reinjection. This move has significantly reduced their freshwater intake and unveiled a secondary recovery revenue stream, solidifying long-term operation and maintenance contracts in the Indian water and wastewater treatment technology arena. In 2025, Chemical and Petrochemical clusters in Gujarat and Maharashtra responded to daily discharge penalties imposed by state boards. They installed evaporator-crystallizer trains, a strategic move to safeguard their high-margin exports from potential compliance disruptions.

Pulp and Paper mills have transitioned to elemental-chlorine-free bleaching, achieving a substantial reduction in adsorbable organic halides. However, they still necessitate multi-stage biological polishing, ensuring continued demand for nutrient removal modules. The Poultry and Agriculture sectors, with treatment adoption rates below five percent, present a lucrative opportunity for decentralized anaerobic digesters. In 2025, the Hospitality sector and commercial real estate entities installed membrane bioreactors. This move was in response to building codes mandating on-site greywater recycling, further broadening the customer base of India's water and wastewater treatment technology industry. These trends highlight how diverse regulatory landscapes and sector-specific water-quality benchmarks are shaping a myriad of micro-markets, collectively driving robust growth in India's water and wastewater treatment technology sector.

Geography Analysis

In 2025, Tamil Nadu, Karnataka, Gujarat, and Maharashtra—southern and western states—together accounted for a significant portion of the investments. This surge was driven by industrial corridors mandating Zero Liquid Discharge (ZLD) compliance and municipal corporations adept at securing ESG-linked debt at competitive rates. Gujarat stands out with heightened demand for ultra-pure water, primarily due to the clustering of semiconductor fabs in Sanand and Dholera. Here, state incentives not only shorten payback periods but also attract high-spec systems like reverse osmosis, electrodeionization, and brine management into India's regional water and wastewater treatment market. Meanwhile, Karnataka, with its drought-prone districts, is home to prestigious green-hydrogen projects. These projects depend on captive desalination units sourced from secondary reservoirs, further expanding the state's procurement pipeline.

Northern states are making strides, especially as the Central Pollution Control Board highlights compliance issues along the Ganga basin. Uttar Pradesh issued several tenders for sewage plants, although payment delays continue to be a hurdle for smaller contractors. Rajasthan and Haryana are utilizing treated effluent for cooling in thermal power stations, a move that conserves freshwater amidst declining aquifer levels. This strategy not only offers a dual advantage but also accelerates approvals for tertiary units, inflating regional orders. In Eastern India, Odisha and West Bengal are prioritizing industrial retrofits in steel and mineral processing. Here, modules for heavy metals removal command premium prices, adding complexity that benefits integrated EPC players.

The north-east, facing topographical challenges and a limited industrial presence, remains largely untapped, accounting for a small share of the national investment. Yet, Jal Jeevan Mission initiatives in Assam and Meghalaya hint at potential, especially with small-footprint membrane bioreactors tailored for challenging terrains. After cyclone-resilience studies confirmed plant durability, coastal desalination ventures in Andhra Pradesh and Tamil Nadu have gained momentum, marking a new chapter in India's water and wastewater treatment technology landscape. While unified digital-twin standards are still in their infancy, smart-city initiatives in Pune, Surat, and Visakhapatnam showcase the potential of remote operations. These can cut lifetime operations and maintenance costs, a trend poised to spread northward in the coming years.

Value Chain Analysis

The India water and wastewater treatment (WWT) technology value chain starts with upstream inputs and components (treatment chemicals, membranes, pumps, and instrumentation and controls), and then moves into system design and integration by OEMs and EPC contractors that deliver sewage treatment plants (STPs), effluent treatment plants (ETPs), tertiary reuse packages (for example, TTRO), and ZLD trains (evaporators, MVR, crystallizers). Projects are typically routed through municipal corporations and water boards (often under AMRUT 2.0 or related urban programs) as well as industrial compliance investments in red-category clusters, with long-term O&M increasingly embedded through DBO and similar concession formats.

Downstream, revenue depends on tendering, commissioning, and multi-year service delivery, where performance monitoring, spares, and consumables (membrane replacement, cleaning chemicals, and sensors) support recurring income. Fragmented municipal procurement and delayed payment cycles raise working-capital needs for EPC players, while uneven enforcement of ETP functionality and subsidized water pricing can weaken the business case for reuse in some catchments. Service providers that bundle design-build capabilities with chemical programs for coagulation, flocculation, and anti-scalants also feature in the value chain, shifting demand away from standalone equipment sales.

Competitive Landscape

The India Water and Wastewater Treatment (WWT) Technology Market is moderately fragmented. Technology differentiation centers on membrane chemistry and energy efficiency. Fragmented tender specifications impede localization of high-spec sensors and membranes, compelling suppliers to import critical components, which adds landed costs yet still consistently wins on lifecycle economics. Payment cycles extending beyond 180 days in certain municipalities continue to pressure working capital and can deter foreign OEMs from establishing domestic plants, although proposed procurement harmonization under the National Framework for Water Utilities could standardize technical clauses and unlock manufacturing scale. Intellectual-property barriers remain low in commodity segments but steepen sharply for proprietary membranes and process analytics, signaling an emergent two-track competitive dynamic: commoditized modules dominated by price wars and high-tech niches defended by patents and data ecosystems.

India Water And Wastewater Treatment (WWT) Technology Industry Leaders

WABAG

Veolia

Thermax Limited

IEI

Xylem

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A notable whitespace is scaling tertiary reuse and industrial recycling around mandated bulk-user reuse targets under the 2024 Liquid Waste Management Rules, which shift compliance from disposal toward measurable reuse outcomes across commercial, institutional, and industrial facilities. This regulatory direction is being supported by public funding channels and execution pipelines, including Union Budget 2026-27 outlays for water, sanitation, and river conservation, as well as ongoing urban missions that keep STP construction and upgrades active across multiple states.

Large municipal build and rehabilitation programs continue to drive demand for membrane-based tertiary treatment, automation, and long-duration O&M capability. Examples include the BMC sewage upgrade program in Mumbai (including the 215 MLD Bhandup STP nearing completion with commissioning cited by October 2026) and continued Namami Gange execution momentum, with NMCG reporting 363 out of 524 sanctioned projects completed (total sanctioned value cited at INR 43,031 crore). Industrial and high-purity water corridors also provide an additional lane for advanced technologies, with desalination and polishing capacity additions in metros (such as Chennai’s 400 MLD desalination project targeted for completion by end-2026) and PPP/DBO wins (for example, L&T’s DBO order for water and effluent treatment infrastructure in Guwahati) expanding the addressable market for advanced membranes, sensors, and lifecycle service contracts.

Recent Industry Developments

- May 2026: VA TECH WABAG secured a design, build, and operate (DBO) order from Delhi Jal Board for a 17 MGD wastewater treatment plant at Mitraon, Delhi, including 15 years of operations and maintenance. The long O&M tail and defined delivery timeline (about 21 months for construction) reinforce the move toward performance-linked municipal contracting and sustained demand for tertiary-capable treatment trains.

- July 2025: VA TECH WABAG won an order of about INR 380 crore from the Bangalore Water Supply and Sewerage Board (BWSSB) for wastewater treatment plants with tertiary treatment, along with biogas generation and solar sludge drying beds, followed by 10 years of O&M. The package points to growing interest in integrated resource recovery and energy-offset features being bundled into municipal tenders.

- August 2024: Nalco Water (Ecolab) signed a strategic agreement with Danieli to improve industrial water treatment in the metals sector by combining water treatment chemistry and services with metals-plant technology integration. The tie-up supports wider adoption of water and wastewater optimization in heavy industry, where compliance, water productivity, and footprint reduction increasingly inform equipment and service selection.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers the value of equipment and technology used to treat water and wastewater in India, across municipal and industrial applications, where spending is tracked at the technology supply and deployment level.

Scope exclusions: We exclude standalone treatment chemicals, routine O&M services, and broader water infrastructure construction that is not directly tied to treatment technology equipment.

Segmentation Overview

- By Equipment Type

- Treatment Equipment

- Oil/Water Separation

- Suspended Solids Removal

- Dissolved Solids Removal

- Biological Treatment/Nutrient and Metals Recovery

- Disinfection/Oxidation

- Other Treatment Equipment

- Process Control Equipment and Pumps

- Treatment Equipment

- By End-user Industry

- Municipal

- Food and Beverage

- Pulp and Paper

- Oil and Gas

- Healthcare

- Poultry and Agriculture

- Chemical and Petrochemical

- Other End-user Industries

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the factual base for India treatment spending and to keep the model anchored to measurable demand signals. Public sources such as the Central Pollution Control Board (CPCB) and State Pollution Control Boards help us interpret compliance-driven wastewater needs, while Jal Jeevan Mission and AMRUT program disclosures help frame municipal treatment additions and project timelines.

We also reviewed India budget documents, tender portals, and project award notices to understand typical technology choices and ordering cycles, which then fed into timing assumptions. Supporting context came from sources such as the Central Water Commission, Ministry of Housing and Urban Affairs publications, peer-reviewed papers on treatment performance, and customs trade statistics for selected equipment categories. Company annual reports and investor presentations were used to sanity check revenue mix exposure to India treatment projects, and we referenced paid subscriptions for company financials and for shipment-level import or export checks where they improved confidence. These desk research sources are illustrative, and many other public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions were used to test equipment ASP movement, adoption rates of advanced processes, and realistic project execution pacing, since these points are often unclear in public documents. We spoke with a mix of technology suppliers, EPC and integrator teams, municipal operators, and industrial water managers to confirm what gets procured, how systems are bundled, and which end uses are currently spending. For an India-only market, interviews were spread across major industrial corridors and large urban clusters so that assumptions were not driven by one state or one end-user pattern.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 16% | |

| Mid tier: 50% | Functional/Unit leaders: 36% | |

| Smaller Players: 17% | Managers: 48% |

Market-Sizing & Forecasting

Sizing started from a top-down build that reconstructs the India demand pool using treatment capacity additions, project pipeline signals, and technology penetration by application, which are then translated into yearly equipment value. To keep totals realistic, results were corroborated with selective bottom-up approximations, such as sampled project BOM checks, supplier revenue exposure estimates, and ASP times volume sanity checks for commonly procured equipment.

Inputs that mattered most included municipal STP and WTP additions and rehabilitation timing, industrial capex linked to compliance upgrades, reuse and ZLD adoption intensity in regulated sectors, imported equipment intensity for certain unit operations, and commissioning delays that shift revenue recognition. Where local data was patchy, conservative gap-filling was done by using nearby state analogs and by applying ranges validated in primary calls, and then narrowing the range during analyst review.

For forecasting, scenario analysis was used so that capex cycles, tender flow, and regulatory enforcement changes could be reflected without forcing one straight-line curve. Assumptions on technology mix and ASP progression were updated using expert consensus from interviews, and then tested against macro indicators like urban population served and industrial output trends.

Data Validation & Update Cycle

Model outputs were cross-checked against independent signals like tender award volumes, commissioning news, and reported order books, and any sharp deviations were investigated before sign-off. We also run variance checks by end user and by equipment grouping so totals do not look accurate only at the headline level, and then become inconsistent when broken down.

Reports are refreshed annually, and interim updates are made when material events occur, such as major policy shifts, large program reallocations, or sharp input-cost moves that can change ASPs. Before delivery, an analyst performs a fresh pass across key assumptions and recent public updates so clients receive the latest updated view.

Mordor Intelligence's India Water and Wastewater Treatment Wwt Technology Market Sizing Compared With Other Published Estimates

Published market sizes for India treatment can differ quite a bit, even when the topic sounds similar, because the boundary of what is counted is not always the same. Differences usually come from whether chemicals and services are included, whether water-only is mixed with wastewater, and how project timing is converted into yearly spending.

The table shows a narrower spread when technology equipment is isolated from adjacent spending buckets, and in Mordor Intelligence's model, the value is limited to treatment equipment, process control equipment, and pumps within India, rather than folding in chemicals, O&M services, or broad water infrastructure work. Some sources also publish faster growth by assuming aggressive execution of municipal programs or immediate compliance upgrades in industry, while others understate near-term value by missing equipment ASP escalation and longer lead-time project billing patterns.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.98 B (2025) | |

| Industry Marketplace A | USD 2.73 B (2025) | Often leans on a tighter set of equipment categories and can apply conservative timing for project conversion, which can reduce the counted value in the base year. |

| Domestic Advisory B | USD 3.98 B (2025) | Typically blends technology with chemicals and services under a broader water and wastewater treatment definition, which increases the reported number even if the India demand pool is similar. |

Taken together, the spread is mainly explained by scope boundaries and the way project pipelines are translated into annual revenue. Our approach stays traceable because each step is tied back to visible capacity, procurement signals, and interview-tested assumptions on mix, pricing, and execution timing.

Key Questions Answered in the Report

What is the projected value of the India water and wastewater treatment technology market by 2031?

The market is forecast to reach USD 5.17 billion by 2031, reflecting a 9.62% CAGR from USD 3.27 billion.

Which equipment category is growing the fastest?

Process Control Equipment and Pumps are set to grow at an 11.25% CAGR through 2031, driven by digitization and mandatory real-time compliance dashboards.

Why is healthcare demand rising in this sector?

Tighter antibiotic-residue limits require advanced oxidation and adsorption steps, pushing healthcare wastewater systems to adopt higher-spec treatment trains, resulting in a 10.72% CAGR.

How do green-hydrogen projects influence technology adoption?

Each gigawatt of electrolyzer capacity needs around 12 million liters per day of ultra-pure water, spurring demand for multi-stage RO, electrodeionization, and brine-management systems.

What are the key regulatory programs shaping the market?

AMRUT 2.0, Jal Jeevan Mission, and Swachh Bharat Mission 2.0 collectively fund tertiary reuse modules, enforce 100% treatment mandates, and subsidize viability-gap financing for public-private partnerships.

Page last updated on: